growmark, inc. consolidated financial … inc. consolidated financial statements years ended august...

TRANSCRIPT

GROWMARK, INC.

CONSOLIDATED FINANCIAL STATEMENTS

YEARS ENDED AUGUST 31, 2016 AND 2015

with

REPORT OF INDEPENDENT AUDITORS

Report of Independent Auditors

The Board of Directors of GROWMARK, Inc.

We have audited the accompanying consolidated financial statements of GROWMARK, Inc., which comprise the consolidated statements of financial position as of August 31, 2016 and 2015, and the related consolidated statements of operations, comprehensive income, shareholders’ equity and cash flows for the years then ended, and the related notes to the consolidated financial statements.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in conformity with U.S. generally accepted accounting principles; this includes the design, implementation and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free of material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audits. We did not audit the financial statements of Total Grain Marketing, LLC, and Western Grain Marketing, LLC, subsidiaries of the Company, which statements reflect total assets constituting 7% as of August 31, 2016 and 10% as of August 31, 2015 and net sales constituting 8% for the year ended August 31, 2016 and 9% for the year ended August 31, 2015 of the related consolidated totals. We also did not audit the financial statements of FS Grain, LLC, a limited liability company in which the Company has a 44% interest. In the consolidated financial statements, the Company’s investment in FS Grain, LLC, is stated at $34 million and $0 as of December 31, 2016 and 2015, respectively, and the Company’s equity in the net income (loss) of FS Grain, LLC, is stated at $(2) million and $0, for the years then ended. The statements for the previously mentioned subsidiaries and investee company were audited by other auditors whose reports have been furnished to us, and our opinion, insofar as it relates to the amounts included for those subsidiaries, is based solely on the reports of the other auditors. We conducted our audits in accordance with auditing standards generally accepted in the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement.

A member firm of Ernst & Young Global Limited

Ernst & Young LLP 155 North Wacker Drive Chicago, IL 60606-1787

Tel: +1 312 879 2000 Fax: +1 312 879 4000 ey.com

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, based on our audits and the reports of the other auditors, the financial statements referred to above present fairly, in all material respects, the consolidated financial position of GROWMARK, Inc. at August 31, 2016 and 2015, and the consolidated results of its operations and its cash flows for the years then ended in conformity with U.S. generally accepted accounting principles.

November 1, 2016

A member firm of Ernst & Young Global Limited

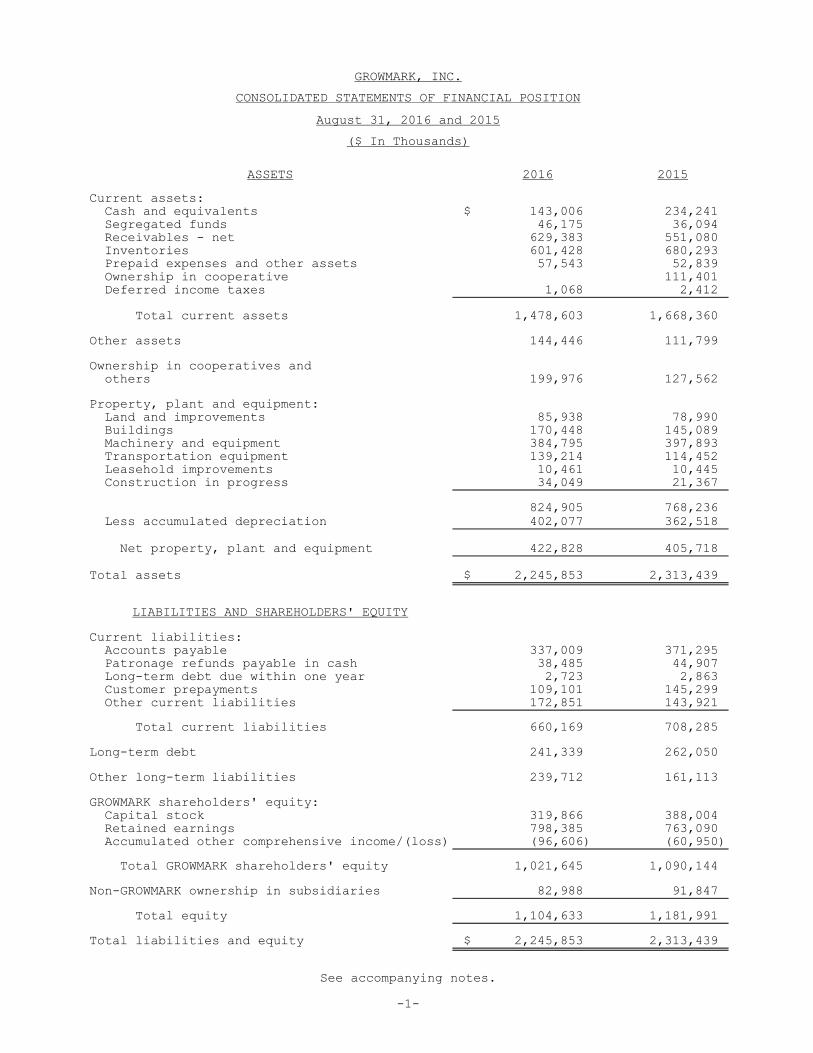

ASSETS 2016 2015

Current assets:

Cash and equivalents $ 143,006 234,241

Segregated funds 46,175 36,094

Receivables - net 629,383 551,080

Inventories 601,428 680,293

Prepaid expenses and other assets 57,543 52,839

Ownership in cooperative 111,401

Deferred income taxes 1,068 2,412

Total current assets 1,478,603 1,668,360

Other assets 144,446 111,799

Ownership in cooperatives and

others 199,976 127,562

Property, plant and equipment:

Land and improvements 85,938 78,990

Buildings 170,448 145,089

Machinery and equipment 384,795 397,893

Transportation equipment 139,214 114,452

Leasehold improvements 10,461 10,445

Construction in progress 34,049 21,367

824,905 768,236

Less accumulated depreciation 402,077 362,518

Net property, plant and equipment 422,828 405,718

Total assets $ 2,245,853 2,313,439

LIABILITIES AND SHAREHOLDERS' EQUITY

Current liabilities:

Accounts payable 337,009 371,295

Patronage refunds payable in cash 38,485 44,907

Long-term debt due within one year 2,723 2,863

Customer prepayments 109,101 145,299

Other current liabilities 172,851 143,921

Total current liabilities 660,169 708,285

Long-term debt 241,339 262,050

Other long-term liabilities 239,712 161,113

GROWMARK shareholders' equity:

Capital stock 319,866 388,004

Retained earnings 798,385 763,090

Accumulated other comprehensive income/(loss) (96,606) (60,950)

Total GROWMARK shareholders' equity 1,021,645 1,090,144

Non-GROWMARK ownership in subsidiaries 82,988 91,847

Total equity 1,104,633 1,181,991

Total liabilities and equity $ 2,245,853 2,313,439

-1-

August 31, 2016 and 2015

See accompanying notes.

GROWMARK, INC.

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION

($ In Thousands)

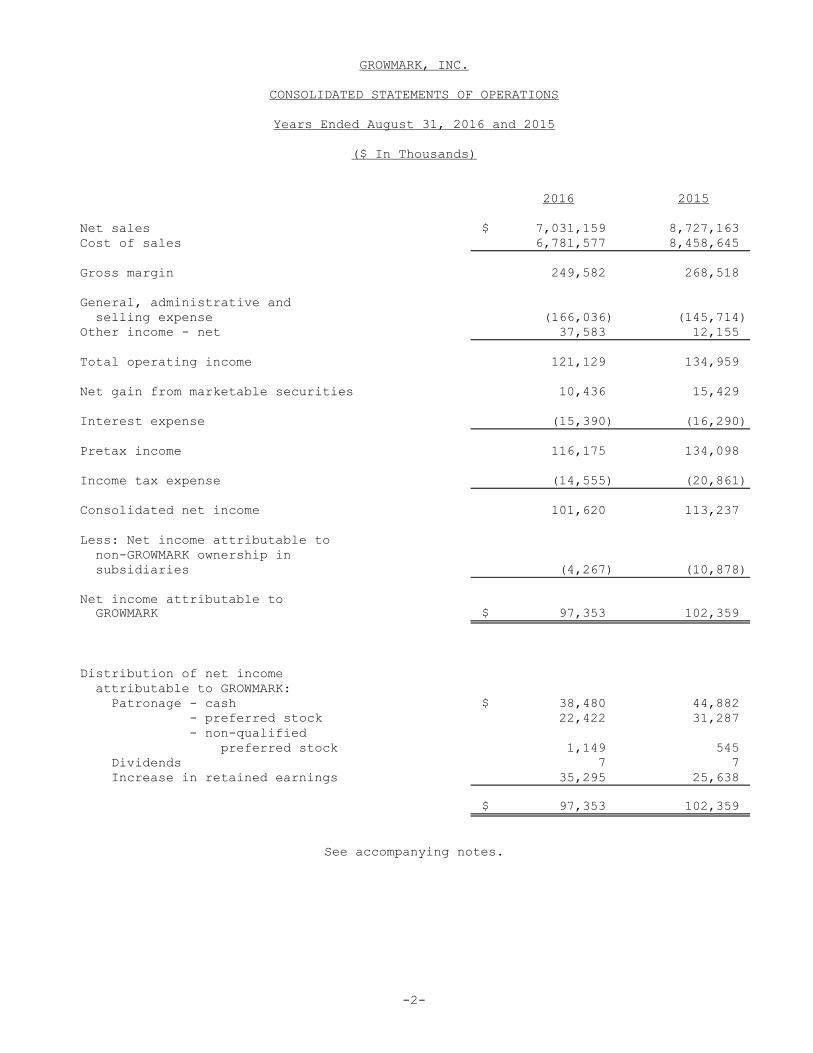

GROWMARK, INC.

CONSOLIDATED STATEMENTS OF OPERATIONS

Years Ended August 31, 2016 and 2015

($ In Thousands)

2016 2015

Net sales $ 7,031,159 8,727,163

Cost of sales 6,781,577 8,458,645

Gross margin 249,582 268,518

General, administrative and

selling expense (166,036) (145,714)

Other income - net 37,583 12,155

Total operating income 121,129 134,959

Net gain from marketable securities 10,436 15,429

Interest expense (15,390) (16,290)

Pretax income 116,175 134,098

Income tax expense (14,555) (20,861)

Consolidated net income 101,620 113,237

Less: Net income attributable to

non-GROWMARK ownership in

subsidiaries (4,267) (10,878)

Net income attributable to

GROWMARK $ 97,353 102,359

Distribution of net income

attributable to GROWMARK:

Patronage - cash $ 38,480 44,882

- preferred stock 22,422 31,287

- non-qualified

preferred stock 1,149 545

Dividends 7 7

Increase in retained earnings 35,295 25,638

$ 97,353 102,359

See accompanying notes.

-2-

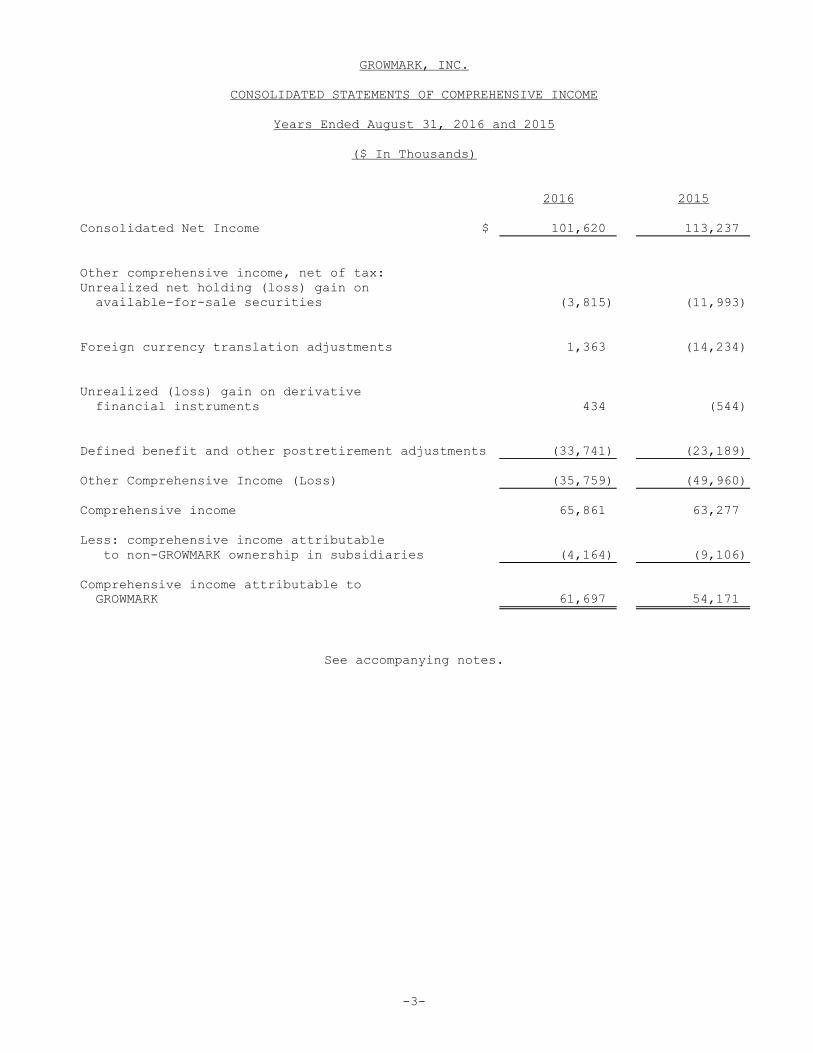

GROWMARK, INC.

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

Years Ended August 31, 2016 and 2015

($ In Thousands)

2016 2015

Consolidated Net Income $ 101,620 113,237

Other comprehensive income, net of tax:

Unrealized net holding (loss) gain on

available-for-sale securities (3,815) (11,993)

Foreign currency translation adjustments 1,363 (14,234)

Unrealized (loss) gain on derivative

financial instruments 434 (544)

Defined benefit and other postretirement adjustments (33,741) (23,189)

Other Comprehensive Income (Loss) (35,759) (49,960)

Comprehensive income 65,861 63,277

Less: comprehensive income attributable

to non-GROWMARK ownership in subsidiaries (4,164) (9,106)

Comprehensive income attributable to

GROWMARK 61,697 54,171

See accompanying notes.

-3-

GROWMARK, INC.

CONSOLIDATED STATEMENTS OF SHAREHOLDERS' EQUITY

Years Ended August 31, 2016 and 2015

($ In Thousands)

GROWMARK

Accumulated

Other Non-GROWMARK

Capital Retained Comprehensive Ownership in

Stock Earnings Income Subsidiaries

Balance at August 31, 2014 $ 393,025 737,452 (12,762) 87,037

Net earnings before patronage refunds 102,358 10,878

Cash dividends on preferred stock (7)

Preferred stock redemption (36,853)

Patronage dividends to be distributed

in cash (44,882)

Patronage dividends to be distributed

in capital stock 31,287 (31,287)

Patronage dividends to be distributed in

non-qualified capital stock 545 (545)

Contributions by owners

Distributions to owners (4,296)

Unrealized net holding loss on

available-for-sale securities

$1,395, net of tax $541 (11,759) (234)

Foreign currency translation adjustments

$(2,363), net of tax $(831) (12,986) (1,248)

Unrealized gain on derivative

financial instruments $3,667

net of tax $1,367 (544)

Defined benefit and other postretirement

plan adjustments $(35,824),

net of tax $(13,701) (22,899) (290)

Balance at August 31, 2015 $ 388,004 763,089 (60,950) 91,847

Net earnings before patronage refunds 97,353 4,267

Cash dividends on preferred stock (7)

Preferred stock redemption (91,709)

Patronage dividends to be distributed

in cash (38,479)

Patronage dividends to be distributed

in capital stock 22,422 (22,422)

Patronage dividends to be distributed in

non-qualified capital stock 1,149 (1,149)

Deconsolidation of subsidiaries (11,375)

Contributions by owners

Distributions to owners (1,648)

Unrealized net holding loss on

available-for-sale securities

$(5,699), net of tax $(2,199) (3,499) (316)

Foreign currency translation adjustments

$2,003, net of tax $734 1,269 94

Unrealized gain on derivative

financial instruments $518

net of tax $84 434

Defined benefit and other postretirement

plan adjustments $(54,972),

net of tax $(21,112) (33,860) 119

Balance at August 31, 2016 $ 319,866 798,385 (96,606) 82,988

319,866 798,385 96,606 82,988

0 0 0 0

2015 2016

Cumulative unrealized holding gains on

available-for-sale securities, net of tax

$10,602 in 2016, $12,801 in 2015 $ 20,469 $ 16,969

Cumulative foreign currency translation

adjustments, net of tax $(6,118) in 2016,

$(6,853) in 2015 (9,824) (8,554)

Cumulative unrealized gains (losses)

on derivative financial instruments, net

of tax $(131) in 2016, $(139) in 2015 (224) 209

Cumulative defined benefit/

postretirement accounting, net of tax

$(65,368) in 2016, $(44,256) in 2015 (71,371) (105,230)

$ (60,950) $ (96,606)

See accompanying notes.

-4-

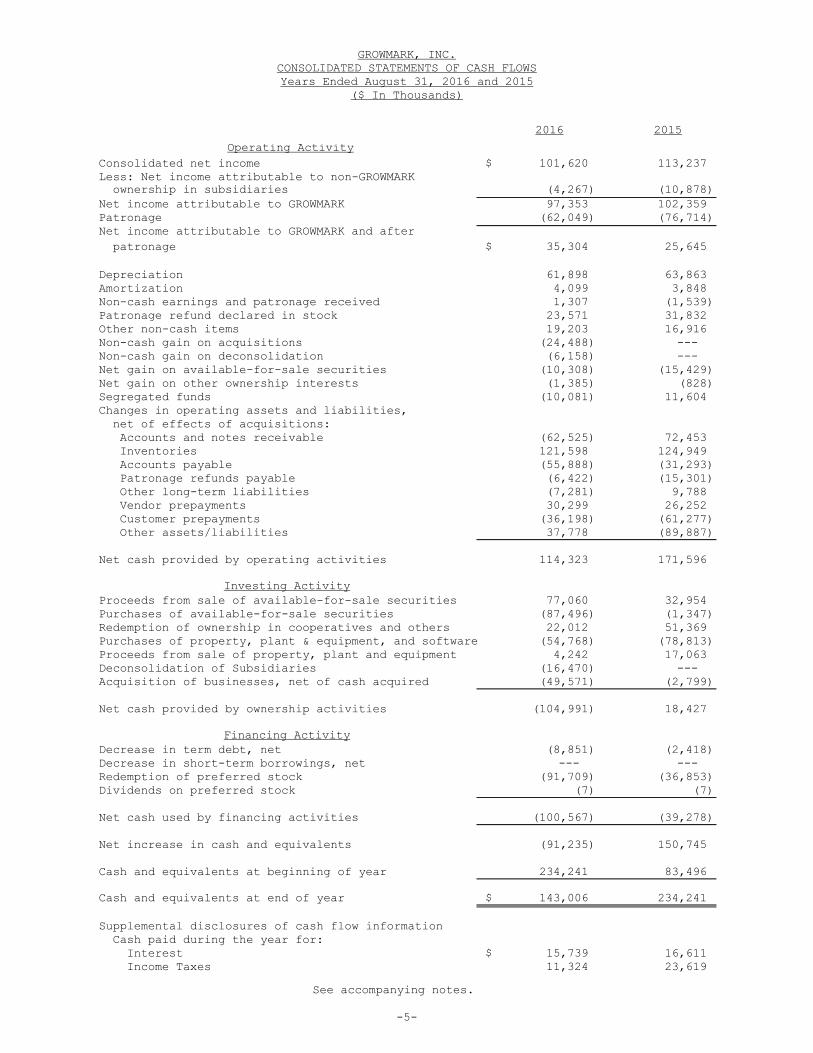

($ In Thousands)

2016 2015

Operating Activity

Consolidated net income $ 101,620 113,237

Less: Net income attributable to non-GROWMARK

ownership in subsidiaries (4,267) (10,878)

Net income attributable to GROWMARK 97,353 102,359

Patronage (62,049) (76,714)

Net income attributable to GROWMARK and after

patronage $ 35,304 25,645

Depreciation 61,898 63,863

Amortization 4,099 3,848

Non-cash earnings and patronage received 1,307 (1,539)

Patronage refund declared in stock 23,571 31,832

Other non-cash items 19,203 16,916

Non-cash gain on acquisitions (24,488) ---

Non-cash gain on deconsolidation (6,158) ---

Net gain on available-for-sale securities (10,308) (15,429)

Net gain on other ownership interests (1,385) (828)

Segregated funds (10,081) 11,604

Changes in operating assets and liabilities,

net of effects of acquisitions:

Accounts and notes receivable (62,525) 72,453

Inventories 121,598 124,949

Accounts payable (55,888) (31,293)

Patronage refunds payable (6,422) (15,301)

Other long-term liabilities (7,281) 9,788

Vendor prepayments 30,299 26,252

Customer prepayments (36,198) (61,277)

Other assets/liabilities 37,778 (89,887)

Net cash provided by operating activities 114,323 171,596

Investing Activity

Proceeds from sale of available-for-sale securities 77,060 32,954

Purchases of available-for-sale securities (87,496) (1,347)

Redemption of ownership in cooperatives and others 22,012 51,369

Purchases of property, plant & equipment, and software (54,768) (78,813)

Proceeds from sale of property, plant and equipment 4,242 17,063

Deconsolidation of Subsidiaries (16,470) ---

Acquisition of businesses, net of cash acquired (49,571) (2,799)

Net cash provided by ownership activities (104,991) 18,427

Financing Activity

Decrease in term debt, net (8,851) (2,418)

Decrease in short-term borrowings, net --- ---

Redemption of preferred stock (91,709) (36,853)

Dividends on preferred stock (7) (7)

Net cash used by financing activities (100,567) (39,278)

Net increase in cash and equivalents (91,235) 150,745

Cash and equivalents at beginning of year 234,241 83,496

Cash and equivalents at end of year $ 143,006 234,241

Supplemental disclosures of cash flow information

Cash paid during the year for:

Interest $ 15,739 16,611

Income Taxes 11,324 23,619

See accompanying notes.

-5-

GROWMARK, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

Years Ended August 31, 2016 and 2015

-6-

GROWMARK, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

August 31, 2016 and 2015

1. Principal accounting policies

a. Organization

GROWMARK, Inc. (the Company) is an agricultural cooperative

corporation operating for the benefit of its common shareholders/

patrons. The Company is primarily a wholesale supplier of

agricultural products operating principally in the Midwestern United

States and the Province of Ontario, Canada. Through certain

divisions/subsidiaries, the Company is a retail supplier in the

Northeastern and Midwestern United States, and Ontario Canada.

Pursuant to its Certificate of Incorporation and Bylaws, Common

Stock shall be issued only to agricultural producers or to

associations of agricultural producers meeting the requirements of

and operating in accordance with the provisions of an Act of

Congress entitled the "Agricultural Marketing Act," as amended (12

U.S.C. § 1141), or an Act of Congress known as the Capper-Volstead

Act (7 U.S.C. § 291), or by cooperatives which serve agricultural

producers, and which are incorporated under and governed by the Co-

operative Corporations Act of Ontario, Canada (R.S.O. 1990 c. C.35),

as amended, or comparable legislation of Canada or another province

of Canada (“Associations of Producers”).

Further, no dividends shall be paid on the common stock. Whenever

full dividends upon all classes of preferred stock at the rate

specified shall have been paid or declared, all remaining earnings

for the year, after providing for such reasonable reserves and

additions to retained earnings as may be determined by the Board of

Directors, shall be distributed and paid in cash, property,

qualified or nonqualified written notices of allocation, patronage

-7-

equity credits, notes, stock or stock credits to the common

shareholders and, at the discretion of the Board of Directors, to

nonmember patrons upon the basis of patronage. In the event of

distribution of retained earnings, such distribution shall be made

to the common shareholders.

b. Consolidation policies

The consolidated financial statements of GROWMARK, Inc. include the

accounts of the parent company and its controlled subsidiaries.

c. Cash and equivalents

Cash and equivalents includes all short-term highly-liquid

negotiable instruments with original maturities of three months or

less.

d. Financial instruments

The Company believes that the carrying value of its financial

instruments, which include cash and equivalents, segregated funds,

accounts receivable, notes receivable and accounts payable,

approximates their fair value based on market rates currently

available for financial instruments with similar terms and remaining

maturities (note 10). The Company has determined it is not

practical to calculate the fair value of debt without incurring

excessive cost to do so. See notes 5 and 6 for disclosure about

fair values of available for sale investments and derivatives,

respectively.

e. Receivables

Receivables are stated net of an allowance for doubtful accounts of

$11.3 million at August 31, 2016 and $11.3 million in 2015. The

Company estimates the allowance based on an aging of the receivables

and an evaluation of the likelihood of success in collecting the

receivables. Aging for delinquency purposes is based on the due

dates and terms of the receivables. Receivables are written off

through a charge to the allowance for doubtful accounts after

reasonable collection efforts have been made and management has

determined collection is doubtful.

-8-

f. Ownership in cooperatives and others

Securities of nonsubsidiary cooperatives which have been purchased

are carried at cost, and securities received as patronage refunds

are carried generally at par value, less adjustments for

impairments. The Company believes it is not practicable to estimate

the fair value of the securities without incurring excessive costs

because there is no established market for these securities and it

is highly subjective to estimate future cash flows which are largely

dependent on future patronage earnings of the nonsubsidiary

cooperatives.

The Company does not reflect its potential equity in the undistri-

buted earnings of nonsubsidiary cooperatives. The Company believes

that it would be entitled to receive portions of the undistributed

earnings of certain nonsubsidiary cooperatives in the event of

liquidation of these cooperatives. However, the amounts which would

be received are subject to various uncertainties and unpredictable

future events, including changes in the share of the business of

these nonsubsidiary cooperatives done with the Company in future

years, the form of any distributions and the taxability thereof, and

legal interpretations as to the methods of computation of the

Company's share of any such future distributions. Such

uncertainties preclude reasonable determination of such amounts

prior to actual liquidation of the nonsubsidiary cooperatives and

resolution of the uncertainties.

Available for sale securities are measured at fair value.

Unrealized holding gains and losses are excluded from earnings and

reported in other comprehensive income until realized.

Non-cooperative equity method investments giving the Company the

ability to exercise significant influence over operating and

financial policies of the investee are accounted for under the

equity method. The Company adjusts the carrying amount of the

investment and recognizes its share of the earnings or losses of the

investee in the periods for which they are reported by the investee.

-9-

g. Accounting for sales-based taxes

The Company follows a policy of accounting for taxes on a net basis

when the tax is assessed by a governmental authority and is both

imposed on and concurrent with revenue-producing transactions.

h. Inventories and cost of sales

In 2016, the Company early adopted ASU 2015-11, Simplifying the

Measurement of Inventory. Inventory within the scope of ASU 2015-11

is measured at the lower of cost and net realizable value. Net

realizable value is the estimated selling prices in the ordinary

course of business, less reasonably predictable costs of completion,

disposal, and transportation. The Company expects the adoption of

ASU 2015-11 to reduce the cost and complexity of valuing inventory

subsequent to its original purchase.

Inventories are valued at the lower of cost or net realizable value

(lower of cost or market in 2015), except for grain which is valued

at market. Cost is determined on the first-in, first-out method.

Patronage refunds are recorded when received and are included in the

Consolidated Statements of Operations primarily as reductions of

cost of sales.

Costs related to the storage, handling and distribution of products

sold by the Company are included in cost of sales.

i. Intangibles

The Company and its subsidiaries have goodwill and other intangible

assets primarily including trademarks, customer lists, and covenants

not to compete (see Note 4). Beginning September 1, 2013, the

Company elected to apply the accounting alternative within

Accounting Standards Codification (ASC) 350 – Intangibles – Goodwill

and Other, allowing private companies to amortize goodwill and use a

simplified one-step impairment test. Goodwill is amortized on a

straight-line basis over 10 years, and is tested for impairment at

the entity level if a triggering event occurs. Previously, goodwill

was tested annually for impairment and not amortized.

-10-

j. Property, plant and equipment

Property, plant and equipment is carried at cost less accumulated

depreciation. Depreciation is determined on the straight-line

method for all assets.

k. Foreign operations

Included in the Company’s Consolidated Statements of Financial

Position at August 31, 2016 and 2015 are the total assets of its

Ontario, Canada operations which total approximately $264 million

($182 million in 2015.)

l. Use of estimates

The preparation of financial statements in conformity with generally

accepted accounting principles in the United States requires

management to make estimates and assumptions that affect the amounts

reported in the financial statements and accompanying notes. Actual

results could differ from these estimates.

m. Subsequent events

Subsequent events have been evaluated through November 1, 2016 which

is the date that the financial statements were available to be

issued.

2. Acquisitions

During 2016, the Company and its subsidiaries acquired various

wholesale and retail businesses in the energy and agronomy sectors

of the agricultural industry. As a result of these acquisitions,

the Company expects to realize revenue growth and increased

earnings. The aggregate purchase price was $50.6 million ($50.3

million paid in cash). The results of these operations have been

included in the consolidated financial statements since the dates of

acquisition.

The acquisitions are accounted for in accordance with the provisions

of ASC 805 Business Combinations. The Company estimated the fair

value of assets and liabilities at the time of acquisition and used

appraisals to assist in determining the fair market value for

acquired tangible assets. These appraisals represent level 2 fair

-11-

value measures.

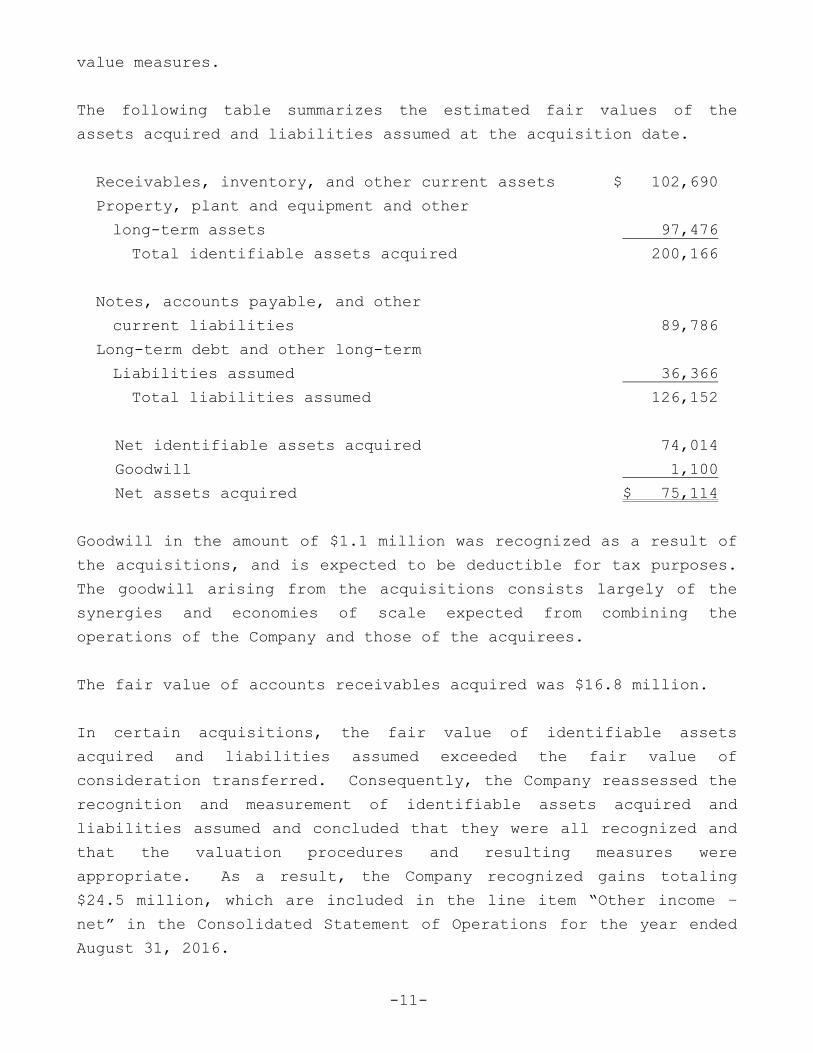

The following table summarizes the estimated fair values of the

assets acquired and liabilities assumed at the acquisition date.

Receivables, inventory, and other current assets $ 102,690

Property, plant and equipment and other

long-term assets 97,476

Total identifiable assets acquired 200,166

Notes, accounts payable, and other

current liabilities 89,786

Long-term debt and other long-term

Liabilities assumed 36,366

Total liabilities assumed 126,152

Net identifiable assets acquired 74,014

Goodwill 1,100

Net assets acquired $ 75,114

Goodwill in the amount of $1.1 million was recognized as a result of

the acquisitions, and is expected to be deductible for tax purposes.

The goodwill arising from the acquisitions consists largely of the

synergies and economies of scale expected from combining the

operations of the Company and those of the acquirees.

The fair value of accounts receivables acquired was $16.8 million.

In certain acquisitions, the fair value of identifiable assets

acquired and liabilities assumed exceeded the fair value of

consideration transferred. Consequently, the Company reassessed the

recognition and measurement of identifiable assets acquired and

liabilities assumed and concluded that they were all recognized and

that the valuation procedures and resulting measures were

appropriate. As a result, the Company recognized gains totaling

$24.5 million, which are included in the line item “Other income –

net” in the Consolidated Statement of Operations for the year ended

August 31, 2016.

-12-

The Company adopted ASU 2014-18 in fiscal 2015, and no longer

recognizes separately from goodwill (1) customer-related intangible

assets unless they are capable of being sold or licensed

independently from the other assets of the business and (2)

noncompetition agreements. Entities electing this accounting

alternative must adopt the private company alternative to amortize

goodwill per ASU 2014-02, which the Company previously adopted.

During 2015, the Company and its subsidiaries acquired wholesale

businesses in the energy industry. The aggregate purchase price was

$2.8 million ($2.8 million paid in cash).

3. Segregated funds

A significant portion of the segregated funds of a subsidiary of the

Company is held in interest-bearing accounts by ADM Investor

Services, Inc., the subsidiary’s principal clearing broker.

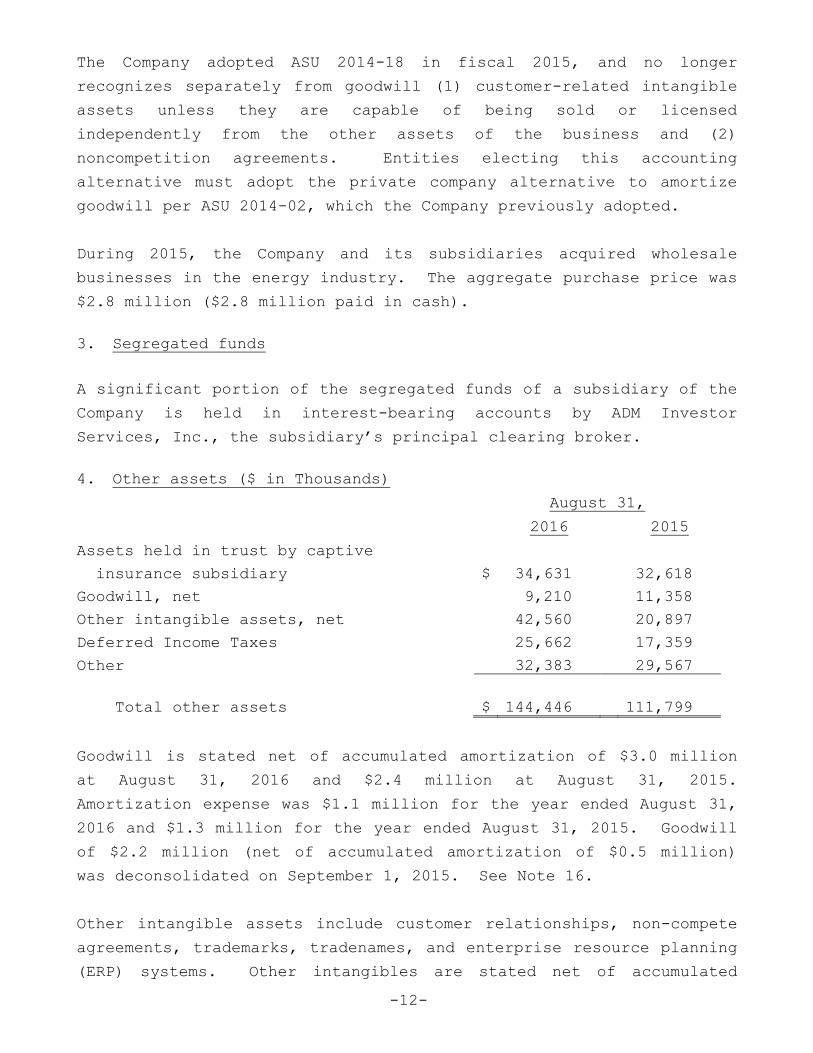

4. Other assets ($ in Thousands)

August 31,

2016 2015

Assets held in trust by captive

insurance subsidiary $ 34,631 32,618

Goodwill, net 9,210 11,358

Other intangible assets, net 42,560 20,897

Deferred Income Taxes

2

0

25,662 17,359

Other 32,383 29,567

Total other assets $ 144,446 111,799

Goodwill is stated net of accumulated amortization of $3.0 million

at August 31, 2016 and $2.4 million at August 31, 2015.

Amortization expense was $1.1 million for the year ended August 31,

2016 and $1.3 million for the year ended August 31, 2015. Goodwill

of $2.2 million (net of accumulated amortization of $0.5 million)

was deconsolidated on September 1, 2015. See Note 16.

Other intangible assets include customer relationships, non-compete

agreements, trademarks, tradenames, and enterprise resource planning

(ERP) systems. Other intangibles are stated net of accumulated

-13-

amortization of $20.5 million at August 31, 2016 and $17.5 million

at August 31, 2015. Amortization expense was $3.0 million for the

year ended August 31, 2016 and $2.5 million for the year ended

August 31, 2015.

The Company began the process of implementing a new enterprise

resource planning (ERP) system during 2015. Capitalized computer

software costs totaled $35.1 million at August 31, 2016 ($11.1

million at August 31, 2015). Amortization of capitalized computer

software costs began in 2016 when the software was ready for use.

Estimated amortization expense for the succeeding five years for

goodwill and other intangibles is ($ in thousands) $7,848 in 2017,

$8,080 in 2018, $7,976 in 2019, $7,957 in 2020, and $7,896 in 2021.

5. Ownership in cooperatives and others

August 31,

($ in Thousands) 2016 2015

Nonsubsidiary cooperatives:

National Cooperative Refinery

Association (NCRA) $ --- 109,492

CHS 24,042 5,034

CoBank, ACB 6,935 6,771

Other cooperatives 9,370 3,390

40,347 124,687

Available-for-sale securities

($53,014 cost at August 31,

2016, $31,795 at August 31,

2015) 79,062 65,329

Non-coop equity method investments:

FS GRAIN, LLC 33,508 ---

UPI, Inc. 12,960 12,925

Other 34,099 34,113

Total ownership in coops and others

199,976 237,054

NCRA reclassified to current assets –

ownership in cooperative

---

(109,492)

( Ownership in coops and others

$ 199,976 127,562

-14-

At August 31, 2016, the gross pre-tax unrealized gains on long-term

available-for-sale securities were $27.6 million (or $17.0 million,

net of $10.6 million of deferred income taxes). The gross pre-tax

unrealized losses on long-term available-for-sale securities were

$1.1 million (or $.7 million, net of $.4 million of deferred income

taxes) at August 31, 2016. At August 31, 2015, the gross pre-tax

unrealized gains on long-term available-for-sale securities were

$33.3 million (or $20.5 million, net of $12.8 million of deferred

income taxes). There were no gross pre-tax unrealized losses on

long-term available-for-sale securities at August 31, 2015.

The gross realized loss on sales of long-term available-for-sale

securities was $1.4 million during 2016 (none in 2015). The gross

realized gain on sales of long-term available-for-sale securities

was $11.8 million as reported in the Statement of Operations for the

year ended August 31, 2016 ($15.4 million in 2015). The cost basis

used to compute the net realized gain on sales was specific

identification for all available-for-sale securities.

During 2012, the Company executed a Stock Transfer Agreement to sell

its National Cooperative Refinery Association (NCRA) shares to CHS,

Inc. (CHS). CHS had the right as majority shareholder to initiate

the process of acquiring full ownership of the refinery operation.

The transition of ownership occurred in four annual installments

beginning September 2012. Each of the first three installments

(September 2012, 2013 and 2014) were for approximately one-fifth of

total holdings and the last installment (in September 2015) was for

the remaining shares held by the Company. The Company did not incur

any loss as a result of the Agreement.

According to terms of the Stock Transfer Agreement, the Company

received par value for the shares sold plus a contingent amount for

each of two years following each sale installment. The contingency

is based on the amount by which average annual refinery margins are

in excess of a specified minimum per barrel, product sales by the

refinery during each fiscal year and on the shares sold. The

proceeds from each installment sale, including the contingent

portion, were recorded at fair value at each closing date. In

subsequent periods, adjustments to amounts recognized for the

-15-

contingent portion will be evaluated pursuant to ASC 450,

Contingencies.

During 2016, the Company recorded a gain on the sale of the fourth

and final installment of $1.9 million ($2.7 million on the third

installment in 2015) which is included in Other income – net in the

Consolidated Statement of Operations. The value of the shares that

were sold in September 2015 ($111.4 million) were classified as

Current assets – Ownership in cooperative.

6. Derivative instruments

($ and Quantities in Thousands, unless stated otherwise)

The Company manages interest rate risk with derivatives designated

in a hedging relationship as cash flow hedges having a maximum term

of 7 months at August 31, 2016. The objective is to minimize the

risk and volatility of interest expense by fixing the interest rate

on a portion of actual or forecasted borrowings. These derivative

instruments may include over-the-counter (OTC) swap and option

contracts. The changes in the market value of such contracts has

historically been, and is expected to continue to be, highly

effective at offsetting changes in expected cash flows on the

underlying floating rate debt and is a component of other

comprehensive income.

Interest rate swaps outstanding at August 31, 2016 hedge $30 million

of projected future variable rate borrowings ($70 million at August

31, 2015). Unrealized gains and losses on interest rate swaps

currently recorded in accumulated other comprehensive income will be

reclassified as a component of interest expense as the derivatives

approach maturity in the same period or periods during which the

hedged transaction affects earnings. The Company anticipates that

approximately $0.1 million will be reclassified to interest expense

within the next twelve months.

The Company also manages some of its overall commodity price risk

with derivatives designated in a hedging relationship as cash flow

hedges having a maximum term of 7 months at August 31, 2016. The

objective is to reduce the variability of cash flows associated with

-16-

the Company’s forecasted purchases and sales of soybeans and corn.

These derivative instruments may include exchange-traded futures and

options contracts. The changes in the market value of such

contracts has historically been, and is expected to continue to be,

highly effective at offsetting changes in the expected cash flows

associated with purchasing and selling the underlying commodity and

is a component of other comprehensive income.

The contract quantity of soybean and wheat futures and options at

August 31, 2016 is (0.2) million bushels (0.8 million bushels in

2015). Unrealized gains and losses on futures and options contracts

currently recorded in accumulated other comprehensive income will be

reclassified as a component of cost of sales as the derivatives

approach maturity in the same period or periods during which the

hedged transaction affects earnings. The Company anticipates that

approximately $(0.4) million will be reclassified to cost of sales

within the next twelve months.

Certain operations and subsidiaries of the Company hold derivative

instruments that have not been designated as hedges, such as

futures, options, forward contracts, and over-the-counter (OTC)

swaps that are believed to provide an economic hedge of overall

price risk of grain, fuel, and fertilizer commodities. The purpose

in holding these derivatives is to reduce the variability of cash

flows associated with forecasted purchases and sales of the

underlying commodities.

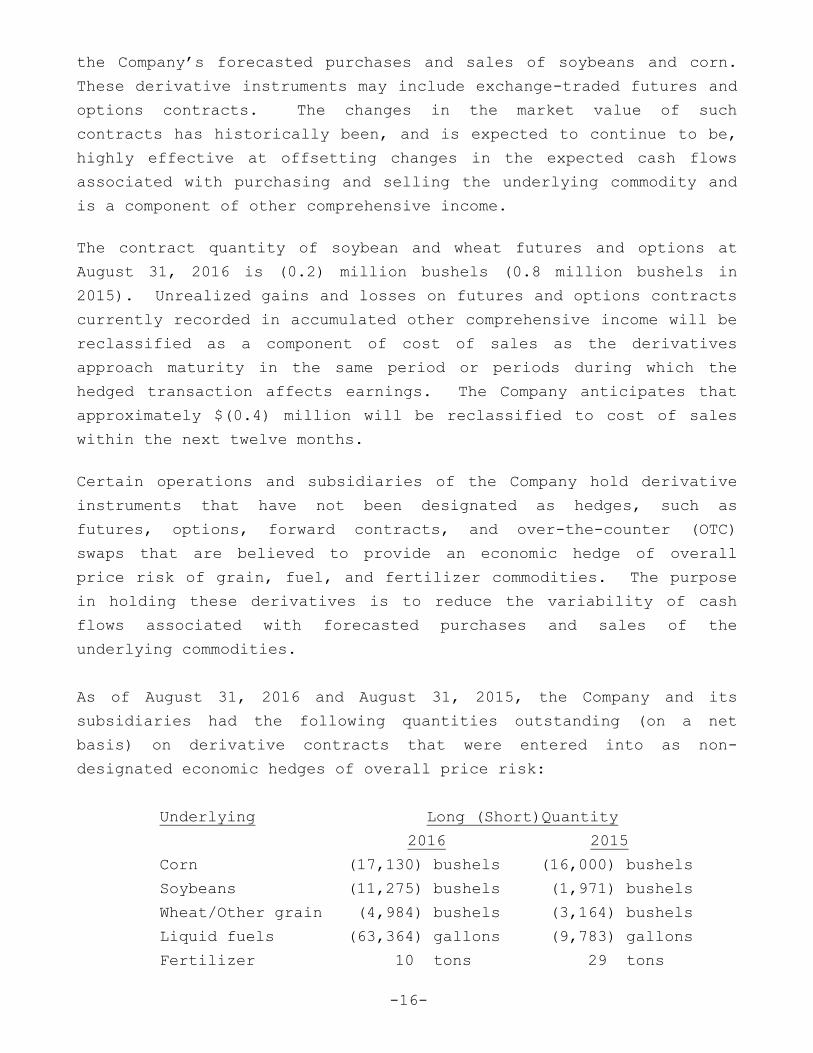

As of August 31, 2016 and August 31, 2015, the Company and its

subsidiaries had the following quantities outstanding (on a net

basis) on derivative contracts that were entered into as non-

designated economic hedges of overall price risk:

Underlying Long (Short)Quantity

2016 2015

Corn (17,130) bushels (16,000) bushels

Soybeans (11,275) bushels (1,971) bushels

Wheat/Other grain (4,984) bushels (3,164) bushels

Liquid fuels (63,364) gallons (9,783) gallons

Fertilizer 10 tons 29 tons

-17-

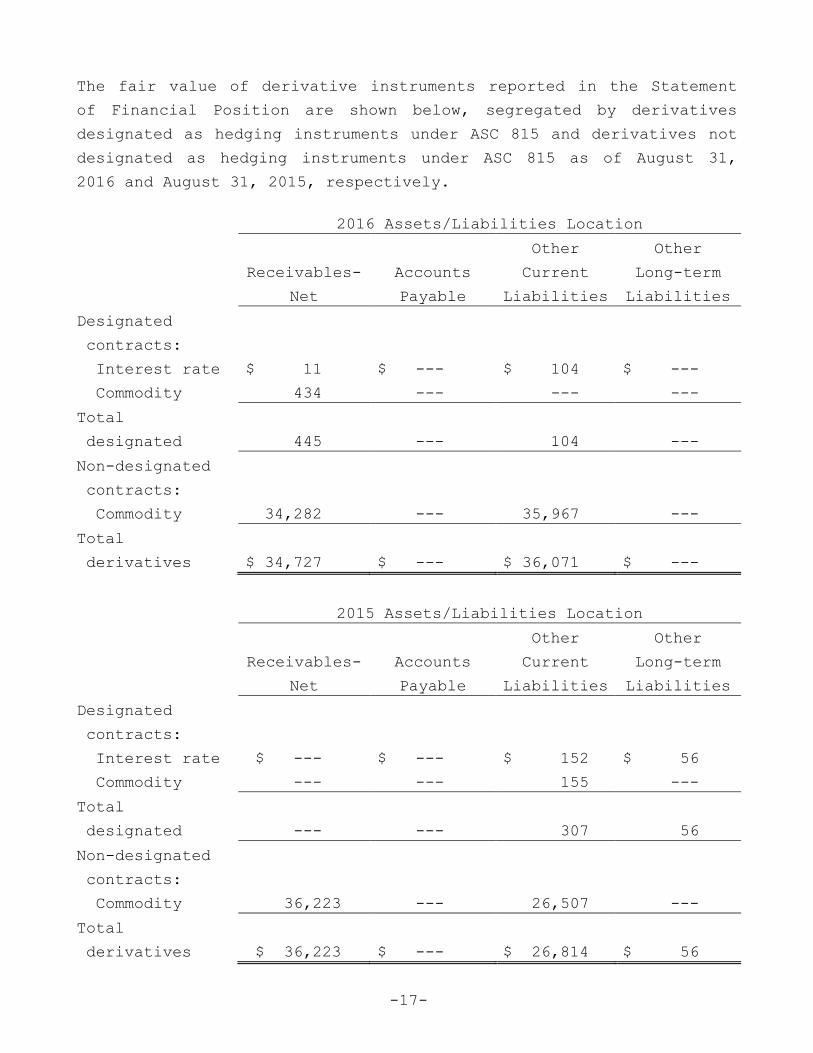

The fair value of derivative instruments reported in the Statement

of Financial Position are shown below, segregated by derivatives

designated as hedging instruments under ASC 815 and derivatives not

designated as hedging instruments under ASC 815 as of August 31,

2016 and August 31, 2015, respectively.

2016 Assets/Liabilities Location

Receivables-

Accounts

Other

Current

Other

Long-term

Net Payable Liabilities Liabilities

Designated

contracts:

Interest rate $ 11 $ --- $ 104 $ ---

Commodity 434 --- --- ---

Total

designated 445 --- 104 ---

Non-designated

contracts:

Commodity 34,282 --- 35,967 ---

Total

derivatives $ 34,727 $ --- $ 36,071 $ ---

2015 Assets/Liabilities Location

Receivables-

Accounts

Other

Current

Other

Long-term

Net Payable Liabilities Liabilities

Designated

contracts:

Interest rate $ --- $ --- $ 152 $ 56

Commodity --- --- 155 ---

Total

designated --- --- 307 56

Non-designated

contracts:

Commodity 36,223 --- 26,507 ---

Total

derivatives $ 36,223 $ --- $ 26,814 $ 56

-18-

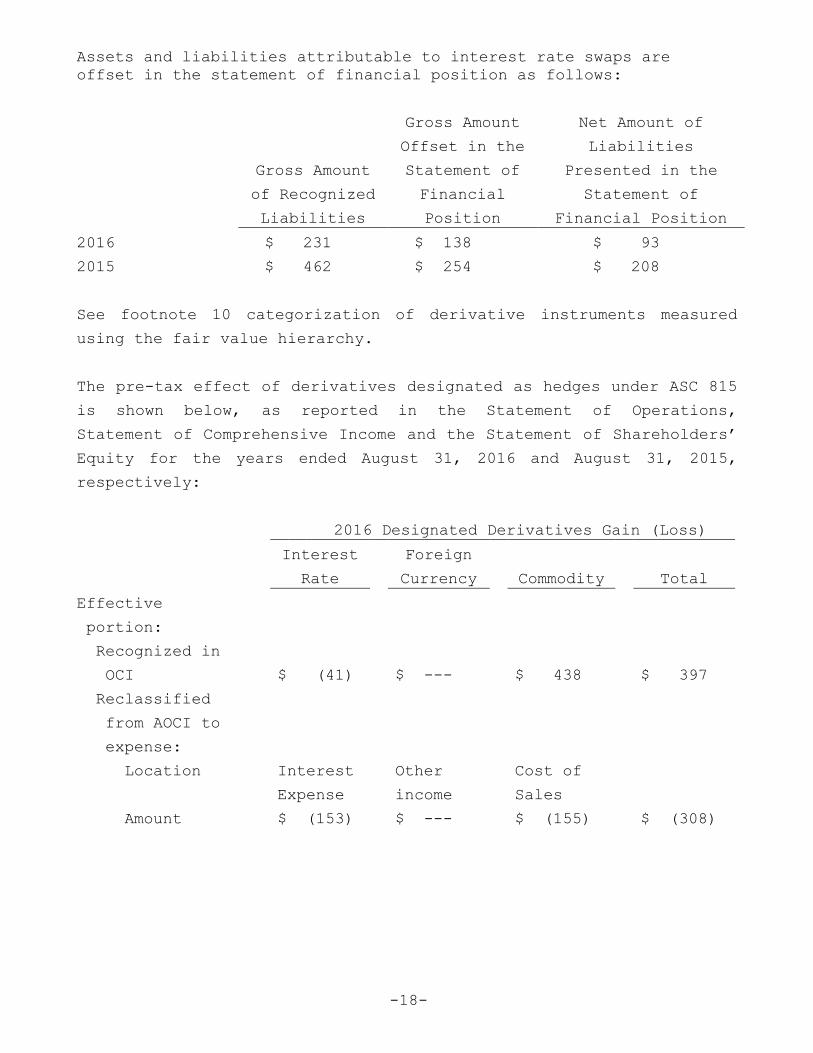

Assets and liabilities attributable to interest rate swaps are

offset in the statement of financial position as follows:

Gross Amount

of Recognized

Liabilities

Gross Amount

Offset in the

Statement of

Financial

Position

Net Amount of

Liabilities

Presented in the

Statement of

Financial Position

2016 $ 231 $ 138 $ 93

2015 $ 462 $ 254 $ 208

See footnote 10 categorization of derivative instruments measured

using the fair value hierarchy.

The pre-tax effect of derivatives designated as hedges under ASC 815

is shown below, as reported in the Statement of Operations,

Statement of Comprehensive Income and the Statement of Shareholders’

Equity for the years ended August 31, 2016 and August 31, 2015,

respectively:

2016 Designated Derivatives Gain (Loss)

Interest Foreign

Rate Currency Commodity Total

Effective

portion:

Recognized in

OCI $ (41) $ --- $ 438 $ 397

Reclassified

from AOCI to

expense:

Location Interest Other Cost of

Expense income Sales

Amount $ (153) $ --- $ (155) $ (308)

-19-

2015 Designated Derivatives Gain (Loss)

Interest Foreign

Rate Currency Commodity Total

Effective

portion:

Recognized in

OCI $ (237) $ --- $ (155) $ (392)

Reclassified

from AOCI to

expense:

Location Interest Other Cost of

expense income Sales

Amount $ (74) $ --- $ 535 $ 461

During 2016 and 2015, immaterial levels of ineffectiveness were

recognized in interest expense.

The effect of derivatives held as economic hedges but not designated

under ASC 815 is shown below, as reported in the Statement of

Operations for the years ended August 31, 2016 and August 31, 2015,

respectively:

Non-Designated Derivatives

Gain (Loss)

Commodity Contracts

2016 2015

Recognized in income:

Location Cost of sales Cost of sales

Amount $ 19,137 $ 99,789

-20-

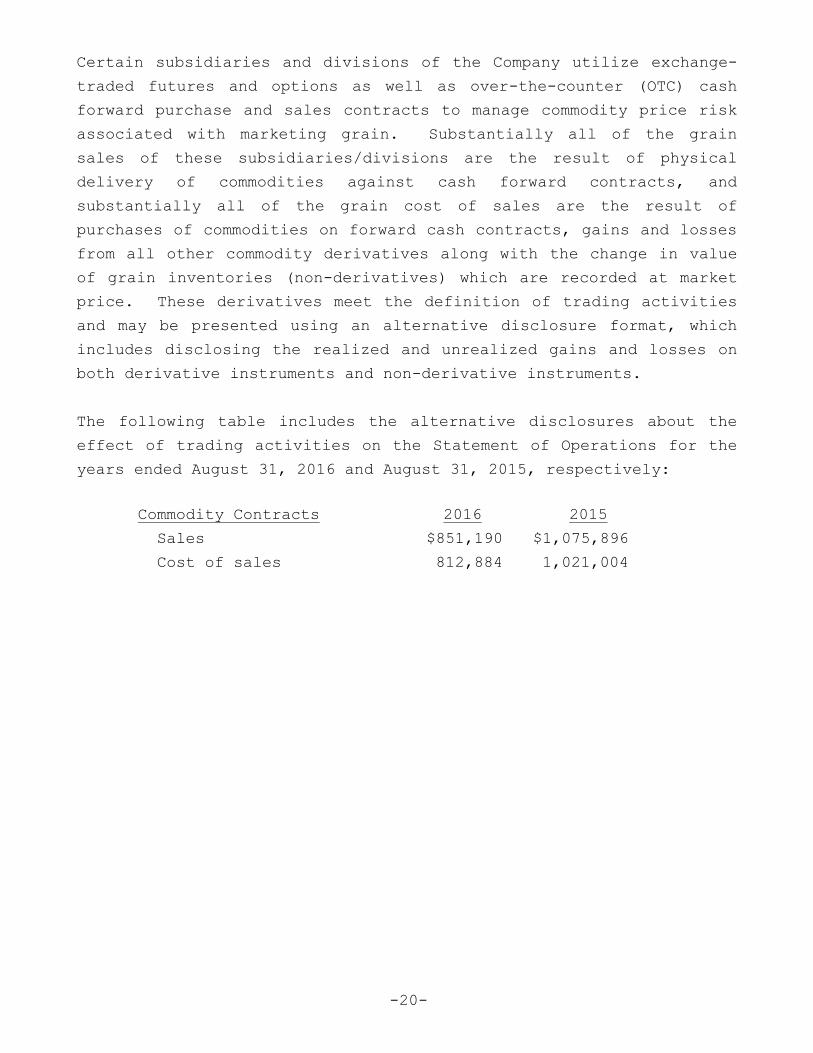

Certain subsidiaries and divisions of the Company utilize exchange-

traded futures and options as well as over-the-counter (OTC) cash

forward purchase and sales contracts to manage commodity price risk

associated with marketing grain. Substantially all of the grain

sales of these subsidiaries/divisions are the result of physical

delivery of commodities against cash forward contracts, and

substantially all of the grain cost of sales are the result of

purchases of commodities on forward cash contracts, gains and losses

from all other commodity derivatives along with the change in value

of grain inventories (non-derivatives) which are recorded at market

price. These derivatives meet the definition of trading activities

and may be presented using an alternative disclosure format, which

includes disclosing the realized and unrealized gains and losses on

both derivative instruments and non-derivative instruments.

The following table includes the alternative disclosures about the

effect of trading activities on the Statement of Operations for the

years ended August 31, 2016 and August 31, 2015, respectively:

Commodity Contracts 2016 2015

Sales $851,190 $1,075,896

Cost of sales 812,884 1,021,004

-21-

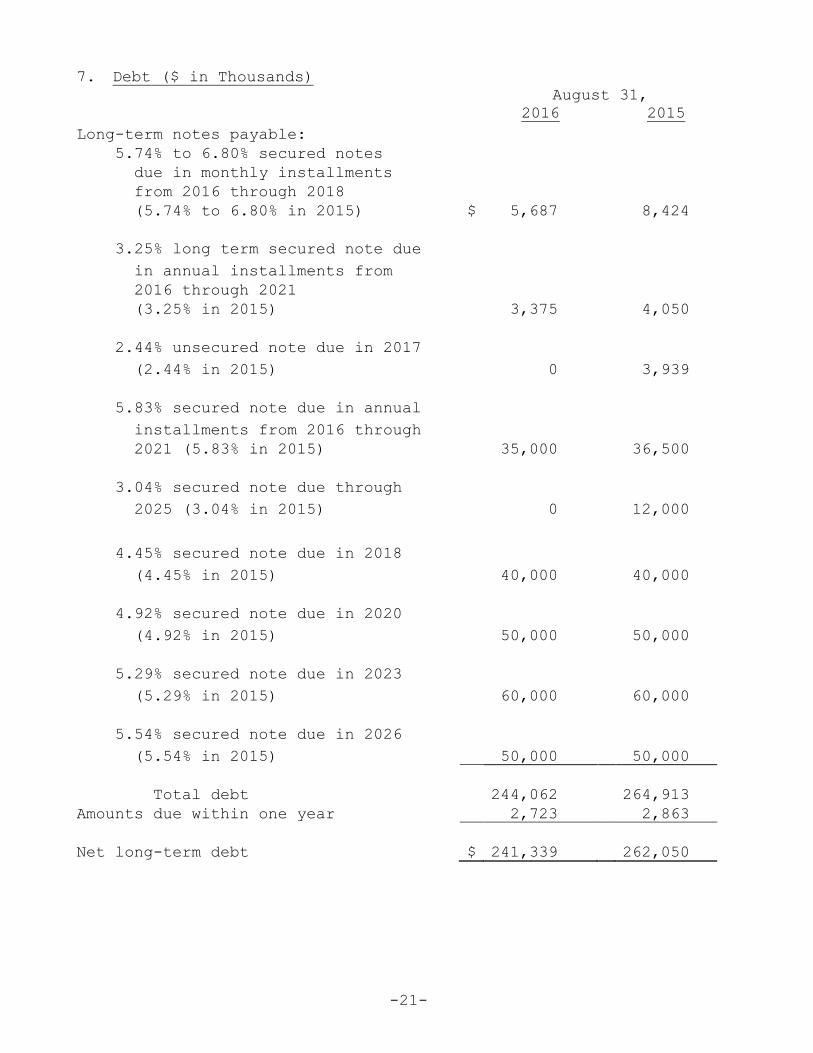

7. Debt ($ in Thousands)

August 31,

2016 2015

Long-term notes payable:

5.74% to 6.80% secured notes

due in monthly installments

from 2016 through 2018

(5.74% to 6.80% in 2015) $ 5,687 8,424

3.25% long term secured note due

in annual installments from

2016 through 2021

(3.25% in 2015)

3,375 4,050

2.44% unsecured note due in 2017

3

3

(2.44% in 2015) 0 3,939

5.83% secured note due in annual

installments from 2016 through

2021 (5.83% in 2015) 35,000 36,500

3.04% secured note due through

2025 (3.04% in 2015) 0 12,000

4.45% secured note due in 2018

(4.45% in 2015) 40,000 40,000

4.92% secured note due in 2020

(4.92% in 2015) 50,000 50,000

5.29% secured note due in 2023

(5.29% in 2015) 60,000 60,000

5.54% secured note due in 2026

(5.54% in 2015) 50,000 50,000

Total debt 244,062 264,913

Amounts due within one year 2,723 2,863

Net long-term debt $ 241,339 262,050

-22-

Long-term debt maturities for the four years succeeding August 31,

2017 are $47.3 million in 2018, $2.2 million in 2019, $52.2 million

in 2020 and $29.7 million in 2021.

During 2016, gross advances on term debt were $48.8 million ($42.5

million in 2015), and gross repayments were $57.6 million ($45.1

million in 2015). Gross advances on short-term debt were $568.9

million in 2015 ($1.4 billion in 2015), and gross repayments were

$568.9 million ($1.4 billion in 2015).

Long-term notes payable of the Company

Long-term notes payable of $5.7 million ($8.4 million at August 31,

2015) are secured by a mortgage or a security agreement of

approximately equal value on certain real property and equipment of

the Company.

During 2011, the Company secured $200 million of long term fixed

rate debt through a private placement. Substantially all of the

Company’s and certain subsidiaries’ current assets, as well as

certain ownership in other companies are pledged as collateral.

These notes expire between 2018 and 2026 and rank pari passu with

the Company’s syndicated short-term line of credit.

The Company has a long-term note payable of $35.0 million with

Metropolitan Life Insurance Company ($36.5 million at August 31,

2015). The note has a fixed rate and is secured by certain public

stock holdings of the Company.

The Company has a fixed rate long-term note payable of $3.4 million

($4.1 million at August 31, 2015) with Nationwide Exchange Services

Corp., which is secured by a mortgage on certain real property.

During 2016, the Company paid in full and terminated an unsecured

variable rate promissory note payable to Central States Enterprises,

LLC ($3.9 million at August 31, 2015).

-23-

Certain covenants of these loans require the Company to maintain a

minimum amount of net worth and working capital, and limit the

amount of debt and direct or contingent obligations.

Short-term notes payable of the Company

The Company has secured short-term lines of credit extending to June

2020 totaling $600.0 million at August 31, 2016 ($600.0 million at

August 31, 2015). At August 31, 2016, there were no borrowings

outstanding at variable rates (none at August 31, 2015).

Substantially all of the Company’s and certain subsidiaries’ current

assets and certain ownership in other companies are security under a

syndicated credit facility agreement for this short-term line of

credit. On June 12, 2015, a second amendment to the short-term

credit agreement was executed. The Company reduced the cost of

borrowing, enhanced operational flexibility, and extended the

maturity from August 2017 to June 2020. These lines of credit rank

pari passu with the Company’s long term fixed rate private placement

debt.

During 2016, the Company paid in full and terminated a $25 million

short-term note payable with Wells Fargo. The note had no

borrowings outstanding at August 31, 2015 was secured by certain

public stock holdings of the Company.

Consolidated non-recourse long-term notes payable

At August 31, 2016, a subsidiary (Total Grain Marketing, LLC, or

TGM) of the Company has a long-term revolving note payable with

CoBank (non-recourse to the Company), with a total capacity of $15

million and no borrowings outstanding at August 31, 2016. At August

31, 2015, a subsidiary (Total Grain Marketing, LLC, or TGM) of the

Company had two long-term revolving notes payable defined as

“Reducing Revolving A” and “Reducing Revolving B” (non-recourse to

the Company), each in a syndicated bank agreement with CoBank as

Administrative Agent. The capacity of the notes was $30 million in

Reducing Revolving A and $20 million in Reducing Revolving B. No

borrowings were outstanding at August 31, 2015. The notes are

collateralized by a first mortgage on TGM’s facilities, security

agreement, assignment of leases and rents and fixture filing, and

-24-

are not cross- collateralized with assets of the Company.

At August 31, 2016, a subsidiary (WESTERN GRAIN MARKETING, LLC, or

WGM) of the Company has a long-term revolving note payable with

CoBank (non-recourse to the Company), with a total capacity of $17.8

million and no borrowings outstanding at August 31, 2016 ($17.8

million capacity and no borrowings outstanding at August 31, 2015).

The note is collateralized by a security agreement and mortgages

covering all assets of the subsidiary and is not cross-

collateralized with assets of the Company.

In 2016, a subsidiary (NORTHERN GRAIN MARKETING, LLC, or NGM) was

deconsolidated. At August 31, 2015, NGM had a long-term revolving

note payable with CoBank (non-recourse to the Company), with a total

capacity of $12.0 million and no borrowings outstanding.

In 2016, a subsidiary (EASTERN GRAIN MARKETING, LLC, or EGM) of the

Company was deconsolidated. August 31, 2015, EGM had a long-term

revolving note payable with CoBank (non-recourse to the Company),

with a total capacity of $16.0 million and $12.0 million

outstanding.

Consolidated non-recourse short-term notes payable

At August 31, 2016, a subsidiary (TGM) of the Company has a short-

term line of credit of $160.0 million ($200.0 million at August 31,

2015) with CoBank (a syndication led by CoBank in 2015) that is

collateralized by a security agreement covering personal property of

TGM (not cross collateralized with assets of the Company) and is

used to finance business operations with no borrowings outstanding

at August 31, 2016 (none at August 31, 2015).

At August 31, 2016, a subsidiary (WGM) of the Company has a short-

term line of credit of $35.0 million ($50.0 million at August 31,

2015) with CoBank that is collateralized by a security agreement

covering all assets of WGM (not cross-collateralized with assets of

the Company) and is used to finance business operations with no

borrowings outstanding at August 31, 2016 (none at August 31, 2015).

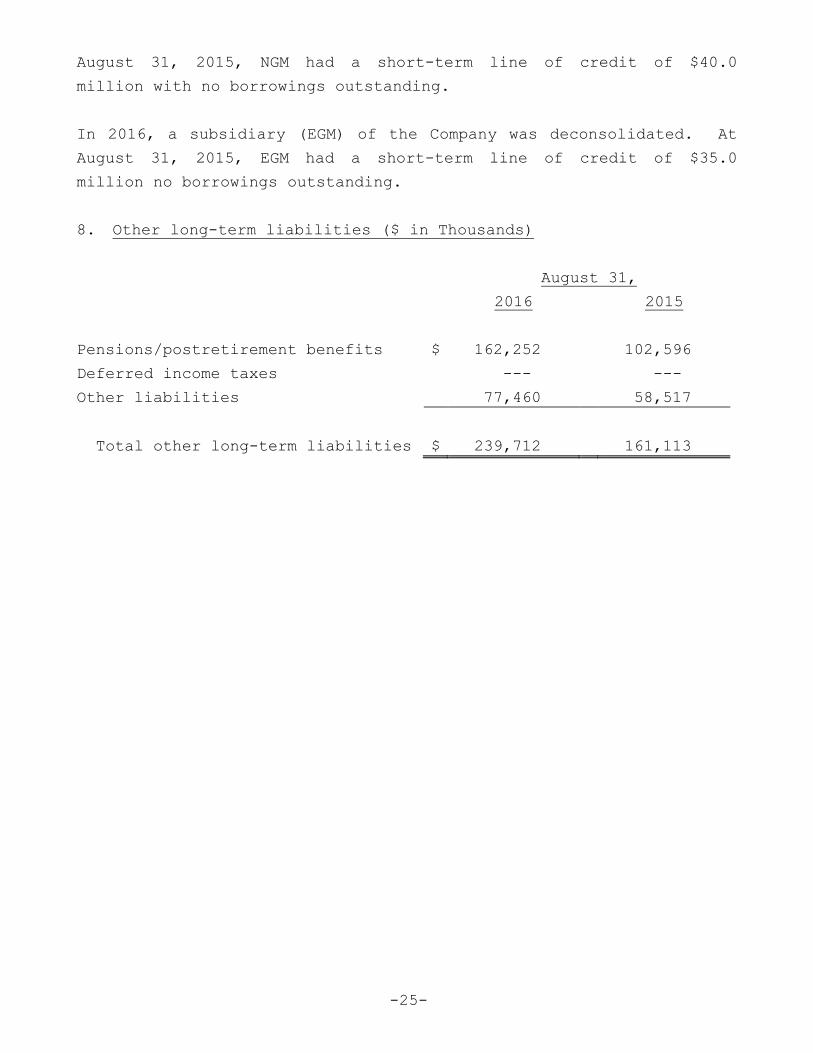

In 2016, a subsidiary (NGM) of the Company was deconsolidated. At

-25-

August 31, 2015, NGM had a short-term line of credit of $40.0

million with no borrowings outstanding.

In 2016, a subsidiary (EGM) of the Company was deconsolidated. At

August 31, 2015, EGM had a short-term line of credit of $35.0

million no borrowings outstanding.

8. Other long-term liabilities ($ in Thousands)

August 31,

2016 2015

Pensions/postretirement benefits $ 162,252 102,596

Deferred income taxes --- ---

Other liabilities 77,460 58,517

Total other long-term liabilities $ 239,712 161,113

-26-

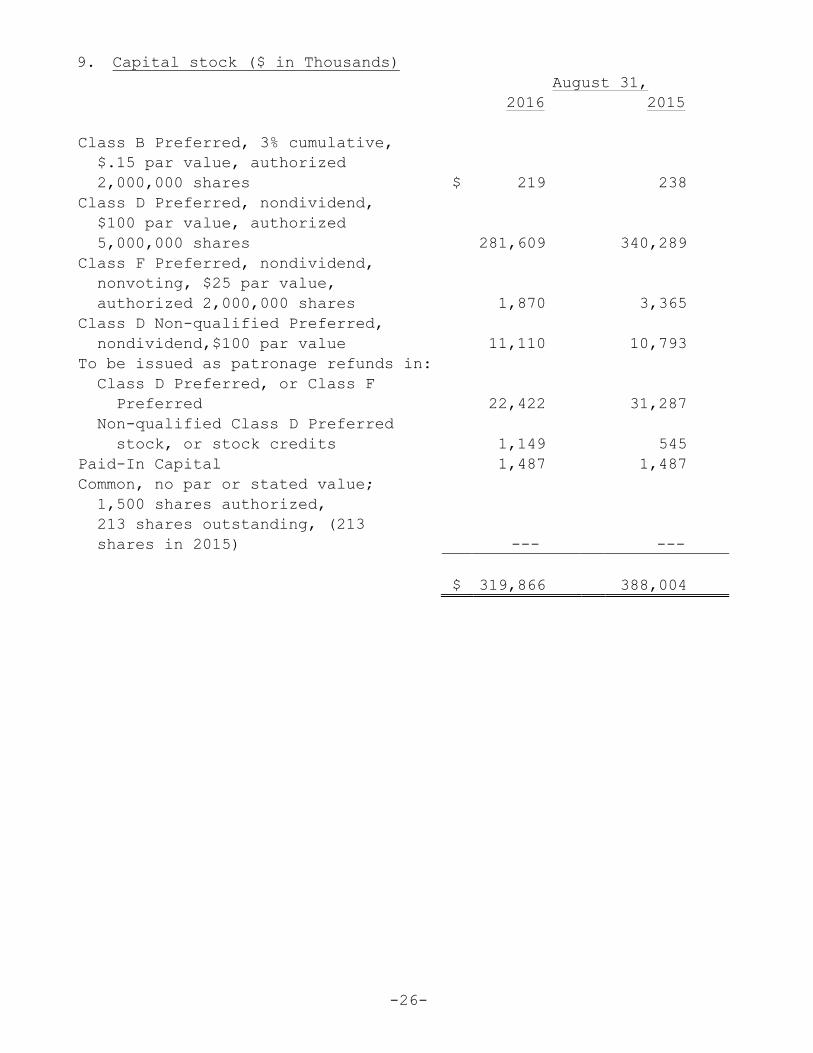

9. Capital stock ($ in Thousands)

August 31,

2016

2015

Class B Preferred, 3% cumulative,

$.15 par value, authorized

2,000,000 shares $ 219

238

Class D Preferred, nondividend,

$100 par value, authorized

5,000,000 shares

281,609

340,289

Class F Preferred, nondividend,

nonvoting, $25 par value,

authorized 2,000,000 shares

1,870

3,365

Class D Non-qualified Preferred,

nondividend,$100 par value

11,110

10,793

To be issued as patronage refunds in:

Class D Preferred, or Class F

Preferred

22,422

31,287

Non-qualified Class D Preferred

stock, or stock credits

1,149

545

Paid-In Capital

1,487

1,487

Common, no par or stated value;

1,500 shares authorized,

213 shares outstanding, (213

shares in 2015)

---

---

$ 319,866 388,004

-27-

10. Fair value measurements ($ in Thousands)

Assets and liabilities recorded at fair value on the balance sheets

are categorized based upon the level of judgment associated with the

inputs used to measure their fair values. That framework provides a

fair value hierarchy that prioritizes the inputs to valuation

techniques used to measure fair value. The hierarchy gives the

highest priority to unadjusted quoted prices in active markets for

identical assets or liabilities (level 1 measurements) and the

lowest priority to unobservable inputs (level 3 measurements). The

three levels of the fair value hierarchy under ASC 820 are described

below:

Level 1 – Inputs to the valuation methodology are unadjusted quoted

prices for identical assets or liabilities in active markets that

the Company has the ability to access.

Level 2 – Inputs to the valuation methodology include:

Quoted prices for similar assets or liabilities in active

markets;

Quoted prices for identical or similar assets or liabilities in

inactive markets;

Inputs other than quoted prices that are observable for the

asset or liability;

Inputs that are derived principally from or corroborated by

observable market data by correlation or other means.

If the asset or liability has a specified (contractual) term, the

Level 2 input must be observable for substantially the full term of

the asset or liability.

Level 3 – Inputs to the valuation methodology are unobservable and

significant to the fair value measurement.

-28-

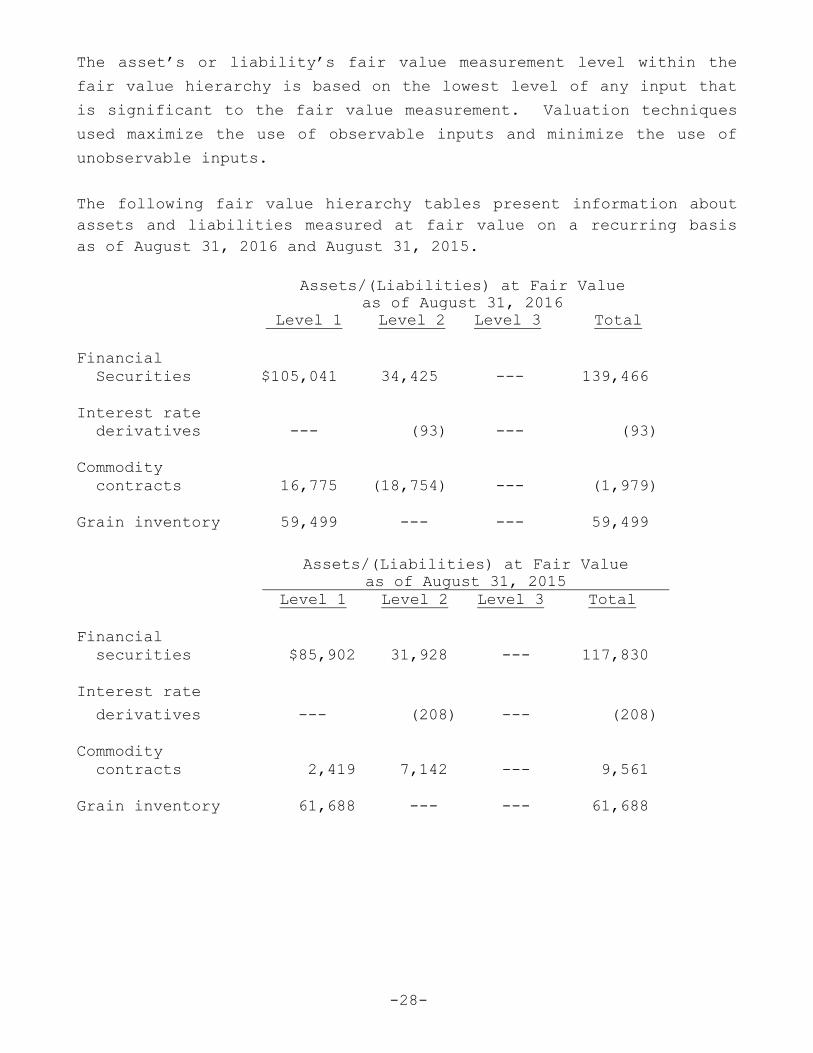

The asset’s or liability’s fair value measurement level within the

fair value hierarchy is based on the lowest level of any input that

is significant to the fair value measurement. Valuation techniques

used maximize the use of observable inputs and minimize the use of

unobservable inputs.

The following fair value hierarchy tables present information about

assets and liabilities measured at fair value on a recurring basis

as of August 31, 2016 and August 31, 2015.

Assets/(Liabilities) at Fair Value

as of August 31, 2016

Level 1 Level 2 Level 3 Total

Financial

Securities $105,041 34,425 --- 139,466

Interest rate

derivatives --- (93) --- (93)

Commodity

contracts 16,775 (18,754)

--

--- (1,979)

Grain inventory 59,499 --- ---

61

59,499

Assets/(Liabilities) at Fair Value

as of August 31, 2015

Level 1 Level 2 Level 3 Total

Financial

securities $85,902

$118,451

118,451

31,928 --- 117,830

Interest rate

derivatives --- (208) --- (208)

Commodity

contracts 2,419 7,142 --- 9,561

Grain inventory 61,688 --- --- 61,688

-29-

The valuation of financial assets and liabilities classified in

Level 2 is determined using a market approach based upon quoted

prices for similar assets and liabilities in active markets, or

other inputs that are observable for substantially the full term of

the financial instrument. For additional required disclosures

regarding the Company’s use of derivative instruments see footnote

6.

11. Income taxes ($ in Thousands)

At August 31, 2016, the Company and its subsidiaries have total net

deferred tax assets of $26.7 million ($19.8 million net deferred tax

asset at August 31, 2015) with deferred assets totaling $125.3

million and deferred liabilities totaling $98.6 million ($98.9

million and $79.1 million at August 31, 2015, respectively).

The deferred items include temporary differences related to

accounting methods being used for financial accounting that differ

from those used for tax accounting. The types of differences

include items such as bad debt expense, depreciation of property,

plant and equipment, pension cost, postretirement health benefit

cost, and the unrealized gain on available-for-sale securities.

The following table identifies key components of income tax expense:

Years Ended August 31,

2016 2015

Current tax expense $ 4,488 19,385

Deferred tax expense 10,067 1,476

$ 14,555 20,861

-30-

The Company and its subsidiaries are subject to income tax filing

requirements imposed by the federal, state, and provincial taxing

authorities in the United States and Canada. Income tax returns

filed, or to be filed, by the Company and its U.S. subsidiaries are

subject to examination by the U.S. federal, state and local taxing

authorities for tax years ending after August 31, 2008. The income

tax returns filed, or to be filed, by the Company and its foreign

subsidiaries are subject to examination by the Canadian and

provincial taxing authorities for tax years ending after August 31,

2008.

The Company and its subsidiaries recognize interest and penalty

expense, if any, in its provision for income taxes. Interest

expense related to unrecognized tax benefits in the Consolidated

Statement of Operations is immaterial for the years ended August 31,

2016 and August 31, 2015. The Company and its subsidiaries do not

expect that the total amounts of unrecognized tax benefits will

significantly increase or decrease during the next twelve months.

The effective income tax rate for fiscal 2016 and 2015 is less than

the statutory rate, primarily due to the issuance of patronage

refunds, which are deductible for tax purposes but treated as a

distribution for financial reporting purposes.

-31-

12. Pensions and postretirement health benefits ($ in Thousands)

The pension and health benefits measurements below are based on an

August 31 valuation date.

U.S. defined benefit plans:

Pension Health Benefits

August 31, August 31,

2016 2015 2016 2015

Total plan assets $468,526 411,433 --- ---

Total projected

benefit

obligation 606,303 489,070 26,894 27,565

Funded status $(137,777) (77,637) (26,894) (27,565)

Accumulated

benefit

obligation $542,639 441,076 --- ---

Pension Health Benefits

Years Ended August

31,

Years Ended August 31,

2016 2015 2016 2015

Service cost $ 14,733 $ 14,401 105 164

Interest cost 22,889 20,170 1,227 1,126

Expected return

on plan assets (27,631) (30,486)

(26,180)

--- ---

Net amortization 8,683 4,603 (199) (711)

Settlement

loss/(gain)

(410) --- --- 114

Benefit cost $ 18,264 $ 8,689 1,133 693

Benefits paid 17,896 15,095 896 935

Premiums paid by

company --- --- 896 935

Employer

contribution 24,539 13,702 --- ---

-32-

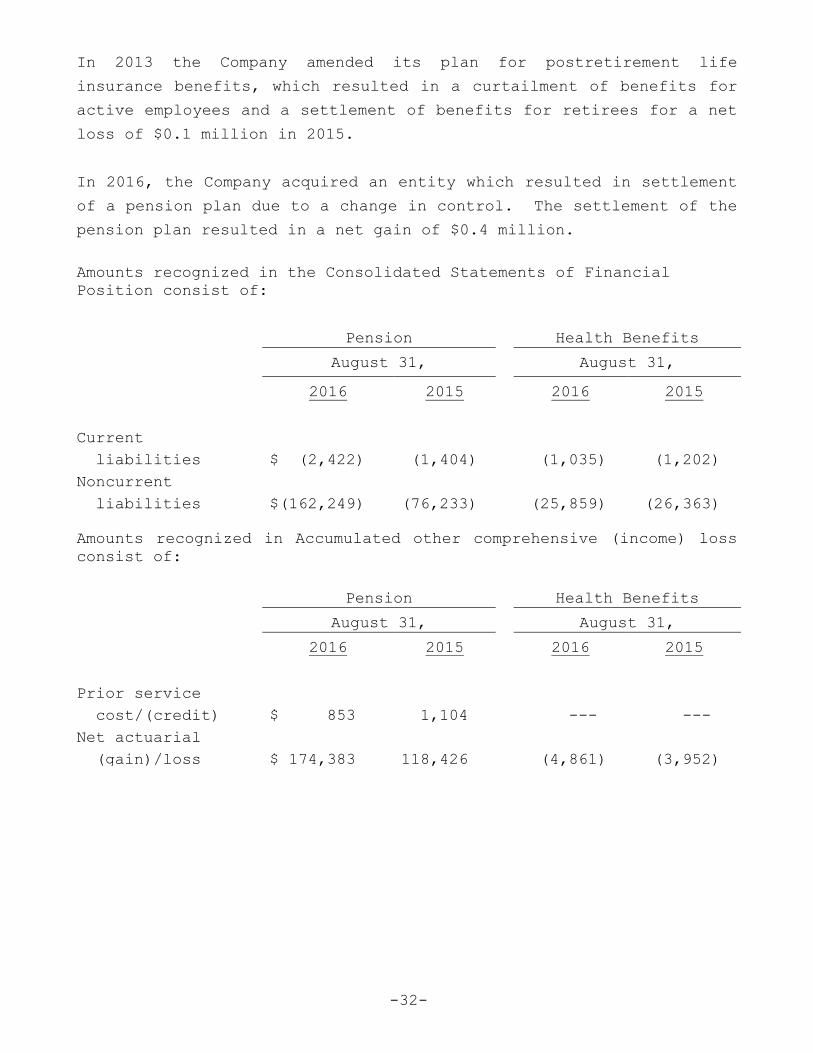

In 2013 the Company amended its plan for postretirement life

insurance benefits, which resulted in a curtailment of benefits for

active employees and a settlement of benefits for retirees for a net

loss of $0.1 million in 2015.

In 2016, the Company acquired an entity which resulted in settlement

of a pension plan due to a change in control. The settlement of the

pension plan resulted in a net gain of $0.4 million.

Amounts recognized in the Consolidated Statements of Financial

Position consist of:

Pension Health Benefits

August 31, August 31,

2016 2015 2016 2015

Current

liabilities $ (2,422) (1,404) (1,035) (1,202)

Noncurrent

liabilities $(162,249) (76,233) (25,859) (26,363)

Amounts recognized in Accumulated other comprehensive (income) loss

consist of:

Pension Health Benefits

August 31, August 31,

2016 2015 2016 2015

Prior service

cost/(credit) $ 853 1,104 --- ---

Net actuarial

(gain)/loss $ 174,383 118,426 (4,861) (3,952)

-33-

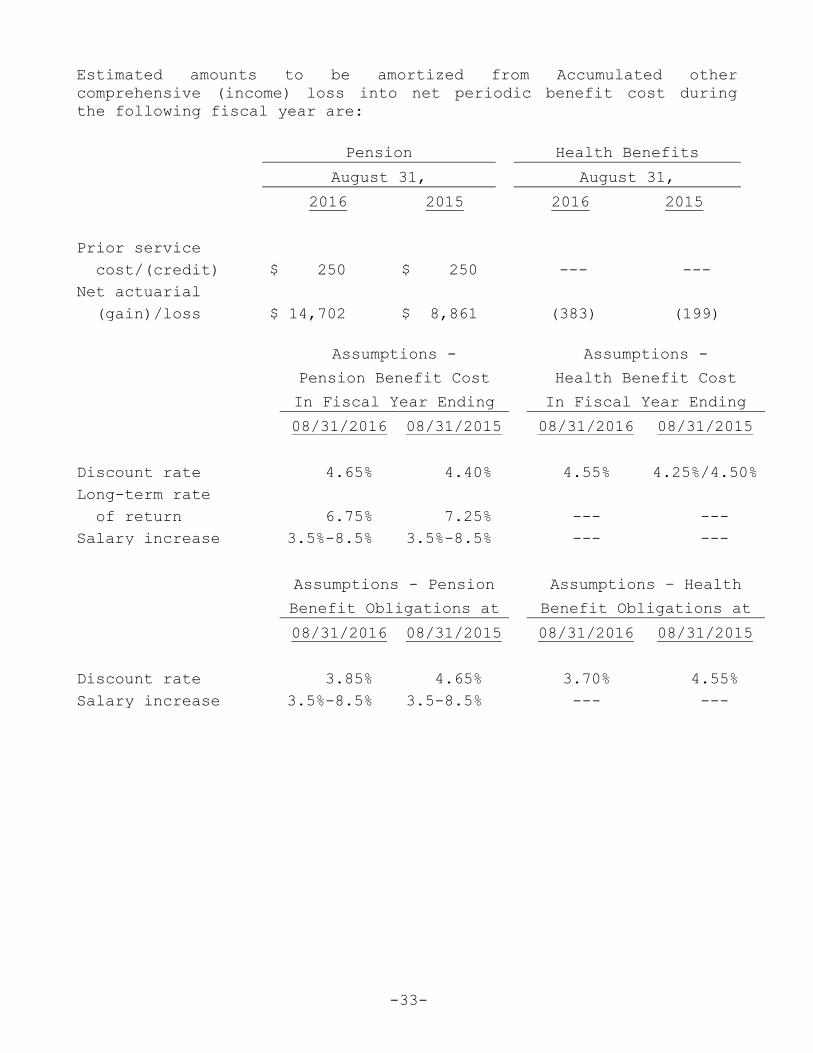

Estimated amounts to be amortized from Accumulated other

comprehensive (income) loss into net periodic benefit cost during

the following fiscal year are:

Pension Health Benefits

August 31, August 31,

2016 2015 2016 2015

Prior service

cost/(credit) $ 250 $ 250 --- ---

Net actuarial

(gain)/loss $ 14,702 $ 8,861 (383) (199)

Assumptions - Assumptions -

Pension Benefit Cost Health Benefit Cost

In Fiscal Year Ending In Fiscal Year Ending

08/31/2016 08/31/2015 08/31/2016 08/31/2015

Discount rate 4.65% 4.40% 4.55% 4.25%/4.50%

Long-term rate

of return 6.75% 7.25% --- ---

Salary increase 3.5%-8.5% 3.5%-8.5% --- ---

Assumptions - Pension Assumptions – Health

Benefit Obligations at Benefit Obligations at

08/31/2016 08/31/2015 08/31/2016 08/31/2015

Discount rate 3.85% 4.65% 3.70% 4.55%

Salary increase 3.5%-8.5% 3.5-8.5% --- ---

-34-

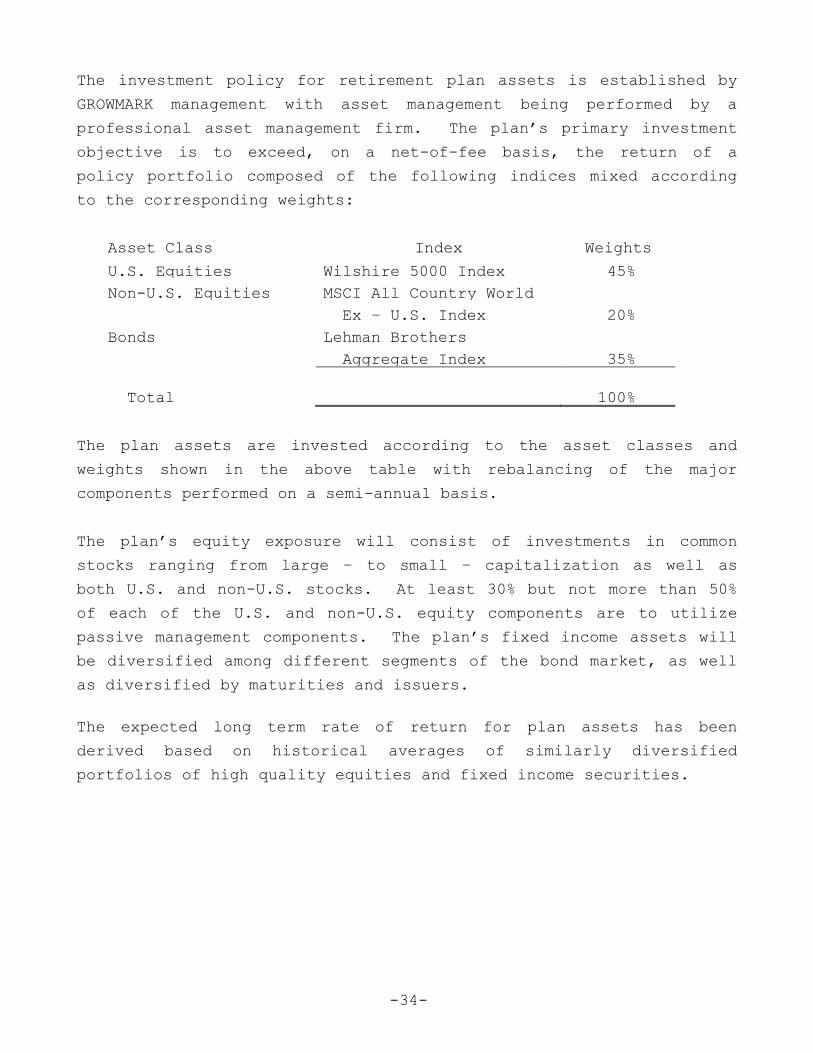

The investment policy for retirement plan assets is established by

GROWMARK management with asset management being performed by a

professional asset management firm. The plan’s primary investment

objective is to exceed, on a net-of-fee basis, the return of a

policy portfolio composed of the following indices mixed according

to the corresponding weights:

Asset Class Index Weights

(%) U.S. Equities Wilshire 5000 Index 45%

Non-U.S. Equities MSCI All Country World

Ex – U.S. Index 20%

Bonds Lehman Brothers

Aggregate Index 35%

Total 100%

The plan assets are invested according to the asset classes and

weights shown in the above table with rebalancing of the major

components performed on a semi-annual basis.

The plan’s equity exposure will consist of investments in common

stocks ranging from large – to small – capitalization as well as

both U.S. and non-U.S. stocks. At least 30% but not more than 50%

of each of the U.S. and non-U.S. equity components are to utilize

passive management components. The plan’s fixed income assets will

be diversified among different segments of the bond market, as well

as diversified by maturities and issuers.

The expected long term rate of return for plan assets has been

derived based on historical averages of similarly diversified

portfolios of high quality equities and fixed income securities.

-35-

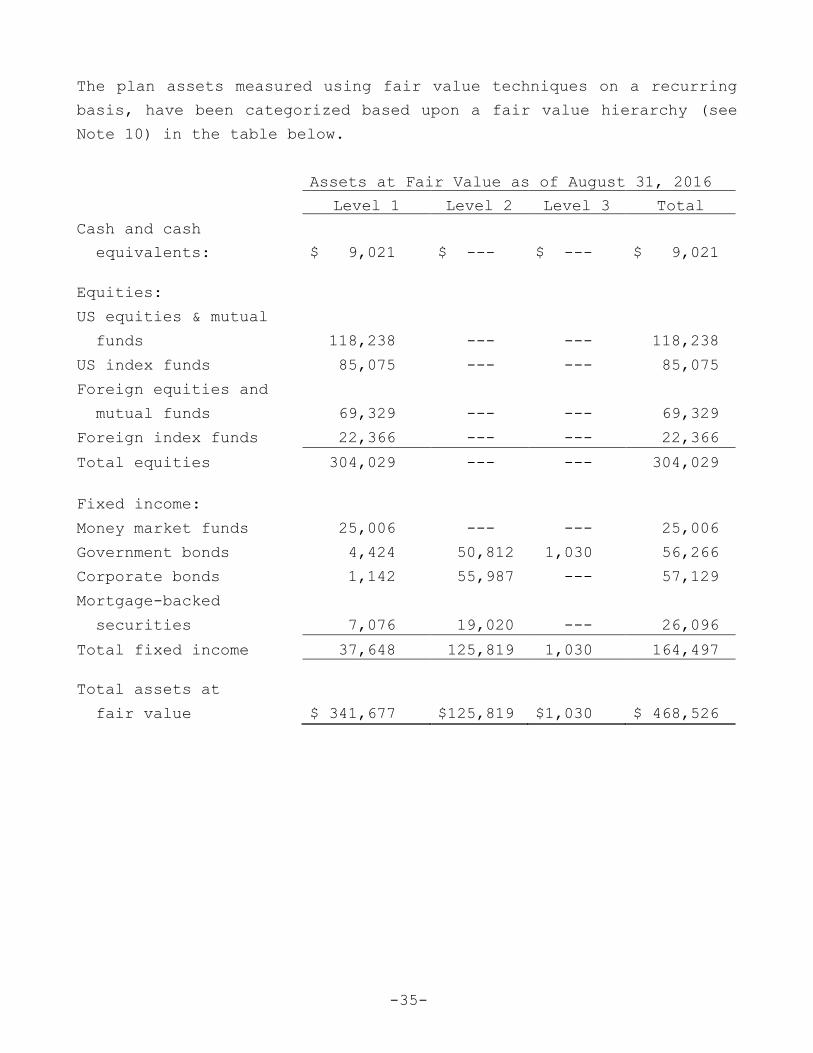

The plan assets measured using fair value techniques on a recurring

basis, have been categorized based upon a fair value hierarchy (see

Note 10) in the table below.

Assets at Fair Value as of August 31, 2016

Level 1 Level 2 Level 3 Total

Cash and cash

equivalents: $ 9,021 $ --- $ --- $ 9,021

Equities:

US equities & mutual

funds 118,238 --- --- 118,238

US index funds 85,075 --- --- 85,075

Foreign equities and

mutual funds 69,329 --- --- 69,329

Foreign index funds 22,366 --- --- 22,366

Total equities 304,029 --- --- 304,029

Fixed income:

Money market funds 25,006 --- --- 25,006

Government bonds 4,424 50,812 1,030 56,266

Corporate bonds 1,142 55,987 --- 57,129

Mortgage-backed

securities 7,076 19,020 --- 26,096

Total fixed income 37,648 125,819 1,030 164,497

Total assets at

fair value $ 341,677 $125,819 $1,030 $ 468,526

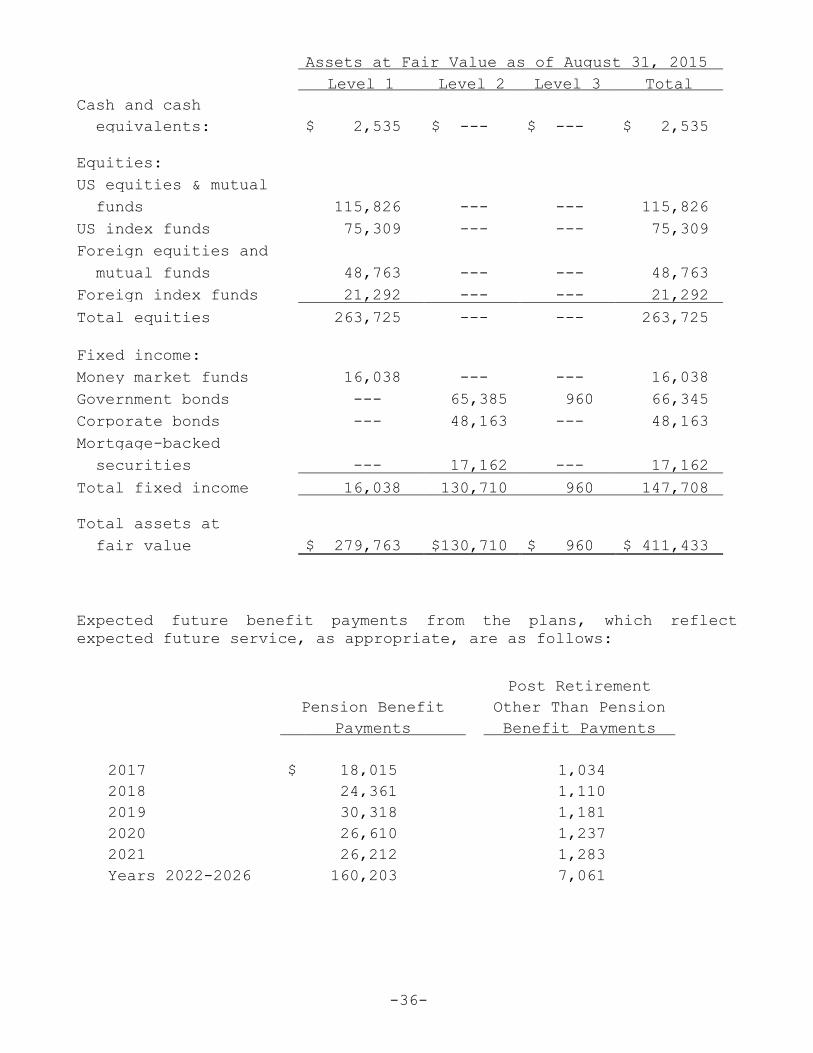

-36-

Assets at Fair Value as of August 31, 2015

Level 1 Level 2 Level 3 Total

Cash and cash

equivalents: $ 2,535 $ --- $ --- $ 2,535

Equities:

US equities & mutual

funds 115,826 --- --- 115,826

US index funds 75,309 --- --- 75,309

Foreign equities and

mutual funds 48,763 --- --- 48,763

Foreign index funds 21,292 --- --- 21,292

Total equities 263,725 --- --- 263,725

Fixed income:

Money market funds 16,038 --- --- 16,038

Government bonds --- 65,385 960 66,345

Corporate bonds --- 48,163 --- 48,163

Mortgage-backed

securities --- 17,162 --- 17,162

Total fixed income 16,038 130,710 960 147,708

Total assets at

fair value $ 279,763 $130,710 $ 960 $ 411,433

Expected future benefit payments from the plans, which reflect

expected future service, as appropriate, are as follows:

Post Retirement

Pension Benefit Other Than Pension

Payments

Pension Benefit

Payments

Benefit Payments

Other Than Pension

Benefit Payments

2017 $ 18,015 1,034

2018 24,361 1,110

2019 30,318 1,181

2020 26,610 1,237

2021 26,212 1,283

Years 2022-2026 160,203 7,061

-37-

The assumed annual rates of increase in the per capita cost of

covered medical benefits for retirees is 7.60% in 2016 and 8.20% in

2017. It is assumed by 2025 that rates will have changed to 4.50%.

13. Rentals under operating leases ($ In Thousands)

The following is a schedule of minimum future rentals on non-

cancelable operating leases as of August 31, 2016:

Year ending August 31,

2017 $ 16,678

2018 12,540

2019 6,815

2020 3,638

2021 2,164

Later years 13,737

$ 55,572

Rent expense was $17,549 in 2016 ($18,075 in 2015).

14. Commitments and guarantees

At August 31, 2016, a subsidiary of the Company was contingently

liable under a guarantee for up to $25.0 million ($25.0 million at

August 31, 2015) of loans to patrons of GROWMARK, Inc. member

cooperatives participating in the FS Agri-Finance program.

The estimated fair value of the guarantee was deemed to be an

immaterial amount and therefore has not been accounted for as a

liability on the subsidiary’s financial statements. The Company

anticipates that in the event that this guarantee was activated

there would be sufficient proceeds from liquidation of collateral to

materially cover the maximum potential amount of future payments.

At August 31, 2016, the Company was contingently liable for $153

million under recourse provisions of FS Agri-Finance and other

producer financing arrangements. The estimated fair value of the

recourse contingency was deemed to be an immaterial amount and

-38-

therefore has not been accounted for as a liability on the Company’s

financial statements.

As part of the Company's overall risk management program the Company

self-insures for certain risk exposure situations. As part of this

program, a performance bond has been purchased from an insurance

company. As of August 31, 2016, the amount of the performance bond

coverage was $15.5 million ($15.5 million at August 31, 2015).

15. Other litigation and claims

The Company is involved as a defendant in various lawsuits, claims,

and disputes which are in the normal course of business. The

Company intends to vigorously defend itself against these actions

and proceedings. The Company believes the resolution of any such

matters will not have a material adverse impact on the consolidated

financial position of the Company.

16. Deconsolidation of Subsidiaries

On September 1, 2015, two of the Company’s subsidiaries, NORTHERN

GRAIN MARKETING, LLC, AND EASTERN GRAIN MARKETING, LLC, merged with

other grain businesses to form FS GRAIN, LLC. As a result of this

merger, the Company has a non-controlling ownership in FS GRAIN,

LLC. The two subsidiaries had combined assets of $69.9 million as

of August 31, 2015 and combined sales of $170.6 million for the year

ended August 31, 2015. The Company realized a gain of $6.2 million

upon the de-consolidation and related remeasurement at fair value of

the previously consolidated subsidiaries. The gain on

deconsolidation is included in the line item “Other income – net” in

the Consolidated Statement of Operations for the year ended August

31, 2016.

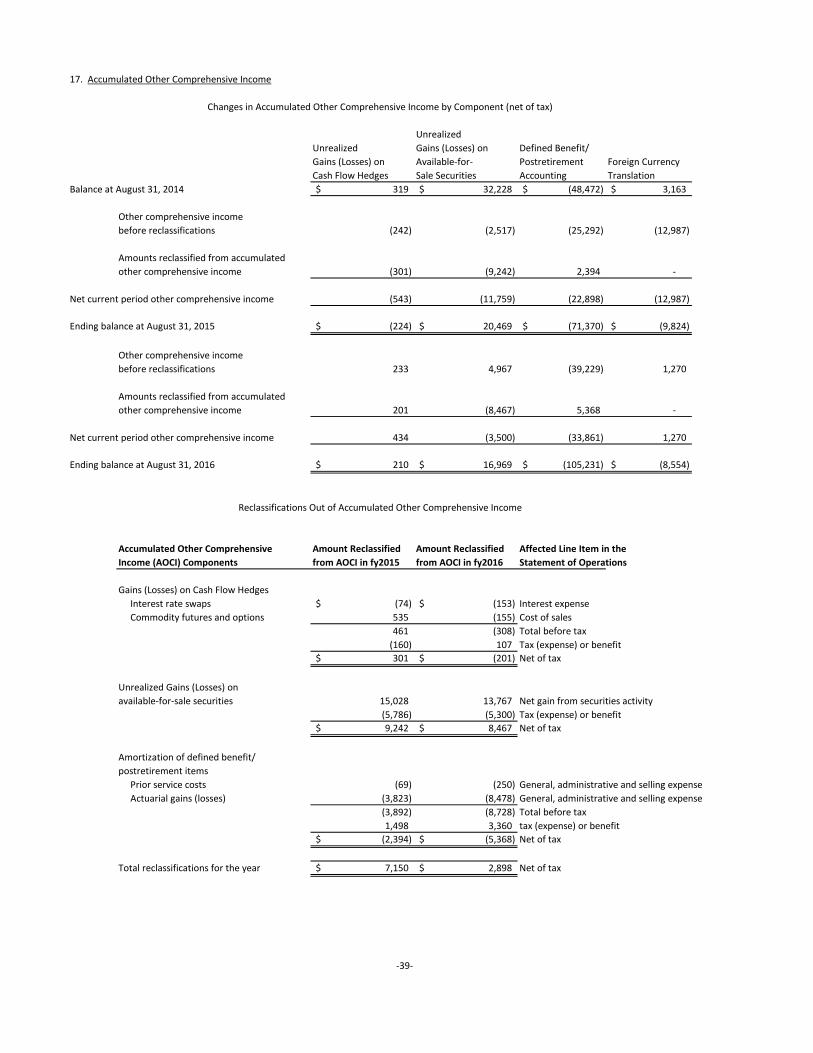

17. Accumulated Other Comprehensive Income

Unrealized

Unrealized Gains (Losses) on Defined Benefit/

Gains (Losses) on Available-for- Postretirement Foreign Currency

Cash Flow Hedges Sale Securities Accounting Translation

Balance at August 31, 2014 319$ 32,228$ (48,472)$ 3,163$

Other comprehensive income

before reclassifications (242) (2,517) (25,292) (12,987)

Amounts reclassified from accumulated

other comprehensive income (301) (9,242) 2,394 -

Net current period other comprehensive income (543) (11,759) (22,898) (12,987)

Ending balance at August 31, 2015 (224)$ 20,469$ (71,370)$ (9,824)$

Other comprehensive income

before reclassifications 233 4,967 (39,229) 1,270

Amounts reclassified from accumulated

other comprehensive income 201 (8,467) 5,368 -

Net current period other comprehensive income 434 (3,500) (33,861) 1,270

Ending balance at August 31, 2016 210$ 16,969$ (105,231)$ (8,554)$

Accumulated Other Comprehensive Amount Reclassified Amount Reclassified Affected Line Item in the

Income (AOCI) Components from AOCI in fy2015 from AOCI in fy2016 Statement of Operations

Gains (Losses) on Cash Flow Hedges

Interest rate swaps (74)$ (153)$ Interest expense

Commodity futures and options 535 (155) Cost of sales

461 (308) Total before tax

(160) 107 Tax (expense) or benefit

301$ (201)$ Net of tax

Unrealized Gains (Losses) on

available-for-sale securities 15,028 13,767 Net gain from securities activity

(5,786) (5,300) Tax (expense) or benefit

9,242$ 8,467$ Net of tax

Amortization of defined benefit/

postretirement items

Prior service costs (69) (250) General, administrative and selling expense

Actuarial gains (losses) (3,823) (8,478) General, administrative and selling expense

(3,892) (8,728) Total before tax

1,498 3,360 tax (expense) or benefit

(2,394)$ (5,368)$ Net of tax

Total reclassifications for the year 7,150$ 2,898$ Net of tax

Changes in Accumulated Other Comprehensive Income by Component (net of tax)

Reclassifications Out of Accumulated Other Comprehensive Income

-39-