grap compliance: preparing for your 2014/15 audit mariëtte muller bcom hons, cta, professional...

TRANSCRIPT

GRAP Compliance: Preparing for your 2014/15

audit

Mariëtte Muller

BCom Hons, CTA, Professional Accountant (SA), GTP(SA), CET, PCT

Senior Manager - Altimax

IMFO Seminar

Today’s presentation

• GRAP standards effective 2014/15 year• GRAP standards effective 2015/16 year• What will you do differently on GRAP this year?• Who is Altimax?

2

GRAP standards effective 2014/15

3

New GRAPs

Amendments to Standards effective 1 April 2014:

• GRAP 5 – Borrowing Costs• GRAP 100 – Discontinued Operations

4

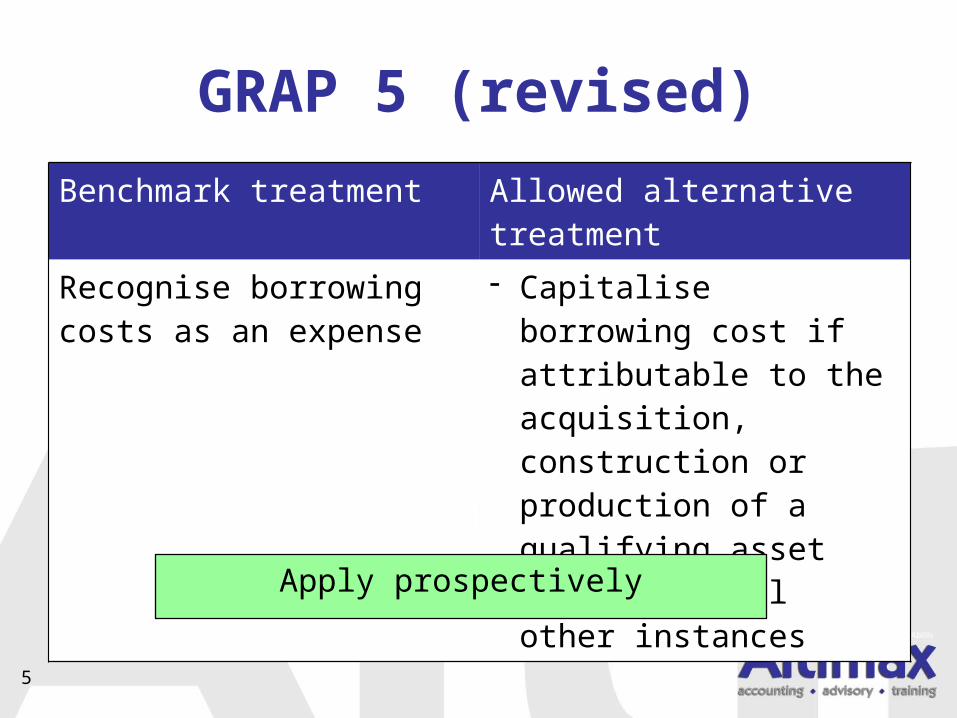

GRAP 5 (revised)

Benchmark treatment Allowed alternative treatment

Recognise borrowing costs as an expense

- Capitalise borrowing cost if attributable to the acquisition, construction or production of a qualifying asset

- Expense in all other instances

5

Apply prospectively

GRAP 100 (revised)• GRAP 100 now only deals with discontinued operations• Will no longer be required to reclassify assets as

held for sale• Certain disclosure must be made if, at the reporting date,

management has taken a decision to dispose of a significant asset or a group of assets and liabilities

• These disclosures will be included in GRAP 1

6

Apply measurement requirements prospectively and presentation and

disclosure requirements retrospectively

New GRAPsStandards that may be used in developing an accounting policy in 2014/15:

• GRAP 32 – Service Concession Arrangements: Grantor• GRAP 108 – Statutory Receivables• IGRAP 17 – Service Concession Arrangements: Grantor

Controls Significant Residual Interest• GRAP 105 – Transfers of Functions Between Entities

Under Common Control• GRAP 106 – Transfers of Functions Between Entities Not

Under Common Control • GRAP 107 – Mergers • GRAP 20 – Related Party Disclosures

7

GRAP 32 - Service Concession Arrangements:

Grantor• Applies to a contractual arrangement between grantor

and operator

• Operator uses service concession asset to provide a mandated function on behalf of the grantor for a specified period of time

• Operator can be either a private party or another public sector entity

8

GRAP 32

Link to PPP (public-private-partnership) agreements:

• Under PPP agreements, the definition thereof refers to “private party” and “entity"

• GRAP 32 uses the terms “operator” and “grantor”, but these include other public entities as well

• Therefore not limited to private entities as under PPP agreements

9

GRAP 32

• PPP agreements fall under the PFMA and MFMA• There is also a guideline on accounting for PPP agreements

issued by the ASB• PPP agreements governed and regulated i.t.o. the PFMA and

MFMA, are some of the arrangements that fall within the scope of GRAP 32

• Any other arrangements that meet the control criteria in paragraph .07 of GRAP 32 should also apply the principles in the standard

10

GRAP 32

Recognise asset if:

• Grantor controls or regulates:– what services the operator must provide with the asset– to whom it must provide the services– at what price

• Grantor controls—through ownership, beneficial entitlement or otherwise—any significant residual interest in the asset at the end of the term of the arrangement

11

GRAP 32

• If one or both of these criteria are not met, consider principles in IGRAP 3 - Determining whether an arrangement contains a lease

• If not a lease, consider the principles in the Framework

12

GRAP 32

• Recognise corresponding liability as follows:

13

Financial liability model Grant of right to operator model

- Unconditional obligation to pay cash or another financial asset

- To operator for the construction, development, acquisition, or upgrade of a service concession asset

- Recognise as financial liability under GRAP 104

- No unconditional obligation to pay cash or another financial asset

- To operator for the construction, development, acquisition, or upgrade of a service concession asset

- Grants the operator right to earn revenue from third party users

- Recognise as unearned portion of revenue arising from exchange of assets

GRAP 32

Proposed transitional provisions:

• The new standard is based on IFRIC 12 and the Guideline on Accounting of PPPs issued by ASB

• Consequently proposing no “special” transitional provisions

• Apply retrospectively

14

GRAP 108 - Statutory Receivables

• Dealing with receivables arising from legislation or similar means, which require settlement in cash or another financial asset

• To be statutory in nature, specific legislation should require the entity to undertake the transactions, such as outlining who should be taxed and at what rates and amounts

15

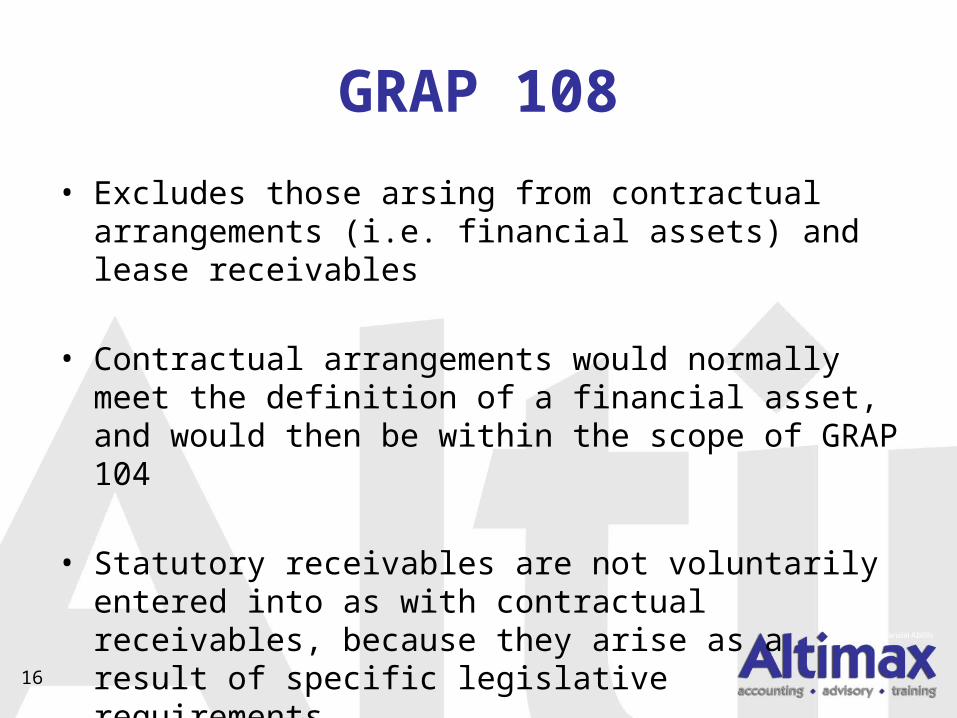

GRAP 108

• Excludes those arsing from contractual arrangements (i.e. financial assets) and lease receivables

• Contractual arrangements would normally meet the definition of a financial asset, and would then be within the scope of GRAP 104

• Statutory receivables are not voluntarily entered into as with contractual receivables, because they arise as a result of specific legislative requirements

16

GRAP 108

• Examples of revenue types for which the receivable will be statutory in nature and therefore accounted for under GRAP 108:

– taxes, including property rates– fines– penalties– appropriations and grants– fees charged in terms of legislation

17

GRAP 108

18

Transaction is exchange transaction

Transaction is non-exchange transaction

None of the previous mentioned

Apply GRAP 9 Apply GRAP 23 Only recognise the receivable when:- Definition of asset is

met- It is probable that the

future economic benefits or service potential associated with the asset will flow to the entity and the transaction amount can be measured reliably

GRAP 108

• Recognised at transaction amount• After initial recognition measured using the cost method• Cost method - only change initial measurement of

receivables for:– Interest and other charges– Impairment losses– Amounts derecognised

19

GRAP 108

Impairment

• Carrying amount less estimated future cash flows (not present value of estimated future cash flows as is the case in GRAP 104)

• Will only need to calculate the present value of future cash flows– Effect of time value of money is material

20

GRAP 108

Proposed transitional provisions:

• Apply retrospectively, except for:– Derecognition – Impairment

• Three year transitional period with regards to classification and measurement of statutory receivables (SR)

21

GRAP 108

Proposed transitional provisions:

• Disclosure follows complying with classification and measurement requirements

• May continue to apply previous accounting policies for classifying and measuring SR that don’t comply with GRAP 108 as yet

22

GRAP standards effective 2015/16

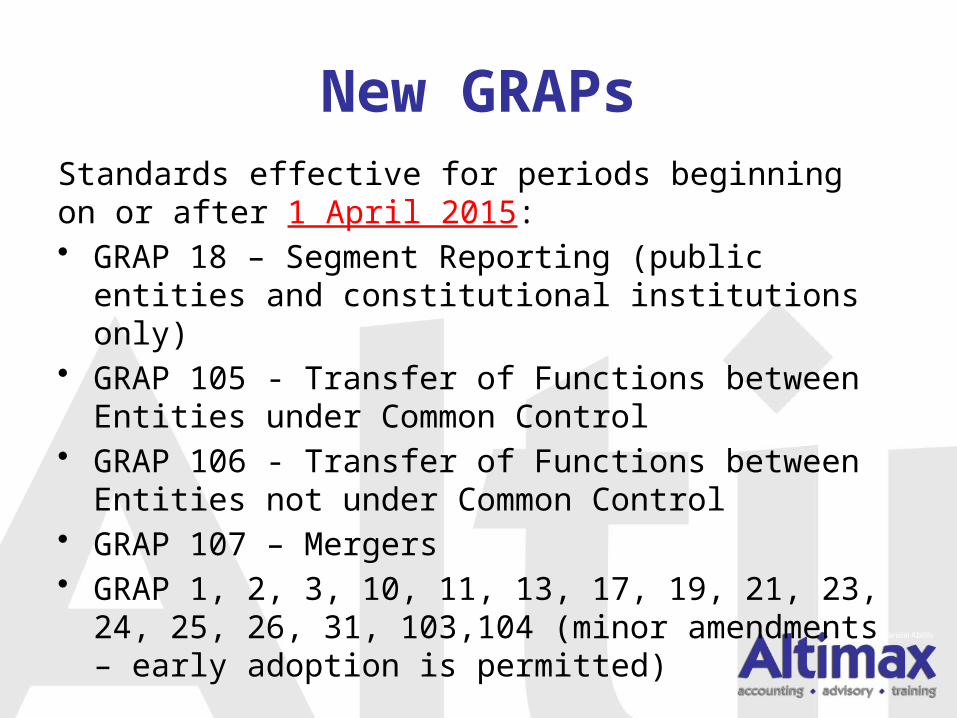

23

New GRAPsStandards effective for periods beginning on or after 1 April 2015:• GRAP 18 – Segment Reporting (public entities and

constitutional institutions only)• GRAP 105 - Transfer of Functions between Entities

under Common Control• GRAP 106 - Transfer of Functions between Entities not

under Common Control• GRAP 107 – Mergers• GRAP 1, 2, 3, 10, 11, 13, 17, 19, 21, 23, 24, 25, 26, 31,

103,104 (minor amendments – early adoption is permitted)

New GRAPs…

New directive effective 1 April 2015:• Directive 11 - Changes in the Measurement Bases

Following the Initial Adoption of the Standards of GRAP (early adoption is permitted)

Directive 11

• Currently in GRAP 3 - change in accounting policy from revaluation model or fair value model to cost model can only be made if:– Required by GRAP– Will result in AFS providing reliable and more relevant

information

• Difficult to prove the latter

26

Directive 11

• If inappropriate accounting policy choice was made on initial adoption of GRAP 16, 17, 31 or 103

• Is allowed to make a once-off change from revaluation model or fair value model to cost model

• Apply retrospectively and provide relevant disclosure

27

Directive 11

• Subsequently can only change accounting policy if it meets the requirements in GRAP 3

• Can only take advantage of the provisions in Directive within a period of three years following:– Expiry of transitional provisions applied on initial adoption

of GRAP, or– Effective date of the directive – 1 April 2015– Whichever is later

28

New GRAPsStandards that may be used in developing an accounting policy in 2015/16:

• GRAP 32 – Service Concession Arrangements: Grantor• GRAP 108 – Statutory Receivables• IGRAP 17 – Service Concession Arrangements: Grantor

Controls Significant Residual Interest

29

New GRAPsStandards that may be used for disclosure in financial statements for 2015/16:

• GRAP20 – Related Party Disclosures

30

What will you do differently on GRAP this year?

GRAP is a way of living not a way of doing

GRAP has nothing to do with Finance

31

What will you do differently on GRAP this year?...

You do not need a consultant to be GRAP compliant

You do not need a degree to be GRAP compliant

32

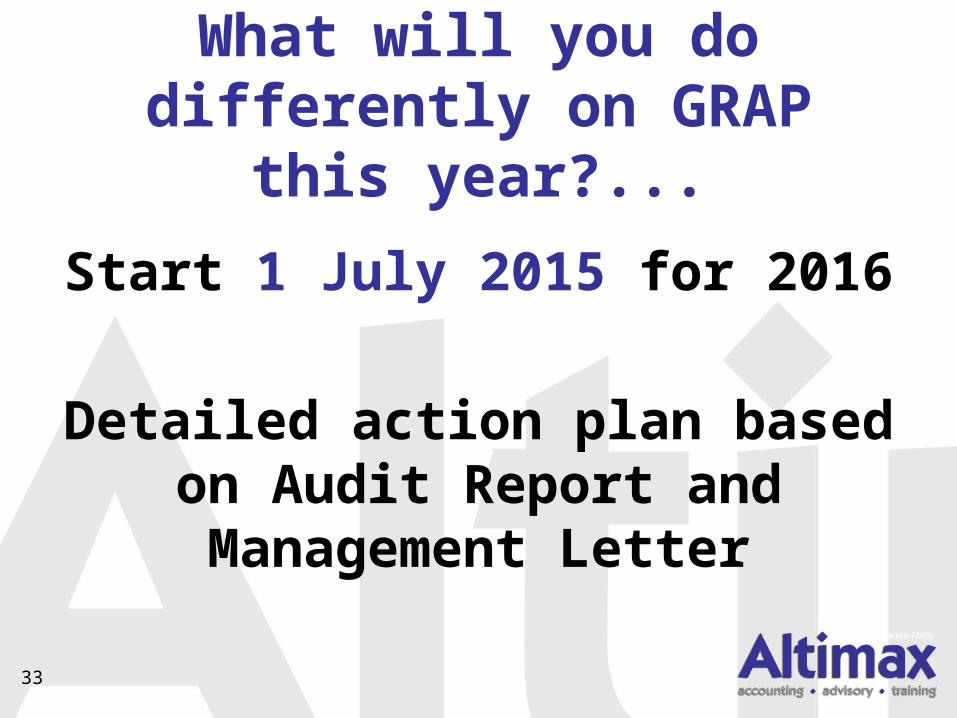

What will you do differently on GRAP this year?...

Start 1 July 2015 for 2016

Detailed action plan based on Audit Report and Management

Letter

33

Who is Altimax?

• Accounting - Advisory - Training• Level 1 B-BBEE• Operated for 11 years in public sector• > 110 public entities• > 110 municipalities• Involved in >10% of the municipalities with a

clean audit• Over the past number of years served on GRAP

panels for NT, KZN Treasury, NW Treasury

Who is Altimax?…

• GRAP training for Auditor General – 2006 to 2013

• GRAP manuals for NT– First 26 and New 8

• Provider of LGAC and LGAAC for SAICA• Provider of MFMP• Pre issuance for the Auditor General since

2006

What Altimax can do for you

Unqualified to Clean– Controls– HR– SCM– Compliance– Sustainability

What Altimax can do for you…

Training / skills development– Duration: ½ day to 5 day courses– Type: Short courses and FASSET or LG SETA accredited

courses– Topics: MFMP / Technical skills / Soft skills and leadership– Audience: Councillors / audit coms / management /

support staff– Where: On site or off site– When: Your choice

Skills Transfer

LEARN Principle 1

SHAREPrinciple 2

DO Principle 3

Skills Transfer…

Year 1 Year 2 Year 30%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Dependency on consultant

Skills of staff

The Altimax value proposition

• Values driving excellence• Peace of mind• Getting it right the 1st time• Client 1st approach• Strategic partnership

Contact details

• Tel: +27 (0) 12 940 0286• E-mail: [email protected] • Follow us on Facebook • Join us on LinkedIn