gms & pension update lia northwest

TRANSCRIPT

GMS & Pension UpdateLIA NorthWest

John McInerneyPensions Technical Manager

Aviva: Public

What we’ll cover

►What is it and who it is for? ►What happens if they die in service?

►What’s under the bonnet ►What happens if they get seriously ill?

►Contributions ►What happens if they leave the GMS?

►What are the investment options

►Where do you come into it?

►Retirement options ►Questions

2

Aviva: Public

What is it and who is it for?

3

A scheme for GPs who have GMS IncomeAutomatically enrolled/Can’t accept transferOccupational pension or a Trust RAC?It isn’t the state Superannuation SchemeIt isn’t Defined BenefitIt’s complicated!

Aviva: Public

What does the scheme look like?

GMS

Administered by Mercer

Investment Managers

(mainly Mercer)

4 Investment

options

Both HSE and GPs

contribute

AVCs can be made to

scheme

NRA is 65

4

Aviva: Public

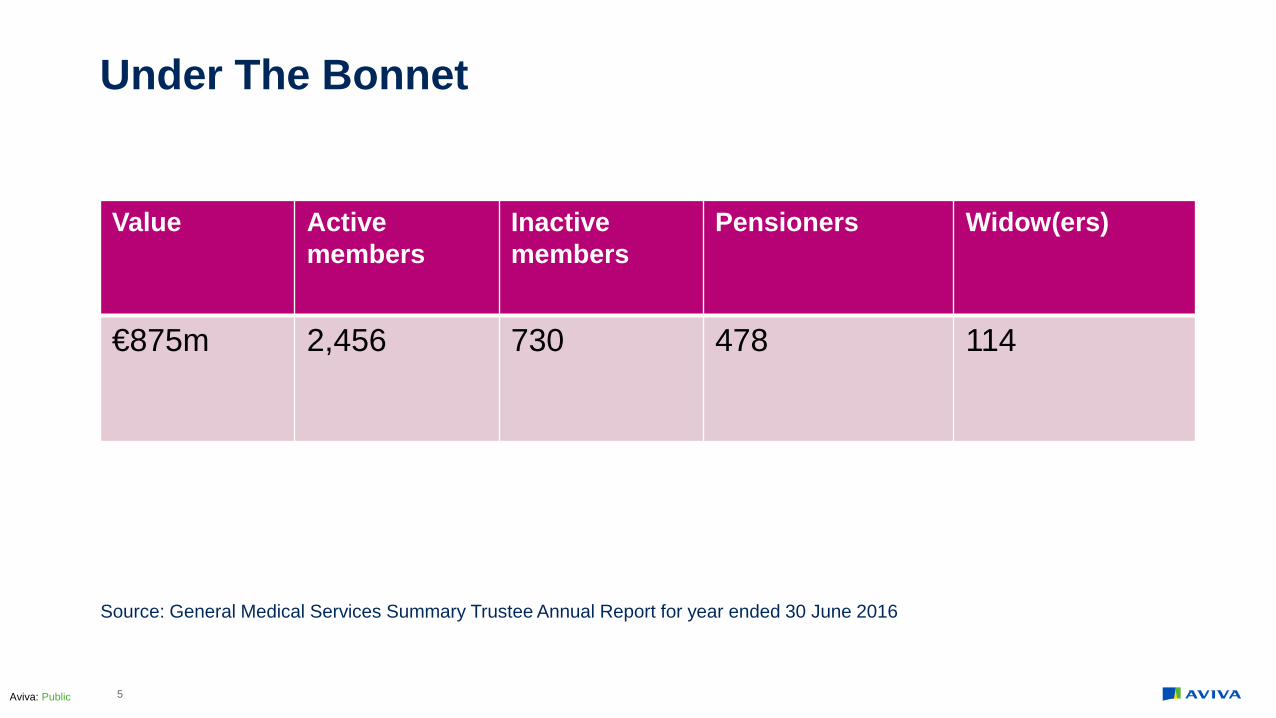

Under The Bonnet

Value Activemembers

Inactivemembers

Pensioners Widow(ers)

€875m 2,456 730 478 114

Source: General Medical Services Summary Trustee Annual Report for year ended 30 June 2016

5

Aviva: Public

ContributionsPaid To The

Scheme

Aviva: Public

Contributions paid in

HSE pays in 10% of Capitation Fees per month

Member pays in 5% of Capitation Fees per month

Members can make AVCs up to relevant limits

The HSE 10% does not form part of taxable income for member and so doesn’t go into tax return

7

Aviva: Public

What happens to the contributions?

Each member has their own account within the scheme

95% of HSE contribution is invested

Other 5% is used to pay Death in Service/ill health retirement benefits and cost of administering the scheme

No deduction on member’s 5%

8

Aviva: Public

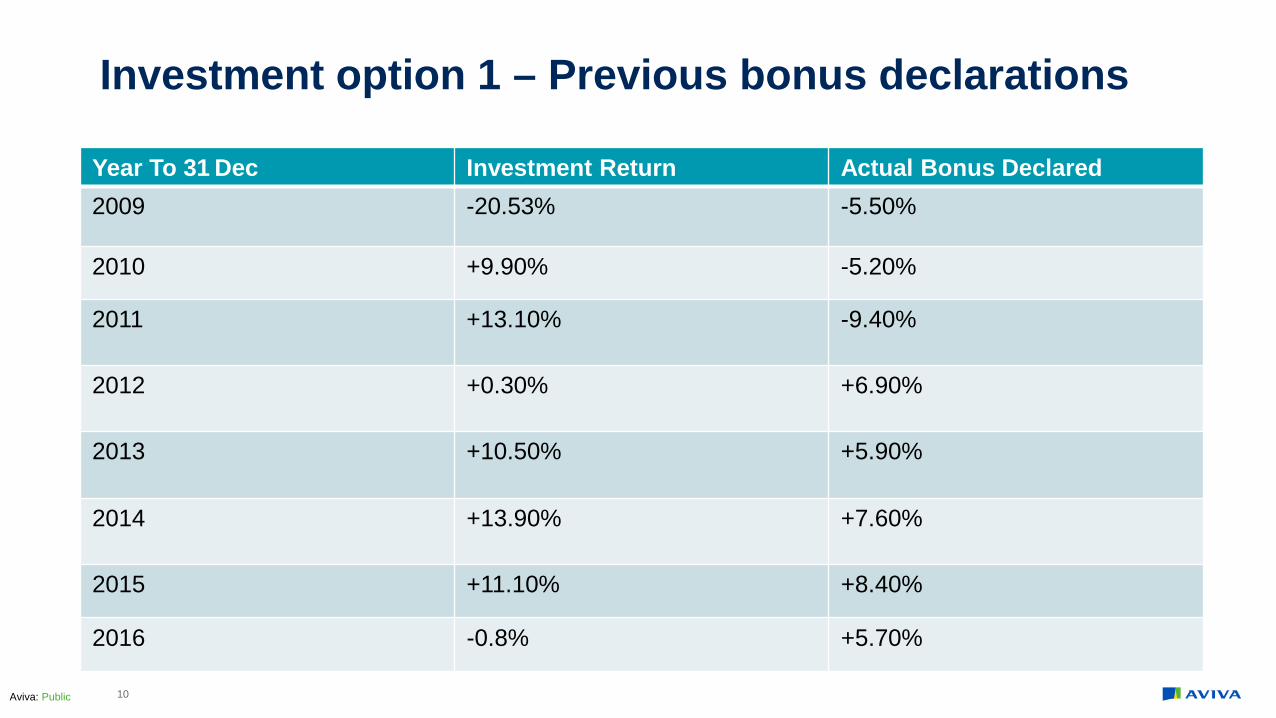

Investment option 1 - “Main GMS Fund”

What exactly do we mean by “Main GMS fund”?

A bonus is applied to each members’ account every 31 December

This is a percentage of the average value throughout the year

Calculated by reference to the gains and losses averaged over four years

From age 55, member can switch out at end of quarter – can’t switch back

Member receives a statement outlining bonus

9

Aviva: Public

Investment option 1 – Previous bonus declarations

Year To 31 Dec Investment Return Actual Bonus Declared2009 -20.53% -5.50%

2010 +9.90% -5.20%

2011 +13.10% -9.40%

2012 +0.30% +6.90%

2013 +10.50% +5.90%

2014 +13.90% +7.60%

2015 +11.10% +8.40%

2016 -0.8% +5.70%

10

Aviva: Public

Investment option 2 - Cash fund

Only available from age 55

Transfer of the realisable value

Quarterly switching from main GMS fund

Can’t switch back

Can switch all or part

11

Aviva: Public

Investment option 3 - Bond fund

Only available from age 55

Transfer of the realisable value

Quarterly switching from main GMS fund

Can’t switch back

Can switch all or part

12

Aviva: Public

Investment Option 4 - Lifestyle option

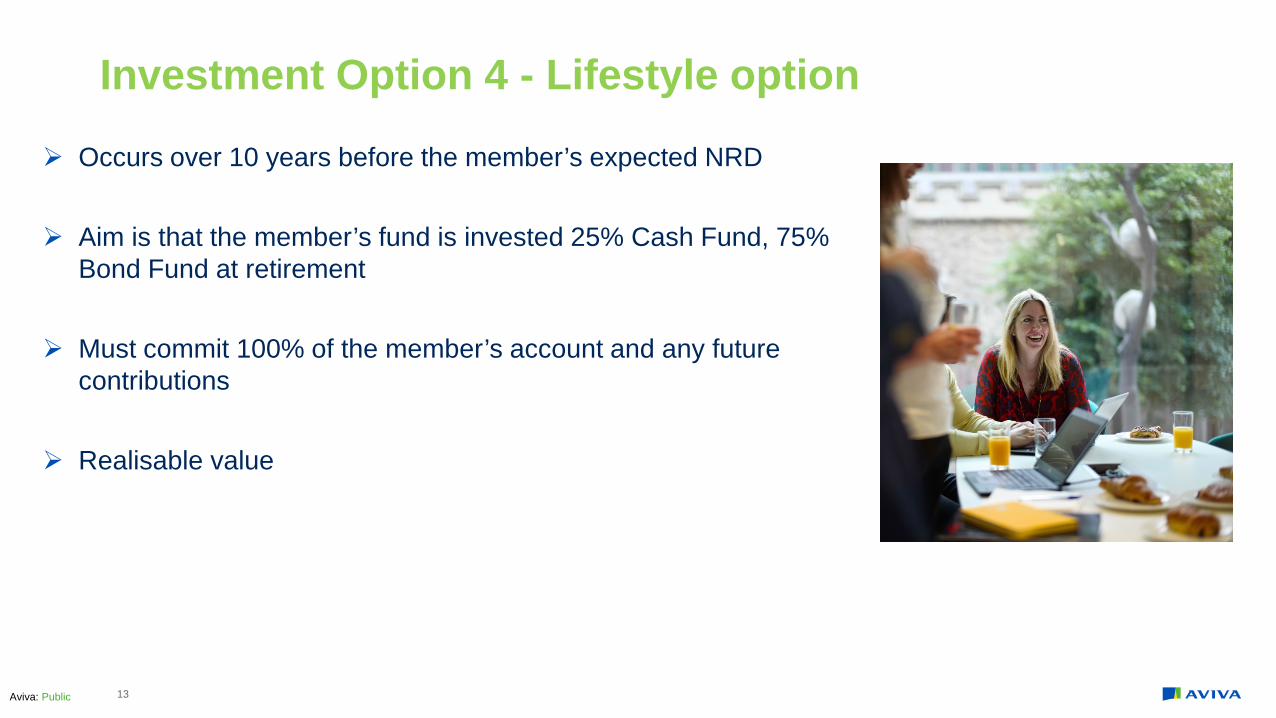

Occurs over 10 years before the member’s expected NRD

Aim is that the member’s fund is invested 25% Cash Fund, 75% Bond Fund at retirement

Must commit 100% of the member’s account and any future contributions

Realisable value

13

Aviva: Public

Options At

NormalRetirementAge

Aviva: Public

Retirement options

Normal Retirement Age is 65

Can work past NRA if they wish

Can retire from 50 onwards if they’ve given up their GMS practice

Can retire early on ill health at any age

15

Aviva: Public

What are the traditional retirement benefits?

Based on pension pot built up

Subject to Revenue Limits (scheme)

Can take 25% of main scheme as a cash lump sum

Balance used to purchase an annuity

This doesn’t include the AVC fund

16

Aviva: Public

Where does the member’s pension income come from? Can be purchased from a life company

Can be paid from GMS scheme

A rate is calculated by the scheme with a view (but not a promise) to provide cost of living increases

Pension cannot be reduced according to current scheme rules

Max of 2/3 of pension to spouse/civil partner on death

Pension Increase of 1.5% in 2015. Prior to that last paid in 2007

17

Aviva: Public

ARF Option

Out of the blue

Allow the ARF Option

Good news for all

Financial advice still needed to decide best option

18

Aviva: Public

Ill health early retirement Pension pot would be its current value or value calculated by formula involving age,

service, average capitation fees and member contributions

Member has two options:

Take pension benefits immediately

Leave invested and take pension benefits at a later date

19

Aviva: Public

Death In Service A lump sum is payable to estate

Greater of fund value or a % of members Annual Capitation Fees over previous 5 years plus refund of member contribution plus interest

For example under 45 with 5 or more years service equals 400%

Table in Trustee Annual Report

Normal Revenue Death in Service rules apply so any fund over 4 times salary must be used to purchase an annuity for dependants

20

Aviva: Public

Withdrawal from service Refund of contributions not allowed

Taking a transfer value (TV) not allowed (or in)

TV can be made where there is a PAO

Account left invested on their behalf

Can access from age 50 onwards

21

Aviva: Public

Where can

you add

value?

Aviva: Public

Where you come in

Retirement Age 65

25% of main scheme as a cash lump sum

Balance to provide pension (either payable from scheme or purchase annuity)

Additional Voluntary Contributions (AVCs) – when you know the rules you can help your client get a higher lump sum and a greater pension pot

23

Aviva: Public

A quick example

Frank is a GP about to retire:

GMS Scheme: €350,000 AVC: €100,000 Age 65 with >20yrs service Net GMS Final Remuneration of €125,000

What he could do is:

Take 25% cash lump sum €87,500 Use €262,500 to buy an annuity Have €100,000 post retirement

24

However, if you know the rules he could:

Get a cash lump sum €187,500 Use €262,500 to buy an annuity

By using his AVC fund to increase his lump sum entitlement.

Aviva: Public

Additional Voluntary Contributions- It’s as easy as AVC!

Can make AVCs up to relevant age related limits

Remember, they’re already paying in 5% of Capitation Fees themselves

Deadline of 31 October each year

2% of AVC will be deducted to cover administrative expenses

Members don’t have to make AVCs to GMS Scheme – Can make them to PRSA AVC

25

Aviva: Public

Why make AVCs? Tax relief Give your pension a boost! Aim to provide a larger pension pot at retirement Flexible retirement options - ARF option Increase Lump Sum Entitlement

26

Aviva: Public

Where to make the AVC?

Why a PRSA AVC?

DiversificationChoose providerGreater fund choiceChoose charging structurePortabilityGet Advice

GMS Scheme PRSA AVCOR

Why the GMS scheme?

SimplicityAll funds in one placeEase of administrationAnnuity From Scheme

27

Aviva: Public

Pension UpdateA Roadmap For Pensions Reform 2018-2013

Aviva: Public

Launched Wednesday 28th February

6 Strands:

• Reform of the State Pension• A New Automatic Enrolment Savings System• Improving governance and regulation• Measures to support Defined Benefit Schemes• Public Service Pension Reform• Supporting fuller working

A Roadmap For Pensions Reform

© Aviva PLC Private and confidential29

Aviva: Public

• Set at a level of approx. 34%/35% of average earnings

• Line future increases to changes in CPI and wage levels to ensure value is maintained

• PAYG model works once there is 4:1. In 40 years 2.3:1

• Potential deficit of up to €400 bn over next 50 years

• Total Contributions Approach (TCA) to calculate level of pension entitlement

• More logical and transparent. Will need a full record of 40 years PRSI contributions

• No further increase in SPA prior to 2035 other than those already provided for

Strand 1 – Reform of the State Pension

© Aviva PLC Private and confidential30

Aviva: Public

• No further increase in SPA prior to 2035 other than those already provided for

• Any change in SPA directly linked to increases in life expectancy

• Give a notice period of 13 years with first assessment in 2022

• Assessment every 5 years

• Social Insurance Contribution Rates and classes are actuarially reviewed annually

• Consider and present options for the amalgamation of PRSI and USC

Strand 1 – Reform of the State Pension

© Aviva PLC Private and confidential31

Aviva: Public

• Pension Funds of circa €110 Bn in Ireland

• 1% of EU population but 50% of all pension schemes! 160,000 of them!

• 35% of private sector workforce has such cover

• Complexity and lack of confidence has led to a choice paralysis

• “Opt Out” rather than an “Opt In” basis

• By 2022 begin implementation of an Auto Enrolment system

• Going to develop and publish a “strawman” Auto Enrolment design

Strand 2 – Auto Enrolment

© Aviva PLC Private and confidential32

Aviva: Public

• Over 23 years and earning over €20,000 per annum without existing private provision

• Contributions by both workers/employers and the state

• Opt out following a minimum period (9 months)

• 6%/6%/2% - Moving there over a specific time period

• Will replace rather than augment existing tax reliefs

• Payable at the same age as the State Pension

• Can retain existing arrangements

Strawman

© Aviva PLC Private and confidential33

Aviva: Public

• Too many large pension schemes/fees are too high/poor governance

• Require higher standards in the management and governance of schemes

• Empower PA to take a risk based approach and enforce fitness and probity on schemes

• New & existing schemes to gain “authorised status” from PA

• Lead In Time for existing schemes of 18-24 months

• Rationalise the number of different types of products

• Reduce the large number of pension schemes in operation – Master Trust

Strand 3 – Improving governance and regulation

© Aviva PLC Private and confidential34

Aviva: Public

• Trustees are fit and proper

• New professional standards

• Trustee Boards must consist of two trustees

• One has appropriate qualification and one has at least 2 years experience

• PA have powers of removal

• Corporate Trustees have two directors one with experience and one with qualification

• Trustee Development and CPD

• PA to publish new governance codes and standards

Trustees

© Aviva PLC Private and confidential35

Aviva: Public

• Big is good and small is bad

• Introduce master trusts and get rid of one member/small schemes

• Rationalise amount of pension products/Eliminate anomalies

• Review the cost of funded supplementary pensions to the Exchequer

• Can ARFs be improved?

• Not regulated by the PA

• Could the facilitate group ARF products or in-scheme drawdown

Reducing number of schemes/pension products

© Aviva PLC Private and confidential36

Aviva: Public

• DB schemes have dropped from 2,220 in 1996 to 667 in 2016

• Still 102,000 pensioners, 111,000 active members and 415,000 deferred

• DB assets under management is €62 bn

• 26% of schemes still not meeting the funding standard

• Advance Social Welfare, Pensions & Civil Registration Bill 2017

• More scrutiny, provision of information and increased powers

• Review Funding Standard

Strand 04 – Support DB Schemes

© Aviva PLC Private and confidential37

Aviva: Public

• SPSPS from 2013 – NRA in line with SPA with compulsory age of 70

• Joined before 2004. Compulsory retirement age of 65/66

• Increase compulsory retirement age to 70 for pre 2004 people

• PRD to be converted to a permanent Additional Superannuation Contribution (ASC)

Strand 5 – Public Service Pension Reform

© Aviva PLC Private and confidential38

Aviva: Public

• People encouraged and facilitated in working………..if the wish to

• State Pension Deferral System

• People on reaching state pension age can defer pension

• Actuarial adjustment would be applied

• Could make PRSI contributions past State Pension Age

• Clarify mandatory retirement age provisions

• Review pension drawdown rules - NRAs

Strand 6 – Supporting fuller working lives

© Aviva PLC Private and confidential39

Aviva: Public

Questions