g.q. capital advisors date antoine landriault arbour javier hernandez-cotton paul-henri grange xxx...

TRANSCRIPT

G.Q. Capital Advisors

G.Q. Capital AdvisorsDATEAntoine Landriault ArbourJavier Hernandez-CottonPaul-Henri Grange

XXX

XXX

Presented to Mr. XXX and the B.O.D. on behalf of XXX

1. Introduction & Key Considerations

2. Analysis & Strategic Rationale

3. Valuation & Financial Assessment

4. Implementation Strategy

Introduction & Key Considerations

G.Q. Capital Advisors

Mandate

Introduction Analysis Valuation Implementation

G.Q. Capital Advisors

Recommended Course of Action

Introduction Analysis ValuationImplementati

on

G.Q. Capital Advisors

Introduction M&A

Acquirer

Target

Key Considerations:

Existing Bid

Introduction Analysis Valuation Implementation

1. Introduction & Key Considerations

2. Analysis & Strategic Rationale

3. Valuation & Financial Assessment

4. Implementation Strategy

Analysis & Strategic Rationale

G.Q. Capital Advisors

Value Drivers

Introduction Analysis ValuationImplementati

on

G.Q. Capital Advisors

Nordstrom Consideration

Introduction Analysis Valuation Implementation

G.Q. Capital Advisors

Strategic Ideation

Business Considerations Key Insight

Introduction Analysis ValuationImplementati

on

G.Q. Capital Advisors

Strategic Fit

Aim of Acquisition

Strategy

Acquisition Thesis

Our Concluding Rationale for The Acquisition:

Introduction Analysis Valuation Implementation

1. Introduction & Key Considerations

2. Analysis & Strategic Rationale

3. Valuation & Financial Assessment

4. Implementation Strategy

Valuation & Financial Assessment

G.Q. Capital Advisors

Valuation Overview

Introduction Analysis Valuation Implementation

Key Decision Metrics

Accretion / Dilution Financial Leverage

ValuationDCF Comparables Precedents

Financial Statement ProjectionsX X

G.Q. Capital Advisors

Assumptions Overview

Introduction Analysis Valuation Implementation

X Projections

• Revenue growth of x% per annum, decreasing to X%

• Cost of sales of x%, decreasing to X%

• Operating expenses of x%, decreasing to X% (operational leverage)

X Projections

• Revenue growth of X% per annum, decreasing to X%

• Cost of sales of x%, decreasing to X%

• Operating expenses of x%, decreasing to X% (operational leverage)

X Valuation

• WACC of x%, terminal growth of x%

• Working Capital days remain constant

• Capex equals D&A to reflect maturity and lower growth (maintenance capex)

Revenue growth and margins based on average historical performanceAssumes slight operational leverage moving forward

G.Q. Capital Advisors

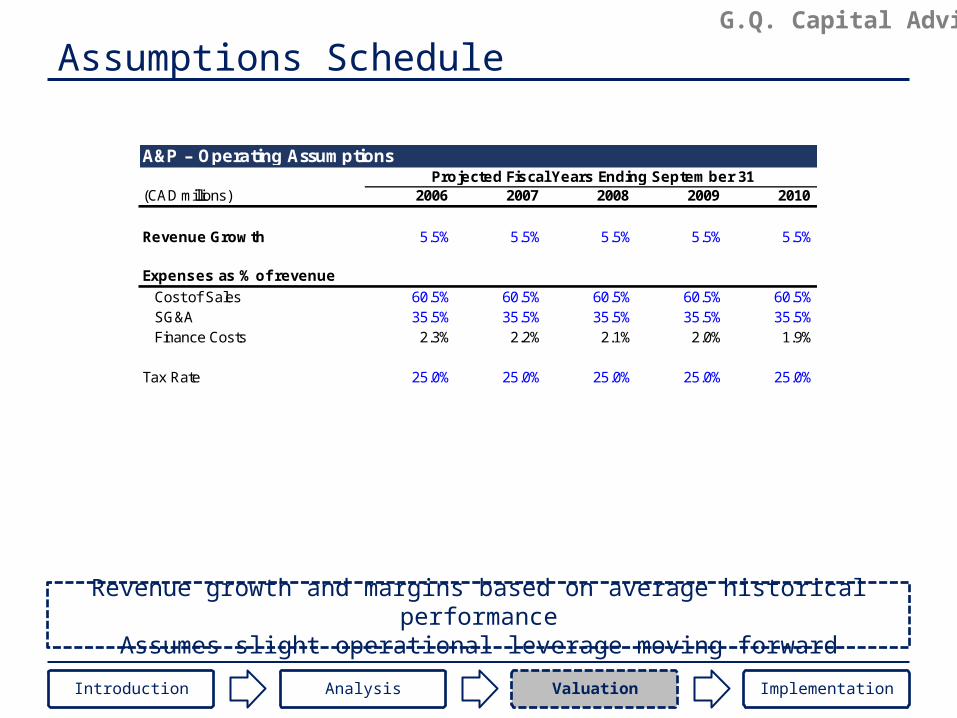

Assumptions Schedule

Introduction Analysis Valuation Implementation

Revenue growth and margins based on average historical performanceAssumes slight operational leverage moving forward

A&P – Operating AssumptionsProjected Fiscal Years Ending September 31

(CAD millions) 2006 2007 2008 2009 2010

Revenue Growth 5.5% 5.5% 5.5% 5.5% 5.5%

Expenses as % of revenue

Cost of Sales 60.5% 60.5% 60.5% 60.5% 60.5%SG&A 35.5% 35.5% 35.5% 35.5% 35.5%Finance Costs 2.3% 2.2% 2.1% 2.0% 1.9%

Tax Rate 25.0% 25.0% 25.0% 25.0% 25.0%

G.Q. Capital Advisors

X Income Statement

Introduction Analysis Valuation Implementation

Assumes slight operational leverage & financial leverage

Revenues growing at a 5.5% CAGR; earnings at 11.8%

A&P – Income Statement CAGRProjected Fiscal Years Ending September 31

(CAD millions) 2006 2007 2008 2009 2010

Retail Sales 4,301 4,538 4,787 5,051 5,328 5.5%Cost of Sales (2,600) (2,743) (2,894) (3,053) (3,221)Gross Profit 1,701 1,795 1,893 1,997 2,107 5.5%

SG&A (1,528) (1,612) (1,700) (1,794) (1,892)Operating Income 173 183 193 204 215 5.5%

Finance Costs (100) (100) (100) (100) (100)Income Before Taxes 73 83 93 104 115

Income Taxes (18) (21) (23) (26) (29)Net Income 55 62 70 78 86 11.8%

G.Q. Capital Advisors

X2 Income Statement

Introduction Analysis Valuation Implementation

Assumes slight operational leverage & financial leverage

Revenues growing at a 5.5% CAGR; earnings at 11.8%

A&P – Income Statement CAGRProjected Fiscal Years Ending September 31

(CAD millions) 2006 2007 2008 2009 2010

Retail Sales 4,301 4,538 4,787 5,051 5,328 5.5%Cost of Sales (2,600) (2,743) (2,894) (3,053) (3,221)Gross Profit 1,701 1,795 1,893 1,997 2,107 5.5%

SG&A (1,528) (1,612) (1,700) (1,794) (1,892)Operating Income 173 183 193 204 215 5.5%

Finance Costs (100) (100) (100) (100) (100)Income Before Taxes 73 83 93 104 115

Income Taxes (18) (21) (23) (26) (29)Net Income 55 62 70 78 86 11.8%

G.Q. Capital Advisors

Valuation – Working Capital Schedule

Introduction Analysis Valuation Implementation

Working capital requirements based on average historical performanceOperational leverage requires less working capital as % of sales / COGS

A&P – Working Capital ScheduleProjected Fiscal Years Ending September 31

(CAD millions) 2006 2007 2008 2009 2010

Accounts receivable 108 114 121 127 134Inventories 1,543 1,627 1,717 1,811 1,911Accounts payable 555 585 618 652 687

Accounts receivable (% of revenues) 2.5% 2.5% 2.5% 2.5% 2.5%Inventories (% of cost of sales) 59.3% 59.3% 59.3% 59.3% 59.3%Accounts payable (% of cost of sales) 21.3% 21.3% 21.3% 21.3% 21.3%

Net Working Capital 1,096 1,156 1,220 1,287 1,358Change in NWC 428 60 64 67 71

G.Q. Capital Advisors

Valuation – PP&E Schedule

Introduction Analysis Valuation Implementation

Depreciation expected to equal capex as company matures

A&P – PP&E ScheduleProjected Fiscal Years Ending September 31

(CAD millions) 2006 2007 2008 2009 2010

D&A as % of revenues 2.5% 2.5% 2.5% 2.5% 2.5%Capex as % of revenues 3.8% 3.8% 3.8% 3.8% 3.8%

D&A 106 111 117 124 131Capex 162 171 181 190 201

G.Q. Capital Advisors

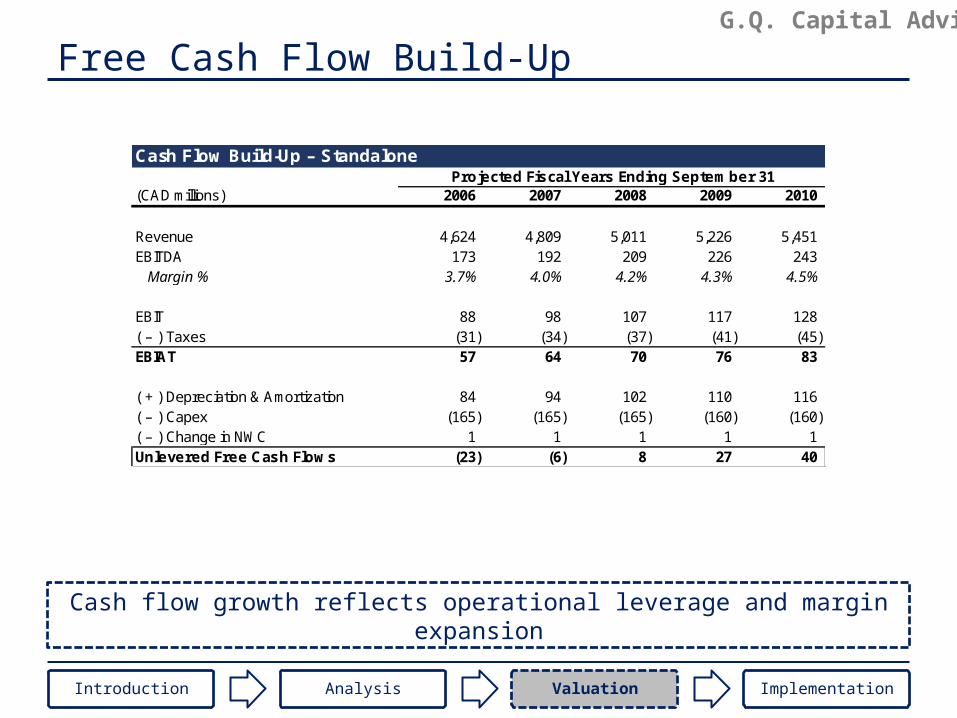

Free Cash Flow Build-Up

Introduction Analysis Valuation Implementation

Cash flow growth reflects operational leverage and margin expansion

Cash Flow Build-Up – StandaloneProjected Fiscal Years Ending September 31

(CAD millions) 2006 2007 2008 2009 2010

Revenue 4,624 4,809 5,011 5,226 5,451EBITDA 173 192 209 226 243

Margin % 3.7% 4.0% 4.2% 4.3% 4.5%

EBIT 88 98 107 117 128( – ) Taxes (31) (34) (37) (41) (45)EBIAT 57 64 70 76 83

( + ) Depreciation & Amortization 84 94 102 110 116( – ) Capex (165) (165) (165) (160) (160)( – ) Change in NWC 1 1 1 1 1Unlevered Free Cash Flows (23) (6) 8 27 40

G.Q. Capital Advisors

Valuation – Beta

Introduction Analysis Valuation Implementation

Public comparables provide a good estimate for an unlevered (asset) beta

Target D/E ratio below peers to reflect the

company’ preference for low debt

Levered Market Debt / Unlevered

Beta Cap Debt Equity Tax Rate Beta

Beta Comps

MGM Mirage 0.99 27.7 14.1 51% 40% 0.76

Harrah's Entertainment 0.85 16.4 12.3 75% 40% 0.59

Las Vegas Sands 1.18 42.2 7.3 17% 40% 1.07

Eastern Start 1.33 4.7 0.4 9% 40% 1.26

Wynn Resorts 1.14 15.4 1.0 6% 40% 1.10

Median 1.14 16.4 7.3 17% 40% 1.07

Average 1.10 21.3 7.0 32% 40% 0.95

A&P

Debt/Equity 50%

Tax Rate 40%

Comps Median Unlevered Beta 1.07

Levered Beta 1.39

G.Q. Capital Advisors

Valuation – Cost of Capital

Introduction Analysis Valuation Implementation

We believe a WACC of x% represents an adequate discount rate (and expected return) given its risk profile

WACC

Risk-free Rate 2.5%

Market Risk Premium 5.5%

Beta 1.00CAPM Cost of Equity 8.0%

Cost of Debt 4.0%Tax Rate 35.0%After-tax Cost of Debt 2.6%

WACC 7.2%

Terminal GR 1.5%

Target Capital StrucutreDebt 15.0%

Equity 85.0%

Additional premium to reflect the riskier nature of

private companies (information asymmetry) and their lack of liquidity

Inline with long-term GDP growth rate

Slightly below industry average

G.Q. Capital Advisors

Discounted Cash Flow Analysis – Standalone

Introduction Analysis Valuation Implementation

Implies a 5x EBITDA exit multiple vs current multiple of 5xValue created mostly through cash flow growth, not multiple expansion

Discounted Cash Flow Analysis – StandaloneProjected Fiscal Years Ending September 31

(CAD millions) 2006 2007 2008 2009 2010

Unlevered Free Cash Flow s (23) (6) 8 27 40Terminal Value 717Total (23) (6) 8 27 757

Discount Factor 0.50 1.50 2.50 3.50 4.50

PV of FCFs (22) (6) 6 21 554

Enterprise Value 554

WACC vs Terminal Growth Rate$553.94 6.0% 6.5% 7.0% 7.5% 8.0%

1.0% 658 588 530 481 4391.5% 731 647 578 521 4722.0% 822 718 636 568 5122.5% 940 808 706 625 5593.0% 1,097 924 795 695 615

G.Q. Capital Advisors

Discounted Cash Flow Analysis – W/ Synergies

Introduction Analysis Valuation Implementation

Discounted Cash Flow Analysis – StandaloneProjected Fiscal Years Ending September 31

(CAD millions) 2006 2007 2008 2009 2010

Unlevered Free Cash Flow s (23) (6) 8 27 40Terminal Value 717Total (23) (6) 8 27 757

Discount Factor 0.50 1.50 2.50 3.50 4.50

PV of FCFs (22) (6) 6 21 554

Enterprise Value 554

WACC vs Terminal Growth Rate$553.94 6.0% 6.5% 7.0% 7.5% 8.0%

1.0% 658 588 530 481 4391.5% 731 647 578 521 4722.0% 822 718 636 568 5122.5% 940 808 706 625 5593.0% 1,097 924 795 695 615

Implies a 5x EBITDA exit multiple vs current multiple of 5xValue created mostly through synergies, not multiple expansion

Enterprise value is highly sensitive to expected

synergies

G.Q. Capital Advisors

Trading Comparables Analysis

Introduction Analysis Valuation Implementation

Enterprise Value of $1310 using peer group’s median EV / EBITDA multiple

Comps Valuation

Peer Group Median Multiple 0.4x 8.4x 14.2xA&P Metrics 4,486 156 47

Enterprise Value 1,929 1,310 683

Comparables Analysis

EV / EV /

Canadian Food Retailers Revenue EBITDA P / E

Loblaw 0.9x 10.4x 18.6xMETRO 0.4x 8.4x 14.0xSobeys 0.2x 5.6x 14.2x

Median 0.4x 8.4x 14.2xAverage 0.5x 8.1x 15.6x

Screened for comps with similar growth prospects, margins, size, and overall risk profile

Trading multiples yields a higher

value because of the comps’ larger scale and greater liquidity (better access to capital

markets)

G.Q. Capital Advisors

Precedent Transactions Analysis

Introduction Analysis Valuation Implementation

Enterprise Value of $1513 using peer group’s median EV / EBITDA multiple

Comparables Analysis

EV / EV / EV /

Company Revenue EBITDA EBIT

Shaw 's Supermarkets 0.5x 6.9x 11.2xHannaford Bros. 1.1x 12.4x 19.0xRandall's 0.7x 10.5x 16.7xRichfood 0.7x 7.8x 10.9xOshaw a 0.2x 8.2x 13.3xProvigo 0.3x 8.9x 13.5xDominick's 0.8x 10.8x 17.7xGiant Food 0.7x 12.3x N/A

Median 0.7x 9.7x 13.5xAverage 0.6x 9.7x 14.6x

Comps Valuation

Peer Group Median Multiple 0.7x 9.7x 13.5xA&P Metrics 4,486 156 81

Enterprise Value 3,140 1,513 1,094

Screened for transactions closed in a similar market environment, with

similar growth, margins and size

A&P falls around the median margin, we

therefore selected the median

multiple

G.Q. Capital Advisors

Market Environment

Introduction Analysis Valuation Implementation

Bull markets justify higher transaction multiples

G.Q. Capital Advisors

Market Environment

Introduction Analysis Valuation Implementation

Bull markets justify higher transaction multiples

G.Q. Capital Advisors

Valuation Summary

Introduction Analysis Valuation Implementation

Final price target of $XWeighted the X and X valuations more

$0.00 $2.00 $4.00 $6.00 $8.00 $10.00 $12.00 $14.00 $16.00 $18.00 $20.00

EV / Revenue

EV / EBITDA

EV / EBIT

P / E

EV / Revenue

EV / EBITDA

EV / EBIT

P / E

DCF – Standalone

DCF – W/ Synergies

Precendent Transactions:

Trading Comps:

G.Q. Capital Advisors

Accretion / Dilution Analysis

Introduction Analysis Valuation Implementation

Deal is accretive as of the first year at a valuation of $XAssuming 20% stock and 80% debt financing

Accretion / Dilution Analysis

Metro Standalone Pretax Income 241A&P Standalone Pretax Income 81Combined Pretax Income 322

( – ) Interest Expense from New Deal Debt (63)( – ) Forgone Interest Income on Cash -( – ) Deal Fees (Advisory, Legal, Etc.) (7)( – ) Financing Fees Amortization (2)

( – ) Incremental D&A Expense -( + ) Synergies 35Pro Forma Pretax Income 284

Pro Forma Net Income 199Pro Forma Shares Outstanding 109

Pro Forma EPS $1.83Metro Standalone EPS $1.91

Accretion (Dilution) per Share -$0.07Accretion (Dilution) % (3.8%)

G.Q. Capital Advisors

Accretion / Dilution Sensitivity Analysis

Introduction Analysis Valuation Implementation

Depreciation expected to equal capex as company matures

Premium Paid vs % Stock Consideration

-4% -% 10.0% 20.0% 30.0% 40.0%-% 5.8% 3.0% 0.2% (2.6%) (5.4%)

10.0% 3.8% 0.9% (1.9%) (4.7%) (7.5%)20.0% 1.9% (1.0%) (3.8%) (6.6%) (9.4%)30.0% 0.2% (2.7%) (5.6%) (8.4%) (11.1%)40.0% (1.4%) (4.3%) (7.2%) (10.0%) (12.6%)

Synergies vs % Stock Consideration

-4% 5 20 35 50 65-% (11.0%) (5.4%) 0.2% 5.8% 11.4%

10.0% (12.6%) (7.2%) (1.9%) 3.4% 8.7%20.0% (14.0%) (8.9%) (3.8%) 1.2% 6.3%30.0% (15.3%) (10.4%) (5.6%) (0.8%) 4.1%40.0% (16.5%) (11.8%) (7.2%) (2.6%) 2.1%

G.Q. Capital Advisors

Solvency Analysis

Introduction Analysis Valuation Implementation

NewCo is able to deleverage rapidly trough strong cash flow generationand maintain reasonable interest coverage ratios

G.Q. Capital Advisors

Solvency Stress Test

Introduction Analysis Valuation Implementation

NewCo is still solvent after a substantial decrease in EBIT (~20%)

1. Introduction & Key Considerations

2. Analysis & Strategic Rationale

3. Valuation & Financial Assessment

4. Implementation Strategy

Implementation Strategy

G.Q. Capital Advisors

Alternatives

Introduction Analysis ValuationImplementat

ion

G.Q. Capital Advisors

Alternatives

Introduction Analysis ValuationImplementat

ion

G.Q. Capital Advisors

Recommended Course of Action

Introduction Analysis ValuationImplementat

ion

G.Q. Capital Advisors

Implementation Timeline

Introduction Analysis ValuationImplementat

ion

G.Q. Capital Advisors

Risk Assessment

Risks Mitigations Contingencies

Introduction Analysis ValuationImplementat

ion

1. Introduction & Key Considerations

2. Analysis & Strategic Rationale

3. Valuation & Financial Assessment

4. Implementation Strategy

Conclusion

Appendix1. 1

2. 2

3. 3

4. 4

5. 5

6. 6

7. 7

8. 8

9. 9

10. 10

11. 11

12. 12

13. 13