grid-connected spv rooftop systems - mpcz.co.in folders... · by 2017 roof top solar power cost...

TRANSCRIPT

Grid-connected SPV Rooftop systems

Dr. Arun K Tripathi Director,

Government of India

Ministry of New and Renewable Energy

MNRE

Grid-connected SPV Rooftop systems Concept…

These are SPV systems installed on rooftops

of residential, commercial or industrial

premises.

Electricity generated could be…

-fed into the grid at regulated feed-in tariffs or

-used for self consumption with net-metering

approach

MNRE

Grid-connected SPV Rooftop systems Concept…

MNRE

Grid-connected SPV Rooftop systems Advantages …..

Savings in transmission and distribution losses

Low gestation time

No requirement of additional land

Improvement of tail-end grid voltages and

reduction in system congestion with higher

self-consumption of solar electricity

Local employment generation

MNRE

Growth of Solar Capacity (MW)

3 11 36

936

1684

2101

2008-09 2009-10 2010-11 2011-12 2012-13 2013-14

So

lar

Ca

pcit

y (

MW

) State MWp % Gujarat 860.4 41.0%

Rajasthan 656.15 31.2%

Maharashtra 207.25 9.9%

Madhya

Pradesh 162.315

7.7%

Andhra

Pradesh 68.9

3.3%

Uttar

Pradesh 17.375

0.8%

Tamil Nadu 28.18 1.3%

Jharkhand 16 0.8%

Karnataka 24 1.1%

Orissa 15.5 0.7%

Punjab 9.325 0.4%

Haryana 7.8 0.4%

West Bengal 7.05 0.3%

A & N Island 5.1 0.2%

Uttarakhand 5.05 0.2%

Chhattisgarh 7 0.3%

Delhi 2.6 0.1%

Lakshadwee

p 0.8

0.0%

Roof top PV-Towards grid parity

Source:KPMG

By 2017 roof top solar power cost will reach the grid parity.

Benefits of Roof top PV

• On national level, reduces requirement of

land for addition of solar capacities.

• For consumers, it

– Reduces the dependency on grid power.

– Mitigates diesel generator dependency.

– Long term reliable power source.

• For Discoms, it reduces

– Day Peak load Demand

– T&D and conversion losses as power is consumed

at the point of generation.

• Most suitable for commercial establishments

– Max generation during peak usage time.

– Solar power cost is close to the commercial power

cost.

Roof top PV potential in INDIA • According to 2011 Census India is having

– 330 million houses.

– 166 million electrified houses.

– 76 million houses uses kerosene for lighting.

– 1.08 million houses are using solar for lighting.

– 140 million houses with proper roof (Concrete or

Asbestos / metal sheet).

– 130 million houses are having > 2 rooms.

• Average house can accommodate 1-3 kWp of

solar PV system.

• The large commercial roofs can accommodate

larger capacities.

• As a conservative estimate, about 25000 MW

capacity can be accommodated on roofs of

buildings having > 2 rooms alone if we

consider 20% roofs.

Grid-connected SPV Rooftop systems

World-wide Experience …..

Germany, USA and Japan are leaders in adopting grid-connected SPV Rooftop systems.

Germany has highest PV installed capacity of 36.0 GW of which 71% is in rooftop segment (as on 31.05 .2014).

Italy has 12.7 GW PV installation with over 60% rooftop systems

In Europe of total 50.6 GW PV installation, over 50% in in rooftop segment.

FIT is norm in Europe while net-metering is popular in USA.

MNRE

PV market segments in Germany

Image : Solarwatt

Private buildings:

1-10 kWp

Social, commercial,

agricultural buidlings:

10-100 kWp

Image : Solarwatt

Image: Sharp

Image : BP

Large commercial

buildings:

> 100 kWp

Image : Schüco

Image : Geosol Image:

Geosol

Image: Grammer

10% 38% 23%

Source: BSW-Solar, E.Quadrat GmbH

Gro

un

d-m

ou

nte

d R

oo

fto

p

Bu

ild

ing

in

teg

rate

d

<1%

71%

28% Market share in %

of MW installed in

2011

MNRE

Germany …1000 Roofs Programme 1991-1995

Only German producers (local contentCapital Grant of 70% of investment provided(50% by the federation and 20% by Federal States)

Grid connected PV installation with 1-5 kWp rooftops of single and two family houses were eligible

Every installation had to install 3 meters:

- Generation meter, metering at production

- Feed-in-Meter, metering at fed electricity

- Import Meter, metering the purchased electricity

Obligation for installation operators to record over 5 years monthly meter results

MNRE

Loan Programme through KfW

300 MW of newly installed capacity from PV

Loans at reduced rate of interest (soft loan)

Interest rate of 1.91%

Installations of min. 1kWp of individuals,

Freelansers or SMEs

Germany …100,000 Roofs Programme 1999-2003 MNRE

TOP 3 PV success factors in Germany

1. EEG – Feed-in law (20 year state guaranteed FIT , RE feed-in priority,

one simple national binding scheme)

Attractive business case for all kind of investors from house owner to international investment trusts created

2. Long term & stable legal framework

Non-recourse project financing enabled

3. Quality standards (establishment of high technical standards &

development of qualified technical resources e.g. EPCs / integrators)

Secure long term yields and system security

MNRE

Grid-connected SPV Rooftop systems World-wide Experience ….. USA

Net metering is popular in 43 States but specific

rules defer from States to States.

Energy Policy Act 2005 mandates all public

electricity utilities to make net metering options

available to all customers.

California had maximum installed onsite

customer generated solar capacity of 991 MWp

with 1,01,284 net metering consumers from

115000 sites.

MNRE

Net Metering mechanism

The Net Metering mechanism shall allow the consumer to reduce its electricity import

The utility benefits by avoiding purchase of electricity from short term market

Electricity generation at load center also minimises the loss of electricity in wires

Capacity for development under Net Metering Mechanism may be allowed in phases to take care of the following aspects.

• Equivalent to suitable percentage the utility propose under the intra state network losses or

• Capacity projected for purchase of Short Term market

• Financial viability

MNRE

Business Models for Net Metering – 1 Consumer end model

C1

C2

C3

Cn

DISCOM

Consumers are owners of the

facility

Challenges:

Limited know-how of installing and

operating

Limited know-how for requirements of

approvals and clearances

Administration cost of utility may increase

Utility needs to interact with consumers,

energy accounting on individual basis

MNRE

C1

C2

C3

Cn

DISCOM

Business Models for Net Metering – 2 Consumer end Community based model

Repre

senta

tive

Capacities may be bundled by a

facilitator/ representative who

undertakes necessary formalities and

may avail subsidy for consumers

Administration cost of utility less

compared to earlier model

Utility needs to interact with

facilitator/ representative of

consumers/owners

Energy accounting at community level

Sharing of benefits among consumers

may take place on the basis of their

contribution

MNRE

Business Models for Net Metering – 3 RESCO/3rd party model based on FIT

C1

C2

C3

Cn

3rd Party

RESCO/3rd party shall supply

electricity to the DISCOM at

determined FIT

DISCOM may also call for competitive

bidding for selection of RESCO/3rd

Party

RESCO makes investments for

installing facilities at consumers‟ roof

Consumers get suitable rent for

lending their roofs

3rd Party gets subsidy from the MNRE

Energy accounting takes place at

consumer end

Utility purchases solar electricity for

meeting RPO

DISCOM

MNRE

Emerging Market Models for Net Metering – 4 3rd Party model based on consumer tariff bidding

C1

C2

C3

Cn

3rd

Party

Selection of RESCO/3rd Party at

upper cap estimated by DISCOM

Consumer gets net energy metered at

its premise

Consumers get suitable rent for

using their roofs which shall reflect

in their electricity bills

3rd Party gets subsidy from MNRE

Streams of revenue include,

Sale of electricity to DISCOM

Sale of RECs

Tax Benefit, Accel. Depreciation

benefit etc.

DISCOM

Consumer tariff assumed

to be increasing

MNRE

Grid-connected SPV Rooftop systems Indian Experience: Initiatives by West Bengal

Grid connected rooftop is allowed only for

institutional consumers with 2-100 kW size

Connectivity is allowed at low or medium

voltage(6 kV or 11 kV) of distribution system

Solar injection is permitted only upto 90% of

annual electricity consumption.

Net energy supplied by the utility to be billed as

per existing slab tariffs.

Solar generation to offset consumption in the

highest tariff slab and then the lower slab.

MNRE

Grid-connected SPV Rooftop systems Indian Experience: Initiatives by West Bengal

As per recent policy All existing and upcoming commercial and business establishments having more than 1.5 MW contract demand to install SPV rooftop systems to meet at least 2% of their total electrical load

All existing and upcoming schools and colleges, hospitals, large housing societies, and and Govt. establishments having more than 0.5 MW contract demand to install SPV rooftop systems to meet at least 1.5% of their total electrical load.

Policy targets 16 MW of rooftop and small PV installations by 2017.

MNRE

Grid-connected SPV Rooftop systems Indian Experience: Initiatives by Gujarat

Gandhinagar city initiated a 5 MW(4 MW in Govt.

buildings and 1 MW in private homes) rooftop PV

programme based on FIT/sale to utility.

Two project developers for 2.5 MW each selected

through reverse bidding with GERC cap of rs.

12.44/kwh.

Torrent Power will buy from Azur @ Rs. 11.21/kWh for

25 years and Azure will pass on Rs. 3.0/kWh to

rooftop owner as roof rent.

Recently 5 more cities-Bhavnagar Mehsana, Rajkot,

Surat and Vadodara started installing pilot rooftop

projects.

MNRE

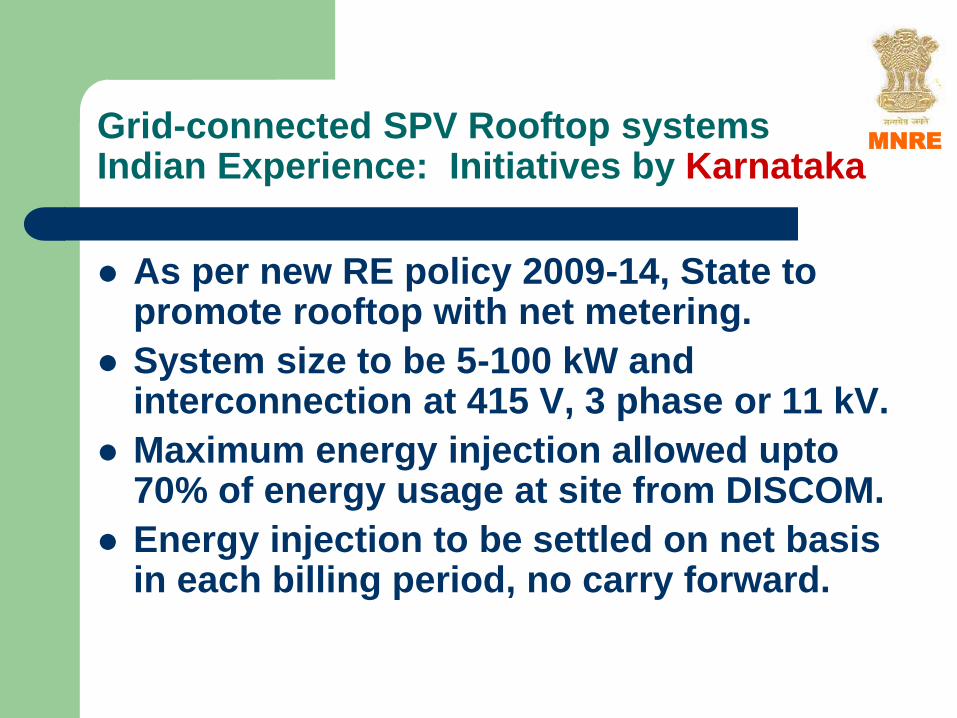

Grid-connected SPV Rooftop systems Indian Experience: Initiatives by Karnataka

As per new RE policy 2009-14, State to promote rooftop with net metering.

System size to be 5-100 kW and interconnection at 415 V, 3 phase or 11 kV.

Maximum energy injection allowed upto 70% of energy usage at site from DISCOM.

Energy injection to be settled on net basis in each billing period, no carry forward.

MNRE

Grid-connected SPV Rooftop systems Indian Experience: Initiatives by Karnataka

25000 PV rooftops of 5-10 kWp size with

net metering targeted during next 5 years

with 250 MW potential and 350 MU

generation.

Grid connected PV rooftop projects to be

given priority under Green Energy Fund.

Pilot projects may come up in Mysore and

Hubli-Dharwad solar cities.

MNRE

Grid-connected SPV Rooftop systems Indian Experience: Initiatives by Tamil Nadu

As per „State Solar Policy 2012‟ 350 MW

SPV rooftop targeted during 2012-2014.

50 MW rooftop to be supported through

GBI @ Rs. 2.0/kWh for the first 2 years,

Rs. 1.0/kWh for the next 2 and Rs.

0.50/kWh for other 2 years.

Net metering will be allowed at multiple

voltage level

MNRE

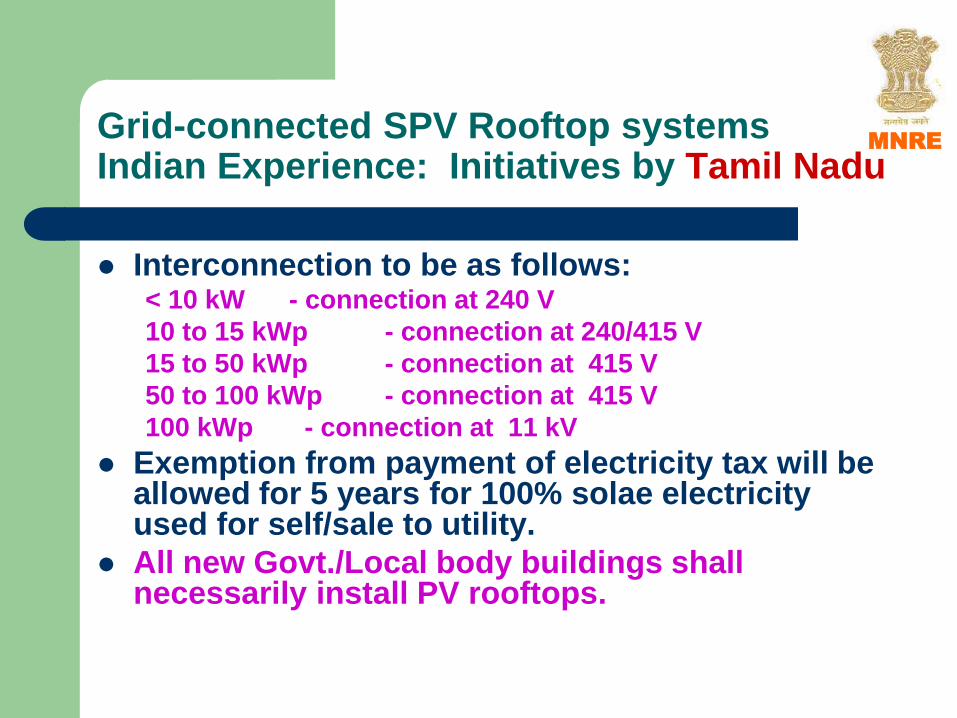

Grid-connected SPV Rooftop systems Indian Experience: Initiatives by Tamil Nadu

Interconnection to be as follows: < 10 kW - connection at 240 V

10 to 15 kWp - connection at 240/415 V

15 to 50 kWp - connection at 415 V

50 to 100 kWp - connection at 415 V

100 kWp - connection at 11 kV

Exemption from payment of electricity tax will be allowed for 5 years for 100% solae electricity used for self/sale to utility.

All new Govt./Local body buildings shall necessarily install PV rooftops.

MNRE

Grid-connected SPV Rooftop systems Indian Experience: Initiatives by Chandigarh

5.14 MW projects of SPV grid connected

PV rooftops projects sanctioned for

model solar city are under installation of

which 2.00 MW commissioned.

DISCOMS agreed to purchase power and

JERC has given rates for a project.

MNRE

Grid-connected SPV Rooftop systems Indian Experience: Initiatives by Chandigarh

Interconnection to be as follows:

-Upto 10 kW : Low voltage single phase

-10 kW to 100 kW :3 phase low voltage supply

-100 kW to 1.5 MW : Connection at 11 kV level

-1.5 MW to 5.o MW : Connection at 11 kV/33

kV/66kV as per site conditions

Petition filed with the JERC and the

finalization of rate in progress

MNRE

Grid-connected SPV Rooftop systems Indian Experience: Initiatives by Kerala

10,000 solar PV rooftops recently launched

with 1.0 kWp each system of total 10 MW

At present only off grid system covered but

Kerala has plans to launch 75,000 grid

connected rooftops soon.

Rs. 39,000/- state subsidy is available for

each 1.0 kWp system

Grid-connected SPV Rooftop systems Action being initiated …..

CEA has notified “Technical Standards for Connectivity of the Distibuted Generation Resources-CEA Regulations 2013” in October 2013 which permits the grid connectivity of SPV rooftop also.

CEA has submitted a draft “CEA (Installation and Operation of Meters- Regulation 2013” to M/o Power for approval for metering arrangement for inter connection of SPV rooftop with grid.

CERC has brought out the draft guidelines for grid connectivity and metering arrangements for SPV rooftops.

MNRE

Grid-connected SPV Rooftop systems Action being initiated …..

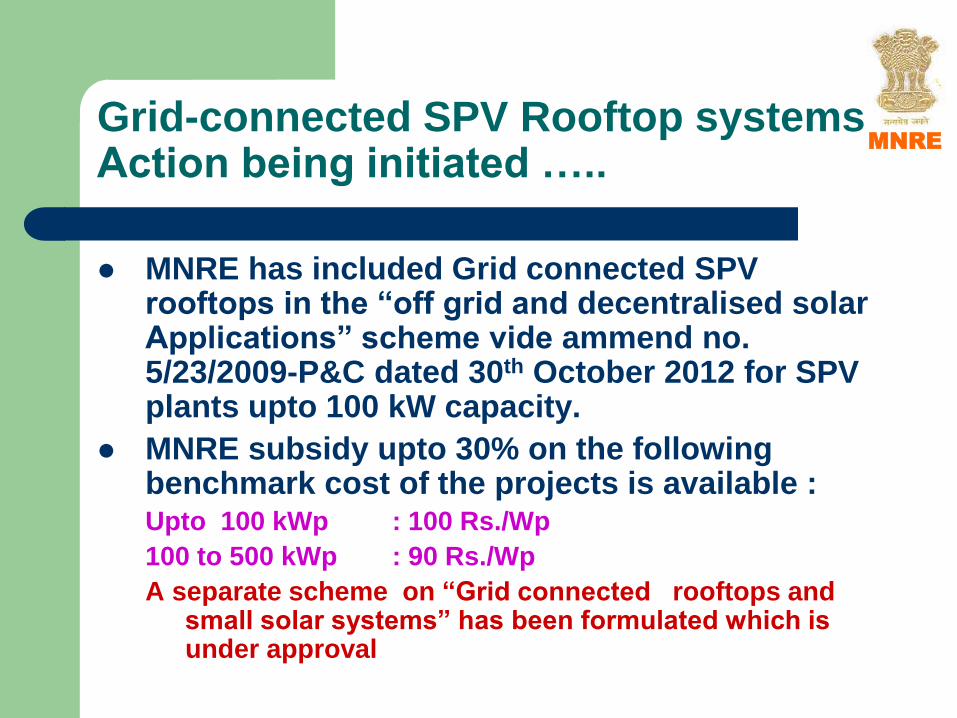

MNRE has included Grid connected SPV rooftops in the “off grid and decentralised solar Applications” scheme vide ammend no. 5/23/2009-P&C dated 30th October 2012 for SPV plants upto 100 kW capacity.

MNRE subsidy upto 30% on the following benchmark cost of the projects is available : Upto 100 kWp : 100 Rs./Wp

100 to 500 kWp : 90 Rs./Wp

A separate scheme on “Grid connected rooftops and small solar systems” has been formulated which is under approval

MNRE

Grid Connected Rooftop and Small Solar Power Plants Scheme of MNRE

• Objective of the scheme is to promote the grid connected SPV rooftop and small SPV power plants in the residential, community, institutional, industrial and commercial establishments.

• Project capacity of 1.0 kW to 500 kWp per project/system

• Implementation through programme (upto 50 kWp ) and project modes(above 50 kWp)

• Implementing agencies- SNAs, Solar Energy Corporation of India(SECI), Channel Partners, FIs/Financial Integrators, Other Govt. Departments/Agencies/PSUs etc.

• CFA is 30% of the benchmark for general and 70% CFA for NE and Special Category States for Govt. projects.

• 300 MW target for the 12th FY Plan

Grid-connected SPV Rooftop systems Action initiated …..

29.1 MWp SPV grid connected rooftop project sanctioned under NCEF funding are under execution by SECI (26.6 MWp) and Ministry of Railways(2.5 MWp).

50 MWp SPV grid connected rooftop project approved under NCEF funding sanctioned to SECI.

MNRE sanctioned 43.254 MWp projects to 10 States; AP,MP, Rajasthan, Punjab, Chandigarh, Kerala, Uttarakhand, Gujarat, Uttar Pradesh, Tamil Nadu.

4 MWp projects in Surat, Chandigarh and Nagpur Solar Cities are under execution of which 2 MWp projects in Chandigarh completed.

MNRE

Grid-connected SPV Rooftop systems Actions required by States…

Remaining States to announce suitable

policies on grid connected PV rooftop

systems

States to establish dialogue with

DISCOMs and finalize suitable tariff.

DISCOMs to formulate and sign PPAs,

States to set up few pilot projects.

MNRE

Key Considerations…….

Lack of public domain knowledge of technical standards

and guidelines for grid connectivity, metering, safety and

security

Energy accounting and commercial settlement

guidelines for grid connected solar rooftop projects still

evolving

Regulatory provisions relating to applicability of charges

relating to wheeling, open access, cross subsidy etc. for

solar rooftop projects needs to be clarified

Projects so far, implemented in India, have been either

under gross metering arrangement or on captive

consumption arrangements

Roof Space requirement for rooftop system

10-15 sq. meter roof space is required for

1.0 kW system

A 100 sq. meter roof space can have

8- 10 kW SPV system

Cost of 1.0 kW system is about

Rs. 1.00 lakh

30% CFA is available from MNRE

MNRE

Economics of Grid Connected Rooftop (100 kWp Rooftop Plant)

Capital Cost : Rs. 80 Lakh

Subsidy (30%) : Rs. 24 Lakh

Net Cost to Customer : Rs. 56 Lakh

Avg. Annual Generation : Rs.1,50,000 kWh

Annual Revenue(@Rs.7.0/kWh): Rs 10.5 lakh

Simple pay back : 5.33 years

Avg. elect. generation cost : Rs. 8.0/kWh (without Subsidy)

Avg. elect. generation cost : Rs. 5.60/kWh (with Subsidy)

Potential of SPV rooftop

One million industrial units and each

with average 500 sq. meter rooftop

space can have about 25,000 MWeq Solar

PV rooftop installations.

Only 800 Kendriya Vidyalayas in India can

host about 20 MW eq. Solar PV rooftops.

About 100 million houses can install 100

million 100,000 MW eq. Solar PV rooftops.

……and so on

MNRE

360 kWp Solar grid connected rooftop plants at Super Auto Forge, Chennai

Rooftop SPV system (50 kWp) at

Paryawaran Bhawan, Chandigarh

25 KWp SPV Plant at Police Hq, Chandigarh

70 KWp SPV Plant at Govt Multi Speciality Hospital , sec-16, Chandigarh

Thank You

MNRE

June 17, 2014

Bhopal

Design of Framework for Implementation of Rooftop Solar

Photovoltaic Projects

Project Partners

Presentation on proposed transaction framework in Bhopal, Jabalpur and Indore

© 2014. Deloitte Touche Tohmatsu India Private Limited.

Contents

• About the Project

• Proposed Transaction Framework

‒ Business Model

‒ Commercial

• Bid Process Management

• Key Timelines

• Salient Features

‒ RFP

‒ PPA, PIA

About the Project

© 2014. Deloitte Touche Tohmatsu India Private Limited.

About the Project

• Pilot Rooftop Solar Photovoltaic project of an aggregate capacity of 5 MW to be deployed in

the cities of Bhopal, Jabalpur and Indore

• Project to be deployed under gross metering mechanism wherein entire power procurement

to be done by MP Power Management Company Ltd. (MPPMCL)

• Project to receive support in the form of central financial assistance of upto Rs. 15 Cr (Rs. 3

Cr/MW) towards capital subsidy

• Subsidy to be routed through MP Madhya Kshetra Vidyut Vitran Company Ltd. (MPMKVVCL)

for disbursement

• Entire capacity of 5 MW envisaged to be deployed on public rooftops (state govt. and state

PSU buildings) and preferably on a zero lease rental basis

• Selection of private developers shall be through a competitive bidding process

4

Proposed Transaction Framework

- Business Model

- Commercial Arrangements

© 2014. Deloitte Touche Tohmatsu India Private Limited.

Business Model

6

Project Bidders Project Off Taker Incentive

Structure

Solar Project

Developers

EPC Players

Govt.

Buildings

Quoted

Tariff &

Capital

Subsidy

Public Buildings

– Zero Lease

Rental

Incentives for

Leasing of

Rooftop

Interconnect

provider & Energy

Accounting

State

Discom

MPPMCL

Off-taker

© 2014. Deloitte Touche Tohmatsu India Private Limited.

Commercial Arrangements

7

Rooftop Owner

(Lessor)

Developer

(Lessee)

MPPMCL

Nodal Agency

Quoted Tariff & Quoted

Project Cost

Capital Subsidy

Lease Agreement

Project Implementation

Agreement (PIA)

Power Purchase

Agreement (PPA)

Commercial Relationship / Agreements

Financial Obligations

(Central Discom)

MNRE

Zero Lease Rental

Bid Process Management

8

© 2014. Deloitte Touche Tohmatsu India Private Limited.

Bid Process Management ..1

• Single Bid Process to allow participation for all three (3) cities

• Single stage two envelope bidding to be conducted for selection of Bidders

‒ Technical Bid to provide shortlisting of Bidders

‒ Financial Bid of qualified Bidders to be opened for evaluation and selection

• RFP Documents to be uploaded on the websites of MPPMCL and MPMKVVCL

• Pre-bid conference to be held in Bhopal/Jabalpur for all three (3) cities for Bidder’s queries

on RFP documents

9

© 2014. Deloitte Touche Tohmatsu India Private Limited.

Bid Process Management ..2

• Portfolio Attractiveness

‒ Total project size of 5 MW to be awarded in three (3) packages to three (3) different Bidders as shown

below:

‒ Technical survey of public rooftops has been completed and more than 5 MW has been estimated as

deployable capacity

‒ Bidders to submit a Bid Bond for Rs. 5 lakh/MW at the time of submission of bid in the form of a

bank guarantee as per the format specified in RFP

• Bidder’s Structure

- Bidder can be a Bidding Company or a Bidding Consortium with the no. of members not exceeding

three (3) in no. including the Lead Member

- Bidding Company/Member can utilize the credentials/strength of its Affiliate/Parent/Ultimate Parent to

meet the qualification requirements

10

Proposed Package Cities Capacity (MW)

Package 1 Bhopal 2 MW

Package 2 Indore 2 MW

Package 3 Jabalpur 1 MW

RFP – Salient Features

11

© 2014. Deloitte Touche Tohmatsu India Private Limited.

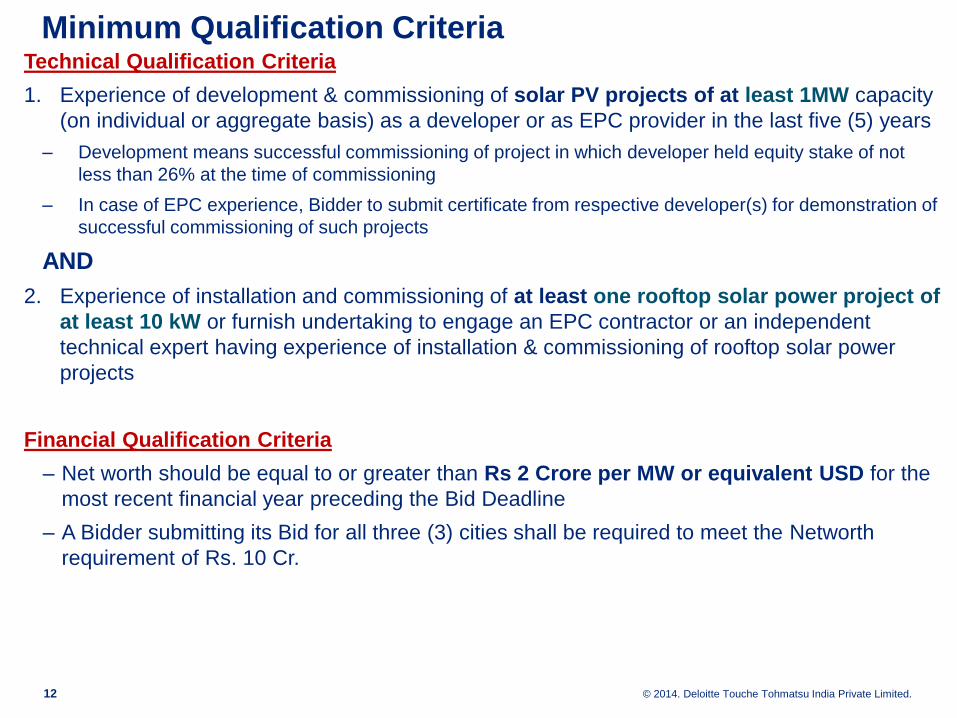

Minimum Qualification Criteria

Technical Qualification Criteria

1. Experience of development & commissioning of solar PV projects of at least 1MW capacity

(on individual or aggregate basis) as a developer or as EPC provider in the last five (5) years

‒ Development means successful commissioning of project in which developer held equity stake of not

less than 26% at the time of commissioning

‒ In case of EPC experience, Bidder to submit certificate from respective developer(s) for demonstration of

successful commissioning of such projects

AND

2. Experience of installation and commissioning of at least one rooftop solar power project of

at least 10 kW or furnish undertaking to engage an EPC contractor or an independent

technical expert having experience of installation & commissioning of rooftop solar power

projects

Financial Qualification Criteria

‒ Net worth should be equal to or greater than Rs 2 Crore per MW or equivalent USD for the

most recent financial year preceding the Bid Deadline

‒ A Bidder submitting its Bid for all three (3) cities shall be required to meet the Networth

requirement of Rs. 10 Cr.

12

© 2014. Deloitte Touche Tohmatsu India Private Limited.

Minimum Equity Lock In Requirements

Minimum Equity to be held by the Promoter(s)

• No change in the shareholding to be permitted from the date of submitting RFP bid and till

the execution of the PPA

• After execution of PPA, the controlling shareholding (controlling shareholding shall mean at

least 26% of the voting rights) in the Company developing the project shall be maintained

up to a period of five (5) years post COD

• Bidding Company allowed to form a Project Company for submission of bid/signing the

PPA. In case of a Consortium, formation of Project Company is mandatory

• In case of a Consortium, the Lead Member shall continue to hold at least 51% (fifty one

percent) of the subscribed and paid up equity in the Project Company up to a period of 2

(two) years after Commercial Operation Date of the relevant Project and at least 26%

(twenty six percent) for a period of 3 (three) years thereafter.

13

© 2014. Deloitte Touche Tohmatsu India Private Limited.

Selection Criteria ..1 • Hybrid Model capturing Capital Cost and Tariff based bidding

• Bidding Criteria based on the following:

• Capital Cost for the identified capacity (with a ceiling of Rs. 10Cr/MW)

• Tariff equivalent to or lower than specified ceiling* in RFP

• Selection Criteria based on the following:

• Total Capital Subsidy requirement based on Rs. 3 Cr/MW shall be identified

• NPV of Quoted Tariff for 25 years shall be added to the above

• Bidder having the lowest payout shall be selected as Successful Bidder

• Bid Illustration to be shared with the Bidders in the RFP document

• Illustration

• Project Size = 1 MW; Life of Project = 25 Years ; Discount rate : 10.20% as per MPERC Order

• CUF :19% with 1% deration every year as per MPERC Order

14

Bidder Capital Cost

(Rs Cr/MW)

A

Capital

Subsidy (Rs

Cr/MW)

B = (30%*A)

Tariff

(Rs/Kwh)

C

NPV of Power

Purchase Cost (Rs Cr)

D = NPV of PPC for 25

years)

Total Outlay on

Project (Rs Cr)

B+D

B1 10 3 8.55 12.54 15.54

B2 6.75 2.025 6.44 9.44 11.47

B3 6.5 1.95 6.5 9.53 11.48

• Ceiling for quoted tariff to be based on most recent competitive bidding

• In the above illustration, Bidder B2 emerges as the successful Bidder for a capacity of 1 MW

© 2014. Deloitte Touche Tohmatsu India Private Limited.

Selection Criteria ..2

• In the event of tie between two Bidders, selection to be based on the actual Networth of

Tie Bidders

‒ In case a Tie Bidder is a Consortium, the Networth of Lead Member shall be considered for evaluation

• In the event, a Qualified Bidder emerges as the successful Bidder for both the packages,

then it shall be awarded the package for which it has quoted the lowest tariff

• In the event, the lowest tariff/cost as quoted by the Qualified Bidder emerges to be the

same for both the packages, then such Qualified Bidder shall be awarded one (1) package

with the principle that the other package shall be awarded to the next lowest qualified

Bidder who has quoted the next lowest tariff for the packages

15

© 2014. Deloitte Touche Tohmatsu India Private Limited.

Formats for Bid Submission

1. Covering Letter

2. Power of Attorney

3. Consortium Agreement

4. Letter of Consent from Consortium Members

5. Bidder’s composition and ownership structure

6. Qualification Requirement (Technical Criteria, Financial requirement)

7. Performance Bank Guarantee

8. Undertaking

9. Board Resolutions

10. Earnest Money Deposit/ Bid Bond

11. Financial Bid

12. Checklist for Bid submission requirements

13. Disclosure

14. Format for certificate of relationship of Parent Company or Affiliate with the Bidding Company or with

the Member of the Bidding Consortium, including the Lead Member

15. Undertaking with respect to rooftop solar experience

16. Authorization from Affiliate/Parent/Ultimate Parent for utilizing credentials by Bidder

16

© 2014. Deloitte Touche Tohmatsu India Private Limited.

Time Schedule

17

Event Duration

1 Issuance of RFP T0

2 Pre Bid Conference and issuance of

revised RFP documents, if required T0+15 days

3 Submission of RFP bid T0+ 45 days

4 Evaluation of Technical Bids and

shortlisting of Qualified Bidders T0+65 days

5

Evaluation of Financial Bids of

Qualified Bidders

T0+75 days

6 Issue of Letter of Intent Within 15 days from evaluation of proposals (T0+90 days)

7 Execution of Agreements (PPA, PIA &

Lease for public rooftops) Within 30 days from the date of issue of LoI

8 Financial Closure of the project 90 days from the date of signing of PPA

9 Commissioning of the Project 12 months from the date of signing of PPA*

*MNRE Sanction letter allows for an implementation period of 12 months starting 31st Dec. 2013. Accordingly the

implementation period may reduce for the project

PPA, PIA – Salient Features

18

© 2014. Deloitte Touche Tohmatsu India Private Limited.

Scheduled Commissioning & LDs (PPA, PIA)

• Performance Guarantee:

‒ Computed at the rate of Rs. 10 lakhs/MW of contracted capacity

‒ To be submitted within 30 days of issuance of LoI

• Scheduled COD: Within 12 months from signing of PPA (Phased Commissioning)

‒ First Phase having not less than 10% of contracted capacity within three (3) months from Effective

Date

‒ Second Phase to have at least 60% of contracted capacity within nine (9) months from Effective Date

‒ Third Phase: Balance of contracted capacity not later than Scheduled COD

• In case of delay in Scheduled COD, MPPMCL entitled to encash the Performance

Guarantee in the following manner:

‒ Delay upto 2 month – Rs 10,000/MW per day

‒ Delay of more than 2 month & upto 6 months– Rs 15,000/MW per day

‒ Beyond 6 months from Scheduled COD: Termination of PPA

• Independent Engineer:

‒ Appointment to be done by MPPMCL with costs being borne by the Project Developer

‒ Independent Engineer to verify the monthly progress reports to be made available by the developer

including the verification of the technical specifications and verify the results of the commissioning

tests for each Unit and issue certificate for the same to the developer

19

© 2014. Deloitte Touche Tohmatsu India Private Limited.

CUF Requirements & CDM

• CUF requirements:

‒ Minimum CUF requirement : At least 13% in each Contract Year

‒ Maximum CUF: Distribution Utility obliged to purchase energy corresponding to not more than CUF of

22 % in any Contract Year

• Sharing of CDM Benefits: In the event, the Solar Company gets CDM benefits, it shall be

shared with the utility starting from 100% to the Solar Company in the first year after COD

and thereafter being reduced by 10% every year till the sharing becomes equal to 50:50 in

the sixth year and then shall remain equal till the rest of the term of the Agreement

20

© 2014. Deloitte Touche Tohmatsu India Private Limited.

Payment Security Mechanism (PPA)

• Letter of Credit

‒ MPPMCL shall provide to Project developer, in respect of payment of its Monthly Bills and/or

Supplementary Bills, a monthly unconditional, revolving and irrevocable letter of credit (“Letter of

Credit”),

‒ Term of twelve (12) Months and shall be renewed annually, for an amount equal for the first Contract

Year, equal to

• for the first year, equal to 1.1 (one point one) times the estimated average Tariff Invoice based on

Normative CUF of the project

• for each subsequent year, equal to the one point one (1.1) times the average of the monthly Tariff

Payments of the previous Contract Year

21

© 2014. Deloitte Touche Tohmatsu India Private Limited.

Key Obligations of Distribution Utility

• Key obligations of the discom under the PPA shall include;

‒ Facilitating in getting interconnection for the project to the nearest grid point as per technical

schematic approved by the Independent Engineer

‒ Ensuring grid availability for the identified feeders

‒ Allow the project to run as a must –run generating facility subject to the provisions of the PPA

‒ Ensure monthly meter reading with the solar company’s representative based on the billing schedule

‒ Ensure timely payment of monthly invoices as specified in the PPA

‒ Provide adequate payment security mechanism to ensure PPA bankability

22

© 2014. Deloitte Touche Tohmatsu India Private Limited.

Thank You

23

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of

which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche

Tohmatsu Limited and its member firms.

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected

network of member firms in more than 140 countries, Deloitte brings world-class capabilities and deep local expertise to help clients succeed wherever they

operate. Deloitte's approximately 169,000 professionals are committed to becoming the standard of excellence.

This publication contains general information only, and none of Deloitte Touche Tohmatsu Limited, Deloitte Global Services Limited, Deloitte Global

Services Holdings Limited, the Deloitte Touche Tohmatsu Verein, any of their member firms, or any of the foregoing’s affiliates (collectively the “Deloitte

Network”) are, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This

publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your

finances or your business. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified

professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this publication.

©2014 Deloitte Touche Tohmatsu India Private Limited

© 2014. Deloitte Touche Tohmatsu India Private Limited.

Contractual Arrangements

Project Implementation Agreement

• Parties: MPMKVVCL (on behalf of Govt. of MP) & Project Developer

• Key Features:

‒ Role of developer: To Design, Construct, Develop, Operate & Maintain the project

‒ Role of MPMKVVCL: To Facilitate approval of lease of public rooftops, monitoring of project, appointment of

Independent Engineer, disbursement of subsidy

‒ Provisions for Liquidated Damages (LDs), Force Majeure (FM), Dispute Resolution etc. between the parties

Power Purchase Agreement

• Parties: Project Developer & MPPMCL

• Key Features:

‒ Role of developer: To Design, Construct, Develop, Operate & Maintain the project

‒ Role of MPPMCL: Allow project to run as must-run facility, accept all Delivered Energy up to Contracted Capacity,

pay to Developer the lower of Quoted Tariff/Base tariff for Delivered energy & Deemed Generation)

‒ Provisions for LDs, FM, Dispute Resolution, Renewable Purchase Obligation (RPO) compensation payments etc.

between the parties

Lease Agreement

• Parties: Project Developer & Rooftop owner

• Key Features:

‒ Role of Developer: To Design, Construct, Develop, Operate & Maintain the project

‒ Role of rooftop owner: Provide rooftop access to the developer, Termination & Relocation of the project, Provisions

for FM, Dispute Resolution etc. between the parties

27

PV ROOFTOP - GLOBAL PERSPECTIVES

Pic

ture

s:

SO

LO

N E

ne

rgy, G

IZ

5 MW RTPV Solar Project in the state of Madhya

Pradesh – Investors’ Meet, 17.06.2014, Bhopal

Timon Herzog, GIZ / ComSolar

• Federal enterprise to support the German Government in achieving its

objectives in the field of international cooperation for sustainable

development

• Operations in Germany and in over 130 countries around the world

• Around 17,000 employees

• Operates in India since 60 years, currently 250 staff members in

India

GIZ profile

2009 – 2016, BMUB & MNRE

Approach:

• Demonstration lighthouse projects

• Supporting regulative/policy framework

• Capacity & awareness building

Focus Areas:

PV Rooftop & solar thermal process heat

Project Team Delhi:

7 National & International experts

Commercialisation of solar energy in urban and

industrial areas (www.ComSolar.in)

• Global PV Market Highlights & Trends

• Germany – Case Study for RTPV

• Rooftop Examples

• Recommendations

Pic

ture

s:

GIZ

, D

B

Market

200 GW

@ 49 GW

TOP 3 p.a.

China

Japan

USA

Policy

Markets

61% FIT

driven

Global PV Market - Trends 2014 (Sources: EPIA , BSW, BNEF)

TOP 3 p.a.

Germany

China

Italy

Market

100 GW

@ 30 GW

ROW: Rest of the World, MEA: Middle East and Africa, APAC: Asia Pacific

Policy

Captive

NME

PPAs

2012 2014

Share of cumulative capacities end 2012 (Source: IEA PVPS, 2013)

• Still unbalanced structure

(Germany 1/3 of world

capacity)

• 13 countries entered the GW

capacity class

• 9 further close

• China has ~ 60% share of

global PV Cell & Panel

manufacturing

USD/kWh

Grid Parity: retail Electricity Prices vs. PV LCOE

kWh/kW/y

Highest Retail Electricity Prices

Lowest Retail Electricity Prices

PV “socket parity” in several regions (Source: IEA, 2013)

Global Trends 2014 – Summary & Conclusions

• 200 GWp mark likely to be exceeded worldwide

• Stable further growth with 40 – 50 GW p.a. likely (e.g. China alone 13

GW in 2013)

• Grid parity achieved in many regions

• Global growth is diversifying – shift of regional focus

PV will play a major role in the global electricity mix

Pic

ture

s:

SO

LO

N E

nerg

y

• Global PV Market Highlights & Trends

• Germany – Case Study for RTPV

• Rooftop Examples

• Recommendations

Relevant key facts compared to India

900-1300 kWh/m2

80,3 Mio

357,021 km2

1250-2150 kWh/m2

1,2 Bn

3,287,263 km2

Why is Germany pushing the pedal?

• Fight climate change

• Reduce energy imports

• Stimulate innovation &

green economy

• Strengthen energy

security & local

economy

The energy transition – 80% RE 2050 & nuclear phase out

until 2022 is decided to:

More details: www.energytransition.de

Macro economic benefit (Source: Fraunhofer Institute / IWES – Energy Policy Business

Model with 100% renewable energy by 2050)

• Fight climate change

• Reduce energy imports

• Stimulate innovation &

green economy

Fuel savings vs. RE CAPEX & OPEX with 200 GW PV an 180 GW Wind capacity

Subsidies to be phased out by 2020 –@ 52 GW

Fraunhofer IWES 100% Scenario: 200 GW PV 2050

German PV Market 2013, grid connected

(Source: Bundesnetzagentur / German grid authority)

31.12.2013:

Total Capa.

35.692 GWp

# Systems:

> 1.4 Million

• Cost reduction by 66% since 2006

• LCOE below electricity retail price – grid parity @ POS

• Attention: National differences in pricing & currency

German System prices for

<= 10 kW rooftop

Bottom line 2013 @

143 INR/Wp

(1.709 EUR with 84 INR/EUR)

Massive PV system price reduction (Source: BSW, PV-Exchange 2013, EPIA, own calculations)

EPIA scenario for residential

Segment in the EU at

1.30 Eur/Wp (109 INR) in

2022

2022

PV market segments in Germany

Image : Solarwatt

Private buildings:

1-10 kWp

Social, commercial,

agricultural buidlings:

10-100 kWp

Image : Solarwatt

Image: Sharp

Image : BP

Large commercial

buildings:

> 100 kWp

Image:

Geosol

Image: Grammer

10% 38% 23%

Source: BSW, E.Quadrat GmbH, based on 2012 data

<1%

71%

28%

Bu

ild

ing

in

teg

rate

d

Gro

un

d

Mo

un

ted

R

oo

fto

p

• Only 15% > 1 MW by 31.12.13

• Average system size: 25 kW

• Largest groups of owners: Private

persons, farmers, SMEs and newly

founded local Energy Cooperatives

• Fraunhofer ISE: On national average 98% @ LV distribution grid

• Large share of small distributed PV: local match of supply & demand

• Very limited requirement to improve of transport grid

Distributed PV has main impact on LV distribution grid

85% 15% <1%

Grid connection (Sources: Badenova, RENI / Solarpraxis)

Share of RE Systems connected to grid of Badenova

Average annual interruption within top 3 EU and < 50 Minutes (total SAIDI)

(Despite world largest share of PV/Wind)

Impact to grid stabilty (Source: Council of European Energy Regulators CEER, 12/2013)

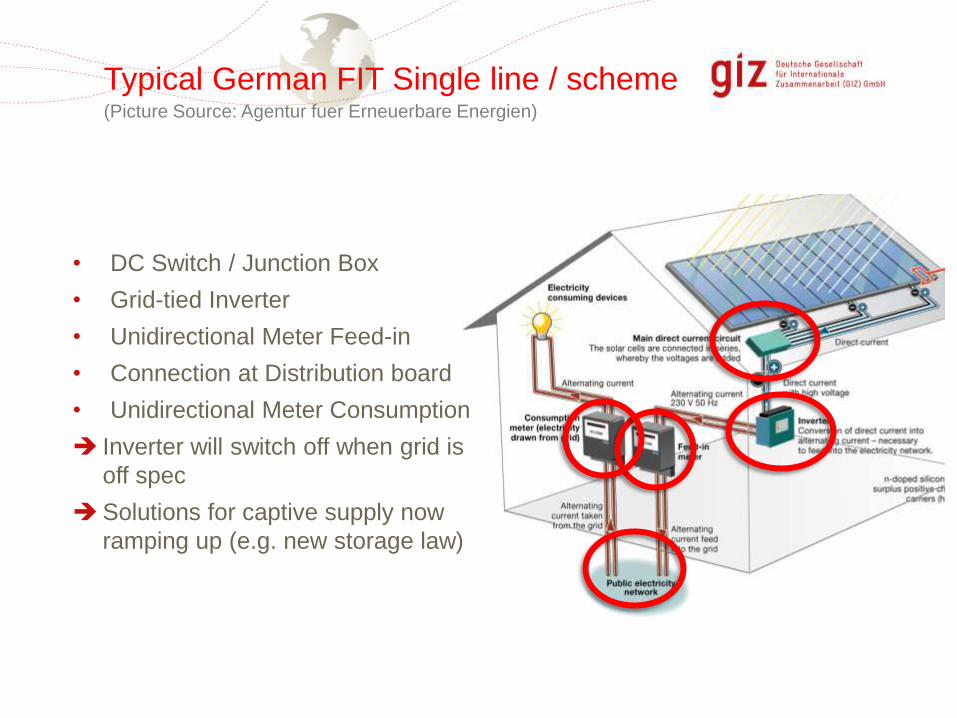

Typical German FIT Single line / scheme (Picture Source: Agentur fuer Erneuerbare Energien)

• DC Switch / Junction Box

• Grid-tied Inverter

• Unidirectional Meter Feed-in

• Connection at Distribution board

• Unidirectional Meter Consumption

Inverter will switch off when grid is

off spec

Solutions for captive supply now

ramping up (e.g. new storage law)

Germany PV Market - Conclusions

1. Distributed PV is a success model

Potential alone for “dark” Germany: 203 GW (following calculations

of Prof. Drg. Ing. Volker Quaschning HTW Berlin)

2. FAST grid integration is possible without problems

Proven with 35 GWp in more than 1.4 Mio Systems on the grid in

our small county without smart grid measures

3. Solar PV is economical feasible & competitive – today

Grid improvement & storage required for larger shares

Pic

ture

s:

GIZ

• Global PV Market Highlights & Trends

• Germany – Case Study for RTPV

• Rooftop Examples

• Recommendations

Examples: Standard Rooftop

Family home 9,7 KWp Brieselang, Germany

Cowshed 61,27 KWp Hohenreinkendorf, Germany, 2005

Church – 5 KWp Kablow, Berlin, Germany, 1994

Community center 135 KWp Sonnenschiff, Freiburg, Germany, 2003

Pic

ture

: P

ara

bel A

G

Pic

ture

: P

ara

bel A

G

Pic

ture

: IE

A P

VP

S

Pic

ture

: S

OL

ON

AG

Examples: Integrated PV

Roof – integrated 824 KW BMW World, Munich, Germany

Facade – integrated 12 KW Zara, Cologne, Germany, 2002

Roof – integrated 123 KW Paul-Loebe-Haus, Berlin, Germany, 2002

Roof – integrated 189 KW Mainstation, Berlin, Germany, 2002

Pic

ture

: S

OL

ON

AG

Pic

ture

: S

OL

ON

AG

Pic

ture

: P

VP

S / B

MW

Pic

ture

: D

B

Busport 2MW Sevilla, Spain, SOLON AG

Examples: Added value Systems

Noise Protection 500 kW Highway, Freiburg, Germany

Carport, 251 kW Mainz, Germany, Juwi Solar

Pic

ture

: IE

A-P

VP

S

Pic

ture

: S

OL

ON

AG

Pic

ture

: A

uto

hau

s

Freeland

91 MW

Briest, Germany.

2011, Q-Cells

Large rooftop

3.8 MW

Muggensturm,Germany.

2006, TAUBER-SOLAR

Examples: Large Scale

Further case studies incl. details see http://www.pvdatabase.org/

Pic

ture

: Q

-Ce

lls

P

ictu

re:

IEA

PV

PS

Pic

ture

s:

GIZ

• Global PV Market Highlights & Trends

• Germany – Case Study for RTPV

• Rooftop Examples

• Recommendations

Recommendations

1. Simple opportunities / low hanging fruits first

Integrated- and added value-systems induce extra efforts/costs

2. Quality should have highest priority

Cheap hardware will cause high lifecycle costs and lower yields

3. Distributed RTPV offers largest benefits

No additional land occupation, local value creation, minor grid

impact

4. Be cautious when planning large scale PV plants

Evacuation infrastructure and T&D losses become issues

Thank you!

ComSolar - Indo German Energy Programme

Deutsche Gesellschaft für Internationale Zusammenarbeit (GIZ) GmbH

GIZ Office New Delhi

www.giz.de - www.comsolar.in

Backup

2014 growth forecasts