graduate course - sol.du.ac.in · according to the present value method of capital budgeting, if...

TRANSCRIPT

Graduate Course Paper XIX Elective Group EA : Finance I

FINANCIAL AND INVESTMENT MANAGEMENT

FINANCIAL MANAGEMENT

Contents :

UNIT : 3

1. Cost of Capital – I

2. Cost of Capital – II

3. Capital Structure Theories

4. Capital Structure : Planning & Design

5. Financing Decision : EBIT-EPS Analysis

6. Financing Decision – Leverage Analysis

UNIT : 4

1. Dividend Decision and Valuation of the Firm

2. Dividend Policy : Determinants and Constraints

UNIT : 5

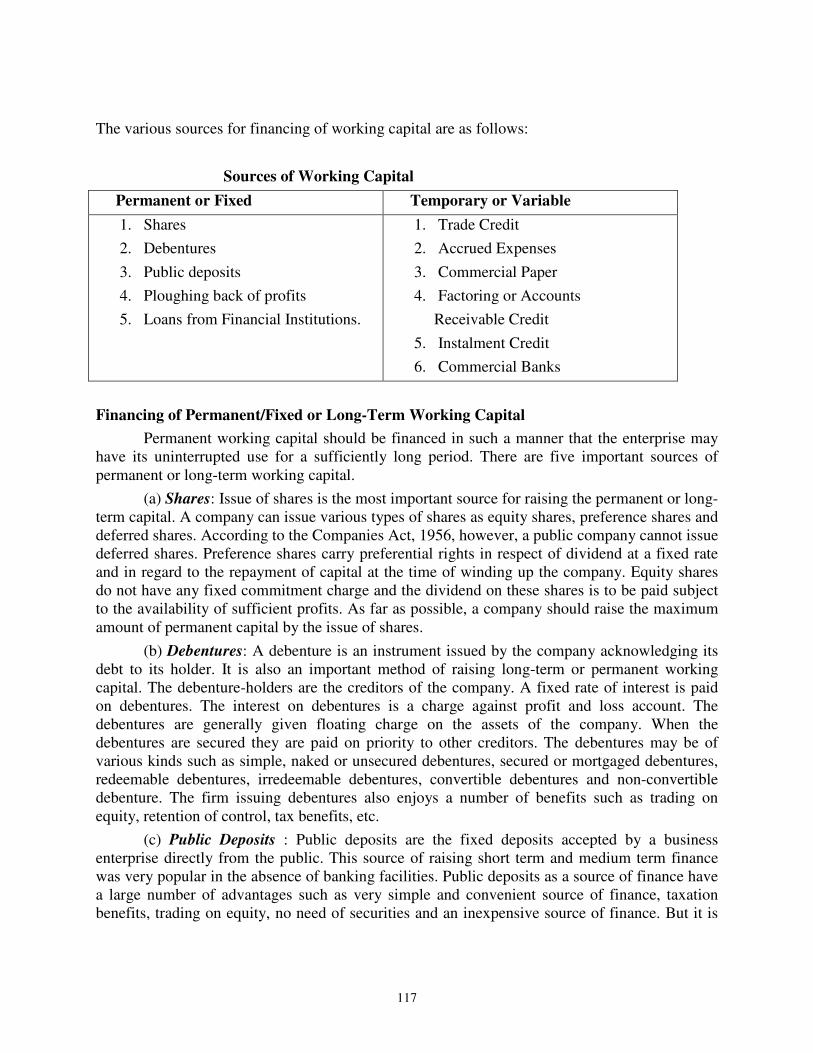

1. Working Capital : Management and Finance

2. Working Capital : Estimation and Calculation

3. Financing of Working Capital

4. Management of Cash

5. Receivable Management

6. Inventory Management

Editor :

K.B. Gupta

SCHOOL OF OPEN LEARNING UNIVERSITY OF DELHI

5, CAVALRY LANE

DELHI-110007

SESSION 2007-08

©School of Open Leaning

Published by the Executive Director, School of Open Learning, University of

Delhi, 5 Cavalry Lane, Delhi-110007.

Laser typeset : S.O.L. Computer Centre

Printed at :

UNIT 3

1

COST OF CAPITAL- I

Smriti Chawla

Shri Ram College of Commerce University of Delhi

Meaning, Concept and Definition

The cost of capital of a firm is the minimum rate of return expected by its investors. It is

the weighted average cost of various sources of finance used by a firm. The capital used by a

firm may be in the form of debt, preference capital, retained earnings and equity shares. The

concept of cost of capital is very important in the financial management. A decision to invest in a

particular project depends upon the cost of capital of the firm or the cut off rate which is the

minimum rate of return expected by the investors. In case a firm is not able to achieve even the

cut off rate, the market value of its shares will fall. In fact cost of capital is the minimum rate of

return expected by its investors which will maintain the market value of shares at its present

level. Hence to achieve the objective of wealth maximisation, a firm must earn a rate of return

more than its cost of capital. The cost of capital of a firm or the minimum rate of return expected

by its investors has a direct relation with the risk involved in the firm. Generally, higher the risk

involved in a firm, higher is the cost of capital.

According to Solomon Ezra Cost of capital is the minimum required rate of earnings or

the cut-off rate of capital expenditures.

Thus, we can say that cost of capital is that minimum rate of return which a firm, and, is

expected to earn on its investments so as to maintain the market value of its shares.

From the definitions given above we can conclude three basic aspects of the concept of cost of

capital:

CHAPTER OBJECTIVES

� Understand the Meaning, Concept and Significance of Cost of Capital.

� Classification of Cost

� Problems in Determining the Cost of Capital � Computation of Specific Source of Finance

Cost of Debt Cost of Preference Capital Cost of Equity Share Capital

Cost of Retained Earnings � Illustrations

2

(i) Cost of capital is not a cost as such. In fact, it is the rate of return that a firm requires

to earn from its projects.

(ii) It is the minimum rate of return. Cost of capital of a firm is that minimum rate of

return which will at least maintain the market value of the shares.

(iii) It comprises of three components. As there is always some business and financial risk

in investing funds in a firm, cost of capital comprises of three components:

(a) the expected normal rate of return at zero risk level, say the rate of interest

allowed by banks;

(b) the premium for business risk; and

(c) the premium for financial risk on account of pattern of capital structure.

Symbolically cost of capital may be represented as:

where, K = ro+b+f

K=Cost of capital

ro=Normal rate of return at zero risk level

b=Premium for business risk.

f=Premium for financial risk.

Significance of the Cost of Capital

The concept of cost of capital is very important in the financial management. It plays a

crucial role in both capital budgeting as well as decisions relating to planning of capital structure.

Cost of capital concept can also be used as a basis for evaluating the performance of a firm and it

further helps management in taking so many other financial decisions.

(1) As an Acceptance Criterion in Capital Budgeting: Capital budgeting decisions can be made

by considering the cost of capital. According to the present value method of capital budgeting, if

the present value of expected returns from investment is greater than or equal to the cost of

investment, the project may be accepted; otherwise the project may be rejected. The present

value of expected return is calculated by discounting the expected cash inflows at cut-off rate

(which is the cost of capital). Hence, the concept of cost of capital is very useful in capital

budgeting decision.

(2) As a Determinant of Capital Mix in Capital Structure Decisions: Financing the firm’s

assets is a very crucial problem in every business and as a general rule there should be a proper

mix of debt and equity capital in financing a firm’s assets. While designing an optimal capital

structure, the management has to keep in mind the objective or maximising the value of the firm

and minimising the cost of capital. Measurement of cost of capital from various sources is very

essential in planning the capital structure of any firm.

(3) As a basis for evaluating the Financial Performance: The concept of cost of capital can be

used to ‘evaluate the financial performance of top management’. The actual profitability of the

project is compared to the projected overall cost of capital and the actual cost of capital of funds

raised to finance the project. If the actual profitability of the project is more than the projected

and the actual cost of capital, the performance may be said to be satisfactory.

(4) As a Basis for taking other Financial Decisions: The cost of capital is also used in making

other financial decisions such as dividend policy, capitalisation of profits, making the rights issue

and working capital.

3

Classification of Cost

(1) Historical cost and Future Cost: Historical costs are book costs which are related to the past.

Future costs are estimated costs for the future. In financial decisions future costs are more

relevant than the historical costs. However, historical costs act as guide for the estimation of

future costs.

(2) Specific Cost and Composite Cost: Specific cost refers to the cost of a specific source of

capital while composite cost is combined cost of various sources of capital. It is the weighted

average cost of capital. In case more than one form of capital is used in the business, it is the

composite cost which should be considered for decision-making and not the specific cost. But

where only one type of capital is employed the specific cost of that type of capital may be

considered.

(3) Explicit Cost and Implicit Cost: An explicit cost is the discount rate which equates the

present value of cash inflows with the present of cash outflows. In other words it is the internal

rate of return.

( ) ( ) ( ) ( )

∑− +

=+

++

++

=n

t

t

t

n

n

o

K

O

k

O

k

O

K

OI

12

21

11..................................

11

where, Io, is the net cash inflow at zero point of time,

Ot is the outflow of cash in period 1, 2 and n.

k is the explicit cost of capital.

Implicit cost also known as the opportunity cost is the cost of the opportunity foregone is order

to take up a particular project.

(4) Average Cost and Marginal Cost: An average cost refers to the combined cost of various

sources of capital such as debentures, preference shares and equity shares. It is the weighted

average cost of the costs of various sources of finance. Marginal cost of capital refers to the

average cost of capital which has to be incurred to obtain additional funds required by a firm. In

investment decisions, it is the marginal cost which should be taken into consideration.

Determination of Cost of Capital

It has already been stated that the cost of capital plays a crucial role in the decisions

relating to financial management. However, the determination of the cost of capital of a firm is

not an easy task because of both conceptual problems as well as uncertainties of proposed

investments and the pattern of financing. The major problems concerning the determination of

cost of capital are discussed as below:

Problems in determining Cost of Capital

1. Conceptual controversies regarding the relationship between the cost of capital and

the capital structure : Different theories have been propounded by different authors explaining

the relationship between capital structure, cost of capital and the value of the firm. This has

resulted into various conceptual difficulties. According to the Net Income Approach and the

traditional theories both the cost of capital as well the value of the firm have a direct relationship

with the method and level of financing. In their opinion, a firm can minimise the weighted

average cost of capital and increase the value of the firm by using debt financing. On the other

4

hand, Net Operating Income and Modigliani and Miller Approach prove that the cost of capital is

not affected by changes in the capital structure or say that debt equity mix is irrelevant in

determination of cost of capital structure determination of cost of capital and the value of a firm.

However, the M and M approach is based upon certain unrealistic assumptions such as, there is a

perfect market or the expected earnings of all the firms have identical risk characteristic, etc.

2. Problems in computation of cost of equity: The computation of cost of equity capital

depends upon the expected rate of return by its investors. But the quantification of the

expectations of equity shareholders is a very difficult task because there are many factors which

influence their valuation about a firm.

3. Problems in computation of cost of retained earnings: It is sometimes argued that

retained earnings do not involve any cost but in reality, it is the opportunity cost of dividends

foregone by its shareholders. Since different shareholders may have different opportunities for

investing their dividends, it becomes very difficult to compute the cost of retained earnings.

4. Problems in assigning weights: For determining the weighted average cost of capital,

weights have to be assigned to the specific cost of individual source of finance. The choice of

using the book value of the source or the market value of the source poses another problem in the

determination of capital.

COMPUTATION OF SPECIFIC SOURCE OF FINANCE

Computation of each specific source of finance, viz, debt, preference share capital equity

share capital and retained earnings is discussed as below:

1. Cost of Debit

The cost of debt is the rate of interest payable on debt. For example, a company issues

Rs. 1,00,000 debentures at par; the before tax cost of this debt issue will also be 10%. By way of

formula, before-tax-cost of debt may be calculated as:

(i) Kdb =P

I

where, Kdb = Before tax cost of debt

I = Interest

and P = Principal

In case the debt is raised at premium or discount, we should consider P as the amount of

the net proceeds received from the issue and not the face value of securities. The formula may be

changed to

(ii) Kdb =NP

I (where, NP = Net Proceeds)

Further, when debt is used as a source of finance, the firm saves a considerable amount in

payment of tax as the interest is allowed as a deductable expense in computation tax. Hence, the

effective cost of debt is reduced. The after tax cost of debt may be calculated with the help of

following formula;

(iii) Kda = Kdb (1-t) = ( )tNP

I−1

where, Kda = After tax cost of debt

t = Rate of tax.

5

Cost of Redeemable Debt Usually, the debt is issued to be redeemed after a certain period during lifetime of a firm.

Such a debt issue is known as Redeemable debt. The cost of redeemable debt capital be

computed as:

(iv) Before-tax cost of debt

( )

( )NPP

NPPn

I

Kdb

+

−+

=

2

1

1

where, I = Interest

N = Number of years in which debt is to be redeemed

P = Proceeds at par

NP = Net Proceeds

(v) After tax cost of debt, Kda = Kdb (1-t)

where,

( )

( )NPP

NPPn

I

Kdb

+

−+

=

2

1

1

Illustration1: A Company issues shares of Rs.10,00,000, 10% redeemable debentures at

a discount of 5%. The cost of floatation amount to Rs.30,000. The debentures are redeemable

after 5 years. Calculate before tax and after tax cost of debt assuming tax rate of 50%.

Solution:

Before-tax cost of debt,

( )

( )NPP

NPPn

I

Kdb

+

−+

=

2

1

1

=

( )

( )000,0,9000,00,102

1

000,20,9000,00,105

1000,00,1

+

−+

(NP=Rs. 10,00,000-50,000 (discount) – 30,000 cost of floatation)

= %09.12000,60,9

000,16,1

000,60,9

000,16000,00,1==

+

After tax cost of debt, Kda = Kdb (1-0.5)

= 12.09 (1-0.5) = 6.04%

Cost of Debt Redeemable at Premium

Sometimes debentures are to be redeemed at a premium; i.e at more than the face value

after the expiry of a certain period. The cost of such debt redeemable at premium can be

computed as below:

6

(i) Before tax cost of debt,

( )

( )NPRV

NPRVn

I

Kdb

+

−+

=

2

1

1

where, I = Interest

n = Number of years in which debt is to be redeemed

RV= Redeemable value of debt

NP = Net Proceeds

(ii) After-tax cost of debt,

Kda= Kdb (1-t)

Illustration2: A 5-year Rs.100 debenture of a firm can be sold for a net price of

Rs.96.50. The coupon rate of interest is 14 %per annum and debenture will be redeemed at 5%

premium on maturity. The firm tax rate is 40%. Compute the after tax cost of debentures.

Solution:

( )

( )NPRV

NPRVn

I

Kdb

+

−+

=

2

1

1

=

( )

( )%58.15

75.100

70.15

50.961052

1

50.961055

114

==

+

−+

After-tax cost of debt,

Kda = Kdb (1-t)

= 15.58 (1-0.4) = 15.58 x 0.6 = 9.35%

Cost of Debt Redeemable in Instalments

Financial institutions generally require principal to be amortised in instalments. A

company may also issue a bond or debenture to be redeemed periodically. In such a case,

principal amount is repaid each period instead of a lump sum at maturity and hence cash period

include interest and principal. The amount of interest goes on decreasing each period as it is

calculated on decreasing each period as it is calculated on the outstanding amount of debt. The

before-tax cost of such a debt can be calculated as below:

( ) ( ) ( )n

d

nn

dd

d

KI

PI

KI

PI

K

PIV

+

+++

+

++

+

+= ................

12

22

1

11

or, Vd = ( )

∑− +

+n

t

t

d

tt

KI

PI

1

where, Vd = Present value of bond or debt

I1, I2....In = Annual interest (Rs.) in period 1,2... and so on.

P1,P2...Pn=Periodic payment of principal in period 1, 2, and so on.

7

n = Number of years to maturity

Kd = Cost of debt or Required rate of return.

Cost of Existing Debt

If a firm wants to compute the current cost of its existing debt, the current market yield of

the debt should be taken into consideration. Suppose a firm has 10% debentures of Rs. 100 each

outstanding on January 1, 1994 to be redeemed on December 31, 2000 and the new debentures

could be issued at a net realisable price of Rs. 90 in the beginning of 1996, the current cost of

existing debt will be computed as:

( )

( )901002

1

901005

110

+

−+

=db

K = %63.1295

12=

Further, if the firm’s tax rate is 40% the after-tax cost of debt will be:

Kda = Kdb (1-t)

= 12.63 (1-0.4)

= 7.58%

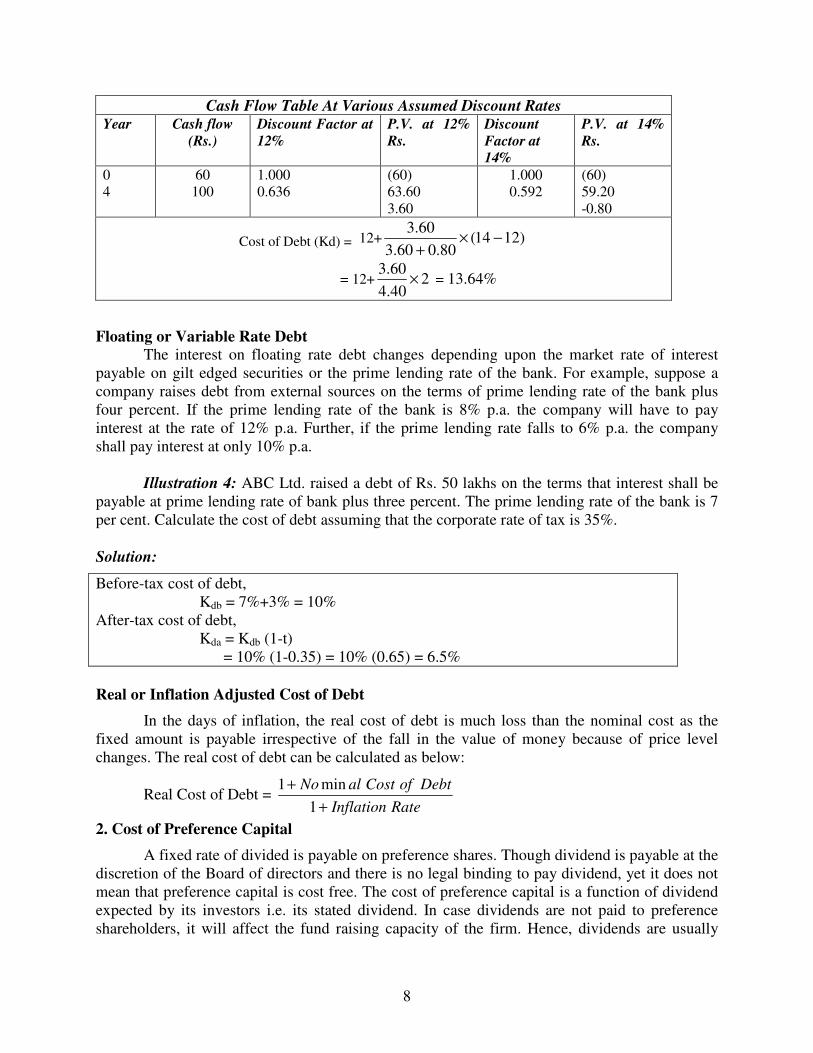

Cost of Zero Coupon Bonds

Sometimes companies issue bonds or debentures at a discount from their eventual maturity

value and having zero interest rate. No interest is payable on such debentures before their

redemption and at the time of redemption the maturity value of the bond is to be paid to the

investors. The cost of such debt can be calculated by finding the present values of cash flows as

below:

(i) Prepare the cash flow table using an arbitrary assumed discount rate to discount the

cash flows to the present value.

(ii) Find out the net present value by deducting the present value of the outflows from the

present value of the inflows.

(iii) If the net present value is positive apply higher rate of discount.

(iv) If the higher discount rate still gives a positive net present value increase the discount

rate further until the UPV becomes negative.

(v) If the NPV is negative at this higher rate the cost of debt must be between these two

rates.

Illustration 3: X Ltd. has issued redeemable zero coupon bonds of Rs. 100 each at a discount

rate of Rs. 60 repayable at the end of fourth year. Calculate the cost of debt.

8

Cash Flow Table At Various Assumed Discount Rates

Year Cash flow

(Rs.)

Discount Factor at

12%

P.V. at 12%

Rs.

Discount

Factor at

14%

P.V. at 14%

Rs.

0

4

60

100

1.000

0.636

(60)

63.60

3.60

1.000

0.592

(60)

59.20

-0.80

Cost of Debt (Kd) = 12+ )1214(80.060.3

60.3−×

+

= 12+ 240.4

60.3× = 13.64%

Floating or Variable Rate Debt

The interest on floating rate debt changes depending upon the market rate of interest

payable on gilt edged securities or the prime lending rate of the bank. For example, suppose a

company raises debt from external sources on the terms of prime lending rate of the bank plus

four percent. If the prime lending rate of the bank is 8% p.a. the company will have to pay

interest at the rate of 12% p.a. Further, if the prime lending rate falls to 6% p.a. the company

shall pay interest at only 10% p.a.

Illustration 4: ABC Ltd. raised a debt of Rs. 50 lakhs on the terms that interest shall be

payable at prime lending rate of bank plus three percent. The prime lending rate of the bank is 7

per cent. Calculate the cost of debt assuming that the corporate rate of tax is 35%.

Solution:

Before-tax cost of debt,

Kdb = 7%+3% = 10%

After-tax cost of debt,

Kda = Kdb (1-t)

= 10% (1-0.35) = 10% (0.65) = 6.5%

Real or Inflation Adjusted Cost of Debt

In the days of inflation, the real cost of debt is much loss than the nominal cost as the

fixed amount is payable irrespective of the fall in the value of money because of price level

changes. The real cost of debt can be calculated as below:

Real Cost of Debt = RateInflation

DebtofCostalNo

+

+

1

min1

2. Cost of Preference Capital

A fixed rate of divided is payable on preference shares. Though dividend is payable at the

discretion of the Board of directors and there is no legal binding to pay dividend, yet it does not

mean that preference capital is cost free. The cost of preference capital is a function of dividend

expected by its investors i.e. its stated dividend. In case dividends are not paid to preference

shareholders, it will affect the fund raising capacity of the firm. Hence, dividends are usually

9

paid regularly on preference shares except when there are no profits to pay dividends. The cost

of preference capital which is perpetual can be calculated as:

Kp = P

D

where Kp = Cost of Preference Capital

D = Annual Preference Dividend

P = Preference Share Capital (Proceeds.)

Further, if preference shares are issued at Premium or Discount or when costs of

floatation are incurred to issue preference shares, the nominal or par value of preference share

capital has to be adjusted to find out the net proceeds from the issue of preference shares. In such

a case, the cost of preference capital can be computed with the following formula:

Kp = NP

D

It may be noted that as dividend are not allowed to be deducted in computation of tax, no

adjustment is required for taxes.

Sometimes Redeemable Preference Shares are issued which can be redeemed or

cancelled on maturity date. The cost of redeemable preference share capital can be calculated as:

( )NPMV

n

NPMVD

Kpr

+

−+

=

2

1

where, Kpr = Cost of Redeemable Preference Shares

D = Annual Preference dividend

MV = Maturity Value of Preference Shares

NP = Net proceeds of Preference Shares

Illustration 5: A company issues 10,000 shares 10% Preference Shares of Rs. 100 each. Cost of

issue is Rs. 2 per share. Calculate cost of preference capital if these shares are issued (a) at par,

(b) at a premium of 10% and (c) at a discount of 5%.

Solution:

Cost of Preference Capital, Kp = NP

D

(a) %2.10100000,80,9

000,00,1100

000,20000,00,10

000,00,1=×=×

−=

pK

(b) 100000,20000,00,1000,00,10

000,00,1×

−+=

PK = 100

000,80,10

000,00,1×

= 9.26%

(c) 100000,20000,50000,00,10

000,00,1×

−−=

PK = 100

000,30,9

000,00,1×

=10.75%

10

3. Cost of Equity Share Capital

The cost of equity is the maximum rate of return that the company must earn on equity

financed portion of its investments in order to leave unchanged the market price of its stock.’

The cost of equity capital is function of the expected return by its investors. The cost of equity is

not the out-of-pocket cost of using equity capital as the equity shareholders are not paid dividend

at a fixed rate every year. Moreover, payment of dividend is not a legal binding. It may or may

not be paid. But it does not mean that equity share capital is a cost free capital. The cost of equity

can be computed in following ways:

(a) Dividend Yield Method or Dividend/Price Ratio Method : According to this method,

the cost of equity capital is the ‘discount rate that equates the present value of expected future

dividends per share with the net proceeds (or current market price) or a share’. Symbolically.

Ke = MP

Dor

NP

D

where, Ke = Cost of Equity Capital

D = Expected dividend per share

NP = net proceeds per share

and MP = Market Price per share.

Illustration 6: A company issues 1000 equity shares of Rs. 100 each at a premium of 10%. The

company has been paying 20% dividend to equity shareholders for the past five years and

expects to maintain the same in the future also. Compute the cost of equity capital, Will it make

any difference if the market price of equity share is Rs. 160?

Solution:

Ke = NP

D

= %18.18100x110

20=

If the market price of a equity share is Rs. 160

Ke = MP

D

= %5.12100x160

20=

(b) Dividend yield plus growth in dividend method : When the dividends of the firm are

expected to grow at a constant rate and the dividend pay out ratio is constant this method may be

used to compute the cost of equity capital. According to this method the cost of equity capital is

based on the dividends and the growth rate.

Ke = ( )

GNP

gDG

NP

DO +

+=+

11

where, Ke = Cost of equity capital

D1 = Expected Dividend per share at the end of the year

NP = Net proceeds per share

G = Rate of growth in dividends

Do = previous year’s dividend.

11

Further, in case cost of existing equity share capital is to be calculated, the NP should be

changed with MP (market price per share) in the above equation.

Ke = GMP

D+1

Illustration7: (a) A company plans to issue 1000 new shares of Rs. 100 each at par. The

floatation costs are expected to be 5% of the share price. The company pays a dividend of Rs. 10

per share initially and the growth in dividends is expected to be 5%. Compute the cost of new

issue of equity shares.

(b) If the current market price of an equity share is Rs. 150, calculate the cost of existing equity

share capital.

Solution:

(a) Ke = GNP

D+

= %53.15%55100

10=+

−

(b) Ke = GMP

D+

= %67.11%5150

10=+

(c) Earning Yield Method : According to this method, the cost of equity capital is the

discount rate that equates the present values of expected future earnings per share with the net

proceeds (or, current market price) of a share. Symbolically:

Ke = oceedsNet

shareperEarnings

Pr

= NP

EPS

where, the cost of existing capital is to be calculated:

Ke = SharePericeMarket

shareperEarnings

Pr

= MP

EPS

(d) Realised Yield Method: One of the serious limitations of using dividend yield method

or earnings yield method is the problem of estimating the expectations of the investors regarding

future dividends and earnings. It is not possible to estimate future dividends and earnings

correctly; both of these depend upon so many uncertain factors. To remove this drawback,

realised yield method which takes into account the actual average rate of return realised in the

past may be applied to compute the cost of equity share capital. To calculate the average rate of

return realised, dividend received in the past along with the gain realised at the time of sale of

shares should be considered. The cost of equity capital is said to be the realised rate of return by

the shareholders. This method of computing cost of equity share capital is based upon the

following assumptions:

12

(a) The firm will remain in the same risk class over the period.

(b) The shareholders expectations are based upon the past realised yield.

(c) The investors get the same rate of return as the realised yield even if they invest elsewhere;

(d) The market price of shares does not change significantly.

4. Cost of Retained Earning

It is sometimes argued that retained earnings do not involve any cost because a firm is not

required to pay dividends on retained earnings. However, the shareholders expect a return on

retained profits. Retained earnings accrue to a firm only because of some sacrifice made by the

shareholders in not receiving the dividends out of the available profits.

The cost of retained earnings may be considered as the rate of return which the existing

shareholders can obtain by investing the after tax dividends in alternative opportunity of equal

qualities. It is, thus, the opportunity cost of dividends foregone by the shareholders. Cost of

retained earnings can be computed with the help of following formula:

Kr = GNP

D+

where,

Kr = Cost of retained earnings

D = Expected dividend

NP = Not proceeds of share issue

G = Rate of growth.

13

2

COST OF CAPITAL – II

Smriti Chawla Shri Ram College of Commerce

University of Delhi

Computation of Weighted Average Cost of Capital

Weighted average cost of capital is the average cost of the costs of various source of

financing. Weighted average cost of capital is also known as composite cost of capital, overall

cost of capital or average cost of capital. Once the specific cost of individual sources of finance

is determined, we can compute the weighted average cost of capital by putting weights to the

specific costs of capital in proportion of various sources of funds to total. The weights may be

given either by using the book value of source or market value of source. If there is a difference

between market value and book value weights, the weights, the weighted average cost of capital

would also differ. The market value weighted average cost would be overstated if market value

of the share is higher than book value and vice versa. The market value weights are sometimes

preferred to the book value weights because the market value represents the true value of

investors. However, the market value weights suffer from the following limitations:

(i) It is very difficult to determine the market values because of frequent fluctuations.

(ii) With the use of market value weights, equity capital gets greater importance.

For the above limitations, it is better to use book value which is readily available. Weighted

average cost of capital can be computed as follows:

Kw = W

XW

∑

∑

Kw = Weighted average cost of capital

X = Cost of specific source of finance

CHAPTER OBJECTIVES

� Computation of weighted average cost of capital

� Marginal cost of capital � Cost of Equity using Capital Asset Pricing Model

� Illustrations � Lets Sum Up

� Questions

14

W = Weight, proportion of specific source of finance

Illustration1: A firm has the following capital structure and after-tax costs for the different

sources of funds used:

Source of Funds Amount

Rs.

Proportion

%

After-tax cost

%

Debt

Preference Shares

Equity Shares

Retained Earnings

Total

15,00,000

12,00,000

18,00,000

15,00,000

60,00,000

25

20

30

25

100

5

10

12

11

You are required to compute the weighted average cost of capital.

Solution:

Computation of Weighted Average Cost of Capital

Source of Funds Proportion %

(W)

Cost %

(X)

Weighted Cost %

Proportion ×Cost

(XW) %

Debt

Preference shares

Equity Shares

Retained Earnings

25

20

30

25

5

10

12

11

1.25

2.00

3.60

2.75

Weighted Average Cost of

Capital

9.60%

Illustration2: Continuing illustration 1, the firm has 18,000 equity shares of Rs. 100 each

outstanding and the current market price is Rs. 300 per calculate the market, value weighted

average cost of capital assuming that the market values and book values of the debt and

preference capital are same.

Solution:

Sources of Funds

Amount

(Rs.)

Proportion %

W

Cost

% X

Weighted Cost

Proportion ×

Cost XW

Debt

Preference Capital

Equity Share Capital

(18000 shares @ Rs. 300)

15,00,000

12,00,000

54,00,000

81,00,000

18.52

14.81

66.67

100

5

10

12

0.93

1.48

8.00

Weighted Average Cost of Capital 10.41%

Marginal Cost of Capital

The marginal cost of capital is the weighted average cost of new capital calculated by

using the marginal weights. The marginal weights represent the proportion of various sources of

funds to be employed in raising additional funds. In case, a firm employs the existing proportion

15

of capital structure and the component costs remain the same the marginal cost of capital shall be

equal to the weighted average cost of capital. But in practice, the proportion and /or the

component costs may change for additional funds to be raised. Under this situation the marginal

cost of capital shall not be equal to weighted average cost of capital. However, the marginal cost

of capital concept ignores the long-term implications of the new financing plans, and thus,

weighted average cost of capital should be preferred for maximisation of shareholder’s wealth in

the long-run.

Illustration3: A firm has the following capital structure and after-tax costs for the different

sources of funds used:

Source of Funds Amount (Rs.) Proportion (%) After-tax Cost (%)

Debt

Preference Capital

Equity Capital

4,50,000

3,75,000

6,75,000

15,00,000

30

25

45

100

7

10

15

(a) Calculate the weighted average cost of capital using book-value weights.

(b) The firm wishes to raise further Rs. 6,00,000 for the expansion of the project as below.

Debt Rs. 3,00,000

Preference Capital Rs. 1,50,000

Equity Capital Rs. 1,50,000

Assuming that specific costs do not change, compute the weighted marginal cost of capital.

Solution:

Computation of Weighted Average Cost of Capital (WACC)

Source of Funds Proportion (%) (W) After tax cost (%)

(X)

Weighted Cost %

(XW) %

Debt

Preference Capital

Equity Capital

30

25

45

7

10

15

2.10

2.50

6.75

Weighted Average Cost of Capital (WACC) 11.35%

Computation of Weighted Marginal Cost of Capital (WMCC)

Source of Funds Marginal Weights

Proportion (%) (W)

After tax cost (%)

(X)

Weighted Marginal

Cost %

Debt

Preference Capital

Equity Capital

50

25

25

7

10

15

3.50

2.50

3.75

Weighted Marginal Cost of Capital (WMCC) 9.75%

Cost of Equity Using Capital Asset Pricing Model (CAPM)

The value of an equity share is a function of cash inflows expected by the investors and risk

associated with cash inflows. It is calculated by discounting the future stream of dividends at

required rate of return called capitalization rate. The required rate of return depends upon the

16

element of risk associated with investment in share. It will be equal to the risk free arte of

interest plus the premium for risk. Thus required rate of return Ke for the share is,

Ke = Risk – free rate of interest + Premium for risk

According to CAPM, the premium for risk is the difference between market return from

diversified portfolio and risk free rate of return. It is indicated of beta coefficient (β):

Risk – premium= (Market return of a diversified portfolio – Risk free return) x β I =β I (Rm - Rf )

Thus, cost of equity, according to CAPM can be calculated as below:

Ke = Rf + β I (Rm - Rf )

where, Ke = Cost of equity capital

Rf = Risk free rate of return

Rm = Market return of a diversified portfolio

β I = Beta coefficient of the firm’s portfolio

Illustration3: You are given the following facts about a firm:

1.Risk free rate of return is 11%.

2.Beta co-efficient βI of the firm is 1.25.

Compute the cost of equity capital using Capital Asset Pricing Model (CAPM) assuming a

market return of 15 percent next year. What would be the cost of equity if βI rises to 1.75.

Solution:

Ke = Rf + β I (Rm - Rf )

when βI = 1.25

Ke =11% +1.25(15%-11%)

=11%+5% =16%

when βI =1.75 Ke= 11%+1.75(15%-11%)

=11%+7%

=18%

Illustration 4: The following is an extract from the financial statement of KPN Ltd.

Rs.lakhs (Operating

Profit 105

Less :Interest on debentures 33

72

Less: Income –tax (50%) 36

Net Profit 36

Equity Share capital (shares of Rs.10 each) 200

Reserves and Surplus 100

15%Non-convertible

debentures (of Rs.100 each) 220

520

17

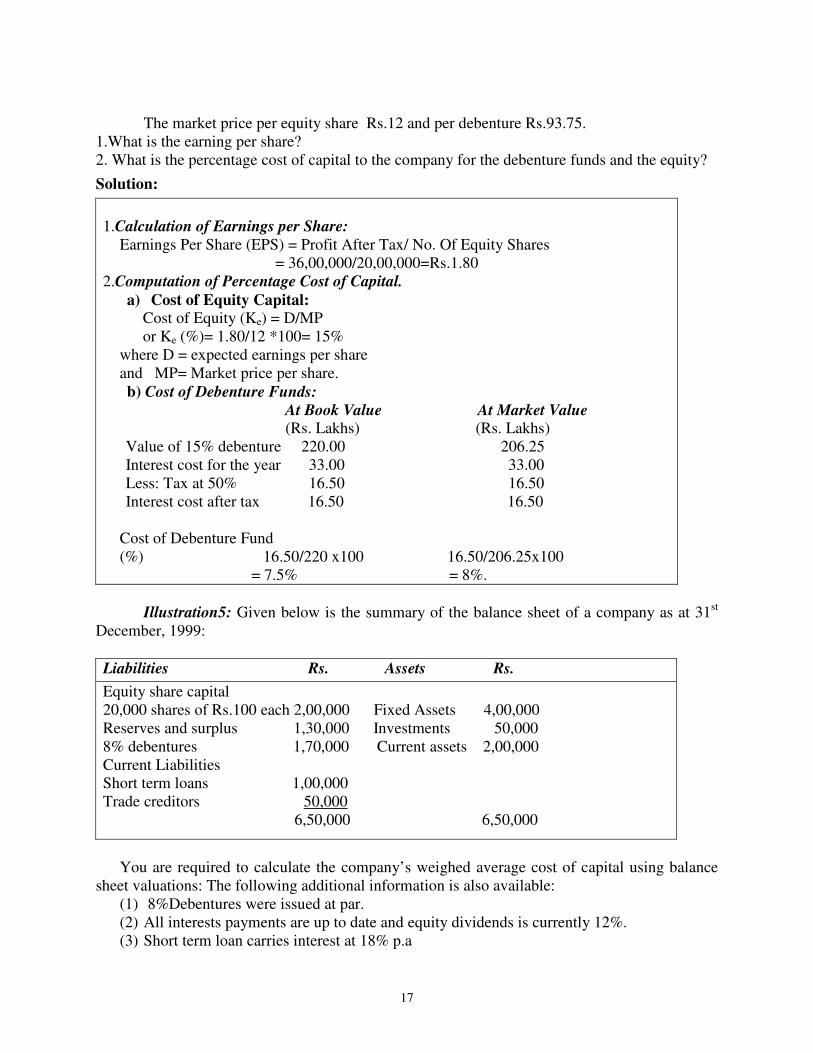

The market price per equity share Rs.12 and per debenture Rs.93.75.

1.What is the earning per share?

2. What is the percentage cost of capital to the company for the debenture funds and the equity?

Solution:

1.Calculation of Earnings per Share:

Earnings Per Share (EPS) = Profit After Tax/ No. Of Equity Shares

= 36,00,000/20,00,000=Rs.1.80

2.Computation of Percentage Cost of Capital.

a) Cost of Equity Capital:

Cost of Equity (Ke) = D/MP

or Ke (%)= 1.80/12 *100= 15%

where D = expected earnings per share

and MP= Market price per share.

b) Cost of Debenture Funds:

At Book Value At Market Value

(Rs. Lakhs) (Rs. Lakhs)

Value of 15% debenture 220.00 206.25

Interest cost for the year 33.00 33.00

Less: Tax at 50% 16.50 16.50

Interest cost after tax 16.50 16.50

Cost of Debenture Fund

(%) 16.50/220 x100 16.50/206.25x100

= 7.5% = 8%.

Illustration5: Given below is the summary of the balance sheet of a company as at 31st

December, 1999:

Liabilities Rs. Assets Rs.

Equity share capital

20,000 shares of Rs.100 each 2,00,000 Fixed Assets 4,00,000

Reserves and surplus 1,30,000 Investments 50,000

8% debentures 1,70,000 Current assets 2,00,000

Current Liabilities

Short term loans 1,00,000

Trade creditors 50,000

6,50,000 6,50,000

You are required to calculate the company’s weighed average cost of capital using balance

sheet valuations: The following additional information is also available:

(1) 8%Debentures were issued at par.

(2) All interests payments are up to date and equity dividends is currently 12%.

(3) Short term loan carries interest at 18% p.a

18

(4) The shares and debentures of the company are all quoted on the Stock Exchange and

current Market prices are as follows:

Equity Shares Rs.14 each

8% Debentures Rs.98 each.

(5) The rate of tax for the company may be taken at 50%.

Solution:

Calculation of the Cost of Equity: Rs.

Equity Share 2,00,000

Reserves and Surplus 1,30,000

Equity (Shareholder’s )Fund 3,30,000

Book Value Per Share = 3,30,000/20,000 =Rs.16.50.

Equity Dividend Per Share = 12/100*10 =Rs.1.20

Therefore, Cost Of Equity (%)= 1.20/16.50*100= 7.273 %

Computation of Weighted Average Cost of Capital:

Capital Structure or

Type of Capital Amount (Rs) Before Tax After Tax Weighted Average

cost Cost% (Rs.) Cost%

Equity Funds 3,30,000 7.273% 7.273% 24,000

Debentures 1,70,000 8% 4% 6,800

Total 5,00,000 30,800

Weighted Average Cost of Capital = 30,800/5,00,000*100 =6.16 %.

19

Summary of Formulae

S.No

Purpose Formula

1

2

3

4

5

6

7

8

9

10

11

12

13

Before tax cost of debt

After cost of debt

Before tax cost of redeemable debt

After tax cost of redeemable debt

Cost of debt redeemable at premium

Cost of debt redeemable in instalments

Cost of irredeemable preference share capital

Cost of redeemable preference share capital

Cost of equity –dividend yield approach

Cost of equity – dividend yield plus constant

growth

Cost of retained earnings

Weighted average cost of capital

Cost of equity – CAPM approach

Kdb =NP

I

Kda = Kdb (1-t) = ( )tNP

I−1

( )

( )NPP

NPPn

I

Kdb

+

−+

=

2

1

1

Kda = Kdb (1-t)

( )

( )NPRV

NPRVn

I

Kdb

+

−+

=

2

1

1

Vd = ( )

∑− +

+n

t

t

d

tt

KI

PI

1

Kp = NP

D

( )NPMV

n

NPMVD

Kpr

+

−+

=

2

1

Ke = MP

Dor

NP

D

Ke = ( )

GNP

gDG

NP

DO +

+=+

11

Kr = GNP

D+

Kw = W

XW

∑

∑

Ke = Rf + β I (Rm - Rf )

20

Lets Sum Up

� The cost of capital is the minimum required rate of return which firm must earn on its

funds in order to satisfy the expectation of its supplier of funds. If the return from capital

budgeting proposals is more than cost of capital then difference will be added to wealth

of shareholders.

� The concept of cot of capital has a role to play in capital budgeting as well as in finalizing

the capital structure for the firm. The cost of capital depends upon the risk free interest

rate and risk premium, which depends upon the risk of investment and risk of firm.

� The cost of capital may be defined in terms of (1) explicit cost, which the firm pays to

supplier, and (2) implicit cost. i.e. opportunity cost of funds to firm. The cost of capital is

calculated in after tax terms.

� Different sources of funds available to firm may be grouped into Debt, Pref. share capital,

Equity share capital and retained earning and these sources have their specific cost of

capital. However the overall cost of capital of the firm may be ascertained as the

weighted average of these specific costs of capital.

� The cost of retained earnings is lower than cost of equity as former does not have any

floatation cost.

� The Weighted average cost of capital WACC may be ascertained by applying book value

weights or market value weights of different sources of funds. The WACC is denoted as

Kw.

QUESTIONS

1. What is the relevance and significance of cost of capital in capital budgeting? How does the

cost of capital enter the capital budgeting process?

2. Define the concept of cost of capital? State how you would determine the weighted average

cost of capital of a firm?

3. How cost of equity capital is determined under CAPM?

4. Write short notes on (a) Marginal cost of capital (b) Cost of retained earnings

5. The cost of preference capital is generally lower than cost of equity. State the reasons?

6. What are the problems in determining the cost of capital?

7. How is the cost of zero coupon bonds determined?

21

3

CAPITAL STRUCTURE THEORIES

Smriti Chawla Shri Ram College of Commerce

University of Delhi

Concept of Capital Structure

Capital Structure refers to the proportionate amount that makes up capitalisation. Some

authors include retained earnings and capital surplus for the purpose of capital structure; in that

case capital structure shall be:

Rs. Proportion/Mix

Equity Share Capital 10,00,000 42.55%

Preference Share Capital 5,00,000 21.28%

Long-Term loans and Debentures 2,00,000 8.51%

Retained Earnings 6,00,000 25.53%

Capital Surplus 50,000 2.13%

23,50,000 100%

Hence, the term capital structure refers to the firm’s permanent or long term financing

consisting of equity share capital, retained earnings, preference share capital, debentures and

long-term debts.

CHAPTER OBJECTIVES

� Concept of Capital Structure � Optimal Capital Structure � Objects of Appropriate Capital Structure � Importance of Capital Structure � Theories of Capital Structure

o Net Income Approach o Net Operating Income Approach o Traditional Approach

o Modigliani and Miller Model

22

Optimal Capital Structure

The capital structure decision can influence the value of the firm through the cost of

capital and trading on equity or leverage. The optimum capital structure may be defined as “that

capital structure or combination of debt and equity that leads to the maximum value of the firm”

optimal capital structure ‘maximum’ the value of the company and hence the wealth of its

owners and minimizes the company’s cost of capital’ (Solomon, Ezra, the Theory of Financial

Management). Thus every firm should aim at achieving the optimal capital structure and then to

maintain it.

The following considerations should be kept in mind while maximizing the value of the

firm in achieving the goal of optimum capital structure:

(i) If the return on investment is higher than the fixed cost of funds, the company should

prefer to raise funds having a fixed cost, such as debentures, loans and preference share

capital. It will increase earnings per share and market value of the firm. Thus, a company

should, make maximum possible use of leverage.

(ii) When debt is used as source of finance, the firm saves a considerable amount in payment

of tax as interest is allowed a deductible expense in computation of tax. Hence, the

effective cost of debt is reduced called tax leverage. A company should, therefore, take

advantage of tax leverage.

(iii) The firm should undue financial risk attached with the use of increased debt financing. It

the shareholders perceive high risk in using further debt-capital, it will reduce the market

price of shares.

(iv) The capital structure should be flexible.

Objects of an Appropriate Capital Structure

The objects of an appropriate capital structure have been summarized by Soloman Ezra in

the following words:

“The advantage of having an appropriate financial structure, if such an optimum does

exist, are two fold, it maximizes value of the company and hence the wealth of its owner; it

minimizes the company’s cost of capital which in turn increases its ability to find new wealth

creating investment opportunities. Also by increasing the firm’s opportunities to engage in future

wealth creating investment, it increases the economy’s rate of investment and growth.”

More specifically, the objects may be classified as follows:

� Minimisation of cost of capital

� Minimization of Risk

� Maximization of Return

� Preservation of control

Importance of Capital Structure

The term 'Capital structure' refers to the relationship between the various long-term forms

of financing such as debenture, preference share capital and equity share capital. Financing the

firm's assets is a very crucial problem in every business and as a general rule there should be a

proper mix of debt and equity capital in financing the firm’s assets. The use of long –term fixed

23

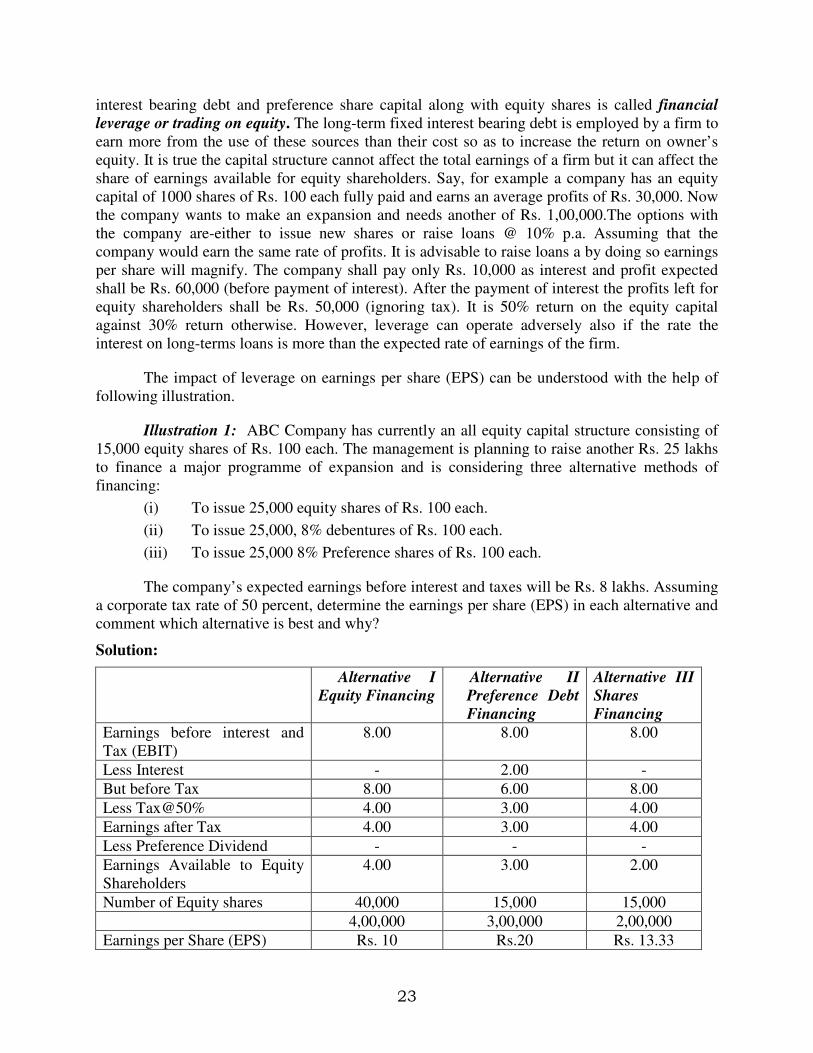

interest bearing debt and preference share capital along with equity shares is called financial

leverage or trading on equity. The long-term fixed interest bearing debt is employed by a firm to

earn more from the use of these sources than their cost so as to increase the return on owner’s

equity. It is true the capital structure cannot affect the total earnings of a firm but it can affect the

share of earnings available for equity shareholders. Say, for example a company has an equity

capital of 1000 shares of Rs. 100 each fully paid and earns an average profits of Rs. 30,000. Now

the company wants to make an expansion and needs another of Rs. 1,00,000.The options with

the company are-either to issue new shares or raise loans @ 10% p.a. Assuming that the

company would earn the same rate of profits. It is advisable to raise loans a by doing so earnings

per share will magnify. The company shall pay only Rs. 10,000 as interest and profit expected

shall be Rs. 60,000 (before payment of interest). After the payment of interest the profits left for

equity shareholders shall be Rs. 50,000 (ignoring tax). It is 50% return on the equity capital

against 30% return otherwise. However, leverage can operate adversely also if the rate the

interest on long-terms loans is more than the expected rate of earnings of the firm.

The impact of leverage on earnings per share (EPS) can be understood with the help of

following illustration.

Illustration 1: ABC Company has currently an all equity capital structure consisting of

15,000 equity shares of Rs. 100 each. The management is planning to raise another Rs. 25 lakhs

to finance a major programme of expansion and is considering three alternative methods of

financing:

(i) To issue 25,000 equity shares of Rs. 100 each.

(ii) To issue 25,000, 8% debentures of Rs. 100 each.

(iii) To issue 25,000 8% Preference shares of Rs. 100 each.

The company’s expected earnings before interest and taxes will be Rs. 8 lakhs. Assuming

a corporate tax rate of 50 percent, determine the earnings per share (EPS) in each alternative and

comment which alternative is best and why?

Solution:

Alternative I

Equity Financing

Alternative II

Preference Debt

Financing

Alternative III

Shares

Financing

Earnings before interest and

Tax (EBIT)

8.00 8.00 8.00

Less Interest - 2.00 -

But before Tax 8.00 6.00 8.00

Less Tax@50% 4.00 3.00 4.00

Earnings after Tax 4.00 3.00 4.00

Less Preference Dividend - - -

Earnings Available to Equity

Shareholders

4.00 3.00 2.00

Number of Equity shares 40,000 15,000 15,000

4,00,000 3,00,000 2,00,000

Earnings per Share (EPS) Rs. 10 Rs.20 Rs. 13.33

24

Comments: As the earnings per share highest in alternative II, i.e. debt financing, the

company should issue 25,000 8% debentures of Rs. 100 each. It will double the earnings of the

equity shareholders without loss of any control over the company.

Theories of Capital Structure

Different of theories have been propounded by different authors to explain the

relationship between capital structure, cost of capital and value of the firm. The main

contributors to the theories are Durand, Ezra, Solomon, Modigliani and Miller. The important

theories are discussed below:

1. Net Income Approach.

2. Net Operating Income Approach.

3. The Traditional Approach

4. Modigliani and Miller Approach.

Assumptions: For clear understanding of the theories of capital structure and relationship

between capital structure, cost of capital and the value of firm, following assumptions are

made:

� The firm uses only two sources of funds i.e debt and equity

� The firm’s total assets are given and its investment decisions do not change.

� The firm’s total financing remains unchanged but degree of leverage can be changed for

replacing debt for equity or equity for debt.

� The firm’s dividend pay out ratio is 100% and it does not a all retain the earnings.

� The EBIT is not expected to grow.

� Business risk of the firm is constant and it is assumed to be independent of capital

structure and financial risk.

� Investor’s subjective probability distribution of the future expected operating earnings of

the firm is the same.

(1) Net Income Approach

According to this approach, a firm can minimize the weighted average cost of capital and

increase the value of the firm as well as market price of equity shares by using debt financing

to the maximum possible extent. The theory propounds that a company can increase its value

and reduce the overall cost of capital by increasing the proportion of debt in its capital

structure. This approach is based upon the following assumptions:

(i) The cost of debt is less than the cost of equity.

(ii) There are no taxes.

(iii) The risk perception of inventors is not changed by the use of debt.

25

The line of argument in favour of net income approach is that as proportion of debt

financing in capital structure increase¸ the proportion of and cheaper source of funds increases.

This result in the decrease in overall (weighted average) cost of capital leading to an increase in

the value of the firm. The reasons for assuming cost of debt to be less than the cost of equity are

that interest rates are usually lower than dividend rates due to element of risk and the benefit of

tax as the interest is a deductible expense.

The figure shows that kd and ke are constant for all levels of leverages i.e. for all levels of

debt financing. As the debt proportion of the financial leverage increases, the WACC, ko,

decreases as the kd is less than ke. This result in the increase in value of the firm. It may be noted

that ko will approach kd as the debt proportion is increased. However, ko will never touch kd as

there cannot be a 100% debt firm. Some element of equity must be there. However, if the firm is

100% equity firm, then the ko is equal to ke. The rate of decline in ko depends upon the relative

position of kd and ke. Net Income Approach suggests that higher the degree of leverage, better it

is, as the value of the firm would be higher.

Illustration 2: (a) A company expects a net income of Rs. 80,000. It has Rs. 2,00,000,

8% Debentures. The equity capitalization rate of the company is 10%. Calculate the value of the

firm and overall capitalisation rate according to the Net Income Approach (ignoring income-tax).

(b) If the debenture debt is increased to Rs. 3,00,000, what shall be the value of the firm and the

overall capitalisation rate?

26

Solution:

(a) Calculation Of The Value Of The Firm

Market Value of Equity = 64, 000× 10

100

= Rs. 6,40,000

Market Value of Debentures = Rs. 2,00,000

Value of the Firm = Rs. 8,40,000

Calculation Of Overall Capitalisation Rate

Overall Cost of Capital (ko) =

V

EBIT

firmtheofValue

Earningsx

= 100x000,40,8

000,80

= 9.52%

b) Calculation Of Value Of The Firm If Debenture Debits Raised To Rs. 3,00,000

Rs

Net Income 80,000

Less: Interest on 8% Debentures of Rs. 3,00,000 24,000

Earnings available to equity shareholders 56,000

Equity Capitalisation Rate 10% 10%

Market Value of Equity = 56,000× 10

100

= Rs. 5,60,000

Market Value of Debentures = Rs. 3,00,000

Value of the Firm = Rs. 8,60,000

Overall Capitalisation Rate = 000,60,8

000,80× 100 = 9.30%

27

Thus, it is evident that with the increase in debt financing the value of the firm has increased and

the overall cost of capital has decreased.

( 2 ) Net Operating Income Approach

This theory as suggested Durand is another extreme of the effect of leverage on the value

of the firm. It is diametrically opposite to the net income approach. According to this approach,

change in the capital structure of a company does not affect the market value of the firm and the

overall cost of capital remains constant irrespective of the method of financing. It implies that the

overall of capital remains the same whether the debt-equity mix is 50:50 or 20:80 or 0:100.

Thus, there is nothing as an optimal capital structure and every capital structure is the optimum

capital structure. This theory presumes that:

(i) the market capitalizes the value of the firm as a whole;

(ii) the business risk remains constant at every level of debt equity mix.

The reasons propounded for such assumptions are that the increased use of debt increase

the financial risk of the equity shareholders and hence the cost of equity increases. On the other

hand, the cost of debt remains constant with the increasing proportion of debt as the financial

risk of the lenders is not affected. Thus, the advantage of using the cheaper source of funds, i.e.;

debt is exactly offset by the increased cost of equity.

The figure shows that the cost of debt, kd, and the overall cost of capital, ko, are constant

for all levels of leverage. As the debt proportion or the financial leverage increases, the risk of

the shareholders also increases and thus the cost of equity capital, ke also increases. However, the

increase in ke, is such that the overall value of the firm remains same. It may be noted that for an

all equity firm, the ke is just equal to ko. As the debt proportion is increased, the ke also increases.

However, the overall cost of capital remains constant because increase in ke is just sufficient to

off set the benefits of cheaper debt financing.

28

Illustration 3 (a): A company expected a net operating income of Rs. 1,00,000. It has Rs.

5,00,000, 6% Debentures. The overall capitalisation rate is 10%. Calculate the value of the firm

and the equity capitalisation rate (cost of equity) according to the Net Operating Income

Approach.

(b) If the debenture debt is increased to Rs. 7,50,000. what will be the effect on the value of the

firm and the equity capitalisation rate?

Solution:

(a) Net Operating Income = Rs. 1,00,000

Overall Cost of Capital = 10%

Market Value of the first (V) = )(0K

EBIT

CapitalofCostOverall

comeOpeartingnNet

= 1,00,000× 10

100

= Rs. 10,00,000

Market Value of Firm Rs. 10,00,000

Less: Market Value of Debentures Rs. 5,00,000

Total Market Value of Equity Rs. 5,00,000

Equity Capitalisation Rate or Cost of equity (Ke)

= Earnings available to equity shareholders or EBIT – I/V - B

Total market value of equity shares

(where, EBIT means Earnings before Interest and Tax)

V is Value of the firm

B is Value of debt capital

I is interest on debt

= 1,00,000 – 30,000/10,00,000 – 5,00,000 × 100

=

000,00,5

000,70×100=14%

(b) If the debenture debt is increased to Rs. 7,50,000, the value of the firm shall remain

unchanged at Rs. 10,00,000. The equity capitalisation rate will increase as follows:

29

Equity Capitalization Rate (ke)

= EBIT – I / V - B

= 1,00,000 – 45,000/10,00,000 – 7,50,000×100

= 000,50,2

000,55×100 = 22%

(3) The Traditional Approach

The traditional approach, also known as Intermediate approach, is a compromise between

the two extremes of net income approach and net operating income approach. According to this

theory, the value of the firm can be increased initially or the cost of capital can be decreased by

using more debt as the debt is a cheaper source of funds than equity. Thus, optimum capital

structure can be reached by a proper debt-equity mix. Beyond a particular point, the cost of

equity increases because increase debt increases the financial risk of the equity shareholders. The

advantage of cheaper debt at this point of capital structure is offset by increased cost of equity

after this there comes a stage, when the increased cost of equity cannot be offset by the

advantage of low-cost debt. Thus, overall cost of capital, according to this theory, decreases upto

a certain point, remains more or less unchanged for moderate increase in debt thereafter: and

increase or rises beyond a certain point. Even the cost of debt may increase at this state due to

increased financial risk.

Traditional View point on the relationship between Leverage, cost of

capital and value of the firm.

The figure shows that there can either be a particular financial leverage (as in Part A) or a

range of financial leverage (as in Part B) when the overall cost of capital, ko is minimum. The

figure in Part A shows that at the financial leverage level O, the firm has the lowest ko and

therefore, the capital structure at that financial leverage is optimal. The Part B of the figure

shows that there is not one optimal capital structure, rather there is a range of optimal capital

structure from leverage level O to level P. Every capital structure over this range of financial

leverage is an optimal capital structure. Thus, as per the traditional approach, a firm can be

benefited from a moderate level of leverage when the advantages using debt (having lower cost)

out weigh the disadvantages of increasing ke (as a result of higher financial risk). The overall

cost of capital, ko, therefore is a function of the financial leverage. The value of the firm can be

affected therefore, by the judicious use of debt and equity in the capital structure.

30

Illustration 4: Compute the market value of the firm, value of shares and the average cost of

capital from the following information:

Rs.

Net Operating Income 2,00,000

Total Investment 10,00,000

Equity Capitalisation Rate:

a) If the firm uses no debt 10%

b) If the firm uses Rs. 4,00,000 debentures 11%

c) If the firm uses Rs. 6,00,000 debentures 13%

Assume that Rs.4,00,000 debentures can be raised at 5% rate of interest whereas Rs. 6,00,000

debentures can be raised at 6% rate of interest.

Solution:

Computation of Market Value of Firm, Value of Shares & the Average Cost of Capital

(a) No debt (b)Rs.4,00,000

5%Debentures

(c)Rs.6,00,000

6%Debentures

Net Operating Income Rs. 2,00,000 Rs. 2,00,000 Rs. 2,00,000

Less: Interest i.e., Cost of

debt:

20,000

36,000

Earnings available to

Equity Shareholders

Rs. 2,00,000 Rs.1,80,000 Rs. 1,64,000

Equity Capitalisation Rate 10% 11% 13%

Market Value of shares 2,00,000×

10

100 1,80,000×

11

100 1,64,000×

13

100

Rs. 20,00,000 Rs. 16,36,363 Rs. 12,61,538

Market value of debt

(debentures)

Market Value of firm

20,00,000

4,00,000

20,36,363

6,00,000

18,61,538

Average Cost of Capital

000,00,20

000,00,2×100

363,36,20

000,00,2×100

538,61,18

000,00,2×100

V

EBITor

firmtheofValue

Earnings

= 10% = 9.8% = 10.7%

Comments: It is clear from the above that if debt of Rs. 4,00,000 is used the value of the firm

increases and the overall cost of capital decreases. But, if more debt is used to finance in place of

equity, i.e., Rs. 6,00,000 debentures, the value of the firm decreases and the overall cost of

capital increases.

31

(4) Modigliani-Miller Approach

M&M hypothesis is identical with the Net Operating Income approach if taxes are

ignored. However, when corporate taxes are assumed to exist, their hypothesis is similar to the

Net Income Approach.

(a) In the absence of taxes: The theory proves that the cost of capital is not affected by

changes in the capital structure or say that the debt-equity mix is irrelevant in the determination

of the total value of a firm. The reason argued is that though debt is cheaper to equity, with

increased use of debt as a source of finance, the cost of equity increases. This increases in cost of

equity offsets the advantages of low cost of debt. Thus, although the financial leverage affects

the cost of equity, the overall cost of capital remains constant. The theory emphasizes the fact

that firm’s operating income is a determinant of its total value. The theory further propounds that

beyond a certain limit of debt, the cost of debt increases (due to increased financial risk) but the

cost of equity falls thereby again balancing the two costs. In the opinion of Modigliani & Miller,

two identical firms in all respects except their capital structure cannot have different market

values or cost of capital because of arbitrage process. In case two identical firms except for their

capital structure have different market values or cost of capital arbitrage will take place and the

investors will engage in ‘personal leverage’ (i.e. they will buy equity of the other company in

preference to the company having lesser value) as against the corporate leverage’: and this will

again render the two firms to have the same total value.

The M&M approach is based upon the following assumptions:

(i) There are no corporate taxes.

(ii) There is a perfect market.

(iii) Investors act rationally.

(iv) The expected earnings of all the firms have identical risk characteristics.

(v) The cut-off point of investment in a firm is capitalization rate.

(vi) Risk to investors depends upon the random fluctuations of expected earnings and

the possibility that the actual value of the variables may turn out to be different

from best estimates.

(vii) All earnings are distributed to the shareholders.

(b) When the corporate taxes are assumed to exist: Modigliani and Miller, in their

article of 1963 have recognized that the value of the firm will increase or the cost of capital will

decrease with the use of debt on account of deductibility of interest charges for tax purpose.

Thus, the optimum capital structure can be achieved by maximizing the debt mix in the equity of

a firm.

According to the M&M approach, the value of a firm unlevered can be calculated as.

Value of unlevered firm (Vu)

= Earnings before interest and tax/Overall cost of capital

= EBIT/ko (1 – t)

and, the value of a levered firms is:

VL=Vu+tD

32

where, Vu is value of unlevered firm

and, tD is the discounted present value of the tax savings resulting from the tax deductibility of

the interest charges, t is the rate of tax and D the quantum of debt used in the mix.

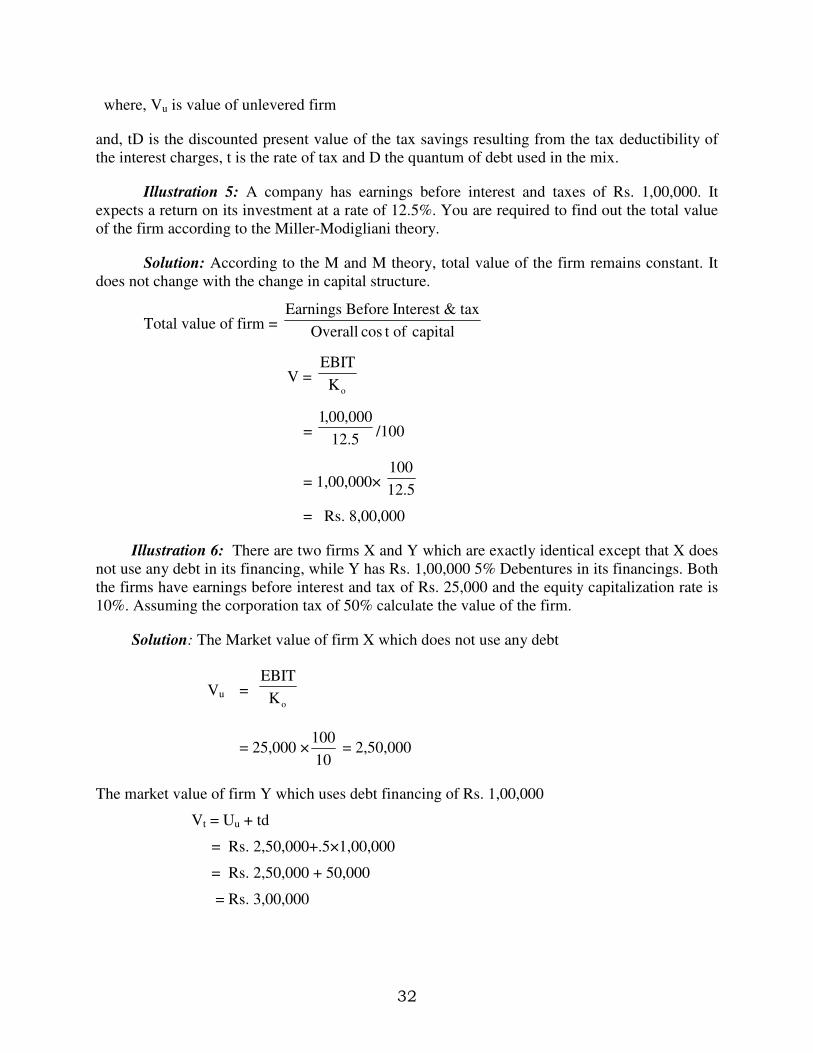

Illustration 5: A company has earnings before interest and taxes of Rs. 1,00,000. It

expects a return on its investment at a rate of 12.5%. You are required to find out the total value

of the firm according to the Miller-Modigliani theory.

Solution: According to the M and M theory, total value of the firm remains constant. It

does not change with the change in capital structure.

Total value of firm = capitaloftcosOverall

tax&InterestBeforeEarnings

V =oK

EBIT

= 5.12

000,00,1/100

= 1,00,000× 5.12

100

= Rs. 8,00,000

Illustration 6: There are two firms X and Y which are exactly identical except that X does

not use any debt in its financing, while Y has Rs. 1,00,000 5% Debentures in its financings. Both

the firms have earnings before interest and tax of Rs. 25,000 and the equity capitalization rate is

10%. Assuming the corporation tax of 50% calculate the value of the firm.

Solution: The Market value of firm X which does not use any debt

Vu = oK

EBIT

= 25,000 ×10

100 = 2,50,000

The market value of firm Y which uses debt financing of Rs. 1,00,000

Vt = Uu + td

= Rs. 2,50,000+.5×1,00,000

= Rs. 2,50,000 + 50,000

= Rs. 3,00,000

33

How does the Arbitrage Process Work?

We have noticed in illustration that the market value of firm Y, which uses debt content

in its capital structure, is higher than the market value of firm X which does not use debt content

in its capital structure. According to M & M theory, this situation cannot remain for a long

period because of the arbitrage process. As the investors in company Y can earn a higher rate of

return on their investment with lower financial risk, they will sell their holding of shares in

company X and invest the same in company Y. Further, as company Y does not use any debt in

its capital structure the financial risk to the investors will be less, thus, they will engage in

personal leverage by borrowing additional funds equivalent to their proportionate share in firm

X’s debt at the same rate of interest and invest the borrowed funds also in company Y. The

arbitrage process will continue till the prices of shares of company X fall and that of company Y

rise so as to make the market value of the two funds identical However, in the arbitrage process,

such investors who switch their holdings will gain. Illustration, given below, illustrates the

working of arbitrage process.

Illustration 7: The following is the data regarding two companies ‘A’ and ‘B’ belonging to the

same equivalent risk class:

Company A Company B

Number of ordinary shares 1,00,000 1,50,000

8% Debentures 50,000 _

Market Price per share Rs. 1.30 Rs. 1.00

Profit before interest Rs. 20,000 Rs. 20,000

All profits after paying debenture interest are distributed as dividends. You are required to

explain how under Modigliani and Miller approach, an investor holding 10% of shares in

company ‘A’ will be better off in switching his holding to company ‘B’

Solution: In the opinion of Modigliani & Miller, two identical firms in all respects except their

capital structure cannot have different market values because of arbitrage process. In case two

identical firms except for their capital structure have different market values, arbitrage will take

place and the investors will engage in ‘personal leverage’ as against the corporate leverage. In

the given problem, the arbitrage will work out as below:

1. The investor will sell in the market 10% of shares in company ‘A’ for Rs. 13,000

(100

10×1,00,000×1.30)

2. He will raise a loan of Rs. 5000 (100

10×50,000) to take advantage of personal leverage

as against the corporate leverage as company ‘B’ does not use debt content in its

capital structure.

3. He will buy 18,000 shares in company ‘B’ with the total amount realised from 1 and

2, i.e., Rs. 13,00 plus Rs. 5000, Thus he will have 12% of shares in company ‘B’.

34

The investor will gain by switching his holding as below:

Present income of the investor in company ‘A’:

Profit before interest of the company = Rs. 20,000

Less Interest on debentures (8%) = Rs. 4,000

Profit after Interest 16,000

Share of the investor = 10% of Rs. 16,000 i.e. Rs. 1600

Income of the investor after switching holding to company ‘B’

Profit before interest for company ‘B’ = Rs. 20,000

Less Interest = Nil

Profit after interest 20,000

Share of the investor = 20,000 × 000,50,1

000,18 = Rs. 2400

Less: Interest paid on loan taken 8% of Rs. 5000 = 400

Net Income of the investor 2000

As the net income of the investor in company ‘B’ is higher than the loss of income from

company ‘A’ due to switching the holding, the investor will gain in switching his holding to

company ‘B’.

35

4

CAPITAL STRUCTURE: PLANNING AND DESIGNING

Smriti Chawla

Shri Ram College of Commerce University of Delhi

Capital Structure Management or Planning The Capital Structure

Estimation of capital requirements for current and future needs is important for a firm.

Equally important is the determining of capital mix. Equity and debt are the two principle

sources of finance of a business. But, what should be the proportion between debt and equity in

the capital structure of a firm now much financial leverage should a firm employ? This is a very

difficult question. To answer this question, the relationship between the financial leverage and

the value of the firm or cost of capital has to be studied. Capital structure planning, which aims at

the maximisation of profits and the wealth of the shareholders, ensures the maximum value of a

firm or the minimum cost of the shareholders. It is very important for the financial manager to

determine the proper mix of debt and equity for his firm. In principle every firm aims at

achieving the optimal capital structure but in practice it is very difficult to design the optimal

capital structure. The management of a firm should try to reach as near as possible of the

optimum point of debt and equity mix.

Essential Features of a Sound Capital Mix

A sound or an appropriate capital structure should have the following essential features:

(i) Maximum possible use of leverage.

CHAPTER OBJECTIVES

� Capital Structure Management or planning the Capital Structure

� Essential features of sound capital mix

� Factors determining capital structure � Profitability and Capital Structure: EBIT

– EPS Analysis � Liquidity and Capital Structure: Cash

Flow Analysis

� Illustrations � Lets Sum Up

� Questions

36

(ii) The capital structure should be flexible.

(iii) To avoid undue financial/business risk with the increase of debt.

(iv) The use of debt should be within the capacity of a firm. The firm should be in a

position to meet its obligation in paying the loan and interest charges as and when

due.

(v) It should involve minimum possible risk of loss of control.

(vi) It must avoid undue restrictions in agreement of debt.

(vii) The capital structure should be conservative. It should be composed of high grade

securities and debt capacity of the company should never be exceeded.

(viii) The capital structure should be simple in the sense that can be easily managed and

also easily understood by the investors.

(ix) The debt should be used to the extent that it does not threaten the solvency of the

firm.

Factors Determining the Capital Structure

The capital structure of a concern depends upon a large number of factors such as

leverage or trading on equity, growth of the company, nature and size of business, the idea of

retaining control, flexibility of capital structure, requirements of investors costs of floatation of

new securities, timing of issue, corporate tax rate and the legal requirements. It is not possible to

rank them because all such factors are of different importance and the influence of individual

factors of a firm changes over a period of time. Every time the funds are needed. The financial

manager has to advantageous capital structure. The factors influencing the capital structure are

discussed as follows:

1. Financial leverage of Trading on Equity: The use of long term fixed interest bearing

debt and preference share capital along with equity share capital is called financial

leverage or trading on equity. The use of long-term debt increases, magnifies the earnings

per share if the firm yields a return higher than the cost of debt. The earnings per share

also increase with the use of preference share capital but due to the fact that interest is

allowed to be deducted while computing tax, the leverage impact of debt is much more.

However, leverage can operate adversely also if the rate of interest on long-term loan is

more than the expected rate of earnings of the firm. Therefore, it needs caution to plan the

capital structure of a firm.

2. Growth and stability of sales: The capital structure of a firm is highly influenced by the

growth and stability of its sale. If the sales of a firm are expected to remain fairly stable,

it can raise a higher level of debt. Stability of sales ensures that the firm will not face any

difficulty in meeting its fixed commitments of interest repayments of debt. Similarly, the

rate of the growth in sales also affects the capital structure decision. Usually greater the

rate of growth of sales, greater can be the use of debt in the financing of firm. On the

37

other hand, if the sales of a firm are highly fluctuating or declining, it should not employ,

as far as possible, debt financing in its capital structure.

3. Cost of Capital. Every rupee invested in a firm has a cost. Cost of capital refers to the

minimum return expected by its suppliers. The capital structure should provide for the

minimum cost of capital. The main sources of finance for a firm are equity, preference

share capital and debt capital. The return expected by the suppliers of capital depends

upon the risk they have to undertake. Usually, debt is a cheaper source of finance

compared to preference and equity capital due to (i) fixed rate of interest on

debt: (ii) legal obligation to pay interest: (iii) repayment of loan and priority in payment

at the time of winding up of the company. On the other hand, the rate of dividend is not

fixed on equity capital. It is not a legal obligation to pay dividend and the equity

shareholders undertake the highest risk and they cannot be paid back except at the

winding up of the company and that too after paying all other obligations. Preference

capital is also cheaper than equity because of lesser risk involved and a fixed rate of

dividend payable to preference shareholders. But debt is still a cheaper source of finance

than even preference capital because of tax advantage due to deductibility of interest.

While formulating a capital structure, an effort must be made to minimize the overall cost