gst-fringe benefits tax

TRANSCRIPT

________________________________________________________________________________ GST- Fringe Benefits (June 2017) © The Institute of Certified Bookkeepers Page 1

Fringe benefits tax is a tax paid on certain benefits employers provide to their employees or their employee’s ‘associates’ (typically family members). FBT is separate from income tax and is based on the taxable value of the various fringe benefits provided. Fringe Benefits Tax is payable by any employer who provides employees with benefits, regardless of the type of business structure. The FBT year runs from 1 April to 31 March. A fringe benefit is a benefit provided in reward for employment. This effectively means a benefit provided to an employee (or their associate) because they are an employee. An employer can provide these benefits, or they can be provided by:

! An associate of theirs ! A third party under an arrangement with the employer. An employee can be a current, future or

former employee. FBT was established when the government realised that people were being paid in benefits rather than as salary. Employers had been creative with ways of paying their people: provision of cars when they did not really need them for work, payment of expenses (mortgage, school fees, holidays, long lunches etc.), that had nothing to do with the expenses of the business other than it was paid as part of the reward for the employee. History When employees are paid a salary/wage, it is caught in the PAYG Withholding system: i.e., you pay money to the employee then you need to withhold tax. Development Increase the reward to the employee by paying their expenses for them. Why Company tax rates are only 30% compared to personal tax rates, which can be as high as 47%. As an example, an employee had a $100 non-deductible expense to pay e.g., mortgage or school fees and was paying 47% tax. If the employee had to pay it out of after tax salary then they had to earn $189 before tax ($89 as tax to government, $100 to employee for expense). If the company paid the $100 for the expense then it costs the company only $130 ($100 for the expense and $30 for the additional company income tax because it was not a tax deduction). Government response Fringe Benefits Tax was created so that the cost to the company and the amount of tax is the same as if it was salary. The current rate of FBT is 47%.

Fringe Benefits Tax

________________________________________________________________________________ GST- Fringe Benefits (June 2017) © The Institute of Certified Bookkeepers Page 2

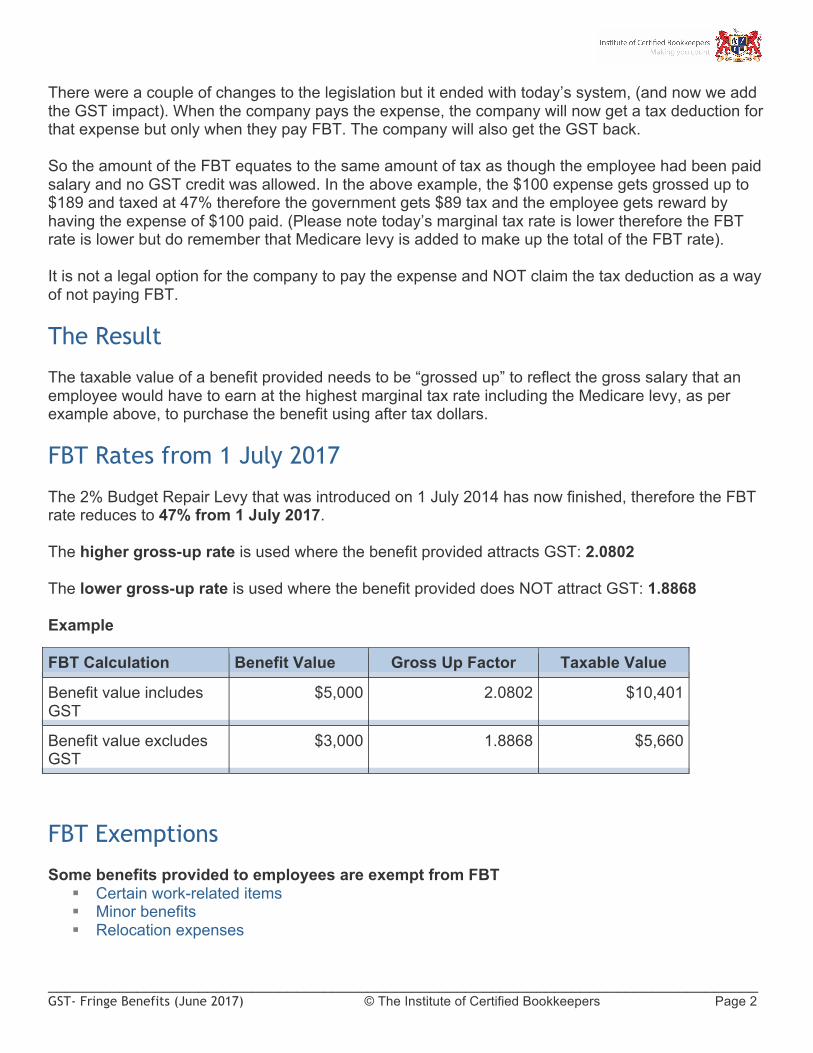

There were a couple of changes to the legislation but it ended with today’s system, (and now we add the GST impact). When the company pays the expense, the company will now get a tax deduction for that expense but only when they pay FBT. The company will also get the GST back. So the amount of the FBT equates to the same amount of tax as though the employee had been paid salary and no GST credit was allowed. In the above example, the $100 expense gets grossed up to $189 and taxed at 47% therefore the government gets $89 tax and the employee gets reward by having the expense of $100 paid. (Please note today’s marginal tax rate is lower therefore the FBT rate is lower but do remember that Medicare levy is added to make up the total of the FBT rate). It is not a legal option for the company to pay the expense and NOT claim the tax deduction as a way of not paying FBT. The Result The taxable value of a benefit provided needs to be “grossed up” to reflect the gross salary that an employee would have to earn at the highest marginal tax rate including the Medicare levy, as per example above, to purchase the benefit using after tax dollars. FBT Rates from 1 July 2017 The 2% Budget Repair Levy that was introduced on 1 July 2014 has now finished, therefore the FBT rate reduces to 47% from 1 July 2017. The higher gross-up rate is used where the benefit provided attracts GST: 2.0802 The lower gross-up rate is used where the benefit provided does NOT attract GST: 1.8868 Example

FBT Exemptions Some benefits provided to employees are exempt from FBT

! Certain work-related items ! Minor benefits ! Relocation expenses

FBT Calculation Benefit Value Gross Up Factor Taxable Value

Benefit value includes GST

$5,000 2.0802 $10,401

Benefit value excludes GST

$3,000 1.8868 $5,660

________________________________________________________________________________ GST- Fringe Benefits (June 2017) © The Institute of Certified Bookkeepers Page 3

Items not subject to FBT ! Salary and wages ! Acquisition of shares under employee approved scheme ! Superannuation employer contributions ! Termination payments that includes a company car given or sold ! Certain benefits provided by religious institutions to their religious practitioners

Items exempt from FBT

! Minor benefits <$300 ! Portable electronic device ! Computer software ! Protective clothing ! Briefcase ! Tool of trade

Eligible not for profit organisations Organisations need to be endorsed by the ATO in order to be eligible for FBT exemptions.

! Public benevolent institutions and health promotion charities: the reportable amount is over $30,000 (grossed up amount) per employee

! Public and not for profit hospitals and public ambulance services: the reportable amount is $17,000 (grossed up amount) per employee

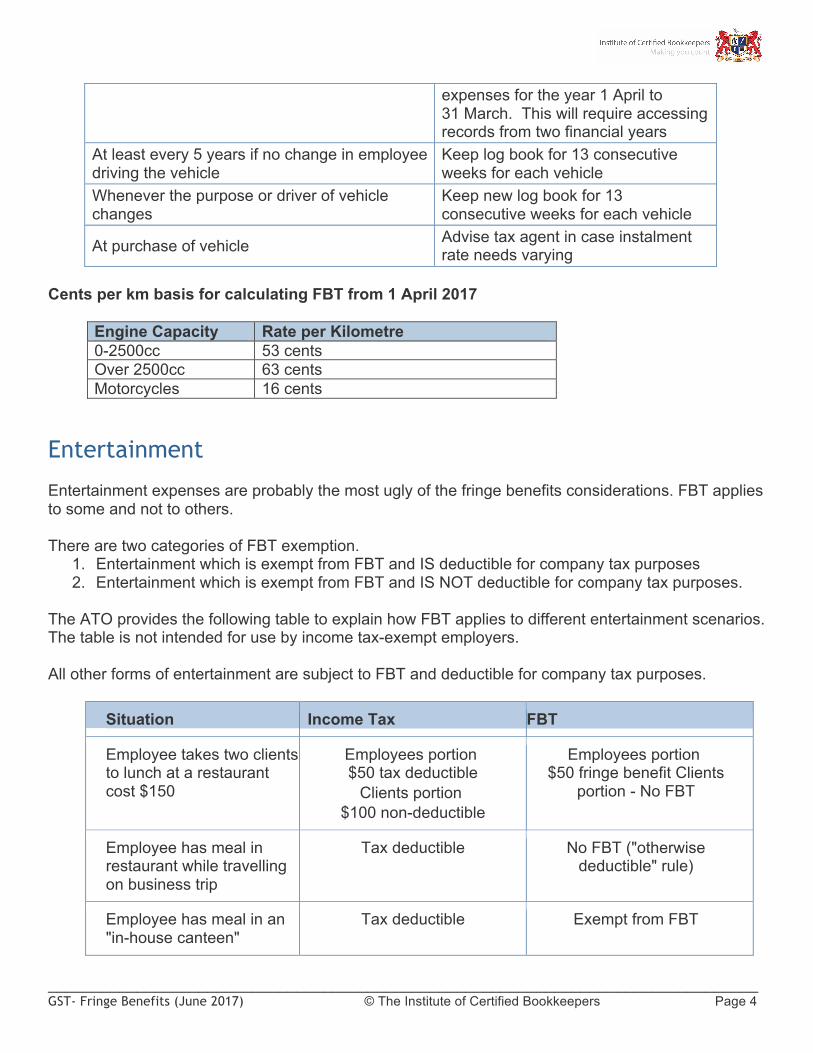

Types of Benefits Common fringe benefits are vehicles, travel, parking, entertainment, financial (i.e., paying expenses on behalf of the employee or providing a loan), accommodation, meals and property. There are a number of benefits that are not considered for FBT, for example, work related items such as computer, tools of trade or mobile phones. Other exemptions include some taxi travel to or from the workplace, some car parking, and some minor benefits that have a value of less than $300. Cars The most common Fringe Benefit has been the car. The employer picks up all the costs of the car and provides it to the employee who has that car available for private use. We now have a variety of different arrangements including company owned vehicle, leased, novated lease etc., where it is still considered that the company is providing a fringe benefit. It is the fact that the car is available for private use that is the issue; then it immediately becomes subject to Fringe Benefits Tax. Car Fringe Benefits - What you need to do

When Action At purchase of a car, sale of a car, change of employee driving a car and every 31 March

Get odometer declaration signed by the employee driving the car

31 March Provide summary of each vehicle’s

________________________________________________________________________________ GST- Fringe Benefits (June 2017) © The Institute of Certified Bookkeepers Page 4

expenses for the year 1 April to 31 March. This will require accessing records from two financial years

At least every 5 years if no change in employee driving the vehicle

Keep log book for 13 consecutive weeks for each vehicle

Whenever the purpose or driver of vehicle changes

Keep new log book for 13 consecutive weeks for each vehicle

At purchase of vehicle Advise tax agent in case instalment rate needs varying

Cents per km basis for calculating FBT from 1 April 2017

Engine Capacity Rate per Kilometre 0-2500cc 53 cents Over 2500cc 63 cents Motorcycles 16 cents

Entertainment Entertainment expenses are probably the most ugly of the fringe benefits considerations. FBT applies to some and not to others. There are two categories of FBT exemption.

1. Entertainment which is exempt from FBT and IS deductible for company tax purposes 2. Entertainment which is exempt from FBT and IS NOT deductible for company tax purposes.

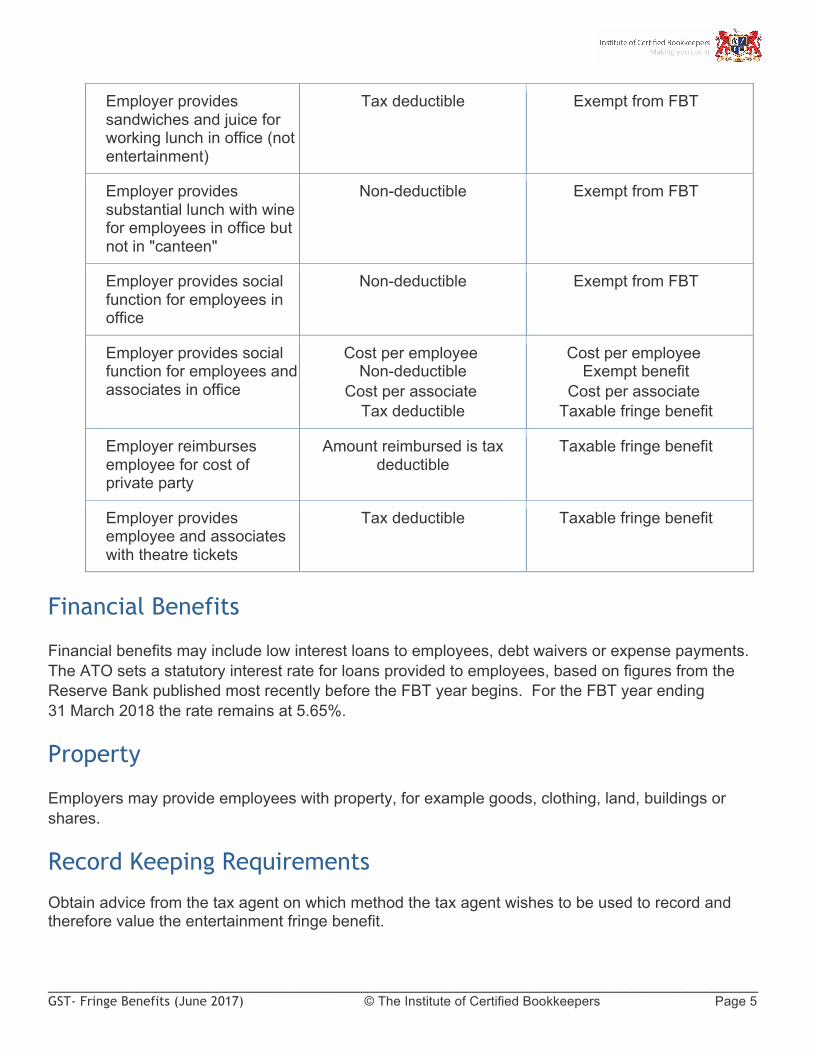

The ATO provides the following table to explain how FBT applies to different entertainment scenarios. The table is not intended for use by income tax-exempt employers. All other forms of entertainment are subject to FBT and deductible for company tax purposes.

Situation Income Tax FBT

Employee takes two clients to lunch at a restaurant cost $150

Employees portion $50 tax deductible

Clients portion $100 non-deductible

Employees portion $50 fringe benefit Clients

portion - No FBT

Employee has meal in restaurant while travelling on business trip

Tax deductible No FBT ("otherwise deductible" rule)

Employee has meal in an "in-house canteen"

Tax deductible Exempt from FBT

________________________________________________________________________________ GST- Fringe Benefits (June 2017) © The Institute of Certified Bookkeepers Page 5

Employer provides sandwiches and juice for working lunch in office (not entertainment)

Tax deductible Exempt from FBT

Employer provides substantial lunch with wine for employees in office but not in "canteen"

Non-deductible Exempt from FBT

Employer provides social function for employees in office

Non-deductible Exempt from FBT

Employer provides social function for employees and associates in office

Cost per employee Non-deductible

Cost per associate Tax deductible

Cost per employee Exempt benefit

Cost per associate Taxable fringe benefit

Employer reimburses employee for cost of private party

Amount reimbursed is tax deductible

Taxable fringe benefit

Employer provides employee and associates with theatre tickets

Tax deductible Taxable fringe benefit

Financial Benefits Financial benefits may include low interest loans to employees, debt waivers or expense payments. The ATO sets a statutory interest rate for loans provided to employees, based on figures from the Reserve Bank published most recently before the FBT year begins. For the FBT year ending 31 March 2018 the rate remains at 5.65%.

Property Employers may provide employees with property, for example goods, clothing, land, buildings or shares. Record Keeping Requirements Obtain advice from the tax agent on which method the tax agent wishes to be used to record and therefore value the entertainment fringe benefit.

________________________________________________________________________________ GST- Fringe Benefits (June 2017) © The Institute of Certified Bookkeepers Page 6

You need to keep any and all records that allow the FBT liability to be assessed, for 5 years from the end of the FBT year. Records you need:

! The taxable value of each fringe benefit provided to each employee, e.g., invoices, travel diaries, log books, odometer readings.

! The method of allocating the taxable value of a fringe benefit provided to two or more employees, e.g., a written agreement regarding the apportionment of fringe benefits.

! To show that 100% of the taxable value has been allocated to employees. (Excluded benefits not needed).

! If total benefits to an employee have a taxable value of more than $2,000 (in the FBT year), then this must be shown on the employee’s payment summary. Note that the grossed up amount is shown.

Bookkeeper Recording and Reporting Recommendation You will need to track expenses and benefits that incur FBT. This may be via jobs or tags/identifiers or by using separate accounts. Cars: dissect or tag the expenses for each vehicle. Entertainment (meal benefit), use the 50 / 50 method so ensure all meal entertainment expenses are tagged or allocated to one chart of account line and this is advised to the accountant (this type of FB doesn’t have to be reported on each employee’s PAYG Summary). All other benefits, tag them. Because these expenses are typically part of an employee’s package then many employers would/should allocate such expenses to one account called “Salary package expenses”. If they are expenses outside of the package then maybe it’s an account simply called Fringe Benefits. At least the amounts are then caught and obvious for each FBT year reporting. Who pays FBT on the BAS?

! Businesses that have cars as a salary package ! Businesses with high entertainment expenses ! Not for Profit organisations salary sacrifice packages ! Living Away Allowance for employees ! Businesses that have an FBT instalment

FBT Instalment If the FBT liability was $3,000 or more in the previous year, the ATO will provide a quarterly instalment amount based on the most recent FBT assessment. Bookkeeper Role If a business purchases a car or some other expense that is subject to FBT within the period of the BAS then it’s important to advise the tax agent of the acquisitions as the instalment rate may need varying.

________________________________________________________________________________ GST- Fringe Benefits (June 2017) © The Institute of Certified Bookkeepers Page 7

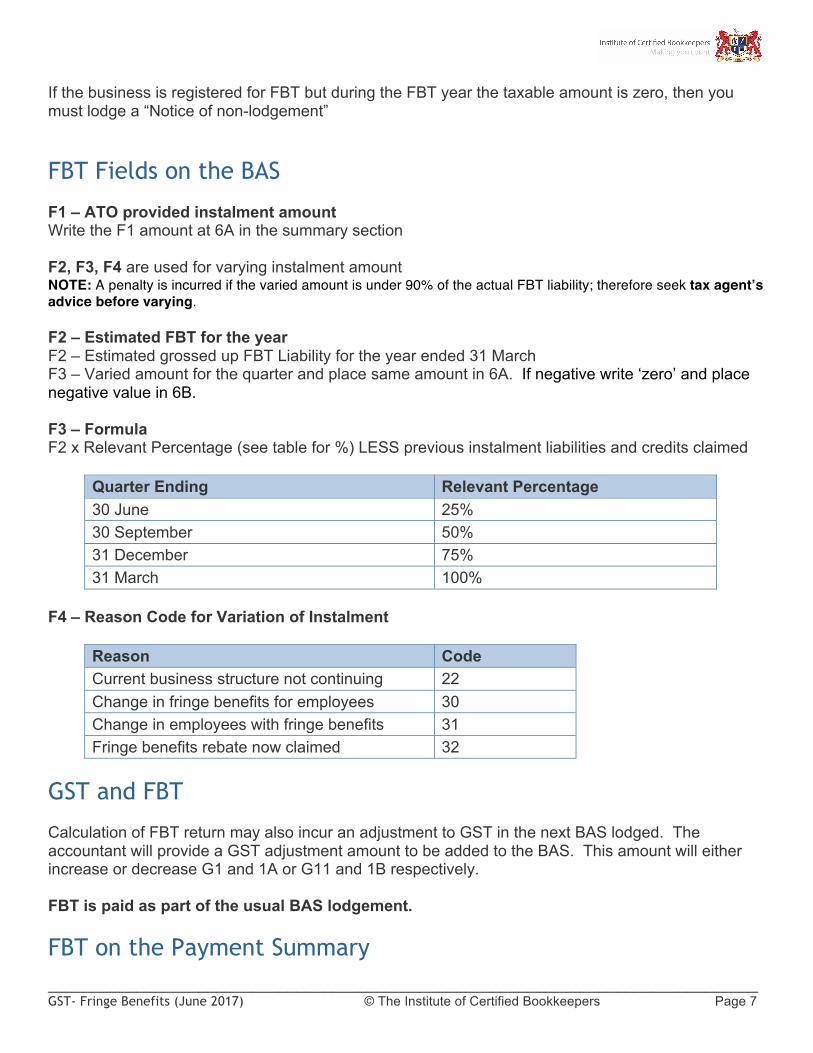

If the business is registered for FBT but during the FBT year the taxable amount is zero, then you must lodge a “Notice of non-lodgement” FBT Fields on the BAS F1 – ATO provided instalment amount Write the F1 amount at 6A in the summary section F2, F3, F4 are used for varying instalment amount NOTE: A penalty is incurred if the varied amount is under 90% of the actual FBT liability; therefore seek tax agent’s advice before varying. F2 – Estimated FBT for the year F2 – Estimated grossed up FBT Liability for the year ended 31 March F3 – Varied amount for the quarter and place same amount in 6A. If negative write ‘zero’ and place negative value in 6B. F3 – Formula F2 x Relevant Percentage (see table for %) LESS previous instalment liabilities and credits claimed

Quarter Ending Relevant Percentage 30 June 25% 30 September 50% 31 December 75% 31 March 100%

F4 – Reason Code for Variation of Instalment

Reason Code Current business structure not continuing 22 Change in fringe benefits for employees 30 Change in employees with fringe benefits 31 Fringe benefits rebate now claimed 32

GST and FBT Calculation of FBT return may also incur an adjustment to GST in the next BAS lodged. The accountant will provide a GST adjustment amount to be added to the BAS. This amount will either increase or decrease G1 and 1A or G11 and 1B respectively. FBT is paid as part of the usual BAS lodgement. FBT on the Payment Summary

________________________________________________________________________________ GST- Fringe Benefits (June 2017) © The Institute of Certified Bookkeepers Page 8

If an employee’s total fringe benefit amount in the FBT year (1 April to 31 March) exceeds $2,000.00, the amount must be “grossed-up” by the relevant rate and reported in the reportable fringe benefit amount field of the payment summary; this is entered manually, the software will not calculate this. The reportable amount is higher for some eligible not for profit organisations—see below for details. Verify the Reportable Amount with the Tax Agent If your employees have fringe benefits please contact the tax agent of the client to discuss which of these needs to be included on the payment summaries. A bookkeeper/BAS agent may assist the accountant and provide information, but they may not ascertain the amount of liability or advise the client. New FBT Reporting Requirement for 2017 Payment summaries must now show whether or not employers have an FBT exemption under Section 57A of the Fringe Benefits Tax Assessment Act 1986. If you report an FBT value on a payment summary you are required tick the following box

! Answer Yes if you have exemption under section 57A. (See Eligible Exemption Entitles) ! Answer No for employees of entities that are not eligible for an exemption.

Eligible Exemption Entities

! Registered public benevolent institution endorsed by the Commissioner of Taxation. ! Public hospitals. ! Hospital carried on by society/organisation that is a rebatable employer. ! Registered health promotion charity endorsed by Commissioner of Taxation. ! Provision of a public ambulance service.

Summary Although this information refers only to fringe benefits provided to employees, fringe benefits can also be provided to an employee’s friends or associates (such as a family member). Remember that to “ascertain and advise” on FBT liability is a tax agent matter, however, a bookkeeper or BAS agent can assist in compiling the material and providing information to the tax agent. The BAS agent can also submit the FBT as part of the BAS assuming the figures have been verified by a tax agent. References

! ATO – FBT Rates ! ATO - FBT Car Calculator ! ATO - Fringe Benefits Tax ! ATO - Entertainment ! ATO – FBT Exemptions ! ICB - Payment Summary Guide