goldman sachs - asean coal initiation - jun 2oo8

DESCRIPTION

ASEAN Coal Initiation - Jun 2OO8TRANSCRIPT

June 19, 2008 ASEAN: Metals & Mining: Coal

Goldman Sachs Global Investment Research 1

June 19, 2008

ASEAN: Metals & Mining: Coal

Bullish on cycle, earnings momentum; initiate 4 cos, Banpu to CL

Initiate on ASEAN coal sector with an attractive stance

We believe thermal coal is at the cusp of a stronger and longer upcycle as

continued robust demand from emerging markets, unceasing supply

constraints and relative attractiveness of coal to oil underpin high prices till

2010E/2011E. We initiate coverage on the ASEAN coal sector with an attractive

stance on the back of our bullish outlook for thermal coal. As the largest

exporters of seaborne thermal coal, we believe that Indonesian coal producers

will emerge as major beneficiaries of the thermal coal price rally as they enter a

new phase of unprecedented earnings growth.

Major themes supporting our bullish view

1) We believe that incremental coal supply from Indonesia is likely to be

regimented—given underinvestment in exploration over the past few years,

infrastructure and equipment constraints, and rising domestic demand—

which would support regional prices, 2) At the same time, prices of

Indonesian coal are breaking out from their historical trends given rising

pricing power in the export market and strong demand drivers in the

domestic market, 3) We are positive on the domestic upcycle driven by

higher substitution demand for coal, 4) Strong cost inflation on rising diesel

prices will lift marginal costs of production and provide a floor to regional

prices, in our view, and 5) Valuations of ASEAN coal companies also stack

up favorably as compared with its global peers at 16%-29% discount over its

China and US peers, respectively, on a 12-month forward P/E basis.

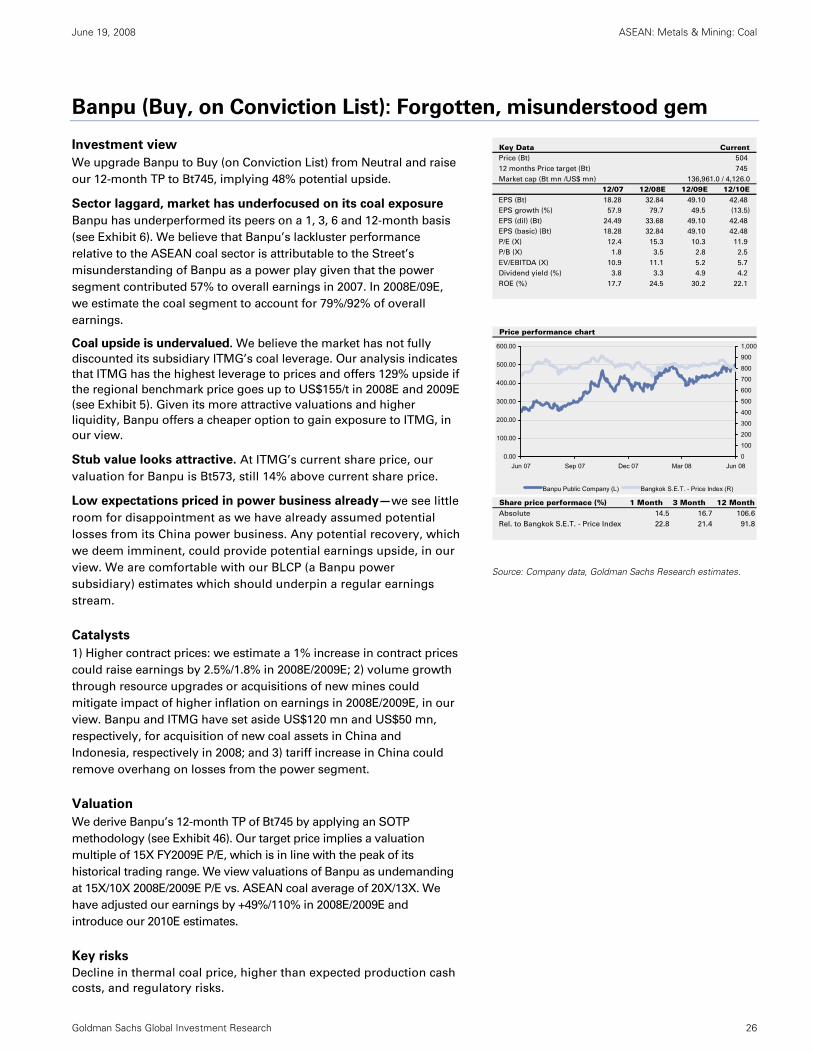

Banpu is our top pick, we also like TB Bukit Asam

Yoke Fong Chee is assuming primary coverage of Banpu. We upgrade Banpu

to Buy from Neutral, add it to our Conviction list, and raise our 12-m SOTP-

based TP to Bt745 (from Bt258), implying 48% potential upside. Banpu has

been the sector laggard as its coal exposure has been overlooked, in our view.

We believe Banpu offers cheaper coal exposure via its Indocoal subsidiary

ITMG, which has the highest upside potential to rising coal prices. We initiate

on ITMG with Buy and 12-m TP of Rp49,500 (13X FY09E P/E), implying 46%

potential upside. We initiate on TB Bukit Asam with a Buy (12-m DCF-based TP

of Rp20,500, 40% potential upside) based on its long-term growth prospects

and exposure to the growing domestic sector, and Bumi Resources and Straits

Asia Resources both with Neutral and 12-m TPs of Rp9,700 (18X FY09E P/E)

and S$4.70 (13X FY09E P/E), respectively, on lower relative risk-reward.

Risks: Regulatory risks (new Mining Bill) and decline in coal prices.

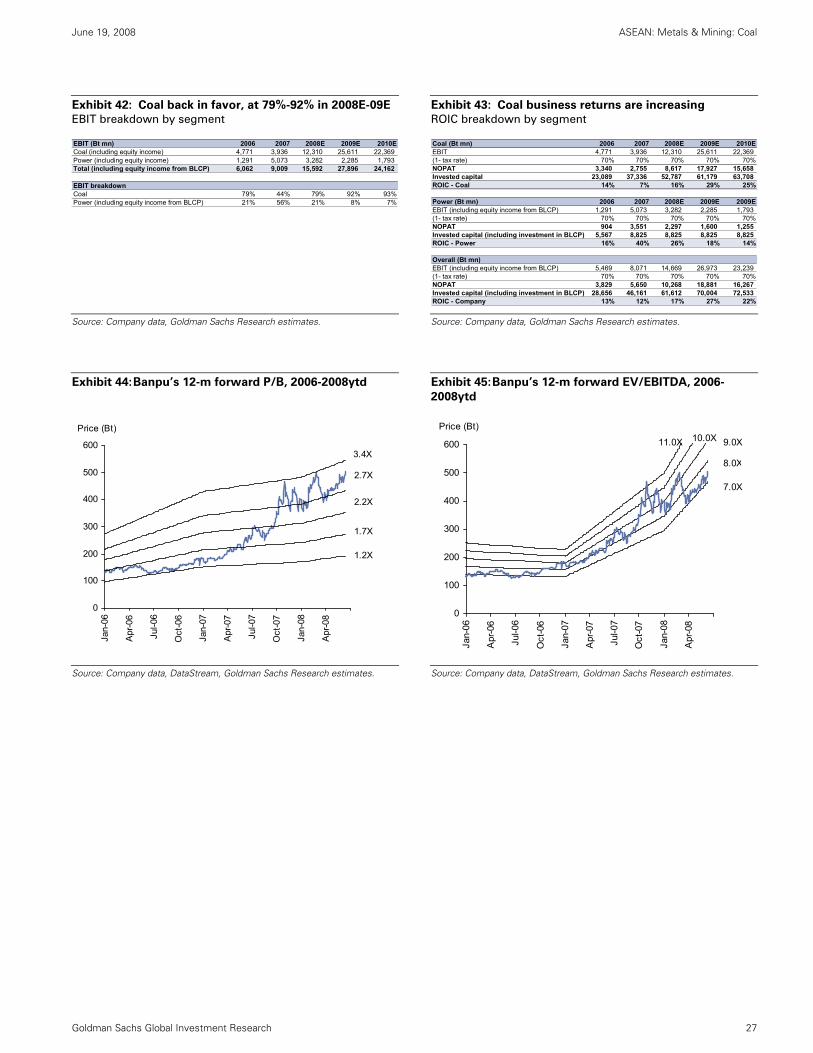

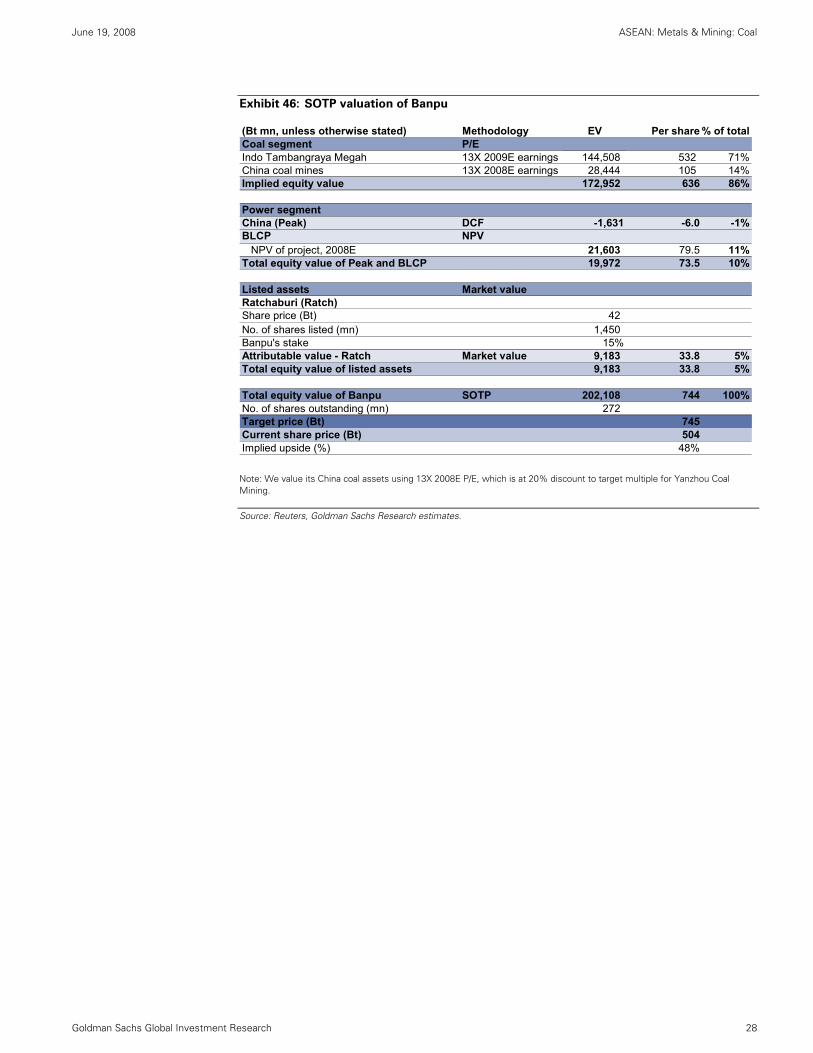

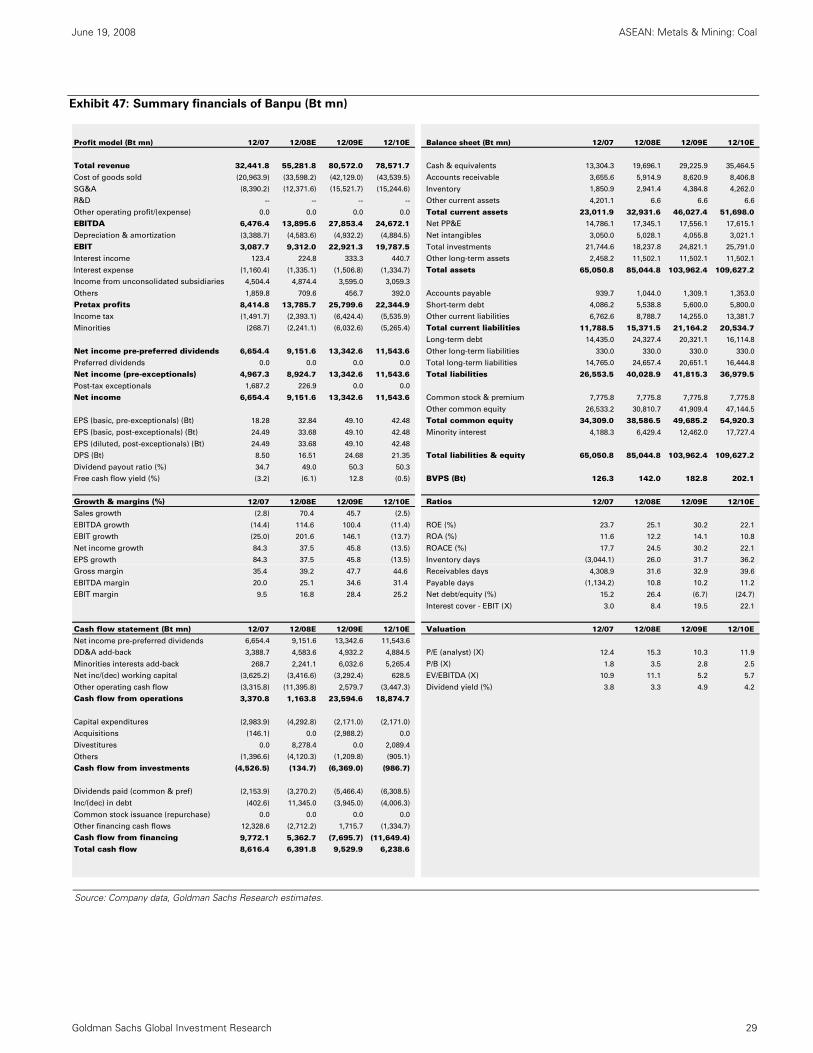

Banpu (BANP.BK, TP: Bt745, Buy, on Conviction List)

Key Data CurrentPrice (Bt) 504

Market cap (Bt mn /US$ mn) 136,961.0 / 4,126.0

12/07 12/08E 12/09E 12/10EEPS growth (%) 57.9 79.7 49.5 (13.5)

P/E (X) 12.4 15.3 10.3 11.9

EV/EBITDA (X) 10.9 11.1 5.2 5.7

ROE (%) 17.7 24.5 30.2 22.1

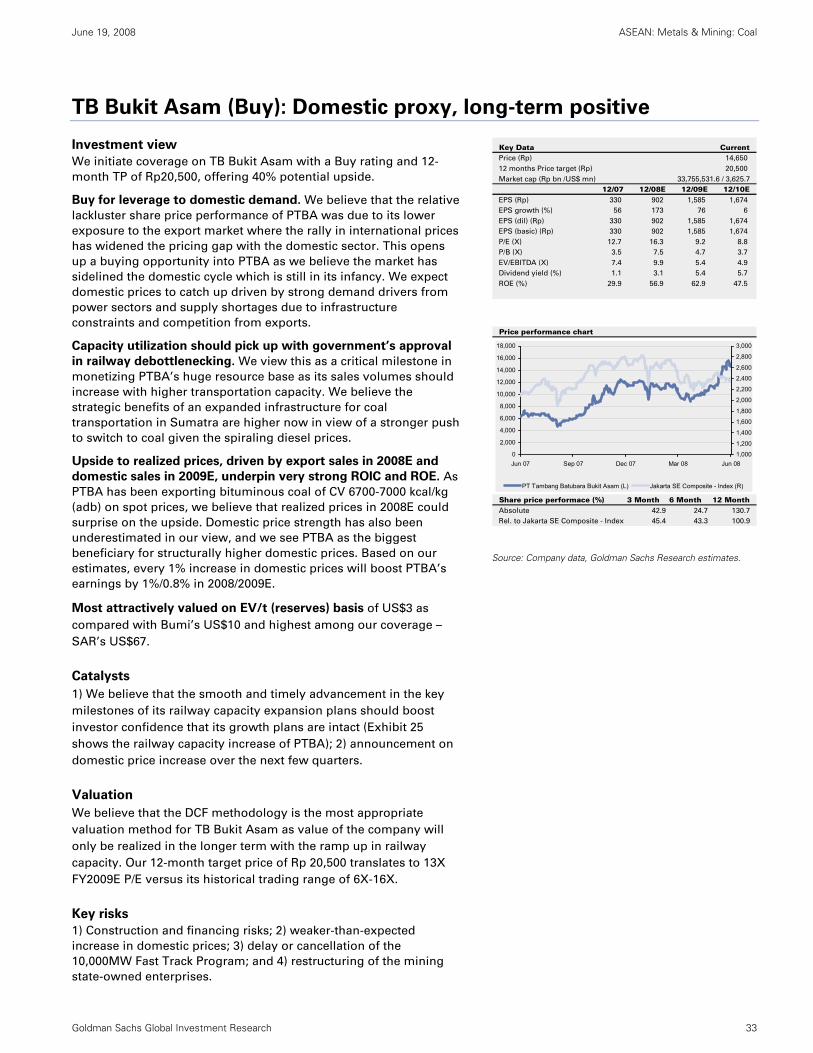

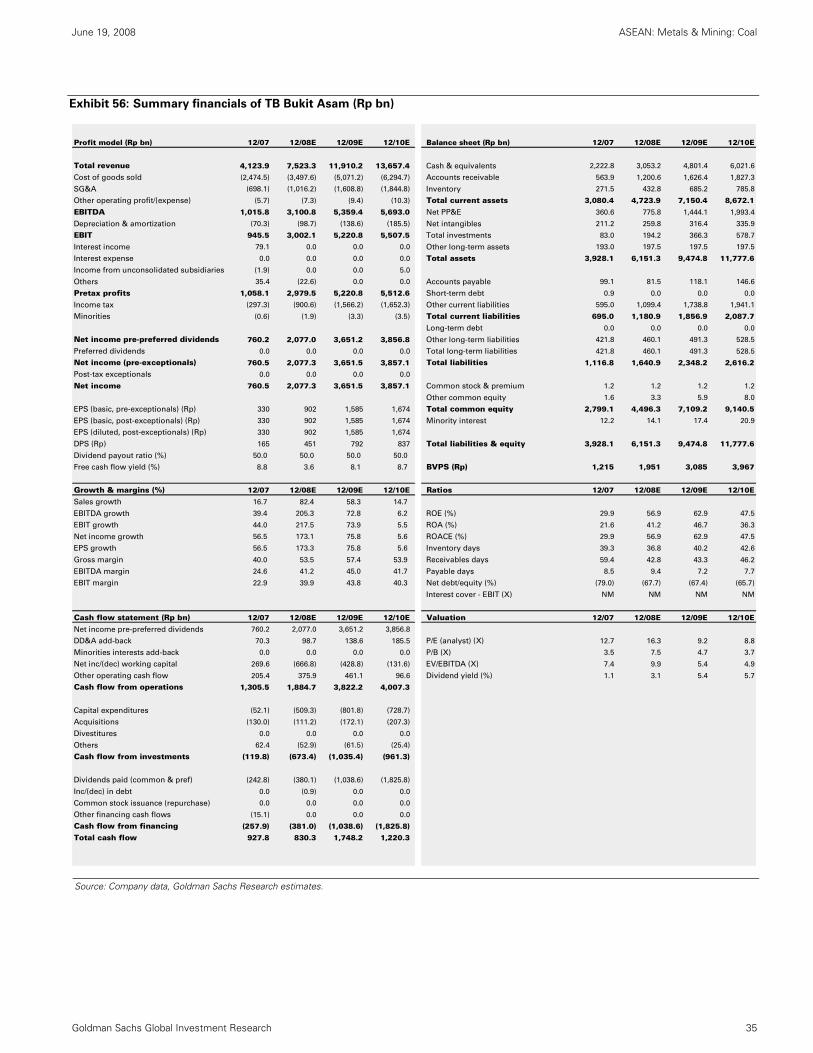

TB Bukit Asam (PTBA.JK, TP: Rp20,500, Buy)

Key Data CurrentPrice (Rp) 14,650

Market cap (Rp bn /US$ mn) 33,755,531.6 / 3,625.7

12/07 12/08E 12/09E 12/10EEPS growth (%) 56 173 76 6

P/E (X) 12.7 16.3 9.2 8.8

EV/EBITDA (X) 7.4 9.9 5.4 4.9

ROE (%) 29.9 56.9 62.9 47.5

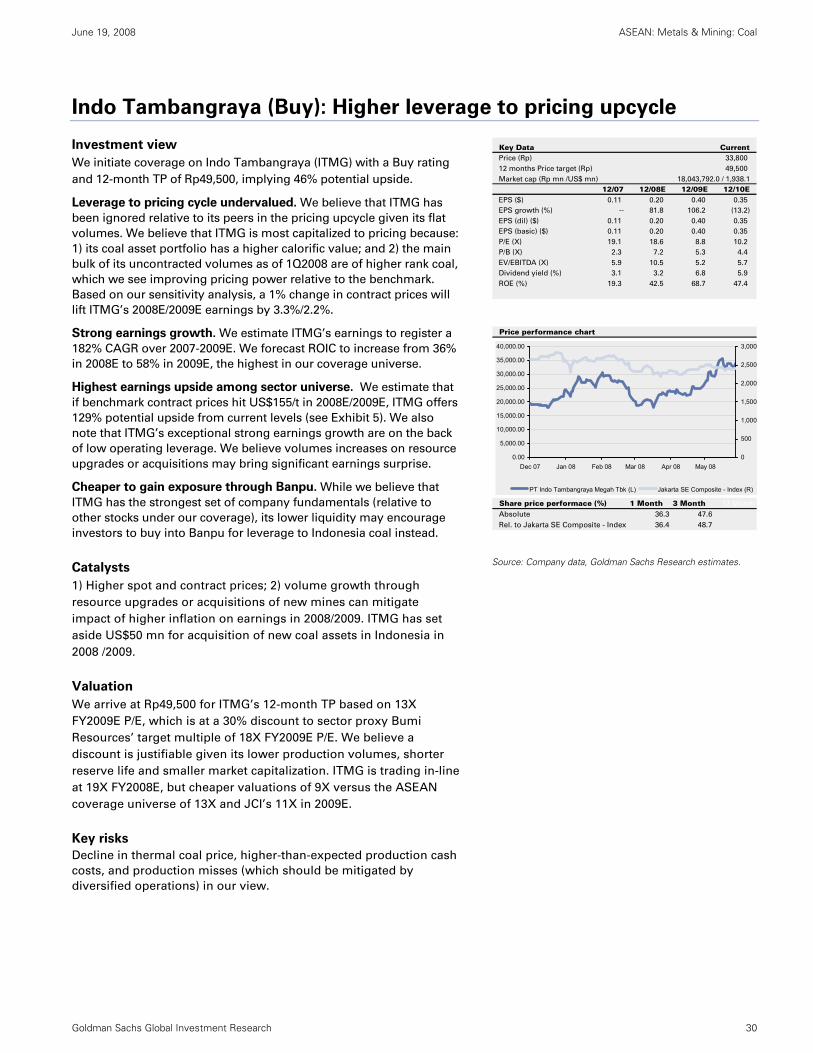

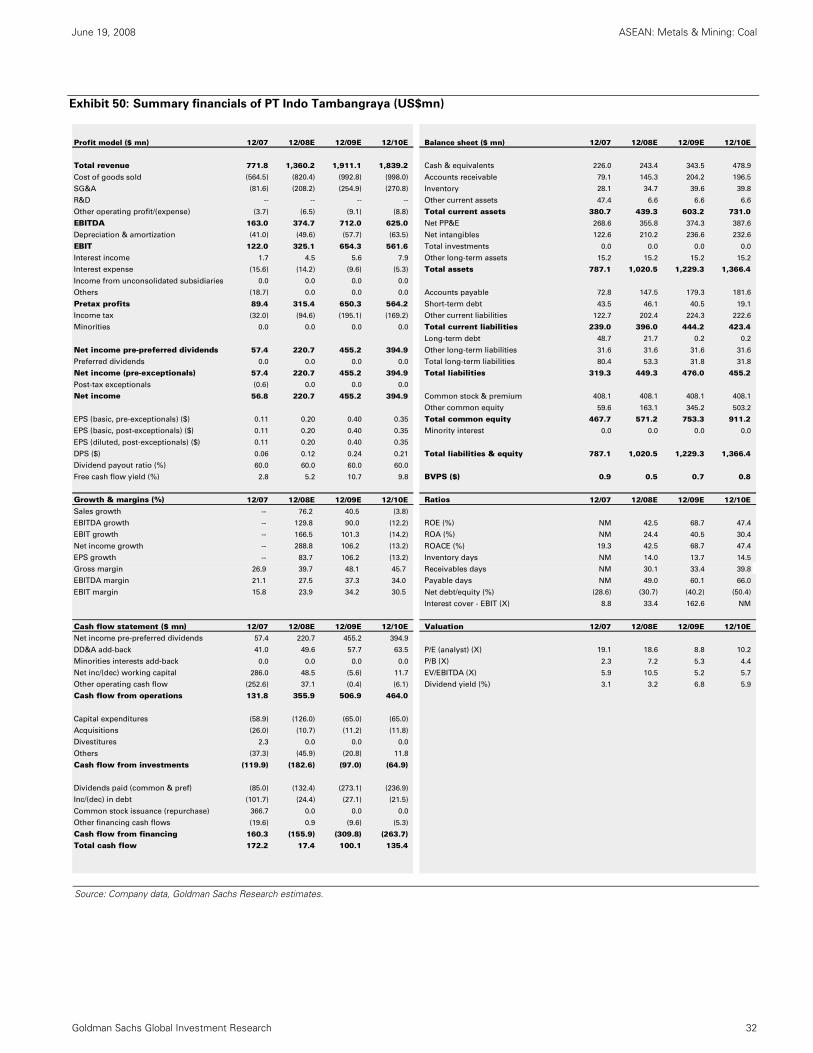

PT Indo Tambangraya (ITMG.JK, TP: Rp49,500, Buy)

Key Data CurrentPrice (Rp) 33,800

Market cap (Rp mn /US$ mn) 18,043,792.0/1,938.1

12/07 12/08E 12/09E 12/10EEPS growth (%) -- 81.8 106.2 (13.2)

P/E (X) 19.1 18.6 8.8 10.2

EV/EBITDA (X) 5.9 10.5 5.2 5.7

ROE (%) 19.3 42.5 68.7 47.4

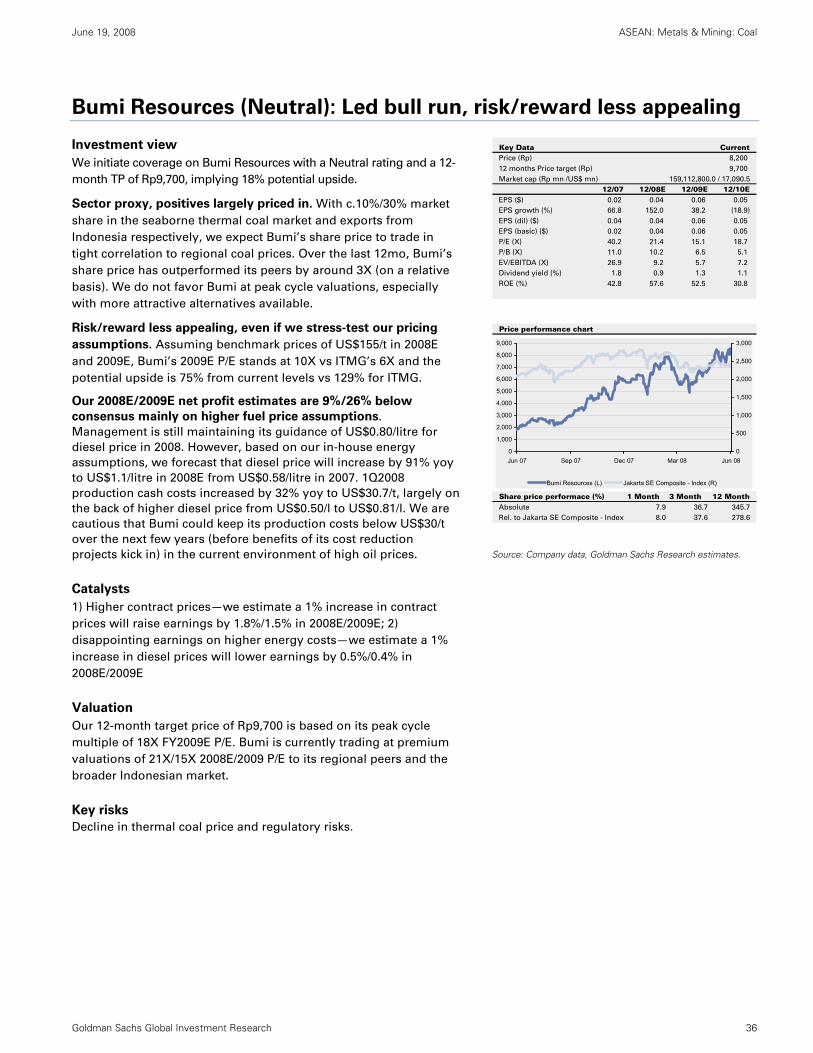

Bumi Resources (BUMI.JK, TP: Rp9,700, Neutral)

Key Data CurrentPrice (Rp) 8,200

Market cap (Rp mn /US$ mn) 159,112,800.0 / 17,090.5

12/07 12/08E 12/09E 12/10EEPS growth (%) 66.8 152.0 38.2 (18.9)

P/E (X) 40.2 21.4 15.1 18.7

EV/EBITDA (X) 26.9 9.2 5.7 7.2

ROE (%) 42.8 57.6 52.5 30.8

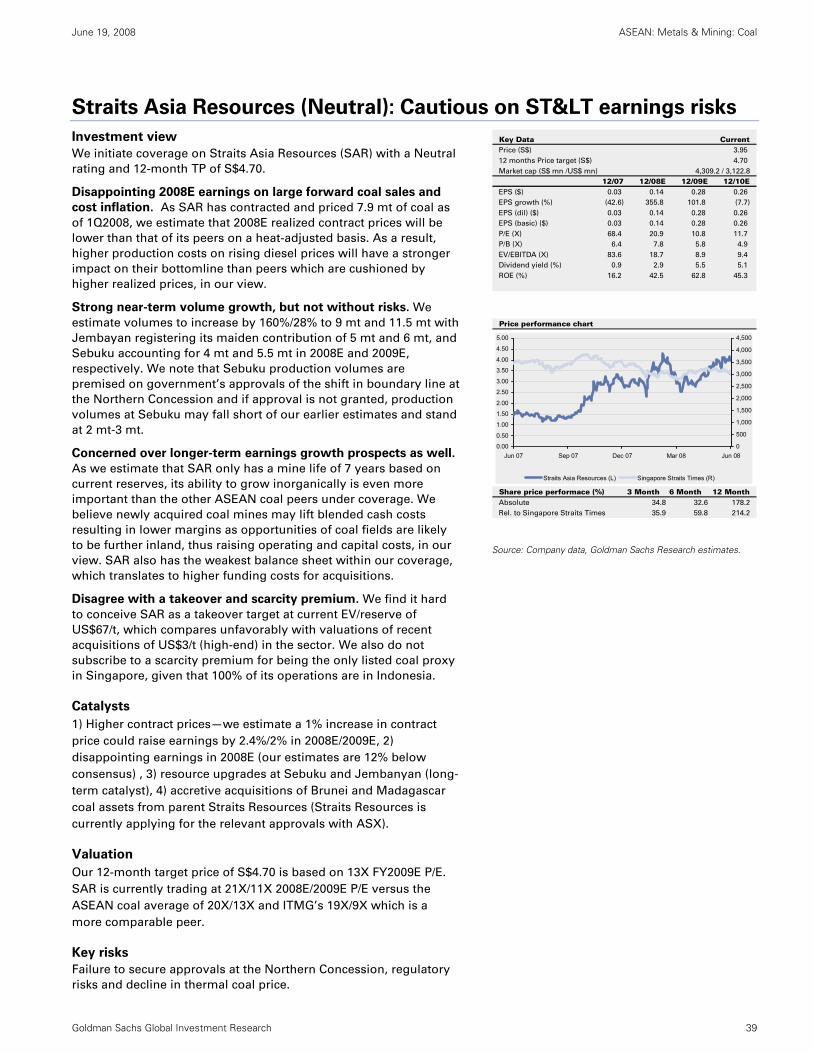

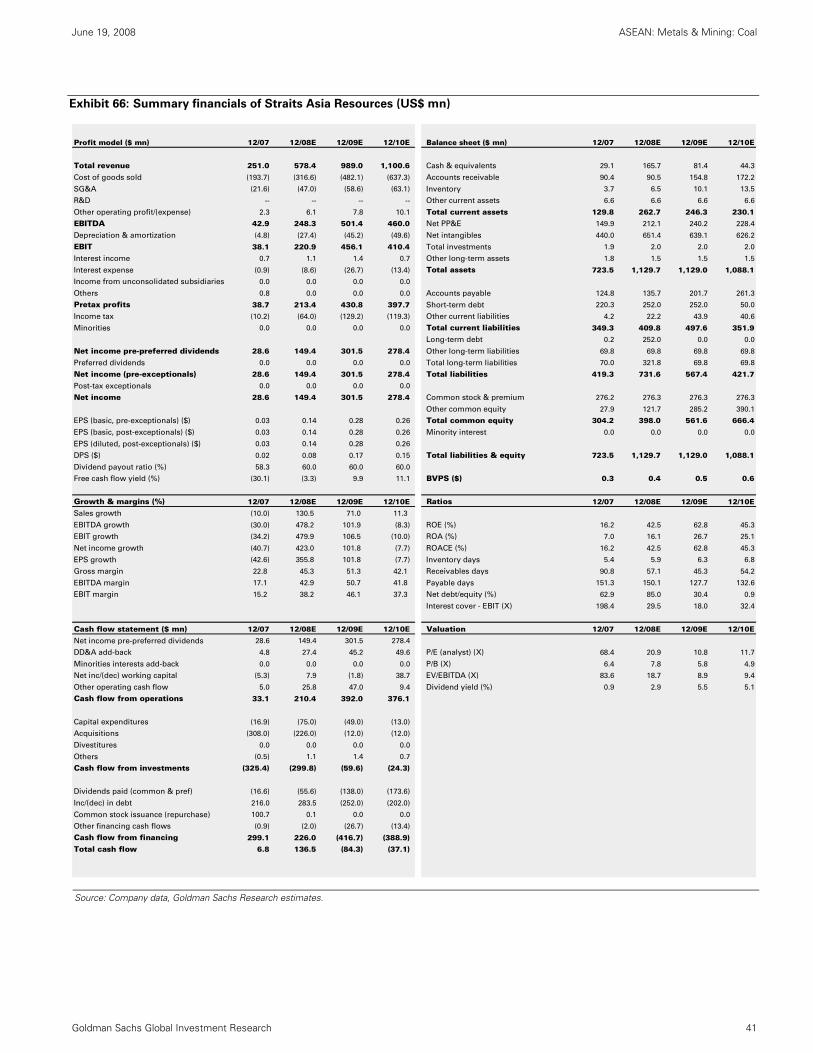

Straits Asia Resources (STRL.SI, TP: S$4.70, Neutral)

Key Data CurrentPrice (S$) 3.95

Market cap (S$ mn /US$ mn) 4,309.2,/3122.8

12/07 12/08E 12/09E 12/10EEPS growth (%) (42.6) 355.8 101.8 (7.7)

P/E (X) 68.4 20.9 10.8 11.7

EV/EBITDA (X) 83.6 18.7 8.9 9.4

ROE (%) 16.2 42.5 62.8 45.3

Note: Our target prices are based on a 12-month horizon.

Source: DataStream, Goldman Sachs Research estimates.

Yoke Fong Chee +65-6889-2486 | [email protected] Goldman Sachs (Singapore) Pte

Song Shen +852-2978-1131 | [email protected] Goldman Sachs (Asia) L.L.C.

The Goldman Sachs Group, Inc. does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. For Reg AC certification, see the text preceding the disclosures. For other important disclosures go to www.gs.com/research/hedge.html. Analysts employed by non-US affiliates are not required to take the NASD/NYSE analyst exam.

The Goldman Sachs Group, Inc. Global Investment Research

June 19, 2008 ASEAN: Metals & Mining: Coal

Goldman Sachs Global Investment Research 2

Table of contents

Stronger, longer upcycle drives next leg of outperformance 2

New phase of the upcycle merits peak valuation 7

Solid fundamentals continue to drive prices; we expect further upside to thermal coal cycle 11

Indonesian producers poised to benefit significantly as earnings momentum picks up 15

Risks: Spotlight will be on the long-delayed mining laws 25

Banpu (Buy, on Conviction List): Forgotten, misunderstood gem 27

Indo Tambangraya (Buy): Higher leverage to pricing upcycle 31

TB Bukit Asam (Buy): Domestic proxy, long-term positive 34

Bumi Resources (Neutral): Led bull run, risk/reward less appealing 37

Straits Asia Resources (Neutral): Cautious on ST< earnings risks 40

Disclosures 44

EXPECTED NEWS FLOW/EVENTS

DATE EVENT COMMENT

3Q2008 Release of the new Indonesian mining laws The long-delayed new mining laws should provide more clarity on the

legislative framework for investment.

2H2008 IPO of PT Adaro and other coal companies The IPO provides investors with alternatives to gain exposure to the

Indonesian coal industry, in our view.

Jul-Aug 2008 Interim earnings announcement We forecast stronger qoq earnings as 2Q2008 results should reflect higher

thermal coal spot prices. We expect management to provide guidance on

FY2008 realized contract prices.

Source: Bloomberg, Company data, Goldman Sachs Research estimates.

The prices in the body of this report are based on the market close of June 13, 2008.

Stronger, longer upcycle drives next leg of outperformance

The rally in the regional thermal coal spot prices has boosted the performance of ASEAN

coal stocks over the past 12 months (+35%/+270% ytd and over the past 12 month). We

believe the price rally is justified given the positive regional thermal coal fundamentals.

We initiate coverage on the ASEAN coal sector with an attractive stance as we still see

room for outperformance. High crude price, robust demand for coal-fired power plants in

emerging markets and persistent supply-side constraints will continue to act as

cornerstones of spot price strength, underpinning the potential for a longer-and stronger

phase of supernormal profits for the ASEAN coal producers, in our view.

We expect emerging domestic demand—which is fast evolving into a key growth engine—

to constrain export growth as we believe underinvestment in exploration, infrastructure

and equipment over the past decade has hampered Indonesia’s ability to simultaneously

manage overwhelming exports and domestic demand. We believe rising pricing power in

both the export and domestic markets should also drive higher returns. Although the

producers need to combat cost inflation, we do not think that this will derail the path of

their earnings acceleration which is driven by rising contract prices. We believe regulatory

risks will continue to be a key concern, but adopt a more sanguine view on their impact on

incumbents such as Bumi Resources and Indo Tambangraya.

June 19, 2008 ASEAN: Metals & Mining: Coal

Goldman Sachs Global Investment Research 3

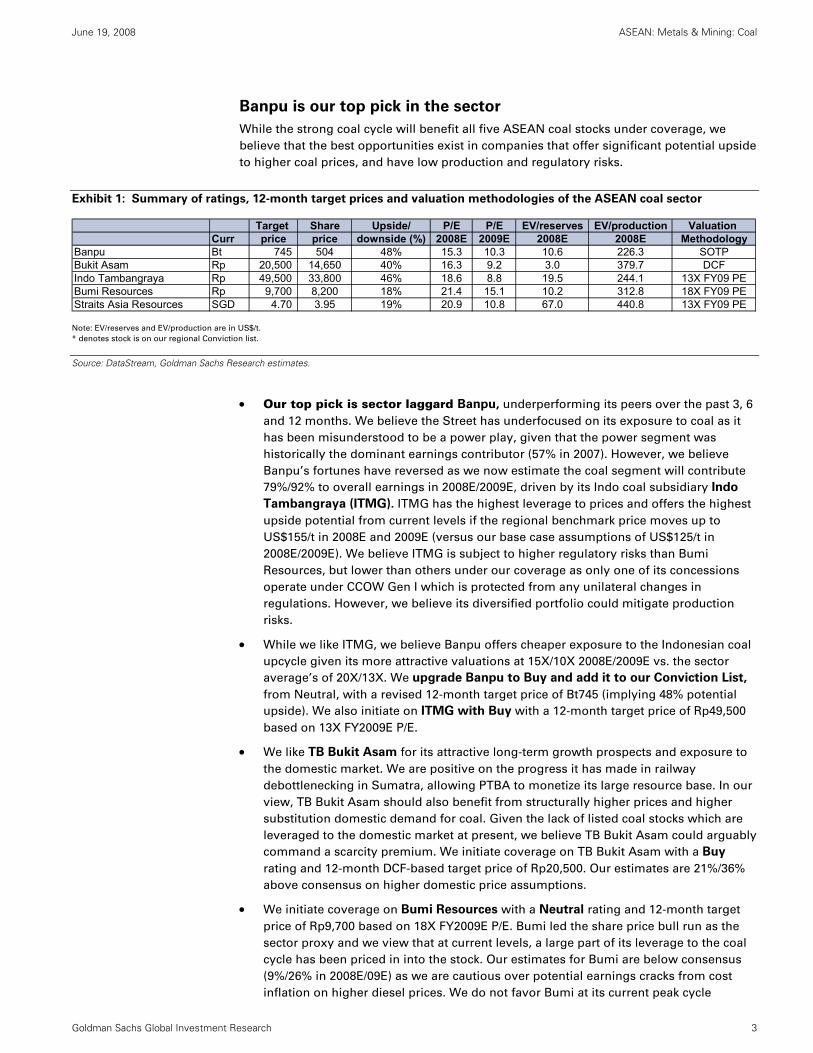

Banpu is our top pick in the sector

While the strong coal cycle will benefit all five ASEAN coal stocks under coverage, we

believe that the best opportunities exist in companies that offer significant potential upside

to higher coal prices, and have low production and regulatory risks.

Exhibit 1: Summary of ratings, 12-month target prices and valuation methodologies of the ASEAN coal sector

Target Share Upside/ P/E P/E EV/reserves EV/production Valuation Curr price price downside (%) 2008E 2009E 2008E 2008E Methodology

Banpu Bt 745 504 48% 15.3 10.3 10.6 226.3 SOTPBukit Asam Rp 20,500 14,650 40% 16.3 9.2 3.0 379.7 DCFIndo Tambangraya Rp 49,500 33,800 46% 18.6 8.8 19.5 244.1 13X FY09 PEBumi Resources Rp 9,700 8,200 18% 21.4 15.1 10.2 312.8 18X FY09 PEStraits Asia Resources SGD 4.70 3.95 19% 20.9 10.8 67.0 440.8 13X FY09 PE

Note: EV/reserves and EV/production are in US$/t.

* denotes stock is on our regional Conviction list.

Source: DataStream, Goldman Sachs Research estimates.

• Our top pick is sector laggard Banpu, underperforming its peers over the past 3, 6

and 12 months. We believe the Street has underfocused on its exposure to coal as it

has been misunderstood to be a power play, given that the power segment was

historically the dominant earnings contributor (57% in 2007). However, we believe

Banpu’s fortunes have reversed as we now estimate the coal segment will contribute

79%/92% to overall earnings in 2008E/2009E, driven by its Indo coal subsidiary Indo

Tambangraya (ITMG). ITMG has the highest leverage to prices and offers the highest

upside potential from current levels if the regional benchmark price moves up to

US$155/t in 2008E and 2009E (versus our base case assumptions of US$125/t in

2008E/2009E). We believe ITMG is subject to higher regulatory risks than Bumi

Resources, but lower than others under our coverage as only one of its concessions

operate under CCOW Gen I which is protected from any unilateral changes in

regulations. However, we believe its diversified portfolio could mitigate production

risks.

• While we like ITMG, we believe Banpu offers cheaper exposure to the Indonesian coal

upcycle given its more attractive valuations at 15X/10X 2008E/2009E vs. the sector

average’s of 20X/13X. We upgrade Banpu to Buy and add it to our Conviction List,

from Neutral, with a revised 12-month target price of Bt745 (implying 48% potential

upside). We also initiate on ITMG with Buy with a 12-month target price of Rp49,500

based on 13X FY2009E P/E.

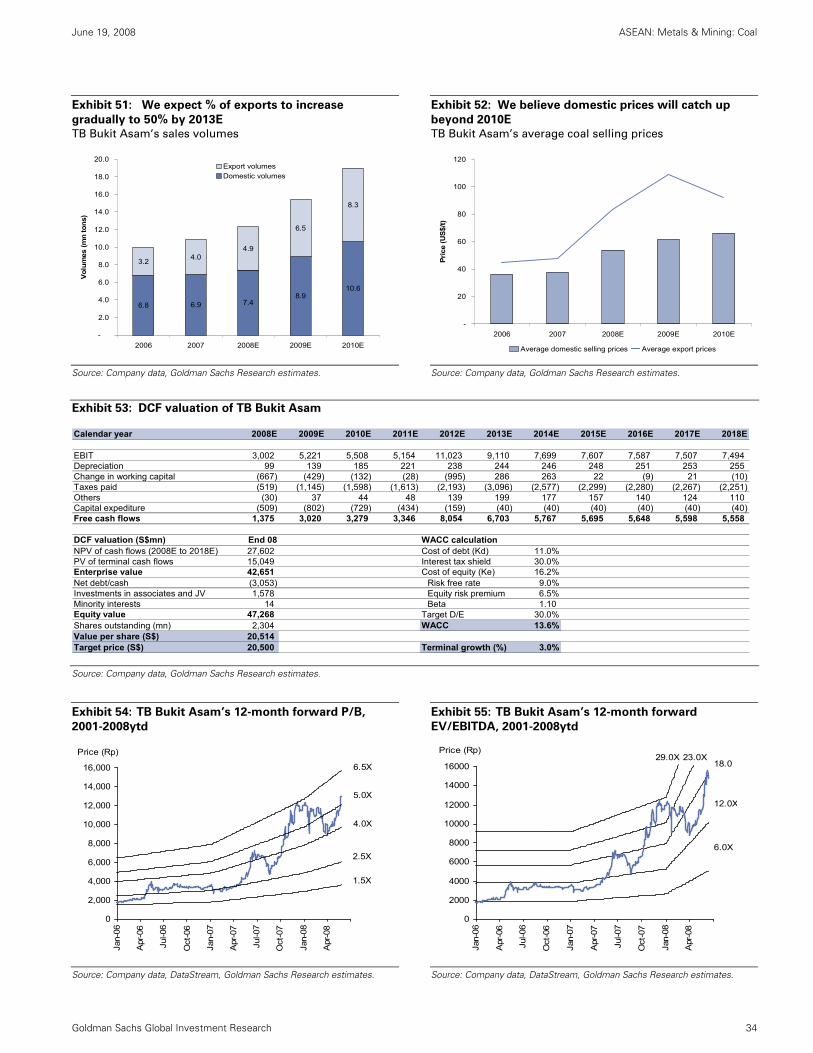

• We like TB Bukit Asam for its attractive long-term growth prospects and exposure to

the domestic market. We are positive on the progress it has made in railway

debottlenecking in Sumatra, allowing PTBA to monetize its large resource base. In our

view, TB Bukit Asam should also benefit from structurally higher prices and higher

substitution domestic demand for coal. Given the lack of listed coal stocks which are

leveraged to the domestic market at present, we believe TB Bukit Asam could arguably

command a scarcity premium. We initiate coverage on TB Bukit Asam with a Buy

rating and 12-month DCF-based target price of Rp20,500. Our estimates are 21%/36%

above consensus on higher domestic price assumptions.

• We initiate coverage on Bumi Resources with a Neutral rating and 12-month target

price of Rp9,700 based on 18X FY2009E P/E. Bumi led the share price bull run as the

sector proxy and we view that at current levels, a large part of its leverage to the coal

cycle has been priced in into the stock. Our estimates for Bumi are below consensus

(9%/26% in 2008E/09E) as we are cautious over potential earnings cracks from cost

inflation on higher diesel prices. We do not favor Bumi at its current peak cycle

June 19, 2008 ASEAN: Metals & Mining: Coal

Goldman Sachs Global Investment Research 4

valuation given better opportunities elsewhere. Nonetheless, we believe there will be

trading interest in Bumi as a traditional beneficiary leveraged to the Indonesian

thermal coal sector if spot prices continue to climb.

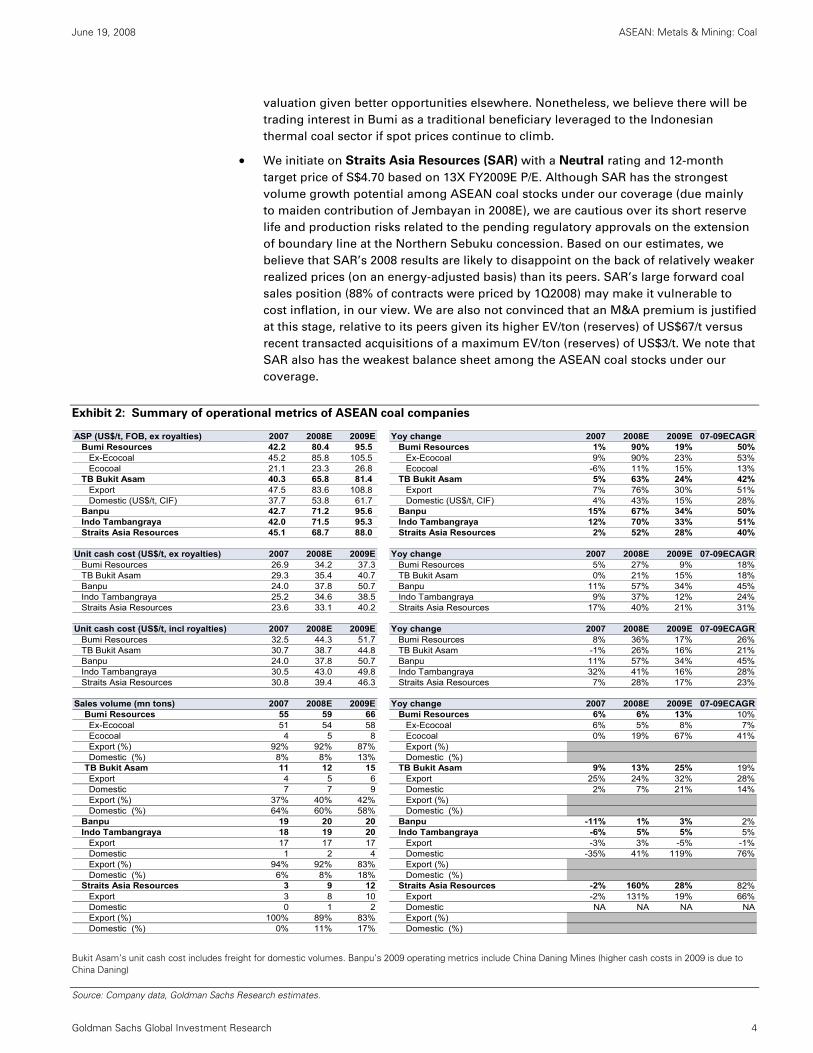

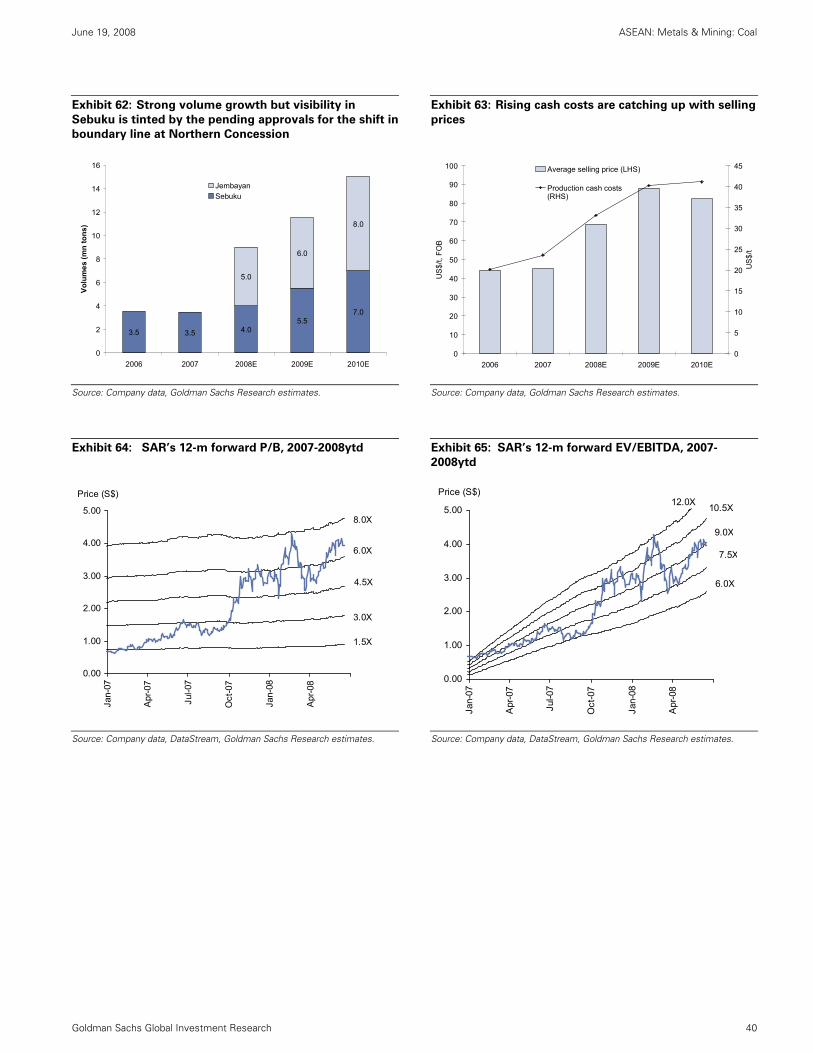

• We initiate on Straits Asia Resources (SAR) with a Neutral rating and 12-month

target price of S$4.70 based on 13X FY2009E P/E. Although SAR has the strongest

volume growth potential among ASEAN coal stocks under our coverage (due mainly

to maiden contribution of Jembayan in 2008E), we are cautious over its short reserve

life and production risks related to the pending regulatory approvals on the extension

of boundary line at the Northern Sebuku concession. Based on our estimates, we

believe that SAR’s 2008 results are likely to disappoint on the back of relatively weaker

realized prices (on an energy-adjusted basis) than its peers. SAR’s large forward coal

sales position (88% of contracts were priced by 1Q2008) may make it vulnerable to

cost inflation, in our view. We are also not convinced that an M&A premium is justified

at this stage, relative to its peers given its higher EV/ton (reserves) of US$67/t versus

recent transacted acquisitions of a maximum EV/ton (reserves) of US$3/t. We note that

SAR also has the weakest balance sheet among the ASEAN coal stocks under our

coverage.

Exhibit 2: Summary of operational metrics of ASEAN coal companies

ASP (US$/t, FOB, ex royalties) 2007 2008E 2009E Yoy change 2007 2008E 2009E 07-09ECAGRBumi Resources 42.2 80.4 95.5 Bumi Resources 1% 90% 19% 50%

Ex-Ecocoal 45.2 85.8 105.5 Ex-Ecocoal 9% 90% 23% 53%Ecocoal 21.1 23.3 26.8 Ecocoal -6% 11% 15% 13%

TB Bukit Asam 40.3 65.8 81.4 TB Bukit Asam 5% 63% 24% 42%Export 47.5 83.6 108.8 Export 7% 76% 30% 51%Domestic (US$/t, CIF) 37.7 53.8 61.7 Domestic (US$/t, CIF) 4% 43% 15% 28%

Banpu 42.7 71.2 95.6 Banpu 15% 67% 34% 50%Indo Tambangraya 42.0 71.5 95.3 Indo Tambangraya 12% 70% 33% 51%Straits Asia Resources 45.1 68.7 88.0 Straits Asia Resources 2% 52% 28% 40%

26.2 34.3 39.2 0.2 Unit cash cost (US$/t, ex royalties) 2007 2008E 2009E Yoy change 2007 2008E 2009E 07-09ECAGR

Bumi Resources 26.9 34.2 37.3 Bumi Resources 5% 27% 9% 18%TB Bukit Asam 29.3 35.4 40.7 TB Bukit Asam 0% 21% 15% 18%Banpu 24.0 37.8 50.7 Banpu 11% 57% 34% 45%Indo Tambangraya 25.2 34.6 38.5 Indo Tambangraya 9% 37% 12% 24%Straits Asia Resources 23.6 33.1 40.2 Straits Asia Resources 17% 40% 21% 31%

Unit cash cost (US$/t, incl royalties) 2007 2008E 2009E Yoy change 2007 2008E 2009E 07-09ECAGRBumi Resources 32.5 44.3 51.7 Bumi Resources 8% 36% 17% 26%TB Bukit Asam 30.7 38.7 44.8 TB Bukit Asam -1% 26% 16% 21%Banpu 24.0 37.8 50.7 Banpu 11% 57% 34% 45%Indo Tambangraya 30.5 43.0 49.8 Indo Tambangraya 32% 41% 16% 28%Straits Asia Resources 30.8 39.4 46.3 Straits Asia Resources 7% 28% 17% 23%

Sales volume (mn tons) 2007 2008E 2009E Yoy change 2007 2008E 2009E 07-09ECAGRBumi Resources 55 59 66 Bumi Resources 6% 6% 13% 10%Ex-Ecocoal 51 54 58 Ex-Ecocoal 6% 5% 8% 7%Ecocoal 4 5 8 Ecocoal 0% 19% 67% 41%Export (%) 92% 92% 87% Export (%)Domestic (%) 8% 8% 13% Domestic (%)

TB Bukit Asam 11 12 15 TB Bukit Asam 9% 13% 25% 19%Export 4 5 6 Export 25% 24% 32% 28%Domestic 7 7 9 Domestic 2% 7% 21% 14%Export (%) 37% 40% 42% Export (%)Domestic (%) 64% 60% 58% Domestic (%)

Banpu 19 20 20 Banpu -11% 1% 3% 2%Indo Tambangraya 18 19 20 Indo Tambangraya -6% 5% 5% 5%

Export 17 17 17 Export -3% 3% -5% -1%Domestic 1 2 4 Domestic -35% 41% 119% 76%Export (%) 94% 92% 83% Export (%)Domestic (%) 6% 8% 18% Domestic (%)

Straits Asia Resources 3 9 12 Straits Asia Resources -2% 160% 28% 82%Export 3 8 10 Export -2% 131% 19% 66%Domestic 0 1 2 Domestic NA NA NA NAExport (%) 100% 89% 83% Export (%)Domestic (%) 0% 11% 17% Domestic (%)

Bukit Asam’s unit cash cost includes freight for domestic volumes. Banpu’s 2009 operating metrics include China Daning Mines (higher cash costs in 2009 is due to China Daning)

Source: Company data, Goldman Sachs Research estimates.

June 19, 2008 ASEAN: Metals & Mining: Coal

Goldman Sachs Global Investment Research 5

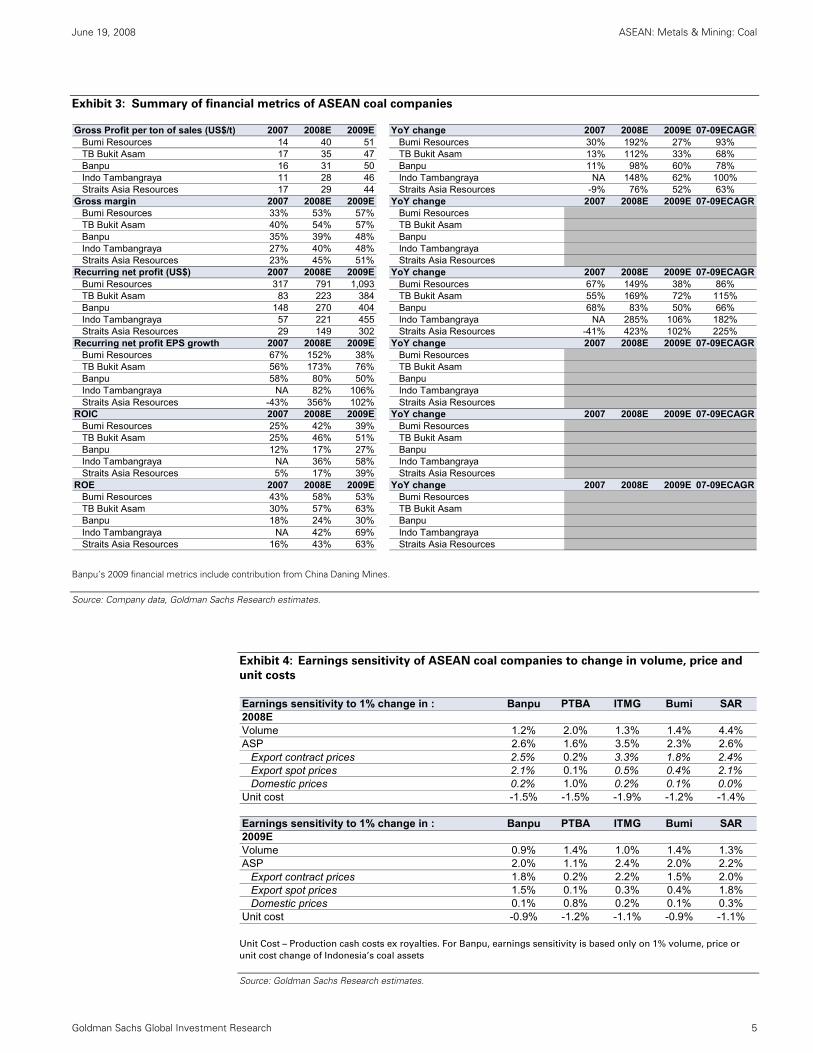

Exhibit 3: Summary of financial metrics of ASEAN coal companies

Gross Profit per ton of sales (US$/t) 2007 2008E 2009E YoY change 2007 2008E 2009E 07-09ECAGRBumi Resources 14 40 51 Bumi Resources 30% 192% 27% 93%TB Bukit Asam 17 35 47 TB Bukit Asam 13% 112% 33% 68%Banpu 16 31 50 Banpu 11% 98% 60% 78%Indo Tambangraya 11 28 46 Indo Tambangraya NA 148% 62% 100%Straits Asia Resources 17 29 44 Straits Asia Resources -9% 76% 52% 63%

Gross margin 2007 2008E 2009E YoY change 2007 2008E 2009E 07-09ECAGRBumi Resources 33% 53% 57% Bumi ResourcesTB Bukit Asam 40% 54% 57% TB Bukit AsamBanpu 35% 39% 48% BanpuIndo Tambangraya 27% 40% 48% Indo TambangrayaStraits Asia Resources 23% 45% 51% Straits Asia Resources

Recurring net profit (US$) 2007 2008E 2009E YoY change 2007 2008E 2009E 07-09ECAGRBumi Resources 317 791 1,093 Bumi Resources 67% 149% 38% 86%TB Bukit Asam 83 223 384 TB Bukit Asam 55% 169% 72% 115%Banpu 148 270 404 Banpu 68% 83% 50% 66%Indo Tambangraya 57 221 455 Indo Tambangraya NA 285% 106% 182%Straits Asia Resources 29 149 302 Straits Asia Resources -41% 423% 102% 225%

Recurring net profit EPS growth 2007 2008E 2009E YoY change 2007 2008E 2009E 07-09ECAGRBumi Resources 67% 152% 38% Bumi ResourcesTB Bukit Asam 56% 173% 76% TB Bukit AsamBanpu 58% 80% 50% BanpuIndo Tambangraya NA 82% 106% Indo TambangrayaStraits Asia Resources -43% 356% 102% Straits Asia Resources

ROIC 2007 2008E 2009E YoY change 2007 2008E 2009E 07-09ECAGRBumi Resources 25% 42% 39% Bumi ResourcesTB Bukit Asam 25% 46% 51% TB Bukit AsamBanpu 12% 17% 27% BanpuIndo Tambangraya NA 36% 58% Indo TambangrayaStraits Asia Resources 5% 17% 39% Straits Asia Resources

ROE 2007 2008E 2009E YoY change 2007 2008E 2009E 07-09ECAGRBumi Resources 43% 58% 53% Bumi ResourcesTB Bukit Asam 30% 57% 63% TB Bukit AsamBanpu 18% 24% 30% BanpuIndo Tambangraya NA 42% 69% Indo TambangrayaStraits Asia Resources 16% 43% 63% Straits Asia Resources

Banpu’s 2009 financial metrics include contribution from China Daning Mines.

Source: Company data, Goldman Sachs Research estimates.

Exhibit 4: Earnings sensitivity of ASEAN coal companies to change in volume, price and

unit costs

Earnings sensitivity to 1% change in : Banpu PTBA ITMG Bumi SAR2008EVolume 1.2% 2.0% 1.3% 1.4% 4.4%ASP 2.6% 1.6% 3.5% 2.3% 2.6%

Export contract prices 2.5% 0.2% 3.3% 1.8% 2.4%Export spot prices 2.1% 0.1% 0.5% 0.4% 2.1%Domestic prices 0.2% 1.0% 0.2% 0.1% 0.0%

Unit cost -1.5% -1.5% -1.9% -1.2% -1.4%

Earnings sensitivity to 1% change in : Banpu PTBA ITMG Bumi SAR2009EVolume 0.9% 1.4% 1.0% 1.4% 1.3%ASP 2.0% 1.1% 2.4% 2.0% 2.2%

Export contract prices 1.8% 0.2% 2.2% 1.5% 2.0%Export spot prices 1.5% 0.1% 0.3% 0.4% 1.8%Domestic prices 0.1% 0.8% 0.2% 0.1% 0.3%

Unit cost -0.9% -1.2% -1.1% -0.9% -1.1%

Unit Cost – Production cash costs ex royalties. For Banpu, earnings sensitivity is based only on 1% volume, price or

unit cost change of Indonesia’s coal assets

Source: Goldman Sachs Research estimates.

June 19, 2008 A

SEAN

: Metals &

Mining: C

oal

Goldm

an Sachs Global Investm

ent Research

6

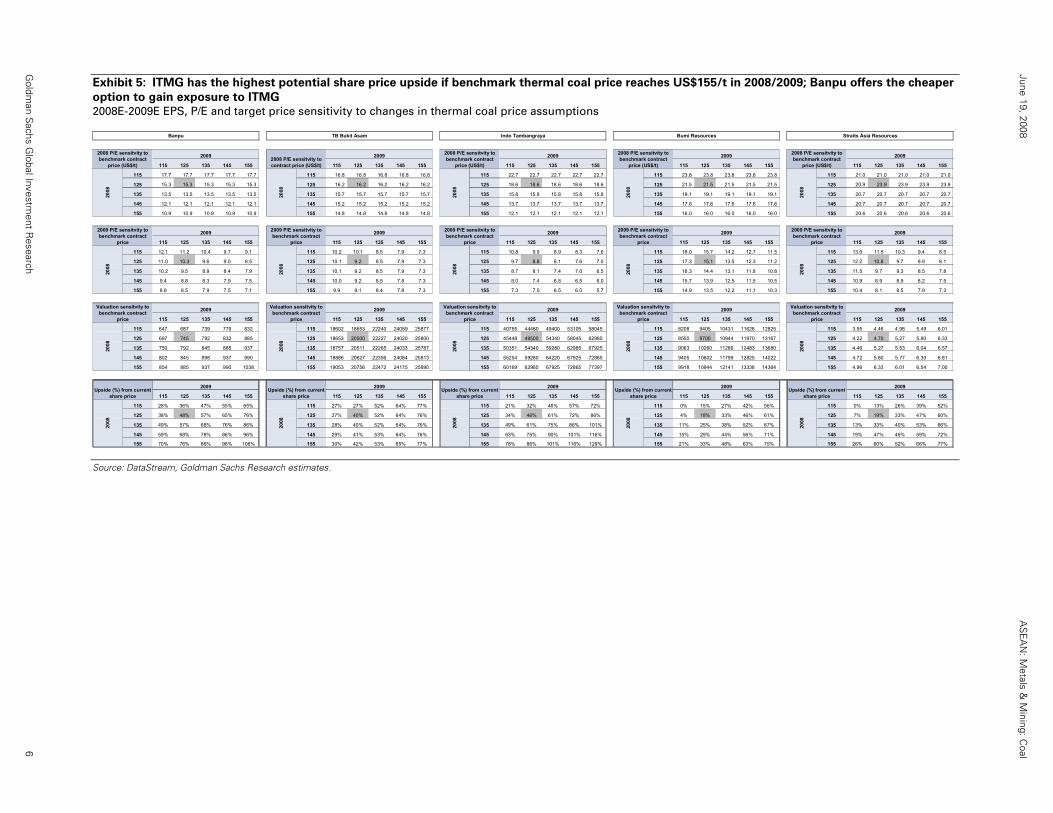

Exhibit 5: ITMG has the highest potential share price upside if benchmark thermal coal price reaches US$155/t in 2008/2009; Banpu offers the cheaper

option to gain exposure to ITMG

2008E-2009E EPS, P/E and target price sensitivity to changes in thermal coal price assumptions

2009 2009 2009 2009

115 125 135 145 155 115 125 135 145 155 115 125 135 145 155 115 125 135 145 155 115 125 135 145 155

115 17.7 17.7 17.7 17.7 17.7 115 16.8 16.8 16.8 16.8 16.8 115 22.7 22.7 22.7 22.7 22.7 115 23.8 23.8 23.8 23.8 23.8 115 21.0 21.0 21.0 21.0 21.0

125 15.3 15.3 15.3 15.3 15.3 125 16.2 16.2 16.2 16.2 16.2 125 18.6 18.6 18.6 18.6 18.6 125 21.5 21.5 21.5 21.5 21.5 125 20.9 23.9 23.9 23.9 23.9

135 13.5 13.5 13.5 13.5 13.5 135 15.7 15.7 15.7 15.7 15.7 135 15.8 15.8 15.8 15.8 15.8 135 19.1 19.1 19.1 19.1 19.1 135 20.7 20.7 20.7 20.7 20.7

145 12.1 12.1 12.1 12.1 12.1 145 15.2 15.2 15.2 15.2 15.2 145 13.7 13.7 13.7 13.7 13.7 145 17.6 17.6 17.6 17.6 17.6 145 20.7 20.7 20.7 20.7 20.7

155 10.9 10.9 10.9 10.9 10.9 155 14.8 14.8 14.8 14.8 14.8 155 12.1 12.1 12.1 12.1 12.1 155 16.0 16.0 16.0 16.0 16.0 155 20.6 20.6 20.6 20.6 20.6

2009 2009 2009 2009

115 125 135 145 155 115 125 135 145 155 115 125 135 145 155 115 125 135 145 155 115 125 135 145 155

115 12.1 11.2 10.4 9.7 9.1 115 10.2 10.1 8.5 7.9 7.3 115 10.8 9.9 8.9 8.3 7.6 115 18.0 15.7 14.2 12.7 11.5 115 13.0 11.5 10.3 9.4 8.5

125 11.0 10.3 9.6 9.0 8.5 125 10.1 9.2 8.5 7.9 7.3 125 9.7 8.8 8.1 7.6 7.0 125 17.3 15.1 13.5 12.3 11.2 125 12.2 10.8 9.7 8.9 8.1

135 10.2 9.5 8.9 8.4 7.9 135 10.1 9.2 8.5 7.9 7.3 135 8.7 8.1 7.4 7.0 6.5 135 16.3 14.4 13.1 11.8 10.8 135 11.5 9.7 9.3 8.5 7.8

145 9.4 8.8 8.3 7.9 7.5 145 10.0 9.2 8.5 7.8 7.3 145 8.0 7.4 6.8 6.5 6.0 145 15.7 13.9 12.5 11.5 10.5 145 10.9 8.9 8.9 8.2 7.5

155 8.8 8.5 7.9 7.5 7.1 155 9.9 9.1 8.4 7.8 7.3 155 7.3 7.0 6.5 6.0 5.7 155 14.9 13.5 12.2 11.1 10.3 155 10.4 8.1 8.5 7.9 7.3

2009 2009 2009 2009

115 125 135 145 155 115 125 135 145 155 115 125 135 145 155 115 125 135 145 155 115 125 135 145 155

115 647 687 739 779 832 115 18602 18653 22240 24059 25877 115 40755 44460 49400 53105 58045 115 8208 9405 10431 11628 12825 115 3.95 4.46 4.98 5.49 6.01

125 697 745 792 832 885 125 18653 20500 22227 24020 25800 125 45448 49500 54340 58045 62985 125 8550 9700 10944 11970 13167 125 4.22 4.70 5.27 5.80 6.33

135 750 792 845 885 937 135 18757 20511 22265 24033 25787 135 50351 54340 59280 62985 67925 135 9063 10260 11286 12483 13680 135 4.46 5.27 5.53 6.04 6.57

145 802 845 898 937 990 145 18886 20627 22356 24084 25813 145 55254 59280 64220 67925 72865 145 9405 10602 11799 12825 14022 145 4.72 5.80 5.77 6.30 6.81

155 854 885 937 990 1038 155 19053 20756 22472 24175 25890 155 60169 62985 67925 72865 77397 155 9918 10944 12141 13338 14364 155 4.96 6.33 6.01 6.54 7.00

2009 2009 2009 2009 2009

115 125 135 145 155 115 125 135 145 155 115 125 135 145 155 115 125 135 145 155 115 125 135 145 155

115 28% 36% 47% 55% 65% 115 27% 27% 52% 64% 77% 115 21% 32% 46% 57% 72% 115 0% 15% 27% 42% 56% 115 0% 13% 26% 39% 52%

125 38% 48% 57% 65% 76% 125 27% 40% 52% 64% 76% 125 34% 46% 61% 72% 86% 125 4% 18% 33% 46% 61% 125 7% 19% 33% 47% 60%

135 49% 57% 68% 76% 86% 135 28% 40% 52% 64% 76% 135 49% 61% 75% 86% 101% 135 11% 25% 38% 52% 67% 135 13% 33% 40% 53% 66%

145 59% 68% 78% 86% 96% 145 29% 41% 53% 64% 76% 145 63% 75% 90% 101% 116% 145 15% 29% 44% 56% 71% 145 19% 47% 46% 59% 72%

155 70% 76% 86% 96% 106% 155 30% 42% 53% 65% 77% 155 78% 86% 101% 116% 129% 155 21% 33% 48% 63% 75% 155 26% 60% 52% 66% 77%

Valuation sensitvity to benchmark contract

price

2008

Upside (%) from current share price

2008

Upside (%) from current share price

2008

Valuation sensitvity to benchmark contract

price

2008

Valuation sensitvity to benchmark contract

price

2008

Upside (%) from current share price

2008

Upside (%) from current share price

2008

Upside (%) from current share price

2008

2009 P/E sensitvity to benchmark contract

price

2008

Valuation sensitvity to benchmark contract

price

2008

Straits Asia Resources

2008

2008 P/E sensitvity to benchmark contract

price (US$/t)

2008

2009 2008 P/E sensitvity to benchmark contract

price (US$/t)

Bumi Resources

2009 P/E sensitvity to benchmark contract

price

2008

2008

2008 P/E sensitvity to benchmark contract

price (US$/t)

2008

2009 P/E sensitvity to benchmark contract

price

2008

Banpu

Valuation sensitvity to benchmark contract

price

2008 P/E sensitvity to benchmark contract

price (US$/t)

2008

TB Bukit Asam

2008 P/E sensitvity to contract price (US$/t)

2008

Indo Tambangraya

2009

2009

2009 P/E sensitvity to benchmark contract

price

2008

2008

2009 P/E sensitvity to benchmark contract

price

Source: DataStream, Goldman Sachs Research estimates.

June 19, 2008 ASEAN: Metals & Mining: Coal

Goldman Sachs Global Investment Research 7

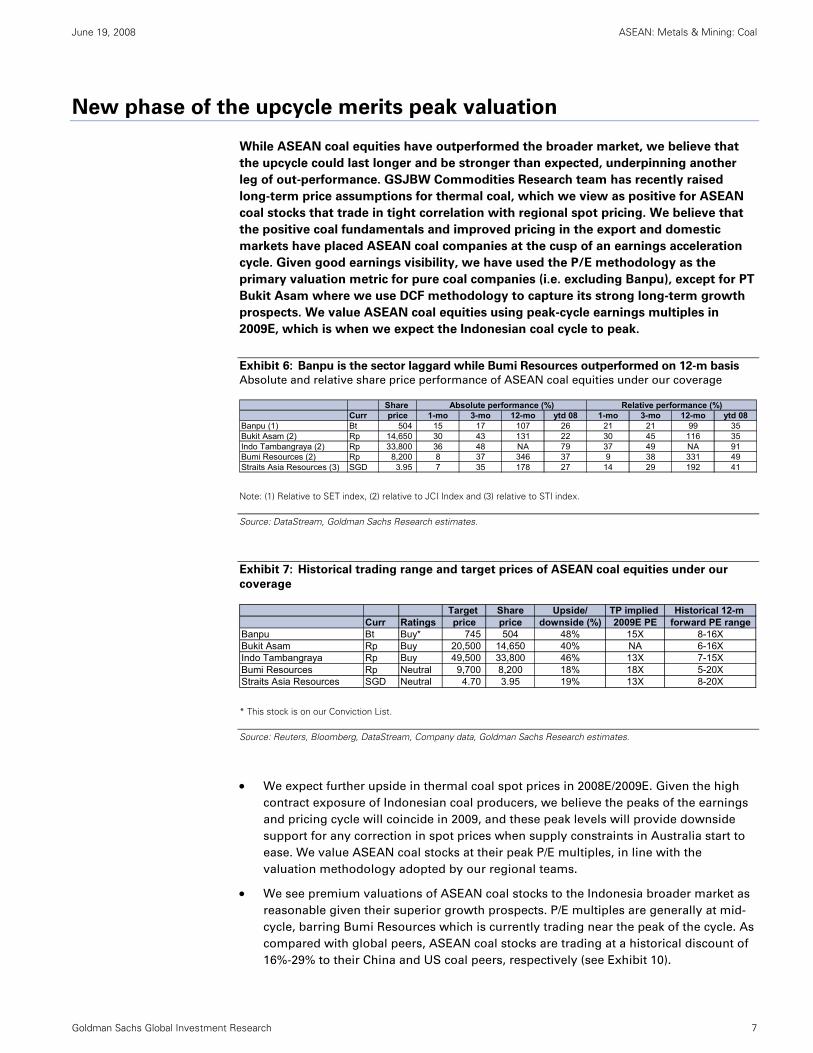

New phase of the upcycle merits peak valuation

While ASEAN coal equities have outperformed the broader market, we believe that

the upcycle could last longer and be stronger than expected, underpinning another

leg of out-performance. GSJBW Commodities Research team has recently raised

long-term price assumptions for thermal coal, which we view as positive for ASEAN

coal stocks that trade in tight correlation with regional spot pricing. We believe that

the positive coal fundamentals and improved pricing in the export and domestic

markets have placed ASEAN coal companies at the cusp of an earnings acceleration

cycle. Given good earnings visibility, we have used the P/E methodology as the

primary valuation metric for pure coal companies (i.e. excluding Banpu), except for PT

Bukit Asam where we use DCF methodology to capture its strong long-term growth

prospects. We value ASEAN coal equities using peak-cycle earnings multiples in

2009E, which is when we expect the Indonesian coal cycle to peak.

Exhibit 6: Banpu is the sector laggard while Bumi Resources outperformed on 12-m basis

Absolute and relative share price performance of ASEAN coal equities under our coverage

Share Curr price 1-mo 3-mo 12-mo ytd 08 1-mo 3-mo 12-mo ytd 08

Banpu (1) Bt 504 15 17 107 26 21 21 99 35Bukit Asam (2) Rp 14,650 30 43 131 22 30 45 116 35Indo Tambangraya (2) Rp 33,800 36 48 NA 79 37 49 NA 91Bumi Resources (2) Rp 8,200 8 37 346 37 9 38 331 49Straits Asia Resources (3) SGD 3.95 7 35 178 27 14 29 192 41

Absolute performance (%) Relative performance (%)

Note: (1) Relative to SET index, (2) relative to JCI Index and (3) relative to STI index.

Source: DataStream, Goldman Sachs Research estimates.

Exhibit 7: Historical trading range and target prices of ASEAN coal equities under our

coverage

Target Share Upside/ TP implied Historical 12-m Curr Ratings price price downside (%) 2009E PE forward PE range

Banpu Bt Buy* 745 504 48% 15X 8-16XBukit Asam Rp Buy 20,500 14,650 40% NA 6-16XIndo Tambangraya Rp Buy 49,500 33,800 46% 13X 7-15XBumi Resources Rp Neutral 9,700 8,200 18% 18X 5-20XStraits Asia Resources SGD Neutral 4.70 3.95 19% 13X 8-20X

* This stock is on our Conviction List.

Source: Reuters, Bloomberg, DataStream, Company data, Goldman Sachs Research estimates.

• We expect further upside in thermal coal spot prices in 2008E/2009E. Given the high

contract exposure of Indonesian coal producers, we believe the peaks of the earnings

and pricing cycle will coincide in 2009, and these peak levels will provide downside

support for any correction in spot prices when supply constraints in Australia start to

ease. We value ASEAN coal stocks at their peak P/E multiples, in line with the

valuation methodology adopted by our regional teams.

• We see premium valuations of ASEAN coal stocks to the Indonesia broader market as

reasonable given their superior growth prospects. P/E multiples are generally at mid-

cycle, barring Bumi Resources which is currently trading near the peak of the cycle. As

compared with global peers, ASEAN coal stocks are trading at a historical discount of

16%-29% to their China and US coal peers, respectively (see Exhibit 10).

June 19, 2008 ASEAN: Metals & Mining: Coal

Goldman Sachs Global Investment Research 8

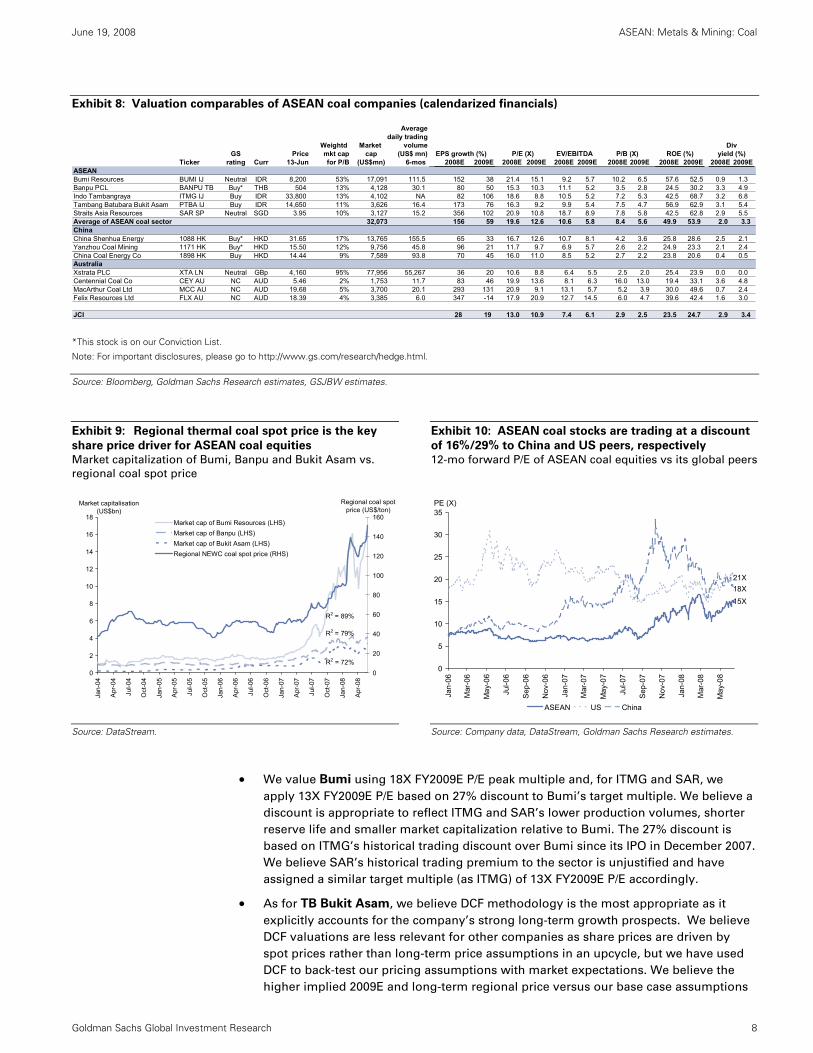

Exhibit 8: Valuation comparables of ASEAN coal companies (calendarized financials)

Averagedaily trading

Weightd Market volumeGS Price mkt cap cap (US$ mn) EPS growth (%)

Ticker rating Curr 13-Jun for P/B (US$mn) 6-mos 2008E 2009E 2008E 2009E 2008E 2009E 2008E 2009E 2008E 2009E 2008E 2009EASEANBumi Resources BUMI IJ Neutral IDR 8,200 53% 17,091 111.5 152 38 21.4 15.1 9.2 5.7 10.2 6.5 57.6 52.5 0.9 1.3Banpu PCL BANPU TB Buy* THB 504 13% 4,128 30.1 80 50 15.3 10.3 11.1 5.2 3.5 2.8 24.5 30.2 3.3 4.9Indo Tambangraya ITMG IJ Buy IDR 33,800 13% 4,102 NA 82 106 18.6 8.8 10.5 5.2 7.2 5.3 42.5 68.7 3.2 6.8Tambang Batubara Bukit Asam PTBA IJ Buy IDR 14,650 11% 3,626 16.4 173 76 16.3 9.2 9.9 5.4 7.5 4.7 56.9 62.9 3.1 5.4Straits Asia Resources SAR SP Neutral SGD 3.95 10% 3,127 15.2 356 102 20.9 10.8 18.7 8.9 7.8 5.8 42.5 62.8 2.9 5.5Average of ASEAN coal sector 32,073 156 59 19.6 12.6 10.6 5.8 8.4 5.6 49.9 53.9 2.0 3.3 ChinaChina Shenhua Energy 1088 HK Buy* HKD 31.65 17% 13,765 155.5 65 33 16.7 12.6 10.7 8.1 4.2 3.6 25.8 28.6 2.5 2.1Yanzhou Coal Mining 1171 HK Buy* HKD 15.50 12% 9,756 45.8 96 21 11.7 9.7 6.9 5.7 2.6 2.2 24.9 23.3 2.1 2.4China Coal Energy Co 1898 HK Buy HKD 14.44 9% 7,589 93.8 70 45 16.0 11.0 8.5 5.2 2.7 2.2 23.8 20.6 0.4 0.5AustraliaXstrata PLC XTA LN Neutral GBp 4,160 95% 77,956 55,267 36 20 10.6 8.8 6.4 5.5 2.5 2.0 25.4 23.9 0.0 0.0Centennial Coal Co CEY AU NC AUD 5.46 2% 1,753 11.7 83 46 19.9 13.6 8.1 6.3 16.0 13.0 19.4 33.1 3.6 4.8MacArthur Coal Ltd MCC AU NC AUD 19.68 5% 3,700 20.1 293 131 20.9 9.1 13.1 5.7 5.2 3.9 30.0 49.6 0.7 2.4Felix Resources Ltd FLX AU NC AUD 18.39 4% 3,385 6.0 347 -14 17.9 20.9 12.7 14.5 6.0 4.7 39.6 42.4 1.6 3.0

JCI 28 19 13.0 10.9 7.4 6.1 2.9 2.5 23.5 24.7 2.9 3.4

ROE (%) yield (%)Div

P/E (X) P/B (X) EV/EBITDA

*This stock is on our Conviction List.

Note: For important disclosures, please go to http://www.gs.com/research/hedge.html.

Source: Bloomberg, Goldman Sachs Research estimates, GSJBW estimates.

Exhibit 9: Regional thermal coal spot price is the key

share price driver for ASEAN coal equities

Market capitalization of Bumi, Banpu and Bukit Asam vs.

regional coal spot price

Exhibit 10: ASEAN coal stocks are trading at a discount

of 16%/29% to China and US peers, respectively

12-mo forward P/E of ASEAN coal equities vs its global peers

0

2

4

6

8

10

12

14

16

18

Jan-

04

Apr

-04

Jul-0

4

Oct

-04

Jan-

05

Apr

-05

Jul-0

5

Oct

-05

Jan-

06

Apr

-06

Jul-0

6

Oct

-06

Jan-

07

Apr

-07

Jul-0

7

Oct

-07

Jan-

08

Apr

-08

Market capitalisation (US$bn)

0

20

40

60

80

100

120

140

160

Regional coal spot price (US$/ton)

Market cap of Bumi Resources (LHS) Market cap of Banpu (LHS)Market cap of Bukit Asam (LHS)Regional NEWC coal spot price (RHS)

R2 = 89%

R2 = 79%

R2 = 72%

0

5

10

15

20

25

30

35

Jan-

06

Mar

-06

May

-06

Jul-0

6

Sep

-06

Nov

-06

Jan-

07

Mar

-07

May

-07

Jul-0

7

Sep

-07

Nov

-07

Jan-

08

Mar

-08

May

-08

PE (X)

ASEAN US China

15X

21X18X

Source: DataStream.

Source: Company data, DataStream, Goldman Sachs Research estimates.

• We value Bumi using 18X FY2009E P/E peak multiple and, for ITMG and SAR, we

apply 13X FY2009E P/E based on 27% discount to Bumi’s target multiple. We believe a

discount is appropriate to reflect ITMG and SAR’s lower production volumes, shorter

reserve life and smaller market capitalization relative to Bumi. The 27% discount is

based on ITMG’s historical trading discount over Bumi since its IPO in December 2007.

We believe SAR’s historical trading premium to the sector is unjustified and have

assigned a similar target multiple (as ITMG) of 13X FY2009E P/E accordingly.

• As for TB Bukit Asam, we believe DCF methodology is the most appropriate as it

explicitly accounts for the company’s strong long-term growth prospects. We believe

DCF valuations are less relevant for other companies as share prices are driven by

spot prices rather than long-term price assumptions in an upcycle, but we have used

DCF to back-test our pricing assumptions with market expectations. We believe the

higher implied 2009E and long-term regional price versus our base case assumptions

June 19, 2008 ASEAN: Metals & Mining: Coal

Goldman Sachs Global Investment Research 9

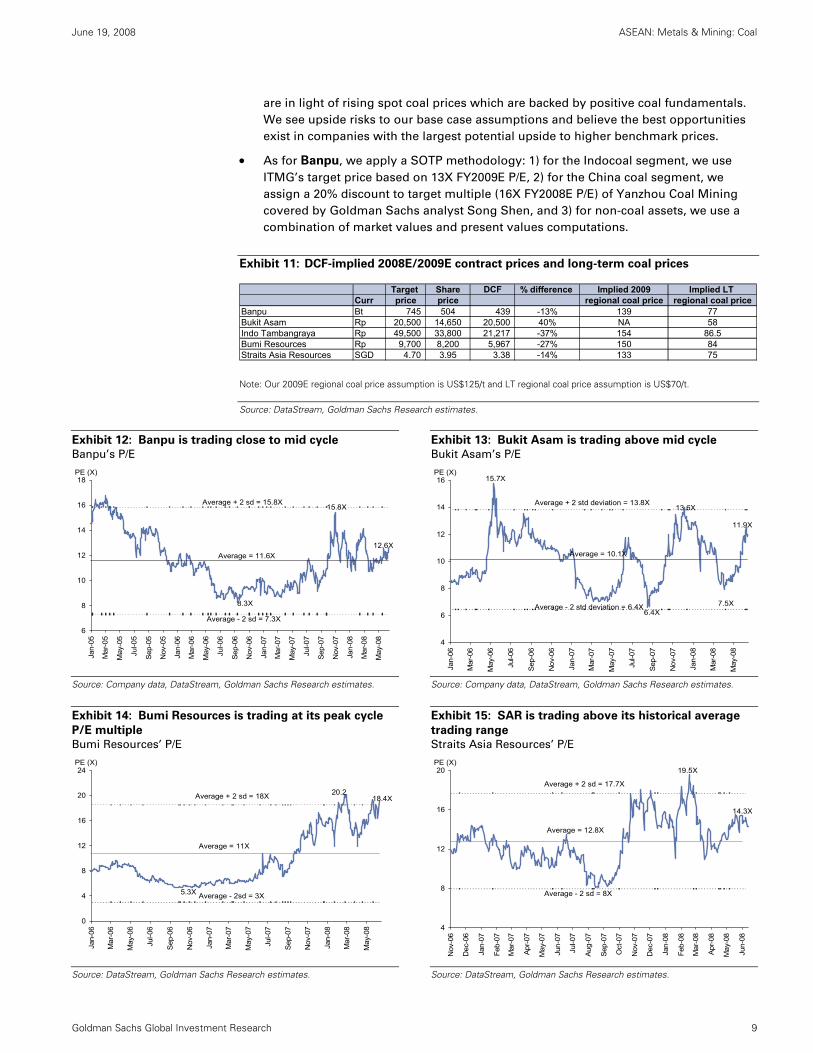

are in light of rising spot coal prices which are backed by positive coal fundamentals.

We see upside risks to our base case assumptions and believe the best opportunities

exist in companies with the largest potential upside to higher benchmark prices.

• As for Banpu, we apply a SOTP methodology: 1) for the Indocoal segment, we use

ITMG’s target price based on 13X FY2009E P/E, 2) for the China coal segment, we

assign a 20% discount to target multiple (16X FY2008E P/E) of Yanzhou Coal Mining

covered by Goldman Sachs analyst Song Shen, and 3) for non-coal assets, we use a

combination of market values and present values computations.

Exhibit 11: DCF-implied 2008E/2009E contract prices and long-term coal prices

Target Share DCF % difference Implied 2009 Implied LT Curr price price regional coal price regional coal price

Banpu Bt 745 504 439 -13% 139 77Bukit Asam Rp 20,500 14,650 20,500 40% NA 58Indo Tambangraya Rp 49,500 33,800 21,217 -37% 154 86.5Bumi Resources Rp 9,700 8,200 5,967 -27% 150 84Straits Asia Resources SGD 4.70 3.95 3.38 -14% 133 75

Note: Our 2009E regional coal price assumption is US$125/t and LT regional coal price assumption is US$70/t.

Source: DataStream, Goldman Sachs Research estimates.

Exhibit 12: Banpu is trading close to mid cycle

Banpu’s P/E

Exhibit 13: Bukit Asam is trading above mid cycle

Bukit Asam’s P/E

6

8

10

12

14

16

18

Jan-

05

Mar

-05

May

-05

Jul-0

5

Sep-

05

Nov

-05

Jan-

06

Mar

-06

May

-06

Jul-0

6

Sep-

06

Nov

-06

Jan-

07

Mar

-07

May

-07

Jul-0

7

Sep-

07

Nov

-07

Jan-

08

Mar

-08

May

-08

PE (X)

12.6X

15.8X

8.3X

Average = 11.6X

Average - 2 sd = 7.3X

Average + 2 sd = 15.8X

4

6

8

10

12

14

16

Jan-

06

Mar

-06

May

-06

Jul-0

6

Sep-

06

Nov

-06

Jan-

07

Mar

-07

May

-07

Jul-0

7

Sep-

07

Nov

-07

Jan-

08

Mar

-08

May

-08

PE (X)

11.9X

6.4X

15.7X

13.6X

7.5X

Average = 10.1X

Average + 2 std deviation = 13.8X

Average - 2 std deviation = 6.4X

Source: Company data, DataStream, Goldman Sachs Research estimates. Source: Company data, DataStream, Goldman Sachs Research estimates.

Exhibit 14: Bumi Resources is trading at its peak cycle

P/E multiple

Bumi Resources’ P/E

Exhibit 15: SAR is trading above its historical average

trading range

Straits Asia Resources’ P/E

0

4

8

12

16

20

24

Jan-

06

Mar

-06

May

-06

Jul-0

6

Sep

-06

Nov

-06

Jan-

07

Mar

-07

May

-07

Jul-0

7

Sep

-07

Nov

-07

Jan-

08

Mar

-08

May

-08

PE (X)

5.3X

20.218.4X

Average = 11X

Average + 2 sd = 18X

Average - 2sd = 3X

4

8

12

16

20

Nov

-06

Dec

-06

Jan-

07

Feb-

07

Mar

-07

Apr-0

7

May

-07

Jun-

07

Jul-0

7

Aug-

07

Sep-

07

Oct

-07

Nov

-07

Dec

-07

Jan-

08

Feb-

08

Mar

-08

Apr-0

8

May

-08

Jun-

08

PE (X)19.5X

14.3X

Average = 12.8X

Average + 2 sd = 17.7X

Average - 2 sd = 8X

Source: DataStream, Goldman Sachs Research estimates. Source: DataStream, Goldman Sachs Research estimates.

June 19, 2008 ASEAN: Metals & Mining: Coal

Goldman Sachs Global Investment Research 10

Exhibit 16: Bumi Resources is trading at a premium to peers and market, offering a

relatively attractive opportunity for smaller companies such as ITMG, Bukit Asam to catch

up

ASEAN coal equities’ PE premium/(discount) to MSCI

-60%

-40%

-20%

0%

20%

40%

60%

May

-07

Jun-

07

Jul-0

7

Aug

-07

Sep

-07

Oct

-07

Nov

-07

Dec

-07

Jan-

08

Feb-

08

Mar

-08

Apr-0

8

May

-08

Bumi ResourcesBukit AsamIndo TambangrayaStraits Asia ResourcesBanpu

5%

40%

9%

-9%

-3%

Note: We use MSCI Indonesia for Bumi Resources, Bukit Asam and Indo Tambangraya, MSCI Thailand for Banpu and MSCI Singapore for Straits Asia Resources.

Source: DataStream, Goldman Sachs Research estimates.

Solid fundamentals continue to drive prices; we expect further upside to thermal coal cycle

Risk/reward for the regional thermal coal market remains on the upside in our view

as the pricing upcycle is supported by: confluence of strong demand drivers and

incessant supply side risks, relative attractiveness of coal to crude oil on a heat

equivalent basis, and higher long-term thermal coal prices driven by elevated

marginal costs of production.

Crude oil price upside will drive coal price higher

Against the backdrop of an uncertain long-term supply environment arising from “the

revenge of the oil political economy” and continued robust demand growth from BRICs,

our GS Global Commodities Research team (refer to Goldman Sachs Energy Watch report

A lesson from long-dated oil: A steadily rising price forecast, dated May 16, 2008) believes

that the current oil market is experiencing a structural repricing with long-dated oil prices

driving the market until a new equilibrium is attained. The team believes that WTI crude

will come in 14% above current levels at US$141/bbl in 2H2008, US$148 bn for full year

2009 and long-term oil price of US$75/bbl.

As oil prices advance, coal prices should catch up. Although coal prices are at a

historical high level, coal is still cheaper than oil on a heat equivalent basis. And if

crude oil reaches the GS projected “super spike” level of US$200/bbl, the ratio drops

to a trough level of 17%.

June 19, 2008 ASEAN: Metals & Mining: Coal

Goldman Sachs Global Investment Research 11

Exhibit 17: Regional coal spot price is at a new high of

US$160/t (+79% ytd) but has lagged oil over the past 10

years

WTI Crude oil price vs. regional coal spot and contract prices

Exhibit 18: Thermal coal prices are still undervalued at

25% of oil prices, below historical average of 26% and

February’s high of 30% on a heat equivalent basis

Regional coal price (NEWC Index) as % of Brent oil (FOB) on

heat-equivalent basis

0

20

40

60

80

100

120

140

160

Aug

-95

Mar

-96

Oct

-96

May

-97

Dec

-97

Jul-9

8

Feb-

99

Sep

-99

Apr

-00

Nov

-00

Jun-

01

Jan-

02

Aug

-02

Mar

-03

Oct

-03

May

-04

Dec

-04

Jul-0

5

Feb-

06

Sep

-06

Apr

-07

Nov

-07

Jun-

08

US$/bbl

0

20

40

60

80

100

120

140

160

180

US$/ton

WTI crude oil price (LHS)

Regional NEWC coal spot price (RHS)

Australia/Japanese coal contract price(RHS)

37%

15%

34%

51%

15%

17%

14% 14%17%

30%

25%

Average = 26%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

55%

May

-96

Nov

-96

May

-97

Nov

-97

May

-98

Nov

-98

May

-99

Nov

-99

May

-00

Nov

-00

May

-01

Nov

-01

May

-02

Nov

-02

May

-03

Nov

-03

May

-04

Nov

-04

May

-05

Nov

-05

May

-06

Nov

-06

May

-07

Nov

-07

May

-08

CurrentOil: $132/bblCoal: $160/t

Oil: $36/bblCoal: $63/t

Oil: $17/bblCoal: $28/t

Oil: $35/bblCoal: $25/t

Oil: $38/bblCoal: $26/t

Oil: $88/bblCoal: $125/t

Oil: $59/bblCoal: $39/t

Oil: $10/bblCoal: $23/t

17% nowIf Oil = $200/bbl

24% nowIf Oil = $141/bbl

Source: Globalcoal, DataStream, GSJBW Research estimates.

Source: Goldman Sachs Commodity Research estimates, GSJBW Research estimates.

Exhibit 19: Our thermal coal contract price and WTI crude oil forecasts

2008E 2009E 2010E 2011E 2012E 2013NThermal coal contract prices (US$/ton) 125 125 100 90 90 70WTI crude oil prices (US$/bbl) 125 148YoY change in thermal coal (%) 0% -20% -10% 0%YoY change in WTI crude oil (%) 18%

Source: Goldman Sachs Commodities research and GSJBWere research estimates.

Demand and supply-led upcycle underpins the perfect storm in medium term

The current bull run in thermal coal cycle is largely attributed to the remarkably tight

market as a consequence of the confluence of strong demand momentum, driven by rapid

upsurge in coal-fired power generation capacity expansion in Asia (China, India, Indonesia,

Malaysia, etc) and supply side constraints (see Exhibit 23) such as logistical bottlenecks in

Australia, South Africa and China.

We see India and China as key drivers of seaborne thermal coal demand over the next 10-

20 years as both countries will account for 80% of the growth in coal related energy

demand growth, according to IEA. On the back of robust market demand, the tight energy

market is exceptionally sensitive to any supply disruptions (eg, news on delays to coal

infrastructure investment in Australia and/or a sharper-than-expected slowdown in

Indonesian and Colombia coal export growth) which presents key upside risks to our

medium-term price outlook for thermal coal. We believe that the delicate demand-supply

model of thermal coal is likely to persist till 2010E/2011E when rail or port expansions in

NSW (Australia) are expected to significantly add to export supply and when South African

coal export resumes following an inventory rebuilding programme by Eskom by 2011.

June 19, 2008 ASEAN: Metals & Mining: Coal

Goldman Sachs Global Investment Research 12

Exhibit 20: Global thermal coal imports likely to grow at

least 3% pa in line with consumption growth

% yoy changes in global thermal coal consumption and

seaborne trade

Exhibit 21: Supply constraints in most exporting

countries are unlikely to alleviate; Indonesia (the largest

exporter) should benefit in a big way, in our view

Major exporters and importers of thermal coal

-5%

0%

5%

10%

15%

20%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2008-2012

YoY changes in global consumptionYoY changes in seaborne thermal trade

-800

-600

-400

-200

0

200

400

600

800

2006 2007 2008E 2012E

Indonesia

Colombia

USA

Australia

S. AfricaRussiaChina

VietnamExports

Imports

Maj

or e

xpor

ters

Others

India

Europe

MalaysiaChina

S. Korea

Japan

Taiwan

Maj

or im

porte

rs

mn tons

Source: IEA, Clarkson Research studies, McCloskey’s, TEX report, ABARE, GSJBW Research estimates.

Source: IEA, Clarkson Research studies, McCloskey’s, TEX report, ABARE, GSJBW Research estimates.

Exhibit 22: Regional thermal coal imports driven by India and China

Major importers of seaborne thermal coal (mn tons)

Major Coal Importers 2003 2004 2005 2006 2007 2008E 2012EJapan 101 109 112 119 122 122 130India 12 14 20 24 29 34 55S. Korea 51 54 56 60 65 70 82Taiwan 45 48 53 58 61 63 74China 8 12 19 33 44 50 65Malaysia 8 10 10 11 13 15 20Other Asia 22 21 22 27 33 33 48Total Asia Imports 247 268 292 332 367 391 474YoY change (%) 6% 9% 9% 14% 11% 7%Total global imports 453 475 493 635 673 699 790 YoY change (%) 11% 5% 4% 29% 6% 4%

YoY growth rate of key import marketsJapan 5% 8% 3% 6% 3% 0% 1%India 20% 17% 43% 20% 21% 17% 10%S. Korea 2% 6% 4% 7% 8% 8% 3%Taiwan 7% 7% 10% 9% 5% 3% 3%China -20% 50% 58% 74% 33% 14% 5%

Source: IEA, Clarkson Research studies, McCloskey’s, TEX report, ABARE, GSJBW Research estimates.

June 19, 2008 ASEAN: Metals & Mining: Coal

Goldman Sachs Global Investment Research 13

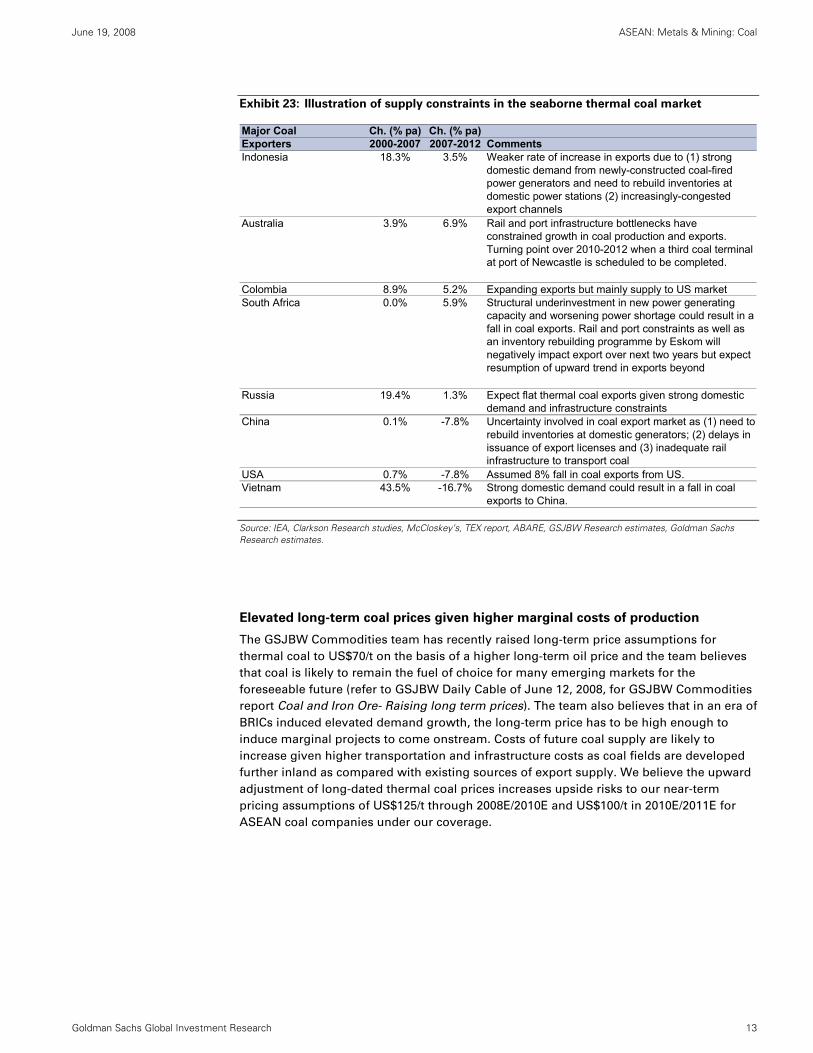

Exhibit 23: Illustration of supply constraints in the seaborne thermal coal market

Major Coal Ch. (% pa) Ch. (% pa)Exporters 2000-2007 2007-2012 CommentsIndonesia 18.3% 3.5% Weaker rate of increase in exports due to (1) strong

domestic demand from newly-constructed coal-fired power generators and need to rebuild inventories at domestic power stations (2) increasingly-congested export channels

Australia 3.9% 6.9% Rail and port infrastructure bottlenecks have constrained growth in coal production and exports. Turning point over 2010-2012 when a third coal terminal at port of Newcastle is scheduled to be completed.

Colombia 8.9% 5.2% Expanding exports but mainly supply to US marketSouth Africa 0.0% 5.9% Structural underinvestment in new power generating

capacity and worsening power shortage could result in a fall in coal exports. Rail and port constraints as well as an inventory rebuilding programme by Eskom will negatively impact export over next two years but expect resumption of upward trend in exports beyond

Russia 19.4% 1.3% Expect flat thermal coal exports given strong domestic demand and infrastructure constraints

China 0.1% -7.8% Uncertainty involved in coal export market as (1) need to rebuild inventories at domestic generators; (2) delays in issuance of export licenses and (3) inadequate rail infrastructure to transport coal

USA 0.7% -7.8% Assumed 8% fall in coal exports from US. Vietnam 43.5% -16.7% Strong domestic demand could result in a fall in coal

exports to China.

Source: IEA, Clarkson Research studies, McCloskey’s, TEX report, ABARE, GSJBW Research estimates, Goldman Sachs Research estimates.

Elevated long-term coal prices given higher marginal costs of production

The GSJBW Commodities team has recently raised long-term price assumptions for

thermal coal to US$70/t on the basis of a higher long-term oil price and the team believes

that coal is likely to remain the fuel of choice for many emerging markets for the

foreseeable future (refer to GSJBW Daily Cable of June 12, 2008, for GSJBW Commodities

report Coal and Iron Ore- Raising long term prices). The team also believes that in an era of

BRICs induced elevated demand growth, the long-term price has to be high enough to

induce marginal projects to come onstream. Costs of future coal supply are likely to

increase given higher transportation and infrastructure costs as coal fields are developed

further inland as compared with existing sources of export supply. We believe the upward

adjustment of long-dated thermal coal prices increases upside risks to our near-term

pricing assumptions of US$125/t through 2008E/2010E and US$100/t in 2010E/2011E for

ASEAN coal companies under our coverage.

June 19, 2008 ASEAN: Metals & Mining: Coal

Goldman Sachs Global Investment Research 14

Indonesian producers poised to benefit significantly as earnings momentum picks up

We believe the environment is conducive for a stronger and longer Indonesian

thermal coal cycle. Our constructive view of Indonesian thermal coal is predicated on

a positive view of the regional seaborne thermal coal sector as 74% of Indonesia’s

production is for the export markets. We believe incremental coal supply from

Indonesia is likely to be regimented on rising domestic demand, and infrastructure

and regulatory constraints, which add to support high regional thermal coal spot

prices. At the same time, we believe that prices of Indonesian coal are breaking out

from historical trends given rising negotiation power in the export market and strong

demand drivers in the domestic market. We believe that the stronger-than-expected

increase in realized prices will be more than sufficient to offset the elevated

production costs in line with higher diesel prices, bringing about significantly higher

returns in the industry. Regulatory risks remain a key concern but we adopt a more

sanguine view on export controls and actual impact of any regulatory changes

introduced by the new Mining Law on the existing big Indonesian coal producers.

Investment theme #1: Constrained export growth will keep regional prices up

Given the very tight thermal coal seaborne market, growth in Indonesian exports will be

critical in satisfying global import demand over the next few years. We believe a ramp-up

in export volumes is unlikely given underinvestment in exploration over the past few years,

infrastructure and equipment constraints and rising domestic demand. We estimate

Indonesian exports to witness a 6% CAGR over 2007-2010E from 167 mt to 199 mt in 2010E.

Regulatory uncertainty has discouraged large-scale greenfield exploration which is

essential to drive growth. Despite Indonesia’s rich resource base which presents

significant commercial opportunities to the global resource players, the less robust

regulatory framework has hampered prospects for major new investments. Although

small-scale projects have been awarded to existing industry players over the past few

years, they are unlikely to contribute to significant growth as substantial capital is required

for developments of new coal fields which are located further inland.

June 19, 2008 ASEAN: Metals & Mining: Coal

Goldman Sachs Global Investment Research 15

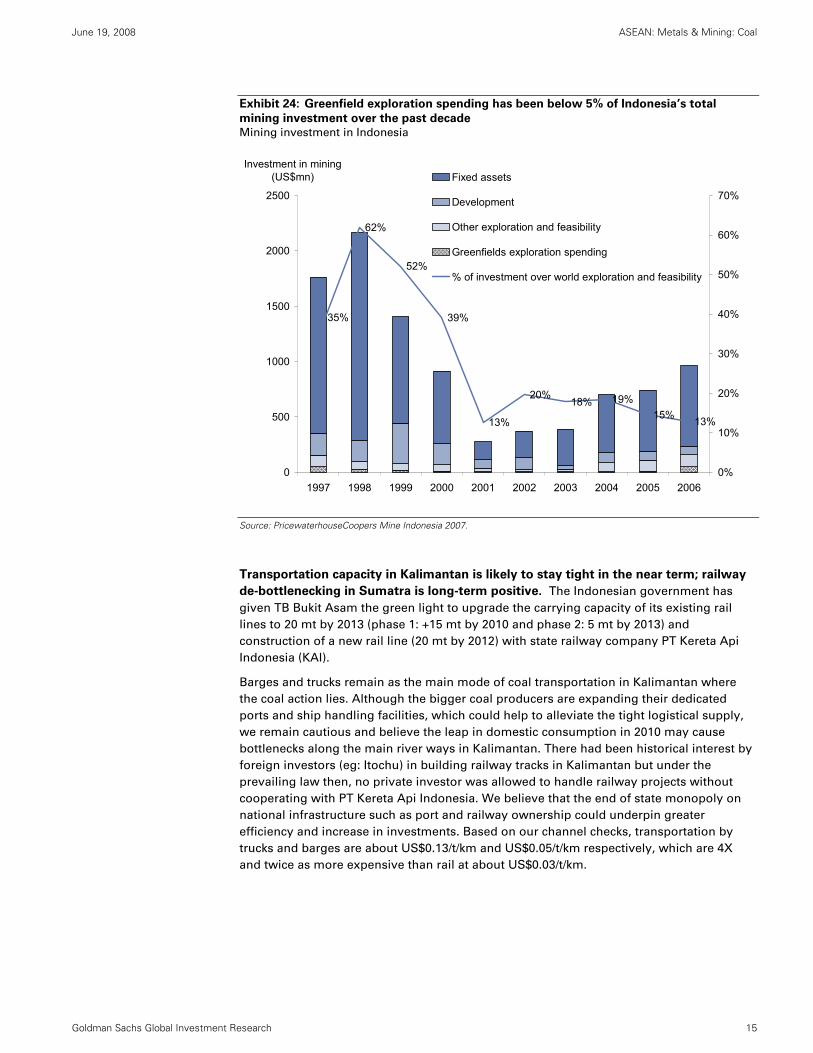

Exhibit 24: Greenfield exploration spending has been below 5% of Indonesia’s total

mining investment over the past decade

Mining investment in Indonesia

62%

52%

39%

13%

20%18% 19%

15% 13%

35%

0

500

1000

1500

2000

2500

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Investment in mining (US$mn)

0%

10%

20%

30%

40%

50%

60%

70%

Fixed assets

Development

Other exploration and feasibility

Greenfields exploration spending

% of investment over world exploration and feasibility

Source: PricewaterhouseCoopers Mine Indonesia 2007.

Transportation capacity in Kalimantan is likely to stay tight in the near term; railway

de-bottlenecking in Sumatra is long-term positive. The Indonesian government has

given TB Bukit Asam the green light to upgrade the carrying capacity of its existing rail

lines to 20 mt by 2013 (phase 1: +15 mt by 2010 and phase 2: 5 mt by 2013) and

construction of a new rail line (20 mt by 2012) with state railway company PT Kereta Api

Indonesia (KAI).

Barges and trucks remain as the main mode of coal transportation in Kalimantan where

the coal action lies. Although the bigger coal producers are expanding their dedicated

ports and ship handling facilities, which could help to alleviate the tight logistical supply,

we remain cautious and believe the leap in domestic consumption in 2010 may cause

bottlenecks along the main river ways in Kalimantan. There had been historical interest by

foreign investors (eg: Itochu) in building railway tracks in Kalimantan but under the

prevailing law then, no private investor was allowed to handle railway projects without

cooperating with PT Kereta Api Indonesia. We believe that the end of state monopoly on

national infrastructure such as port and railway ownership could underpin greater

efficiency and increase in investments. Based on our channel checks, transportation by

trucks and barges are about US$0.13/t/km and US$0.05/t/km respectively, which are 4X

and twice as more expensive than rail at about US$0.03/t/km.

June 19, 2008 ASEAN: Metals & Mining: Coal

Goldman Sachs Global Investment Research 16

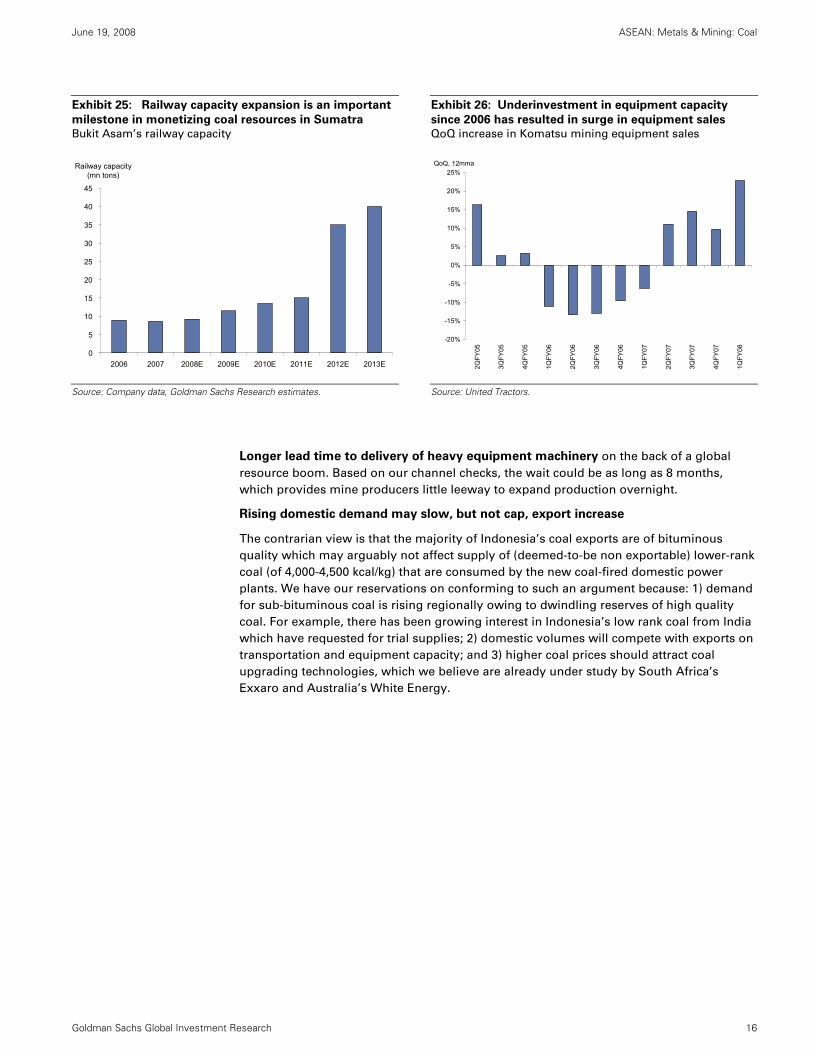

Exhibit 25: Railway capacity expansion is an important

milestone in monetizing coal resources in Sumatra

Bukit Asam’s railway capacity

Exhibit 26: Underinvestment in equipment capacity

since 2006 has resulted in surge in equipment sales

QoQ increase in Komatsu mining equipment sales

0

5

10

15

20

25

30

35

40

45

2006 2007 2008E 2009E 2010E 2011E 2012E 2013E

Railway capacity (mn tons)

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

2QFY

05

3QFY

05

4QFY

05

1QFY

06

2QFY

06

3QFY

06

4QFY

06

1QFY

07

2QFY

07

3QFY

07

4QFY

07

1QFY

08

QoQ, 12mma

Source: Company data, Goldman Sachs Research estimates.

Source: United Tractors.

Longer lead time to delivery of heavy equipment machinery on the back of a global

resource boom. Based on our channel checks, the wait could be as long as 8 months,

which provides mine producers little leeway to expand production overnight.

Rising domestic demand may slow, but not cap, export increase

The contrarian view is that the majority of Indonesia’s coal exports are of bituminous

quality which may arguably not affect supply of (deemed-to-be non exportable) lower-rank

coal (of 4,000-4,500 kcal/kg) that are consumed by the new coal-fired domestic power

plants. We have our reservations on conforming to such an argument because: 1) demand

for sub-bituminous coal is rising regionally owing to dwindling reserves of high quality

coal. For example, there has been growing interest in Indonesia’s low rank coal from India

which have requested for trial supplies; 2) domestic volumes will compete with exports on

transportation and equipment capacity; and 3) higher coal prices should attract coal

upgrading technologies, which we believe are already under study by South Africa’s

Exxaro and Australia’s White Energy.

June 19, 2008 ASEAN: Metals & Mining: Coal

Goldman Sachs Global Investment Research 17

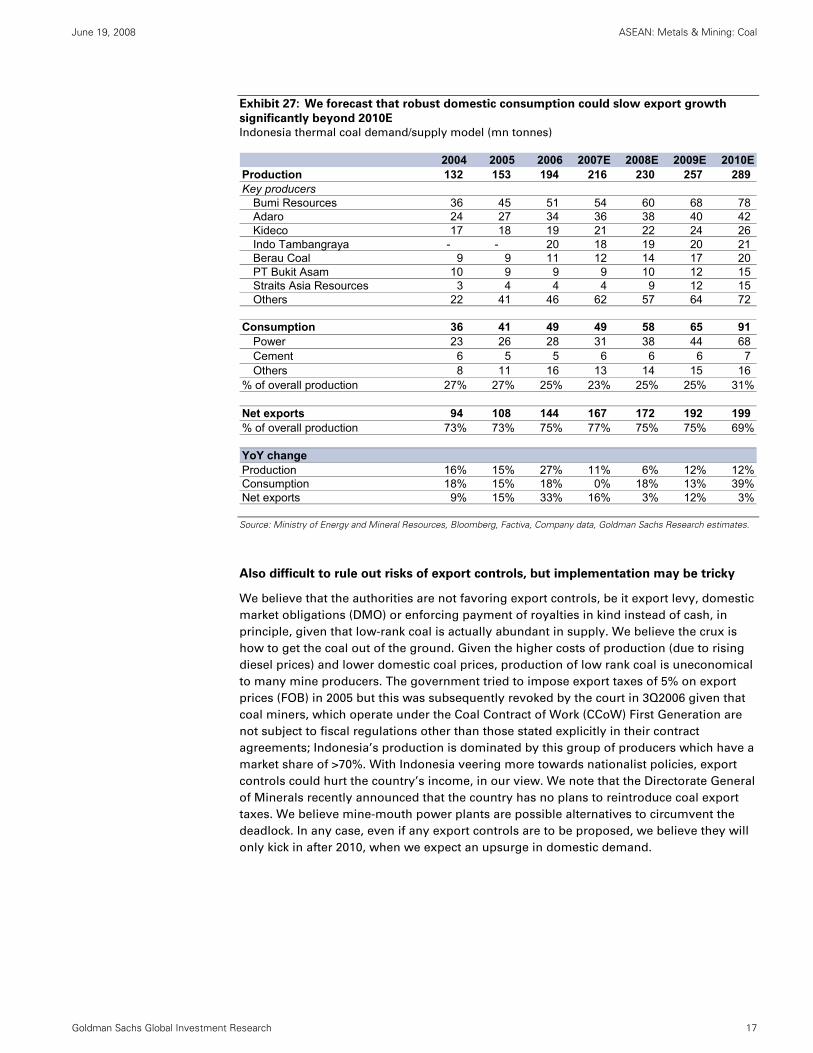

Exhibit 27: We forecast that robust domestic consumption could slow export growth

significantly beyond 2010E

Indonesia thermal coal demand/supply model (mn tonnes)

2004 2005 2006 2007E 2008E 2009E 2010EProduction 132 153 194 216 230 257 289 Key producers 11

Bumi Resources 36 45 51 54 60 68 78 Adaro 24 27 34 36 38 40 42 Kideco 17 18 19 21 22 24 26 Indo Tambangraya - - 20 18 19 20 21 Berau Coal 9 9 11 12 14 17 20 PT Bukit Asam 10 9 9 9 10 12 15 Straits Asia Resources 3 4 4 4 9 12 15 Others 22 41 46 62 57 64 72

Consumption 36 41 49 49 58 65 91 Power 23 26 28 31 38 44 68 Cement 6 5 5 6 6 6 7 Others 8 11 16 13 14 15 16

% of overall production 27% 27% 25% 23% 25% 25% 31%

Net exports 94 108 144 167 172 192 199 % of overall production 73% 73% 75% 77% 75% 75% 69%

YoY change Production 16% 15% 27% 11% 6% 12% 12%Consumption 18% 15% 18% 0% 18% 13% 39%Net exports 9% 15% 33% 16% 3% 12% 3%

Source: Ministry of Energy and Mineral Resources, Bloomberg, Factiva, Company data, Goldman Sachs Research estimates.

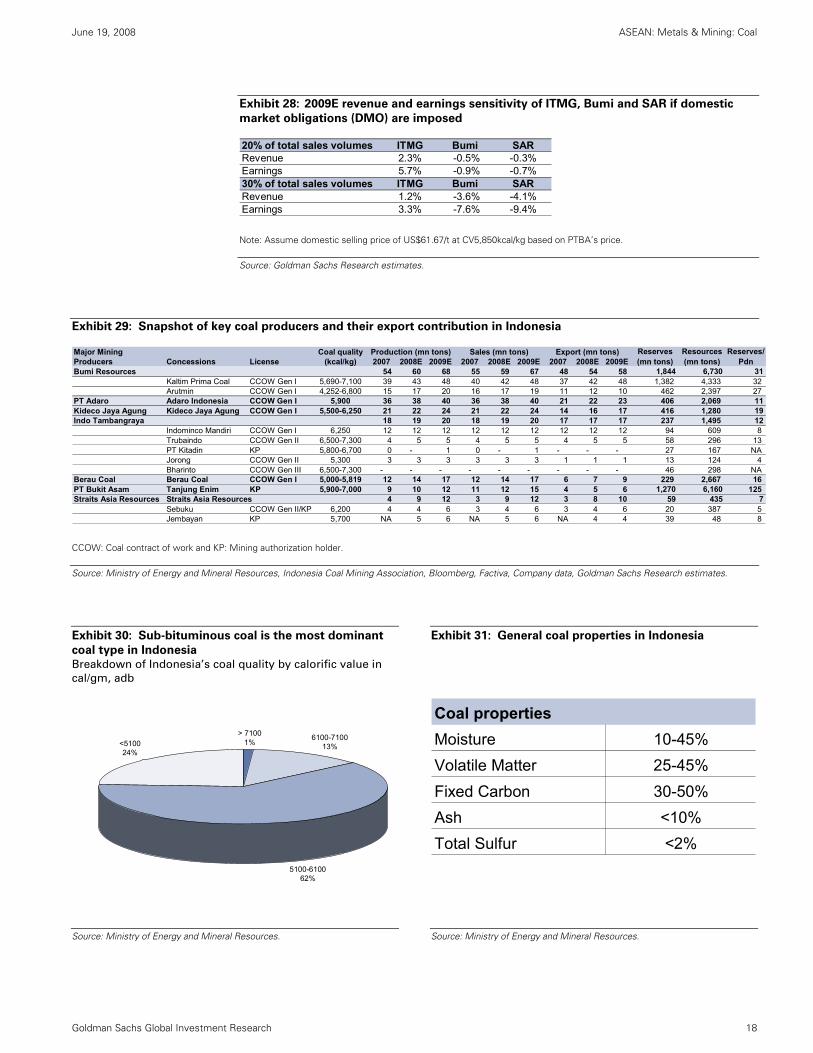

Also difficult to rule out risks of export controls, but implementation may be tricky

We believe that the authorities are not favoring export controls, be it export levy, domestic

market obligations (DMO) or enforcing payment of royalties in kind instead of cash, in

principle, given that low-rank coal is actually abundant in supply. We believe the crux is

how to get the coal out of the ground. Given the higher costs of production (due to rising

diesel prices) and lower domestic coal prices, production of low rank coal is uneconomical

to many mine producers. The government tried to impose export taxes of 5% on export

prices (FOB) in 2005 but this was subsequently revoked by the court in 3Q2006 given that

coal miners, which operate under the Coal Contract of Work (CCoW) First Generation are

not subject to fiscal regulations other than those stated explicitly in their contract

agreements; Indonesia’s production is dominated by this group of producers which have a

market share of >70%. With Indonesia veering more towards nationalist policies, export

controls could hurt the country’s income, in our view. We note that the Directorate General

of Minerals recently announced that the country has no plans to reintroduce coal export

taxes. We believe mine-mouth power plants are possible alternatives to circumvent the

deadlock. In any case, even if any export controls are to be proposed, we believe they will

only kick in after 2010, when we expect an upsurge in domestic demand.

June 19, 2008 ASEAN: Metals & Mining: Coal

Goldman Sachs Global Investment Research 18

Exhibit 28: 2009E revenue and earnings sensitivity of ITMG, Bumi and SAR if domestic

market obligations (DMO) are imposed

20% of total sales volumes ITMG Bumi SARRevenue 2.3% -0.5% -0.3%Earnings 5.7% -0.9% -0.7%30% of total sales volumes ITMG Bumi SARRevenue 1.2% -3.6% -4.1%Earnings 3.3% -7.6% -9.4%

Note: Assume domestic selling price of US$61.67/t at CV5,850kcal/kg based on PTBA’s price.

Source: Goldman Sachs Research estimates.

Exhibit 29: Snapshot of key coal producers and their export contribution in Indonesia

Major Mining Coal qualityProducers Concessions License (kcal/kg) 2007 2008E 2009E 2007 2008E 2009E 2007 2008E 2009EBumi Resources 54 60 68 55 59 67 48 54 58 1,844 6,730 31

Kaltim Prima Coal CCOW Gen I 5,690-7,100 39 43 48 40 42 48 37 42 48 1,382 4,333 32 Arutmin CCOW Gen I 4,252-6,800 15 17 20 16 17 19 11 12 10 462 2,397 27

PT Adaro Adaro Indonesia CCOW Gen I 5,900 36 38 40 36 38 40 21 22 23 406 2,069 11 Kideco Jaya Agung Kideco Jaya Agung CCOW Gen I 5,500-6,250 21 22 24 21 22 24 14 16 17 416 1,280 19 Indo Tambangraya 18 19 20 18 19 20 17 17 17 237 1,495 12

Indominco Mandiri CCOW Gen I 6,250 12 12 12 12 12 12 12 12 12 94 609 8 Trubaindo CCOW Gen II 6,500-7,300 4 5 5 4 5 5 4 5 5 58 296 13 PT Kitadin KP 5,800-6,700 0 - 1 0 - 1 - - - 27 167 NAJorong CCOW Gen II 5,300 3 3 3 3 3 3 1 1 1 13 124 4 Bharinto CCOW Gen III 6,500-7,300 - - - - - - - - - 46 298 NA

Berau Coal Berau Coal CCOW Gen I 5,000-5,819 12 14 17 12 14 17 6 7 9 229 2,667 16 PT Bukit Asam Tanjung Enim KP 5,900-7,000 9 10 12 11 12 15 4 5 6 1,270 6,160 125 Straits Asia Resources Straits Asia Resources 4 9 12 3 9 12 3 8 10 59 435 7

Sebuku CCOW Gen II/KP 6,200 4 4 6 3 4 6 3 4 6 20 387 5 Jembayan KP 5,700 NA 5 6 NA 5 6 NA 4 4 39 48 8

Reserves/Pdn

Production (mn tons) Export (mn tons) Reserves (mn tons)

Resources (mn tons)

Sales (mn tons)

CCOW: Coal contract of work and KP: Mining authorization holder.

Source: Ministry of Energy and Mineral Resources, Indonesia Coal Mining Association, Bloomberg, Factiva, Company data, Goldman Sachs Research estimates.

Exhibit 30: Sub-bituminous coal is the most dominant

coal type in Indonesia

Breakdown of Indonesia’s coal quality by calorific value in

cal/gm, adb

Exhibit 31: General coal properties in Indonesia

> 71001%

5100-610062%

<510024%

6100-710013%

Coal propertiesMoisture 10-45%Volatile Matter 25-45%Fixed Carbon 30-50%Ash <10%Total Sulfur <2%

Source: Ministry of Energy and Mineral Resources.

Source: Ministry of Energy and Mineral Resources.

June 19, 2008 A

SEAN

: Metals &

Mining: C

oal

Goldm

an Sachs Global Investm

ent Research

19

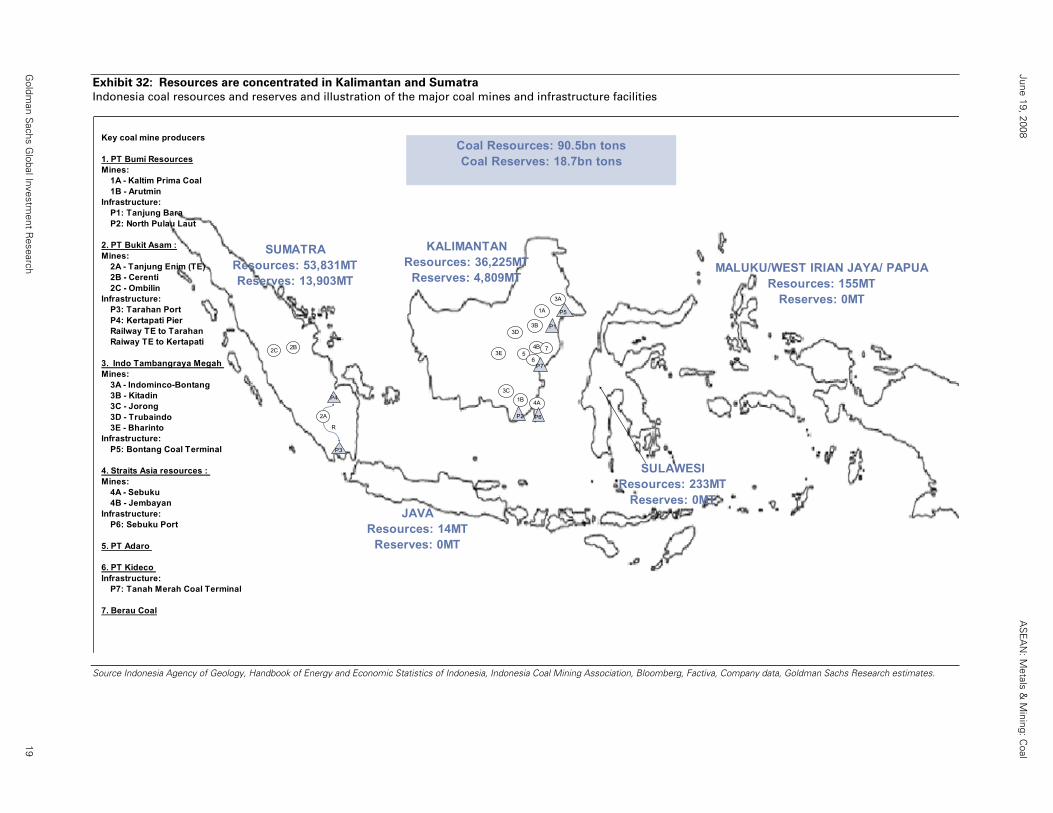

Exhibit 32: Resources are concentrated in Kalimantan and Sumatra

Indonesia coal resources and reserves and illustration of the major coal mines and infrastructure facilities

3D

1A

1B

2B

2A

4A

4B

SUMATRAResources: 53,831MTReserves: 13,903MT

KALIMANTAN Resources: 36,225MT

Reserves: 4,809MT

SULAWESIResources: 233MT

Reserves: 0MT

2C

JAVAResources: 14MT

Reserves: 0MT

MALUKU/WEST IRIAN JAYA/ PAPUAResources: 155MT

Reserves: 0MT

Coal Resources: 90.5bn tonsCoal Reserves: 18.7bn tons

P5

P2

3C

3E

3B

3A

P1

5

P3

P4

R

P6

6P7

7

Key coal mine producers

1. PT Bumi ResourcesMines: 1A - Kaltim Prima Coal 1B - ArutminInfrastructure: P1: Tanjung Bara P2: North Pulau Laut

2. PT Bukit Asam :Mines: 2A - Tanjung Enim (TE) 2B - Cerenti 2C - OmbilinInfrastructure: P3: Tarahan Port P4: Kertapati Pier Railway TE to Tarahan Raiway TE to Kertapati

3. Indo Tambangraya Megah Mines: 3A - Indominco-Bontang 3B - Kitadin 3C - Jorong 3D - Trubaindo 3E - BharintoInfrastructure: P5: Bontang Coal Terminal

4. Straits Asia resources : Mines: 4A - Sebuku 4B - JembayanInfrastructure: P6: Sebuku Port

5. PT Adaro

6. PT Kideco Infrastructure: P7: Tanah Merah Coal Terminal

7. Berau Coal

Source Indonesia Agency of Geology, Handbook of Energy and Economic Statistics of Indonesia, Indonesia Coal Mining Association, Bloomberg, Factiva, Company data, Goldman Sachs Research estimates.

June 19, 2008 ASEAN: Metals & Mining: Coal

Goldman Sachs Global Investment Research 20

Investment theme #2: More upside to realized prices with rising pricing power in

the export and domestic market

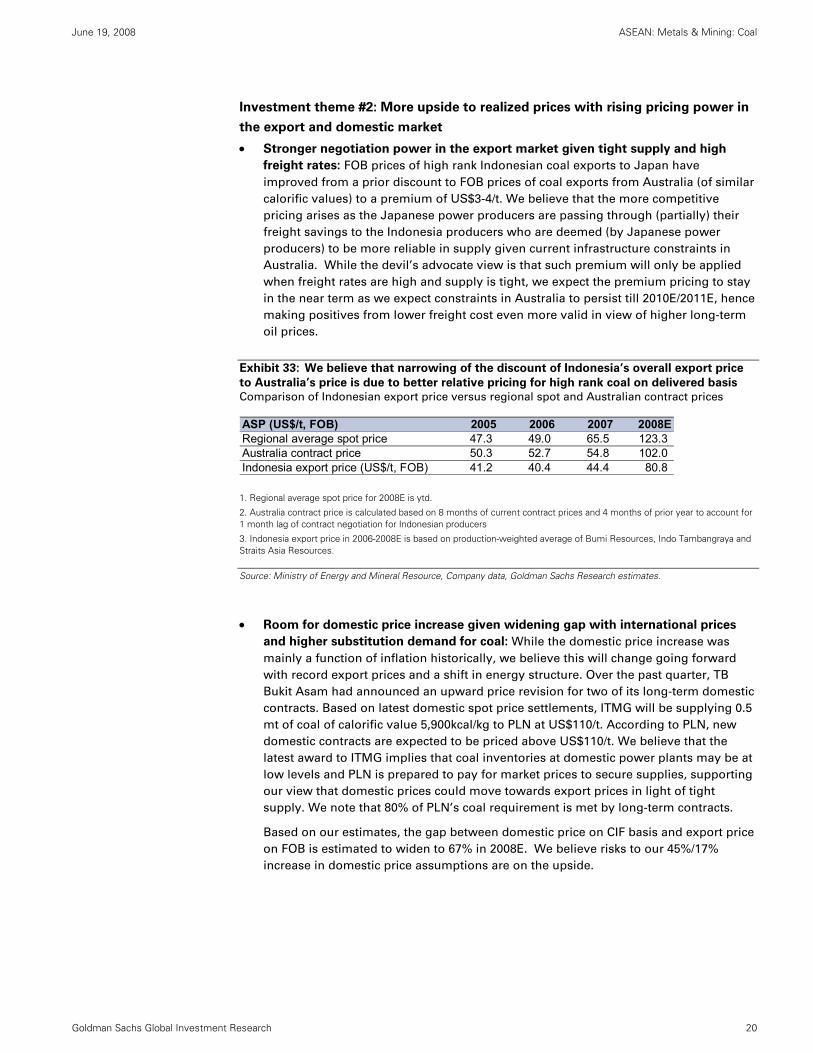

• Stronger negotiation power in the export market given tight supply and high

freight rates: FOB prices of high rank Indonesian coal exports to Japan have

improved from a prior discount to FOB prices of coal exports from Australia (of similar

calorific values) to a premium of US$3-4/t. We believe that the more competitive

pricing arises as the Japanese power producers are passing through (partially) their

freight savings to the Indonesia producers who are deemed (by Japanese power

producers) to be more reliable in supply given current infrastructure constraints in

Australia. While the devil’s advocate view is that such premium will only be applied

when freight rates are high and supply is tight, we expect the premium pricing to stay

in the near term as we expect constraints in Australia to persist till 2010E/2011E, hence

making positives from lower freight cost even more valid in view of higher long-term

oil prices.

Exhibit 33: We believe that narrowing of the discount of Indonesia’s overall export price

to Australia’s price is due to better relative pricing for high rank coal on delivered basis

Comparison of Indonesian export price versus regional spot and Australian contract prices

ASP (US$/t, FOB) 2005 2006 2007 2008ERegional average spot price 47.3 49.0 65.5 123.3 Australia contract price 50.3 52.7 54.8 102.0 Indonesia export price (US$/t, FOB) 41.2 40.4 44.4 80.8

1. Regional average spot price for 2008E is ytd.

2. Australia contract price is calculated based on 8 months of current contract prices and 4 months of prior year to account for 1 month lag of contract negotiation for Indonesian producers

3. Indonesia export price in 2006-2008E is based on production-weighted average of Bumi Resources, Indo Tambangraya and Straits Asia Resources.

Source: Ministry of Energy and Mineral Resource, Company data, Goldman Sachs Research estimates.

• Room for domestic price increase given widening gap with international prices

and higher substitution demand for coal: While the domestic price increase was

mainly a function of inflation historically, we believe this will change going forward

with record export prices and a shift in energy structure. Over the past quarter, TB

Bukit Asam had announced an upward price revision for two of its long-term domestic

contracts. Based on latest domestic spot price settlements, ITMG will be supplying 0.5

mt of coal of calorific value 5,900kcal/kg to PLN at US$110/t. According to PLN, new

domestic contracts are expected to be priced above US$110/t. We believe that the

latest award to ITMG implies that coal inventories at domestic power plants may be at

low levels and PLN is prepared to pay for market prices to secure supplies, supporting

our view that domestic prices could move towards export prices in light of tight

supply. We note that 80% of PLN’s coal requirement is met by long-term contracts.

Based on our estimates, the gap between domestic price on CIF basis and export price

on FOB is estimated to widen to 67% in 2008E. We believe risks to our 45%/17%

increase in domestic price assumptions are on the upside.

June 19, 2008 ASEAN: Metals & Mining: Coal

Goldman Sachs Global Investment Research 21

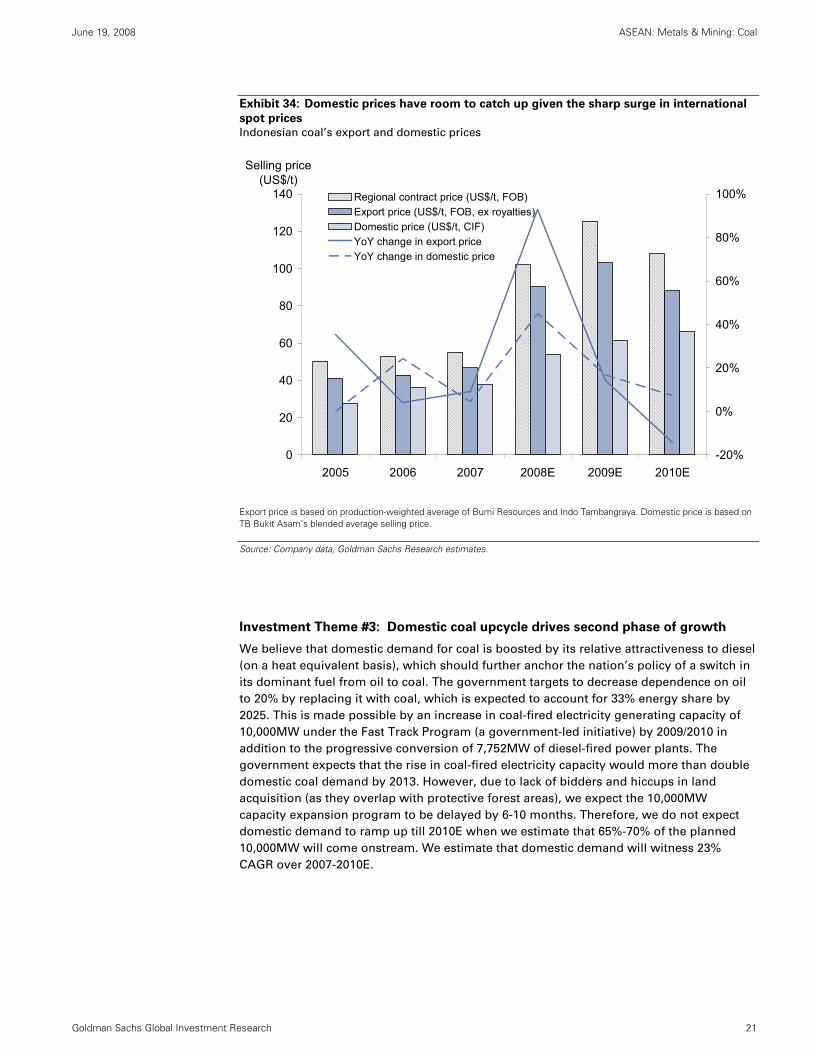

Exhibit 34: Domestic prices have room to catch up given the sharp surge in international

spot prices

Indonesian coal’s export and domestic prices

0

20

40

60

80

100

120

140

2005 2006 2007 2008E 2009E 2010E

Selling price (US$/t)

-20%

0%

20%

40%

60%

80%

100%Regional contract price (US$/t, FOB)Export price (US$/t, FOB, ex royalties)Domestic price (US$/t, CIF)YoY change in export price YoY change in domestic price

Export price is based on production-weighted average of Bumi Resources and Indo Tambangraya. Domestic price is based on TB Bukit Asam’s blended average selling price.

Source: Company data, Goldman Sachs Research estimates.

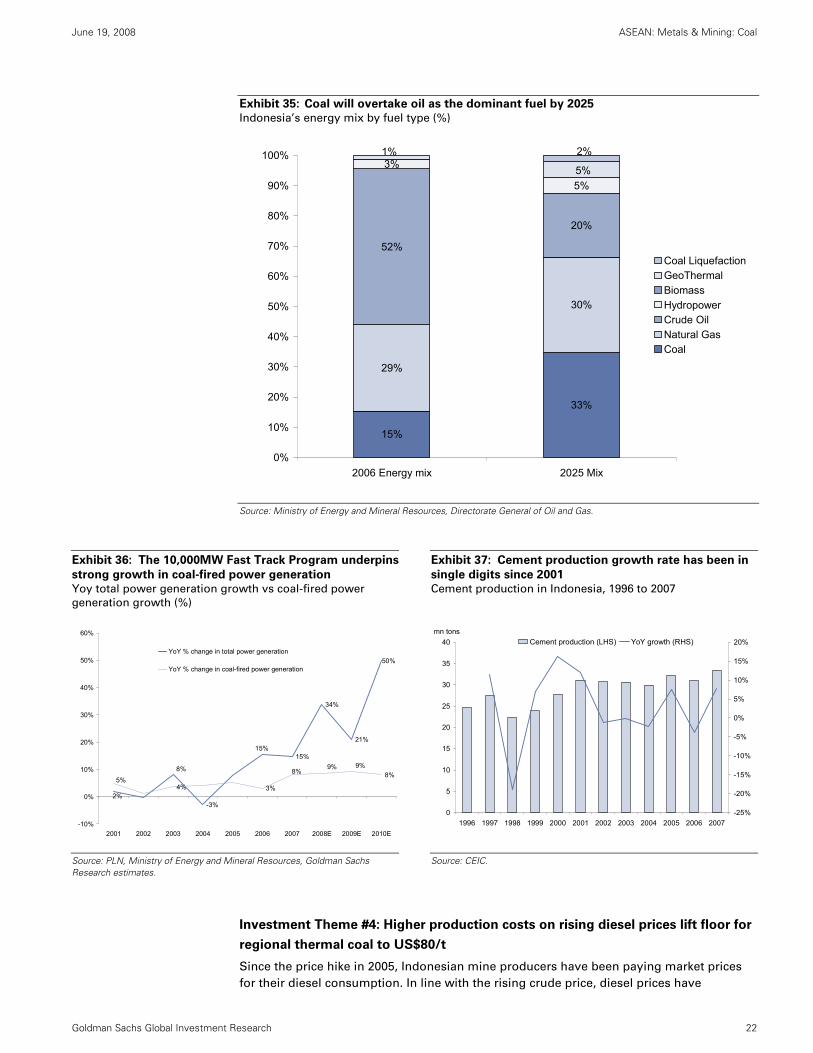

Investment Theme #3: Domestic coal upcycle drives second phase of growth

We believe that domestic demand for coal is boosted by its relative attractiveness to diesel

(on a heat equivalent basis), which should further anchor the nation’s policy of a switch in

its dominant fuel from oil to coal. The government targets to decrease dependence on oil

to 20% by replacing it with coal, which is expected to account for 33% energy share by

2025. This is made possible by an increase in coal-fired electricity generating capacity of

10,000MW under the Fast Track Program (a government-led initiative) by 2009/2010 in

addition to the progressive conversion of 7,752MW of diesel-fired power plants. The

government expects that the rise in coal-fired electricity capacity would more than double

domestic coal demand by 2013. However, due to lack of bidders and hiccups in land

acquisition (as they overlap with protective forest areas), we expect the 10,000MW

capacity expansion program to be delayed by 6-10 months. Therefore, we do not expect

domestic demand to ramp up till 2010E when we estimate that 65%-70% of the planned

10,000MW will come onstream. We estimate that domestic demand will witness 23%

CAGR over 2007-2010E.

June 19, 2008 ASEAN: Metals & Mining: Coal

Goldman Sachs Global Investment Research 22

Exhibit 35: Coal will overtake oil as the dominant fuel by 2025

Indonesia’s energy mix by fuel type (%)

15%

33%

29%

30%

52%

20%

3%

5%5%

1% 2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2006 Energy mix 2025 Mix

Coal LiquefactionGeoThermalBiomassHydropowerCrude OilNatural GasCoal

Source: Ministry of Energy and Mineral Resources, Directorate General of Oil and Gas.

Exhibit 36: The 10,000MW Fast Track Program underpins

strong growth in coal-fired power generation

Yoy total power generation growth vs coal-fired power

generation growth (%)

Exhibit 37: Cement production growth rate has been in

single digits since 2001

Cement production in Indonesia, 1996 to 2007

-3%

15%

34%

21%

50%

4% 3%

8%

2%

15%

8% 9%9%8%

5%

-10%

0%

10%

20%

30%

40%

50%

60%

2001 2002 2003 2004 2005 2006 2007 2008E 2009E 2010E

YoY % change in total power generation

YoY % change in coal-fired power generation

0

5

10

15

20

25

30

35

40

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

mn tons

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%Cement production (LHS) YoY growth (RHS)

Source: PLN, Ministry of Energy and Mineral Resources, Goldman Sachs Research estimates.

Source: CEIC.

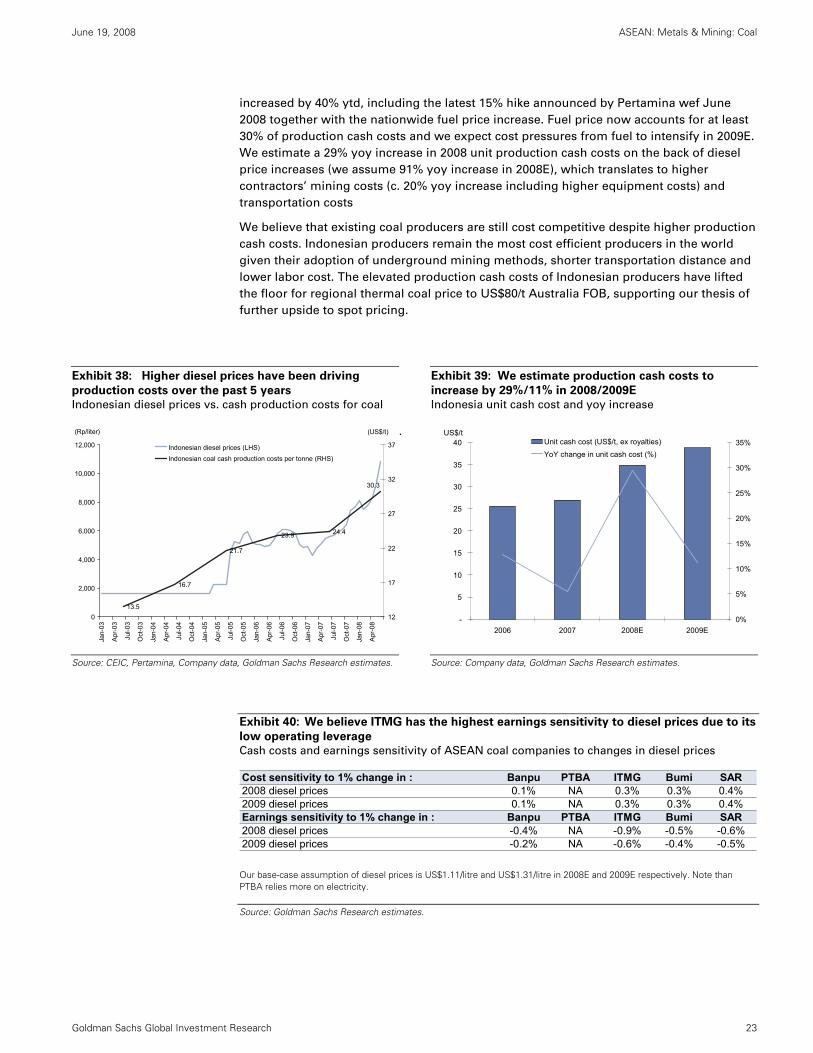

Investment Theme #4: Higher production costs on rising diesel prices lift floor for

regional thermal coal to US$80/t

Since the price hike in 2005, Indonesian mine producers have been paying market prices

for their diesel consumption. In line with the rising crude price, diesel prices have

June 19, 2008 ASEAN: Metals & Mining: Coal

Goldman Sachs Global Investment Research 23

increased by 40% ytd, including the latest 15% hike announced by Pertamina wef June

2008 together with the nationwide fuel price increase. Fuel price now accounts for at least

30% of production cash costs and we expect cost pressures from fuel to intensify in 2009E.

We estimate a 29% yoy increase in 2008 unit production cash costs on the back of diesel

price increases (we assume 91% yoy increase in 2008E), which translates to higher

contractors’ mining costs (c. 20% yoy increase including higher equipment costs) and

transportation costs

We believe that existing coal producers are still cost competitive despite higher production

cash costs. Indonesian producers remain the most cost efficient producers in the world

given their adoption of underground mining methods, shorter transportation distance and

lower labor cost. The elevated production cash costs of Indonesian producers have lifted

the floor for regional thermal coal price to US$80/t Australia FOB, supporting our thesis of

further upside to spot pricing.

Exhibit 38: Higher diesel prices have been driving

production costs over the past 5 years

Indonesian diesel prices vs. cash production costs for coal

Exhibit 39: We estimate production cash costs to

increase by 29%/11% in 2008/2009E

Indonesia unit cash cost and yoy increase

13.5

16.7

21.7

23.9 24.4

30.3

0

2,000

4,000

6,000

8,000

10,000

12,000

Jan-

03

Apr

-03

Jul-0

3

Oct

-03

Jan-

04

Apr

-04

Jul-0

4

Oct

-04

Jan-

05

Apr

-05

Jul-0

5

Oct

-05

Jan-

06

Apr

-06

Jul-0

6

Oct

-06

Jan-

07

Apr

-07

Jul-0

7

Oct

-07

Jan-

08

Apr

-08

(Rp/liter)

12

17

22

27

32

37

(US$/t)

Indonesian diesel prices (LHS)Indonesian coal cash production costs per tonne (RHS)

.

-

5

10

15

20

25

30

35

40

2006 2007 2008E 2009E

US$/t

0%

5%

10%

15%

20%

25%

30%

35%Unit cash cost (US$/t, ex royalties)YoY change in unit cash cost (%)

Source: CEIC, Pertamina, Company data, Goldman Sachs Research estimates.

Source: Company data, Goldman Sachs Research estimates.

Exhibit 40: We believe ITMG has the highest earnings sensitivity to diesel prices due to its

low operating leverage

Cash costs and earnings sensitivity of ASEAN coal companies to changes in diesel prices

Cost sensitivity to 1% change in : Banpu PTBA ITMG Bumi SAR2008 diesel prices 0.1% NA 0.3% 0.3% 0.4%2009 diesel prices 0.1% NA 0.3% 0.3% 0.4%Earnings sensitivity to 1% change in : Banpu PTBA ITMG Bumi SAR2008 diesel prices -0.4% NA -0.9% -0.5% -0.6%2009 diesel prices -0.2% NA -0.6% -0.4% -0.5%

Our base-case assumption of diesel prices is US$1.11/litre and US$1.31/litre in 2008E and 2009E respectively. Note than PTBA relies more on electricity.

Source: Goldman Sachs Research estimates.

June 19, 2008 ASEAN: Metals & Mining: Coal

Goldman Sachs Global Investment Research 24

Investment Theme #5: M&A should continue to fuel interest

Rising energy prices have spurred a flurry of domestic and foreign interest in acquisition of

prime coal assets. According to the Head of the Indonesia Coal Mining Association, there

are at least 15 foreign companies currently exploring acquisition opportunities in coal

mines in Indonesia, with particularly strong interest from China and India steel and energy

producers. Leading India power producers such as Tata Power and Reliance Power have

bought stakes in Indonesia coal mines. According to a Reuters news report dated May 12,

2008, India’s state-run National Thermal Power Corporation is also looking at potentially

buying majority stakes in Indonesian coal mines with reserves of up to 300 mt to secure

supplies and manage costs. Local companies such as United Tractors and Straits Asia

Resources have also been successful in acquisitions recently, although the scale is much

smaller at about 40 mt of reserves.

We believe the consolidation theme will accelerate, but given significant cost inflation,

both at the capital and operating costs levels, new mining operations will be entering the

industry in the upper portion of the cost curve. Hence, ASEAN coal equities which rely on

acquisitions to extend production life may see lower returns in comparison with existing

producers, in our view.

Exhibit 41: Recently concluded M&A deals in the Indonesian coal sector

Acquirer Reserves (mt)Acquisition

cost (US$mn)Cost/reserves

(US$/ton) Acquired concessionsTata Power 4,206 1,100 0.26 30% of KPC and Arutmin

Reliance 2,000 565 0.28 Coal Mine in South Sumatra: Bintangtiga Energy, Bryayan Bintangtiga Energy and Sugico Pendragon Energy

United Tractors 40 116 2.89 PT Tuah Turangga Agung in KalimantanStraits Asia Resources 39 350 8.97 Jembayan in Kalimantan

PT Indika Energy 47 100 2.13 Acquisition targets not disclosed and the deal will only be concluded in end July 2008.

Emco 105 NA NA PT Bina Insan Sukses Mandiri

Source: Factiva, Reuters, Tex Report.

Risks: Spotlight will be on the long-delayed mining laws

Uncertain regulatory framework; awaiting new mining bill for more clarity

The Indonesian coal mining industry is full of skeptics who believe that the legal

framework is far from robust, which reflects the valuation discount versus its global peers,

in our view. According to a survey by Pricewaterhouse Coopers (covering more than 85%

of the companies operating in Indonesia) published in 2007, the top five impediments to

investment in mining sectors are: 1) conflict between mining and forestry regulations; 2)

duplication or contradiction between central and local governments; 3) taxation issues

such as tax incentives, VAT, etc; 4) delay in finalization of new mining law; and 5)

unfairness in divestment of foreign interests and mine closures.

According to channel checks, the delay in passing of the new Mining Bill was due to a