government and growth francesco daveri. outline some facts theory empirics digging deeper: kneller,...

TRANSCRIPT

Government and Growth

Francesco Daveri

Outline

Some facts

Theory

Empirics

Digging deeper: Kneller, Bleaney and Gemmell

(1999)

Conclusions

Common secular trend towards Bigger Government

Big Government: bad for growth?

Not necessarily

Public good provision (rule of law) enhances factor accumulation …

… and efficiency

.. But taxes discourage market activities

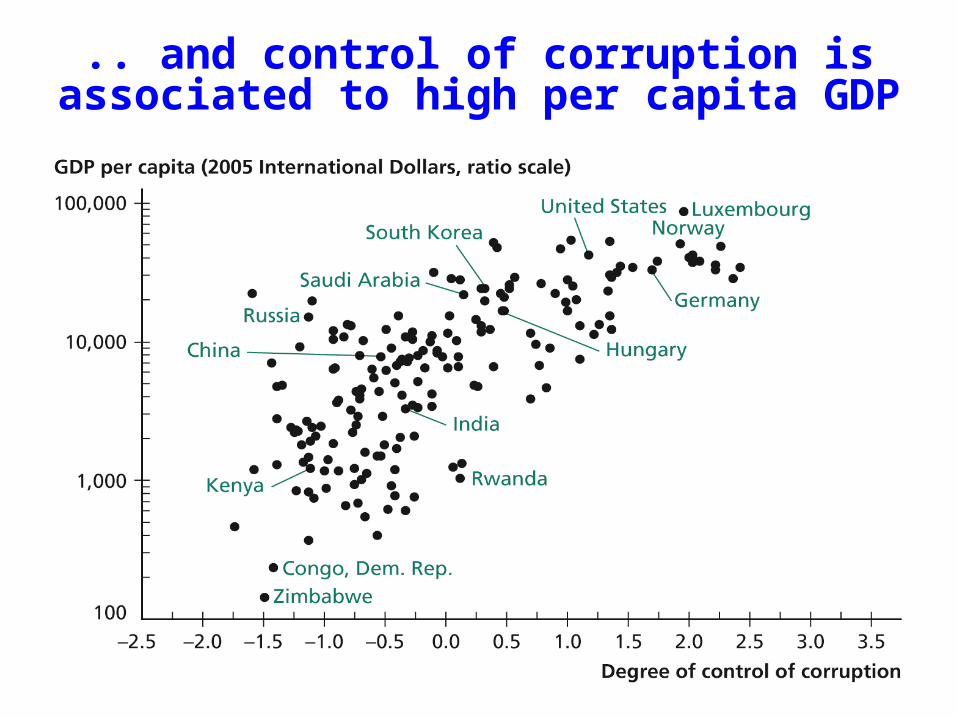

.. and control of corruption is associated to high per capita GDP

Theory: summing upSome Govt-related items affect growth:• Public goods (Productive expenditure) good

for growth• Distorting taxation bad for growth

… while some others are irrelevant for growth:• Non-distorting taxes (citizen tax)• Unproductive expenditure (if financed with non-

distorting taxes)

MAIN MESSAGE: composition of spending and taxation matters

Empirical caseIs the empirical case as apparent as the theoretical

case ? Not really, unfortunately• Barro (1991, 1997)

– public consumption (Gov’t spending minus defense minus education) negatively related to growth.

– Spending in public goods not robustly correlated with growth

• Koester- Kormendi (1989), Easterly-Rebelo (1993): – taxes unrelated to growth along cross-sectional

dimension• Stokey-Rebelo (1995)

– taxes unrelated to growth along time series dimension in the US

Issue: how to measure tax ratesQuestion: by how much is growth rate affected as Gov’t varies

tax rates?• Statutory marginal tax rates

– Rarely used in cross-country growth regressions for they are awkward to compute and update

– Moreover, nominal tax rates often different from effective tax rates

• Tax-to-GDP ratios– Marginal tax rate matters in theory; we only observe average– T/GDP = (T/tax base) * (tax base/GDP). Hence, tax-GDP ratios

may change independently of Gov’t action if income distribution varies

• Average effective tax rates (AETR)– Best available indicators: T / (tax base). – Computed for capital and labor incomes as well as consumption.

What if effective rates used?• Easterly and Rebelo (EER, 1993), AETR

for 40 countries– No detected link with growth

• Mendoda, Razin and Tesar (JME, 1994), AETR for 14 Industrial countries. Updated by DAveri and Tabellini (Economic Policy, 2000)

– Weak link with growth

Other methodological issues

• Gov’t spending in public goods may not reflect effective provision

• ‘Tax systems’ are hardly comparable, for tax structures, degree of enforcement and tax bases vary wildly across countries

• Kneller-Bleaney-Gemmell (KBG, 1999): most studies focus on just one side of the budget. Both sides should be included to avoid biasing results.

KBG (1999)Put the Govt budget constraints in the growth

regression!

Problem: if append spending, taxes and deficit variables

perfect collinearity among fiscal regressors

… so?

Leave out one fiscal variable … which one???

Theory helps: eliminate a “non-affecting growth item” to avoid the omitted variable problem

KBG (1999)

Growth= c+ j=1,..,m jXij + dcontrols + error

…eliminate the mth variable:

Growth= c+ j=1,..,(m-1) jXij + dcontrols + error

KBG (1999) if the m variable is omitted:

Growth= c+ + d controls+ errors

• the null:

• coeff meaning: effect of a unit change in the relevant variable offset by a unit change in the omitted category

the implicit financing element is the mth

Data

22 developed countries

Annual data 1970-1995 five-year avarages to remove the

effects of business cycle

KBG regression results

KBG regression results

Non distorting taxation (rndis) and non productive spending (enprd): hypothesis of same coefficient not rejected

Productive expenditure (eprd): positive and significant coefficient

Distorting taxation (rdis) : negative and significant coefficient

Budget surplus (sur): positive and significant coefficient

Mis-specifying the Budget Constraints

A correct specification of the Government budget constraint is important for interpreting fiscal parameters

• Including tax rates without budget deficit biases estimated coefficient toward zero if tax cuts financed in deficit

Conclusion Impact of fiscal policy on growth depends on the

structure of taxation and expenditure

Non productive expenditure and non-distorting taxation have a zero impact on growth

Productive expenditure has a positive effect on growth if financed by non distortionary taxation

Distorting taxation has a negative effect on growth