grain & biofuel markets in 2015 matthew c. roberts [email protected]

TRANSCRIPT

www.matthewcroberts.com 2

Chinese Meat Consumption 90-13

3

19901992

19941996

19982000

20022004

20062008

20102012

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Beef and Veal Swine Broiler

Thou

sand

Met

ric

Tonn

es

Chinese Oilseed Consumption Growing by 9.8%/yr since 1990

www.matthewcroberts.com 4

1990/1991

1991/1992

1992/1993

1993/1994

1994/1995

1995/1996

1996/1997

1997/1998

1998/1999

1999/2000

2000/2001

2001/2002

2002/2003

2003/2004

2004/2005

2005/2006

2006/2007

2007/2008

2008/2009

2009/2010

2010/2011

2011/2012

2012/2013

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

Sunflowerseed Peanut Rapeseed Cottonseed Soybean

Thou

sand

Met

ric

Tonn

es

Chinese Grain Consumption Climbing by 4%/year since 2006.

www.matthewcroberts.com 51990/1

991

1991/1992

1992/1993

1993/1994

1994/1995

1995/1996

1996/1997

1997/1998

1998/1999

1999/2000

2000/2001

2001/2002

2002/2003

2003/2004

2004/2005

2005/2006

2006/2007

2007/2008

2008/2009

2009/2010

2010/2011

2011/2012

2012/2013

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000Barley Millet Rice, Milled Sorghum Wheat Corn

Global food demand growth is still explosive

• Biofuel growth has stopped in the US.– Largely true globally, too.

• Not just meal, but oil• Global instability:

– Hurts economic growth, hurts food demand

www.matthewcroberts.com 6

Oil Prices Continue to Fall

www.matthewcroberts.com 7

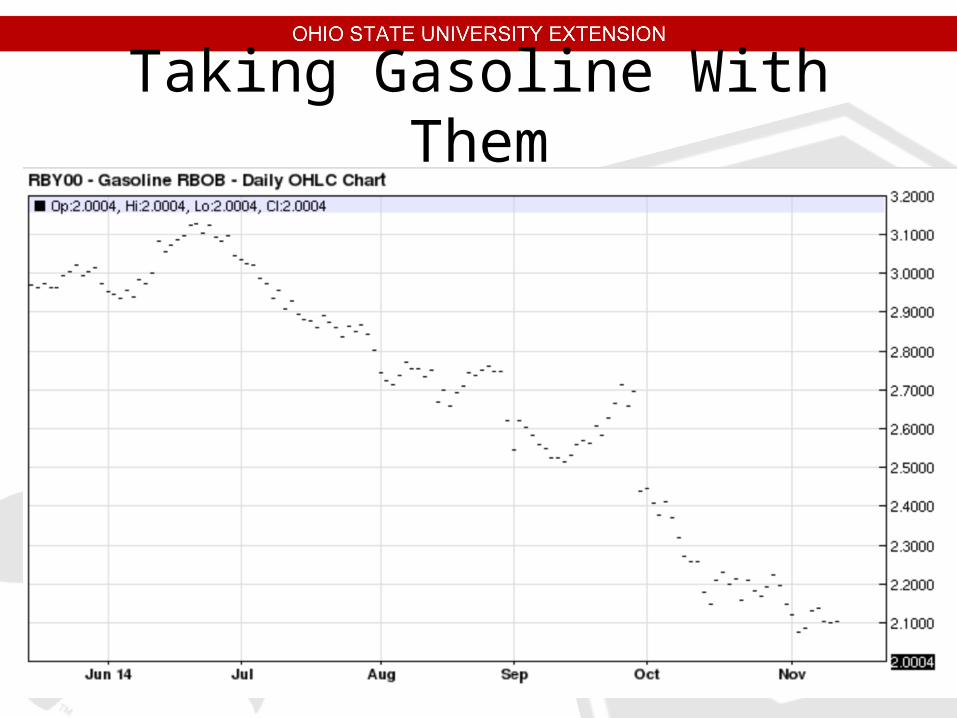

Taking Gasoline With Them

www.matthewcroberts.com 8

www.matthewcroberts.com 9

www.matthewcroberts.com 10

The Long Term Price of Oil

• Demand growth is slowing– Europe– China – US Power Generation

• Supply is increasing– Libya– United States

• Increases in US Production are already slowing

www.matthewcroberts.com 11

Energy Independence and Security Act of 2007Renewable Fuels Standards

Calendar Year

Total Convent’l Biofuel

(min 20% GHG reduc after 2010)

Advanced Biofuel

(min 50% GHG reduction)

Cellulosic Biofuel

(min 60% GHG reduction)

Biobased Diesel

2008 9.00 9.00 - - -

2009 11.10 10.50 0.60 - 0.50

2010 12.95 12.00 0.95 0.10 0.65

2011 13.95 12.60 1.35 0.25 0.80

2012 15.20 13.20 2.00 0.50 1.00

2013 16.55 13.80 2.75 1.00 1.28

2014 18.15 14.40 3.75 1.75 1.28

2015 20.50 15.00 5.50 3.00 1.28

12

0.006

0.0172.2015.21 13.00

0.003

0.001

0.001

How Fast Will Feed Use Recover?

71 74 77 80 83 86 89 92 95 98 '01 '04 '07 '10 '133000

4000

5000

6000

7000

8000Million Bushels

Year

5537

6150

3876 3941

55635375

63506646

Corn Exports Extremely Strong in 13/14, especially given price & competition

70

75

80

85

90

1992

1993

1994

951996

971998

99

'00

'01

'02

'03

'04

'05

'06

'07

'08

'09

'10

'11

'12

'13

'14

0

500

1000

1500

2000

2500

3000 Chart Title

Mil

lion

Bu

shel

s

2420

1220 1328

2350

700

Year

510

2436

1750

Global Corn Exports

17

2000/2001

2001/2002

2002/2003

2003/2004

2004/2005

2005/2006

2006/2007

2007/2008

2008/2009

2009/2010

2010/2011

2011/2012

2012/2013

2013/2014

0

10

20

30

40

50

60

70

Argentina Brazil China

European Union Ukraine United States

Mill

ion

Met

ric T

onne

s

Domestic Production Record Means Much Higher Corn Inventories

0

10

20

30

40

50

60

70

80

90

100

0

2

4

6

8

10

12

14

Year

Percent

Bil

lio

n B

ush

els

Production 14.4

Use 13.66

Stocks-to-Use Ratio (%)

2014: Record Yields

www.matthewcroberts.com 19

19601964

19681972

19761980

19841988

19921996

20002004

20082012

020406080

100120140160180200

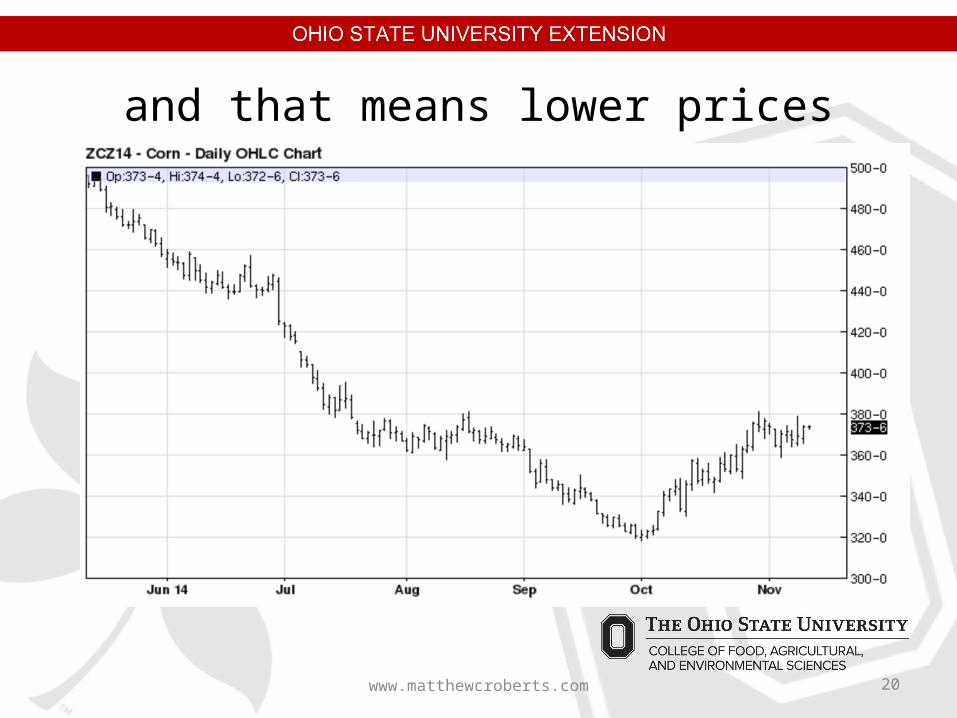

and that means lower prices

www.matthewcroberts.com 20

Old Crop:

• Lows should be in. Seems that pessimism has started to leave the market.

• Still large harvest & large carries.• Booking now for remainder of year

probably good bet.• Few big downside risks, exports a real

upside risk

www.matthewcroberts.com 21

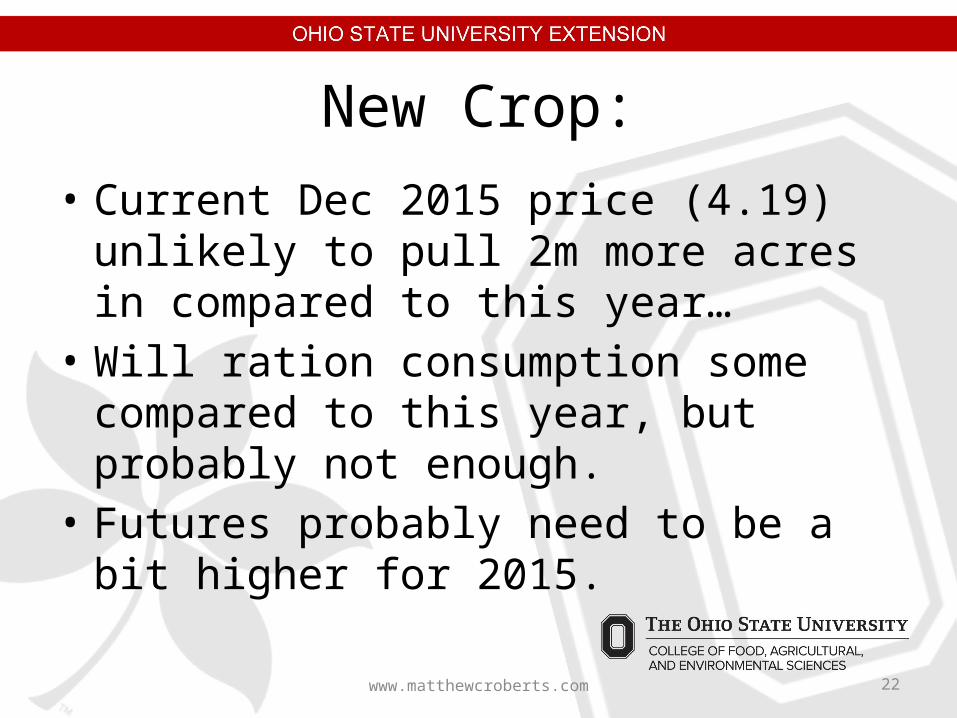

New Crop:

• Current Dec 2015 price (4.19) unlikely to pull 2m more acres in compared to this year…

• Will ration consumption some compared to this year, but probably not enough.

• Futures probably need to be a bit higher for 2015.

www.matthewcroberts.com 22

Soybeans: Domestic Demand Flat

1970

71

72

73

74

1975

76

77

78

79

1980

81

82

83

84

1985

86

87

88

89

1990

91

92

93

94

1995

96

97

98

99

'00

'01

'02

'03

'04

'05

'06

'07

'08

'09

'10

'11

'12

'13

'14

0

500

1,000

1,500

2,000

2,500 Chart Title

Year

Mill

ion

Bu

she

ls 1895

1956

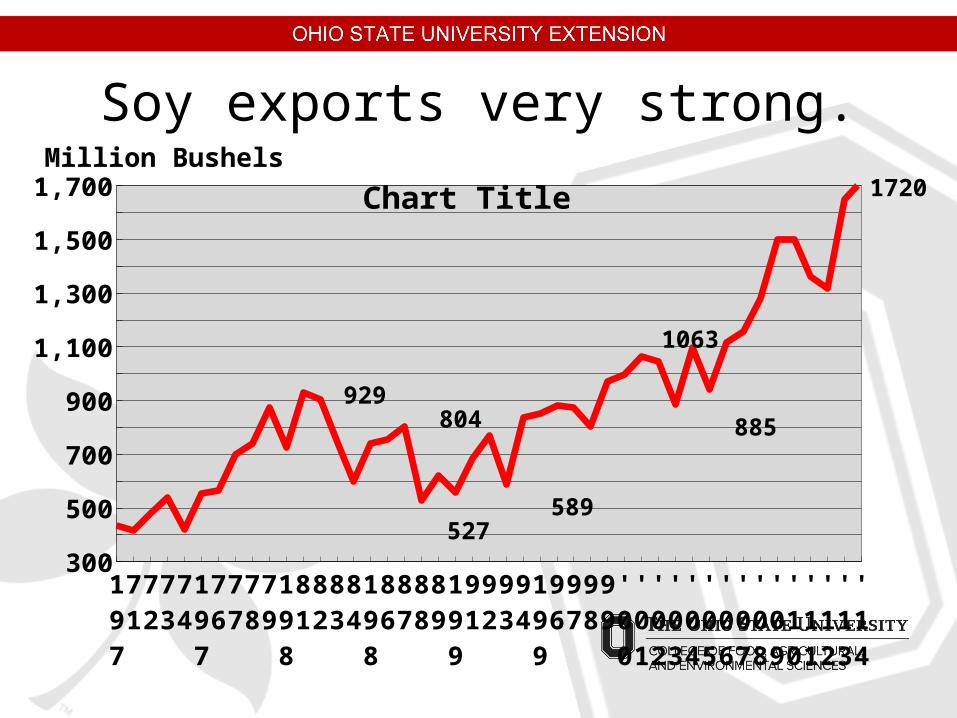

Soy exports very strong.

1970

71

72

73

74

1975

76

77

78

79

1980

81

82

83

84

1985

86

87

88

89

1990

91

92

93

94

1995

96

97

98

99

'00

'01

'02

'03

'04

'05

'06

'07

'08

'09

'10

'11

'12

'13

'14

300

500

700

900

1,100

1,300

1,500

1,700 Chart TitleMillion Bushels

929804 885

589527

1063

1720

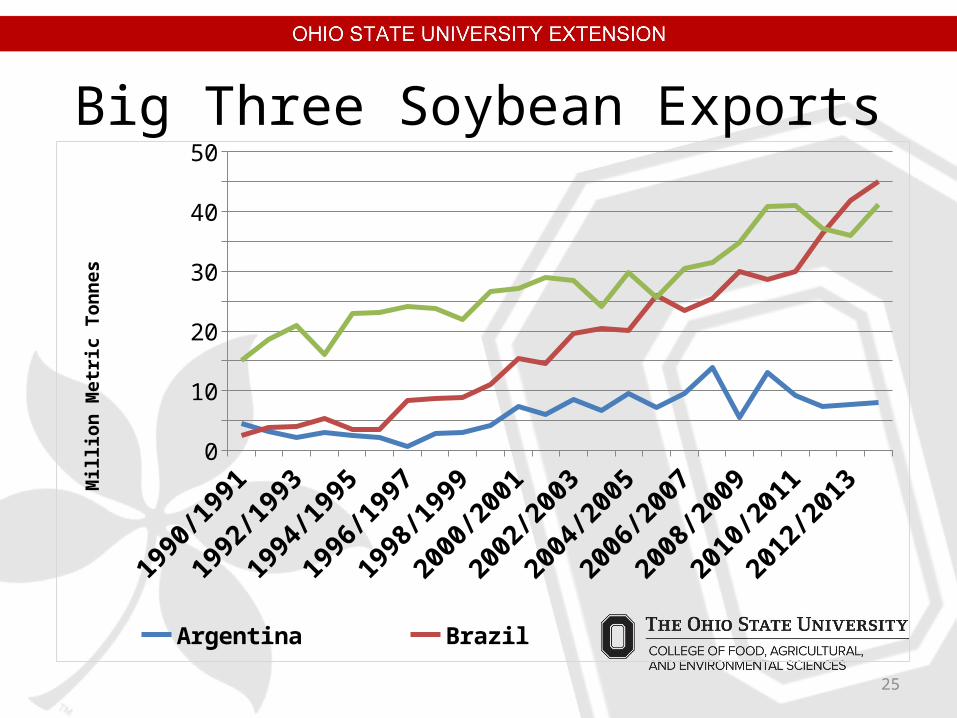

Big Three Soybean Exports

25

1990/1991

1992/1993

1994/1995

1996/1997

1998/1999

2000/2001

2002/2003

2004/2005

2006/2007

2008/2009

2010/2011

2012/2013

05

101520253035404550

Argentina Brazil United States

Mill

ion

Met

ric

Tonn

es

Bean Inventories Jump

85 87 89 91 93 95 97 99 '01 '03 '05 '07 '09 '11 '130

102030405060708090

100

1

1.5

2

2.5

3

3.5

28.0

21.0

15.0

11.0

13.0 18

.013

.613

.410

.714

.07.

85.

4 7.6 13

.410

.78.

87.

16.

44.

4 8.6 15

.618

.66.

74.

54.

5 6.6

5.4

4.5

2.6

12.4

Year

Per

cen

t

Bn

Bu

sh

els

Production 3.96

Use 3.61

Stocks-to-Use Ratio (%)

Global Soybean Production 600m bu Higher in ‘13/14

0

10

20

30

40

50

60

70

50

100

150

200

250

300

19

25

19191820191717

1418

139

15161718172120

232528

2319

2527

232327

Year

Percent

Production 287

Use 271

Million Metric Tons

Stocks-to-Use Ratio (%)

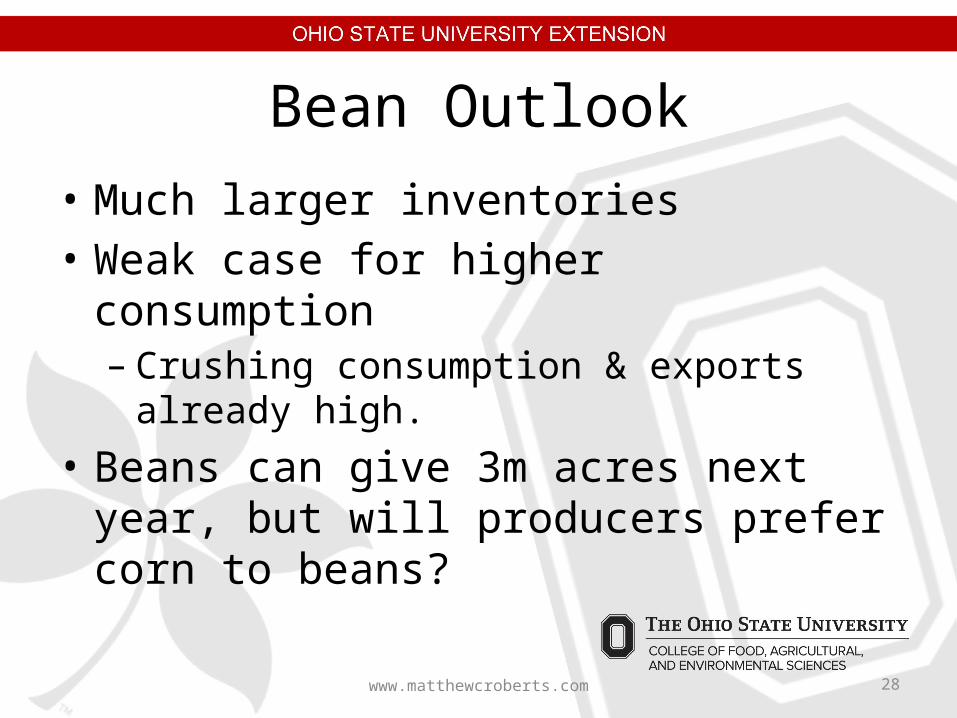

Bean Outlook

• Much larger inventories• Weak case for higher consumption

– Crushing consumption & exports already high.

• Beans can give 3m acres next year, but will producers prefer corn to beans?

www.matthewcroberts.com 28

www.matthewcroberts.com 29

Matt Roberts(614) 688-8686

[email protected]://aede.osu.edu/people/roberts.628

Twitter: @YourEconProf

Questions?