gruppo banca carige · gruppo banca carige ennio la monica general manager page | 1 presentation to...

TRANSCRIPT

GRUPPO BANCA CARIGE

Ennio La MonicaGeneral ManagerGeneral Manager

Page | 1

Presentation to the Financial CommunityMilan, 22 May 2012

Contents

• Carige Group today

• New market scenario

• Carige Group Reorganisation Project

• Target organisational structure• Target organisational structure

• Economic impact of the Reorganisation

• Timeline

• Contacts

Page | 2

Complex banking, insurance and social security organisation...

M k t

~50,000 minor shareholders

9.999.99%% 43.0243.02%%

Market

46.9946.99%%

Fi

BancaBanca CarigeCarige SpASpACassaCassa di di RisparmioRisparmio di di GenovaGenova e Imperiae Imperia

T t

Federalmodel

Listed companies

Mkt Cap: €1.2 Bln

Insurance activities 1Banking activities1

Finance activities 1

Banca Carige

CR Savona

Carige Vita Nuova (vita)

Carige Ass.ni (danni)

Carige AM SGR

Creditis (Credito al

Trustee activities 1

Centro Fiduciario

CR Carrara

BM Lucca

B. Cesare Ponti

consumo)

Own Product Factories

5,974Employees

677 branches &432 insurance outlets

~ 2 Mln customers Shareholders’ equity~€2.9 Bln

Page | 3

1 Major companies

Source: company data to May 2012

...with 677 branches in 5 banks

Branches distribution by bank (as at 31/12/2011)

of which #207 in

84% 560

of which #207 in Liguria1 and

#353 outside Liguria

7% 50

3%

5% 37

23

1%

3% 23

7

100% 677

Page | 44

1 Liguria includes Nice branch

SOURCE: Company data

Carige Group showed strong resilience during the crisis, particularly if compared with peers...

Comparison of pre and post crisis cumulated profits (€ Mln)

2005-2007

2008-2011

-53%775

+64%

309

661775

474

309

Peers average1 Carige

Page | 5

1 BPER, BPM, BPVi, Credem, Creval

SOURCE: Banca Carige, annual reports

… and confirming the federal model’s worth

CAGR Inte mediation acti ities Net P ofit C/I

Federal model: marginal administrative and organisational costs against significant commercial benefits and territorial presence

AquiredCAGR

Pre-deal/2011Intermediation activities

(€ Bln)Net Profit(€ Mln)

C/I(%)

∆ p.p.Pre-deal/2011

Dic2011Pre-deal Pre-deal Dic

2011

24 0 p p

Pre-dealDic

2011

1999Banca del Monte

di Lucca(#23 branches)

2.3

10.6%

0.7

12.7%

0.6

2.5

-24.0 p.p.

86.5

62.5

1999

Cassa di Risparmiodi Savona

(#50 branches)

4.72.8

4.4% 7.3%

5.7

13.3

-13.2 p.p.

71.458.2

2003

Cassa di Risparmiodi Carrara

(#37 branches)

3.2

5.3%

2.1

2.4%

4.14.9

-6.3 p.p.

73.6 67.3

Dicembre

2004

BancaCesare Ponti

(#7 branches)2.4

11.7%

1.1

…

-0.6

8.891.6

-15.3 p.p.

76.3

Page | 6The data "Pre-deal" refers to the last balance sheet prior to the acquisition. For Banca Cesare Ponti data "pre deal" refers to the 2004 balanceSource: company data

Contents

• Carige Group today

• New market scenario

• Carige Group Reorganisation Project

• Target organisational structure• Target organisational structure

• Economic impact of the Reorganisation

• Timeline

• Contacts

Page | 7

The crisis impacted significantly the banking sector…

Impact on Banking systemPeriod Effect Focus

2007-2008Sub-prime mortgages and

toxic assets: low asset quality

LimitedAsset

quality

2009-2010

low asset quality

Economic recession: high credit risk cost Significant

2011Liquidity crisis on

institutional markets: Limited, due to

T

2011 institutional markets: sourcing and disposal

Retail funding cost increase:

Retail funding

Si ifi Li bilitiTomorrow gstructural margin reduction Significant Liabilities

quality

Impacts on Italian banks P&L are strictly connected to the traditional banking model

Page | 8

Impacts on Italian banks P&L are strictly connected to the traditional banking model

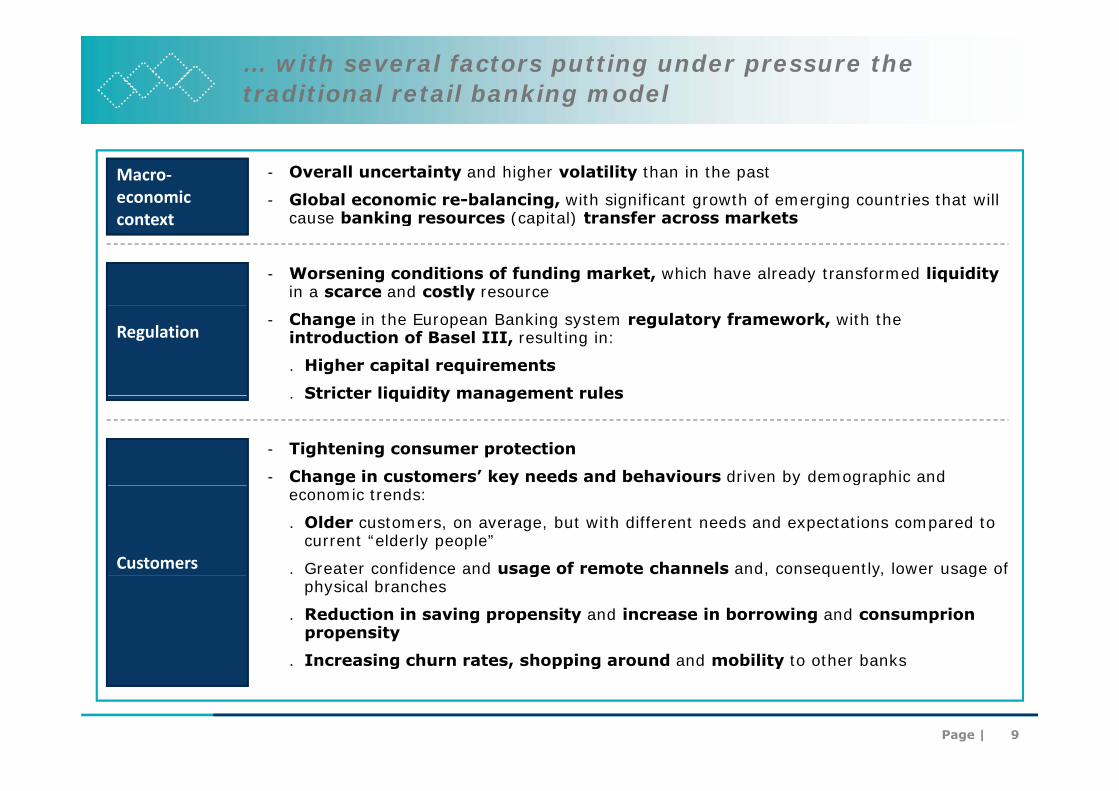

… with several factors putting under pressure the traditional retail banking model

- Overall uncertainty and higher volatility than in the past

- Global economic re-balancing, with significant growth of emerging countries that will cause banking resources (capital) transfer across markets

Macro-economic

t t cause banking resources (capital) transfer across markets

- Worsening conditions of funding market, which have already transformed liquidity in a scarce and costly resource

context

- Change in the European Banking system regulatory framework, with theintroduction of Basel III, resulting in:

. Higher capital requirements

Stricter liquidity management rules

Regulation

• c

. Stricter liquidity management rules

- Tightening consumer protection

- Change in customers’ key needs and behaviours driven by demographic and economic trends:

. Older customers, on average, but with different needs and expectations compared to current “elderly people”

. Greater confidence and usage of remote channels and, consequently, lower usage of Customers g , q y, gphysical branches

. Reduction in saving propensity and increase in borrowing and consumprionpropensity

. Increasing churn rates, shopping around and mobility to other banks

Page | 9

. Increasing churn rates, shopping around and mobility to other banks

Profitability recovery must be achieved by reducing service cost and increasing commercial productivity…

European Banking system profitability evolution1 – ROE, %

Despite the expected

16.7

Despite the expected market growth and the decreasing risk costs, a performance improvement of 25-30% i d d t hi7 9-9 2 is needed to achieve pre-crisis profitability levels, via:

Reduction of service cost

7.4-8.6

1.2-1.41.7-2.0

7.9 9.2

service cost

Increase of commercial productivity

2015 EInertial growth impact

Regulatory impact on

capital

2007 2010

Page | 10SOURCE: External provider analyses based on Thomson-Reuters data

1 Europe-27 and Switzerland

… and leveraging the increasing usage of remote channels, driven by technology innovation and lower costs

Online banking usage1

I70

80

g g

PercentNorway

S dFinland

Netherlands

3-5 years “Self-service”

50

60

70

Switzerland US

Canada

SwedenFinland

Luxembourg

Denmark

10-15 years III

II7-10 years“Multi-channel”

30

40

Japan

South Korea

Australia

UK

Austria

France

SpainIreland

Germany

Belgium

“Brick & mortar”

10-15 years

IV

III

“Online adaptors”10

20 Brazil

ArgentinaColombia

South Korea

Russia

Middle

EastMexico Serbia

Slovenia

PortugalPoland

HungaryItaly

Spain

Czech

Republic

00 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95

IndiaColombia

China

Internet usage1

Mexico Serbia

Turkey MacedoniaRomania GreeceBulgaria

Page | 11

Percent1 Percentage of individuals using the internet/online banking in the last 3 months

Contents

• Carige Group today

• New market scenario

• Carige Group Reorganisation Project

• Target organisational structure• Target organisational structure

• Economic impact of the Reorganisation

• Timeline

• Contacts

Page | 12

The Strategic Plan identifies four main strategicguidelines

Carige Group Strategic Plan 2011 - 2014 has identified strategic guidelines and actions to enable CarigeGroup to overcome the limits of profitability related to the maturity condition of the Banking sector

STRATEGIC GUIDELINES STRATEGIC GOALS

1 Higher commercial productivity :

− Improvement of cross selling

− Product portfolios evolving towards higher-margin higher-commissionDevelopment of revenues and commercial offering: “discover” business areas (territories, products, customers) that still have untapped value potential

Product portfolios evolving towards higher margin, higher commission products (upselling)

− Lower business performance variance

Broader customer base

Development of inter-channelling

• c

Rationalisation of operating costs and processes: constant striving for technical and

ti ffi i

2

Service model fine-tuning

Review of the pricing policies

New sales processes to free up resources for commercial activities

Personnel's proactive commercial attitudeoperating efficiency

Optimisation of liquidity, capital and cost of risk: efficient allocation of short resources

Efficient cost base and process management

Focus on retail and institutional deposits

Closing of the intermediation circuit

Active capital management in a Basel 3 perspective

3

Focus on innovation and skills: not only on processes and products, but also on human

Active capital management in a Basel 3 perspective

Qualitative selection and management of credit

4 Widespread use of technology

Recognition of merit

Page | 13

resources' behaviours and social skills Optimal use of skills and abilities (knowledge and know-how)

By spinning-off Extra-Liguria branch network from BancaCarige and establishing Banca Carige Italia, the bank will reach the Plan’s targets

Two separate banks, specialised on C i G N t i

p , ptheir own geographical areas of reference, with different mission and, as a consequence, radical differences in strategy, distribution model and

Carige Group – Net income€ Mln

commercial approach

Preserving the current positioning in the historical areas of

33010%CAGR:

presence, defending the customer base, the market leadership and thus the profitability of the bank

Liguria

187the bank

Accelerating the acquisition of customers and the growth of

l d i thExtra-

187

volumes reducing the cost of service to self-finance growth Reducing the funding

gap

Extra-Liguria

Page | 14

gap20172011

Banca Carige Italia will be a network bank, consistently with the federal model of the Group

ReorganisationSet up of a new bank, Carige Italia, that will receive Banca C i ’ b h f th E t Li i t k ( t NiReorganisation

ProjectCarige’s branches of the Extra-Liguria network (except Nicebranch)

Market

9.99% 46.99% 43.02%

Target Structure

NewCoBanca

Carige SpA-listed-

Target Structure of the Group

Carige Italia SpA

95.9% 90.0% 60.0% 100%100%

Othercompanies (1)

Page | 151) Insurance companies, financial, fiduciary and instrumental

Two branch networks significantly different for history, geographical presence and productivity

Extra-Liguria networkLiguria network

History

• Significant presence in the territory outside Liguria only from early ’90s

• “Young” network, develop in the last 15 yearsthrough branches acquisition and new openings

• Historical presence in Liguria region for over 500 years

• Mature network and stable number of branches (207 at date)

Market share and

through branches acquisition and new openings (from 40 branches in 1998 to the actual 353)

branches (207 at date)

• High market share (over 20% in terms of branches and deposits)

• Low market share (below 1.5% in all the regions of presence except Piedmont, Sicily and Sardinia)

share and coverage • Diffuse coverage, based on branches

proximity, close to each other• Low coverage (few, distant branches to cover larger

territory)

• Higher productivity by branch, thanks to hi h b f li b h

• Branch productivity far from Liguria’s, due to l b f l b h ( )Productivity high number of clients per branch

• Higher volumes per client

low number of clients per branch (-38%)

• Limited volumes per client vs. Liguria network (-40%) but higher profitability

Customer base

• More balanced portfolio in terms of customer segments vs. Extra Liguria, with Mass Market representing ~63% of total customer base

• Customer base on average older than Liguria’s

• Higher share of Mass Market segment (72%) vs. Liguria network; Affluent e Private segments less represented in the customer portfolio

• Customer base on average younger than Liguria’s

Page | 16

• Customer base on average older than Liguria s, with relevant portion of clients in the senior age bands

Liguria s

Liguria Network represents the historical core of the bank, while Extra-Liguria Network is the result of an intense growth phase during the last 15 years

Number of branches1

1998 2000 2002 2004 2006 2008 2010 2012

Liguria 200 201 200 201 203 205 207 207

1990

129g

Extra-Liguria

40 79 186 189 198 327 348 353

New openings 18 4 3 9 10 1 5

7

337New openings 18 4 3 9 10 1 5

Acquisitions - 21 103 - - 119 20 -

33 90

263

7

-

Total 240 280 386 390 401 532 555 560

Acquired

136

Banco di Sicilia

IntesaCapitalia

ISPUniCredit MPS

Acquired from

Page | 17

1 Net of closed branches

The two networks operate in completely different markets

Banca Carige: Branch Market ShareBranch Market Share

Customer loans Market Share

Direct depositsMarket Share

1.9%1.2%

0.8%

1%

21 2%

1%

Italy: 1.3%Liguria: 18.9%

Extra-Liguria: 0.8%

Italy: 1.2%Liguria: 22.3%

Extra-Liguria: 0.7% 2

1%0.3%

0.4%21.2%

1 4%0.6%

1.6%

1.4%

Italy 2%Liguria: 21.2% 3.6%

Page | 18

Liguria: 21.2%Extra-Liguria: 1.3%

During the last years, the main commercial indicators of Extra-Liguria network improved

Clients / FTEs Bank Accounts / FTEs

297286251

+9% p.a.

243232220

+5% p.a.

201120102009 201120102009201120102009 201120102009

Cross-selling Index Acquisition Index

+3% p.a.

3.93.83 7

+13% p.a.10.4%

9.2%8.2%3.83.7

Page | 19

201120102009 201120102009

However, Extra-Liguria network still counts a lower number of customers per branch…

Index, Liguria=100Data at 31/12/2011

Customers per FTE %

Extra-Liguria Network has

100

Customers per branch %

a lower number of customers per FTE…

100

75100

6200

ExtraLiguria

Liguria

and on

FTE per branch %

Liguria

82100 ...and, on

average, smaller branches

82100

Page | 20

… customers with lower average volume…

Index, Liguria=100Data at 31/12/2011

Volume per customer%

Extra-Liguria has customers

100

Total Income per customer %

significantly smaller…63

100

87100

with higher

Total Income on volume %

Liguria ExtraLiguria

133100 ...with higher

volume profitability

100

Page | 21

… and a gap in terms of Affluent and Private customers, also driven by the lower average age of the customers

Extra-Liguria

Liguria

Customer distribution by segment Average customer age

Mass Market72%

63%

Private4%

Affluent15%

22%

52

57

Small Business10%

7%

Private1%

52

Corporate1

2%

4%

10%

Liguria Extra-Liguria

Page | 221 Includes Mid and Large Corporate, and Public Institutions

It’s time for a step-change and a discontinuity in the way we work

PhaseE Li i kExtra-Liguria network: 353 branches

Discontinuity in the way we work and full

Extra-Liguria network: 40 branches

Acquisition and integration into the Group

way we work and full exploitation of the opportunities out of Liguria region

1998 2012 2017

Objectives Branch network expansion beyond the historical region of the Bank

Full exploitation of the growth potential of the Extra-Liguriathe historical region of the Bank

Improvement of the commercial performance,volumes productivity and profitability

potential of the Extra Liguria network

Step-change in the growth pathof number of clients and volumes, th h b h f t d

Page | 23

through new branch format and distribution model innovation

The performance improvement will be achieved through the implementation of two separated operating and commercial strategies

Objectives Operating and commercial strategy

Maintain actual strategy, focused on volumes profitability and branches operational efficiency, by:

Preserving the current

Defending the customer base and executing qualitative remix (with assignment of specific targets in terms of client acquisition by age band)

Safeguarding profitability Enhancing efficiency (interventions on back office

Carige

positioning in the historical areas of presence, defending the customer base Enhancing efficiency (interventions on back-office

and multi-channel distribution) Improving productivity per square meter

customer base, the market leadership and thus the profitability of the b k

Innovate the client service model, integrating the existing branch network with new and flexible

bank

Accelerating the acquisition of g

acquisition and sales channels and testing new solutions in a “laboratory-style” set-up, with focus on: Increasing number of leads (development) Acquiring new clients

A i i “ l bl ” li t (“ ti ”

Carige Italia

acquisition of customers and the growth of volumes reducing the cost of service to self finance Acquiring “valuable” clients (“native” cross

selling) Develope a new product offer aimed to attract

valuable clients

to self-finance growth Reducing the

funding gap

Page | 24

In order to increase volumes and clients, the strategy of Carige Italia will focus on channel and product innovation

Innovate the h d l

Innovate service model, developing the existing retail capacity and coupling it with low cost and more effective

t h lgrowth model remote channels Introduce “attack” products, simple and appealing for

value customers

Historically, the existence of two completely different networks in one bank h d d i

Increase accountability

Increase transparency on results and differentiate commercial accountability, in order to maximize the values of the two different strategies and avoid mix-up between the objectives Differentiate management performance systems

has produced a mix-up of strategies and commercial approaches, resulting in the acceptance of Differentiate management performance systems,

focusing on growth in terms of objectives and commercial targets, planning process, incentives programs and KPIs

I t d i l t t tt t d

several “compromises” in order to manage safely and profitably the Bank

h li f h Specialize infrastructure

Introduce new commercials systems to attract and manage new clients through remote and innovative channels

The split of the two networks will enable a clear strategy differentiation and the activation of the

Strengthen credit risk control

Achieve a more balanced asset-liability structure, reducing Carige Italia funding gap Differentiate credit powers between Carige and Carige

Italia in order to assure selective loan growth, in compliance to the Holding credit policies

required enablers

Page | 25

compliance to the Holding credit policies

Contents

• Carige Group today

• New market scenario

• Carige Group Reorganisation Project

• Target organisational structure• Target organisational structure

• Economic impact of the Reorganisation

• Timeline

• Contacts

Page | 26

Business model differentiation will take into account innovation needs and the continuous curb of operative cost

Rationale

Diff ti t dHolding Functions

Centralised management and control functions, in order to maintain scale and scope synergiesF C i It li t d l d

Banca Carige

Differentiated strategy and commercial approach to better cope with different

Focus on Carige Italia to develop and test product innovations, service model, ICT platforms, and roll-out them to the Liguria network in a second phase

Centralised back-office functions tocope with different geographic needs and market opportunities

Common operative platform to maintain

Centralised back office functions to leverage economy of scale

platform to maintain scale advantages and possibility to implement specific differentiations

Carige

Network

(Liguria)

CarigeItalia

Network

(

Wholly differentiated commercial networks in terms of role, objectives, and distribution model

Duplication limited to commercial (e.g. pricing) and credit functionsdifferentiations

(Extra-Liguria)

pricing) and credit functions

Page | 27

The target organisational structure of Carige Italia isconsistent with the management of the Group’s Network Banks

BOARD OF DIRECTORS

CEO

Corporate affairs

Managing, directingand controlling

functions centralisedin the Parent Bank

LENDING NETWORK

in the Parent Bank

• c

Market SupportLending Monitoring Development & Private Banking

Large corporate Lending Support NPL management

TUSCANY & UMBRIA Area

PIEDMONT Area

LOMBARDY Area

VENETO Area

EMILIA ROMAGNA Area

LATIUM-MARCHES Area

SARDINIA Area

APULIA Presidium

SICILY Area

Page | 28

SICILY Area

Contents

• Carige Group today

• New market scenario

• Carige Group Reorganisation Project

• Target organisational structure• Target organisational structure

• Economic impact of the Reorganisation

• Timeline

• Contacts

Page | 29

Benefits of the Project

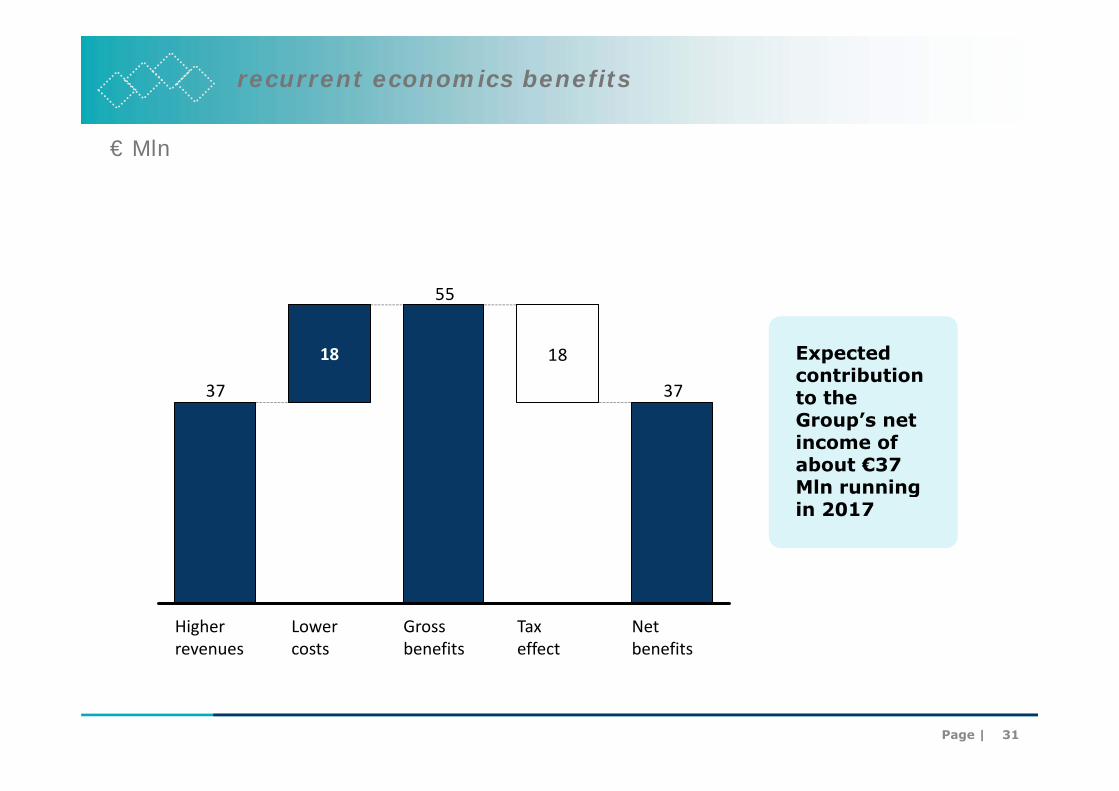

RecurrentBenefits

Running gross benefits equal to €55 Millions (Net €37 Millions):• Increase of annual recurrent revenues equal to €37 Millions (2017), due to

productivity growth and network efficiency, optimisation stabilisation of cost ofinstitutional funding, active capital management, net of higher taxes on intra-groupfunding and dividends

Revenues

funding and dividends

• Running annual cost savings equal to €18 Millions, due to higher efficiency ofinfrastructures, optimisation of processes and tax savings net of the increase ofother minor recurrent structural costs (<1M€)

• Also due to these actions the running Cost/Income for 2017 is expected to be in

Cost savings

Non Recurrent

g / preduction of 13.5% at 45%

Economic• Benefits of €715.8 Millions, of which:

• 456 5 for Banca Carige due to the positive effect of DTL write off DTABenefits • 456.5 for Banca Carige due to the positive effect of DTL write-off, DTA recognition on goodwill not yet amortised as at 31/12/2012 and negative effectof recognition of DTL on the stake in Carige Italia - according to PEX – equal tothe original fiscal value of goodwill

• 259.3 for Carige Italia due to the positive effect of recognition of DTA related

Financial

g p gto the goodwill and negative effect of the substitute tax recognition, due to the exercise of the tax release option applied to the goodwill

• 254 bps benefit on the regulatory ratios, for the fully retained extraordinaryearning, net of the tax benefits already recorded under shareholders’ equity

Investments • Utilisation of a significant part of the investments already planned in the Strategic Plan 2011-2014 (€110 Millions) and of those further expected for

• Core Tier 1 at 9.3% as at 31/12/2012• CET1 full compliant expected to be greater than 8% as at 1/1/2013

Page | 30

Strategic Plan 2011-2014 (€110 Millions) and of those further expected forthe three-years period 2015-2017 (€90-110 Million) supporting the requestedprojects’ initiatives and innovations

recurrent economics benefits

€ Mln

55

18

3737

18 Expected contribution to the3737 to the Group’s net income of about €37 Mln runningMln running in 2017

Grossbenefits

Net benefits

Taxeffect

Lowercosts

Higherrevenues

Page | 31

Detail of the gross recurrent economic benefits

Benefits Action and economic impact Rationale

1 1.1

€ Mln

Optimisation and stabilisation of cost of funding

Stategic and rigorous approach to Capital Management

Development of new customers taking into accont risk/return equilibrium

Improvement of productivity thanks to the newGross

recurrent

Productivity growth and network efficiency

Active capital management

Credit standing improvement

~22

~10

~11

1.1

1.2

1.3

Improvement of productivity thanks to the new commercial model deriving from the establishment of Carige Italia

More efficent allocation of resources

recurrentrevenuesbenefits

Credit standing improvement

Total revenues benefits ~37

~11

Intra-group funding and fiscal ~(6)1.4

Rationalization of localnetwork

Higher efficiency of

~1

~3

2 2.1

2.2

Rationalization of the network and enhancement of local brand

Higher efficiency in the allocation of resources

O i i i f h

infrastructures

Optimisation of processes

~3

~9Gross

recurrentcost

benefits‘ACE’ benefits/reserves

2.3

2.4

~6

Optimisation of the expense processbenefits

Total cost benefits ~18

Other recurrent costs ~(1)2.5

Page | 32

Non recurrent benefits from the Reorganisation Project

Action Effects

Regulatory (bps)

One-off effects(2012)

Core Tier 1 (2012 pro forma)

P&L € Mln

1

One-off effects(2012)

Reg. Cap. € Mln

144457The Project allows a total benefit of 254

Emerging latent deferredtaxation on goodwill 340

bps on the Core Tier 1 ratio at the end of 2012Fiscal recognition of

2

110259Fiscal recognition ofgoodwill ad upfrontwithholding tax

259

2547161Total effect 598

Page | 331 Gross of €5.1 Million one-off costs (€3.4 Mln net) expensed in 2012. Additional one-off costs for €2.4 Million will be expensed from 2013 to 2017

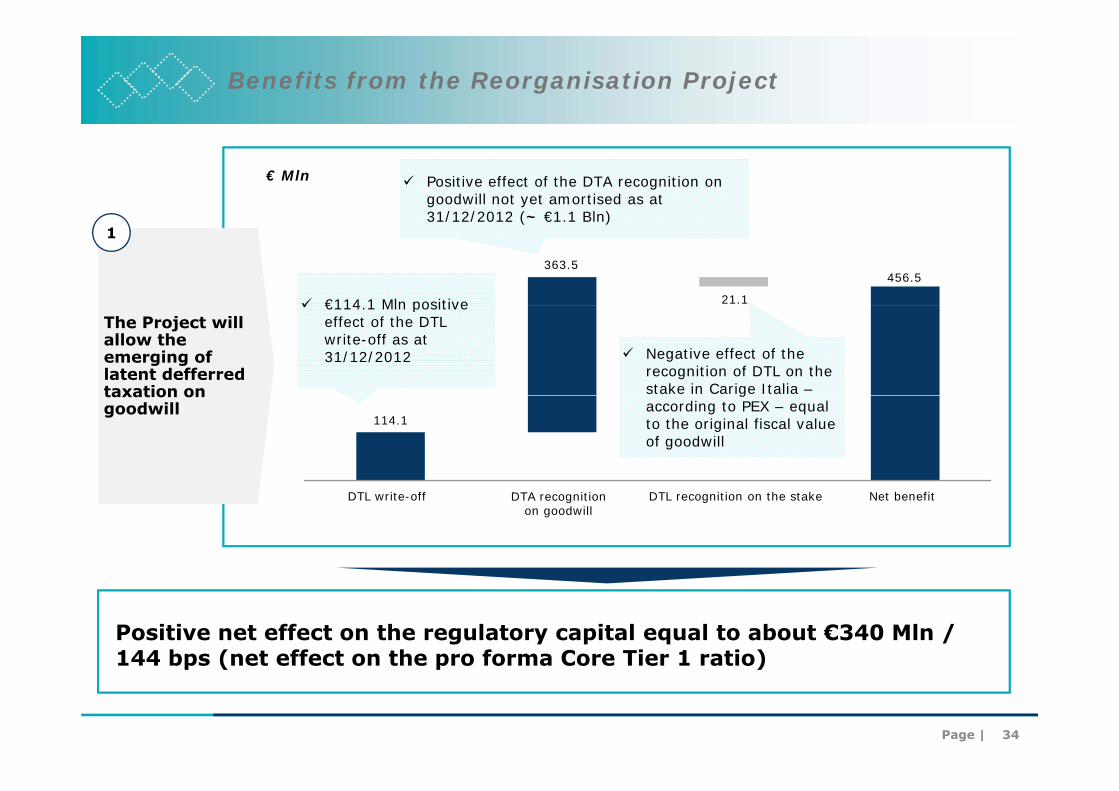

Benefits from the Reorganisation Project

Positive effect of the DTA recognition on goodwill not yet amortised as at 31/12/2012 (~ €1 1 Bln)

€ Mln

1

€114 1 Mln positive

31/12/2012 (~ €1.1 Bln)

456.5363.5

21.1

• c

The Project willallow the emerging oflatent defferredtaxation on

€114.1 Mln positive effect of the DTL write-off as at 31/12/2012 Negative effect of the

recognition of DTL on the stake in Carige Italia –taxation on

goodwillg

according to PEX – equalto the original fiscal valueof goodwill

114.1

DTL write-off DTA recognitionon goodwill

DTL recognition on the stake Net benefit

• cPositive net effect on the regulatory capital equal to about €340 Mln / 144 bps (net effect on the pro forma Core Tier 1 ratio)

Page | 34

144 bps (net effect on the pro forma Core Tier 1 ratio)

Financial benefits of the Reorganisation Project

Upfront withholding taxequal to the 16.0% of the goodwill for Carige Italia

€ Mln

2 DTA relatedto the goodwill (taxrate 33.07%)

goodwill for Carige Italia Effect of the recognition of

DTA related to the goodwill asgranted by art. 15, par. 10 ofthe Legislative Decree n°185/2008 (+ ~110 bps for

502.3

• c

Fiscal recognition ofgoodwill ad upfrontwithholding tax

185/2008 (+ 110 bps forregulatory purposes)

259.3

243.0g

Recognition on goodwill Substitute tax Net benefitRecognition on goodwill Substitute tax Net benefit

• cPositive net effect on the regulatory capital equal to about €260 Mln / 110 bps on the pro forma Core Tier 1 ratio

Page | 35

110 bps on the pro forma Core Tier 1 ratio

Benefits on Regulatory Capital

Effects on Regulatory Capital %

~9.3

2 5

CET1 full compliant as at 1/1/2013

2.5

6.8

5 0 / /greater than8% thanks tothe Reorganisation

5.0

Reorganisation

ReorganisationProject

CT131.03.2012

CT131.12.2012

CT131.12.2011

Page | 36

The resources required to support the strategy will be derived from the investments already planned in the Strategic Plan 2011-2014 and additional investments

Pl d i t t The Group has already planned Planned investments

€ Mln

The Group has already plannedin the Strategic Plan 2011-2014 investiments on technologyequal to about €110 Million

111

90-110

A considerable part of theseinvestments will be used tosupport the project’s initiativesaiming at the innovation of the network (eg automatisedbranches, remote channels toattract new customers), ofproducts, marketing and training (eg for the evolution ofskills of the branch staff)

Additional investments for €90-110 Million planned for the three

2015-20172012-2014110 Million planned for the threeyears period 2015-2017

Page | 37

Financial highlights of the commercial networks, evolution 2011-2017

Carige (branches in Liguria)1 Carige Italia

2011 2017 CAGR 11-17 2011 2017 CAGR 11-17

6.2% 6.2%9.2 13.2 8.9 12.7GROSS LOANS € Bln

4.3%

4 0%

7.1%

6 1%

12.11 15.6

9 72 12 2

7.62 11.42

5 62 8 02

DIRECT DEPOSITS € Bln

INDIRECT DEPOSITS € Bln 4.0%

4.2%

6.1%

6.7%

9.72 12.2

21.8 27.9

5.62 8.02

13.2 19.4

INDIRECT DEPOSITS € Bln

FIA € Bln 4.2%

4.5%3

6.7%

18.9%

21.8 27.9

125.4 163.4

13.2 19.4

53.4 150.7NET PROFIT € Mln

-2.9bp -12.1bp38.5 35.6 60.3 48.2COST INCOME %

Page | 38

1 Banca Carige SpA, in addition to the Liguria commercial network (represented here), maintains also its own internalinstitutional funding, its security portfolio, Leasing, Factoring, medium and long term Pool financing and foreign activities; 2 Intragroup Bonds are reclassified as Direct Deposits; 3 Excluding one-off for cagr calculation purposes

Strategic rationale

1 Acceleretion in achieving the targets of the Carige Group’ Strategic Plan 2011-20141 Acceleretion in achieving the targets of the Carige Group Strategic Plan 2011-2014

Optimisation of the market’s defence by strenghtening the inter-channelling

Cost synergies related to the processes’ optimisation and increasing productivity of the

networks thanks to the specific focus on their core business (unbundling of the Carige network)

and to the emulation effect

2

Strengthening of coordination and control functions of the Parent Bank

Significant strengthening of regulatory capital (even with the new Basel III requirements)2

with expected improvements in the Carige Group’s ratings and, consequently, for its cost of funding

Actions to accelerate the achievement of the targetscommunicated to the market (improving productivity, cost savings, capital

strengthening)…“K i d i l ”

Page | 39

…“Keep growing producing value”

Contents

• Carige Group today

• New market scenario

• Carige Group Reorganisation Project

• Target organisational structure• Target organisational structure

• Economic impact of the Reorganisation

• Timeline

• Contacts

Page | 40

Outlined schedule of the Reorganisation Project

Date Milestones Description

Board of Directors of Banca Carige

Presentation to the Financial Community21 May 2012

22 May 2012

Approval of the Group’s Reorganisation Project

17 SeptemberBoard of Directors of Banca Carige

23 May 2012 Set up of Carige Italia

Approval of the contribution’s balance as at 30/6/20122012

Board of Directors of Banca Carige

Starting Dec. 2012

Extraordinary shareholder’s meeting of

Carige Italia to formally approve the capital

increase

Approval of the capital increase to be realised in nature through

the transfer of the business unit with effect 31/12/2012, and the

subsequent amendments to the Articles of Association with effect

pp o a o t e co t but o s ba a ce as at 30/6/ 0

Starting Dec. 2012

increase subsequent amendments to the Articles of Association with effect

1/1/2013

Draw up of the agreements on the

contribution to Carige Italia

31 December2012

Date of effectiveness of the Reorganisation

Project

Page | 41

Contents

• Carige Group today

• New market scenario

• Carige Group Reorganisation Project

• Target organisational structure• Target organisational structure

• Economic impact of the Reorganisation

• Timeline

• Contacts

Page | 42

Disclaimer

This document has been prepared by Banca Carige S.p.A. solely for information purposes andsolely to present the Group's strategies and key financial data.

The Company, its consultants and representatives shall not be held responsible (for losses arisingfrom negligence or any other

reasons) for any losses arising from the use of this document and of the contents hereof.All forward-looking information contained in this document have been prepared on the basis of

assumptions that may prove incorrect, and therefore the results may vary.In forming their own opinion, readers should keep in mind the aforesaid factors.

This document does not constitute an offer or solicitation to purchase or subscribe shares, andno part of this document can be regarded as the basis of any contract or agreement.

N f th i f ti t i d h i b d d bli h d di t ib t d iNone of the information contained herein may be reproduced, published or distributed, infull or in part, for whatever purpose.

By accepting this notice you agree to all the limits listed above.

**********

The manager responsible for preparing the company’s financial reports Ms. Daria Bagnasco, Deputy General Manager (Governance and Control) of Banca CARIGE S.p.A., declares, pursuant to paragraph 2 of Article 154 bis of the Consolidated Law on Finance, that the consolidated accounting information of Banca CARIGE Group

contained in this presentation corresponds to the document results books and accounting recordscontained in this presentation corresponds to the document results, books and accounting records.

Page | 44