goldman sachs asset management: our approach to esg investing

TRANSCRIPT

FOR CLIENT USE ONLY. NOT FOR USE AND/OR DISTRIBUTION TO YOUR CLIENTS OR THE GENERAL PUBLIC

August 2020

Goldman Sachs Asset Management: Our

Approach to ESG Investing

I. Introduction to Our ESG Views

3 Executive Summary

Integration Across the

Division

180+ investment professionals integrating ESG, including 40+ ESG and impact

investing experts

ESG capabilities within GSAM span public equities, fixed income, liquidity, private

markets

Widespread collaboration among GSAM teams allows for increased leverage and deeper engagement

Investment-Driven

Philosophy

Stewardship is a Key

Focus

Stewardship, engagement, proxy voting, network memberships are core to our

approach

350+ top-down engagements of Global Stewardship Team complement the ~ 2,000

bottom-up engagements of GSAM investment teams

Breadth, Depth, and

Scale Across the Firm

Goldman Sachs has a firmwide commitment to sustainable finance across all of our

business lines, demonstrated by the formation of the Sustainable Finance Group

Ability to leverage firmwide resources allows delivery of comprehensive sustainability

solutions

GSAM’s Approach to ESG and Impact Investing

ESG implemented with a range of approaches: integration, alignment, thematic, impact

Customization to client requirements and objectives

Growing suite of commingled solutions

Source: GSAM, as of 30-Jun-2020. There is no guarantee that these objectiv es will be met. GSAM lev erages the resources of Goldman Sachs & Co. LLC subject to legal, internal and regulatory

restrictions.

196953-TMPL-03/2020-

1156333

4

Source: GSAM, as of June 30, 2020. For illustrative purposes only. There is no guarantee that these objectives will be met. The portfolio risk management process includes an effort to monitor and manage risk, but does not imply low risk.

“For companies to achieve high and sustainable returns over the long term, we believe they must embrace and adopt robust environmental, social and governance (ESG) standards. Failure to do so is their biggest risk.” – Katie Koch; Co-Head of Fundamental Equity

Sound ESG Practices...

...Drive Value Creation

... And Long-Term Performance

Environmental

Energy Management

Emissions

Resource Intensity

Social

Labor Practices

Supply-Chain Management

Community Impact

Governance

Shareholder Rights

Transparency

Management Alignment

Strong Growth

Brand / Trust

Addressable Opportunity / Need

Competitive Position

Higher Profitability

Minimized Waste

Production / Execution Eff iciency

Employee Productivity

Lower Cost of Capital

Higher valuation multiples

Low er discount rates

Greater sustainability of returns

Enhanced understanding of company fundamentals

Increased conviction in

investment decisions

Clear framework for further

engagement

Why ESG Matters ESG analysis can help mitigate risks and uncover investment opportunities

FOR INSTITUTIONAL OR FINANCIAL INTERMEDIARIES USE ONLY – NOT FOR USE AND/OR DISTRIBUTION TO THE GENERAL PUBLIC

5 FOR CLIENT USE ONLY. NOT FOR USE AND/OR DISTRIBUTION TO YOUR CLIENTS OR THE GENERAL PUBLIC

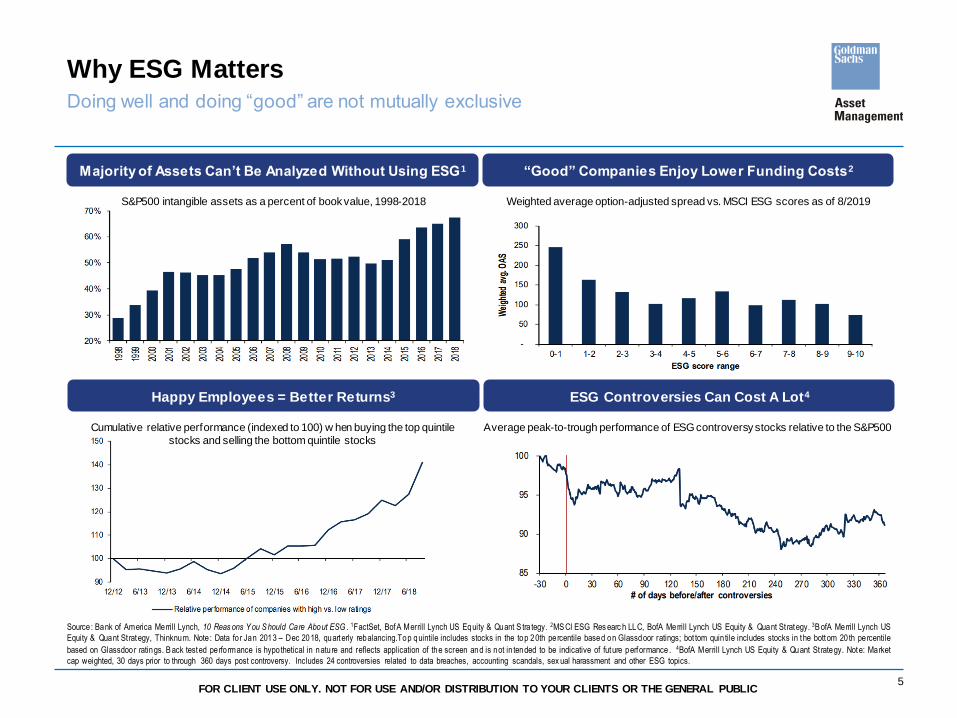

Why ESG Matters Doing well and doing “good” are not mutually exclusive

Majority of Assets Can’t Be Analyzed Without Using ESG1 “Good” Companies Enjoy Lower Funding Costs2

Happy Employees = Better Returns3 ESG Controversies Can Cost A Lot4

Average peak-to-trough performance of ESG controversy stocks relative to the S&P500 Cumulative relative performance (indexed to 100) w hen buying the top quintile

stocks and selling the bottom quintile stocks

Source : Bank of America Merrill Lynch, 10 Reas ons Y ou S hould Care About ESG . 1FactSet, BofA Merrill Lynch US Equity & Quant S tra tegy. 2MS CI ESG Res earc h LLC, BofA Merrill Lynch US Equity & Quant St rategy. 3B ofA Merrill Lynch US

Equity & Quant St rategy, Thinknum. Note : Data fo r Jan 2013 – Dec 2018, quarterly rebalancing.Top quintile includes stocks in the top 20th percentile based on Glassdoor ratings; bot tom quin tile includes stocks in the bottom 20 th percentile

based on Glassdoor ratings. B ack tested perfo rmance is hypothetical in nature and reflects application of the screen and is not in tended to be indicative of future performance . 4BofA Merrill Lynch US Equity & Quant St rategy. Note: Market

cap weighted, 30 days prior to through 360 days post controversy. Includes 24 controversies related to data breaches, accounting scandals, sex ual harassment and other ESG topics.

Weighted average option-adjusted spread vs. MSCI ESG scores as of 8/2019 S&P500 intangible assets as a percent of book value, 1998-2018

6

• Limited quality & availability

• Backward looking

• Inconsistent third party scoring

1. Flawed Data

2. Resource Intensive

• Infrastructure heavy

• Human diligence dependent

• Expertise required

3. Varying Views

• Lack of standardization

• Differing views on materiality

• Diverse client values & objectives

Source: GSAM, as of June 30, 2020. For illustrative purposes only. There is no guarantee that these objectives will be met. 1 GS SUSTAIN, February 2018. Data corresponds to MSCI ACWI constituents. 2 Schroders, March 2018.

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Environmental Social Governance

MSCI vs. Sustainalytics MSCI vs. Thomson ReutersSustainalytics vs. Thomson Reuters

Challenges of the space…

71% of numeric ESG metrics have less than 20% disclosure1

THEREFORE

Common approaches to ESG scoring tend to rely on vague policies,

favoring quantity of ESG disclosure over quality of ESG practices

AND

Scores across the main ESG scoring providers vary considerably2

Sc

ore

Co

rre

lati

on

The Challenges Of Determining ESG Practice ESG investing is inherently complex, lending itself to a fundamentally driven, active

approach

FOR INSTITUTIONAL OR FINANCIAL INTERMEDIARIES USE ONLY – NOT FOR USE AND/OR DISTRIBUTION TO THE GENERAL PUBLIC

II. GSAM ESG Integration Approach

8

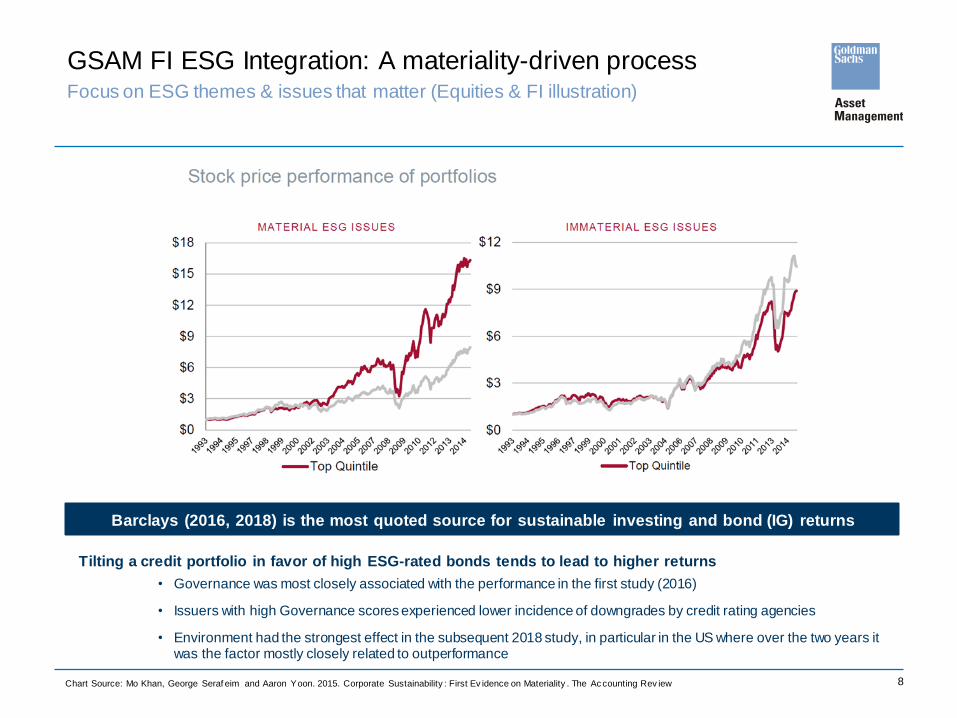

GSAM FI ESG Integration: A materiality-driven process Focus on ESG themes & issues that matter (Equities & FI illustration)

Chart Source: Mo Khan, George Seraf eim and Aaron Yoon. 2015. Corporate Sustainability : First Ev idence on Materiality . The Ac counting Rev iew

• Governance was most closely associated with the performance in the first study (2016)

• Issuers with high Governance scores experienced lower incidence of downgrades by credit rating agencies

• Environment had the strongest effect in the subsequent 2018 study, in particular in the US where over the two years it was the factor mostly closely related to outperformance

Barclays (2016, 2018) is the most quoted source for sustainable investing and bond (IG) returns

Tilting a credit portfolio in favor of high ESG-rated bonds tends to lead to higher returns

9

GSAM ESG Integration: Material themes & issues

E, S or G Theme Issue Risk Exposure Risk mitigation example

Greenhouse gas emissions Carbon tax L/T carbon emissions reduction target

Carbon emissions attributed to upstream supply chain Life cycle management of emissions

Financing environmental impact (fossil fuel risk in Banks' loans portfolio) e.g. climate risk reporting (TCFD)

Energy Management Cost & energy efficiency regulation Energy intensity reduction target

Air quality (pollution) NOx, SOx, VOC standards Year-on-year performance improvement

Waste Plastic regulation Packaging lifecycle approach

Water & Wastewater Water stress regions Water & wastewater management

Ecological Impact & Land Use Deforestation-related commodities Sustainable sourcing (e.g. palm oil)

Raw material sourcing Materials of concern (e.g. deforestation, resource-intensive) Collaborate with suppliers to address impact

Business Model &

Innovation

Green Product/Business

Opportunities

Opportunities in Renewable Energy

Opportunities in Clean Tech

Opportunities in Green Buildings

% of assets in renewables/power generation

Commercializing clean tech products

High % of properties with certification

Human Capital Management Talent & skills shortage Attractive compensation, labor dialogue

Health & Safety Record on incidents & fatalities Accident & safety Management

Human Rights & Labor Rights Child labor, community resistance to projects Audits, community engagement

Product: Safety & Quality Product recalls, litigation Supply chain management

Product: Wellness & Nutrition Sugar tax Food reformulation (nutrients)

Product: Positive Impact Social benefits from products (not credit risk) Opportunities for growth (equities)

Cybersecurity & Data Cyber attacks Controls & remediation plans

Corporate Governance Conflicts of interest Board expertise and independence

Equity owners vs creditor interests Bondholder covenants

Track record & strategic priorities Accounting & disclosure quality

Corruption litigation Anti-bribery & corruption training

Conduct breaches

Customer Complaints

Whistleblower Reports & Complaints

reviewed by the Board

Business Ethics

Governance

Climate ChangeProduct Carbon Footprint

Board and Management

Quality

Conduct & Culture and

Business Ethics

EnvironmentResource Efficiency &

Natural Capital

Social

Product Safety &

Quality, Wellness &

Impact

Human Capital

Factors that are material to a firm’s growth, profitability and risks

Source: GSAM. As of August 2020. For illustrativ e purposes only .

Bondholder focus is primarily on downside risk that impact an issuer’s ability to repay its debts. Equities also looks at tai l risk but additionally upside (sustainability

solutions)

10

GSAM Proprietary ESG rating

c

a. Peer Comparison b. Momentum

5.0 Leader Improving

4.0

3.0

Stable

2.0

1.0 Deteriorating

0.0 Laggard

GSAM ESG Integration: Research Each issuer/stock assessed on ESG, including forward-looking momentum

• Assess risk

• Ev aluate Trend

• E-Climate

• G-Buy backs

• S - Inclusiv e growth

• TCFD

• SASB

• EU Taxonomy

• MSCI

• Bloomberg

• CDP

Third-Party ESG Data

ESG Standards

Direct Engagement

ESG Theme Analytics

ESG Tools / Data & Metrics: acronyms

CDP – formerly known as the Carbon Disclosure Project

TCFD – Task Force for Climate-Related Disclosure

SASB – Sustainability Accounting Standards Board

EU Taxonomy – definitions to help investors understand what is ‘green’

ESG team provides framework, tools, thematic insights

Engagement is an input to ESG ratings (momentum)

Analysts and economists own and assign the ESG rating

Captured on existing research platform/PM systems

ESG Tools / Data & Metrics ESG Rating Framework

Source: GSAM. As of August 2020. For illustrativ e purposes only .

11

Greenhouse Gas

Emissions

Green Product

Air Quality (Pollution)

Water & Wastewater

Human Capital

Management.

Board and Management

Quality

En

viro

nm

en

tal

( 70

% )

So

cia

l ( 1

0%

)

Go

ve

rna

nc

e

( 20

% )

Utility

Iss

ue

r ES

G S

co

re

(0-5

+ tre

nd

)

Implementation e.g. Utilities

GSAM Integration: ESG view captured on Research/PM systems

Corporate ESG criteria

Source: GSAM. As of August 2020. For illustrativ e purposes only .

12

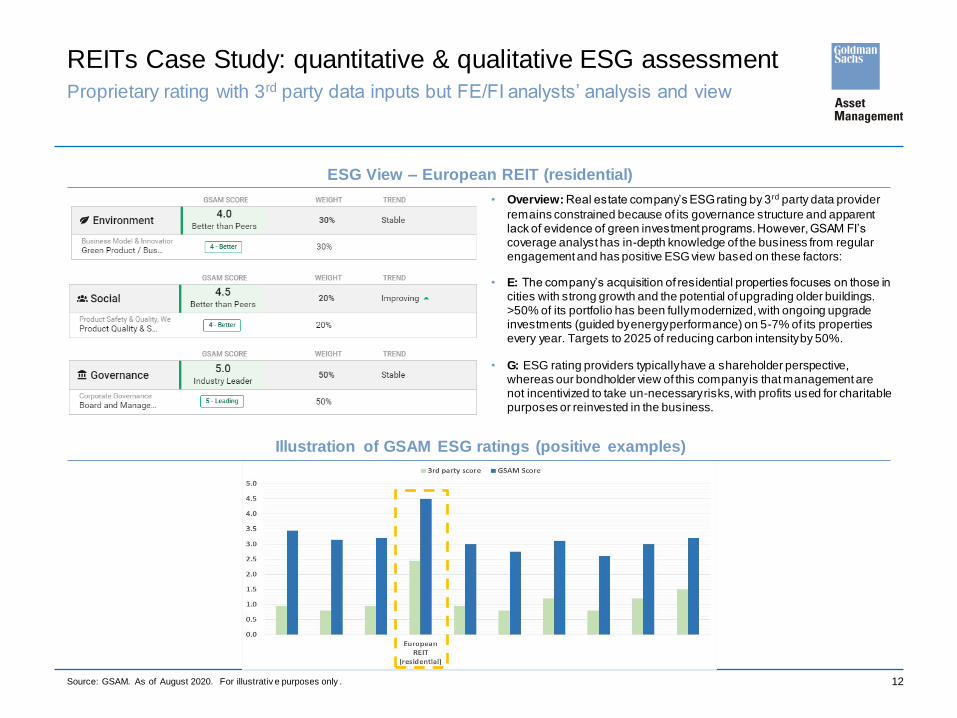

ESG View – European REIT (residential)

• Overview: Real estate company’s ESG rating by 3rd party data provider

remains constrained because of its governance structure and apparent lack of evidence of green investment programs. However, GSAM FI’s coverage analyst has in-depth knowledge of the business from regular engagement and has positive ESG view based on these factors:

• E: The company’s acquisition of residential properties focuses on those in cities with strong growth and the potential of upgrading older buildings. >50% of its portfolio has been fully modernized, with ongoing upgrade investments (guided by energy performance) on 5-7% of its properties every year. Targets to 2025 of reducing carbon intensity by 50%.

• G: ESG rating providers typically have a shareholder perspective, whereas our bondholder view of this company is that management are not incentivized to take un-necessary risks, with profits used for charitable purposes or reinvested in the business.

Illustration of GSAM ESG ratings (positive examples)

Source: GSAM. As of August 2020. For illustrativ e purposes only .

Proprietary rating with 3rd party data inputs but FE/FI analysts’ analysis and view

REITs Case Study: quantitative & qualitative ESG assessment

III. Overview of GSAM ESG Technology

14

Investment Research: Centralized Research Platform Fluent allows us to track ESG views, company engagements and proxy voting outcomes

News & Research

ESG Assessment

Framework

Engagements

Proxy voting

records and

results

Overall view

and ratings

Source: GSAM, as of June 30, 2020. For informational purposes only and should not be construed as research, investment advice or a recommendation. There is no guara ntee that these objectives will be met.

FOR INSTITUTIONAL OR FINANCIAL INTERMEDIARIES USE ONLY – NOT FOR USE AND/OR DISTRIBUTION TO THE GENERAL PUBLIC

15

Portfolio Construction & Risk Management Proprietary portfolio construction and risk tools allow PMs to analyze the ESG

credentials of their portfolios and simulate the impact of potential trades

Trade Simulation Using Portfolio Constructor Daily Risk Assessment Reports

Contributors to

portfolio’s

carbon intensity

Proposed portfolio

would reduce the

carbon intensity below

the benchmark

Source: GSAM, as of June 30, 2020. For informational purposes only and should not be construed as research, investment advice or a recommendation. There is no guara ntee that these objectives will be met. The portfolio risk management

process includes an effort to monitor and manage risk, but does not imply low risk.

FOR INSTITUTIONAL OR FINANCIAL INTERMEDIARIES USE ONLY – NOT FOR USE AND/OR DISTRIBUTION TO THE GENERAL PUBLIC

IV. Engagement and Proxy Voting

17

GSAM Stewardship: Engagement & Proxy Voting

0

10

20

30

40

0

20

40

60

80

100

2011 2012 2013 2014 2015 2016 2017 2018 2019

Other

Asia Pacific

North America

Europe

% Vote in Favour

Number Vote in Fav our (%)

Helping to drive climate disclosure

Source: Prox yInsight, Data compiled by Goldman Sachs Global Investment Research

Engagement with corporates helps us to:

Enhance understanding of company fundamentals

Increase conviction in investment decisions

Inform ‘momentum view’ in our Proprietary ESG rating

Drive disclosure, using our voice as a large, active manager

0%

25%

50%

75%

100%

125%

Jan-2020 Feb-2020 Mar-2020 Apr-2020

Employee Health and Safety Labor Practices

Access and Affordability Product Quality and Safety

Supply Chain Management Other Categories

We’re raising the bar on our expectations of companies

Global Proxy Voting on climate disclosure resolutions Global ESG Topic Share in COVID-19 Related Content

Source: Truvalue Labs, May 2020. Based on >10,000 unique information sources

GSAM Proxy-Voting Highlights:

Supported shareholder proposals on:

climate change disclosures 60% of the time

gender pay gap disclosures 93% of the time

Voted against 312 directors at 214 companies for lacking at least one woman

Contributing to Inclusive Growth

Source: GSAM. As of August 2020. For illustrativ e purposes only .

18

Source: GSAM, as of March 31, 2020. For informational purposes only and should not be construed as research, investment advice or a recommendation. There is no guarantee that these objectives will be met.

FOR CLIENT USE ONLY. NOT FOR USE AND/OR DISTRIBUTION TO YOUR CLIENTS OR THE GENERAL PUBLIC

GSAM’s Engagement Approach We have a robust, global engagement effort that marries the vision of our dedicated

Global Stewardship Team with the expertise of our investment teams

10,000+

Engagements

Annually

“Top-Down”

“Bottom-Up”

The Global Stewardship Team conducts top-down engagements on strategic ESG priorities

Targeted engagements to promote positive change on our strategic policy objectives

Regularly engage ~350 companies over 400+ meetings annually

The Fundamental Equity and Global Fixed Income investment teams conduct bottom-up

engagements as part of ongoing company due-diligence

Investment teams engage companies regularly to inform investment decisions

Regularly engage ~2,000 companies over 10,000+ meetings annually

PRI Engagement Rating: A+

V. Impact of COVID-19 on ESG and Impact Investing Landscape

20

ESG Amplified

Spotlight on S data

Companies’ positive declarations about how they

value their employees,

suppliers and communities

are being put to the test. There is a lack of available

and comparable data on

social factors.

Social

The long-running debate

about the purpose of the corporation has been

invigorated by Covid-19

Green Recovery

An opportunity for

governments as advocated by the IMF and other

policymakers, particularly

Europe

Climate change

Overall, w e expect most companies w ill

recognise that 'green'

investments are secular—

not cyclical—decisions.

Governance

Covid-19 provides new

datasets on the resilience of business models w hen

faced with a stay-at-home

economy and an upside-

dow n energy market.

Is Covid-19 a watershed for ESG investing? Spotlight on interdependencies in human and natural ecosystems

Source: GSAM. As of August 2020. For illustrativ e purposes only .

21

Thank you

Q&A

Appendix

23

Source: GSAM, as of March 31, 2020. Data for July 1, 2018 through June 30, 2019. For illustrative purposes only. There is no guarantee that these objectives will be met. Please see the 2019 GSAM Stewardship Report on our website for

additional information and case studies.

FOR CLIENT USE ONLY. NOT FOR USE AND/OR DISTRIBUTION TO YOUR CLIENTS OR THE GENERAL PUBLIC

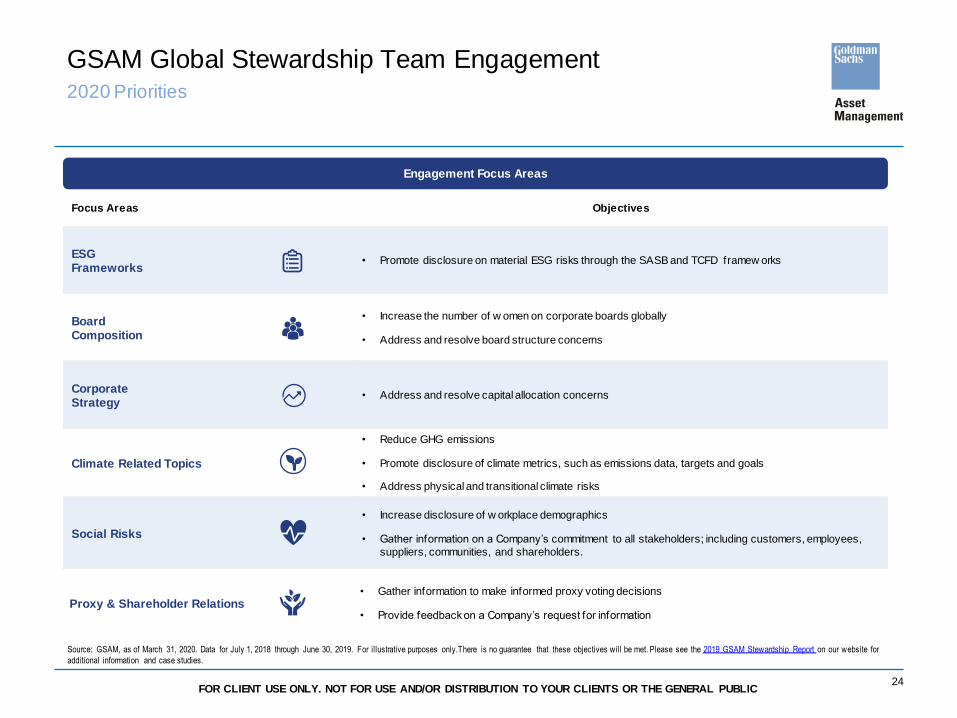

GSAM Global Stewardship Team Engagement 2019 Snapshot

Focus Areas Objectives

ESG

Reporting

• Increase SASB reporting

• Increase disclosure on material ESG risks

Board

Composition

• Increase number of women on corporate boards

• Address and resolv e board structure concerns

Corporate

Strategy • Address and resolv e capital allocation concerns

Environmental

Risks • Reduce GHG emissions

Social Risks • Increase percentage of gender and racial/ethnic

representation in the workplace

Proxy & Shareholder

Relations

• Gather inf ormation to make inf ormed proxy v oting

decisions

• Prov ide f eedback on a Company ’s request f or

inf ormation

Engagements by Sector

Engagements by Theme

27%

23% 17%

12%

12%

9% Proxy & Shareholder Relations

ESG Reporting

Board Composition

Social Risks

Environmental Risks

Corporate Strategy

Sector # of Meetings

Communication Serv ices 13

Consumer Discretionary 42

Consumer Staples 29

Energy 23

Financials 51

Health Care 45

Industrials 68

Inf ormation Technology 63

Materials 29

Real Estate 31

Utilities 23

Total 417

Engagement Focus Areas

24

Source: GSAM, as of March 31, 2020. Data for July 1, 2018 through June 30, 2019. For illustrative purposes only. There is no guarantee that these objectives will be met. Please see the 2019 GSAM Stewardship Report on our website for

additional information and case studies.

FOR CLIENT USE ONLY. NOT FOR USE AND/OR DISTRIBUTION TO YOUR CLIENTS OR THE GENERAL PUBLIC

GSAM Global Stewardship Team Engagement 2020 Priorities

Focus Areas Objectives

ESG Frameworks

• Promote disclosure on material ESG risks through the SASB and TCFD framew orks

Board Composition

• Increase the number of w omen on corporate boards globally

• Address and resolve board structure concerns

Corporate Strategy

• Address and resolve capital allocation concerns

Climate Related Topics

• Reduce GHG emissions

• Promote disclosure of climate metrics, such as emissions data, targets and goals

• Address physical and transitional climate risks

Social Risks

• Increase disclosure of w orkplace demographics

• Gather information on a Company’s commitment to all stakeholders; including customers, employees,

suppliers, communities, and shareholders.

Proxy & Shareholder Relations • Gather information to make informed proxy voting decisions

• Provide feedback on a Company’s request for information

Engagement Focus Areas

25

Using Engagement As A Tool To Drive Outcomes

We use our voice as a shareholder to impact corporate decision making

Pillar Company Engagement Topic(s) Outcome(s)

E

Multinational Energy Company

Emissions Intensity

Reduction Targets

• By 2023, the Company plans to cut methane emissions intensity by 20 – 25% and flaring intensity by 25 – 30% from 2016 levels.

• As of 2019, the Company w ill tie compensation for ~45,000 employees to meeting emissions reductions targets.

Japanese Trading Company

TCFD Reporting

Emissions Disclosures

• Integrated Report disclosures have been materially improving, and the company has committed to issue a fully quantif ied TCFD report w ithin the current f iscal year.

• Plan to deepen their GHG disclosures to Scope 3 (currently only Scope 1 & 2).

S Multinational Financial

Services Firm

Corporate Culture

Employee Benefits

• Published first Human Capital Management report outlining key initiatives and related data on topics such as gender pay equity and employee engagement.

• Recently added benefits for parental leave and adopted a higher than required minimum hourly w age.

• Implemented a policy restricting how the Company solicits compensation

information from candidates during the hiring process.

U.S. Softw are Company

Employee Recruitment & Retention

ESG Reporting

• Expanded ESOP to give more employees access to stock through grants and purchase plans in an effort to better align incentives and increase motivation.

• Moved headquarters to Boston to improve recruiting of young, tech talent.

• Produced latest sustainability report in-line w ith the GRI and SASB standards.

G Eastern European

Bank

Executive Compensation

IT & Cybersecurity Oversight

• Key ESG metrics w ere explicitly included into CEO compensation, w ith transparency around methodology and measurement.

• The company engaged E&Y to conduct an audit of its IT systems, with an emphasis on cybersecurity controls.

• IT & cybersecurity oversight was elevated to the Board level.

U.S. Telecom Company

ESG Oversight

ESG Reporting

• Board of Directors and executive leadership appointed their f irst Chief ESG Officer and created a cross-functional ESG team that includes subject matter expertise in

governance, environmental sustainability, human rights, digital trust, and safety.

• Published first ESG Report w ith SASB and GRI aligned indices and links to key

ESG data, alongside a stand-alone TCFD report.

Source: GSAM, as of March 31, 2019. For informational purposes only and should not be construed as research, investment advice or a recommendation. There is no g uarantee that these objectives will be met.

FOR CLIENT USE ONLY. NOT FOR USE AND/OR DISTRIBUTION TO YOUR CLIENTS OR THE GENERAL PUBLIC

26

Source: GSAM, as of March 31, 2020. Voting data for July 1, 2018 through June 30, 2019. For illustrative purposes only.

FOR CLIENT USE ONLY. NOT FOR USE AND/OR DISTRIBUTION TO YOUR CLIENTS OR THE GENERAL PUBLIC

GSAM’s Global Proxy Voting Approach Robust and technologically enhanced approach to proxy voting

• GSAM’s Global Proxy Voting

Guidelines are updated annually to

incorporate evolving beliefs on key

corporate governance and ESG topics

• Changes are approved each year by

the Mutual Funds’ Boards

• For equities covered under the policy,

proxy voting is a key element of the

portfolio management process

• The GSAM Stew ardship Team drives

the continued enhancement of the

global proxy voting process

• The team w orks w ith internal

stakeholders, such as legal,

compliance, operations, investment

teams and the executive off ice to

ensure our policies allow us to make

voting decisions that are thoughtful

and not influenced by conflicts of

interest

• GSAM has retained a third-party

proxy voting service (ISS) to assist in

the implementation of proxy voting-

related functions, such as operational,

recordkeeping and reporting services

• Within this scope, ISS prepares a

w ritten analysis and recommendation

of each vote that reflects the

application of the GSAM Guidelines to

the particular proxy issues

• GSAM retains the responsibility for

proxy voting decisions

• Every vote is review ed by the

Stew ardship Team and the equity

investment team responsible for the

stock through our proprietary system,

Fluent

• GSAM generally cast votes in-line

w ith the Guidelines and

Recommendations

• Each team may seek approval to

diverge from the Recommendation by

follow ing a process that seeks to

ensure that override decisions are not

inf luenced by any conflict of interest

GSAM Proxy Voting

Guidelines

Stewardship Team

Oversight

Third-Party Voting

Services

Investment Team

Collaboration & Input

27

Source: GSAM, as of March 31, 2020. Voting data for July 1, 2018 through June 30, 2019. For illustrative purposes only. Please see the 2019 GSAM Stewardship Report on our website for additional information and case studies.

10,842

5,529

-

5,000

10,000

15,000

VotedAt Least 1 Vote Against Management Proposals

108,260

12,991

-

50,000

100,000

150,000

Voted Voted Against

Proxy Meetings Voted

Proposals Voted

100% Support for

Shareholder Proposal Related to:

E

S

G

Recycling 2 Degrees Analysis

Health Care Fair Lending

Declassify Board Proxy Access

Proxy Voting Policy Highlights

Board Diversity

Gender Pay Gap

Climate Change

• Vote against directors for lack of female

representation

• Voted against 312 directors at 214 companies for lacking at least one

woman

• Review proposals requesting

reports on policies concerning pay gap

• Supported shareholder

proposals on gender pay gap disclosures 93% of the time

• Strengthen voice around risks,

reduction of emissions and energy efficiency

• Supported shareholder proposals

on climate change disclosures 60% of the time

FOR CLIENT USE ONLY. NOT FOR USE AND/OR DISTRIBUTION TO YOUR CLIENTS OR THE GENERAL PUBLIC

2019 Global Proxy Voting Snapshot We’ve been raising the bar of our expectations from companies

Meetings by Voting Market

36%

25%

18%

15%

6% Americas

EmergingMarketsEMEA

Japan

Asia Pacific

28

Source: GSAM, as of March 31, 2020. For illustrative purposes only. Please see the 2020 Prox y Voting Policy on our website for additional information and case studies.

FOR CLIENT USE ONLY. NOT FOR USE AND/OR DISTRIBUTION TO YOUR CLIENTS OR THE GENERAL PUBLIC

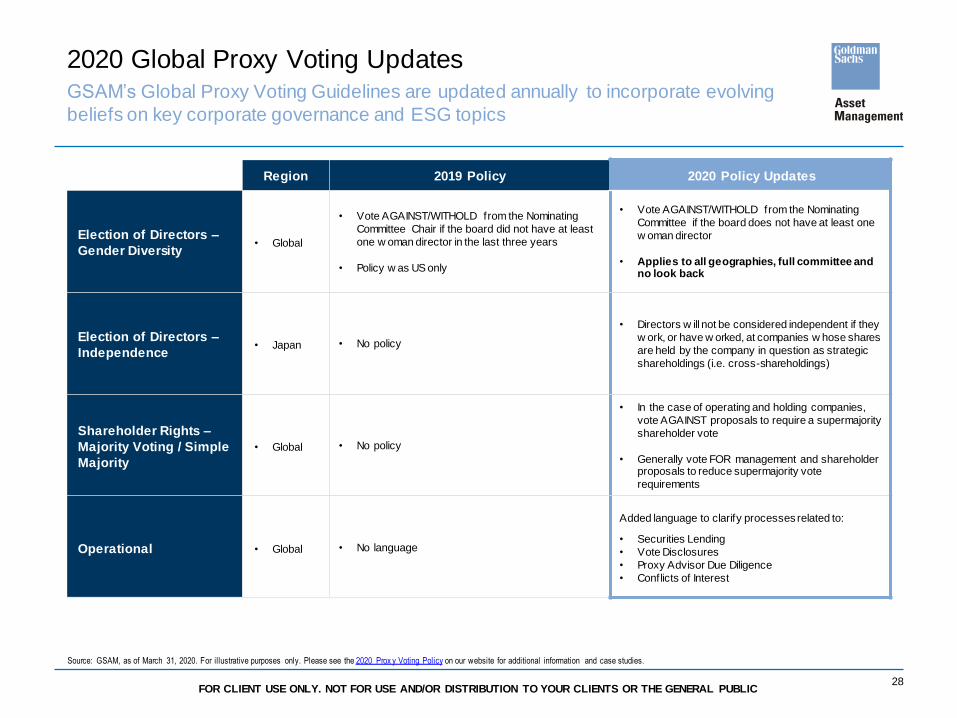

2020 Global Proxy Voting Updates GSAM’s Global Proxy Voting Guidelines are updated annually to incorporate evolving

beliefs on key corporate governance and ESG topics

Region 2019 Policy 2020 Policy Updates

Election of Directors –

Gender Diversity • Global

• Vote AGAINST/WITHOLD from the Nominating

Committee Chair if the board did not have at least

one w oman director in the last three years

• Policy w as US only

• Vote AGAINST/WITHOLD from the Nominating

Committee if the board does not have at least one

w oman director

• Applies to all geographies, full committee and no look back

Election of Directors –

Independence • Japan • No policy

• Directors w ill not be considered independent if they

w ork, or have w orked, at companies w hose shares

are held by the company in question as strategic

shareholdings (i.e. cross-shareholdings)

Shareholder Rights –

Majority Voting / Simple

Majority

• Global • No policy

• In the case of operating and holding companies,

vote AGAINST proposals to require a supermajority

shareholder vote

• Generally vote FOR management and shareholder proposals to reduce supermajority vote

requirements

Operational • Global • No language

Added language to clarify processes related to:

• Securities Lending

• Vote Disclosures

• Proxy Advisor Due Diligence

• Conflicts of Interest

29

This material is prov ided at y our request f or inf ormational purposes only and should not be construed as inv estment adv ice or an of f er or solicitation to buy or sell securities.

The portf olio risk management process includes an ef f ort to monitor and manage risk, but does not imply low risk. Opinions ex pressed are current opinions as of the date appearing in this

material only .

This inf ormation discusses general market activ ity , industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or inv estment

adv ice. This material has been prepared by GSAM and is not f inancial research nor a product of Goldman Sachs Global Inv estment Research (GIR). It was not prepared in compliance with

applicable prov isions of law designed to promote the independence of f inancial analy sis and is not subject to a prohibition on trading f ollowing the distribution of f inancial research. The v iews and

opinions expressed may dif f er f rom those of Goldman Sachs Global Inv estment Research or other departments or div isions of Goldman Sachs and its af f iliates. Inv estors are urged to consult with

their f inancial adv isors bef ore buy ing or selling any securities. This inf ormation may not be current and GSAM has no obligat ion to prov ide any updates or changes.

Views and opinions expressed are f or inf ormational purposes only and do not constitute a recommendation by GSAM to buy , sell, or hold any security . Views and opinions are current as of the

date of this presentation and may be subject to change, they should not be construed as inv estment adv ice.

Ref erences to indices, benchmarks or other measures of relativ e market perf ormance ov er a specif ied period of time are prov ided f or y our inf ormation only and do not imply that the portf olio will

achiev e similar results. The index composition may not ref lect the manner in which a portf olio is constructed. While an adv iser seeks to design a portf olio which ref lects appropriate risk and return

f eatures, portf olio characteristics may dev iate f rom those of the benchmark.

This material contains inf ormation that discusses general market activ ity , industry or sector trends, or other broad-based economic, market or political conditions. It also pertains to past

perf ormance or is the basis f or prev iously -made discretionary inv estment decisions. This inf ormation should not be construed as a current recommendation, research or inv estment adv ice. It

should not be assumed that any inv estment decisions shown will prov e to be prof itable, or that any inv estment decisions made in the f uture will be prof itable or will equal the perf ormance of

inv estments discussed herein. Any mention of an inv estment decision is intended only to illustrate our inv estment approach and/or strategy , and is not indicativ e of the perf ormance of our

strategy as a whole. Any such illustration is not necessarily representativ e of other inv estment decisions.

This material has been prepared by GSAM and is not f inancial research nor a product of Goldman Sachs Global Inv estment Research. It was not prepared in compliance with applicable

prov isions of law designed to promote the independence of f inancial analy sis and is not subject to a prohibition on trading f ollowing the distribution of f inancial research. The v iews and opinions

expressed may dif f er from the v iews and opinions expressed by Goldman Sachs Global Inv estment Research or other departments or div isions of Goldman Sachs and its af f iliates. Inv estors are

urged to consult with their f inancial adv isors bef ore buy ing or selling any securities. This inf ormation should not be relied upon in making an inv estment decision. GSAM has no obligation to

prov ide any updates or changes.

Portf olio holdings and/or allocations shown abov e are as of the date indicated and may not be representativ e of f uture inv est ments. The holdings and/or allocations shown may not represent all

of the portf olio's inv estments. Future inv estments may or may not be prof itable.

Env ironmental, Social, and Gov ernance (“ESG”) strategies may take risks or eliminate exposures f ound in other strategies or broad market benchmarks that may cause perf ormance to div erge

f rom the perf ormance of these other strategies or market benchmarks. ESG strategies will be subject to the risks associated with their underly ing inv estments’ asset classes. Further, the demand

within certain markets or sectors that an ESG strategy targets may not dev elop as f orecasted or may dev elop more slowly than anticipated.

Disclosures

FOR CLIENT USE ONLY. NOT FOR USE AND/OR DISTRIBUTION TO YOUR CLIENTS OR THE GENERAL PUBLIC

30

Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as

up. A loss of principal may occur.

Personnel inv olv ed in the GSAM ESG and impact ("Imprint") ef f ort are comprised of members of our GSAM Quantitativ e Strategies , Fundamental Equity , Fixed Income, and Alternativ e

Inv estments and Manager Selection (AIMS) teams which are distinct groups. An inf ormation barrier exists between GSAM teams that manage internal strategies and external ("open architecture")

strategies. AIMS Imprint is a part of the Alternativ e Inv estments and Manager Selection (AIMS) Group. The AIMS business is self -contained within its own inf ormation barrier within GSAM.

Unless operating under an exception granted by Legal and/or Compliance, AIMS personnel cannot conv ey or receiv e conf idential inf ormation about third party managers (whether or not material)

to or f rom other businesses. In addition, Goldman Sachs policy absolutely prohibits: (a) the communication of any conf idential inf ormation acquired in the course of carry ing out f irm business to

any one (including other Goldman Sachs personnel) except those hav ing a need to know the inf ormation in connection with that business; and (b) the use of such conf idential inf ormation in

connection with any securities transaction that is unrelated to the transaction(s) f or which the inf ormation was intended to be used.

This is marketing material.

This is marketing material f or f inancial instruments.

This document is prov ided to y ou by Goldman Sachs Bank AG, Zürich. Any f uture contractual relationships will be entered into with af f iliates of Goldman Sachs Bank AG, which are domiciled

outside of Switzerland. We would like to remind y ou that f oreign (Non-Swiss) legal and regulatory sy stems may not prov ide the same lev el of protection in relation to client conf identiality and data

protection as of f ered to y ou by Swiss law.

In the United Kingdom, this material is a f inancial promotion and has been approv ed by Goldman Sachs Asset Management International, which is authorized and regulated in the United Kingdom

by the Financial Conduct Authority .

Confidentiality

No part of this material may , without GSAM’s prior written consent, be (i) copied, photocopied or duplicated in any f orm, by any means, or (ii) distributed to any person that is not an employ ee,

of f icer, director, or authorized agent of the recipient.

Although certain inf ormation has been obtained f rom sources believ ed to be reliable, we do not guarantee its accuracy , completeness or f airness. We hav e relied upon and assumed without

independent v erif ication, the accuracy and completeness of all inf ormation av ailable f rom public sources.

© 2020 Goldman Sachs. All rights reserv ed.

Compliance Code: 213315-OTU-1250032

Additional Disclosures

FOR CLIENT USE ONLY. NOT FOR USE AND/OR DISTRIBUTION TO YOUR CLIENTS OR THE GENERAL PUBLIC