go to understanding the core masteraahaminlandempire.org/wp-content/uploads/501r-aaham... ·...

TRANSCRIPT

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

To change the icon on this slide: • Go to View / Slide

Master • Right click on the icon,

select Change picture… • Browse to Y:\CLA

Common\Administrative\Market Solutions\Share\~Image Library\_Icons

• Select icon from the list • To see all the icon

options open the file labeled _CLA-Icon-Usage.pdf

• Click Insert

Investment advisory services are offered through CliftonLarsonAllen Wealth Advisors, LLC, an SEC-registered investment advisor. | ©2015 CliftonLarsonAllen LLP

Understanding the Core Elements of Section 501(r)

Kurt Bennion, CPA

AAHAM Inland Empire Spring Conference

April 14, 2017

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Agenda

• Background

• Penalties and Safe Harbors

• Emergency Medical Care Policy

• Limitation on Charges

• Extraordinary Collection Actions

• Financial Assistance Policy

2

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Learning Objectives

At the end of this session, you will:

• Understand the basic requirements to comply with section 501(r) and the final regulations.

• Understand the areas in which hospitals have struggled with 501(r) compliance.

• Understand the areas in which a hospital has flexibility to operate within section 501(r)’s constraints.

3

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

501(r) Applicability

• 501(r) applies to any hospital that is tax-exempt under 501(c)(3).

– Does not apply to foreign hospitals

– Does not apply to for-profit hospitals

– Probably does not apply to governmental hospitals ◊ If a governmental hospital also has 501(c)(3) status, then most

501(r) requirements apply.

4

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

What is a Hospital?

• A “hospital” is a facility that is required by a state to be licensed, registered, or similarly recognized as a hospital.

– Multiple buildings operated under a single state-issued license are considered a single hospital.

– A single building can have multiple hospitals.

• Buildings, offices, departments, services, etc., that are not covered by the hospital license are not required to comply with 501(r).

– You may choose to have 501(r) apply to them to simplify the hospital’s policies and procedures.

5

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Is the IRS Watching?

• The Secretary of the Treasury is required to review the community benefit activities of every hospital to which 501(r) applies every 3 years. – This responsibility was delegated to the IRS.

• In 2014, the IRS created a group of specialists to monitor the relevant hospitals.

• The reviews are conducted at IRS offices using information already available to the IRS. – Forms 990, information on websites, and whistleblower reports

• There is no hospital contact unless the reviewing agent sees anything they think requires further investigation.

• 501(r)-specific examinations began in Summer 2016.

6

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Penalties for Noncompliance

• Violation of any part of 501(r) can result in loss of the hospital’s tax-exempt status.

– As of the first day of the tax year in which the failure occurs.

• Failure to comply with the community health needs assessment can also result in a $50,000 excise tax per year.

– Reported on and paid with Form 4720.

7

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Safe Harbors

• Safe Harbor #1 – An omission or error is not a failure if: – It was minor; – It was either inadvertent or due to reasonable cause; and – The hospital corrects it as promptly as is reasonable.

• Safe Harbor #2 – an omission or error is excused if: – It was neither willful nor egregious; – The hospital corrects it as promptly as is reasonable; and – The hospital discloses it, either in the next Form 990 or on the hospital’s

website.

• Determination of “minor” is based on the facts and circumstances. • Either safe harbor can be used to avoid loss of 501(c)(3) status. • Only safe harbor #1 can be used to avoid the $50,000 excise tax. • See the “501(r) Correction and Disclosure Guidelines” handout.

8

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Policies

• A policy is established when:

– The written policy is adopted by an authorized body; and

– The hospital consistently follows the policy in practice.

• An authorized body is:

– The hospital’s governing body;

– A committee of the governing body; or

– Another party authorized by the governing body.

9

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

501(r) Requirements

• Conduct a Community Health Needs Assessment at least every three years

• Written emergency medical care policy

• Limitation on charges

• Billing and collection practices

• Written financial assistance policy (“FAP”)

10

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Emergency Medical Care Policy

• 501(r)(4)(B) requires the hospital to establish a written policy requiring the hospital to provide, without discrimination, care for emergency medical conditions to individuals regardless of their eligibility under the hospital’s FAP.

• Emergency medical conditions are defined by section 1867 of the Social Security Act.

11

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Emergency Medical Care Policy

• Details related to the emergency medical care policy are provided in Reg. 1.501(r)-4(c).

• The emergency medical care policy must: – Require the hospital to provide, without discrimination, care for

emergency medical conditions to individuals regardless of whether they are FAP-eligible.

– Require the hospital to provide the care for emergency medical conditions that the hospital is required to provide under Title 42, Chapter IV, Subchapter G of the Code of Federal Regulations.

◊ In other words, Medicare and Medicaid participation requirements

– Prohibit the hospital from engaging in actions that discourage individuals from seeking emergency medical care at the hospital.

12

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Limitation on Charges

• 501(r)(5) requires the hospital to:

– Limit the amount charged for emergency and other medically necessary care provided to FAP-eligible individuals to no more than the amounts generally billed to individuals who have insurance covering such care; and

– Prohibit the use of gross charges.

13

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Limitation on Charges

• For emergency and other medically necessary care, the hospital cannot require a FAP-eligible individual to pay more than the amount generally billed (“AGB”) for that care.

• For other medical care covered by the FAP, the hospital cannot make a FAP-eligible individual pay the gross charges (“chargemaster” rate).

14

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Medically Necessary Care

• A hospital can/must create its own definition of “medically necessary care”.

• IRS ideas for the definition:

– The state’s legal definition ◊ WA = appropriate hospital-based medical care

– The state’s Medicaid definition

– Generally accepted standards of medicine in the hospital’s community

– Based on an examining physician’s determination

15

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Charged

• A FAP-eligible person is considered “charged” only the amount they are personally responsible for paying after all deductions, discounts, and insurance reimbursements have been applied.

– “Discounts” includes financial assistance.

• If a person has insurance, the hospital may collect the full payment from the insurance provider.

• Therefore, the total received by the hospital may exceed the AGB limit, as long as the individual isn’t personally required to pay more than the AGB limit.

16

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Amounts Generally Billed Options

• A hospital must determine its AGB limit using either the look-back method or the prospective method.

– The IRS is allowed to add other methods in the future as payment mechanisms evolve.

• Only one of the methods may be used at a time.

• A hospital may change methods at any time.

• If an organization operates multiple hospitals, the method and details can differ between hospitals.

17

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

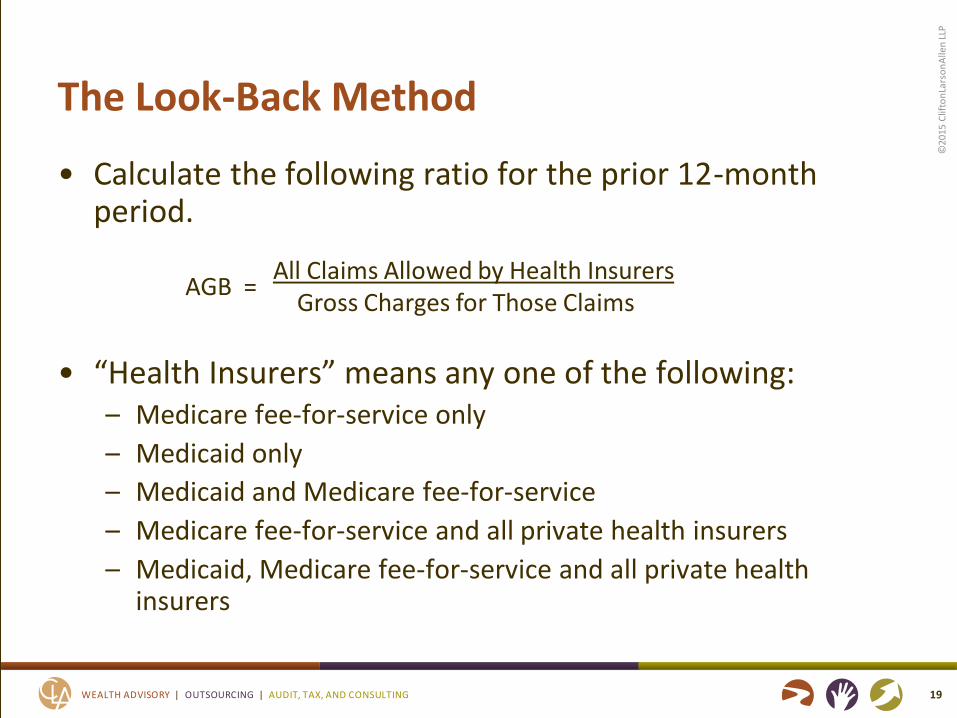

The Look-Back Method

• The AGB limit is calculated by multiplying the hospital’s gross charges for an episode of care by the applicable AGB percentage.

– The AGB limit is a dollar amount.

– The AGB percentage is a percentage.

• The AGB percentage must be calculated at least annually.

18

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

The Look-Back Method

• Calculate the following ratio for the prior 12-month period.

• “Health Insurers” means any one of the following: – Medicare fee-for-service only

– Medicaid only

– Medicaid and Medicare fee-for-service

– Medicare fee-for-service and all private health insurers

– Medicaid, Medicare fee-for-service and all private health insurers

19

AGB = All Claims Allowed by Health Insurers Gross Charges for Those Claims

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

The Look-Back Method

• An episode of care should be included in the AGB calculation if the claims related to that episode were “allowed” by the insurance provider during the specified 12-month period.

• If your hospital isn’t notified of an allowed claim, you may need to find another method of determining the amount allowed.

– An alternative should be acceptable as long as it is consistently applied and doesn’t appear to be arbitrarily benefitting the hospital.

20

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

The Look-Back Method

• Once the hospital determines which episodes of care to include in the calculation, the numerator should include all payments related to those episodes of care.

– Include amounts the individual is personally liable to pay in the form of co-payments, co-insurance, and deductibles.

◊ It doesn’t matter when the amount is actually paid.

• The denominator should include the gross charges for those episodes of care.

21

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

The Look-Back Method

• The hospital may calculate the AGB percentage using either:

– Claims allowed for all medical care; or

– Claims allowed for emergency and other medically necessary care.

• A sample of claims is not allowed.

• The hospital may calculate the AGB percentage as often it likes, but it must always use a full 12 months in the calculation.

22

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

The Look-Back Method

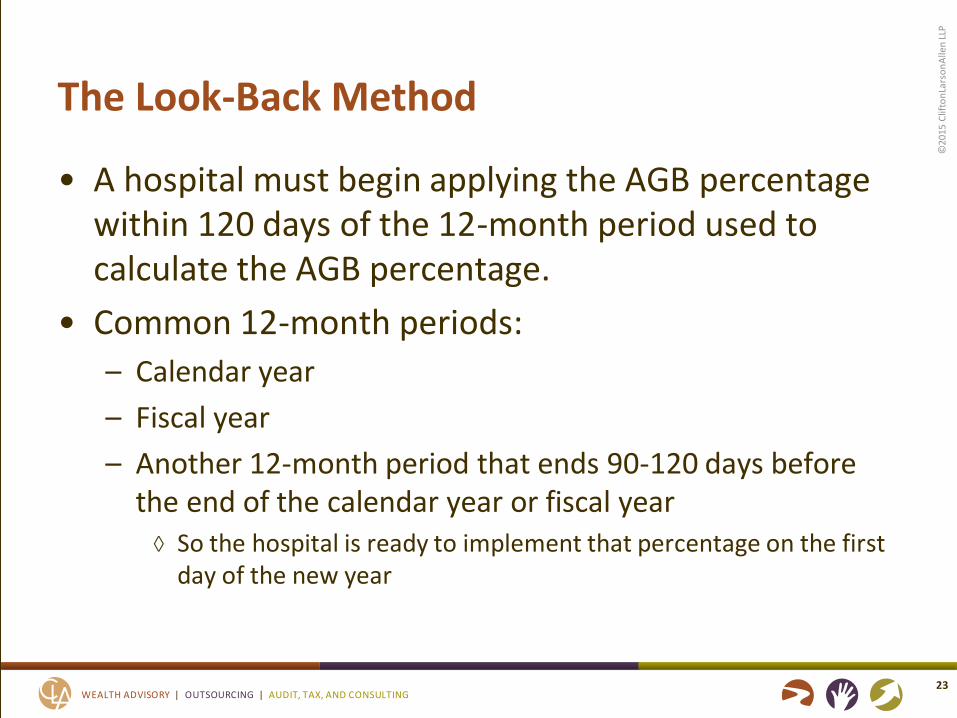

• A hospital must begin applying the AGB percentage within 120 days of the 12-month period used to calculate the AGB percentage.

• Common 12-month periods:

– Calendar year

– Fiscal year

– Another 12-month period that ends 90-120 days before the end of the calendar year or fiscal year

◊ So the hospital is ready to implement that percentage on the first day of the new year

23

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

The Look-Back Method

• A hospital may calculate:

– One average AGB percentage or

– Multiple AGB percentages for separate categories of care. ◊ Inpatient vs. outpatient, by department, by service, etc.

• If multiple AGB percentages are calculated, the hospital must ensure it calculates the AGB percentage for all emergency and other medically necessary care.

24

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

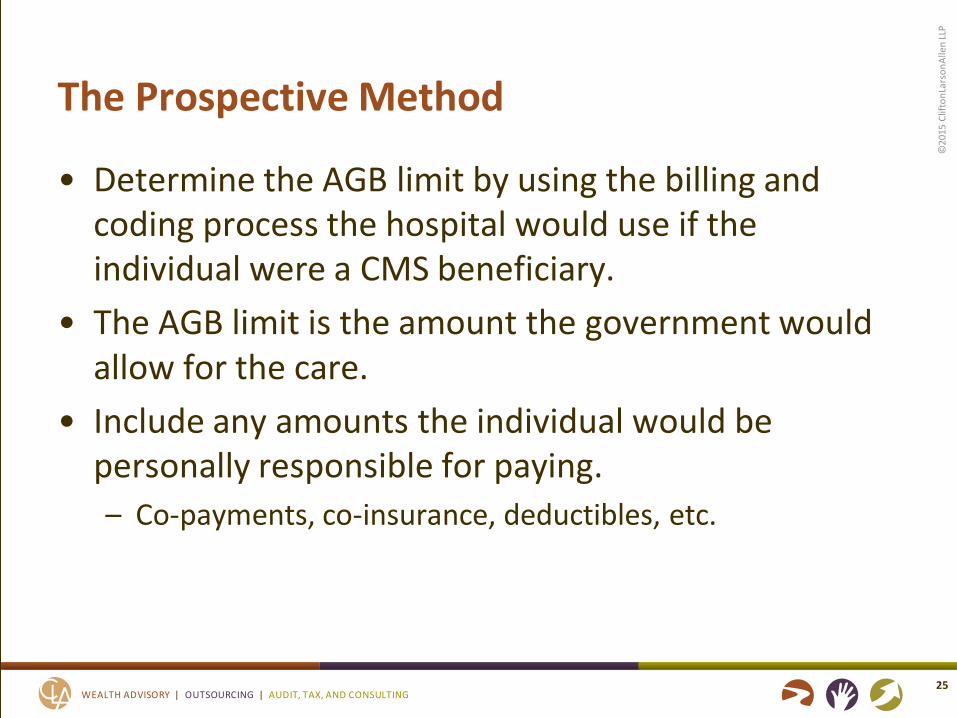

The Prospective Method

• Determine the AGB limit by using the billing and coding process the hospital would use if the individual were a CMS beneficiary.

• The AGB limit is the amount the government would allow for the care.

• Include any amounts the individual would be personally responsible for paying.

– Co-payments, co-insurance, deductibles, etc.

25

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

The Prospective Method

• Can use either Medicare fee-for-service, Medicaid, or both.

– Medicare Parts A and B

• Examples:

– Use Medicare fee-for-service for all calculations

– Use Medicaid for all calculations

– Use Medicare fee-for-service for some calculations and Medicaid for other calculations.

◊ Inpatient based on Medicaid and outpatient based on Medicare fee-for-service

◊ Hospital based on Medicare and clinics based on Medicaid

26

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Gross Charges

• For a FAP-eligible person, it’s okay for the billing statement to indicate gross charges as long as the individual is personally required to pay a smaller amount.

– The financial assistance will decrease the amount.

– Contractual allowances, other discounts, and other deductions may further decrease the amount.

27

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Billing and Collection

• 501(r)(6) requires a hospital to not engage in extraordinary collection actions (“ECA”s) before it has made reasonable efforts to determine whether an individual is FAP-eligible.

28

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

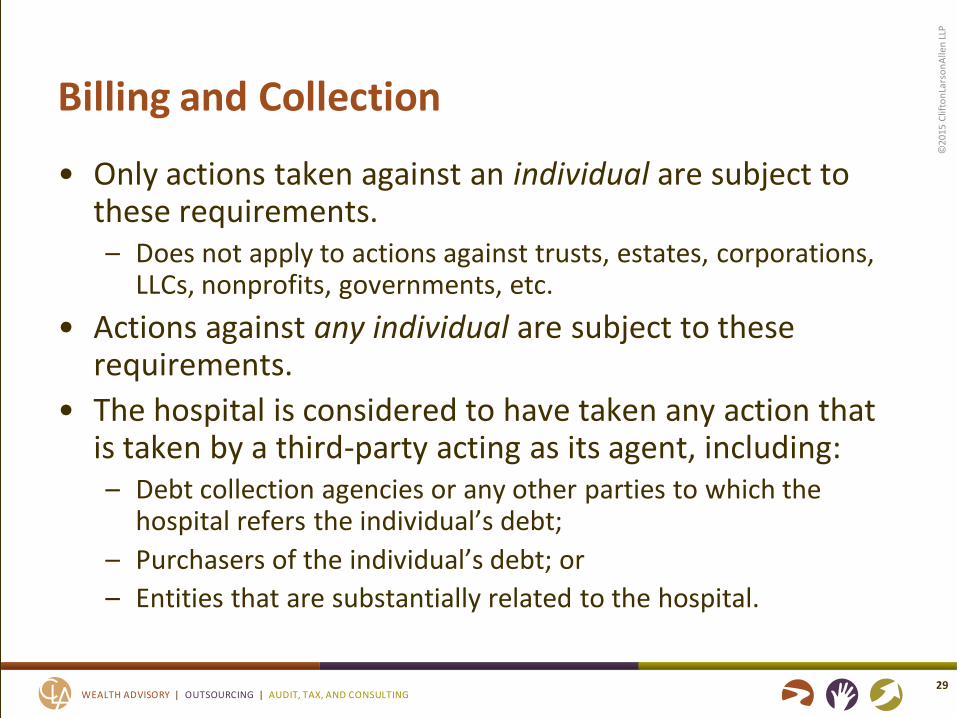

Billing and Collection

• Only actions taken against an individual are subject to these requirements. – Does not apply to actions against trusts, estates, corporations,

LLCs, nonprofits, governments, etc.

• Actions against any individual are subject to these requirements.

• The hospital is considered to have taken any action that is taken by a third-party acting as its agent, including: – Debt collection agencies or any other parties to which the

hospital refers the individual’s debt;

– Purchasers of the individual’s debt; or

– Entities that are substantially related to the hospital.

29

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Extraordinary Collection Actions

• Selling a debt to another party

• Reporting adverse information to a consumer credit reporting agency or credit bureau

• Deferring or denying medically necessary care because of nonpayment of a bill for previously provided care covered under the hospital’s FAP

30

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Extraordinary Collection Actions

• Requiring payment before providing medically necessary care because of nonpayment of a bill for previously provided care covered under the hospital’s FAP

– If an individual has any outstanding bills for previously provided care, any required prepayments are presumed to be because of the outstanding bills unless the hospital can demonstrate otherwise.

– Best evidence is requiring prepayment from all individuals regardless of payment history.

31

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Extraordinary Collection Actions

• Actions that require a legal or judicial process

– Examples: ◊ Liens on property

◊ Foreclosing on real property

◊ Attaching or seizing a bank account or any other personal property

◊ Commencing a civil action

◊ Causing an arrest

◊ Causing to be subject to a writ of body attachment

◊ Garnishing wages

32

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Not Extraordinary

• Selling a debt is not an ECA if, prior to the sale, the parties enter into legally binding written agreement in which: – The buyer is prohibited in engaging in any ECAs to obtain

payment; – The buyer is prohibited from charging interest on the debt in

excess of the rate in effect under section 6621(a)(2) at the time the debt is sold;

– The debt is returnable or recallable upon determination that the individual is FAP-eligible; and

– If the individual is determined to be FAP-eligible but the debt is not returned to the hospital, the buyer is required to follow procedures specified in the agreement to ensure that the individual is not required to pay more than they are responsible for paying as a FAP-eligible individual.

33

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Not Extraordinary

• ECAs do not include asserting a lien on the proceeds of a judgment, settlement, or compromise owed to an individual as a result of personal injuries for which the hospital provided care.

• ECAs do not include filing a claim in a bankruptcy proceeding.

34

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Reasonable Efforts

• The IRS provides three methods to put forth reasonable effort:

– Presumptive determinations

– Notification and processing of applications

– Selling a debt with an appropriate written agreement

• Reasonable efforts and extraordinary collection actions are all based on episodes of care.

35

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Reasonable Effort #1: Presumptive Determinations

• A hospital has made reasonable efforts to determine whether an individual is FAP-eligible if it makes the determination based on information provided by a third party or a prior FAP-eligibility determination.

• Three possible outcomes:

– 100% discount (full write-off)

– Partial discount (partial write-off)

– 0% discount (no write-off)

36

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Presumptive Determinations

• 100% Discount – this method qualifies as reasonable effort if the individual is notified in writing that their liability has been forgiven under the hospital’s FAP.

– No remaining liability = no further collection efforts

• 0% discount – this method does not qualify as reasonable effort.

– Must use reasonable effort method #2 - notification

37

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

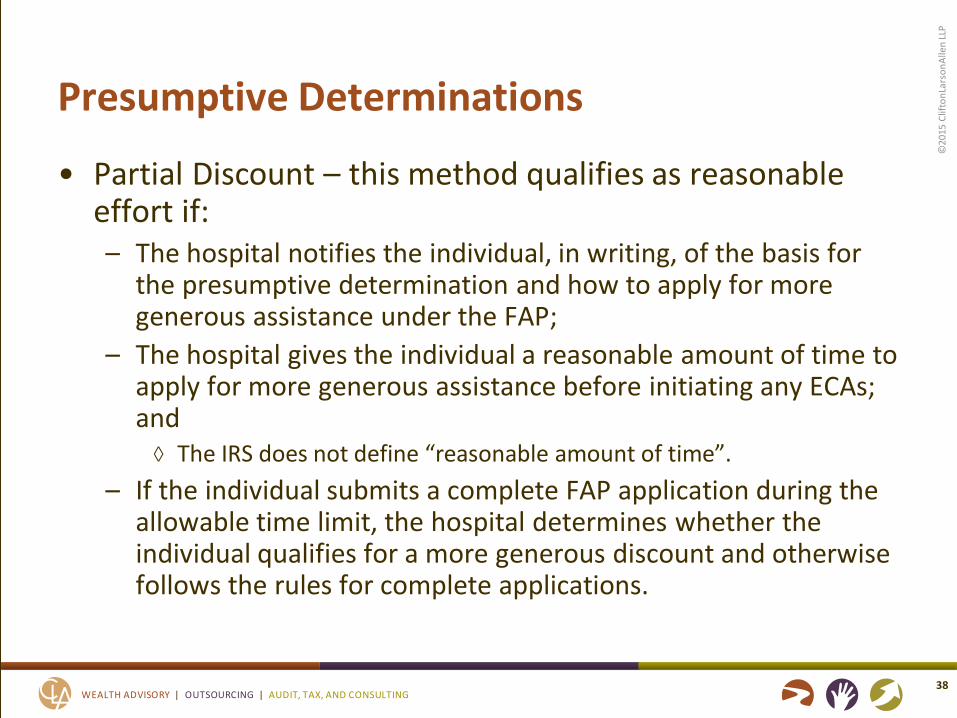

Presumptive Determinations

• Partial Discount – this method qualifies as reasonable effort if: – The hospital notifies the individual, in writing, of the basis for

the presumptive determination and how to apply for more generous assistance under the FAP;

– The hospital gives the individual a reasonable amount of time to apply for more generous assistance before initiating any ECAs; and

◊ The IRS does not define “reasonable amount of time”.

– If the individual submits a complete FAP application during the allowable time limit, the hospital determines whether the individual qualifies for a more generous discount and otherwise follows the rules for complete applications.

38

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Reasonable Effort #2: Notification and Applications • A hospital has made reasonable efforts to determine

whether an individual is FAP-eligible if it: – Notifies the individual about the FAP before initiating any

ECAs;

– Refrains from initiating any ECAs for at least 120 days after the first post-discharge billing statement is sent;

– If a person submits an incomplete FAP application, notifies the individual about how to complete the FAP application; and

– If a person submits a complete FAP application, determines whether the individual is FAP-eligible for the care.

39

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Notification and Applications

• Notifying an individual about the FAP requires the hospital to do all of the following at least 30 days before initiating any ECAs: – Provide the individual with a written notice that includes:

◊ Financial assistance is available for eligible individuals;

◊ Identification of ECAs that the hospital or third parties intend to take; and

◊ A deadline after which such ECAs may be initiated. • Deadline must be at least 30 days after this letter is sent.

– Provides the PLS with the written notice; and

– Makes reasonable efforts to orally notify the individual about the FAP and how they may obtain assistance with the FAP application process.

40

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Notification and Applications

• If a hospital wants to initiate a single ECA related to multiple episodes of care, it must meet the 120-day total deadline and the 30-day notice deadline for the most recent episode of care included in the ECA.

• Example:

– Episodes of care provided on 2/1, 2/15 and 2/28.

– Notice is provided on 5/20. ◊ 90 days after 2/28

– ECAs may be initiated on 6/20. ◊ 30 days after 5/20 and 120 days after 2/28

41

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Notification and Applications

• Special rule for notifying an individual if the hospital intends to delay or deny care due to nonpayment for prior care. – Not reasonable to provide a written notice, then wait 30 days.

• Instead: – Orally notify the individual about the FAP and how they may obtain

assistance with the FAP application process;

– Give a copy of the FAP application and PLS to the individual;

– Give a written notice indicating that financial assistance is available and stating the deadline, if any, after which the hospital will no longer accept a FAP application.

◊ Must be at least 30 days after this notice is provided and 240 days after the first post-discharge billing statement is sent.

– If the individual submits a complete FAP application, process it on an expedited basis.

42

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Notification and Applications

• If an individual submits an incomplete application within 240 days of sending the first post-discharge billing statement, the hospital has notified the individual only if it: – Suspends any ECAs to obtain payment for the care; and

– Provides the individual with a written notice that includes: ◊ The additional information and/or documentation required before

the FAP application will be considered complete;

◊ Phone number and physical address of a hospital office or department that can provide information about the FAP; and

◊ Phone number and physical address of somebody that can assist with the FAP application process.

43

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

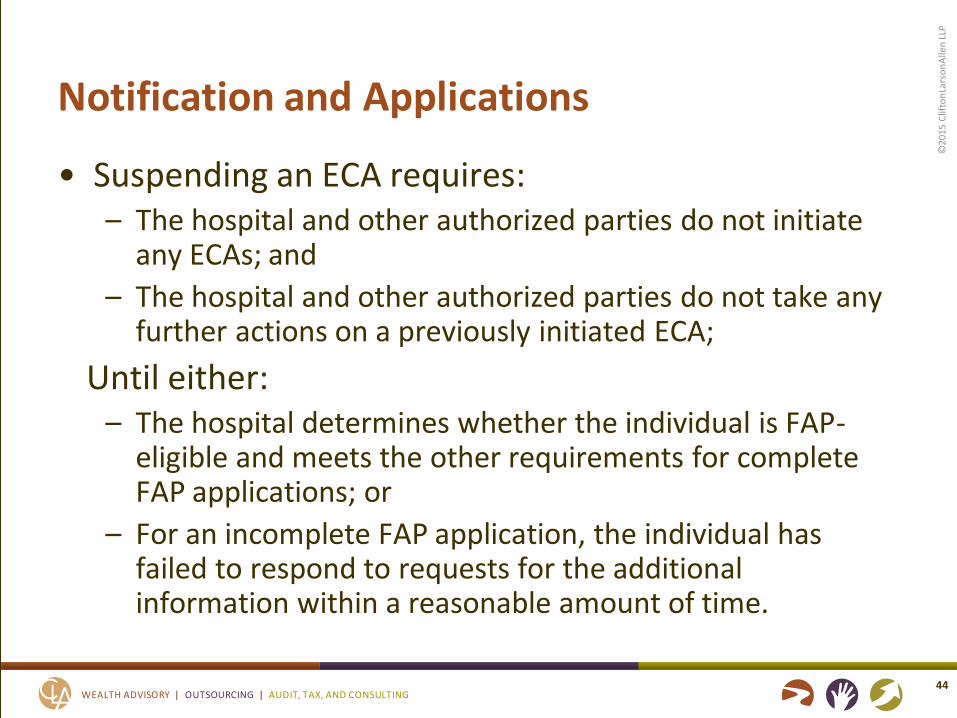

Notification and Applications

• Suspending an ECA requires: – The hospital and other authorized parties do not initiate

any ECAs; and

– The hospital and other authorized parties do not take any further actions on a previously initiated ECA;

Until either: – The hospital determines whether the individual is FAP-

eligible and meets the other requirements for complete FAP applications; or

– For an incomplete FAP application, the individual has failed to respond to requests for the additional information within a reasonable amount of time.

44

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Notification and Applications

• If an individual submits a complete application within 240 days of sending the first post-discharge billing statement, a hospital has made reasonable efforts if: – Any ECAs are suspended;

◊ See prior slide.

– The hospital makes a determination of the individual’s FAP-eligibility;

– Notifies the individual in writing of: ◊ The hospital’s determination;

◊ The basis for the determination; and

◊ If eligible, the assistance for which they qualify;

– Continued on next slide…

45

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Notification and Applications

• Complete applications (continued): – If the hospital determines the individual is eligible for a

discount, but not free care, provide a billing statement that includes:

◊ The remaining amount the individual owes; ◊ How that amount was determined; and ◊ Either state the AGB or describe how the individual can get that

information.

– If the hospital determines the individual is FAP-eligible, refund any amounts they have paid for the care, whether to the hospital or a third party, that exceeds the adjusted amount they owe;

◊ If less than $5, a refund is not required.

– Continued on next slide…

46

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Notification and Applications

• Complete applications (continued):

– If the hospital determines the individual is eligible for free care and had previously initiated any ECAs, take all reasonably available measures to reverse the ECA.

◊ Not required for sale of debt if the appropriate written contract is entered.

• See slide 54.

◊ Examples of reasonable measures:

• Vacating any judgments against the individual

• Lifting a levy or lien on the individual’s property

• Removing any adverse information from a credit report

47

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Anti-Abuse Rules

• A hospital has not made reasonable efforts if it determines an individual is not FAP-eligible based on information that the hospital:

– Has reason to believe is unreliable or incorrect; or

– Obtains under duress or through coercive practices. ◊ Example: delaying or denying emergency medical care until

information is provided

• Obtaining a signed waiver from an individual does not constitute reasonable effort.

48

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Medicaid

• Upon receiving a complete FAP application, it’s acceptable to delay processing the application until the individual is approved or denied by Medicaid.

49

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

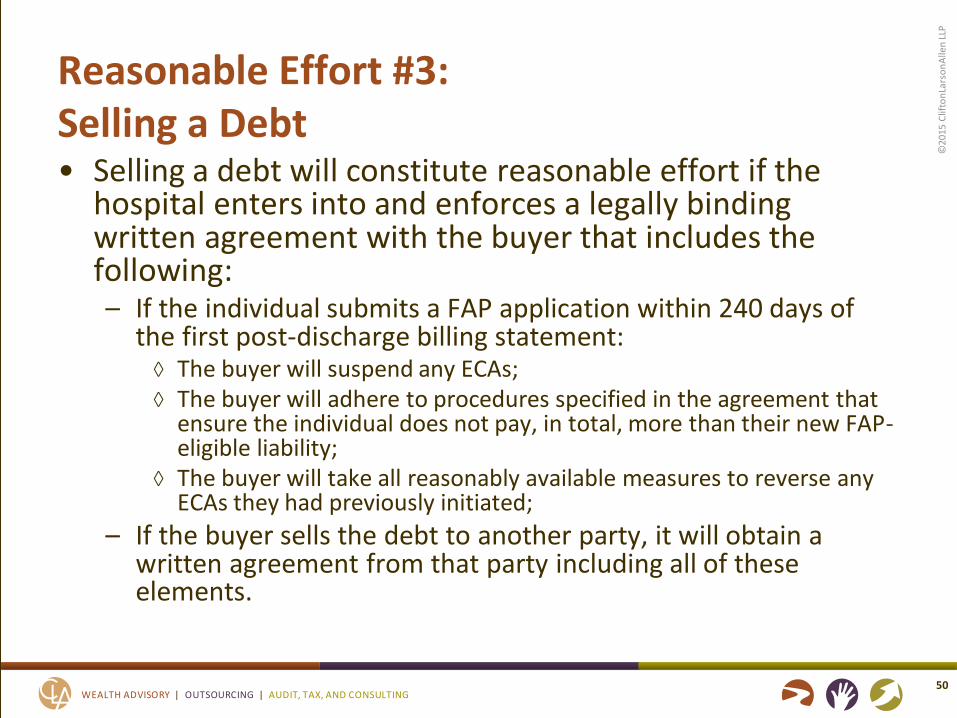

Reasonable Effort #3: Selling a Debt • Selling a debt will constitute reasonable effort if the

hospital enters into and enforces a legally binding written agreement with the buyer that includes the following: – If the individual submits a FAP application within 240 days of

the first post-discharge billing statement: ◊ The buyer will suspend any ECAs; ◊ The buyer will adhere to procedures specified in the agreement that

ensure the individual does not pay, in total, more than their new FAP-eligible liability;

◊ The buyer will take all reasonably available measures to reverse any ECAs they had previously initiated;

– If the buyer sells the debt to another party, it will obtain a written agreement from that party including all of these elements.

50

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

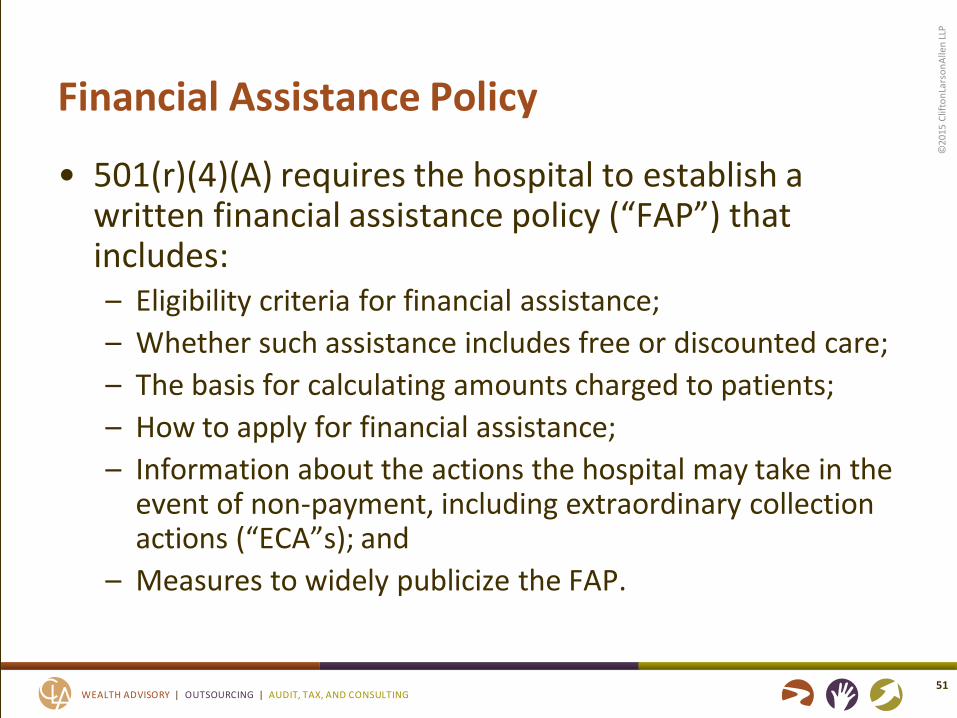

Financial Assistance Policy

• 501(r)(4)(A) requires the hospital to establish a written financial assistance policy (“FAP”) that includes: – Eligibility criteria for financial assistance;

– Whether such assistance includes free or discounted care;

– The basis for calculating amounts charged to patients;

– How to apply for financial assistance;

– Information about the actions the hospital may take in the event of non-payment, including extraordinary collection actions (“ECA”s); and

– Measures to widely publicize the FAP.

51

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Financial Assistance Policy

• The FAP must apply to all emergency and other medically necessary care provided within the hospital.

– If a location or service is not required to comply with 501(r), consider having a separate policy or guidelines for it.

52

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Financial Assistance Policy

• The final regulations added information that must be included in the FAP:

– The eligibility criteria for each level of financial assistance;

– The basis for calculating amounts charged to patients;

– The method of applying for financial assistance;

– Actions that may be taken in the event of nonpayment;

53

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Financial Assistance Policy

• The final regulations added information that must be included in the FAP:

– If applicable, information obtained from third parties that the hospital uses to determine FAP-eligibility;

– Whether and under what circumstances the hospital uses prior FAP-eligibility determinations to presumptively determine an individual’s current FAP-eligibility; and

– A list of providers delivering emergency or other medically necessary care in the hospital, identifying those that are covered by the hospital’s FAP and those that are not.

54

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Interaction With Washington State Law

• Washington State has specific rules related to financial assistance – RCW 70.170, WAC 246-453

• Hospitals must comply with both sets of rules at all times.

• State-specific guidance and assistance – http://www.wsha.org/our-members/resources-for-

hospitals/financial-assistance-information-for-hospitals/

• WSHA contact = Zosia Stanley – (206) 216-2511

55

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Washington Charity Care Sliding Scale

56

Family Income Level Qualifying Patient

0-100% FPL Law: Full write off

101-200% FPL Law: Sliding scale discount Pledge: Discounts to reflect cost of care

201-300% FPL Pledge: Discounts off of charges to reflect 130% cost of care

Can provide steeper discounts – many policy go to 400% FPL

Per hospital policy

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Eligibility Criteria & Basis for Calculations

• The FAP must include:

– All financial assistance available under the FAP;

– The amount(s) to which any discounts will be applied;

– The eligibility criteria for each level of assistance; and

– AGB information.

57

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Eligibility Criteria & Basis for Calculations

• The FAP must include the method used by the hospital to determine AGB. – Look-back method or prospective method

• If the look-back method is used, the FAP must include either: 1. The AGB percentage(s) that the hospital currently uses to

determine the AGB limit and a description of how they were calculated; or

2. How an individual can obtain this information in writing and free of charge. ◊ If #2 is chosen, then this information must be made widely

available to the public in all of the same ways as the FAP itself.

58

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Eligibility Criteria & Basis for Calculations

• Compare eligibility criteria between the following to make sure they align. – FAP

– Application and instructions

– Used in practice

• Examples of criteria used by hospitals: – Federal Poverty Guidelines (“FPG”)

– Residency

– Assets

– Eligibility for other assistance or programs

– Completed application with all required support

– Time limit

59

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Eligibility Criteria & Basis for Calculations

• Be extremely specific and accurate!

• If assets are used:

– Are assets used to determine eligibility?

– Are assets used to determine level of assistance?

– Which assets are included or excluded? ◊ Personal and/or second residence

◊ Vehicles

◊ Retirement assets

◊ Business assets

◊ Personal recreation (ATV, motorcycle, snowmobile, etc.)

60

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Eligibility Criteria & Basis for Calculations

• Be extremely specific and accurate!

• Within a range of FPG, is the discount set or sliding?

– Example: ◊ Financial Assistance: 100% discount below 100% of FPG; 75%

discount between 100% and 200% of FPG.

◊ Personal income is 150% of FPG.

◊ Set Discount = 75%

◊ Sliding Discount = 75% + [25% x (150 - 100) / (200 - 100)] = 87.5%

• How is “income” defined and/or determined?

61

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Method of Applying

• The FAP must include how an individual applies for financial assistance.

• Include information on valid methods of submitting an application.

– Mail – provide address and “attention”

– In person – provide acceptable drop-off locations

– Email – provide address

– Fax – provide number and “attention”

– Phone – provide number

62

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

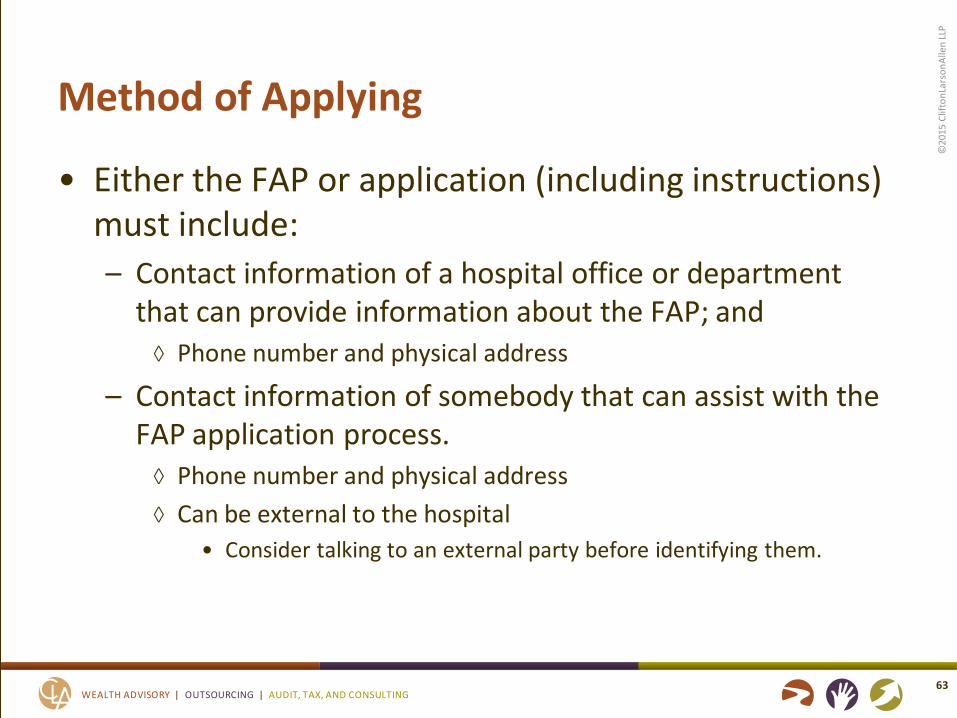

Method of Applying

• Either the FAP or application (including instructions) must include:

– Contact information of a hospital office or department that can provide information about the FAP; and

◊ Phone number and physical address

– Contact information of somebody that can assist with the FAP application process.

◊ Phone number and physical address

◊ Can be external to the hospital

• Consider talking to an external party before identifying them.

63

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Method of Applying

• Either the FAP or application (including instructions) must include the information and documentation a person may be required to submit as part of their FAP application.

– An individual may not be denied for failure to provide information unless the FAP or application specifically identifies it.

– Include anything you may ever want!

– An individual can be granted financial assistance even if they fail to provide required information.

64

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Actions That May Be Taken

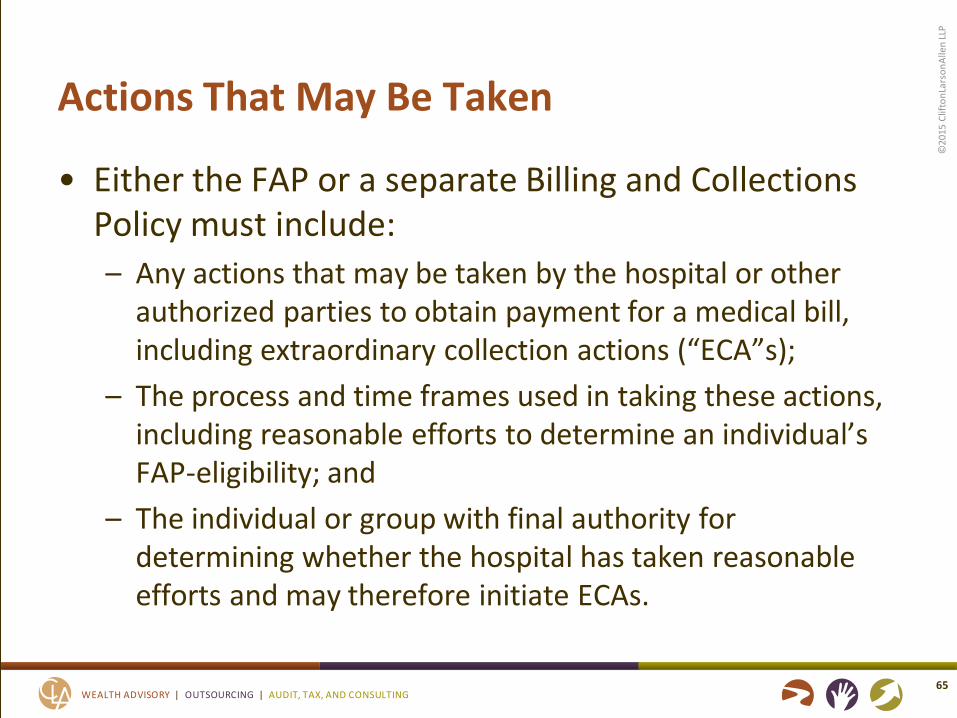

• Either the FAP or a separate Billing and Collections Policy must include:

– Any actions that may be taken by the hospital or other authorized parties to obtain payment for a medical bill, including extraordinary collection actions (“ECA”s);

– The process and time frames used in taking these actions, including reasonable efforts to determine an individual’s FAP-eligibility; and

– The individual or group with final authority for determining whether the hospital has taken reasonable efforts and may therefore initiate ECAs.

65

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Actions That May Be Taken

• Be as detailed and comprehensive as possible in all actions used to obtain payment.

– Actions taken before the person enters the hospital

– Actions taken while at the hospital ◊ Conversations, documents, posters, brochures, etc.

– Actions taken after the person leaves the hospital ◊ Phone calls, billing statements, letters, collection agencies,

reporting to credit bureaus, legal actions, etc.

– Actions taken by third parties

– Identify ECAs as extraordinary

• Be as specific as possible in the time frames.

66

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Actions That May Be Taken

• Be as detailed and comprehensive as possible in all reasonable efforts made.

– Actions taken before the person enters the hospital

– Actions taken while at the hospital ◊ Conversations, documents, posters, brochures, etc.

– Actions taken after the person leaves the hospital ◊ Phone calls, billing statements, letters, presumptive eligibility

determinations, etc.

– Actions taken by third parties

– Identify ECAs

• Be as specific as possible in the time frames.

67

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Actions That May Be Taken

• If a separate Billing and Collections Policy is used, the FAP must include:

– A statement that the actions the hospital may take in the event of nonpayment are described in a separate Billing and Collections Policy; and

– How to obtain a free copy of the Billing and Collections Policy.

68

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Prior Determinations

• The IRS considers financial assistance separately for each episode of care.

• The FAP should specify how long an approval is valid.

– How far into the past?

– How far into the future?

69

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

List of Providers

• The hospital can provide the information as succinctly as possible, as long as it accurately covers all emergency and other medically necessary care offered in the hospital.

• The FAP may list the names of individual doctors, practice groups, or any other entities.

• The FAP may specify providers by reference to a department or a type of service.

70

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

List of Providers

• If a provider’s services are sometimes covered and sometimes not covered, then policy must describe the situations.

• The hospital is not required to indicate whether a provider’s services are (or may be) covered by another entity’s financial assistance policy.

• The provider list may be maintained in an attachment/exhibit/appendix to the FAP. – It must indicate the date it was created or last updated.

– The FAP must indicate that the list is maintained in a separate document and explain where to find it.

71

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Plain Language Summary

• The hospital must create a plain language summary (“PLS”) of its FAP that includes the following: – A statement that the hospital offers financial assistance under a

FAP;

– A statement that a FAP eligible individual will not be charged more than AGB for emergency and other medically necessary care

– A description of the eligibility requirements;

– A description of the assistance offered;

– A summary of how to apply;

– The URL and physical locations where free copies of the FAP and FAP application can be obtained;

72

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Plain Language Summary

• The hospital must create a plain language summary (“PLS”) of its FAP that includes the following: – How to obtain a free copy of the FAP and FAP application

by mail;

– The contact information of the hospital office or department that can provide information about the FAP;

◊ Phone number and physical location

– The contact information of somebody that can assist with the FAP application process; and

◊ Phone number and physical location

– The availability of translations of the FAP, FAP application and PLS into other languages, if applicable.

73

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Publicizing the FAP

• The hospital must:

– Make the FAP, FAP application and PLS widely available on a website.

– Make paper copies of the FAP, FAP application and PLS available upon request and without charge:

◊ By mail,

◊ In the emergency room, and

◊ In all admissions areas;

– Notify and inform members of the community about the FAP in a manner reasonably calculated to reach those individuals who are most likely to require financial assistance from the hospital;

◊ See the “notify and inform” slide.

74

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Publicizing the FAP

• The hospital must (continued):

– Offer a paper copy of the PLS to patients as part of either intake or discharge;

– Include a conspicuous written notice on billing statements about the hospital’s financial assistance; and

– Set up conspicuous public displays (or other measures reasonably calculated to attract attention) that notify and inform patients about the FAP in:

◊ The emergency room, and

◊ All admissions areas.

75

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Websites

• “Widely available on a website” means: – A complete and current version of the document is

conspicuously posted on: ◊ The hospital’s website; ◊ If the hospital doesn’t have its own website, on its parent’s website;

or ◊ On a third party’s website.

– Individuals with access to the internet can access, download, view, and print a copy of the document:

◊ Without requiring special hardware or software; ◊ Without paying any fees; and ◊ Without creating an account or otherwise being required to provide

personally identifiable information.

– The hospital provides the URL to any individual who asks how to access the document online.

76

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

E.R. and Admissions Areas

• The most common methods of making the required documents available are:

– Pre-printed copies are maintained in each location

– Copies are saved on a computer in each location

– A link to the website is on a computer in each location

77

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Billing Statements

• The information on billing statements must include:

– A statement that the hospital offers financial assistance under the FAP;

– The telephone number of the hospital officer or department that can provide information about the FAP; and

– The URL where the documents are available.

78

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Notify and Inform

• The IRS provides no requirements about the methods or frequency used by a hospital to push financial assistance information out to the community.

• The method must include:

– Notification that the hospital offers financial assistance under a FAP; and

– How or where to obtain information about the FAP and application process; and

– How or where to obtain copies of the relevant documents.

79

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Notify and Inform

• Examples:

– Billboards

– TV, radio, or newspaper ads

– Emails

– Mailings

– Pamphlets, flyers, handouts, posters, etc. ◊ Churches

◊ Social service offices

◊ Senior living facilities

◊ Schools

◊ Grocery stores and gas stations

80

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Limited English Proficiency

• If the hospital’s community includes a significant population with limited English proficiency (“LEP”), the hospital is required to:

– Translate the FAP, FAP application, PLS, and all other required documents into that population’s primary language; and

– Widely publicize the translated copies.

81

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Limited English Proficiency

• A population is significant if it exceeds the lesser of: – 1,000 individuals;

– 5% of the hospital’s community; or

– 5% of the population likely to be affected or encountered by the hospital.

• A hospital can use any reasonable method to determine the size of an LEP population. – Most recent U.S. census data is specifically identified as

acceptable. ◊ Google “[county name], [state], u.s. census quickfacts”

◊ “Foreign born persons”

◊ “Language other than English spoken at home”

82

©20

15 C

lifto

nLa

rso

nA

llen

LLP

WEALTH ADVISORY | OUTSOURCING | AUDIT, TAX, AND CONSULTING

Kurt Bennion, CPA

(425) 250-6074

Questions & Answers