government of karnataka - · pdf filestate finance commission’s (sfcs) ... introduction...

TRANSCRIPT

Government of Karnataka

Report:

URBAN LOCAL BODIES IN KARNATAKA:

STRUCTURE AND FINANCES

Center for Financial Accountability and Decentralization

Fiscal Policy Institute

Kengeri, Bengaluru-60

December, 2016

ii

iii

TABLE OF CONTENTS

Abstract ii

Executive Summary iii

List of Chapters v

List of Tables vi

List of Illustrations vi

List of Appendices vi

List of Abbreviations vii

iv

ABSTRACT

Karnataka is one of the fastest urbanizing States in India with the urban population constituting

nearly 39% of the total population. In the background of high urbanization there is also a need

for high investments in urban infrastructure to deliver the basic and obligatory services. Urban

Local Bodies (ULBs) has an important role to play in meeting these requirements. This study

makes an attempt to review the financial status of ULBs in Karnataka. The study finds that own

tax revenue sources of ULBs are not even contributing 20% of the total revenues and ULBs

are dependent on the transfers from the Centre and State Government. At the same time, it was

noticed that only 38% of 13th Finance Commission’s general grants released are being utilized

by the ULBs. Many of the Municipal Corporations in Karnataka are showing surplus in their

accounts and this scenario is mainly owing to grants they are receiving from the Centre and

State Government’s new urban development initiatives such as AMRUT, Smart Cities Mission

& Nagorothana Scheme. Present level of ULBs expenditure in Karnataka is not even covering

one-third of required investments. In the context of huge infrastructural investment

requirements and budget constraints, ULBs have to raise the needed capital through Public

Private Partnership and Bond Financing approach. It is difficult for lower tier of ULBs to reach

the bond markets and hence this study suggests to strengthen the system of ‘Pooled Financing’

and advocates that the Government take an initiative to form an ‘Organization’ which could

approach and raise funds from the bond market and allocate the same for participating ULBs.

v

EXECUTIVE SUMMARY

As per the 2011 Census, Urban population in Karnataka constitutes nearly 39% of the total

population and it is expected to reach 44% by 2021. Karnataka, being the 5th most urbanized

State in India, has to invest more on urban infrastructure to meet the basic requirements of

urban population. Governance of urban areas lies under the Urban Local Bodies and their role

becomes vital in the context of rapid urbanization.

Decentralized structure in India got strengthened with the 73rd and 74th amendment of the

Indian Constitution. With these amendments many of the functional and administrative

responsibilities have been assigned to local bodies. In Karnataka, ‘The Karnataka

Municipalities Act, 1964’ governs the City Municipal Councils and Town Municipal Councils

and ‘Karnataka Municipal Corporation Act, 1976’ governs Municipalities.

As per Article 280(3) of Indian Constitution, Central Finance Commissions (CFCs) have to

recommend measures to augment the consolidated fund of the State Governments based on

State Finance Commission’s (SFCs) report. However, CFCs have complained about untimely

submission of SFC reports, the quality of the reports and severe data problem faced by SFCs.

In order to solve these issues, CFCs have kept aside a lump sum grant to address the data

problem. However, despite these initiatives the problem of data availability still persists. CFCs

primarily adopted two criteria namely area and population for fund devolution to States and in

addition, other important criteria like devolution index, revenue efforts, decentralization index

etc have also been used. Karnataka Government has constituted three SFCs till now and fourth

SFC is constituted recently and is yet to submit its report. SFCs have to make recommendations

to Governor of the State regarding devolutions to local bodies.

Review of ULBs finances in Karnataka reveals that own tax revenue source of ULBs are just

around 20% of total revenue. This scenario is exactly the opposite in several countries like

Canada, where share of own tax revenue constitutes more than 80% of the total revenue. It

implies that ULBs in Karnataka are highly dependent on transfers from the upper level of

Government. Property tax is the major source of tax revenue but collections vary across tiers

of ULBs. It was observed that, in recent years, major share of grants from State Government is

being transferred to city corporations. This trend reveals the emerging need for higher spending

to address the problem of urban agglomeration. Surprisingly, it was found that only 48% of the

released general grants by 13th Finance Commission is being utilized by the ULBs. Utilization

is critical even with regard to performance grants.

vi

Expenditure on salaries and wages and maintenance tops the spending list of ULBs followed

by capital spending. Interestingly, it was observed that all the city corporations, excepting a

few show surplus in their budget and also have remarkable closing balances. This scenario is

mainly owing to extraordinary receipts which they are receiving from the higher levels of

Government. The extraordinary receipts mainly consist of grants from Central and State

Governments for implementation of new urban development initiatives namely AMRUT

scheme, Smart City project and Nagarothana scheme. Extraordinary receipts constitute nearly

30% of total receipts of the city corporations.

It was observed that with the present level of spending by the ULBs it would be difficult to

meet the urban infrastructural requirements. An exercise undertaken in the present study to find

out the required investments by the ULBs (mostly for the urban infrastructure development)

revealed that actual spending is just around 30% of required investments. In the context of huge

infrastructural investment requirements and budget constraints, ULBs have to raise the needed

capital through Public Private Partnership and Bond Financing approach. It will be difficult for

lower tier of ULBs to reach the bond markets and hence this study suggests to strengthen the

system of ‘Pooled Financing’ and advocates the Government to take the initiative to form an

‘Organization’ which could approach and raise funds from the bond market and allocate the

same for participating ULBs.

vii

List of Chapters

Chapter-1: Introduction 1 - 5

1.1 Constitutional Amendments and Local Bodies 1 - 2

1.2 Constitutional Amendments and Developments in Karnataka 2 - 5

1.2.1 The Karnataka Municipalities Act, 1964 2 - 4

1.2.2 The Karnataka Municipal Corporation Act, 1976 4 - 5

Chapter-2: Finance Commissions 6 - 13

2.1 Central Finance Commissions 6 - 11

2.1.1 Criteria adopted by Finance Commissions for Distribution of Grants 9 - 11

2.2 State Finance Commissions 11 - 13

2.2.1 SFC Devolution Criteria 12 - 13

Chapter-3: Urban Local Bodies Structure in Karnataka 23 - 25

3.1 Urbanization in Karnataka 23 - 24

3.2 Structure of ULBs 24 - 25

Chapter-4: Finances of Urban Local Bodies in Karnataka 26 - 38

4.1 Revenues of ULBs: Own Source, Transfers and Grants 26 - 30

4.2 Expenditure of ULBs 31- 32

4.3 Finances of Select Municipal Corporations 32 - 33

4.4 Urban Development: Recent Initiatives 34 - 35

4.5 Urban Infrastructure: Current Status and Required Investments 35 - 38

Chapter-5: Conclusion 39 - 40

Bibliography 41 - 42

Appendix 43 - 44

viii

List of Tables

2.1 Parameters for Finance Commission Grants Distribution amongst the States 10

2.2 Indicators of Devolution of Resources to ULBs 13

3.1 Classification of Towns in Karnataka 16

4.1 Revenue Composition of ULBs 17

4.2 Detailed Description of Revenue Sources of ULBs 18

4.3 Grant Transfers from State to ULBs 20

4.4 Grants Released as a % of Budgeted Transfers 20

4.5 Share of State Government Grants to Tiers of ULBs 20

4.6 13th Finance Commission Grants to ULBs in Karnataka 21

4.7 Grants Allotted for ULBs from 14th Finance Commission 22

4.8 Detailed Item Wise Expenditure of ULBs 23

4.9 Financial Position of Municipal Corporations 25

4.10 Fund Sharing Pattern for AMRUT Mission in Karnataka 26

4.11 Sector wise Allocation for the AMRUT Mission in Karnataka 26

4.12 Financing Gap in Urban Infrastructure 38

List of Illustrations

3.1 Decadal Growth of Urban Population 14

3.2 Level of Urbanization in India & Karnataka 15

4.1 Transfers to ULBs as a % to Revenue Expenditure of State Government 19

4.2 Plan & Non-Plan Transfers to ULBs from the State Government 19

4.3 Item Wise Expenditure of ULBs in Karnataka 22

4.4 Major Components of Receipts and Payments of Municipal Corporations 24

List of Appendices

1 Projections on Upgradation of Lower Tiers of ULBs 35

ix

List of Abbreviations

AMRUT: Atal Mission for Rejuvenation and Urban Transformation

BBMP: Bruhat Bengaluru Mahanagara Palike

CAG: Comptroller and Auditor General

CARE: Credit Analysis and Research Limited

CFC: Central Finance Commission

CMCs: City Municipal Corporations

FIRE-D: Financial Institution Reform and Expansion

GDP: Gross Domestic Product

GSDP: Gross State Domestic Product

HPEC: High-Powered Expert Committee

KFRA: Karnataka Fiscal Responsibility Act

NIPFP: National Institute of Public Finance and Policy

PCI: Per Capita Income

PPP: Public Private Partnership

PRI: Panchayat Raj Institutions

SAAP: State Annual Action Plan

SFC: State Finance Commission

TMCs: Town Municipal Corporations

TPs: Town Panchayats

ULBs: Urban Local Bodies

1

CHAPTER- 1

INTRODUCTION

Karnataka is one of the progressive States in India with consistent growth performance. The

sectoral composition of the State’s economy is moving towards the service sector, which

accounts for around 59% of total Gross State Domestic Product (GSDP). However, dependency

on primary sectoral occupation is still higher. As far as the fiscal indicators of the State are

concerned, all the deficit indicators are well within the prescribed limit. In fact, Karnataka was

the first State to enact Fiscal Responsibility Act in the year 2002, much ahead of the Union

Government. With wide ranging fiscal reforms, there were significant changes in the fiscal

scenario of State in terms of reduction in deficits, increase in capital expenditure and decline

in capital receipts.

With economic development, nations progressively become more and more urbanized.

Karnataka is not an exception to this scenario. Urban population accounted for 33.99% of the

total population of the State in 2001 which increased to 38.7% in 2011 with the decadal growth

in urban population being 31.5%. In comparison, rural population has grown by only 7.4%

between 2001 and 2011. Available projections indicate that urban population would account

for 43.6% by the year 2021 (GoK, 2013). Given these facts, higher investments in urban

infrastructure and governance to meet the upcoming needs are of utmost importance. In these

circumstances, role of Urban Local Bodies (ULBs) in meeting these needs becomes prominent.

1.1 Constitutional Amendments and Local Bodies:

The 73rd and 74th Amendment to the Constitution of India in 1992 paved the way for

strengthening of decentralized structure in India by providing special powers to local bodies.

The 73rd amendment relates to rural local bodies (Panchayat Raj Institutions) while the 74th

amendment of constitution refers to ULBs. In order to improve the performance and

accountability of local bodies, an attempt was made by these amendments to include important

functions like devolution of financial and administrative responsibilities to the third tier of

Governments, thereby paving the way for fiscal federalism (Singh & Singh, 2015).

Prior to the 74th Amendment, ULBs were not able to perform effectively due to inadequate

devolution of powers and functions. However, 74th Amendment has provided a firm

relationship between State Government and ULBs with respect to functions and taxation

powers, revenue sharing, conduct of elections, representation for weaker sections of the society

etc. 74th Amendment constituted three types of Municipalities, namely:

2

1. Nagar Panchayats – areas of transition from rural to urban

2. Municipal Council- smaller urban area

3. Municipal Corporations- larger urban area

Soon after the 74th Amendment to the Constitution, many of the State Governments in India

have taken steps to implement the recommendations and established ULBs. All States except

Jharkhand and Pondicherry have conducted elections to the local bodies (GoI, 2016). It was

required of all the State Governments to review the existing municipal laws to be consistent

with 74th Amendment as per Article 243ZE of the Indian Constitution.

1.2 Constitutional Amendments and Developments in Karnataka:

1.2.1 The Karnataka Municipalities Act, 1964

The city municipal councils and town municipal councils are governed by “The Karnataka

Municipalities Act, 1964”. Prior to this enactment, municipal councils in the State were

governed by seven different enactments in different areas and in order to have uniformity in

law, this Bill was legislated.

Salient Features

Town Panchayats

1. The Town Panchayats are transitional areas which are constituted based on set

following criteria:

a. Population (10000 – 20000)

b. Density of Population (not less than 400 per square kilometer)

c. Occupation (not less than 50% of population should be non-agriculturists)

2. Constitution

a. Consists of directly elected councilor (number of councilors are prescribed

based on population of Transitional area)

b. Nominated members (not more than three, they should be experienced and have

knowledge of administration)

c. Members of House of People and State Legislative Assembly pertaining to the

transitional area

d. Members of Council of States and State Legislative Council pertaining to the

transition area

3

City Municipal Councils or Town Municipal Councils

1. Constitution

a. Elected members (Number of councilors are prescribed based on Population of

Municipal area)

b. Five Government nominated members

c. Local Member of Legislative Assembly and Member of Parliament

d. Reservation (Representation for Scheduled Caste and Scheduled Tribes based

on their population and 1/3rd of the seats are reserved for women)

2. Constitution of Standing Committees for the following

a. Taxation, finance and appeals

b. Public health, education and social justice

c. Town planning and improvement

d. Accounts

3. Municipal Property (Can acquire and hold both movable and immovable property for

the purpose of this Act)

4. Municipal Funds (Consists of all money received by or on behalf of municipal council

by virtue of this Act)

5. Municipal Funds can be applied for the purpose specified in the Act

6. Municipals have powers to deposit, invest & borrow money

7. Municipal Taxation

a. Property Tax (Buildings or vacant lands or both within the Municipal area with

some exception)

b. Duty on transfers of immovable property

c. Tax on advertisements

8. Municipal Accounts and Administrative Reports

a. Prohibition of expenditure not budgeted for

b. Presentation of Accounts- Commissioner shall submit to Municipal council a

detailed budget stating estimation of income and expenditure for ensuing year

with in 15th January of every year. It also should include actual and expected

receipts and expenditure for the official year till 31st March.

c. Maintenance of accounts and restrictions on expenditure as per the rules

d. Accounts should be audited by recognized auditor at least once in a year. The

audit report may sent to certain officers and bodies as Government may direct.

4

e. Annual Administration Report should be submitted to the Director of Municipal

Administration and Government every year

f. Development Plan should be prepared and submitted District Planning Committee

every year

g. Finance Commissions constituted by Government will review financial position

and make recommendations

9. Control- Director of Municipal Administration will be the chief controlling authority.

10. Rules and Bye-Laws- Government by notification may make rules and bye-laws

1.2.2 Karnataka Municipal Corporation Act, 1976

All Municipal corporations except Bruhat Bengaluru Mahanagara Palike (BBMP) are governed

in the State of Karnataka by the “Karnataka Municipal Corporation Act, 1976”. Municipal

governance in BBMP is facilitated directly by the Government of Karnataka. Municipal

corporations are for the larger urban areas. The salient features of Karnataka Municipal

Corporation Act, 1976 are as follows:

1. Specification or Establishment of Corporation

a. Population (not less than three lakh)

b. Density of Population (not less than three thousand inhabitants per square km)

c. Revenue generation (revenue generation of not less than six crore in the year of

last preceding census or rupees two hundred per capita per annum)

d. Employment in non-agriculture sector should not be less than 50% of total

employment.

2. Constitution of Corporation

a. Elected members

b. Government nominees (not more than five)

c. Members of Parliament, Members of Legislative Assembly, Members of Council

of State and Members of State legislative Councils representing the city or part of

the city.

d. Not less than 1/3rd of the seats should be reserved for Scheduled Caste, Scheduled

Tribes and Other Backward Class people.

e. Formation of Standing Committee and Ward Committee

3. Obligatory Functions of the Corporation

a. Solid waste management

b. Construction, maintenance and cleaning of drainage

5

c. Public lighting

d. Maintenance of corporation office, public monuments, public markets etc

4. Taxation

a. Property Tax (Buildings or vacant lands or both within the Municipal area with

some exception. Percent of levy should be less than 0.3% and not more than 0.6%

of the capital value of the property)

a. Duty on transfers of immovable property

b. Tax on advertisements

c. Water supply Cess

d. Levy of infrastructure and solid waste management cess

5. Finance, Accounts and Audit

a. Accounts of all receipts and expenditure of the corporation shall be kept in

prescribed manner

b. The Government shall appoint one of its officer as Corporation Chief Auditor to

conduct auditing of the Corporation finances.

c. Corporation have powers to borrow money with certain pre-conditions

6

CHAPTER-2

FINANCE COMMISSIONS

2.1 Central Finance Commissions

There has been considerable progress in the empowerment of Panchayat Raj institutions and

Municipalities in India after the constitutional amendments. 10th Finance Commission first

made the provision for explicitly supporting local bodies through grants (GoI, 2009). Under

article 280 (3), the Finance Commission has the responsibility to make recommendations to

the President of India regarding the “measures needed to augment the consolidated fund of a

State” once the recommendations of State Finance Commissions (SFCs) become available to

it (GoI, 1994). As the SFC reports were not available at that time, 10th Finance Commission

did not make any recommendation. However, it recommended lump sum grant of Rs. 1000

crore for ULBs to meet their primary obligations.

Timely submission of the State Finance Commission reports are crucial for accomplishment of

Central Finance Commission Grants. Both Eleventh Finance Commission and Twelfth Finance

Commission have recommended grants on an ad hoc basis due to non-furnishing of data by

States as well as the SFC reports in order to provide required funds based on proper estimation.

Eleventh Finance Commission earmarked that released funds should be used for operation and

maintenance of core civic services like education, health, drinking water, street lighting and

sanitation and should not be used for payment of salaries and wages. With the intention of

removing data constraints, the Eleventh Finance Commission set apart grants of Rs 98.6 crore

for maintenance of accounts and Rs 200 crore for creation of database of Finances of local

bodies. Unfortunately, only 30% of the money allocated for creation and maintenance of the

data base was utilized (GoI, 2004). Twelfth Finance Commission also noted the importance of

maintaining data bases of local bodies and urged that part of the grants sanctioned should be

earmarked by State Governments for this purpose. The Twelfth Finance Commission

recommended an amount of Rs. 5000 crore for ULBs across India and stipulated that at least

50% of grants provided should be assigned for solid waste management through Public Private

Partnership (PPP).

The Twelfth Finance Commission also made number of recommendations with regard to the

constitution, composition, mode and methodology of working of State Finance Commissions

which aimed at improving their functioning (GoI, 2009).

7

Main recommendations made by Twelfth Finance Commission regarding SFCs were as

follows:

1. The States should avoid delays in constitution of SFCs, submission of reports. It is

desirable to constitute SFCs at least two years before the required date of

submission.

2. SFCs reports should be readily available for Central Finance Commission.

3. SFCs should follow similar format and procedure for data acquisition as well as

report writing as adopted by Finance Commission.

4. SFCs should be constituted with people of eminent, qualified and experienced in

relevant fields.

5. The convention established at national level of accepting principal recommendation

should be followed by SFCs.

6. It is desirable to follow the procedure adopted by Central Finance Commissions to

transfers resources from Centre to States while transferring resources to local

bodies.

7. While estimating the resources of local bodies, SFCs should follow a normative

approach in the assessment of revenues and expenditure rather than make forecasts

based on historical trends.

8. A permanent SFC cell may be created under Finance Departments of respective

States.

While Twelfth Finance Commission relaxed many stipulated conditions for the States in

drawing grants, it made providing Utilization Certificates for previous instalments a must for

further transfers. Despite such a liberal approach few States were not able to draw down the

grants (GoI, 2009).

In a memorandum to Thirteenth Finance Commission, Ministry of Urban Development

contended that combined expenditure of ULBs shrank from 1.74% of GDP in 1998-99 to

1.54% in 2007-08. Own resource did not cover even 50% of required expenditure while

transfers (as significant part of it was tied and discretionary) are not adequate to meet the

expenditure which increased significantly due to implementation of the Sixth Pay Commission

recommendations, additional operation and maintenance costs due to larger investments in

civic infrastructure and additional investment necessary for improving the accounting system,

computerization of operations, tax administration and project monitoring (GoI, 2009). It also

8

added that previous Central Finance Commissions (CFCs) have adopted an ad hoc approach in

releasing funds to local bodies and the quantum is also low.

Thirteenth Finance Commission claimed that the data provided to the Commission varied in

quality across States. It was inconsistent with the data provided by earlier Finance

Commissions. Quality, scope and analysis of submitted SFC reports were widely divergent

(GoI, 2009). As per Article 243-I of the Indian Constitution, SFCs should be appointed on the

expiration of every fifth year with the intention that all the transfers to local bodies from the

Government to be governed by mandate of current SFC. The mandate is applicable only for

period of five years and should not be extended. In contrast, it was observed by Thirteenth

Finance Commission that in one of the States, SFC report for the period 2005-06 to 2009-10

was submitted as late as 31st March 2009. Thirteenth Finance Commission urged the need of

synchronizing the period covered by SFCs with Central Finance Commissions.

Thirteenth Finance Commission recommended grants under heads of ‘general basic grants’

‘general special area basic grants’ ‘general performance grants’ and ‘general special area

performance grants’. State Governments would be eligible for drawing the general

performance grants if they complied with following conditions:

1. A supplement of budget document be prepared by State Governments showing details

of Plan and non-Plan wise classification of transfers separately for all categories of

ULBs from major head to object head. It should indicate details of funds transferred

directly to local bodies outside State Government’s Budget.

2. State Government must put in place an audit system for local bodies.

3. State Government must put in place a system of independent local body ombudsmen

who will look into complaints of corruption and maladministration against the

functionaries of local bodies.

4. The State Government must put in place a system to electronically transfer local body

grants provided by the Finance Commission to the respective local bodies within five

days of their receipt from Central Government.

5. State Government must prescribe through an Act the qualification of persons eligible

for appointment as members of SFC.

6. All local bodies should be fully enabled to levy property tax and any hindrance in this

regard must be removed.

9

7. State Government must put in place a State level Property Tax Board, which will assist

all municipalities and municipal corporations.

8. Municipalities and Municipal Corporations’ service standards for four services water

supply, sewerage, storm water drainage and solid waste management to be notified by

State Government.

9. All municipal corporations with a population of more than 1 million (2001 census)

should put in place a fire hazard response and mitigation plan for their respective

jurisdictions.

Fourteenth Finance commission too could not base their recommendation entirely on SFCs

reports due to variations in approaches adopted by SFCs, difference in periods covered, non-

synchronization of SFC report period with that of Central Finance Commission and quality of

SFC reports (GoI, 2015). SFCs have pointed out to Fourteenth Finance Commission that there

is lack of coordination between the Finance Department and those dealing with the Rural and

Urban Affairs which hinders the implementation of measures for augmentation of resources

suggested by the SFCs.

It was decided by the Fourteenth Finance Commission to disburse the grants under two heads

namely basic grants and performance grants. Basic grants constitute 80% of total grants and

remaining 20% would be performance grants for ULBs. It was suggested that a detailed

procedure for the disbursal of the performance grant to ULBs be designed by the State

Government concerned, subject to certain eligibility criteria. To be eligible, ULBs should

furnish the following.

1. Submit audited annual accounts that relate to a year not earlier than two years preceding

the year in which it seeks to claim performance grants.

2. It will also have to show an increase in own revenues over the preceding year, as

reflected in these audited accounts.

3. It must publish the service level benchmarks relating to basic urban services each year

for the period of the award and make it publically available. The service level bench

marks of Ministry of Urban Development may be used for this purpose.

2.1.1 Criteria adopted by Finance Commissions for Distribution of Grants

Population and geographical area are two parameters which were adopted by all the Finances

commissions starting from Eleventh to Fourteenth Finance Commissions. Eleventh Finance

Commission has constructed an index of decentralization and assigned weight of 20% (refer

10

Table-2.1). The index was constructed considering ten parameters broadly relating to the

implementation aspects of the 73rd and 74th Amendments of the constitution by local bodies.

The Twelfth Finance Commission gave a weight of 20% for revenue efforts of the States and

10% for Index of Deprivation. This index was constructed based on data relating to minimum

needs of the people namely, percentage of households fetching water from distance, percentage

of the population without latrine and percentage of population without drainage.

Table-2.1

Parameters for Finance Commission Grants Distribution amongst the States

Sl.

No

Parameters 11th Fin Com 12th Fin Com 13th Fin Com 14th Fin Com

1 Population 40% 40% 50% 90%

2 Distance from Higher PCI

a. Distance from higher

Per Capita Sectoral

Income

20% 20%

20%

-

3 Revenue Efforts

a. Rev Efforts with

respect to State Govt’s

Own Rev

b. Rev Efforts with

respect to GSDP of the

State

10%

10%

10%

- -

4 Geographical Area 10% 10% 10% 10%

5 Index of Decentralisation 20% - -

6 Index of Deprivation - 10% - -

7 Index of Devolution - - 15% -

8 Fin Com Local body Grants

Utilisation Index

- - 5% -

Source: Central Finance Commission Reports

It was found by the Thirteenth Finance Commission that significant proportion of grants has

not been drawn by the ULBs and hence it included index of Finance Commission grants

utilization as a parameter for disbursement of grants. The state wise devolution index was

constructed based on amount transferred to ULBs from States own revenue sources adjusting

for population and it was assigned a weight of 15%.

Apart from adopting these criteria, the Fourteenth Finance Commission retained population

and geographical area as parameters for grant devolution. Commission noted that there are

practical differences in considering appropriate indices for devolution and even assuming an

index, it is difficult to measure actual level of devolution to optimal level due to unavailability

11

of accurate data. Under the Constitution, only State Legislature has discretion to assign

functions to local bodies. As neither the Terms of Reference to Finance Commission nor Indian

Constitution permit the Finance Commission to play any role in devolution of powers to local

bodies, Fourteenth Finance Commission considered it appropriate not to use an index of

devolution or decentralization for the purpose of transfers of resources to local bodies. Thus,

the Commission recommended transfers based on population and area parameter by giving

weight of 90% and 10% respectively.

2.2 State Finance Commissions

Article 243I and 243Y of the Indian Constitution prescribe that Governor of the State shall, as

soon as or within the expiry of every fifth year constitute a Finance Commission to review the

financial position of Panchayats and ULBs respectively and make recommendations to the

Governor with regard to the following (GoI, 2015a):

1. The distribution between State and local bodies of the net proceeds of the taxes, duties,

tolls and fees leviable by States, which may be divided between them under this part

and the allocation between Panchayats at all levels of their respective share of such

proceeds;

2. The determination of taxes, duties, tolls and fees which may be assigned as, or

appropriated by the local bodies;

3. The grants in aid to local bodies from the consolidated funds of States;

4. The measures needed to improve the financial position of the local bodies;

5. Any other matter referred to Finance Commission by the Governor in the interests of

sound finance of local bodies.

Accordingly, Government of Karnataka constituted its first State Finance Commission in June

1994 which submitted its report in August 1996. Till now, Government of Karnataka has

constituted three State Finance Commission and presently, Fourth State Finance Commission

has been constituted and is yet to submit the report.

First State Finance Commission of Karnataka recommended total share of PRIs and ULBs to

be 36% in the non-plan gross own revenue receipts of the State Government for the time period

1997-98 to 2001-02. Fifteen percent of this 36% is allotted to ULBs (GoK, 1996). The Second

State Finance Commission was constituted in October, 2000 and it submitted its report in

December, 2002. Second State Finance Commission has adopted ‘Balance Financial

Allocation Approach’ in order to strike a balance in ensuring requirement of funds to meet the

12

responsibilities of local bodies on the one hand and State Government on the other. It

recommended an increase in the share of local bodes in State’s non-plan Gross Own Revenue

Receipts to 40% (GoK, 2002). Around 20% of the devolution was allotted to ULBs (8% for

ULBs and 32% for PRIs out of 40%). Second State Finance Commission observed the need

for maintaining reliable data base and it recommended a ‘Common Purpose Fund’ to facilitate

development of comprehensive data base, computerization, development of software required

for ULBs, training in preparation of draft documents, agreements etc. It recommended a sum

of Rs. 5 crore to be set apart each year out of the total share in devolution to ULBs. Second

State Finance Commission also initiated the incentive scheme for ULBs and an amount of Rs.

10 crore was earmarked for this purpose. A fixed amount of Rs 2 lakh is assured as incentives

to those ULBs whose internal revenue mobilization is 60% and above to the total demand

(including opening balance and inclusive of all taxes, rates, fees etc) in each year for three

consecutive preceding financial year.

Third State Finance Commission was constituted on August 2006 and it submitted its report

on December 2008. The commission recommended a devolution of 33% of States net own

revenue receipts to local bodies. While 30% of the total devolution was assigned to ULBs

(GoK, 2008).

Third State Finance Commission observed that there was considerable delay on the part of

State Government in reacting to recommendations of the Second State Finance Commission.

The Second State Finance Commission submitted its report at the end of year 2002, however,

its implementation started only in the year 2006-07.

4.4.1 SFC Devolution Criteria:

Population and Area are the common indicators used in all the State Finance Commissions.

Percentage of urban population and also the density of population has were given more

weightage by the Third State Finance Commission. The Second State Finance Commission

developed an index of backwardness comprising three indicators, namely illiteracy rate, SC-

ST population and persons per hospital bed. The trend in the percent of devolution to ULBs

clearly indicates the rising trend to meet the needs of growing urban population over the years

as may be seen from the Table-2.2.

13

Table- 2.2

Indicators of Devolution of Resources to ULBs (Weights in %)

Sl.

No

Indicators 1st SFC 2nd SFC 3rd SFC

1 Proportion of Urban

Population

10.30 10.19 13.59

2 Proportion of Urban Area 0.74 0.67 0.54

3 Proportion of Urban SC-ST

Population

3.25 2.22

4 Proportion of Urban

Population per Hospital Bed

1.88 2.50 1.86

5 Proportion of Urban Illiterates 2.97 2

6 Proportion Density in Urban

Areas

9.49

7 Road Length per Sq Km 2.78%

Total 15.75 (Rounded

off to 15%)

19.58

(Rounded off

to 20%)

29.72

(rounded off

to 30%)

Source: State Finance Commission Reports

14

CHAPTER- 3

Urban Local Bodies Structure in Karnataka

3.1 Urbanization in Karnataka

Urbanization in Karnataka has increased from 22% in 1951 to 39.48% in 2011. This trend has

resulted in the State being declared as the fifth most urbanized State in India and it is estimated

to maintain the same position by 2030 (Prabhu, 2013). As per available projections, urban

population in Karnataka will move up to 43.6% by 2021 (DES, 2013). Bangalore is the most

urbanized district in Karnataka followed by Dharwad, Dakshina Kannada and Mysore. Among

the districts Bangalore has witnessed highest decennial growth rate of 47.18%. Decadal growth

of urban population in Karnataka has surpassed the overall India’s decadal growth of urban

population (Refer Figure-3.1). Level of urbanization (% of urban population in total

population) in Karnataka is significantly higher than that of India throughout last five decades

(Refer Figure-3.2). The pace of urbanization in the last decade is higher when compared to

earlier years. Given these facts, urban governance and administration attains greater

importance. In the process of urbanization, ULBs get the prime role in meeting the needs of

people.

Figure-3.1

Decadal Growth of Urban Population (in %)

Source: Census of India, Various Issues

0

10

20

30

40

50

60

70

1 9 5 1 - 6 1 1 9 6 1 - 7 1 1 9 7 1 - 8 1 1 9 8 1 - 9 1 1 9 9 1 - 0 1 2 0 0 1 - 1 1

IN %

YEAR

India Karnataka

15

Figure-3.2

Level of Urbanization in India & Karnataka

(Urban Population as a % of Total Population)

Source: Census of India, Various Issues

3.2 Structure of ULBs

In Karnataka, Urban Local Bodies have been classified into five categories and they are as

follows:

1. Municipal Corporations

2. City Municipal Council

3. Town Municipal Councils

4. Town Panchayats

5. Notified Area Committees

Classification of towns is based primarily on Population criteria and other criteria like density,

percent of contribution from non-agricultural sectors etc. Table- 3.1 provides classification of

towns in Karnataka based on population criteria.

As of November 2016 there are 10 Municipal Corporations, 57 City Municipal Councils, 112

Town Municipal Councils, 91 Town Panchayats and five Notified Area Committees in

Karnataka. The Directorate of Municipal Administration oversees the functioning of

municipalities in Karnataka. Between 2001 and 2011, 8 Town Panchayats became Town

Municipal Councils, 16 Town Municipal Councils became as City Municipal Councils and two

City Municipal Council were upgraded to as Municipal Corporations. This trend is expected to

0

5

10

15

20

25

30

35

40

45

1 9 6 1 1 9 7 1 1 9 8 1 1 9 9 1 2 0 0 1 2 0 1 1

IN %

YEAR

India Karnataka

16

continue. By extrapolating the population growth (assuming population growth between 2001

and 2011 would continue till 2021) it was found that nearly 12 Town Panchayats would be

upgraded as Town Municipal Councils and 9 TMCs may become City Municipal Councils by

2011 (Please Refer Appendix-1 for details).

Table- 3.1

Classification of Towns in Karnataka

Classification Population

Municipal Corporations Above 3 lakh

City Municipal Councils 50000 - 300000

Town Municipal Councils 20000 - 50000

Town panchayats 10000 - 20000

Notified Area Committees Special areas

Source: Directorate of Municipal Administration, GoK, 2016.

17

CHAPTER- 4

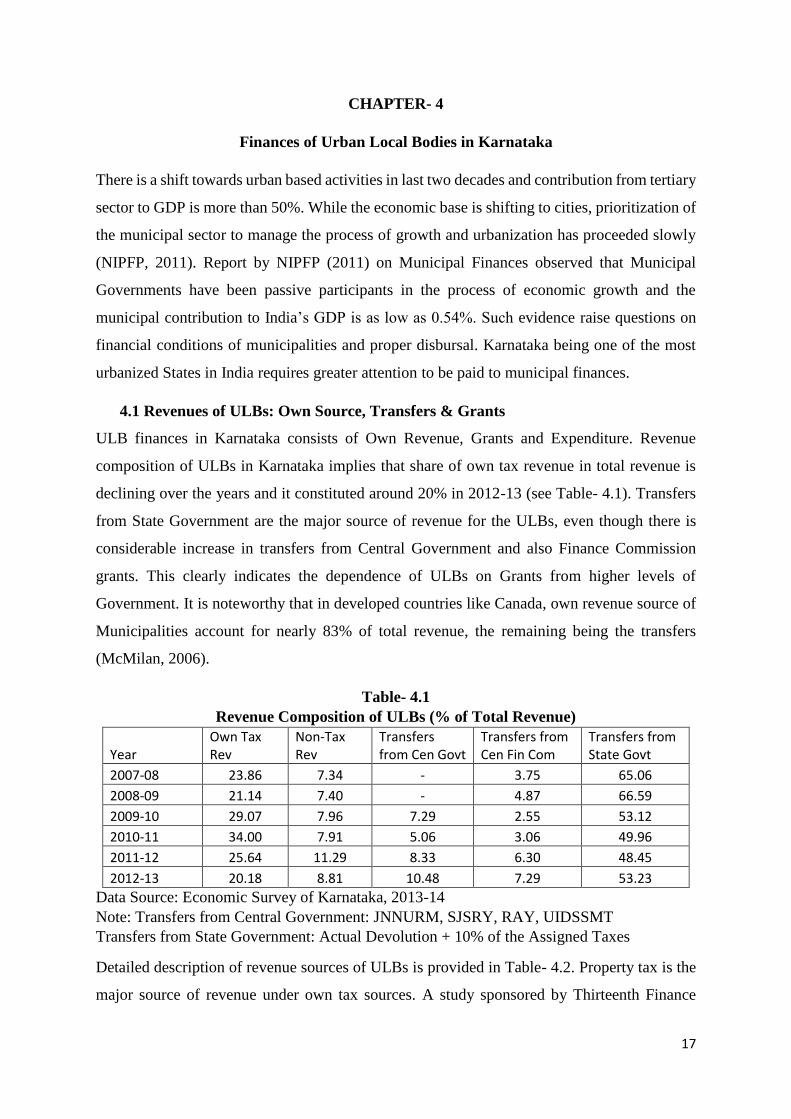

Finances of Urban Local Bodies in Karnataka

There is a shift towards urban based activities in last two decades and contribution from tertiary

sector to GDP is more than 50%. While the economic base is shifting to cities, prioritization of

the municipal sector to manage the process of growth and urbanization has proceeded slowly

(NIPFP, 2011). Report by NIPFP (2011) on Municipal Finances observed that Municipal

Governments have been passive participants in the process of economic growth and the

municipal contribution to India’s GDP is as low as 0.54%. Such evidence raise questions on

financial conditions of municipalities and proper disbursal. Karnataka being one of the most

urbanized States in India requires greater attention to be paid to municipal finances.

4.1 Revenues of ULBs: Own Source, Transfers & Grants

ULB finances in Karnataka consists of Own Revenue, Grants and Expenditure. Revenue

composition of ULBs in Karnataka implies that share of own tax revenue in total revenue is

declining over the years and it constituted around 20% in 2012-13 (see Table- 4.1). Transfers

from State Government are the major source of revenue for the ULBs, even though there is

considerable increase in transfers from Central Government and also Finance Commission

grants. This clearly indicates the dependence of ULBs on Grants from higher levels of

Government. It is noteworthy that in developed countries like Canada, own revenue source of

Municipalities account for nearly 83% of total revenue, the remaining being the transfers

(McMilan, 2006).

Table- 4.1

Revenue Composition of ULBs (% of Total Revenue)

Year Own Tax Rev

Non-Tax Rev

Transfers from Cen Govt

Transfers from Cen Fin Com

Transfers from State Govt

2007-08 23.86 7.34 - 3.75 65.06

2008-09 21.14 7.40 - 4.87 66.59

2009-10 29.07 7.96 7.29 2.55 53.12

2010-11 34.00 7.91 5.06 3.06 49.96

2011-12 25.64 11.29 8.33 6.30 48.45

2012-13 20.18 8.81 10.48 7.29 53.23

Data Source: Economic Survey of Karnataka, 2013-14

Note: Transfers from Central Government: JNNURM, SJSRY, RAY, UIDSSMT

Transfers from State Government: Actual Devolution + 10% of the Assigned Taxes

Detailed description of revenue sources of ULBs is provided in Table- 4.2. Property tax is the

major source of revenue under own tax sources. A study sponsored by Thirteenth Finance

18

Commission found that there exist large intercity variations in property tax revenues. For

instance, Mumbai Municipal Corporation registered a per capita annual revenue of Rs. 1334 as

against Rs. 25 for the Patna Municipal Corporation. It is interesting to note that composition of

revenue moves across different tiers of ULBs. For instance, for municipal corporations

property tax accounts around 30% in 2012-13 where as it is 5.7% and 2% for municipalities

and Nagar Panchayats at all India level. Being at lower tier these ULBs require higher financial

support from the State Government. In accordance, transfers from State Government accounts

more than 80% of total revenue for municipalities and Nagar panchayats. It is also notable from

Table- 4.2 that Central Finance Commission transfers are showing an increasing trend over the

years for all the tiers of ULBs.

Table- 4.2

Detailed Description of Revenue Sources of ULBs (% of Total Revenue)

Year

Immovable Property Tax

Other Tax

Non-Tax (incl of User charges)

Transfers from Cen Govt

Transfers from 12th & 13th Fin Com

Assigned + Devolution from State Govt

Municipal Corporations

2007-08 35.41 5.69 11.65 - 2.09 45.15

2008-09 35.67 1.74 12.68 - 1.74 48.16

2009-10 42.35 1.33 11.48 11.66 1.51 31.67

2010-11 51.19 1.17 11.44 5.26 1.84 29.10

2011-12 37.78 1.13 17.31 11.82 4.04 27.92

2012-13 29.50 1.69 14.14 17.96 4.68 32.03

Municipalities

2007-08 6.84 0.79 3.65 - 5.89 82.82

2008-09 6.81 0.67 3.04 - 7.70 81.77

2009-10 7.76 0.81 3.40 1.06 3.55 83.40

2010-11 6.86 0.64 2.93 3.98 4.89 80.70

2011-12 5.49 0.73 2.31 3.73 9.78 77.95

2012-13 5.71 0.54 1.93 0.54 10.86 80.42

Nagar Panchayats

2007-08 4.20 0.55 1.21 - 3.42 90.62

2008-09 2.35 0.38 1.12 - 7.67 88.48

2009-10 8.36 1.41 2.05 1.82 5.44 80.92

2010-11 2.35 1.12 1.73 7.52 4.86 82.42

2011-12 2.04 1.40 1.86 0.57 9.44 84.68

2012-13 2.06 0.64 0.87 0.30 10.48 85.65

Data Source: Economic Survey of Karnataka, 2013-14

State Government is transferring nearly 6% of its revenue expenditure to ULBs (see Figure-

4.1). Transfers to ULBs from the State Government was around 5% of revenue expenditure in

2006-07 and it increased to 6.67% in 2011-12. As per the Budget Estimates for the year 2015-

19

16, transfers to ULBs from the State Government will be around 5.67% of revenue expenditure.

Figure- 4.2 provides the plan and non-plan transfers to ULBs. Plan transfers were absolutely

nil in 2007-08 and there is an increasing trend thereafter. In 2013-14 plan transfers constituted

around 42% and remaining being the non-plan transfers.

Figure- 4.1

Transfers to ULBs as a % to Revenue Expenditure of State Government (in %)

Source: Accounts at Glance, 2016, Finance Department, GoK

Figure-4.2

Plan and Non-Plan Transfers to ULBs from the State Government

Source: Accounts at Glance, 2016, Finance Department, GoK

Budgeted and released amount of grants from State Government to ULBs in absolute terms are

provided in Table- 4.3. Total grants released increased from Rs. 2472 crore in 2009-10 to Rs.

6010 crore in 2014-15. There is substantial increase in grants released to city corporations.

Grants released to city municipal councils and town municipal councils are nearly stagnant.

There is a decline in grants transferred to town panchayats.

012345678

% o

f R

ev E

xp

Year

Transfers to ULBs

0

20

40

60

80

100

120

% O

F TO

TAL

TRA

NSF

ERS

YEARPlan Non-Plan

20

Table- 4.3

Grant Transfers from State to ULBs (in Rs. Crore)

Year

CC CMCs/TMCs TPs/NACs Total

Budget

Grant

Released Budget

Grant

Released Budget

Grant

Released Budget

Grant

Released

2009-10 679 662 1,335 1,372 351 438 2,365 2,472

2010-11 617 616 1,789 1,936 474 423 2,880 2,975

2011-12 2800 2864 1252 1126 285 258 4337 4248

2012-13 3544 2669 1513 1126 290 214 5347 4009

2013-14 4348 3632 1629 1139 344 248 6321 5019

2014-15 4956 4372 1589 1365 312 273 6857 6010

Source: Audit Reports

Grants released as a percent to budgeted amount was 104% in 2009-10 and it declined to 87%

in 2014-15 (See Table-4.4). All the tiers of ULBs are facing decline in the actual grants released

than the budgeted. In 2012-13 and 2013-14 nearly one quarter of budgeted grants has not been

transferred.

Table- 4.4

Grants Released as a % of Budgeted Transfers (in %)

Year CC CMCs/TMCs TPs/NACs TOTAL

2009-10 97.50 102.77 124.79 104.52

2010-11 99.84 108.22 89.24 103.30

2011-12 102.29 89.94 90.53 97.95

2012-13 75.31 74.42 73.79 74.98

2013-14 83.53 69.92 72.09 79.40

2014-15 88.22 85.90 87.50 87.65

Data Source: Report of CAG on Local Bodies, 2016, GoK

Table- 4.5

Share of State Government Grants to Tiers of ULBs (in %)

Year CC CMCs/TMCs TPs/NACs

2009-10 26.78 55.50 17.72

2010-11 20.71 65.08 14.22

2011-12 67.42 26.51 6.07

2012-13 66.58 28.09 5.34

2013-14 72.37 22.69 4.94

2014-15 72.75 22.71 4.54

Data Source: Report of CAG on Local Bodies, 2016, GoK

It is also to be noted that out of total grants from the State Government, share of city

corporations is more than one-third. The share of City Corporation in total grants has drastically

increased from 26% in 2009-10 to 72% in 2014-15. In contrast, share of city municipal councils

21

and town municipal councils has declined substantially from 55% in 2009-10 to 22.7% in 2014-

15. Even the share of town panchayats has declined significantly. This trend may be owing to

problem of population agglomeration in big cities of the State.

Thirteenth Finance Commission has allocated grants under the heads of General Basic Grants,

General Performance Grants and Grants for construction of Roads and Bridges to ULBs in

Karnataka (see Table- 4.6). As for as basic grants are concerned, between 2011 and 2014

released amount was more than allocated. However, there is drastic decline in 2014-15 to 38%.

In the tenure of Thirteenth Finance Commission, ULBs have received around 86% of total

allocated amount under basic grants. However, it is depressing to note that only 48% of the

released amount has been expended. This situation is even worse under performance grants.

ULBs have utilized only 60% of total grants given for building roads and bridges. CAG report

on Local Bodies Finances, 2015 found that Mysore City Council has utilized only 37% of

grants released between 2010-11 and 2013-14.

Table- 4.6

13th Finance Commission Grants to ULBs in Karnataka

Year

Allocated

Amount

Released

Amount Expenditure

Released amount

as % of Allocated

Expenditure as % of

Released Amount

General Basic Grants

2010-11 144.13 144.12 118.32 99.99 82.10

2011-12 167.15 180.67 142.07 108.09 78.64

2012-13 195.37 205.23 108.9 105.05 53.06

2013-14 231.46 235.71 54.23 101.84 23.01

2014-15 274.05 105.35 0.3 38.44 0.28

2010-15 1012.16 871.08 423.82 86.06 48.65

General Performance Grants

2011-12 58.81 93.28 40 158.61 42.88

2012-13 166.82 238.12 42.48 142.74 17.84

2013-14 196.77 202.55 1.87 102.94 0.92

2011-14 422.4 533.9 84.3 126.4 15.8

Roads and Bridges

2011-12 65.25 65.25 55.6 100 85.21

2012-13 69.53 69.53 59.64 100 85.78

2013-14 74.33 74.33 30.63 100 41.21

2014-15 112.25 32.56 0 29.01 0.00

2011-15 321.36 241.67 145.87 75.20 60.36

Data Source: Economic Survey of Karnataka, 2014-15

Note: Excluding BBMP

22

Table-4.7

Grants Allotted for ULBs from 14th Finance Commission (in Rs. Crore)

Year Basic Grants Performance Grants

2015-16 562.08 -

2016-17 778.29 229.7

2017-18 899.25 259.94

2018-19 1040.27 295.2

2019-20 1405.62 386.54

2015-20 4685.5 1171.38

Source: Report of Fourteenth Finance Commission, GoI (2015)

Allocation by the Fourteenth Finance Commission to ULBs seems to have increased

significantly compared to Thirteenth Finance Commission. However, receiving the

performance grants again depends on fulfillment of required conditions.

4.2 Expenditure of ULBs

Figure- 4.2

Item Wise Expenditure of ULBs in Karnataka (%)

Source: Economic Survey of Karnataka, 2013-14

Major items of expenditure of ULBs consists of Establishment expenditure, Maintenance,

capital expenditure, welfare expenditure and others. Figure- 4.2 indicates that Establishment

expenditure constituted 24% of total expenditure in 2007-08 which increased to 34% in 2013-

Establishment

24%

Maintanance34%

Capital Exp36%

Welfare Exp2%

Others4%

2007-08

Establishment

21%

Maintanance26%

Capital Exp45%

Welfare Exp4%

Others4%

2010-11

Establishment

34%

Maintanance

25%

Capital Exp34%

Welfare Exp3%

Others4%

2013-14

23

14. The maintenance expenditure declined from 34% to 25% between 2007-08 and 2013-14,

whereas the capital expenditure remained almost the same.

Table- 4.8 provides detailed item wise expenditure by ULBs. It clearly indicates that

expenditure on Salaries and wages consistently remains at top. It is followed by maintenance

expenditure like electricity charges, water supply and roads. Among the Capital expenditure,

spending on building of roads is highest followed by water supply and buildings. Welfare

expenditure for citizens constitutes only a smaller portion in the overall expenditure.

Table-4.8

Detailed Item Wise Expenditure of ULBs (as a % of Total Expenditure)

S.No. Item 2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

2013-14

1 Establishment

a) Salaries & wages for Employees 23.01 24.22 20.90 18.94 25.60 32.36 32.36

b) Pension etc. for Employees 0.46 2.75 1.40 1.00 1.65 0.87 0.87

c) Any other (Office Expenses) 0.74 0.88 0.78 0.82 1.04 0.85 0.85

2 Maintenance

a) Water Supply 5.67 7.77 5.13 6.12 5.45 4.94 4.94

b) Buildings 0.67 0.72 0.69 0.77 0.76 0.68 0.68

c) Roads 3.96 3.45 4.24 3.45 3.19 2.66 2.66

d) Any other maintenance Exp (Electricity charges) 23.87 19.46 15.02 15.55 17.21 16.25 16.25

3 Capital Expenditure

a) Water Supply 4.04 2.98 3.74 4.57 3.78 3.93 3.93

b) Buildings 3.59 3.79 3.76 4.19 4.62 3.93 3.93

c) Roads 19.36 19.69 24.96 24.93 20.22 18.53 18.53

d) Any other capital expenditure (SWM, UGD & Street Lights) 8.53 8.07 11.05 11.97 8.13 7.82 7.82

4 Welfare Expenditure for citizens

a) Education (excluding teachers salary's) - - - - - - -

b) Pension etc. for citizens - - - - - - -

c)

Any other welfare expenditure for citizens (22.75%, 7.5% OBC, 3% PH) 2.06 2.77 4.69 3.65 3.71 3.42 3.42

5 Any other (SJSRY) 4.04 3.47 3.62 4.05 4.64 3.77 3.77

Source: Economic Survey of Karnataka, 2013-14

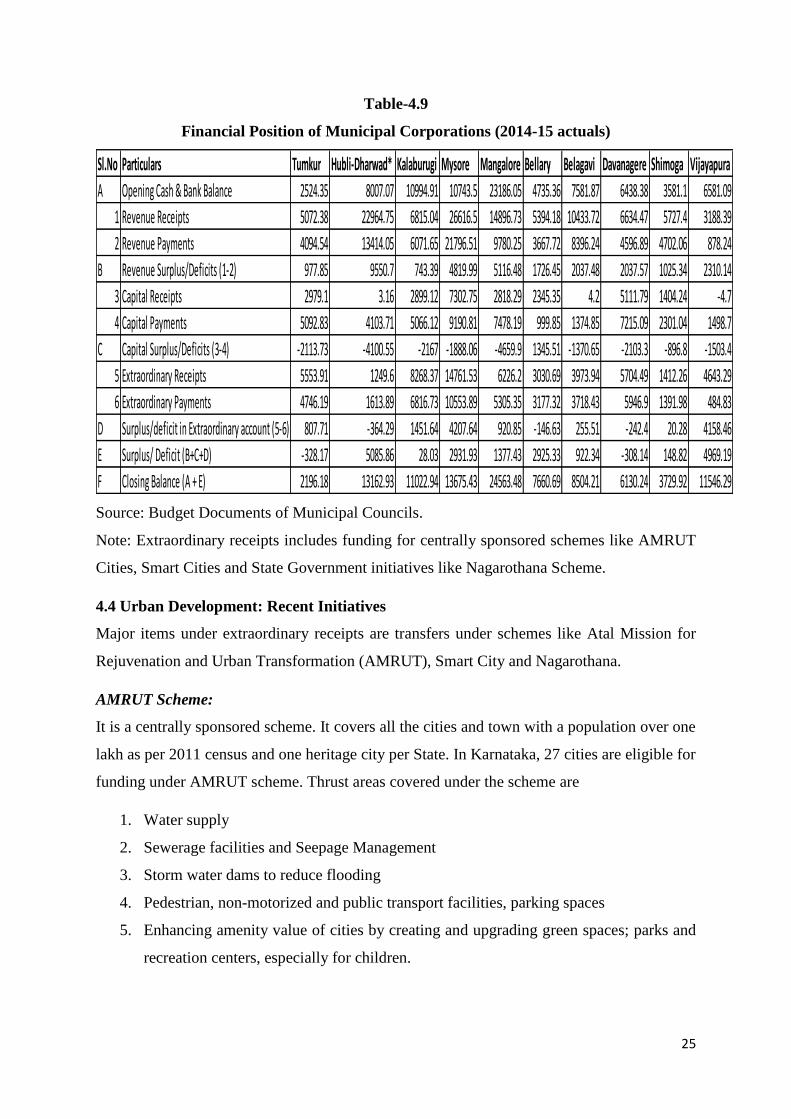

4.3 Finances of Select Municipal Corporations:

Table- 4.9 gives the details of financial position of Municipal Corporations. All the Municipal

Corporations have surplus in revenue account and deficit in capital account. Except Tumakuru

and Davanagere Municipal Corporations, all others have registered surplus in the overall

24

balance. It is notable that all the Municipal Corporations have substantial closing balance in

the account. Municipal Corporations could achieve better financial position mainly owing to

the extraordinary receipts. It consists mainly of transfers from Central Government in the form

of centrally sponsored schemes and also State Government specific transfers. On an average

extraordinary receipts constitutes 29% of total receipts of Municipal Corporations for the year

2014-15 (refer Figure-4.3). It is noteworthy that all Municipal Corporations have revenue

surplus in their revenue account implying that considerable portion of revenue receipts is being

used for capital payments. Table-4.9 also reveals that capital payments exceeds the capital

receipts for all the Municipal Corporations except for Bellary Municipal Corporation resulting

in deficit in the capital account. The deficit in the capital account can be fully offset by the

surplus in the revenue account. It provides a positive implication that Municipal Corporations

were able to meet their capital expenditure from the revenue receipts.

Figure-4.3

Major Components of Receipts and Payments of Municipal Corporations (in %)

Source: Budget Documents of Municipal Corporations

Revenue Receipts

58%Capital

Receipts13%

Extraordinary

Receipts29%

RECEIPTS

Revenue Payment

s47%

Capital Payment

s27%

Extraordinary

Payments

26%

PAYMENTS

25

Table-4.9

Financial Position of Municipal Corporations (2014-15 actuals)

Source: Budget Documents of Municipal Councils.

Note: Extraordinary receipts includes funding for centrally sponsored schemes like AMRUT

Cities, Smart Cities and State Government initiatives like Nagarothana Scheme.

4.4 Urban Development: Recent Initiatives

Major items under extraordinary receipts are transfers under schemes like Atal Mission for

Rejuvenation and Urban Transformation (AMRUT), Smart City and Nagarothana.

AMRUT Scheme:

It is a centrally sponsored scheme. It covers all the cities and town with a population over one

lakh as per 2011 census and one heritage city per State. In Karnataka, 27 cities are eligible for

funding under AMRUT scheme. Thrust areas covered under the scheme are

1. Water supply

2. Sewerage facilities and Seepage Management

3. Storm water dams to reduce flooding

4. Pedestrian, non-motorized and public transport facilities, parking spaces

5. Enhancing amenity value of cities by creating and upgrading green spaces; parks and

recreation centers, especially for children.

Sl.No Particulars Tumkur Hubli-Dharwad* Kalaburugi Mysore Mangalore Bellary Belagavi Davanagere Shimoga Vijayapura

A Opening Cash & Bank Balance 2524.35 8007.07 10994.91 10743.5 23186.05 4735.36 7581.87 6438.38 3581.1 6581.09

1 Revenue Receipts 5072.38 22964.75 6815.04 26616.5 14896.73 5394.18 10433.72 6634.47 5727.4 3188.39

2 Revenue Payments 4094.54 13414.05 6071.65 21796.51 9780.25 3667.72 8396.24 4596.89 4702.06 878.24

B Revenue Surplus/Deficits (1-2) 977.85 9550.7 743.39 4819.99 5116.48 1726.45 2037.48 2037.57 1025.34 2310.14

3 Capital Receipts 2979.1 3.16 2899.12 7302.75 2818.29 2345.35 4.2 5111.79 1404.24 -4.7

4 Capital Payments 5092.83 4103.71 5066.12 9190.81 7478.19 999.85 1374.85 7215.09 2301.04 1498.7

C Capital Surplus/Deficits (3-4) -2113.73 -4100.55 -2167 -1888.06 -4659.9 1345.51 -1370.65 -2103.3 -896.8 -1503.4

5 Extraordinary Receipts 5553.91 1249.6 8268.37 14761.53 6226.2 3030.69 3973.94 5704.49 1412.26 4643.29

6 Extraordinary Payments 4746.19 1613.89 6816.73 10553.89 5305.35 3177.32 3718.43 5946.9 1391.98 484.83

D Surplus/deficit in Extraordinary account (5-6) 807.71 -364.29 1451.64 4207.64 920.85 -146.63 255.51 -242.4 20.28 4158.46

E Surplus/ Deficit (B+C+D) -328.17 5085.86 28.03 2931.93 1377.43 2925.33 922.34 -308.14 148.82 4969.19

F Closing Balance (A + E) 2196.18 13162.93 11022.94 13675.43 24563.48 7660.69 8504.21 6130.24 3729.92 11546.29

26

Central Government has earmarked an amount of Rs. 50000 crore for five years between 2015-

16 and 2019-20. In the annual budgetary allocation for the mission funds, project fund

constitute 80%, incentive for reforms10 %, State funds for administrative and office expenses

8% and Ministry of Urban Development funds for administrative and office expenses 2%.

Project fund will be divided among the States and union territories at the beginning of each

year. An equitable formula is being used for distribution of funds in which 50% weightage is

given to urban population of each State and union territories and the number of Statutory Towns

in the State. The State Annual Action Plan (SAAP) has to decide on inter ULB allocation of

the funds. As reported in State Annual Action Plan 2015-16, Central Government contribute

47%, State Government 20% and ULBs 33% out of total allocated fund of INR 4323.20 for

Karnataka State under AMRUT Mission (refer Table-4.10). Sectoral allocation of this fund

reveals that water supply and sewerage gets major share in total allocation (refer Table-4.11).

Table- 4.10

Fund Sharing Pattern for AMRUT Mission in Karnataka

(in INR crore)

Centre 2025.14 (47%)

State 864.64 (20%)

ULB 1433.42 (33%)

Total 4323.20

Source: State Annual Action Plan 2015-16, Government of Karnataka (2016)

Table- 4.11

Sector Wise Fund Allocation for the AMRUT Mission in Karnataka

(Amount in INR Crore)

Sector 2015-16 2016-17 2017-18 2018-19 2019-20 Total

Water Supply 551.54 451.72 350.04 174.26 90.09 1617.65

Sewerage 612.65 484.25 502.50 396.60 270.97 2266.97

Storm Water Drains 48.80 83.00 84.43 49.50 22.00 287.73

Green Space & Parks 27.65 22.85 21.32 17.52 11.10 100.44

Urban Transport 17.90 11.00 11.00 6.00 4.50 50.40

Total 1258.54 1052.82 969.29 643.88 398.66 4323.19

Source: Source: State Annual Action Plan 2015-16, Government of Karnataka (2016)

27

Smart Cities Mission:

Ministry of Urban Development, Government of India has initiated Smart Cities Mission in

June 2016 with the objective to promote cities that provide core infrastructure and give a decent

quality of life to its citizens, a clean and sustainable environment and application of ‘Smart’

solutions. The focus is on sustainable and inclusive development of cities. The core

infrastructure elements in a Smarty City includes the following:

1. Adequate water supply

2. Assured electricity supply

3. Sanitation, including solid waste management

4. Efficient urban mobility and public transport

5. Affordable housing for poor

6. Robust IT connectivity and digitization

7. Good governance (e-governance)

8. Sustainable environment

9. Safety and security of citizens

10. Health and education

Mission covers 100 cities across India for five years from 2015-16 to 2019-20. Six cities in

Karnataka comes under Smart Cities Mission. In first year of initiation, Government has

proposed to provide Rs. 200 crore for each smart cities to create higher initial corpus followed

by Rs. 100 crore for next three years and matching contribution by the States/ULBs to fund the

program. ULBs can take steps for additional contribution through bond financing, PPPs,

multilateral borrowings etc.

Nagarothana Scheme:

It is a Karnataka State Government’s initiative for development of cities. This scheme is also

called as Chief Minister’s Small & Medium Town Development program. This scheme will

fund plans to develop tier two, three cities and smaller towns. District head quarter town,

Grade-A towns, City Municipal Councils, Town Municipal Councils, Town Panchayats,

Village Panchayats upgraded to Town Panchayats and newly created ULBs will get funds.

State is already in third phase of implementation and it has approved an amount of Rs. 2855

crore for this purpose. Government has announced 35 crore each for district headquarters, 25

crore each for 34 city Municipal Councils and 7.5 crore each for Town Municipal Councils

(“Rs 2855 crore for 271 cities”, 2016).

28

4.5 Urban Infrastructure: Current Status and Required Investments

It was found that many of the municipal corporations have surplus in the balance sheet. It was

also interesting to note that portion of revenue received is being spent as capital expenditure.

Overall the balance sheet appears to be better placed. However, an important question that need

to be answered is whether the current spending on capital formation is sufficient to meet the

need of growing urban population? In essence, whether present spending can meet the required

urban infrastructural needs? An answer to this question really puts up the critical financial

position of ULBs in Karnataka.

There are few important projections on urban infrastructural requirement at aggregate level.

High- Powered Expert Committee (HPEC) for estimating Investment requirement for Urban

Infrastructure Services has estimated urban investment requirement to be approximately

around 39.2 lakh crores for the time period 2012-2031 for India as a whole. These estimates

were arrived by consolidating services in 8 core sectors namely water supply, sewerage, solid

waste management, urban roads, storm water drains, urban transport, street lighting and traffic

support infrastructure. Working group on financing infrastructure by adopting the same method

as of HPEC estimated the spending requirements of the ULBs (GoI, 2011). The working group

has estimated the required capital expenditure to the tune of 1.86% of GDP for 10 years starting

from 2012-13.

Table-4.12

Financing Gap in Urban Infrastructure

(In Rs. Crore)

Year Required Capital & Maintenance Exp

Actual Capital & Maintenance Exp (3)

Financing Gap

GSDP criteria (1) Urban Popu criteria (2) (1-3) (2-3)

2012-13 5191.68 4664.61 1605.44 3586.24 3059.17

2013-14 6463.52 5563.59 1765.99 4697.53 3797.60

Data Source: Report of Working Group on Financing Infrastructure (GoI, 2011) & Economic

Survey of Karnataka, 2013-14.

In order to arrive at State level estimates on urban infrastructural spending, present study has

adopted two criteria to narrow down the estimates to Karnataka State. First criteria is GSDP

criteria and second is the Urban Population Criteria. As per GSDP criteria, percentage of

29

Karnataka’s GSDP in India’s GDP has been considered and as for as the population criteria,

Karnataka’s urban population in India’s urban population has been considered. Table-5.10

clearly reveals that there is financing gap of Rs. 4697.53 crore and Rs.3797.60 crore as per

GSDP criteria and urban population criteria respectively in the year 2013-14. Actual capital

and maintenance expenditure even does not cover one-third of the required investments. This

appears to be an alarming situation and Indian Governments should take necessary steps to fill

this gap. As the budget constraint restricts the spending of Central and State Governments, it

is utmost important for ULBs to raise the own revenue resources to fill the gap. It also appears

from the balance sheets of municipal corporations that many of them have not resorted to debt

financing as they have receiving remarkable amount as extraordinary receipts. As indicated in

Table-4.12 the required expenditure is too high and there is a need to fill this gap in order to

meet the basic requirements of the growing urban population. Property tax is the main source

of own revenue for ULBs in India. However, it was reported that property tax yields have

grown but in no way it reflects the real estate boom happened in many of Indian cities (NIPFP,

2011). It was also observed that inefficiencies reduced property tax by about 71%. A survey

conducted by NIPFP (National Institute of Public Finance and Policy, New Delhi) of 31

municipalities, nearly 54% of the tax demanded was not collected. The NIPFP report also found

that actual municipal revenue are less than a third of what is required (NIPFP, 2011).

There are two important means to fill the existing gap in required expenditure. They are

1. Public-Private Partnership

2. Market Based Financing (Bond Financing)

ULBs can have a partnership with private entities in meeting the required spending. PPPs are

important for bringing capital and efficiency into the infrastructural sector. In recent years,

newly formed Government of Telangana has endorsed PPPs in providing Foot Over Bridges in

ULBs, Pay & Use toilets in ULBs and Operation and Maintenance of street lighting in 9 ULBs

(GoT, 2016). It is being discerned that PPP success stories are rare in urban infrastructure

mainly because of inadequate cost recovery and associated political sensitivity (GoI, 2016a).

Government of India has taken many steps to promote PPPs in Infrastructure investments and

one among these initiative is ‘Viability Gap Funding’ scheme. As per the scheme Central

Government would provide total Viability Gap funding up to 20% of the total project cost. The

PPP projects may be posed by Central Ministries, State Governments and Statutory Authorities

30

like ULBs. There are great opportunities for ULBs to utilize the available provisions in order

to strengthen the private participation in funding infrastructure through PPPs.

In the western countries ‘bond financing’ is the main source of capital spending by the local

bodies. In United States of America (USA) counties and State authorities financed $3.2 trillion

in infrastructural investment using municipal bonds from 2003 to 2012 and nearly 75% of all

infrastructure projects are completed using bond financing (NAC, 2016). Whereas major

source of ULB financing for infrastructure development in Europe is through bank lending.

In India, since 1994, the Indo-US Financial Institution Reform and Expansion (FIRE-D) project

is working with National, State and Local Governments to develop a market based bond market

(Vaidya & Vaidya, 2008). It is noteworthy that several ULBs in India have already issued

bonds and mobilized around Rs12249 millions. Bond ratings are crucial for issuing bonds. The

ratings depends on financial condition of ULBs, credit worthiness, capacity of issuer to make

timely payments, economic base of service area etc. Ahmedabad Municipal Corporation was

rated ‘AA’ by CARE ratings in 2015. As of now, for many of the municipalities ratings are not

in use or ratings have been withdrawn. Greater Vishakapattanam Municipal Corporation was

the last to issue bond in the year 2010 (Singh, 2015).

Many of the medium and smaller Municipalities could not approach the bond market due to

several pre-required conditions. To overcome such problems concept of ‘Pooled Financing’

was brought out. Under this, a special purpose vehicle will be created by pooling several

municipalities. For instance, Tamil Nadu Urban Development Fund issued a bond by pooling

14 municipalities for commercially viable water & sewerage infrastructure project in 2003

(Vaidya & Vaidya, 2008). Subsequently, Government of Karnataka under the pooled financing

raised debt from investors for the Greater Bangalore Water Supply and Sewerage Project. It

covered eight municipal towns around Bangalore and had total project cost of Rs. 6000 million.

A debt fund called the Karnataka Water and Sanitation Pooled Fund was established under the

India Trust Act to access the capital market by issuing bond on behalf of participating ULBs

(Vaidya & Vaidya, 2008).

Approach to municipal bond market by ULBs in Karnataka is in depressing state. There is huge

funding requirement and also there exists an opportunity for the ULBs to tap the funding gap

through bond financing. However for reaching the bond market, ULBs have to furnish the

required details pertaining to its own revenue position, audit reports, in consort with timely

compliance to repayments etc. And on the same, ratings of local bodies are being grounded.

31

Karnataka Government should take an initiative to form an ‘organization’ through which ULBs

can approach bond market and the raised funds can be distributed among ULBs based on pre-

established criteria. Such an initiative would really help the ULBs particularly medium and

small ULBs in approaching and also raising required funds for capital formation.

Chapter-5

Conclusion

This study has analyzed the finances of ULBs in Karnataka. Analysis of fiscal indicators of

Karnataka revealed that all the indicators are in better position compared to other States in

India. However, it’s performance in human development needs attention. Rule based Fiscal

correction mechanism i.e., Karnataka Fiscal Responsibility Act, 2002 has significantly

contributed to fiscal deficit and liabilities reduction. It is good to note that Karnataka has

surplus in revenue account and hence the surplus is being spent for capital formation along

with borrowed amount.

Local bodies Finances consists of own revenue, devolution from State Governments, Central

Finance Commission grants and also Central Government grants. 74th Amendment of the

Indian Constitution in 1992 strengthened the decentralized structure in India. There has been

considerable progress in the empowerment of Panchayat Raj institutions and Municipalities in

India after the constitution amendments. Central Finance Commissions transfers grants broadly

under two heads: General Grants and Performance Grants with the intention to raise the

Consolidated Fund of the State Governments to support local bodies. The transferred amount

will be allocated among the local bodies based on criteria suggested by the State Finance

Commissions. Delay in formation of SFCs, Untimely submission of SFC reports, lack of

compliance of audited data are hindering the proper estimation and transfers to local bodies.

Even the Karnataka’s SFCs have also observed the serious data problems pertaining to local

bodies. This report too emphasis that concerned department should publically accomplish

detailed data on all tiers of ULBs to enable proper research on the subject.

Own revenue source of ULBs in Karnataka is less than one-third of total receipts and remaining

being the transfers from State and Central Governments. Property tax is the major source of

own revenue. It is depressing to note that only 48% of general grants released by 13th Finance

32

Commission has been utilized by ULBs. Among the expenditure, outlay on Salaries and wages

tops the list followed by maintenance expenditure and capital spending.

Karnataka is 5th most urbanized State in India and the urban population growth is significant

and much higher than the national urban population growth. It is projected that Karnataka

maintains same position until 2021. It was observed that nearly 12 Town Panchayats would be

upgraded as Town Municipal Councils and 9 TMCs to become City Municipal Councils by

2021 and hence necessities higher devolution in the near future. The rapid pace of urbanization

requires huge investments on infrastructure. ULBs has to play a significant role in meeting the

needs of the urban population. ULBs in Karnataka, particularly municipal corporations have

shown either balance or surplus in the balance sheets. This surplus was mainly owing to

‘extraordinary receipts’ from the Centre and State Government under the schemes like

AMRUT cities, Nagarothana scheme etc. However, the required infrastructural spending is

huge and present spending does not contribute even one-third of required funding. Given the

budget constraints of the Central and State Governments, ULBs have to take step to raise the

own revenue sources and also find out new avenues to meet the required spending. Two

important means in this regard are PPP and bond financing.

Municipal Bond Market has not been developed in India when compared to western economies.

It constitutes a meagre portion in overall receipts of ULBs and since 2010 there are no attempts

to raise money from bond market by ULBs. There is greater scope for ULBs to tap the required

amount from the Bond market. Karnataka Government should take an initiative to form an

‘organization’ through which ULBs can approach bond market. Funds which has been raised

has to be distributed among participating ULBs. Such an initiative would really help the ULBs

particularly lower tier of ULBs in approaching and also raising required funds for capital

formation.

33

Bibliography

GoI. (1994). Finance Commission report for 1995-2000. New Delhi: Finance Commission India.

GoI. (2000). Report of the Eleventh Finance Commission for (2000-2005). New Delhi: Finance

Commission India.

GoI. (2004). Report of the Twelfth Finance Commission (2005-10). New Delhi: Finance Commission

India.

GoI. (2009). Thirteenth Finance Commission 2010-2015. New Delhi: Finance Commission India.

GoI. (2011). Report of the Working Group on Financing Urban Infrastructure. New Delhi: Planning

Commission, Government of India.

GoI. (2015). Report of the Fourteenth Finance Commission. New Delhi: Finance Commission India.

GoI. (2015a). The Constitution of India. New Delhi: Ministry of Law & Justice, Government of India.

Retrieved from http://lawmin.nic.in/olwing/coi/coi-english/coi-4March2016.pdf

GoI. (2016). Census of India. New Delhi: Registrar General of India, Government of India.

GoI. (2016, November 10). Ministry of Urban Development. Retrieved from moud.gov.in:

moud.gov.in/legislation/constitution

GoI. (2016a, December 6). Smart Cities Mission. Retrieved from Ministry of Urban Development: