government of romania decision - findev gateway...government of romania decision for approval of...

TRANSCRIPT

Government of Romania

DECISION

For approval of micro-credit scheme for licensing of Credit Agencies

in order to administer the US$ 3.6 million stipulated in the Loan Agreement 4509-RO

between Romania and IBRD

Based on the provisions of art. 107 from the Romanian Constitution and of the article 5

from the Government Ordinance no. 40/2000 on Licensing Credit Agencies to Manage Funding

for Micro-credit

Based on the provisions of Annex A of annex no. 1 and of pct. 3, part B of annex no. 2

from the Loan Agreement between Romania and the International Bank for Reconstruction and

Development – I.B.R.D., regarding the financing of Mine Closure and Social Mitigation Project,

amounting to 44.5 million USD, signed in Bucharest on October 13,1999, ratified by the

Government Ordinance no.11 / 2000, and modified by Law no. 168/2000.

G o v e r n m e n t o f R o m a n i a a p p r o v e t h e p r e s e n t D e c i s i o n :

Single article. It is approved the micro-credit scheme presented in the Annex, which is

integral part of the present decision, regarding licensing of the credit agencies in order to

administer the fund amounted to US$ 3.6 million stipulated in the Loan Agreement between

Romania and IBRD no. 4509-RO ratified by the Government Ordinance no.11 / 2000 for the

ratification of the Loan Agreement between Romania and IBRD regarding the financing of Mine

Closure and Social Mitigation Project, amounting to 44.5 million USD, signed in Bucharest on

October 13,1999, ratified by the Government Ordinance no.11 / 2000, and modified by Law no.

168/2000, published in the Official Gazette of Romania, Part I, no. 497 on October 10, 2000.

PRIME MINISTER

Mugur Constantin Isarescu

ANNEX

MICROCREDIT SCHEME On licensing of the Credit Agencies in order to administer the USD 3,60 million fund provided

through 4509-RO Loan granted to Romania by International Bank for Reconstruction and

Development concerning financing of the mine closure and social mitigation Project, amounting

to USD 44,5 million, signed in Bucharest on October 13,1999 and ratified by the Government

Ordinance 11/2000, approved with modifications by the Law 168/2000

CHAPTER I

General Provisions

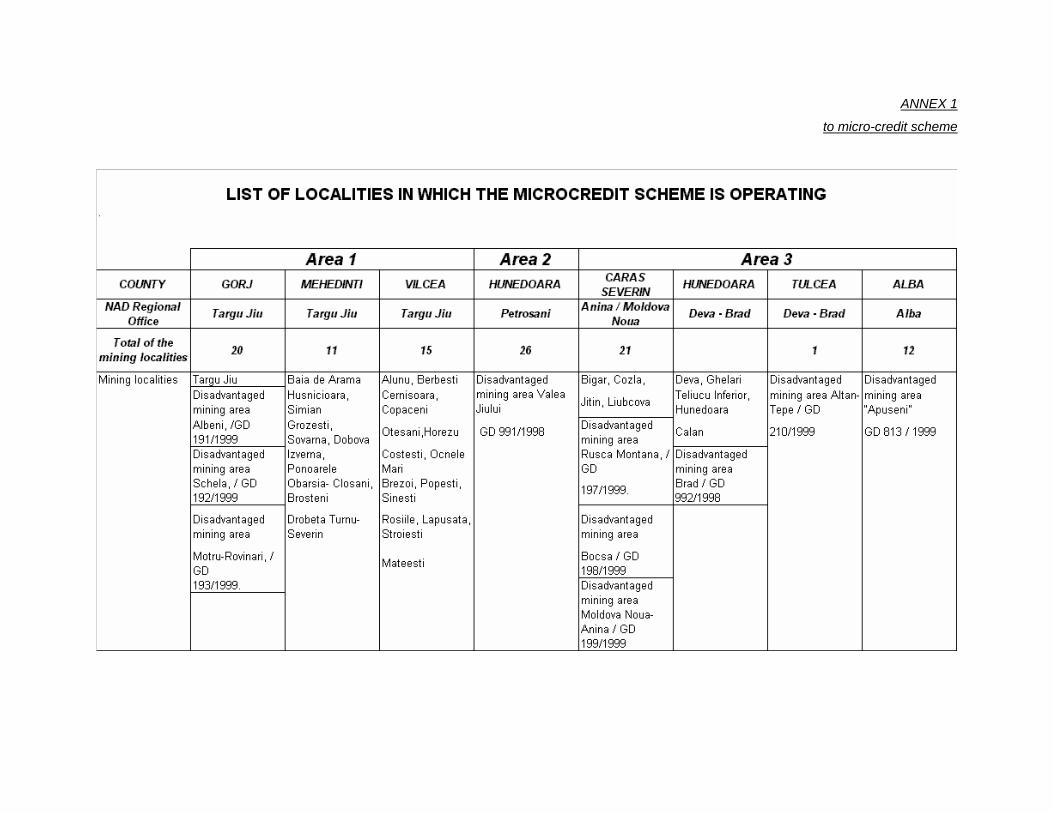

Art.1.- The micro-credit scheme prepared on the basis of GO 40/2000 regarding the licensing of the credit agencies in order to administer the funds for granting micro-credits, has the objective to define the procedures which allow MOIC that through NAD to give in administration public funds constituted on the basis of the state budget starting with 2000, from resources ensured from the 4509 - RO Loan granted to Romania by International Bank for Reconstruction and Development concerning financing of the mine closure and social mitigation Project, amounting to USD 44,5 million, signed in Bucharest on October 13,1999 and ratified by the Government Ordinance 11/2000, approved with modifications by the Law 168/2000, to the credit agencies by public tendering organized under the law provisions. Art.2.- The operating area of the micro-credit scheme is represented by the mining regions grouped in 5 operational areas, as presented in annex no. 1. Art.3.- The credit agencies, selected on the basis of the procedures and criteria approved by this scheme, that receive in administration micro-credit funds, are qualified to grant micro-credits only to the applicants carrying on their activity in the operating area of the scheme, defined in annex no. 1, and belonging to the respective agency.

CHAPTER II Definitions

Art.4.- To the meaning of the present scheme for granting micro-credit, the following terms shall be defined as follows: a) public funds - public financial resources to be used for micro-credit lending, in compliance

with the law, and managed by governmental agencies; b) governmental agencies - public central and local institutions the heads of which have the

authority of main credit coordinators in compliance with the law, institutions that manage public funds for micro-credit lending;

c) credit agencies (CA) - legal entities, non-profit organizations, established or recognized in compliance with the law, licensed according to GO 40/2000, to manage the public funds for micro-credit awarded by government agencies from public funding, by competitive bidding so as the law requires;

d) funds for micro-credits - public funds granted by governmental agencies to credit agencies through competitive bidding so as the law requires, in order to be transform in micro-credit through revolving financing mechanism;

e) micro-credit - repayable loan with or without interest, made to applicants, of up to 10,000 Euro-s nominal value, granted in Romanian Lei at the NBR exchange rate on the day prior the release of the loan, with a payback period of up to 36 months, with or without a grace period, to be used for the purchase of fixed assets, raw materials, materials, energy, fuel, as well as other services required in the implementation of the project with a view to undertake a commercial activity for which it was authorized;

f) applicants - legal entities, incorporated businesses with less than fifty employees under a collective employment contract, licensed self-employed and family associations established under Decree-Law No. 54/1990 or under other normative documents, as well as any natural person who submits a well-founded business plan for starting or developing business;

g) micro-credit recipients – legal entities, incorporated businesses with less than fifty employees under individual employment contract, licensed self-employed and family associations established under Decree-Law No. 54/1990 or under other normative documents, as well as any natural person who submits a well-founded business plan, under the terms it is authorized in compliance with the law;

h) micro-credit scheme - the whole set of rules and procedures to be followed by government agencies, through the approval of which, according to the GO 40/2000 the following are regulated: objectives of the micro-credit scheme; type of micro-credit recipients; biding documents for selecting credit agencies; contents and terms of the contract between the governmental agency and the credit agency; accepted risk level in the recovery of the public funds granted by government agencies to credit agencies for micro-credit lending; proposed duration and financial circuit of the fund; collateral and interest level, as applicable; management of public funds granted to credit agencies as funds for micro-credit lending, mechanism for reporting, evaluation, supervision and control of Cas activities;

i) credit agencies licensing – designation, under the terms of GO 40/2000, and in compliance with the criteria set out in the micro-credit scheme, of the non-profit legal entities established or recognized in compliance with the law, that may be granted funds from public finance by governmental agencies to manage for micro-credit lending, subject to annual auditing in view of renewal of their authorization;

j) MOF – Ministry of Finance; k) MOIC – Ministry of Industry and Commerce; l) MOIC PMU - Project Management Unit subordinated to MOIC, established through GD

418/1999 regarding the implementation of the pilot project on mining sector restructuring; m) CCPI – Committee for Coordinating Project Implementation, established 418/1999; n) IBRD - International Bank for Reconstruction and Development; o) NAD - The National Agency for the Development and the Implementation of the

Reconstruction Programs in the Mining Regions;

p) NAD PIU – NAD Project Implementation Unit, established through GD 418/1999 regarding the implementation of the pilot project on mining sector restructuring;

q) regional office - the subsidiary without legal status subordinated to NAD, that carries on its activity in a locality situated in the operating area of the micro-credit scheme;

r) project - The project "Mine Closure and Social Mitigation" financed through 4509-RO Loan granted to Romania by International Bank for Reconstruction and Development concerning financing of the mine closure and social mitigation Project, amounting to USD 44,5 million, signed in Bucharest on October 13,1999 and ratified by the Government Ordinance 11/2000, approved with modifications by the Law 168/2000;

s) PAD – Project Appraisal Document, edited by IBRD and integrating part of the project; t) Program - a part of the Project component "Social Mitigation", whose objective is to grant in

administration a portion of the micro-credit fund to a Credit Agency selected for one or more of the 5 mining regions and licensed for granting micro-credits as well as provision of the service charges for the micro-credit funds in order to grant micro-credits by CA from public funds according to the provisions of the micro-credit scheme;

u) Advertisement - the text containing the minimum requirements for the Credit Agency presentation, published in "Development Business" and/or in a national newspaper with a wide circulation, referring to NAD requesting the Credit Agencies to send expressions of interest for "Micro-finance Management", in order to prepare the long list;

v) expression of interest - represents the document sent by the Credit Agency until the deadline specified in the advertisement, expressing their interest to participate in the selection organized by NAD for "Micro-finance Management ";

w) long list – the registration of the Credit Agencies having submitted the expressions of interest until the deadline mentioned in the advertisement;

x) short list – the Credit Agencies selected based on the expressions of interest, submitted until the date mentioned in the advertisement;

y) request for proposals – documentation for drawing up and presenting the proposals, comprising: letter of invitation; information for Credit Agency; technical proposal – standard form, financial proposal – standard form, the terms of reference; the standard form of contract; as well as other information that may facilitate for all bidders the preparation of documents in compliance with the IBRD provisions.

z) operating costs – for the services for administrating of the micro-credit fund stipulated in the contract, for the inception period that may not exceed 6 months, represent the costs calculated by each Credit Agency and presented in the financial proposal, made up of: a) costs financed from IBRD funds, as mentioned in the request for proposals, section IV “Financial Proposal IV G – Specimen Budget Format”; b) costs financed from Romanian contribution to the project, in accordance with GO 11/2000, approved with modifications by Law 168/2000. The costs for operating period of the micro-credit scheme are structured in the same manner as for the inception period and will be financed from the interest charged on micro-credits;

aa) Administration services – services performed by the Credit Agency as mentioned in chapter D point 36 Section V from request for proposals;

bb) Risk level - the percentage of micro-credits that was declared lost and was written off.

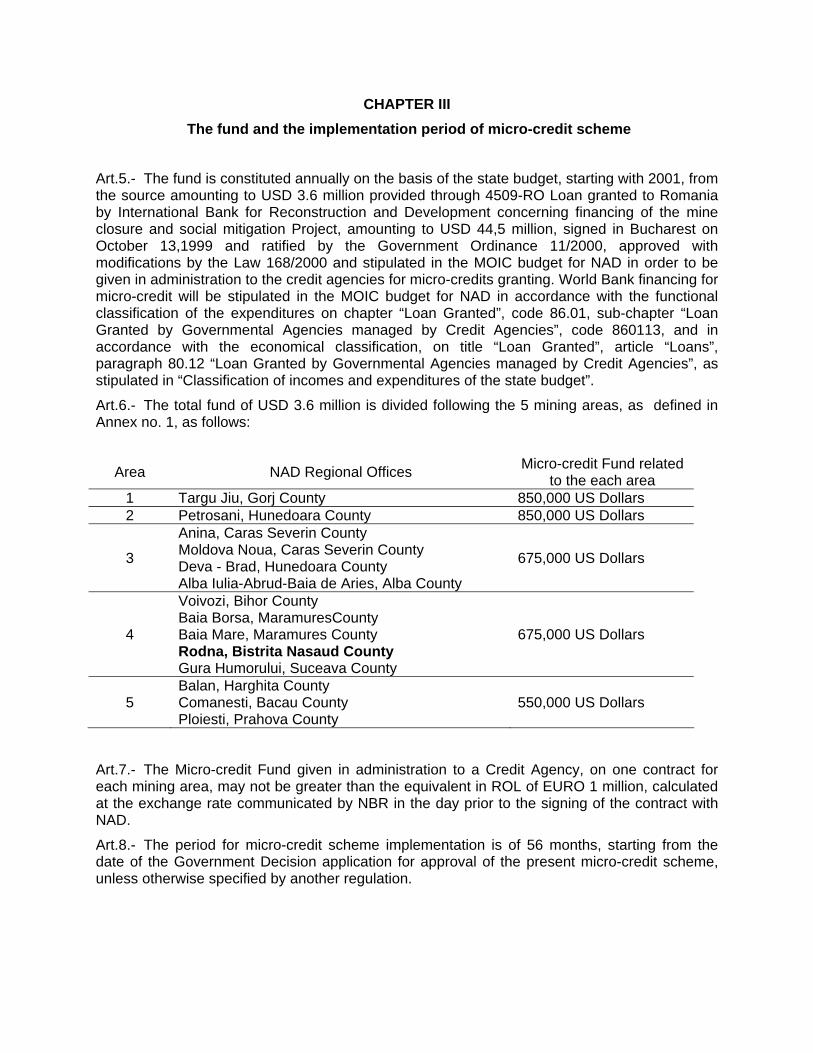

CHAPTER III The fund and the implementation period of micro-credit scheme

Art.5.- The fund is constituted annually on the basis of the state budget, starting with 2001, from the source amounting to USD 3.6 million provided through 4509-RO Loan granted to Romania by International Bank for Reconstruction and Development concerning financing of the mine closure and social mitigation Project, amounting to USD 44,5 million, signed in Bucharest on October 13,1999 and ratified by the Government Ordinance 11/2000, approved with modifications by the Law 168/2000 and stipulated in the MOIC budget for NAD in order to be given in administration to the credit agencies for micro-credits granting. World Bank financing for micro-credit will be stipulated in the MOIC budget for NAD in accordance with the functional classification of the expenditures on chapter “Loan Granted”, code 86.01, sub-chapter “Loan Granted by Governmental Agencies managed by Credit Agencies”, code 860113, and in accordance with the economical classification, on title “Loan Granted”, article “Loans”, paragraph 80.12 “Loan Granted by Governmental Agencies managed by Credit Agencies”, as stipulated in “Classification of incomes and expenditures of the state budget”. Art.6.- The total fund of USD 3.6 million is divided following the 5 mining areas, as defined in Annex no. 1, as follows:

Area NAD Regional Offices Micro-credit Fund related to the each area

1 Targu Jiu, Gorj County 850,000 US Dollars 2 Petrosani, Hunedoara County 850,000 US Dollars

3

Anina, Caras Severin County Moldova Noua, Caras Severin County Deva - Brad, Hunedoara County Alba Iulia-Abrud-Baia de Aries, Alba County

675,000 US Dollars

4

Voivozi, Bihor County Baia Borsa, MaramuresCounty Baia Mare, Maramures County Rodna, Bistrita Nasaud County Gura Humorului, Suceava County

675,000 US Dollars

5 Balan, Harghita County Comanesti, Bacau County Ploiesti, Prahova County

550,000 US Dollars

Art.7.- The Micro-credit Fund given in administration to a Credit Agency, on one contract for each mining area, may not be greater than the equivalent in ROL of EURO 1 million, calculated at the exchange rate communicated by NBR in the day prior to the signing of the contract with NAD. Art.8.- The period for micro-credit scheme implementation is of 56 months, starting from the date of the Government Decision application for approval of the present micro-credit scheme, unless otherwise specified by another regulation.

CHAPTER IV Objectives of micro-credit scheme

Art.9.- The support of the enterprises having less than 50 employees, employed on the basis of

individual labor contract, persons licensed to carry on independent activities and family

associations established on the basis of the Decree-Law 54/1990 or of any other legal acts, as

well as any natural person who presents a well grounded proposal for the purpose of initiation

and development of a business on the operating area of the micro-credit scheme.

Art.10.- Stimulation of employment of the unemployed persons located in the operating area of

the micro-credit scheme.

Art.11.- Stimulation of diversification of the economic environment by developing the private

sector and the profit generating activities in the operating area of the micro-credit scheme.

Art.12.- The support of the employment of the redundant people in order to become

entrepreneurs, beneficiary of micro-credits that may establish small enterprises and support

them in the development of the business for which the loan was requested.

Art.13.- The support of entrepreneurs who develop their business in the workspace centers that

are to be established in 14 regions in the operating area of the micro-credit scheme, as part of

the program "Workspace Centers", included in the "Social Mitigation" component of the project.

Art.14.- Establishment the criteria for selecting credit agencies and authorization of the selected

credit agencies for granting micro-credits to the recipients from the mining areas through a

revolving financing mechanism and according to the provisions of the present micro-credit

scheme.

Art.15.- Stimulation of attracting of independent businesses so that they may become legal.

CHAPTER V Type of micro-credits beneficiaries

Art.16.- Private own capital enterprises, having their registered head-office in one of the localities placed in the operating area of the micro-credit scheme and less than 50 employees with individual labor contract. Art.17.- Regional branches of the private own capital enterprises which develop their activity in the operating area of the scheme and less than 50 employees with individual labor contract.

Art.18.- Family associations and persons authorized to carry on independent activities and established on the basis of the Decree-Law 54/1990 or of any other statutory acts, located in the operating area of the micro-credit scheme. Art.19.- Any natural person who submits a viable proposal for setting up and development of a business in the operating area of the micro-credit scheme, following the authorization in accordance with law.

CHAPTER VI

Selection of Credit Agencies Art.20.- Within 7 working days, starting from the date the Government Decision approving the present scheme is published in the Official Gazette Part I, NAD will proceed with the organization of a public information campaign consisting of: a) publication in a national newspaper of wide circulation, in regional newspapers from the

counties belonging to the operating area of the micro-credit scheme as well as in an specialized newspaper, of the specific advertisement prepared in compliance with the IBRD procedures, containing the invitation to the interested Credit Agencies to submit to NAD expressions of interest for "Micro-finance Management", position 12 of the Annex 6 of PAD, as per annex no. 2;

b) communication of the advertisement mentioned at a) to the Embassies of the countries known as being experienced in development of micro-credit programs;

c) direct information, according to the IBRD procedures, using fax transmission, mail, e-mail and any other communication form that can confirm the reception of the message in writing, of the Credit Agencies (NGO) from inland and from abroad, known as entities offering such services.

Art.21.- Until the date specified in the advertisement from Art. 20, the interested Credit Agencies shall transmit to NAD PIU the expressions of interest, at the address and person mentioned in the advertisement. Art.22.- NAD PIU shall proceed, in accordance with IBRD procedures:

a) drawing up the long lists for each of the 5 regions; b) evaluation by the evaluation committee, on the basis of the criteria published in the advertisement, of the expressions of interest submitted by the Credit Agencies; c) preparing the 5 short lists, according to the 5 areas; d) forwarding to the IBRD the short lists drawn up for comments; e) notifying the Credit Agencies that have not been selected; f) transmitting the Request for Proposals (RFP) to the short listed credit agencies.

Art.23.- Minister of Industry and Commerce, coordinator of the “Mine Closure and Social Mitigation Project” according to GD 418/2000, shall establish through order the score level for evaluation criteria applied to technical proposals from Section II – “Data Sheet” 9.5.3., based on NAD PIU proposal, with the support of MOIC PMU and endorsed by NAD’ s General Director, complying with the World Bank procedures. This information shall be included in the RFP to be transmitted to the short listed credit agencies.

Art.24.- The RFP will be transmitted to the short listed Credit Agencies by express courier; costs related to the transmittal will be paid in accordance with GO 11/2000 for ratify of Loan Agreement between Romania and IBRD concerning the financing of the Mine Closure and Social Mitigation Project, amounted of US$ 44.5 million, signed at Bucharest on October 13, 1999 and approved with modifications by Law 168/2000. Art.25.- The RFP, as presented in annex no. 3, prepared following the standard form of selection of consultants based on cost and quality, edited by the World Bank in January, 1997 and revised in September, 1997 and January, 1999, shall contain the following: a) Letter of invitation (section I); b) Information to credit agencies (section II); c) Technical proposal – standard form (section III); d) Financial proposal – standard form (section IV); e) Terms of reference (section V). Art.26.- The procedures related to the submission of proposals, correspondence with and notification of Credit Agencies, as well as to the public opening, evaluation and negotiation of the contracts will be performed in accordance with the IBRD procedures included in the “World Bank Guidelines for selection of consultants based on cost and quality”, edited by the World Bank in January 1997, revised in September, 1997 and January 1999. Art.27.- Within 14 calendar days from receiving of “No Objection” from the World Bank, NAD PIU will invite the winners for negotiation of the contract, for the micro-credit fund management in mining areas, for which standard form of contract is presented in annex no. 4. Art.28.- The committee for negotiating the contract, established according to the provisions of GD 418/1999 and according to the provisions of IBRD, is empowered with the negotiation of the contracts with the wining CA in the period of its proposal validity. Art.29.- Should the negotiations failed to lead to the conclusion of a acceptable contract in the period of validity of offer specified in the RFP, NAD reserves itself the right that, after informing IBRD, to stop the negotiations with the selected CA, informing it in writing about the reasons for which the negotiations have been stopped. Art.30.- Within a term of two weeks from the date of the notification under art. 29 of the rejected CA, NAD PIU shall invite for negotiation the next CA qualified in the final evaluation report if its proposal is still valid. Art.31.- NAD PIU, upon receiving the agreement form the next CA to maintain its proposal, shall request the approval of IBRD for extension of period of validity of proposal. Art.32.- Should the proposal of the next qualified CA is no more within the period of validity of the proposal for the contract negotiations and signing, NAD PIU shall request the said CA to extend the validity period. Art.33.- Should within a term of 5 working days from the date of notification of the CA qualified next place in the final evaluation report the said CA does not send an answer from which it to result its agreement to took part in negotiation, NAD PIU shall ask the next CA qualified in the final evaluation report.

CHAPTER VII

Accepted risk level in the recovery of the public funds granted by NAD to credit agencies for micro-credit lending

Art.34.- Accepted risk level in the recovery of the public fund to state budget, managed by NAD in order to be granted to credit agencies for micro-credit lending, is maximum 15% from the total loan portfolio. Art.35.- Accepted risk level by present micro-credit scheme, in the recovery of the public fund granted by NAD to credit agencies for micro-credit lending, will be negotiate with NAD but will not exceed 15% from the each CA total loan portfolio. Art.36.- Each CA, which manages a part from micro-credit fund, will create a loan loss provision in amount from a minimum 50% from the accepted risk level in the recovery of the public fund granted by NAD to credit agencies for micro-credit lending. Art.37.- The write off micro-credits will not exceed 15% from total credit portfolio of each CA. Art.38.- The level of the provisions made by CAs will be certified by an independent auditor, which will be contracted and remunerated by NAD, in accordance with article 3 (2) from GO 11/2000.

CHAPTER VIII

Financial Flow Chart Art.39.- The selected CA will open and maintain a foreign currency account at a commercial bank agreed with the NAD, dedicated for trances from micro-credit fund.

Art.40.- PMU-MOIC, at NAD-PIU request, will transfer into CA account, as indicated at art. 39, the respective trances, with a limit of amounts negotiated.

Art.41.- PMU-MOIC, at NAD-PIU request, will transfer into NAD PIU account opened at the State Treasury, amounts representing the CA service charges.

Art.42.- NAD will disburse to CA amounts for service charges for the inception period, in accordance with the negotiated contract.

Art.43.- The selected CA will open and maintain a local currency account designated for micro-credits, at the commercial bank agreed with NAD, for the transfer of amounts in local currency in the state treasury in one of localities, which is near of its regional office within the operating area. This account is also used for reimbursing of micro-credits from beneficiaries.

Art.44.- The selected CA will open and maintain a local currency account at the commercial bank agreed with NAD, designated for reimbursement of the interest from the beneficiaries.

Art.45.- The selected CA will open and maintain a local currency account at the State Treasury within the operating area, and will reimburse amounts from the account opened in conformity with art. 43 and amounts for service charges.

Art.46.- The selected CA will exchange the hard currency amounts form its account opened at the commercial bank into local currency and transfer the resulted amounts in its account opened in conformity with art. 43. These amounts will be transferred at the State Treasury and will be transferred into Beneficiaries State Treasury accounts or will pay the beneficiary’s suppliers.

Art.47.- The Beneficiary will receive the micro-credit amounts in its account opened at the state treasury (for working capital, suppliers’ payments) or will receive the contracted goods and/or services paid directly by the CA, according with the provisions of the contract concluded with the CA.

Art.48.- The first portion of the fund contracted with NAD will be subject of negotiations between the CA and NAD, based on CA experience, total volume of micro-credit granted, and actual rate of reimbursements, and will be indicated in the contract, not exceeding in any case 200,000 US$.

Art.49.- The value of the following portions of the fund, to the extent of the fund contracted with NAD, will be requested by the CA upon the presentation of a financing need estimated according with the selected micro-credit applications.

Art.50.- The minimum value of any fund portion is 50,000 US$.

Art.51.- The beneficiaries will repay the micro-credit, according to the provisions from the contract, in the account opened according to art. 43.

Art.52.- The beneficiaries will repay the interest in the account opened according to art.44.

Art.53.- The amounts collected from the repayment of micro-credits in the account opened according to art. 43 will be transferred in the account opened according to art. 45 for the payment of the amounts to beneficiaries or their suppliers, from the newly lent micro-credits.

Art.54.- The amounts collected from the payment of interests for the micro-credits according to art. 44 will be used for the payment of the CA charge (commission), as agreed within the contract, and the exceeded amounts will be transferred in the account opened according art. 43, for a new financing cycle.

Art.55.- The amounts collected by CA in the account opened according to art. 43 from the repaying the micro-credits beginning with the 57th month from the date the present government decision is issued in the Official Monitor, will be transferred in a bank account in ROL-s opened by NAD at the state treasury, dedicated to micro-credits reimbursement.

Art.56.- NAD, in accordance with art. 22 from the Government Ordinance no. 40/2000, will repay monthly the gathered amounts to MOF, if the GOR will not decide otherwise.

Art.57.- All CA reimbursements and disbursements will be presented monthly to NAD.

Art.58.- Using of funds from interest and for operational costs, and if the case may be, transforming of the exceed into micro-credits, will be made upon the prior written approval from NAD.

CHAPTER IX Collateral and Interests Level

Art.59.- The CA will negotiate with each beneficiary the value and the nature of the collateral considered acceptable for each micro-credit, based on risk evaluation.

Art.60.- The level of collateral requested by CA will be establish in each case and should be made to obtain a security cover of realizable assets as close as is feasible to the nominal value of the credit in each case.

Art.61.- The whole responsibility for the appreciation of the value of collateral for each micro-credit will rest exclusively by CA.

Art.62.- (1) The interests charged to micro-credit recipients may not exceed the amount of the commission due to the credit agency for the operating of micro-credit fund granted by NAD, as specify in the contract.

(2) CAs are allow to grant credit with preferential interests on each recipients, but this interest may not exceed the interests charged by the commercial banks.

(3) The CAs may not make profit from the administration of the scheme.

CHAPTER X

Management of public funds awarded to credit agencies as funds for micro-credit lending

Art.63.- During 30 days from the contract signing with each CA, the said CA will promote a initial public information campaign consist in:

a) Publish in a wide national newspaper of the methodology for micro-credit granting;

b) Publish in a local newspaper from each county from operating area of the micro-credit of the methodology for micro-credit granting;

c) Display at the NAD regional offices of the methodology for micro-credit granting;

d) Organization, with NAD regional offices support, of a public information conference with local authorities, decentralized state institutions, local consortia, private enterprises and trade unions, chamber of commerce and industry from all counties that micro-credit scheme operating area refers to, business unions, promotional conference that will be held in one of the mining regions related to the contract.

Art.64.- The CA will organize public information campaigns during the implementation period, as many times as necessary, through the Public Information and Social Dialogue within the Social Mitigation component of the project.

Art.65.- In maximum 60 normal days from contract signing, the CA will submit to NAD the first report regarding organizing and functioning condition completion, as so is specified in the contract.

Art.66.- Starting with the date specify by publicity campaign, the applicants will submit application to CA for micro-credits.

Art.67.- The CA, on the basis of GO 40/2000 art. 11 alin. 3 will proceed with analysis and evaluations of applications, based on the methodology specify in their proposals, methodology annexed to the contract with NAD.

Art.68.- The methodology presented in proposal will be based on procedures from annex 6 and will take part from contract agreed with NAD.

Art.69.- In 30 calendar days from the registration of the application, the CA are obliged to notify the applicants on the decision.

Art.70.- During the decision taking period, the CA may request supplementary information to the applicants.

Art.71.- CA has the obligation to support the applicants in drawing up the documentation stipulated in the methodology for obtaining micro-credits.

Art.72.- The applicants whose applications received favorable decisions will go to the CA for negotiating and signing the contract, with the standard format shown in annex no. 7.

Art.73.- The CA will sign contracts and lend micro-credits, within the amount limits available in the account opened according to art. 39, the amounts in the ROL-s account, opened according to art. 42 and depending on the repayments schedule.

Art.74.- The CA will monitor each micro-crediting contract by:

a) Supervising the use of funds on each destination, according to the contracts concluded with the beneficiaries;

b) Supervising the compliance with the contracts referring to clauses, micro-credit repayment and its interest, payment deadline;

c) Organizing meetings to check the beneficiaries` activity at the end of each quarter;

d) Checking the activity of beneficiaries who have been late in paying the rates and/or the interest and their notification starting with the fifth working day from their due date;

e) Checking if the guarantee for the micro-credit are in place;

f) Taking all necessarily measures to comply with the contract conditions on the funds use, repayment in time of the credits and interest.

Art.75.- The maximum interest charged by the CA will be negotiated and indicated in the contract concluded with NAD; any modification thereon will not modify the micro-credit contracts signed prior to modification date.

Art.76.- Following the evaluation report, NAD is reserving, under the provisions of the article 9. (2) from Governmental decision no 40/2000, the right to notify within 5 working days form the its approval by the CCPI, the findings regarding the break of the micro-credit scheme provisions, the terms of the contract between NAD and the CA or the contracts concluded between the CA and micro-credit beneficiaries.

Art.77.- If within 45 calendar days from notification, the CA will not respect the provisions of the contact, NAD will unilateral terminate the Contract.

Art.78.- If the evaluation report indicates penal or breaching, within 5 working days from the CCPI report approving, NAD will take all necessarily measures indicated in art. 10 from GO 40/2000.

Art.79.- If the contract is terminated under the provisions of article 4, (4) from the Governmental decision no 40/2000, NAD will take all the liabilities regarding the micro-credit fund management and (1) will transfer, based on the proved performance criteria, to another prior selected CA, based on the World Bank procedures, specified in the guidelines for selection of consultants based on and cost quality, edited by the World Bank in January 1997 and revised in September 1997 and January 1999; (2) will select and sign a new contract through public bidding with another CA.

Art.80.- The CA will remain responsible after the micro-credit scheme implementation for the reimbursement of the on-going micro-credit and for the reimbursement of those amounts to NAD, in order to return the fund to the state budget, under the provisions of the Governmental decision no 40/2000, article 22.

Art.81.- Within 30 calendar days from the termination of the contract, the CA will transfer to NAD the amounts representing the credit loss provisions accumulated on the scheme functioning duration.

Art.82.- The possible plus between the evaluated operating costs and the effective operating costs indicated in the annual balance sheet or in the audit report, recorded by the CA, will be added to the micro-credit fund.

CHAPTER XI The mechanism for reporting, evaluation,

Supervision and control of CA’s activities Art.83.- CAs shall provide NAD with the following reports:

a) By the tenth working day of each month, the report on operating costs (annex no. 8.1);

b) By the tenth working day of each month, the report on the loans portfolio (annex no. 8.2);

c) By the tenth working day of each month, the report on micro-credit lent broken down by categories of beneficiaries (annex no. 8.3);

d) Annual report on the project progress, to be submitted to NAD within 30 days from the end of each fiscal year (point 40, section V, annex no. 3);

e) Final report at the contract completion (point 40, section V, annex no. 3);

f) Any other report that NAD might reasonably request.

Art.84.- CAs will co-operate with NAD Regional Offices in what concerns the reporting and monitoring requirements stipulated in the negotiated contract between CA and NAD.

Art.85.- CA is bound to notify NAD whenever it occur any deviation that could jeopardize the good progress of the contract between CA and NAD.

Art.86.- Following receipt of notification from the CA, the General Director of NAD shall appoint through a decision a committee responsible for investigation and proposal of solving solutions.

Art.87.- CA has the duty of and is responsible for the accounting records related to the micro-credit fund and to the operating cost service as well, in accordance with the national and international standards and is fully responsible for those records.

Art.88.- CA shall allow the access of NAD to the records kept according to art. 87, within the activity program of the working days, following a two days advance notice by NAD.

Art.89. – (1) CA shall contract yearly and no later than six months from the end of the fiscal year, in accordance with the legislation on public procurement and after having received comments from the IBRD, an independent auditor to review its activity, according to the national and international standards.

(2) CA auditing, regarding micro-credit lending, by its own audit department of the public institution to whom NAD is subordinating and by the institution granting micro-credit.

(3) CA is bound to make available to the General Department for internal audit within the Ministry of Finance, all data and information requested in order to control the operations or the essential activities (established on the reprezentativity and evaluation principles) following the entire logical and chronological chain, in order to ensure the closure of the operational circuit under formal and practical aspects regarding the objective or the object of audit, according to the trasability principle stipulated in the minister of finance order no. 1.070/2000, every time that the audit will be done by the audit inspections and / or as the case may be.

Art.90 - CA is bound to make available to NAD the audit report and all necessary documents for the annual appraisal by NAD of CA’s performances, together with the annual report.

CHAPTER XII

Final and transitory provisions Art.91.- The annexes 1 to 8 shall be deemed to form an integral part of this micro-credit

scheme.

Art.92.- This micro-credit scheme has been prepared by NAD and MOIC and refers

exclusively to the management of the micro-credit fund financed by 4509-RO Loan granted to

Romania by International Bank for Reconstruction and Development concerning financing of the

mine closure and social mitigation Project, amounting to USD 44,5 million, signed in Bucharest

on October 13,1999 and ratified by the Government Ordinance 11/2000, approved with

modifications by the Law 168/2000.

Art.93.- While putting into the practice the micro-credit scheme, this methodology can be

amended, upon General Director of NAD request and approved by IBRD, by Ministry of Industry

and Commerce.

ANNEX 1

to micro-credit scheme

ANNEX No. 2

to micro-credit scheme

ROMANIA

Mine Closure and Social Mitigation Project

Loan No 4509 – RO Micro-Finance Management

Expressions of Interest

This request for expressions of interest follows the General Procurement Notice for this project that appeared in Development Business No. 538 of 16th July 2000. The Government of Romania has received a loan from the International Bank for Reconstruction and Development (IBRD) in the amount of 44.5 million US Dollars equivalent toward the cost of the Mines Closure and Social Mitigation Project. It intends to apply part of the proceeds of this loan to payments under this project for the procurement of Micro-Finance Management consultancy services for the component. The Social Mitigation component under the Mine Closure and Social Mitigation Project includes a sub-component establishing a Micro-Credit Fund to support micro-finance services in the 14 mining regions. The programme will be implemented by Micro-Finance Institution(s) (MFI) that will manage the credit line in accordance with the project requirements and guidelines and specified in an operating manual (to be provided by the NAD). The project aims to facilitate new job creation and encourage entrepreneurs to develop their businesses for hiring unemployed people. Loans will also be provided to set up new micro-enterprises, which will be assisted for development, and for maintaining the created jobs. For the purpose of stimulating micro and small enterprise development in the affected mining areas, funding will be provided from the IBRD loan for the establishment and operation of a Micro Credit Fund [MCF].

For project management purposes, the affected mining regions have been grouped into five

areas designated by the location of NAD’s local offices as follows:

Area NAD Office locations 1 Targu Jiu, Gorj County 2 Petrosani, Hunedoara County

3

Anina, Caras Severin County Moldova Noua, Caras Severin County Deva – Brad, Hunedoara County Alba Iulia – Abrud – Baia de Aries, Alba County

4 Voivozi, Bihor County

Baia Borsa, Maramures County

Baia Mare, Maramures County

Rodna, Bistrita Nasaud County

Gura Humorului, Suceava County

5 Balan, Harghita County Comanesti, Bacau County Ploiesti, Prahova County

The numbering assigned to the Areas is solely for administrative reference - each area

can be taken as having the same high development priority.

This project is now seeking to appoint micro funds institutions [MFIs] as the micro credit fund

manager(s) for one or more of the grouped mining areas following a competitive tendering

process. Prospective contractors are invited to tender for the management of the MCF in

one, all or a combination of these areas and should clearly state their choice on their

submissions. Each area should be the subject of a separate tender.

The main objectives of the sub-component are development of entrepreneurial capacity of

people from mining regions, creation of a favourable business environment, hiring of a

measurable portion of unemployed people, creation of regional development strategies. It is

expected to create over 2,000 jobs, during the life of the project.

Prospective contractor(s) must:

• Qualify as legally competent credit agencies in compliance with Government Ordinance No.40 of 31.01.2000 “On Licensing Credit Agencies to Manage Funding for Micro-Credit”.

• Furnish details of past accomplishment in MCFs implementation and portfolio management with particular reference to loan delinquency rates, repayment rates, loan loss rates and profitability.

• Supply the names of all organisations from which they have received micro credit fund management contracts with reference information (current addresses, telephone numbers and contact personnel) as well as a brief report on the work performed and the outcomes.

• Nominate an operational partner which is registered in Romania including the court decision allowing the organisation to operate in Romania, a copy of the Official Monitor declaration authorising the organisation to operate and the official fiscal code of the organisation.

• Furnish details of their existing micro loan portfolios as well as copies of independently audited statements of account for the past three years, or for the most recent years for which accounts are available.

• Local experience could be an advantage • Furnish a copy of the organisation's accounting manual and any other relevant and

accounting procedures. • Furnish evidence of success in originating enterprise projects, project evaluation

methodology and credit monitoring procedures. • Furnish a copy of its corporate organisation chart. • Furnish a statement of its personnel training and development programs. • Furnish a program plan, which clearly defines project implementation methodology and

the target results with a corresponding plan timeframe. • Furnish a detailed forward project budget; • Furnish a description (with examples) of credit evaluation and monitoring systems. • Furnish CVs of key personnel who will be involved in the implementation of the project. It

is expected that the personnel will demonstrate practical experience in setting up and managing successful micro fund programs and the ability to develop collaborative relationships with counterparts, partners and allied organizations;

• Provide documents that shall demonstrate that on the date of their participation in the biding they do not have any overdue tax obligations.

NAD now invites eligible consultants to indicate their interest in providing the services. Interested consultants must provide information indicating that they are qualified to perform the services (brochures, description of similar assignments, experience in similar conditions, availability of appropriate skills among staff, etc.). Consultants may associate to enhance their qualifications. Consultants will be chosen in accordance with Quality and Cost-based Selection procedures set out in the World Bank’s Guidelines – Selection and Employment of Consultants by World Bank Borrowers January 1997(revised September 1997). Interested consultants may obtain further information at the address below. Expressions of interest must be delivered to the address below by close of business on 19.02.2001.

National Agency of Development and Implementation Of the Reconstruction Programs in Mining Regions

Project Implementation Unit Mrs. Elena Gheorghe; Director PIU

152 - 154 Calea Victoriei, lobby floor, room 18-19, Bucharest, Romania Phone: 401 231 66 33

Email: [email protected]

ANNEX No. 3

to micro-credit scheme

REQUEST FOR PROPOSALS For selecting and licensing credit agencies for the administration of public fund

amounted to US$ 3.6 million in order to grant micro-credits

Section 1. Letter of Invitation National Agency for Development and Implementation of the Reconstruction

Programs in Mining Regions 152-154 Calea Victoriei Room 18-19, Lobby Floor

Bucharest Romania

Dear [insert: Name of Consultant]: 1. The Government of Romania has received a loan (hereinafter called “loan”)

from the International Bank for Reconstruction and Development (IBRD)

toward the cost of the Mine Closure and Social Mitigation Project and intends

to apply a portion of this loan to eligible payments under this Contract.

2. The National Agency for Development and Implementation of the

Reconstruction Programs in the Mining Regions (NAD hereinafter called

“Client”) now invites proposals to provide the following consulting services:

“To administer micro credit finance scheme in one or more of the designated

regions in order to develop small businesses in the mining regions”

More details on the services required are provided in the attached Terms of

Reference (Section V)

3. The Request for Proposal (RFP) has been addressed to the following

shortlisted consultants:

[insert: List of Shortlisted Consultants and their origin country]

4. Credit Agency will be selected based on World Bank procedures under Quality

and Cost Based Selection (QCBS) and procedures described in this RFP.

5. The RFP includes the following documents:

Section 1 - Letter of Invitation

Section 2 - Information to Credit Agencies

Section 3 - Technical Proposal - Standard Forms

Section 4 - Financial Proposal - Standard Forms

Section 5 - Terms of Reference

6. Please inform us, upon receipt that you received the letter of invitation.

Yours sincerely, ……………………. NAD PIU Director

Section 2. Information to Credit Agencies 1. Introduction 1.1 NAD will select a credit agency among those listed in the

Letter of Invitation (hereinafter called credit agencies), in accordance with the method of selection specified in the RFP and detailed in the edition of the Guidelines for Selection and Employment of Consultants by World Bank Borrowers, edited by World Bank in January 1997 and revised in September 1997 and January 1999 (The Guidelines for Consultants).

1.2 The Credit Agencies are invited to submit a technical

proposal and a financial proposal, as specified in the Section II point 3 (preparation of proposals). The wining proposal after the evaluation process will be the basis for contract negotiations and ultimately for a signed contract between NAD and selected credit agency.

1.3 The contract shall be implemented in accordance with

the phasing indicated in Section II point 9.1.3 (Data Sheet).

1.4 The credit agencies must familiarise themselves with

local conditions and take them into account in preparing

their proposals. To obtain firsthand information on the assignment and on the local conditions, credit agencies are encouraged to visit the NAD before submitting a proposal and to attend a pre-proposal conference organised at date and place specified in Section II point 9.1.4. Attending the pre-proposal conference and visiting NAD are optional. The credit agencies’ representative should contact the officials named in Section II point 9.1.4 and 9.2.1 (Data Sheet), to arrange for their visit or to obtain additional information on the pre-proposal conference. Credit agency should ensure that these officials are advised of the visit in adequate time to allow them to make appropriate arrangements.

1.5 NAD will provide the inputs specified in the Section II

point 9.1.5 (Data Sheet), needed to carry out the services, and make available relevant project data and reports.

1.6 The credit agencies are informed that (i) the costs of

preparing the proposal and of negotiating the contract, including a visit to the NAD, are not reimbursable as a direct cost of the assignment; and (ii) the NAD is not bound to accept any of the proposals submitted.

1.7 Bank policy requires that credit agencies provide

professional, objective, and impartial advice and at all times hold the NAD’s interests paramount, without any consideration for future work, and strictly avoid conflicts with other assignments or their own corporate interests. Credit agencies shall not be hired for any assignment that would be in conflict with their prior or current obligations to other clients, or that may place them in a position of not being able to carry out the assignment in the best interest of the NAD.

1.7.1 Without limitation on the generality of this rule,

credit agencies shall not be hired under the circumstances set forth below:

(a) A firm which has been engaged by the

NAD to provide goods or works for a project, and any of their affiliates, shall be disqualified from providing consulting services as specified in TORs (Section V)

for the same project. Conversely, firms hired to provide consulting services for the preparation or implementation of a project, and any of their affiliates, shall be disqualified from subsequently providing goods or works or services related to the TORs (Section V) within this project (other than a continuation of the firm’s earlier consulting services) for the same project.

(b) The credit agencies or any of their affiliates

shall not be hired for any assignment which, by its nature, may be in conflict with another assignment implemented by them.

1.7.2 The credit agencies may be hired for downstream

work, when continuity is essential, in which case this possibility shall be indicated in Section II point 9.1.7.2 also mentioned in para. 1.7.1 a), based on credit agencies performance of carried out the assignment. It will be the exclusive decision of the NAD whether or not to have the downstream assignment carried out, and if it is carried out, which credit agencies will be hired for the purpose.

1.7.3 Any previous or ongoing participation in relation to

the assignment by the firm, its professional staff, or its affiliates or associates under a contract with the World Bank may result in rejection of the proposal. The credit agencies should clarify their situation in that respect with the NAD before preparing the proposal.

1.8 It is the Bank’s policy to require that borrowers (including

beneficiaries of Bank loans), as well as credit agencies under Bank-financed contracts, observe the highest standard of ethics during the selection and execution of such contracts. In pursuance of this policy, the Bank:

(a) defines, for the purposes of this provision, the

terms set forth below as follows:

(i) “corrupt practice” means the offering, giving, receiving, or soliciting of anything of

value to influence the action of a public official in the selection process or in contract execution; and

(ii) “Fraudulent practice” means a misrepresentation of facts in order to influence a selection process or the execution of a contract to the detriment of the borrower, and includes collusive practices among credit agencies (prior to or after submission of proposals) designed to establish prices at artificial, non-competitive levels and to deprive the borrower of the benefits of free and open competition.

(b) will reject a proposal for award if it determines that

the firm recommended for award has engaged in corrupt or fraudulent activities in competing for the contract in question;

(c) will cancel the portion of the loan allocated to the

firm’s contract if it at any time determines that corrupt or fraudulent practices were engaged in by representatives of the borrower or of a beneficiary of the loan during the selection process or the execution of that contract, without the borrower having taken timely and appropriate action satisfactory to the Bank to remedy the situation;

(d) will declare a firm ineligible, either indefinitely or

for a stated period of time, to be awarded a Bank-financed contract if it at any time determines that the firm has engaged in corrupt or fraudulent practices in competing for, or in executing, a Bank-financed contract; and

(e) will have the right to require that, in contracts

financed by a Bank loan, a provision be included requiring consultants to permit the Bank to inspect their accounts and records relating to the performance of the contract and to have them audited by auditors appointed by the Bank.

1.9 The credit agencies shall not be under a declaration of

ineligibility for corrupt and fraudulent practices issued by the Bank in accordance with the above sub para. 1.8.

1.10 The credit agencies shall furnish information as

described in the Financial Proposal submission form (Section IV) on commissions and gratuities, if any, paid or to be paid to agents relating to this proposal, and to execute the work if the firm is awarded the contract.

1.11 The credit agencies shall be aware of the provisions on

fraud and corruption stated in Annex 4 to Micro-credit scheme (Contract between NAD and credit agency) under the clauses indicated in Section II point 9 (Data Sheet).

2. Clarification

and Amendment of RFP Documents

2.1 The credit agency may request a clarification of any of the RFP documents up to the number of days indicated in Section II point 9.2.1 (Data Sheet). Any request for clarification must be sent in writing by paper mail, cable, telex, facsimile, or electronic mail to the NAD’s address indicated in Section II point 9 (Data Sheet). NAD will respond by cable, telex, facsimile, or electronic mail to such requests and will send written copies of the response (including an explanation of the query but without identifying the source of inquiry) to all invited credit agencies that intend to submit proposals.

2.2 At any time before the submission of proposals, the NAD

may, for any reason, whether at its own initiative or in response to a clarification requested by an invited firm, amend the RFP. Any amendment shall be issued in writing through addenda. Addenda shall be sent by mail, cable, telex, facsimile, or electronic mail to all invited credit agencies and will be binding on them. NAD may at its discretion extend the deadline for the submission of proposals.

3. Preparation of

Proposal 3.1 The credit agencies are requested to submit a proposal

(para. 1.2) written in the language(s) specified in Section II point 9 (Data Sheet).

Technical Proposal

3.2 In preparing the Technical Proposal, the credit agency is expected to examine the documents constituting this RFP in detail. Material deficiencies (omission in completing of one forms) in providing the information

requested may result in rejection of a proposal. 3.3 While preparing the Technical Proposal, credit agency

must give particular attention to the following:

(i) If a credit agency considers that it does not have all the expertise for the assignment, it may obtain a full range of expertise by associating with individual consultant(s) and/or other credit agency or entities in a joint venture or sub-consultancy, as appropriate. The credit agencies may associate with the other credit agencies invited for this assignment only with approval of the NAD as indicated in the Section II pint 9.3.3. (i). The credit agencies must obtain the approval of NAD to enter into a joint venture with credit agencies not invited for this assignment. The credit agencies are encouraged to seek the participation of local consultants by entering into a joint venture with, or subcontracting part of the assignment to.

(ii) It is desirable that the majority of the key

professional staff proposed be permanent employees of the firm or have an extended and stable working relationship with it.

(iii) Proposed professional staff must, at a minimum,

have the experience indicated in Section II point 9.3.3. (iv), preferably working under conditions similar to those prevailing in the NAD country.

(iv) Alternative professional staff shall not be

proposed, and only one curriculum vita (CV) may be submitted for each position.

(v) Reports to be issued by the credit agencies, as part

of this assignment must be in the language(s) specified in Section II point 9.3.3. (vi). It is desirable that the firm’s personnel have a working knowledge of the Romanian.

3.4 The Technical Proposal shall provide the following

information using the attached Standard Forms (Section III B):

(i) A brief description of the firm’s organization and an outline of recent experience on assignments of a similar nature, as stated in Section V, TORs.

(ii) Any comments or suggestions on the Terms of

Reference and on the data, a list of services, and facilities to be provided by the NAD (Section III C).

(iii) A description of the methodology and work plan

for performing the assignment (Section III D). (iv) The list of the proposed staff team by speciality,

the tasks that would be assigned to each staff team member, and their timing (Section III E).

(v) CVs recently signed by the proposed professional

staff and the authorized representative submitting the proposal (Section III F). Key information should include number of years working for the firm/entity and degree of responsibility held in various assignments during the last ten (10) years.

(vi) Estimates of the total staff input (professional and

support staff; staff time) needed to carry out the assignment, supported by bar chart diagrams showing the time proposed for each professional staff team member (Sections III E and G).

(vii) A detailed description of the proposed

methodology, staffing, and monitoring of training, if Section II point 9.3.4. (vii).

(viii) Any additional information requested in Section II

point 9.3.4 (viii). 3.5 The Technical Proposal shall not include any financial

information.

Financial Proposal

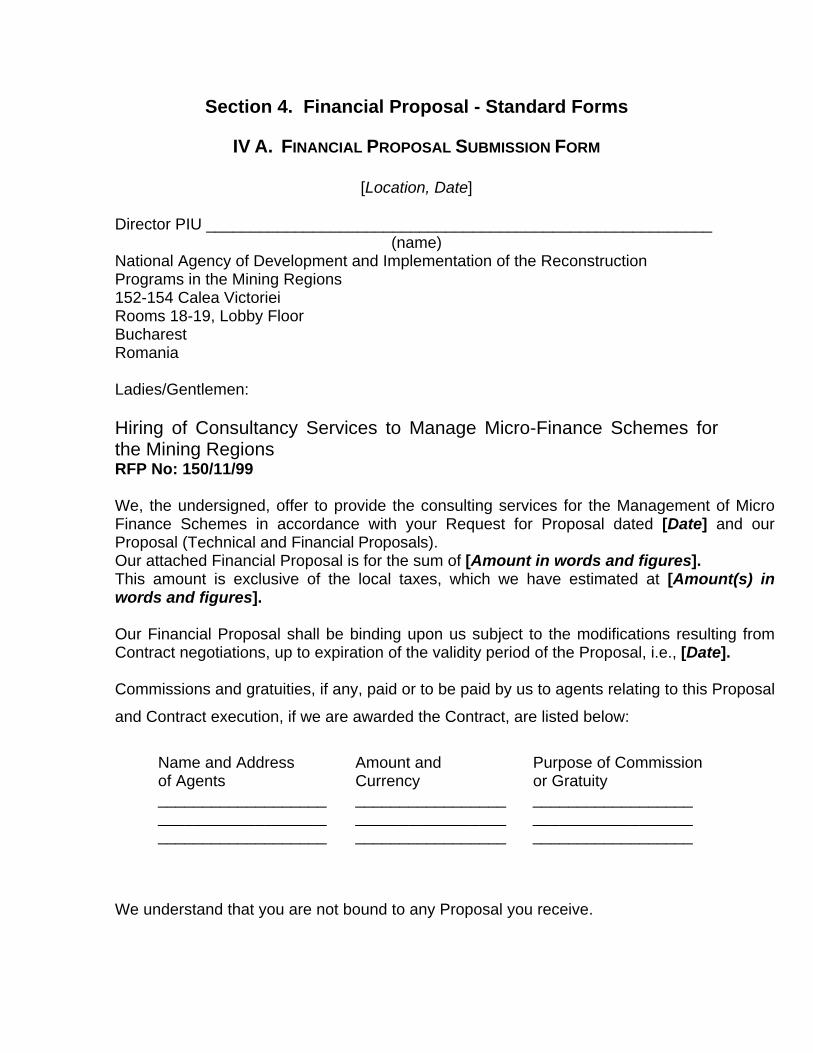

3.6 In preparing the Financial Proposal, the credit agencies are expected to take into account the requirements and conditions outlined in the RFP documents. The Financial Proposal should follow Standard Forms (Section IV). It lists all costs associated with the assignment, including (a) remuneration for staff (foreign

and local, in the field and at headquarters), and (b) reimbursable expenses such as subsistence (per diem, housing), transportation (international and local, for mobilisation and demobilisation), services and equipment (vehicles, office equipment, furniture, and supplies), office rent, insurance, printing of documents, surveys, and training, if it is a major component of the assignment. If appropriate, these costs should be broken down by activity and, if appropriate, into foreign and local expenditures.

3.7 The Financial Proposal should clearly estimate, as a

separate amount, the local taxes (including social security), duties, fees, levies, and other charges imposed under the applicable law, on the consultants, the sub-consultants, and their personnel (other than nationals or permanent residents of the government’s country), unless the Section II point 9 specifies otherwise.

3.8 The credit agencies may express the price of their

services in the currency of any Bank member country or in the European Currency Unit. The credit agencies may not use more than three foreign currencies. NAD may require credit agency to state the portion of their price representing local cost in the national currency if so indicated in Section II point 9.3.8.

3.9 Commissions and gratuities, if any, paid or to be

paid by credit agencies and related to the assignment will be listed in the Financial Proposal submission form (Section IV).

3.10 The Data Sheet (Section II point 9) indicates how long the proposals must remain valid after the submission date. During this period, the credit agency is expected to keep available the professional staff proposed for the assignment described in TORs. NAD will make its best effort to complete negotiations within this period. If the NAD wishes to extend the validity period of the proposals, the credit agencies who do not agree have the right not to extend the validity of their proposals.

4. Submission,

Receipt, and Opening of Proposals

4.1 The original proposal (Technical Proposal and Financial

Proposal) mentioned at Section II point 1.2, shall be

prepared in indelible ink. It shall contain no inter-lineation or

overwriting, except as necessary to correct errors made by

the firm itself. Any such corrections must be initialled by

the persons or person who sign(s) the proposals.

4.2 An authorised representative of the firm initials all pages

of the proposal. The representative’s authorisation is confirmed by a written power of attorney accompanying the proposal.

4.3 For each proposal, the credit agencies shall prepare the

number of copies indicated in Section II point 9.4.3. Each Technical Proposal and Financial Proposal shall be marked “ORIGINAL” or “COPY” as appropriate. If there are any discrepancies between the original and the copies of the proposal, the original governs.

4.4 The original and all copies of the Technical Proposal

shall be placed in a sealed envelope clearly marked “Technical Proposal,” and the original and all copies of the Financial Proposal in a sealed envelope clearly marked “FINANCIAL PROPOSAL” and warning: “DO NOT OPEN WITH THE TECHNICAL PROPOSAL.” Both envelopes shall be placed into an outer envelope and sealed. This outer envelope shall bear the submission address and other information indicated in Section II point 9 and be clearly marked, “DO NOT OPEN, EXCEPT IN PRESENCE OF THE EVALUATION COMMITTEE.”

4.5 The completed Technical and Financial Proposals must

be delivered at the submission address on or before the time and date stated in Section II point 9. Any proposal received after the closing time for submission of proposals shall be returned unopened.

4.6 After the deadline for submission of proposals, the

Technical Proposal shall be opened immediately by the evaluation committee. The Financial Proposal shall remain sealed and deposited with a respectable public auditor or independent authority until all submitted proposals are opened publicly.

5. Proposal

Evaluation Methodology

and evaluation criteria for tehnical proposal

General 5.1 From the time the bids are opened to the time the contract is awarded, if any credit agencies wishes to contact the NAD on any matter related to its proposal, it should do so in writing at the address indicated in Section II point 9. Any effort by the credit agencies to influence NAD in the proposal evaluation, proposal comparison or contract award decisions may result in the rejection of the credit agency’s proposal.

5.2 Evaluators of Technical Proposals shall have no access

to the Financial Proposals until the technical evaluation, including any Bank reviews and issuance of a "no objection" letter, is concluded.

Evaluation of Technical Proposals

5.3 The evaluation committee, appointed by the NAD as a whole, and each of its members individually, evaluates the proposals on the basis of their responsiveness to the Terms of Reference, applying the evaluation criteria, sub-criteria (typically not more than three per criteria), and point system specified in Section II point 9.5.3. Each responsive proposal will be given a technical score (St). A proposal shall be rejected at this stage if it does not respond to important aspects of the Terms of Reference or if it fails to achieve the minimum technical score indicated in Section II point 9.5.3.

5.4 The public opening and evaluation of the Financial

proposals: ranking of the proposals on the basis of cost and quality selection.

Public Opening and Evaluation of Financial Proposals: Ranking (QCBS Method)

5.5 After the evaluation of technical proposals is completed, the NAD shall notify those consultants whose proposals did not meet the minimum qualifying mark or were considered non-responsive to the RFP and Terms of Reference, indicating that their Financial Proposals will be returned unopened after completing the selection process. The NAD shall simultaneously notify the credit agencies that have secured the minimum qualifying mark, indicating the date and time set for opening the Financial Proposals. The opening date shall not be sooner than two weeks after the notification date. The

notification may be sent by registered letter, cable, facsimile, or electronic mail.

5.6 The Financial Proposals shall be opened publicly in the presence of the credit agencies’ representatives who choose to attend. The name of the credit agencies, the quality scores, and the proposed prices shall be read aloud and recorded when the Financial Proposals are opened. NAD shall prepare minutes of the public opening.

5.7 The evaluation committee will determine whether the Financial Proposals are complete (i.e., whether they have costed all items of the corresponding Technical Proposals; if not, NAD will cost them and add their cost to the initial price), correct any computational errors, and convert prices in various currencies to the single currency specified in Section II point 9. The official selling rates used, provided by the source indicated in Section II point 9, will be those in effect on the date indicated in Section II point 9. The evaluation shall exclude those taxes, duties, fees, levies, and other charges imposed under the applicable law; and to be applied to foreign and non-permanent resident consultants (and to be paid under the contract, unless the consultant is exempted), and estimated as per para. 3.7.

5.8 In case of QCBS, the lowest Financial Proposal (Fm) will

be given a financial score (Sf) of 100 points. The financial scores (Sf) of the other Financial Proposals will be computed as indicated in Section II point 9. Proposals will be ranked according to their combined technical (St) and financial (Sf) scores using the weights:

T [%]= the weight given to the Technical Proposal; P [%]= the weight given to the Financial Proposal; T + P = 1 indicated in the Data Sheet: S St T Sf P= × + ×% % .

The credit agency achieving the highest combined technical and financial score will be invited for negotiations.

6. Negotiations 6.1 Negotiations will be held at the address indicated in Section II point 9. The aim is to reach agreement on all points and sign a contract.

6.2 Negotiations will include a discussion of the Technical

Proposal, the proposed methodology (work plan), staffing and any suggestions made by the credit agency to improve the Terms of Reference. NAD and credit agency will then work out final Terms of Reference, staffing, and bar charts indicating activities, staff, periods in the field and in the home office, staff-months, logistics, and reporting. The agreed work plan and final Terms of Reference will then be incorporated in the “Description of Services” and form part of the contract. Special attention will be paid to getting the most the credit agency can offer within the available budget and to clearly defining the inputs required from the NAD to ensure satisfactory implementation of the assignment.

6.3 The financial negotiations will include a clarification (if

any) of the credit agency’s tax liability in the Romania, and the manner in which it will be reflected in the contract; and will reflect the agreed technical modifications in the cost of the services. Unless there are exceptional reasons, the financial negotiations will involve neither the remuneration rates for staff (no breakdown of fees) nor other proposed unit rates in the cases of QCBS.

6.4 Having selected the credit agency on the basis of,

among other things, an evaluation of proposed key professional staff, the NAD expects to negotiate a contract on the basis of the experts named in the proposal. Before contract negotiations, the NAD will require assurances that the experts will be actually available. NAD will not consider substitutions during contract negotiations unless both parties agree that undue delay in the selection process makes such substitution unavoidable or that such changes are critical to meet the objectives of the assignment. If this is not the case and if it is established that key staff was offered in the proposal without confirming their availability, the credit agency may be disqualified.

6.5 The negotiations will conclude with a review of the draft

form of the contract (standard form is presented in Annex 4 to micro-credit scheme). To complete negotiations NAD and the credit agency will initial the agreed contract. If negotiations fail, NAD will invite the credit agency whose proposal received the second highest score to negotiate a Contract.

7. Award of

Contract 7.1 The contract(s) will be awarded following negotiations.

After negotiations are completed, NAD will promptly notify other credit agencies on the shortlist that they were unsuccessful and return the unopened Financial Proposals of those credit agencies who did not pass the technical evaluation (para. 5.3).

7.2 The credit agency(s) is/are expected to commence the

assignment on the date and at the location specified in Section II point 9.7.2.

8. Confidentiality 8.1 Information relating to evaluation of proposals and

recommendations concerning awards shall not be disclosed to the credit agencies who submitted the proposals or to other persons not officially concerned with the process, until the winning credit agency has been notified that it has been awarded the contract.

9. Data Sheet

Clause

Reference in LOI

9.1.1 The name of the Client is: “National Agency of Development and Implementation of the Reconstruction Programs in the Mining Regions” The method of selection is: Quality and Cost Based Selection (QCBS), according to selection procedures described in The Guidelines for selection and employment of consultants by World Bank Borrowers The Edition of the Guidelines is: January 1997 Revised September 1997 and January 1999

9.1.2

Technical and Financial Proposals are requested: Yes

See Terms of Reference for further details

1.3 The assignment is phased: Yes, the project will operate for the operating period of the scheme [months]. The activity of the credit agencies will be reviewed and renewed on an annual basis subject to satisfactory performance defined in the TORs and the contract will be annually revised according to results of the evaluation. See Terms of Reference for further details

9.1.4 NAD will held a pre-proposal conference before the date of proposals submission al: Date_______________ Time______________ Address: Ministry of Industry and Commerce, Calea Victoriei no. 152 – 154, Bucharest 1, Room __________________ The name, address, and telephone numbers of the Client’s official is: NAD official: Name: ___________________, Position:______________________ Address: _______________________________________________ Telephone: ________, Fax: ___________, E-mail: ______________

9.1.5 NAD will provide the following inputs: See Terms of Reference

9.1.7.2 NAD may decide for continuity for downstream work of the credit

agency for the same services when the continuity id essential, based on the performance criteria defined in the Terms of Reference (Section V)

9.1.11 The clause on fraud and corruption in the Contract is: Sub-clause 2.9.1(g) of the General Conditions of Contract (Annex 4 to micro-credit scheme – Standard form of contract)

9.2.1 The credit agencies may request clarifications before 21 days the submission date.

The clarifications will be requested to NAD official: Name: ___________________, Position:______________________Address: _______________________________________________ Telephone: ________, Fax: ___________, E-mail: ______________

9.3.1

Proposals should be submitted in English

9.3.3 (i) Shortlisted firm/entity may associate with other shortlisted firm Yes (ii) Not applicable

(iv) The minimum required experience of proposed professional staff is:

See Terms of Reference (vi) Reports that are part of the assignment must be written in the

following language(s): English and Romanian

9.3.4 (vii) Training is a specific component of this assignment:

Yes, see Terms of Reference (viii) All information requested in the Term of Reference is to be

submitted with the bid

9.3.7

Taxes: The credit agency shall be responsible for all taxes, duties etc resulting from the implementation of the contract, according to Romanian legislation

9.3.8 The credit agency will state local cost in the national currency of Romania

9.3.10

Proposals must remain valid 120 days after the submission date

9.4.3 The credit agencies must submit an original and three (3) additional copies of each proposal. Each envelope will be marked with “Original” and “Copy” as well as RFP 150/11/99/Area ___ –

Technical Proposal and Financial Proposal.

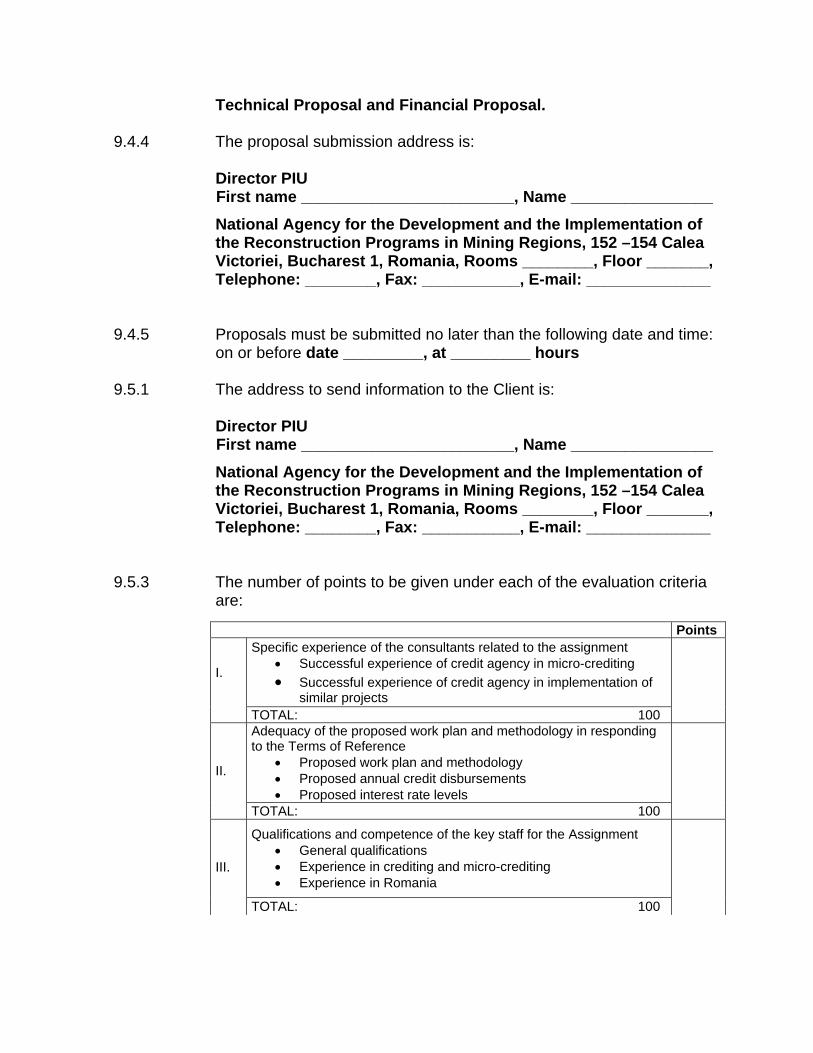

9.4.4 The proposal submission address is: Director PIU First name ________________________, Name ________________National Agency for the Development and the Implementation of the Reconstruction Programs in Mining Regions, 152 –154 Calea Victoriei, Bucharest 1, Romania, Rooms ________, Floor _______, Telephone: ________, Fax: ___________, E-mail: ______________

9.4.5 Proposals must be submitted no later than the following date and time:on or before date _________, at _________ hours

9.5.1

The address to send information to the Client is: Director PIU First name ________________________, Name ________________National Agency for the Development and the Implementation of the Reconstruction Programs in Mining Regions, 152 –154 Calea Victoriei, Bucharest 1, Romania, Rooms ________, Floor _______, Telephone: ________, Fax: ___________, E-mail: ______________

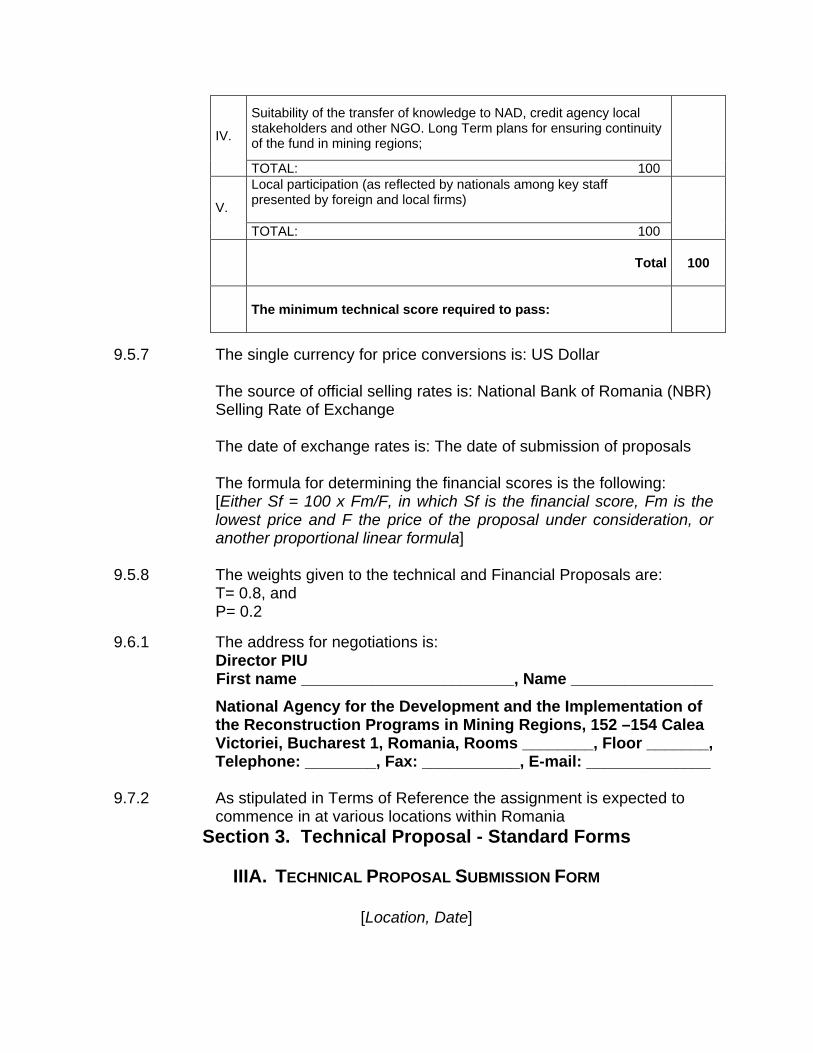

9.5.3 The number of points to be given under each of the evaluation criteria

are:

Points Specific experience of the consultants related to the assignment

• Successful experience of credit agency in micro-crediting • Successful experience of credit agency in implementation of

similar projects I.

TOTAL: 100

Adequacy of the proposed work plan and methodology in responding to the Terms of Reference

• Proposed work plan and methodology • Proposed annual credit disbursements • Proposed interest rate levels

II.

TOTAL: 100

Qualifications and competence of the key staff for the Assignment • General qualifications • Experience in crediting and micro-crediting • Experience in Romania

III.

TOTAL: 100

Suitability of the transfer of knowledge to NAD, credit agency local stakeholders and other NGO. Long Term plans for ensuring continuity of the fund in mining regions; IV.

TOTAL: 100

Local participation (as reflected by nationals among key staff presented by foreign and local firms) V.

TOTAL: 100

Total

100

The minimum technical score required to pass:

9.5.7 The single currency for price conversions is: US Dollar

The source of official selling rates is: National Bank of Romania (NBR) Selling Rate of Exchange The date of exchange rates is: The date of submission of proposals The formula for determining the financial scores is the following: [Either Sf = 100 x Fm/F, in which Sf is the financial score, Fm is the lowest price and F the price of the proposal under consideration, or another proportional linear formula]

9.5.8 The weights given to the technical and Financial Proposals are: T= 0.8, and P= 0.2

9.6.1 The address for negotiations is:

Director PIU First name ________________________, Name ________________National Agency for the Development and the Implementation of the Reconstruction Programs in Mining Regions, 152 –154 Calea Victoriei, Bucharest 1, Romania, Rooms ________, Floor _______, Telephone: ________, Fax: ___________, E-mail: ______________

9.7.2 As stipulated in Terms of Reference the assignment is expected to commence in at various locations within Romania

Section 3. Technical Proposal - Standard Forms

IIIA. TECHNICAL PROPOSAL SUBMISSION FORM

[Location, Date]

Director PIU _________________________________________________________