glow and grow

TRANSCRIPT

Glow and Grow

The Business Future of Electronic AMOLED Displays presented at the 50th Anniversary of the Society for Information Display, 29 Sep 2012

— David Barnes [email protected]

Glow and Grow— the vision thing Emissive displays are more exciting than transmissive or

reflective displays. AMOLED can re-purpose existing AMLCD assets and create

a better cost structure (less material). Panel makers that lead the transition to AMOLED will obtain

competitive advantages (economic scale and product range). AMOLED enables new value propositions, such as formable

or flexible displays, that expand the market (for some).

v2—29 Sep 2012 Glow and Grow 2

The question is how much of this will be realized, when and by whom?

Technologies take time— AMOLED remains a novelty

v2—29 Sep 2012 Glow and Grow 3

OLED Radio 1999

32” LCD TV 2003

Novelty Commodity

Size

LCD Clock 1968

60” TV <$1000 2012

AMLCD TV 1972

AMLCD NB 1988

XEL TV 2008

Retina MP 2010

OLED MP 2002

AMOLED TV 2013?

Why now? Elasticity of demand is favorable for AMLCD AMLCD area demand has been elastic relative to price for leading producers. Elasticity of –1.6 implies a 19% increase in area demand for every 10% decrease in area price. From this perspective, cutting prices seems reasonable… sales revenue increases faster than price decreases.

So why are panel makers losing money and slowing investment?

v2—29 Sep 2012 Glow and Grow 4

Demand Elasticity for AUO + LGD, 2004–2011

Source: public disclosures; BizWitz analysis

y = -1.643x + 28.528

15

16

17

18

6.5 7.5 8.5

LN(area) vs LN(price)

ŋ = –1.6

Why now? Variable costs are unfavorable for AMLCD Material remains the primary source of cost, as rising expenses offset falling depreciation charges. There is no scale benefit.

Operating profit margins cannot cover depreciation charges if producers reinvest in AMLCD capacity. There is no clear path to sustained profitability even if the cost of capital is near zero (government supported) … so let the Chinese do it.

v2—29 Sep 2012 Glow and Grow 5

Cost of Product Structure for LG Display

Source: public disclosures; BizWitz analysis

58% 64% 63%

13% 9% 10%

21% 14% 13%

9% 12% 13%

0%

20%

40%

60%

80%

100%

2005 2011 2H'12

Expenses

Depreciation

Labor+OH

Material

Why now? National industries are under water Including all AMLCD makers in Taiwan (except E Ink) we see cumulative free cash flow reaching nearly –$20b by the end of last year.

This year will probably drive it down further. Taiwan’s panel makers put more than $65b into the ground and generated at net loss of 2% on total sales.

The scale of this financial mess calls for government intervention in order to save domestic jobs… and banks.

Hence changes in national policy allowing Chinese direct investment in Taiwan tech.

v2—29 Sep 2012 Glow and Grow 6

Cumulative Free Cash Flow for Taiwan (USD billion)

Source: public disclosures; BizWitz analysis

($25)

($20)

($15)

($10)

($5)

$0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

.

What now? Leaders seek advantage through technology In contrast to development of the AMLCD industry 20 years ago in Japan, leaders in the AMOLED movement seek advantage though distinct technical choices and their own supply chains. As a result, industry-wide learning is slower this time. Material and tool suppliers face conflicting priorities rather than a consensual roadmap toward AMOLED. As a result, economic scale will take longer to develop.

There are more paths to take, so we may see more variation rather than less, mid-term.

v2—29 Sep 2012 Glow and Grow 7

Present AMOLED Technology Choices

Source: BizWitz, conceptual

LGD

RGB Top Emission

LTPS

a-Si (?)

Polymer OLED

Glass Thin

TFE dyads

Metal

Bottom Emission wOLED

Oxide

SM OLED

Glass frit

SDC SDC

LGD

What now? It’s time for more pixels to constrain AMOLED The more mature AMLCD infrastructure can supply more pixels at modest extra cost. Apple’s supply chain leverages this capability.

In the flat TV market, it’s time for new value propositions. S3D did more for brands than for panel makers, who have always benefitted more from adding pixels to larger panels than from other innovations. Thus, the ITU spec for UHD (8k4k) comes just time. It is not clear what market space OLED TV will find uncontested in the near term. Fight Club?

.

v2—29 Sep 2012 Glow and Grow 8

Potential TV Space for new propositions: the next three years

Source: BizWitz, conceptual

40” 59”

60” 79”

80” 99”

UHD

QHD

HD

LCD 2016

LCD 2014

LCD 2013

LCD 2013

OLED 2013

LCD 2012

Size

Format

100” 109”

LCD 2016

LCD 2012

LCD 2014

LCD 2014

OLED 2016

What now? Different strokes for different folks AMOLED will move from novelty towards commodity status later this decade … but different companies and countries will move at different paces in slightly different directions. Korean leaders will stay ahead for three more years, at least, but Taiwanese may close the gap in small panels by mid decade. Integrated touch and other functions will become means of differentiation. Chinese entrants and Taiwanese incumbents may depress AMLCD prices further and constrain OLED growth.

Korea Taiwan China Japan

Large Panels

Convert fabs now

Add LCD pixels now

Build big AMLCD

Support the brand

Small Panels

Convert fabs now

Convert fabs now

Link-up regionally

Seek niches

Strategy Move first Follow fast Develop capability Right-size

Policy Allow tech transfer

Allow FDI and xfer

Fund capex

Reorg Merge

v2—29 Sep 2012 Glow and Grow 9

Likely Actions, Strategies and Policies for Incumbents

Source: BizWitz, conceptual

Who now? New entrants could buy-into the game A new game attracts new players. We may see other countries throw their hats in the ring this decade. Brazil wants to lever its global position and cut imports. A JV with Foxconn stalled on the question of AMOLED, so Brazil may try again. Hyper-democracy in India hampers development but things could change later this decade (positive for OLED TV with really big speakers!). SE Asia could become a contender by sustaining progress, step by step. Europe might realize its dreams, eventually.

Brazil India SE Asia Europe

Large Panels

Seek JV technology

Assemble for now

Assemble, make parts

Assemble for now

Small Panels

Import for now

Regional design

Assemble, make parts

Invent printing

Strategy Lever position

Balance power

Build industry Leap-frog

Policy Cut imports

Protect local jobs

Reduce risk

Stimulate JD

v2—29 Sep 2012 Glow and Grow 10

Likely Actions, Strategies and Policies for Incumbents

Source: BizWitz, conceptual

What happens … if new suppliers act like old suppliers? A recent forecast for OLED materials by NanoMarkets showed 5½ X growth in value from 2012 to 2017. Their model for material cost by component was relatively constant, however: 5/12 Emission materials* 3/12 Electrodes 4/12 Substrates/encaps. The key question for panel makers is, what portion of total cost will these materials comprise and how much margin can they make by converting these materials? Will material suppliers still extract AMLCD-like rents? v2—29 Sep 2012 Glow and Grow 11

Nominal AMOLED Material Cost Structure

NanoMarkets, Sep ’12; BizWitz analysis * Emission includes HIL, ETL, et cetera

Emission Materials

Electrodes

Substrate/Encap.

What happens … if new entrants play the same old game? Other players will come to the table if they see the leaders making money (or playing for big stakes, at least). If all players bet big (go all-in like on the Poker shows), then they everyone might lose. If some players check (delay), then there may be winnings for the others. One thing is clear: if everyone behaves as they have, then only consumers will win. The best alternative is starting different games so there can be winners at each table.

.

v2—29 Sep 2012 Glow and Grow 12

Potential Adverse Outcome of a Game

Source: BizWitz, conceptual

Shame

Profit?

Profit?

Loss Go All-in

Check

Check Go All-in PLAYER 1

PLAYER 2

What happens? AMOLED becomes the new commodity LCD is vulnerable in the mobile market as PC incumbents

give way to new value propositions and alliances Thinner, more flexible design factors open new markets. Shorter product life reduces technical risks and increases chances. Functional integration and brand architectures enable differentiation.

LCD TV substitution creates a nearly infinite opportunity, at least for a while. CRT TV area share fell from 80% to 20% in 14 quarters. Consumers may not see the LCD–OLED gap to be so big… Nevertheless, substitution could happen fast, later this decade.

AMOLED becomes the new commodity until holography or some other technology emerges next (next) decade.

v2—29 Sep 2012 Glow and Grow 13

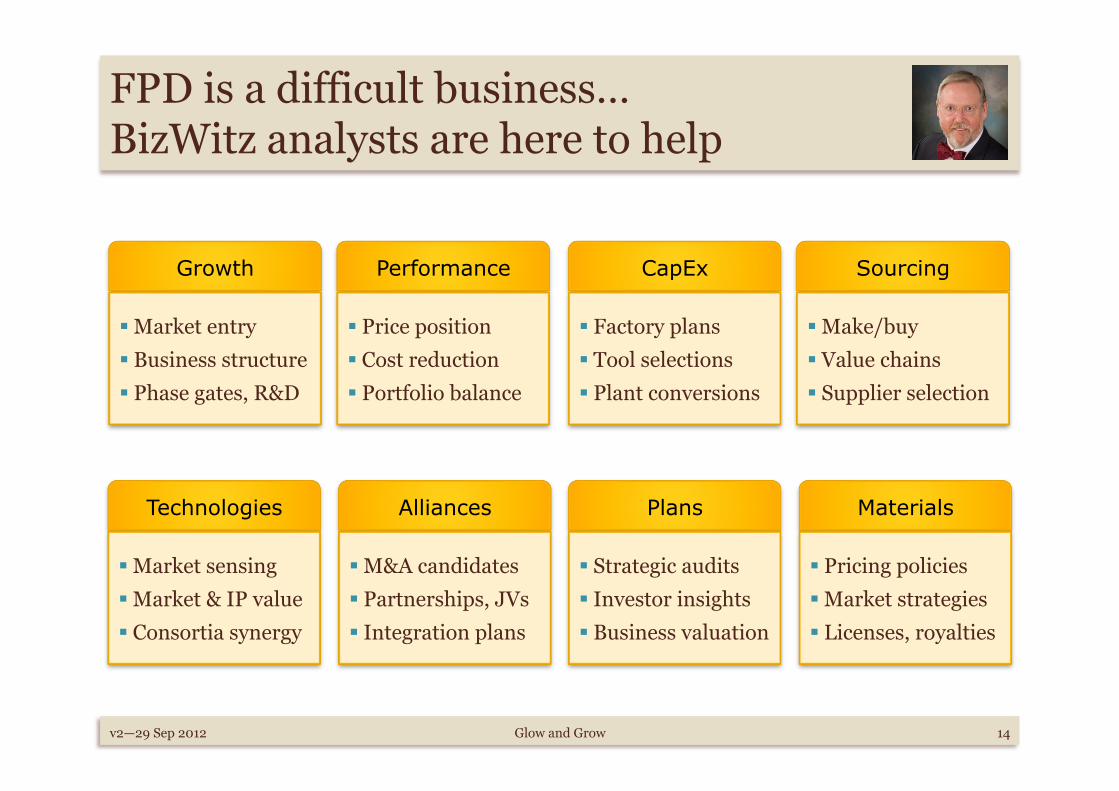

FPD is a difficult business… BizWitz analysts are here to help

v2—29 Sep 2012 Glow and Grow 14

Growth

Market entry Business structure Phase gates, R&D

Technologies

Market sensing Market & IP value Consortia synergy

Alliances

M&A candidates Partnerships, JVs Integration plans

Plans

Strategic audits Investor insights Business valuation

Materials

Pricing policies Market strategies Licenses, royalties

Performance

Price position Cost reduction Portfolio balance

CapEx

Factory plans Tool selections Plant conversions

Sourcing

Make/buy Value chains Supplier selection