group presentation - bucher industries · group presentation july 2014 5 . medium-term earnings...

TRANSCRIPT

Group presentation

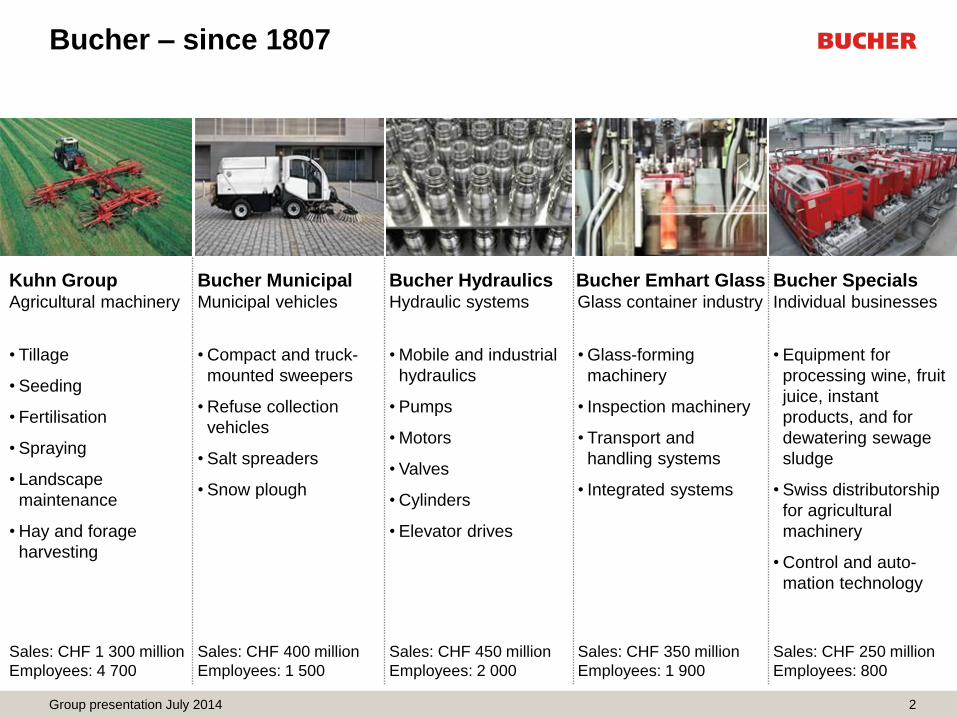

Bucher – since 1807

2

Kuhn Group Agricultural machinery

Bucher Municipal Municipal vehicles

Bucher Hydraulics Hydraulic systems

Bucher Emhart Glass Glass container industry

Bucher Specials Individual businesses

• Tillage

• Seeding

• Fertilisation

• Spraying

• Landscape

maintenance

• Hay and forage

harvesting

• Compact and truck-

mounted sweepers

• Refuse collection

vehicles

• Salt spreaders

• Snow plough

• Mobile and industrial

hydraulics

• Pumps

• Motors

• Valves

• Cylinders

• Elevator drives

• Glass-forming

machinery

• Inspection machinery

• Transport and

handling systems

• Integrated systems

• Equipment for

processing wine, fruit

juice, instant

products, and for

dewatering sewage

sludge

• Swiss distributorship

for agricultural

machinery

• Control and auto-

mation technology

Sales: CHF 1 300 million

Employees: 4 700

Sales: CHF 400 million

Employees: 1 500

Sales: CHF 450 million

Employees: 2 000

Sales: CHF 350 million

Employees: 1 900

Sales: CHF 250 million

Employees: 800

Group presentation July 2014

Number 1 market positions

Kuhn Group worldwide in forage harvesting

machinery and feed mixers

Bucher Municipal in Europe in sweepers

Bucher Hydraulics in Europe in special segments of mobile

hydraulics

Bucher Emhart Glass worldwide in glass container

manufacturing equipment

Bucher Specials worldwide in fruit juice and wine

production equipment

3 Group presentation July 2014

Main manufacturing sites worldwide

4

Total 5 continents

41 sites

Group presentation July 2014

Group strategy

• Increase in company value (RONOA > WACC)

• Diversified group focused on mechanical and vehicle engineering

• Strengthening of existing operating segments

– Continuous product innovation

– Operational efficiency with flexible structures

– Internal growth and targeted acquisitions

• Clear, central functions

– Strategy and operations reviews

– Treasury, Controlling, Tax, Legal, M&A, Investments, Communication

– Management and remuneration systems

• Solid balance sheet for long-term industrial independence

5 Group presentation July 2014

Medium-term earnings targets

6

EBIT margin 2009 2010 2011 20121) 2013 targets

Kuhn Group 7.53) 9.2 11.3 12.5 14.9 11

Bucher Municipal 3.9 7.3 7.0 9.3 8.6 8

Bucher Hydraulics 4.33) 9.9 8.7 9.0 9.4 11

Bucher Emhart Glass 4.0 1.22) 4.5 0.32) 4.8 9

Bucher Specials 5.3 4.6 6.1 8.1 10.0 9

Bucher Industries 5.23) 7.4 8.1 8.9 10.7 9

Group, divisions and independent businesses

RONOA after tax 11.43) 12.4 17.0 17.0 19.3 >16

3) Before impairment changes

2) After restructuring costs of CHF 9 million in 2012 and CHF 5 million in 2010

1) 2012: retrospective restatement owing to first application of IAS 19 (revised)

Group presentation July 2014

Group at a glance 2013

• Favourable market environment

– Good conditions at high level for agricultural machinery

– Low but stable demand for municipal vehicles

– Upturn in demand and sales growth through acquisitions at Bucher Hydraulics and

Bucher Specials

– Subdued first half, picking up in second half in glass-forming machinery

– Good market conditions in fruit juice processing equipment

• Entry into automation technology through takeover of Jetter AG by public

offering; at year-end Bucher held 77.35% of the equity

• Best result in the company’s history

– EBIT margin of 10.7%

– Profit for the year of CHF 196 million

– Earnings per share increase by 27% to CHF 19.64

7 Group presentation July 2014

Group at a glance 2013 (continued)

• Continuity in investments

– CHF 137 million for internal growth

– CHF 63 million for acquisitions at Bucher Hydraulics and Bucher Specials

• Solid financial situation

– Operating free cash flow of CHF 92 million

– Zero net debt at the end of 2013

– Increase in equity ratio from 39% to 44%

– Great financial scope for internal and external growth

8 Group presentation July 2014

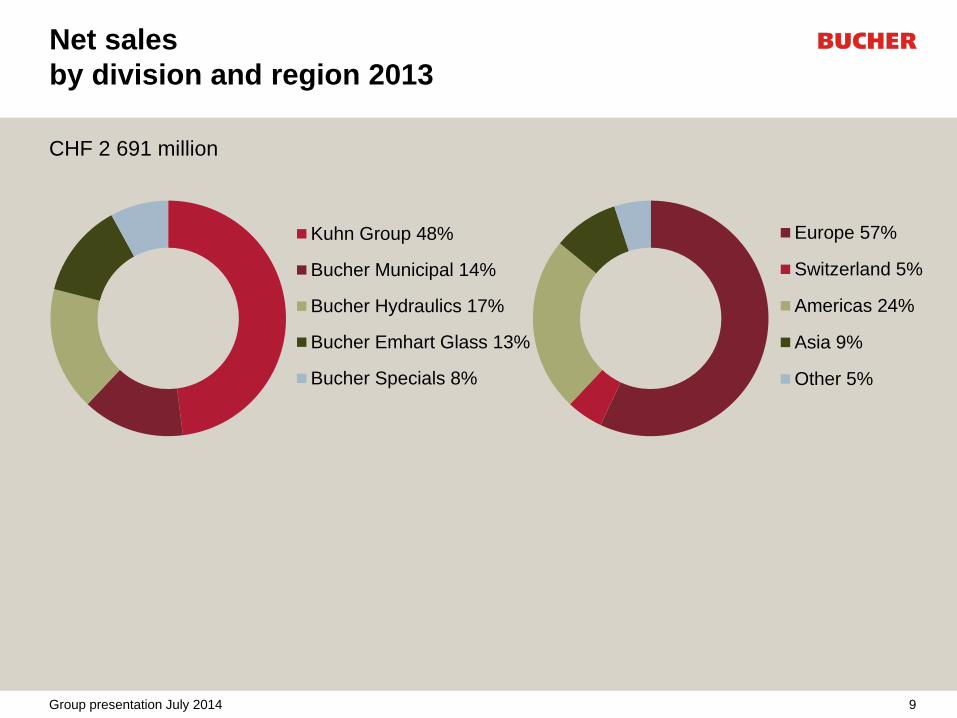

Net sales

by division and region 2013

CHF 2 691 million

Kuhn Group 48%

Bucher Municipal 14%

Bucher Hydraulics 17%

Bucher Emhart Glass 13%

Bucher Specials 8%

Europe 57%

Switzerland 5%

Americas 24%

Asia 9%

Other 5%

9 Group presentation July 2014

Numer of employees

by region 2013

Total 10 916 employees1)

Europe 55%

Switzerland 9%

Americas 21%

Asia 12%

Other 3%

1) Expressed as full time equivalents

10 Group presentation July 2014

Key figures

CHF million Change in

2013 2012 % %2) %3)

Order Intake 2 718 2 490 9.1 9.0 6.6

Net sales 2 691 2 609 3.1 3.0 0.8

Order book 850 795 6.9 6.5 3.3

Operating profit (EBITDA)1)

as % of net sales

371

13.8

307

11.8

20.9

Operating profit (EBIT)1)

as % of net sales

287

10.7

232

8.9

23.9

Profit for the year1)

as % of net sales

196

7.3

156

6.0

25.8

Employees at 31 December 10 916 10 166 7.4 2.1

Average employees during year 10 788 10 383 3.9 0.7

2) Adjusted for currency effects 3) Adjusted for currency, acquisition and disposal effects

1) 2012: retrospective restatement owing to first application of IAS 19 (revised)

11 Group presentation July 2014

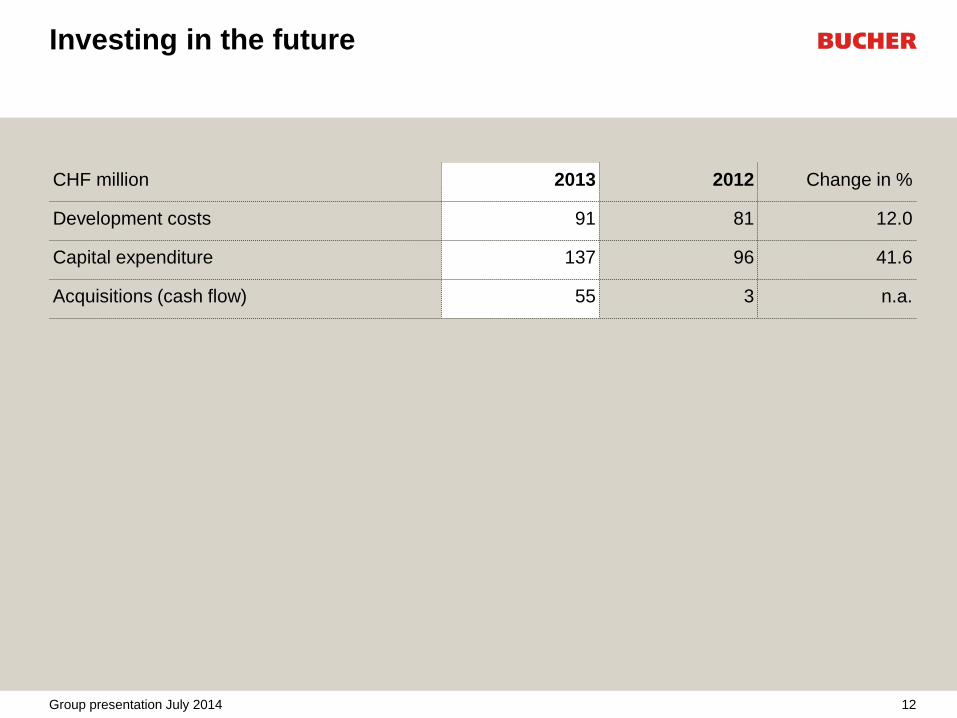

Investing in the future

CHF million 2013 2012 Change in %

Development costs 91 81 12.0

Capital expenditure 137 96 41.6

Acquisitions (cash flow) 55 3 n.a.

12 Group presentation July 2014

Results by division

CHF million 2013 20121)

EBIT EBIT margin EBIT EBIT margin

Kuhn Group 191 14.9% 153 12.5%

Bucher Municipal 33 8.6% 39 9.3%

Bucher Hydraulics 42 9.4% 37 9.0%

Bucher Emhart Glass 17 4.8% 1 0.3%

Bucher Specials 24 10.0% 17 8.1%

Other/consolidation -20 -15

Bucher Industries 287 10.7% 232 8.9%

1) 2012: retrospective restatement owing to first application of IAS 19 (revised)

13 Group presentation July 2014

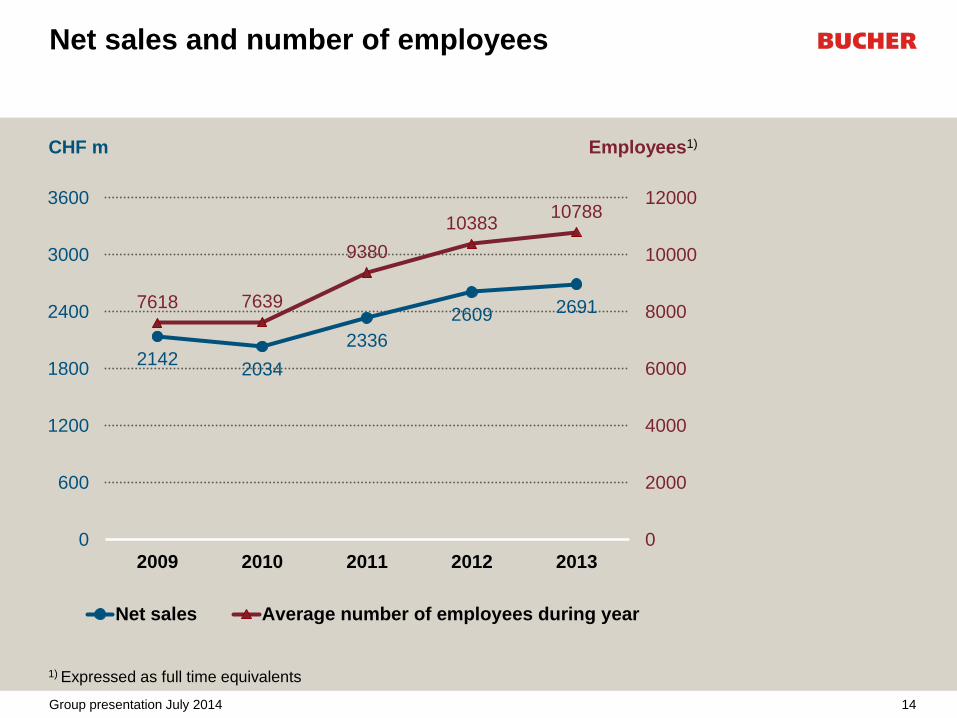

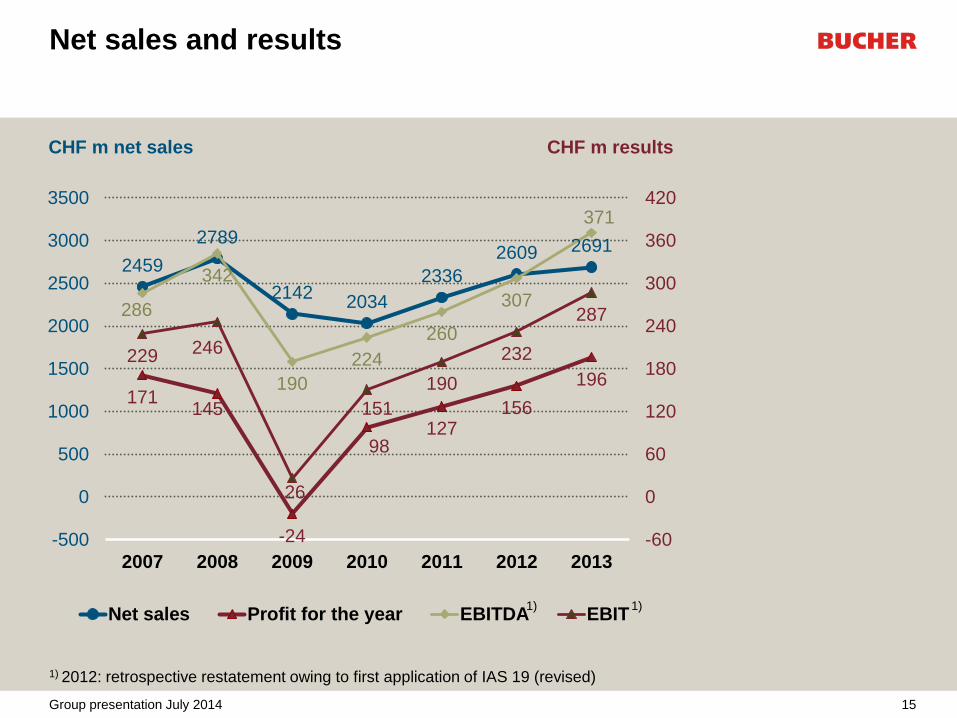

2691 2609

2336

2034 2142

10788 10383

9380

7639 7618

0

2000

4000

6000

8000

10000

12000

0

600

1200

1800

2400

3000

3600

20132012201120102009

Net sales Average number of employees during year

Net sales and number of employees

Employees1) CHF m

1) Expressed as full time equivalents

14 Group presentation July 2014

2691 2609

2336

2034 2142

2789

2459

196

156 127

98

-24

145 171

371

307

260

224

190

342

286 287

232

190

151

26

246 229

-60

0

60

120

180

240

300

360

420

-500

0

500

1000

1500

2000

2500

3000

3500

2013201220112010200920082007

Net sales Profit for the year EBITDA EBIT

Net sales and results

CHF m results

CHF m net sales

1) 2012: retrospective restatement owing to first application of IAS 19 (revised)

1) 1)

15 Group presentation July 2014

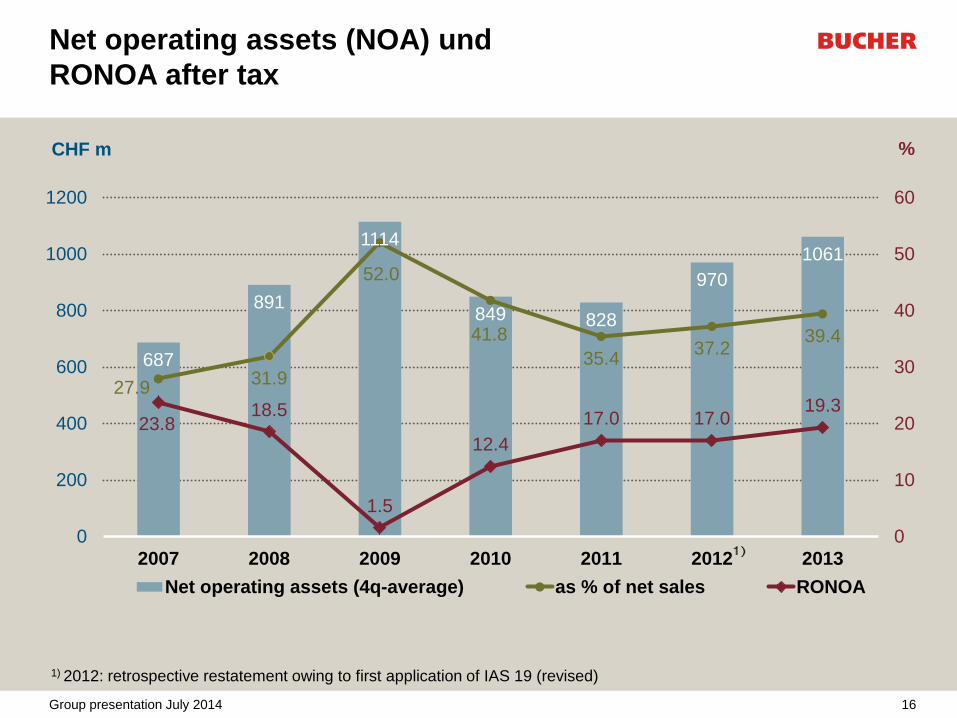

Net operating assets (NOA) und

RONOA after tax

1061

970

828 849

1114

891

687

39.4 37.2

35.4

41.8

52.0

31.9 27.9

19.3 17.0 17.0

12.4

1.5

18.5 23.8

0

10

20

30

40

50

60

0

200

400

600

800

1000

1200

2013201220112010200920082007

Net operating assets (4q-average) as % of net sales RONOA

CHF m

1) 2012: retrospective restatement owing to first application of IAS 19 (revised)

%

16 Group presentation July 2014

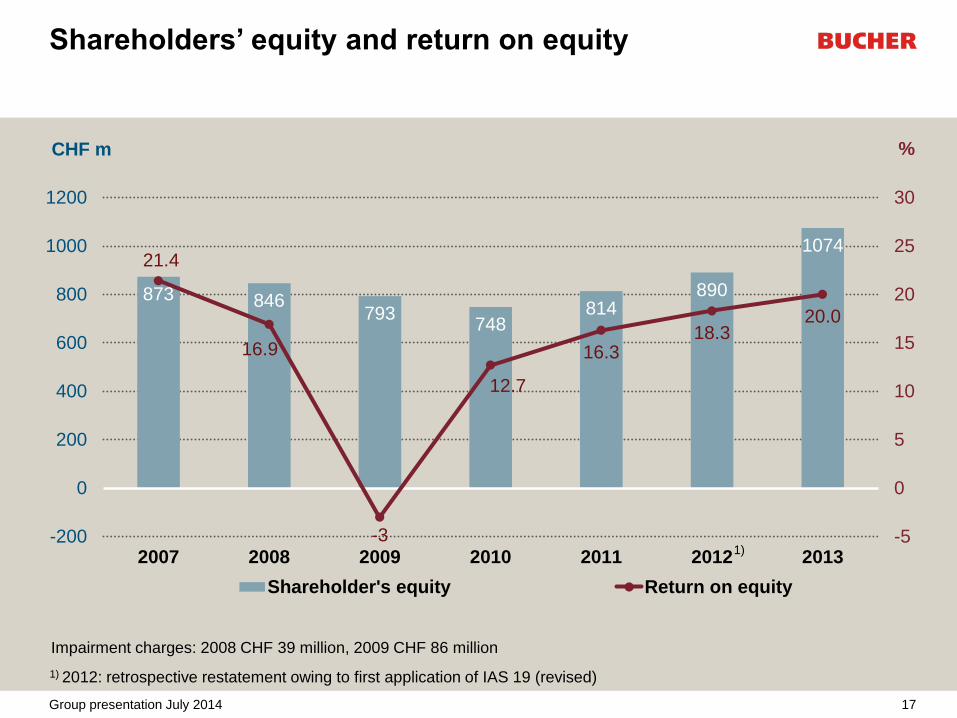

Shareholders’ equity and return on equity

1074

890 814

748 793

846 873

20.0 18.3

16.3

12.7

-3

16.9

21.4

-5

0

5

10

15

20

25

30

-200

0

200

400

600

800

1000

1200

2013201220112010200920082007

Shareholder's equity Return on equity

CHF m

1) 2012: retrospective restatement owing to first application of IAS 19 (revised)

Impairment charges: 2008 CHF 39 million, 2009 CHF 86 million

%

1)

17 Group presentation July 2014

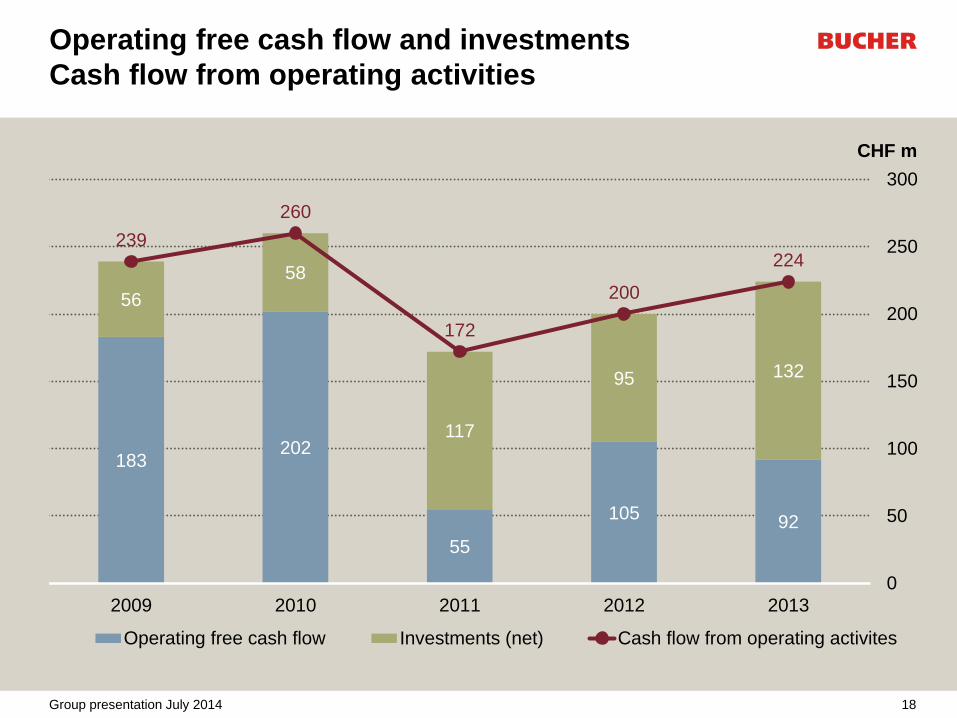

Operating free cash flow and investments

Cash flow from operating activities

18 Group presentation July 2014

CHF m

183 202

55

105 92

56

58

117

95 132

239

260

172

200

224

0

50

100

150

200

250

300

2009 2010 2011 2012 2013

Operating free cash flow Investments (net) Cash flow from operating activites

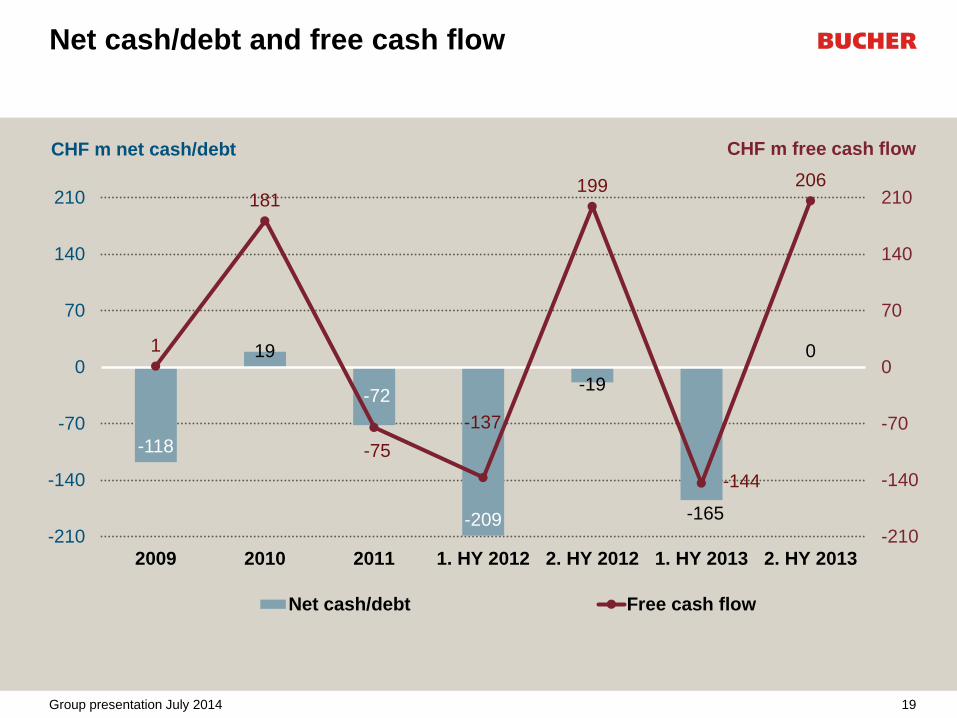

Net cash/debt and free cash flow

0

-165

-19

-209

-72

19

-118

206

-144

199

-137

-75

181

1

-210

-140

-70

0

70

140

210

-210

-140

-70

0

70

140

210

2. HY 20131. HY 20132. HY 20121. HY 2012201120102009

Net cash/debt Free cash flow

CHF m net cash/debt CHF m free cash flow

19 Group presentation July 2014

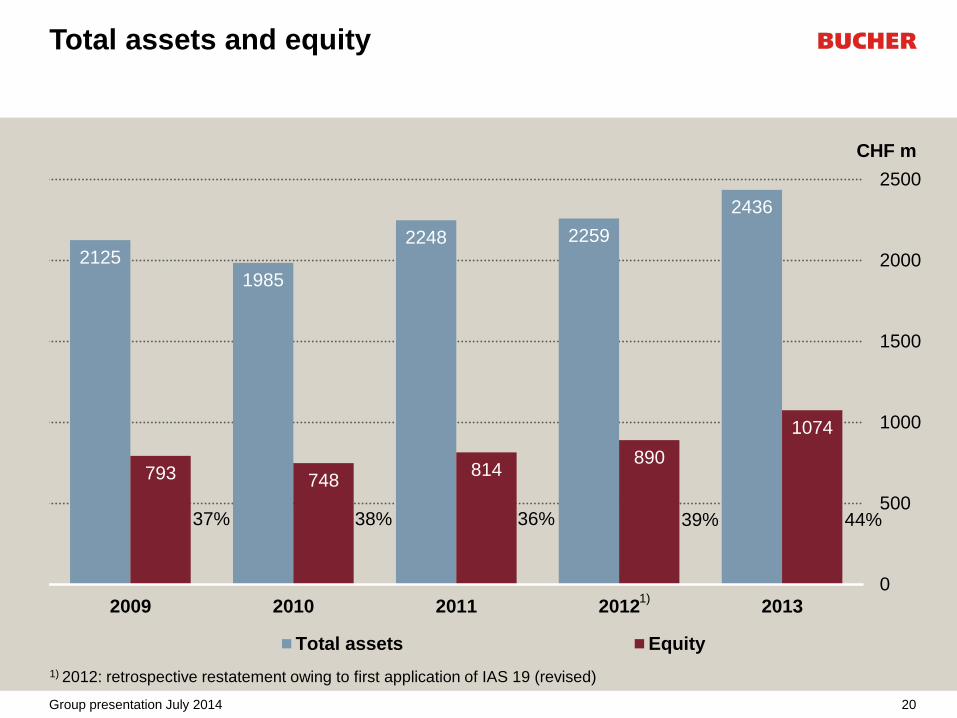

Total assets and equity

2125

1985

2248 2259

2436

793 748 814

890

1074

0

500

1000

1500

2000

2500

2009 2010 2011 2012 2013

Total assets Equity

44%

1) 2012: retrospective restatement owing to first application of IAS 19 (revised)

37% 38% 36% 39%

CHF m

1)

20 Group presentation July 2014

Shareholders’ equity / Intangible assets

21 Group presentation July 2014

793 748

814

890

1074

165 135

174 159 181 60 53 75 73 80

0

200

400

600

800

1000

1200

2009 2010 2011 2012 2013

Shareholders' equity Intangible assets Thereof goodwill

1) 2012: retrospective restatement owing to first application of IAS 19 (revised)

CHF m

1)

Group outlook for 2014

• No significant change in economic environment anticipated

• Confident mood in market segments served by Bucher Industries

– Agricultural machinery: slight decline in demand at very high level

– Municipal vehicles: positive outlook thanks to major order from Moscow

– Hydraulic systems and glass-forming machinery: continuation of positive development

of business

– Bucher Specials expects buoyant demand to continue, with additional boost from

acquisition of Jetter automation technology

• For Group overall, increase in sales and moderate decrease in profitability

compared with record figures in 2013

22 Group presentation July 2014

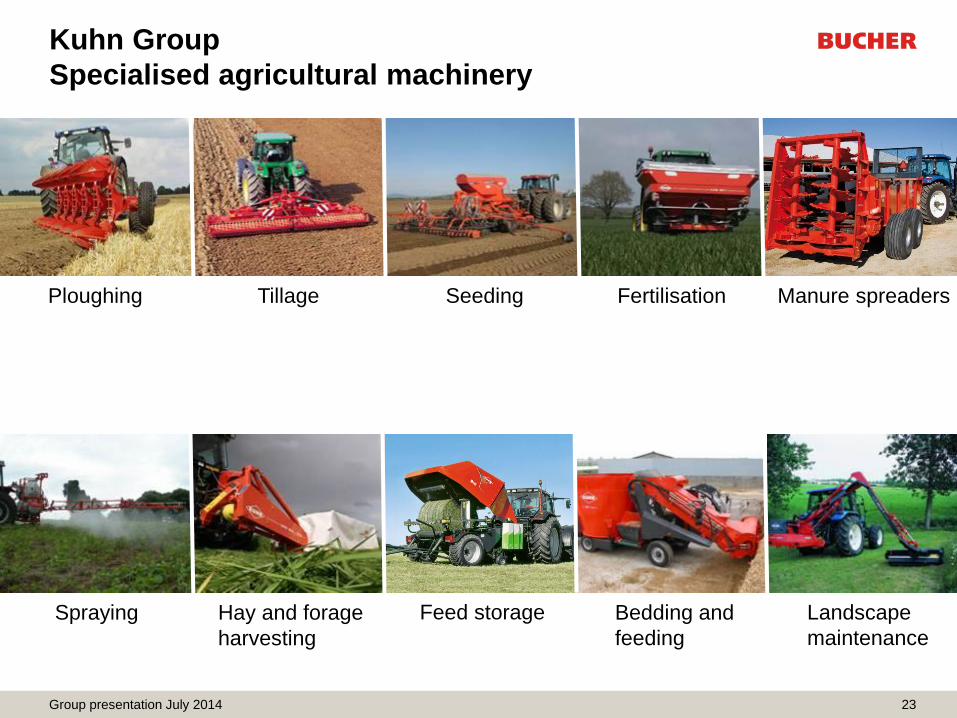

Kuhn Group

Specialised agricultural machinery

23

Ploughing Seeding Fertilisation Manure spreaders

Spraying Landscape

maintenance

Bedding and

feeding

Feed storage Hay and forage

harvesting

Tillage

Group presentation July 2014

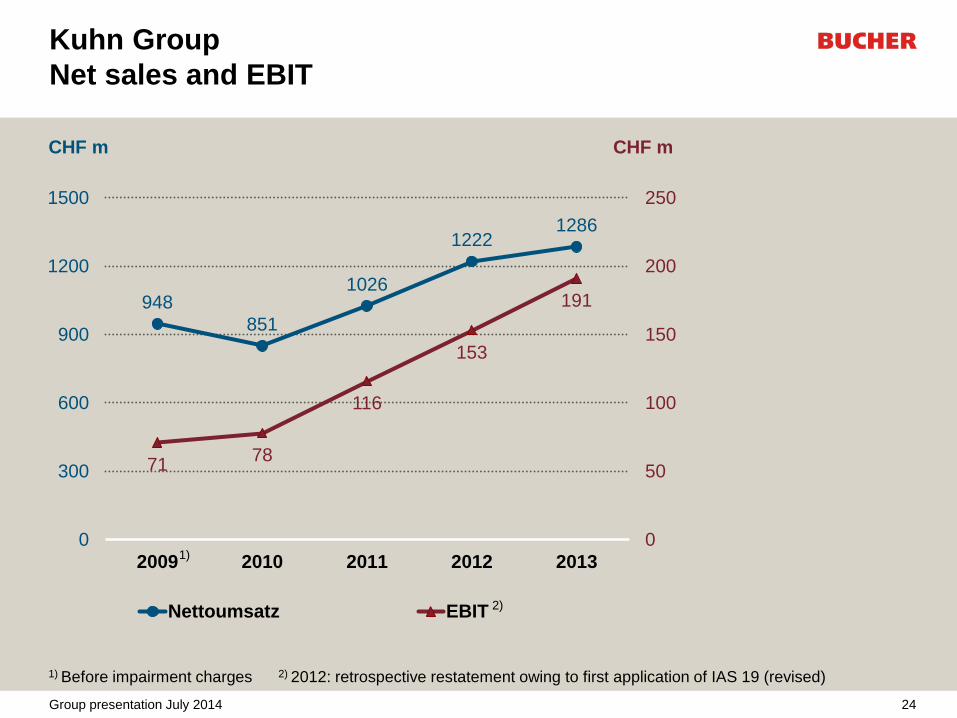

1286 1222

1026

851

948 191

153

116

78 71

0

50

100

150

200

250

0

300

600

900

1200

1500

20132012201120102009

Nettoumsatz EBIT

1) Before impairment charges 2) 2012: retrospective restatement owing to first application of IAS 19 (revised)

Kuhn Group

Net sales and EBIT

CHF m CHF m

1)

2)

24 Group presentation July 2014

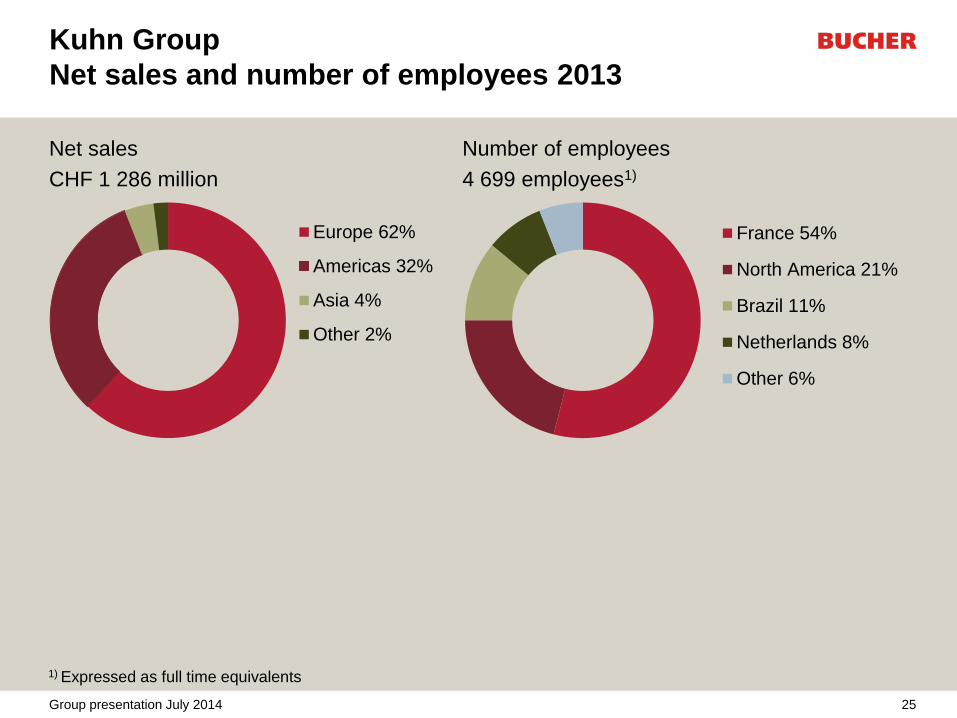

Kuhn Group

Net sales and number of employees 2013

Net sales Number of employees

CHF 1 286 million 4 699 employees1)

Europe 62%

Americas 32%

Asia 4%

Other 2%

France 54%

North America 21%

Brazil 11%

Netherlands 8%

Other 6%

1) Expressed as full time equivalents

25 Group presentation July 2014

Kuhn Group

Market position

• World’s leading manufacturer of specialised tractor-related agricultural

machinery under one brand

• Use of several distribution networks reduces dependence and increases

potential for high market share

• Broad customer base and independence from large customers

• Specialist in hay and forage harvesting machinery, tillage machinery, seed drills,

sprayers, feed mixers

• Market share: up to 30% or more worldwide depending on the product family

• Main competitors: Kverneland (NO), Krone (DE), Claas (DE), Pottinger (AT),

Amazone (DE) and other German, French and Italian manufacturers

26 Group presentation July 2014

Kuhn Group

Complete product range under one brand

27

Competitors Hay and forage Hedge Feed Tillage equipment Seeders Sprea- Spray- Trac- Harvesters

mow-

ers

tedders rakes

balers cutters mixers driven non-driven drilling precision ders ers

tors selfpropelled

Kuhn Group

John Deere

CNH

AGCO

Claas Renault

Krone

Amazone

Pöttinger

Kubota/KVE Gallignani Kubota

Exel / Hardi

Lemken

Horsch

Väderstad

Kongskilde

Lely/Welder

Sulky

Monosem

Group presentation July 2014

Kuhn Group

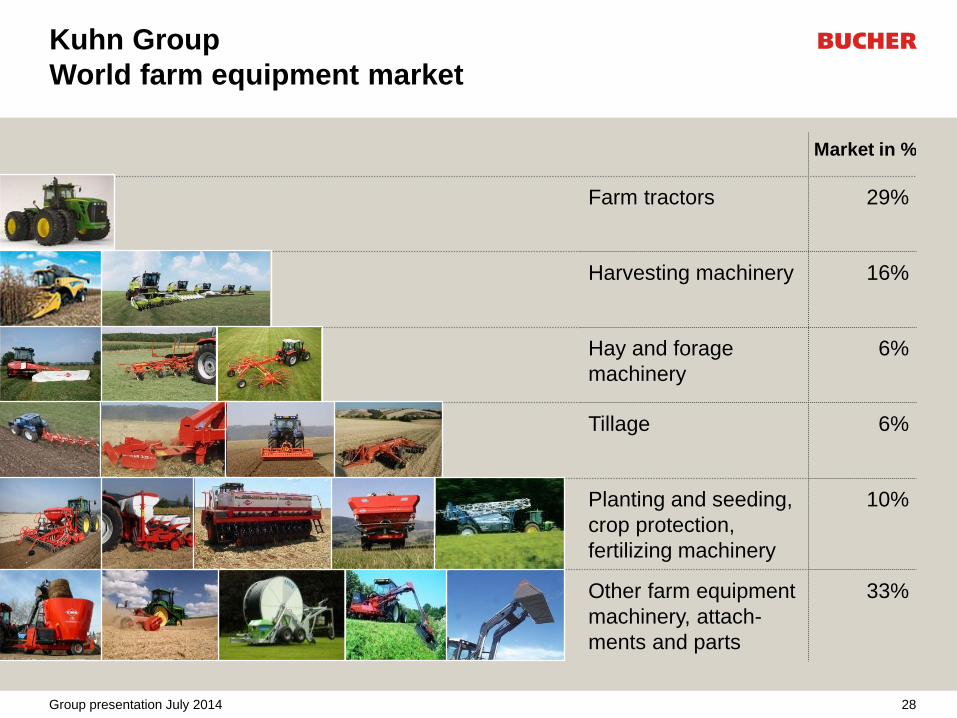

World farm equipment market

Market in %

Farm tractors 29%

Harvesting machinery 16%

Hay and forage

machinery

6%

Tillage 6%

Planting and seeding,

crop protection,

fertilizing machinery

10%

Other farm equipment

machinery, attach-

ments and parts

33%

28 Group presentation July 2014

Kuhn Group

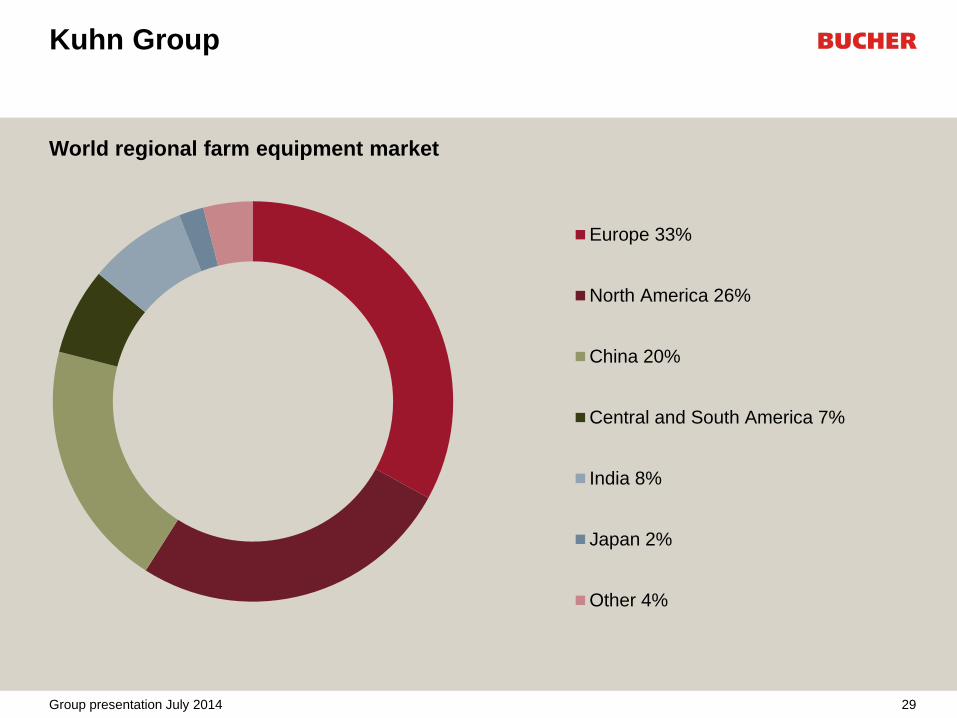

World regional farm equipment market

29

Europe 33%

North America 26%

China 20%

Central and South America 7%

India 8%

Japan 2%

Other 4%

Group presentation July 2014

Kuhn Group

2013 highlights

• Positive market trend

– Despite downward trend, prices for agricultural produce remained at a high level in long-

term comparison

– Investment confidence among farmers remained high

– Delay in growth cycle in springtime, later recovering to large extent

• Successful integration of acquired companies strengthens market position and

profitability

• Excellent profitability thanks to various operational factors

• Acquisition of Montana, Brazil, specialists in self-propelled crop sprayers, and

fertilising equipment, completed at the end of March 2014

• High investments in infrastructure, growth and customer training

30 Group presentation July 2014

Kuhn Group

Acquisition of Montana, Brazil

• Family company in Curitiba, Brazil, with subsidiary in Argentina

• Key figures:

– Sales 2013: BRL 225 million (CHF 96 million)

– Two-digit EBITDA margin

– 600 employees

• Main products (85% of sales):

– Self-propelled crop sprayers

– Self-propelled fertilising spreaders

• Complementary dealer network, primarily large scale farms

31 Group presentation July 2014

Montana

32

Self-propelled

crop sprayers

Self-propelled fertilising equipment

Manufacturing site in Curitiba, Brasilien

Group presentation July 2014

Kuhn Group

Outlook for 2014

• Good long-term prospects

• Market environment still positive, but slight fall in demand

– Favourable income situation for farmers continuing, but slightly lower year on year

– Main markets: America positive overall, Western Europe with lower demand

• Integration of the acquisition, Montana, Brazil, strengthens market position

• Sales slightly higher than previous year and moderate fall in high level of

profitability after record margin in previous year

33 Group presentation July 2014

Bucher Municipal

Sweepers and winter maintenance equipment

34

Compact sweepers Truck-mounted sweepers

Spreaders Refuse collection vehicles

Group presentation July 2014

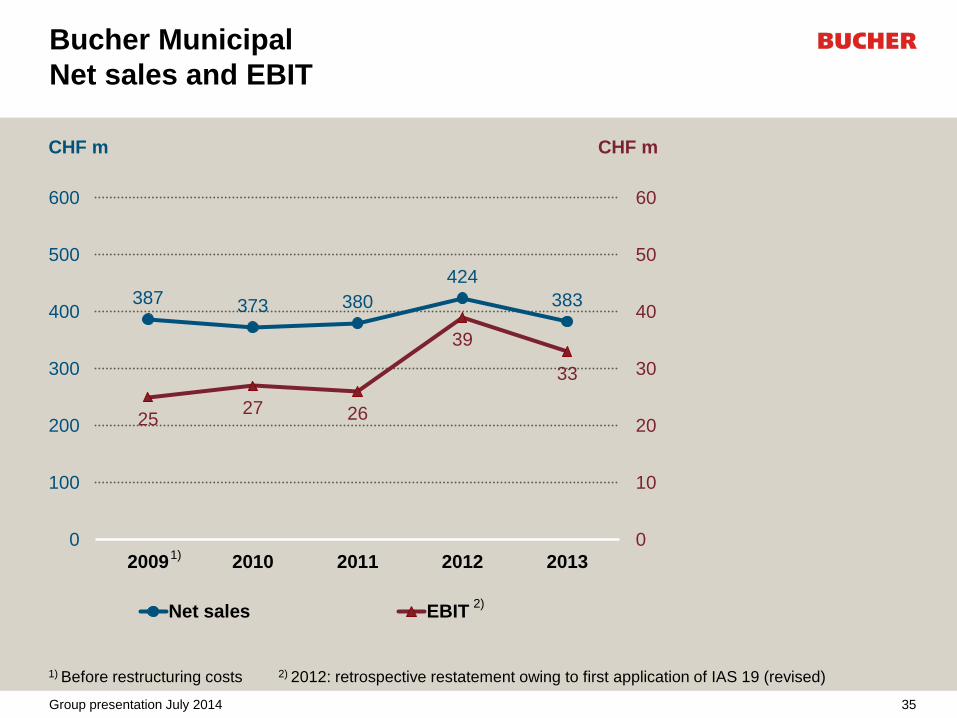

383

424

380 373 387

33

39

26 27 25

0

10

20

30

40

50

60

0

100

200

300

400

500

600

20132012201120102009

Net sales EBIT

1) Before restructuring costs 2) 2012: retrospective restatement owing to first application of IAS 19 (revised)

Bucher Municipal

Net sales and EBIT

CHF m CHF m

1)

2)

35 Group presentation July 2014

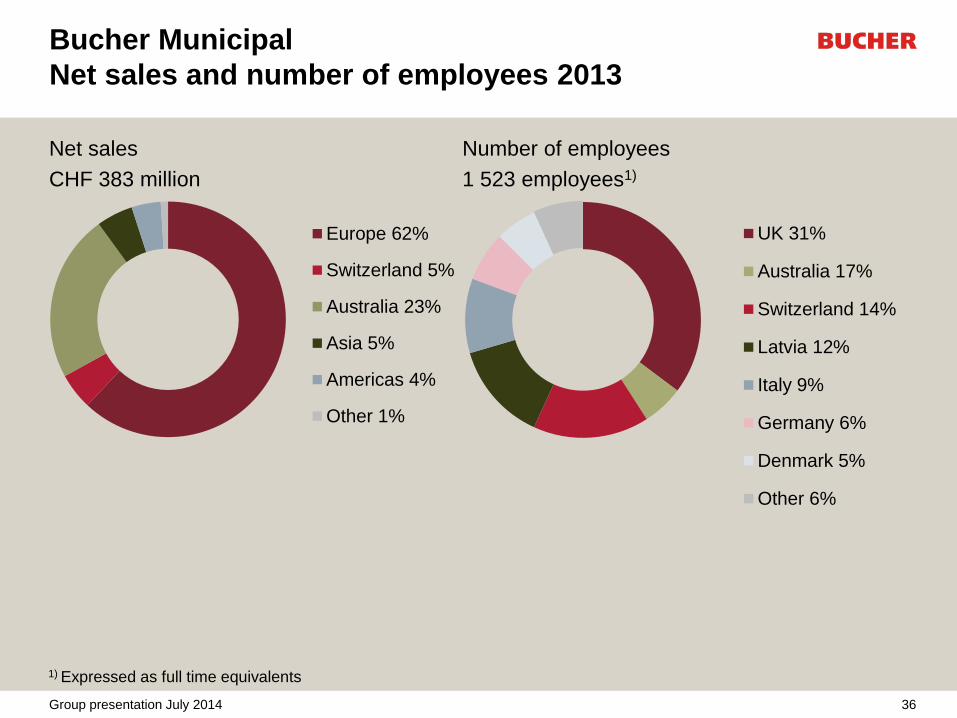

Bucher Municipal

Net sales and number of employees 2013

Net sales Number of employees

CHF 383 million 1 523 employees1)

Europe 62%

Switzerland 5%

Australia 23%

Asia 5%

Americas 4%

Other 1%

UK 31%

Australia 17%

Switzerland 14%

Latvia 12%

Italy 9%

Germany 6%

Denmark 5%

Other 6%

1) Expressed as full time equivalents

36 Group presentation July 2014

Bucher Municipal

Market position

• Market leader in Europe and Australia

• Market shares: Europe Australia

– Compact sweepers: 22% 48%

– Truck-mounted sweepers: 56% 77%

– Refuse collection vehicles: --- 50%

– Winter maintenance equipment: 28% ---

• Complete product line for municipal applications in Europe

• Main competitors: Aebi-Schmidt (DE), Ravo (NL)*, Scarab (UK)*, Hako (DE),

Boschung (CH), Faun (DE) and Elgin (USA)

* Fayat Group

37 Group presentation July 2014

Bucher Municipal

Complete product range

38

Competitors Sweepers Specialised

range

Spreaders

1m3 2m3 4m3 5m3 6m3 8m3 mounted towed

Bucher Municipal

Aebi-Schmidt (DE)

Boschung (CH)

Hako (DE)

Faun (DE)

Fayat Group (FR) *

Elgin (USA)

Dulevo (DE)

Brock (DE)

Tennant (USA)

Epoke (DK)

Acometis (FR)

* Ravo, Scarab, Mathieu

Group presentation July 2014

Bucher Municipal

2013 highlights

• Overall stable demand on a low level in Europe

• In March 2014, major order worth CHF 53 million from the city of Moscow

• Successful merger of production plants in Great Britain and Australia

strengthens competitiveness

• Innovation project for emission-free compact sweepers progressing on schedule

• Sale of profitable auxiliary business with hand-driers in Australia, with book

profit of CHF 4 million

• Good operating performance with gratifying level of profitability

39 Group presentation July 2014

Bucher Municipal

Outlook 2014

• Major order from city of Moscow ensures good performance in 2014

• First tentative signs of recovery in Southern Europe

• Start of production in Kaluga, Russia, with local manufacture of spreaders

• Marked increase in sales and modest improvement in operating profit

40 Group presentation July 2014

Bucher Hydraulics

Customised drive systems

41

Materials

handling

High-voltage

switch gear

Construction

equipment

Dyna-Lift Elevator

technology

Marine/offshore

Industry Agricultural

machinery

Mining /

tunnelling

Municipal

vehicles

Energy

technology

Lift gates

Group presentation July 2014

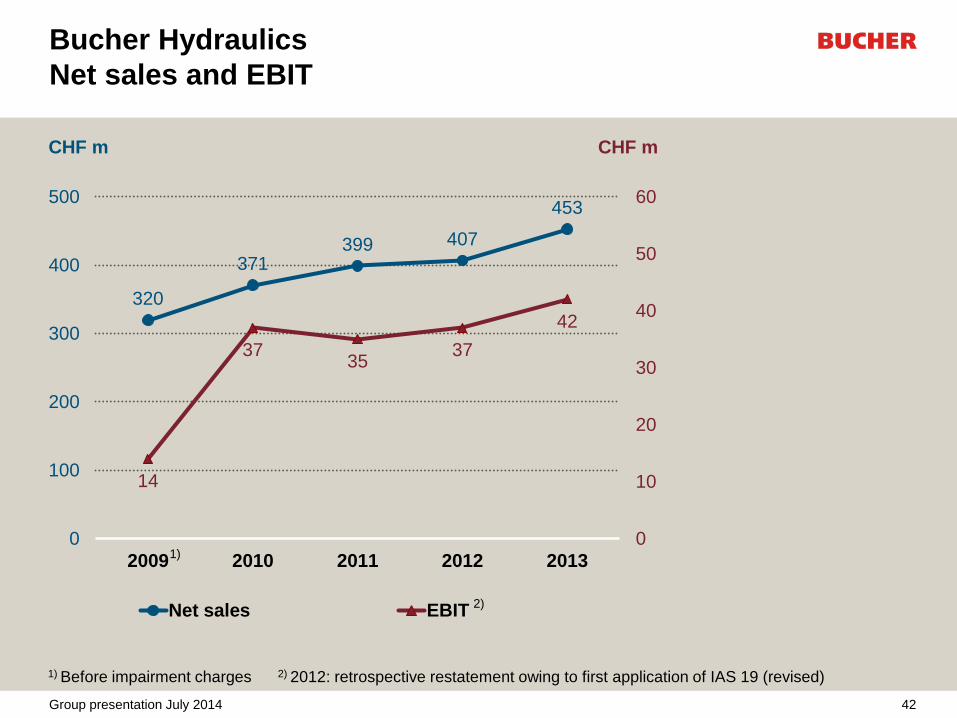

453

407 399 371

320

42

37 35

37

14

0

10

20

30

40

50

60

0

100

200

300

400

500

20132012201120102009

Net sales EBIT

Bucher Hydraulics

Net sales and EBIT

CHF m CHF m

1)

2)

1) Before impairment charges 2) 2012: retrospective restatement owing to first application of IAS 19 (revised)

42 Group presentation July 2014

Bucher Hydraulics

Net sales and number of employees 2013

Net sales Number of employees

CHF 453 million 1 984 employees1)

Europe 64%

Switzerland 4%

Americas 25%

Asia 7%

Germany 39%

Switzerland 23%

North America 16%

Italy 9%

Asia 8%

Brazil 3%

Other 2%

1) Expressed as full time equivalents

43 Group presentation July 2014

Bucher Hydraulics

Market position

• Leading specialist in mobile, industrial and elevator hydraulics across Europe

• Presence built up in the USA and Brazil

• Market share: 10% to 20% across Europe in specialised areas of hydraulic

engineering

• Focus on customised drive solutions

• Main competitors: Bosch-Rexroth (DE), Sauer Danfoss (USA), Parker Hannifin

(USA), Eaton Vickers (USA), Hydac (DE), Hawe (DE), Husco (USA), Denison

(USA), and a large number of further German and Italian manufacturers

44 Group presentation July 2014

Bucher Hydraulics

Complete product range

Pumps Valves Motors &

cylinders

Accessories Power

packs

Competitors

Pis-

ton

Vane Gear Indu-

strial

(Cetop)

Ser-

vo

Direc-

tional-

spool

Car-

tridge

Mani-

folds

Spe-

cial

Gea

r

Pis-

ton

Cylin-

ders

Elec-

tro-

nics

Accu-

mulat-

ors

Fil-

ters

Other Com-

pact

Con-

trac-

ting

Bucher Hydraulics

Parker (USA)

Eaton (USA)

Rexroth (DE)

Sauer Danfoss (DE)

Hydac (DE)

HAWE (DE)

Brevini Group (IT)

Walvoil (IT)

Argo-Hytos (DE)

Moog (USA)

Concentric (SE)

Husco (USA)

Sun Hydraulics (USA)

Hydraforce (USA)

45 Group presentation July 2014

50

60

70

80

90

100

110

120

130

140

150

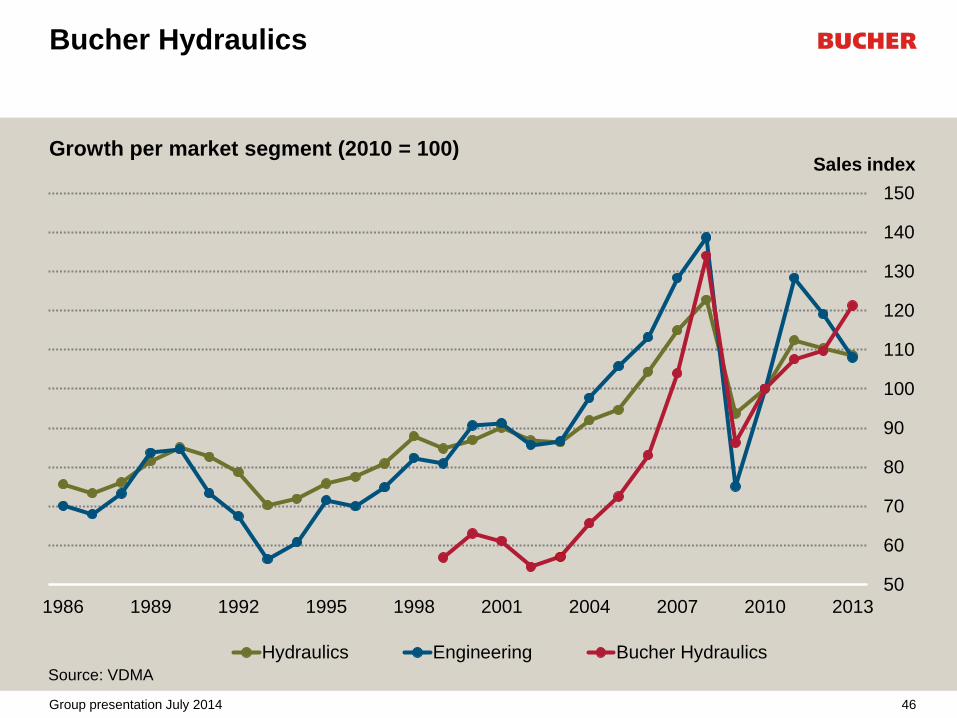

1986 1989 1992 1995 1998 2001 2004 2007 2010 2013

Hydraulics Engineering Bucher Hydraulics

Bucher Hydraulics

46

Sales index Growth per market segment (2010 = 100)

Source: VDMA

Group presentation July 2014

Bucher Hydraulics

2013 highlights

• Varied market environment

– Western Europe: market positive in mobile machinery, weakening in construction

machinery and industrial hydraulics

– USA: good level of demand sustained, preparation for series production in 2014 for

globally active customers

– China: government reins in construction activity

• Smooth integration of acquisition Ölhydraulik Altenerding, Germany, with

synergies in second half of year

• Entry into the Brazilian market through takeover of Eco Sistemas Hydráulica,

Porto Alegre

• Good operating performance with increase in sales, operating profit and EBIT

margin

47 Group presentation July 2014

Bucher Hydraulics

Outlook for 2014

• Positive development of business to continue

– Developments in Germany decisive for hydraulics sales in Europe

– Continuation of good level of demand expected in USA

• Series production in Europe and North America underpins sales development

• Development of new platform in Brazil offers short- and medium-term growth

opportunities

• Slight increase in sales and further improvement in operating profit expected

48 Group presentation July 2014

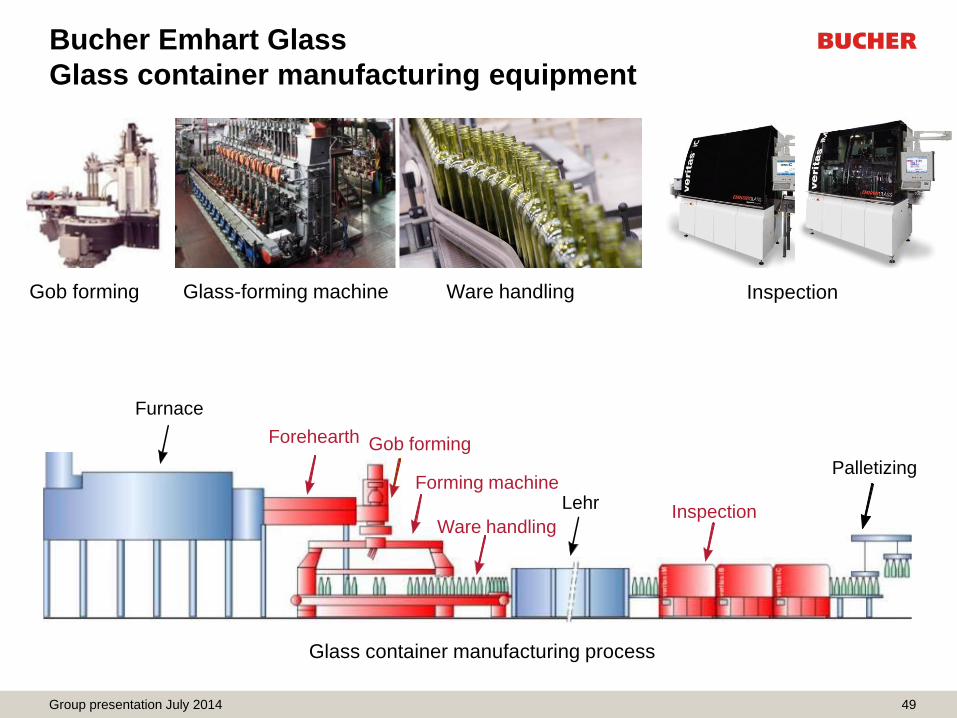

Bucher Emhart Glass

Glass container manufacturing equipment

49

Lehr

Forehearth

Furnace

Lehr

Palletizing

Inspection

Gob forming

Ware handling

Forming machine

Glass container manufacturing process

Gob forming Glass-forming machine Ware handling Inspection

Group presentation July 2014

347 367

345

259

304

17

10

15

8

12

0

10

20

30

40

50

0

100

200

300

400

500

20132012201120102009

Net sales EBIT

Bucher Emhart Glass

Net sales and EBIT

CHF m CHF m

1)

2)

1) Before restructuring costs 2) 2012: retrospective restatement owing to first application of IAS 19 (revised)

1)

50 Group presentation July 2014

Bucher Emhart Glass

Net sales and number of employees 2013

Net sales Number of employees

CHF 347 m 1 864 employees1)

Europe 38%

Asia 36%

Americas 19%

Africa 6%

Other 1%

China 56%

Sweden 15%

Americas 13%

Malaysia 7%

Switzerland 4%

Other 5%

1) Expressed as full time equivalents

51 Group presentation July 2014

Bucher Emhart Glass

Market position

• World’s leading supplier of machinery, equipment and services for glass

container manufacturers

• Market share: 50% worldwide for glass forming machines and services; 25%

worldwide for inspection systems

• Global partnership with Owens-Illinois (USA), the world’s biggest manufacturer

of glass containers

• Main competitors: Verallia (FR), Bottero (IT), BDF (IT), Heye International (DE)

for glass-forming machinery; Tiama (FR), Iris (FR) for inspection machinery

52 Group presentation July 2014

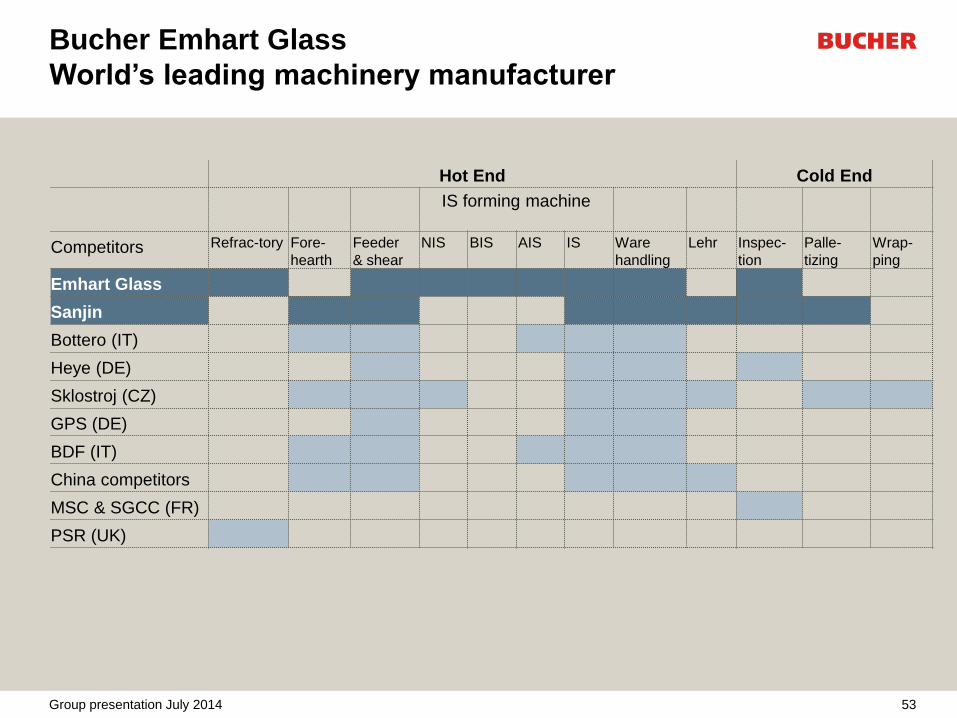

Bucher Emhart Glass

World’s leading machinery manufacturer

53

Hot End Cold End

IS forming machine

Competitors Refrac-tory Fore-

hearth

Feeder

& shear

NIS BIS AIS IS Ware

handling

Lehr Inspec-

tion

Palle-

tizing

Wrap-

ping

Emhart Glass

Sanjin

Bottero (IT)

Heye (DE)

Sklostroj (CZ)

GPS (DE)

BDF (IT)

China competitors

MSC & SGCC (FR)

PSR (UK)

Group presentation July 2014

Bucher Emhart Glass

Glass consumption per capita

54 Group presentation July 2014

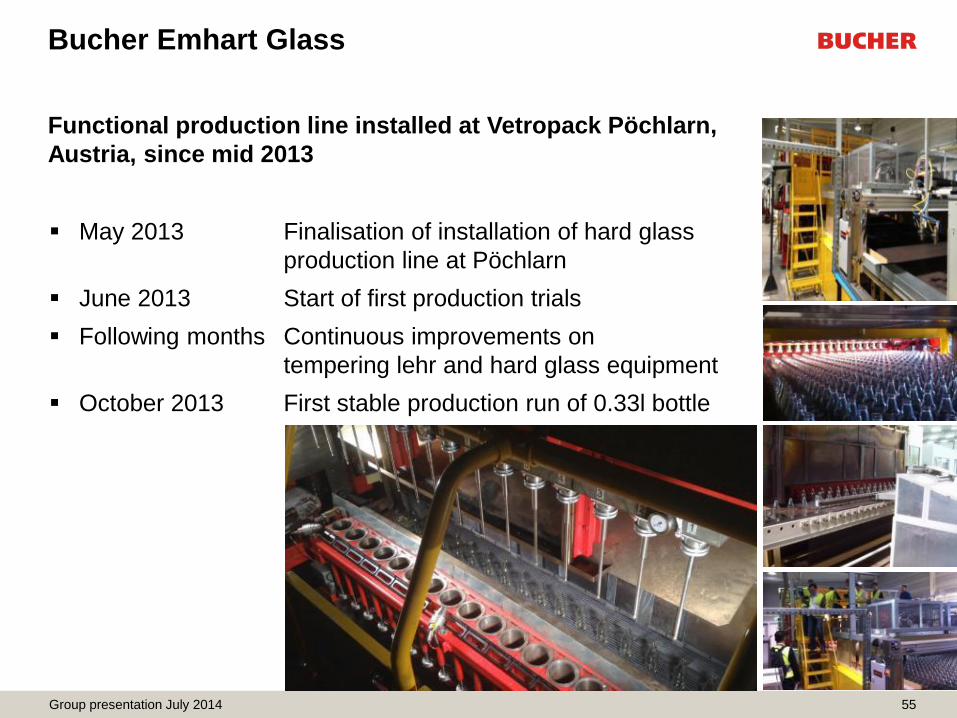

Functional production line installed at Vetropack Pöchlarn,

Austria, since mid 2013

May 2013 Finalisation of installation of hard glass

production line at Pöchlarn

June 2013 Start of first production trials

Following months Continuous improvements on

tempering lehr and hard glass equipment

October 2013 First stable production run of 0.33l bottle über län

55

Bucher Emhart Glass

Group presentation July 2014

Bucher Emhart Glass

56

Inte

rnal P

ressure

(bar)

Samples

Burst pressure after 25 filling line trips

Typical result - Hardglass bottles with significant strength increase over

annealed bottles

0

5

10

15

20

25

30

35

40

45

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20

200g Hardglass

200g Annealed

300g Annealed

Group presentation July 2014

Bucher Emhart Glass

Milestones until full market launch of first bottle

57

March 2015: Full market launch of 0.33l and 1.0l bottle with advertisement and promotion

2013 2014

Nov Dec Jan Feb Mrz Apr Mai Jun Jul Aug Sep Okt Nov Dec

Process

Optimization

Installation

Qualification

15 000 Process

validation

50 000

Qua-

rantine

10 000 filling

& internal

consumption

test

50 000

production

Quarantine

Filling & pre-market

test/launch

50 000 per month

Group presentation July 2014

Bucher Emhart Glass

2013 highlights

• Marked project-related fluctuations in capacity utilisation

• Varied market development

– Demand trend hesitant in first half and then positive in second half

– Slump in demand in China

• First commercial tempered glass system to Vetropack started operations at end

of year

• Realignment of capacities and leverage of worldwide presence

– Expansion of capacity in USA and Europe

– Expanded capacity in Malaysia came on stream ahead of plan

– Start of component sourcing from division’s own plants in Malaysia and China

– Completion of project expected by end of 2015/ beginning of 2016

• Worldwide cooperation agreement with Owens-Illinois came into force in

September

58 Group presentation July 2014

Bucher Emhart Glass

Outlook for 2014

• Market environment expected to be comparable with previous year

– Continuation of good level of demand in USA

– Recovery in Europe

– Stable spare part and service business

– Persistent weakness of Asian markets, especially in China

• Control systems, spare parts and new machines for Owens-Illinois could

provide growth momentum

• Savings arising from the realignment project improve profitability

• Increase in sales and further improvement in operating profit

59 Group presentation July 2014

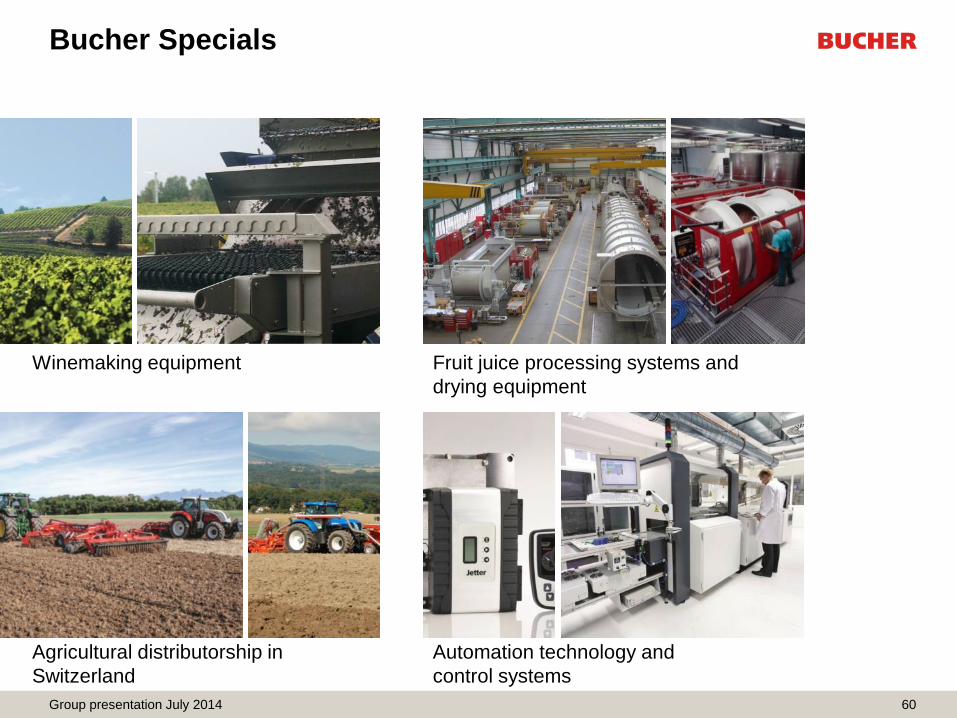

Bucher Specials

60

Winemaking equipment

Agricultural distributorship in

Switzerland

Automation technology and

control systems

Fruit juice processing systems and

drying equipment

Group presentation July 2014

244

206 201 187 188

24

17

12

9 10

0

5

10

15

20

25

30

35

0

50

100

150

200

250

300

20132012201120102009

Net sales EBIT

Bucher Specials

Net sales and EBIT

CHF m CHF m

1)

1) 2012: retrospective restatement owing to first application of IAS 19 (revised)

61 Group presentation July 2014

Bucher Specials

Net sales and number of employees 2013

Net sales Number of employees

CHF 244 m 785 employees1)

Europe 44%

Switzerland 37%

Americas 10%

Asia 7%

Other 2%

France 37%

Germany 29%

Switzerland 27%

Chile 3%

Italy 2%

Other 2%

1) Expressed as full time equivalents

62 Group presentation July 2014

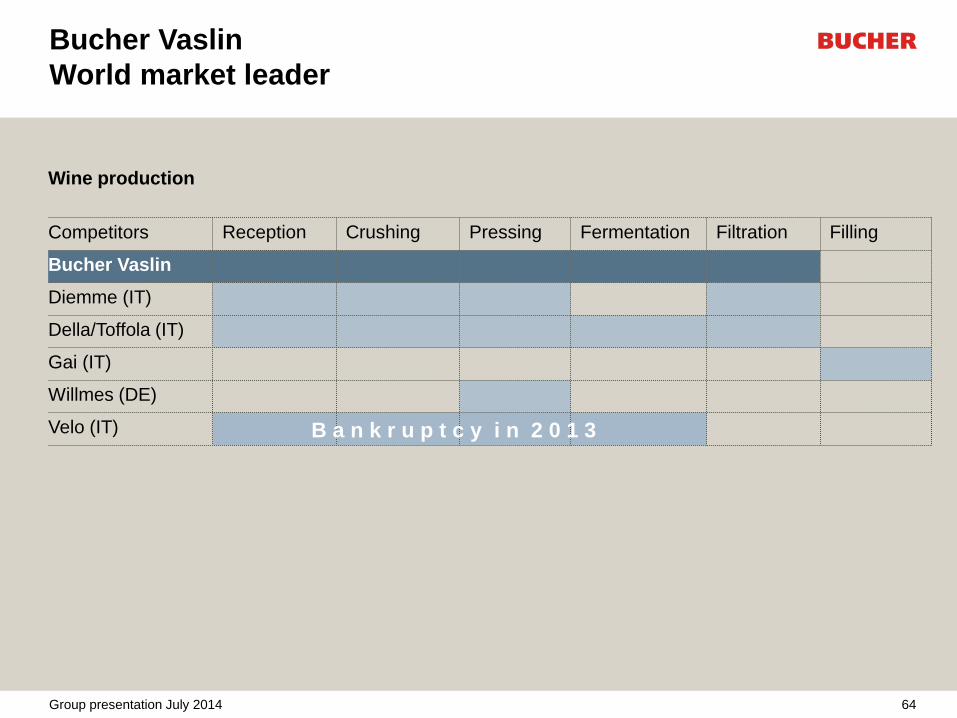

Bucher Vaslin

Market position

• World market leader in winemaking equipment

• Strong global distributor network

• Specialised production facilities in France and Chile

• Market share: 35% to 45% worldwide

• Main competitors: Pera (FR), Della Toffola (IT), Diemme (IT), and further Italian

and German manufacturers

63 Group presentation July 2014

Bucher Vaslin

World market leader

64

Wine production

Competitors Reception Crushing Pressing Fermentation Filtration Filling

Bucher Vaslin

Diemme (IT)

Della/Toffola (IT)

Gai (IT)

Willmes (DE)

Velo (IT) B a n k r u p t c y i n 2 0 1 3

Group presentation July 2014

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

0

5

10

15

20

25

30

35

40

45

50

US

A

Fra

nce

Italy

Sp

ain

Ge

rma

ny

Au

stria

Gre

ece

Po

rtug

al

Sw

itze

rlan

d

Russia

*

Chin

a *

CAGR million hl

2006 2007 2008 2009 2010 2011 prov. 2012 FC 2013 CAGR 06 - 13F

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

0

5

10

15

20

25

30

35

40

45

50

Arg

entin

a

Ch

ile

Bra

zil

South

Afric

a

Austra

lia

Ne

w Z

eala

nd

CAGR million hl

Bucher Vaslin

Wine production

65

Source: OIV, SAWIS

Northern hemisphere Southern hemisphere

* CAGR 06 - 11

Group presentation July 2014

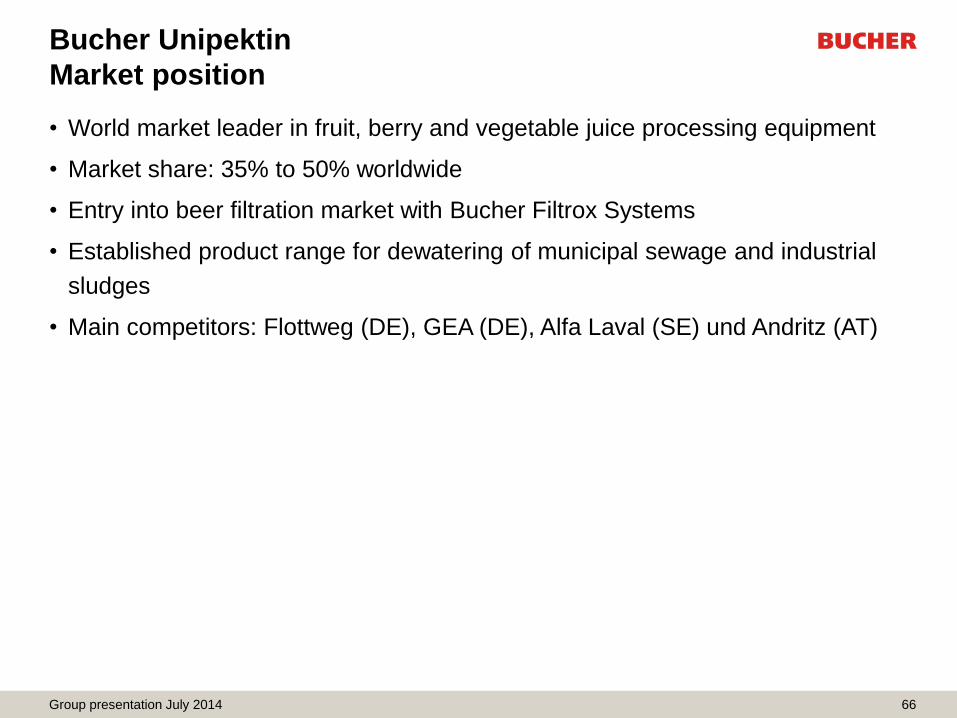

Bucher Unipektin

Market position

• World market leader in fruit, berry and vegetable juice processing equipment

• Market share: 35% to 50% worldwide

• Entry into beer filtration market with Bucher Filtrox Systems

• Established product range for dewatering of municipal sewage and industrial

sludges

• Main competitors: Flottweg (DE), GEA (DE), Alfa Laval (SE) und Andritz (AT)

66 Group presentation July 2014

Bucher Unipektin

World market leader

67

Juice production

Competitors Reception Milling Mash

heating

Dejuicing Pasteuri-

zation

Filtration Adsorp-

tion

Evapo-

ration

Bucher Unipektin

Flottweg (DE)

Bauer & Partners (PL)

GEA Group (DE)

Alfa Laval (SE)

Schmidt-Bretten (DE)

Bellmer (DE)

Kaimi (CN)

Group presentation July 2014

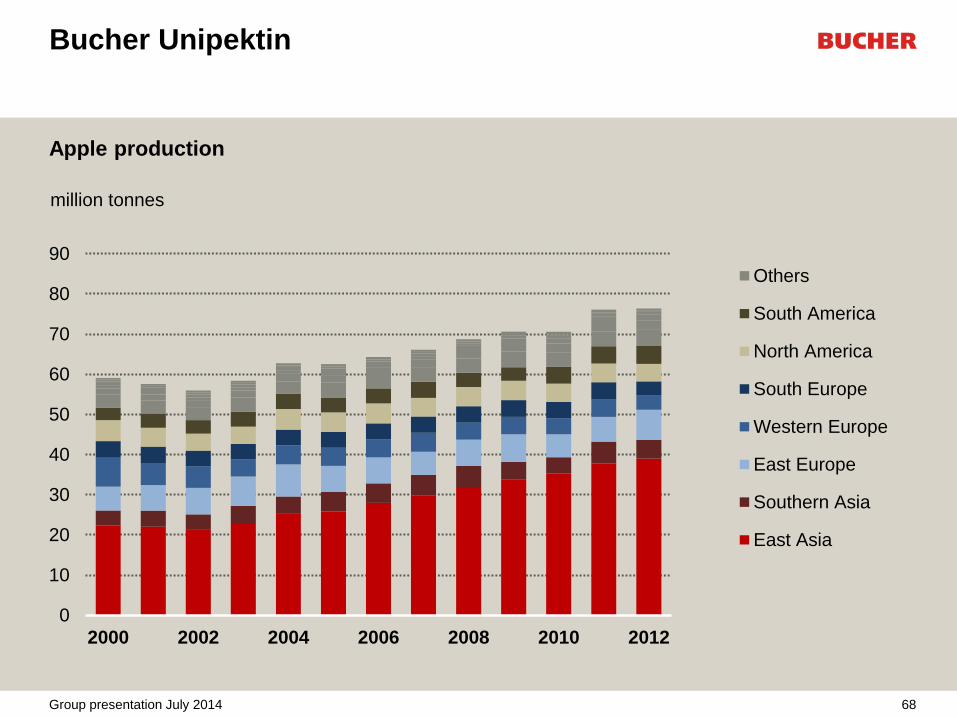

Bucher Unipektin

Apple production

68

0

10

20

30

40

50

60

70

80

90

2000 2002 2004 2006 2008 2010 2012

million tonnes

Others

South America

North America

South Europe

Western Europe

East Europe

Southern Asia

East Asia

Group presentation July 2014

Bucher Landtechnik

Market position (in Switzerland)

• Distributorship of tractors and agricultural machinery

• Well established among farmers and distributors

• Professional distributor network and high quality of service

• Wide range of tractors (New Holland, Case, Steyr), attachments (Kuhn) and

wheel loaders (Weidemann)

• Market share: 20% to 30%

• Main competitors

– Tractors: John Deere, AGCO, SDF, Claas

– Attachments: Pöttinger, Kverneland, Amazone, Lemken, Rabe, Krone, Fella

69 Group presentation July 2014

Bucher Landtechnik

Market leader in Switzerland

70

Competitors Hay and forage Hedge Feed Tillage equipment Seeders Sprea- Spray- Trac- Harvesters Wheel-

Mowers Tedders Rakes Balers cutters mixers driven non-

driven

drilling precision ders ers tors self -

propelled loaders

Bucher

Landtechnik Kuhn Kuhn Kuhn Kuhn Kuhn Kuhn Kuhn Kuhn Kuhn Kuhn Kuhn CNH

Weide-

mann

Matra

(John Deere)

GVS

(AGCO) Krone Krone Krone Krone Rabe Rabe Rabe Rabe

Fendt / MF/

Valtra

Fendt / MF /

Krone Bichon

Serco

(Claas) InTrac

Ott

Landmaschinen Kv Kv Kv Kv Kv

Amazone

Kv

Amazone

Kv

Amazone

Kv

Amazone

Kv

Amazone

Rauch / Kv

Amazone

Kv

Pöttinger CH

Fella CH

Grunderco Rousseau CNH

Lemken CH

Group presentation July 2014

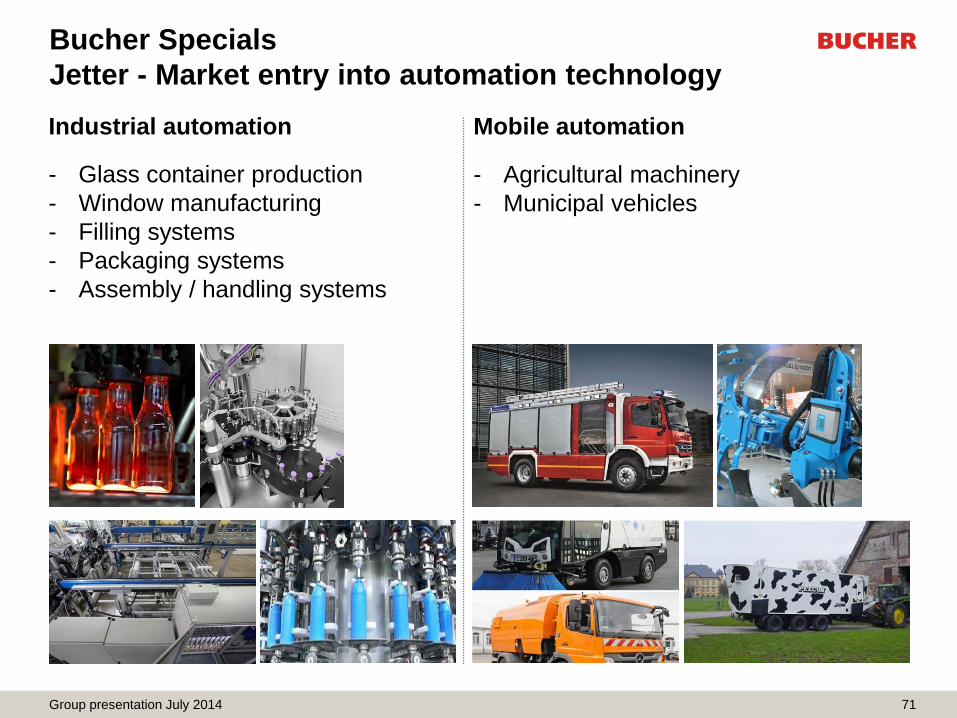

Bucher Specials

Jetter - Market entry into automation technology

71

Industrial automation Mobile automation

- Glass container production

- Window manufacturing

- Filling systems

- Packaging systems

- Assembly / handling systems

- Agricultural machinery

- Municipal vehicles

Group presentation July 2014

Bucher Specials

2013 highlights

• Stable market environment overall

– Upturn in demand for winemaking equipment

– Positive performance in equipment for fruit juice processing, dewatering sewage sludge

and beer filtration

– Sales of equipment for dewatering sewage sludge exceeded CHF 10 million for the first

time

– Buoyant market for the Swiss distributorship for agricultural machinery

– Contribution to sales from automation technology not yet significant; consolidated as of

November

• Operational improvements through streamlining in administrative area and

investments in logistics

• Gratifying rise in sales and operating profit

72 Group presentation July 2014

Bucher Specials

Outlook for 2014

• Market outlook

– Continuation of brisk demand for winemaking equipment

– Stabilization on high level in fruit juice processing equipment

– Increase in projects for dewatering sewage sludge and beer filtration

– Swiss distributorship for agricultural machinery at a high level, but declining

– Strong, acquisition-related sales growth through consolidation of Jetter automation

technology

• Bucher Specials expects strong growth in sales and operating profit

73 Group presentation July 2014