gst transition provisions

TRANSCRIPT

TRANSITION PROVISONS

UNDER GST

CA LGopal Shah

Bhubaneswar

M: 9437124361

CGST ACT 2017

Section No Description of Provision

139 Migration of Existing Tax

payers

140 Transitional Arrangements for

Input Credits

141 Transitional Provision

Related to Job Work

142 Miscellaneous Transitional

Provisions.

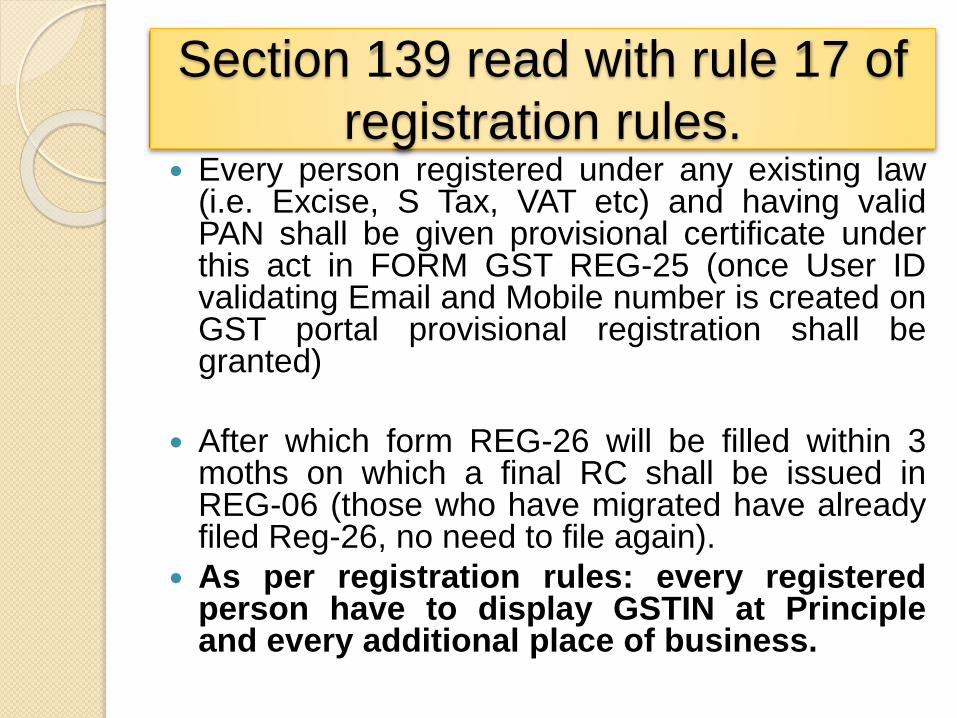

Section 139 read with rule 17 of

registration rules. Every person registered under any existing law

(i.e. Excise, S Tax, VAT etc) and having validPAN shall be given provisional certificate underthis act in FORM GST REG-25 (once User IDvalidating Email and Mobile number is created onGST portal provisional registration shall begranted)

After which form REG-26 will be filled within 3moths on which a final RC shall be issued inREG-06 (those who have migrated have alreadyfiled Reg-26, no need to file again).

As per registration rules: every registeredperson have to display GSTIN at Principleand every additional place of business.

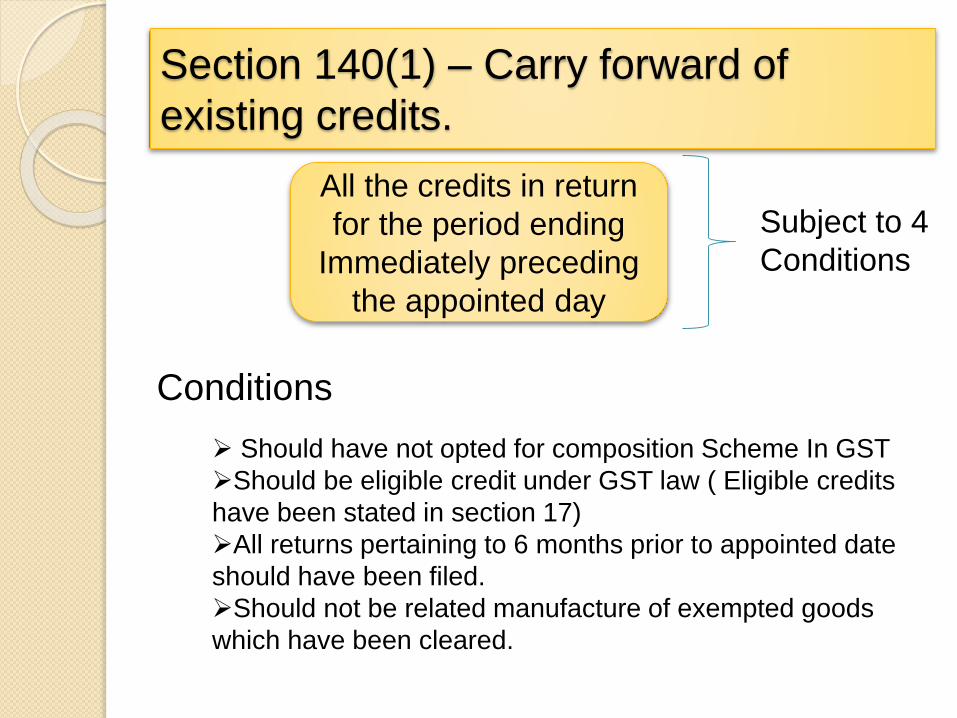

Section 140(1) – Carry forward of

existing credits.

All the credits in return

for the period ending

Immediately preceding

the appointed day

Subject to 4

Conditions

Conditions

Should have not opted for composition Scheme In GST

Should be eligible credit under GST law ( Eligible credits

have been stated in section 17)

All returns pertaining to 6 months prior to appointed date

should have been filed.

Should not be related manufacture of exempted goods

which have been cleared.

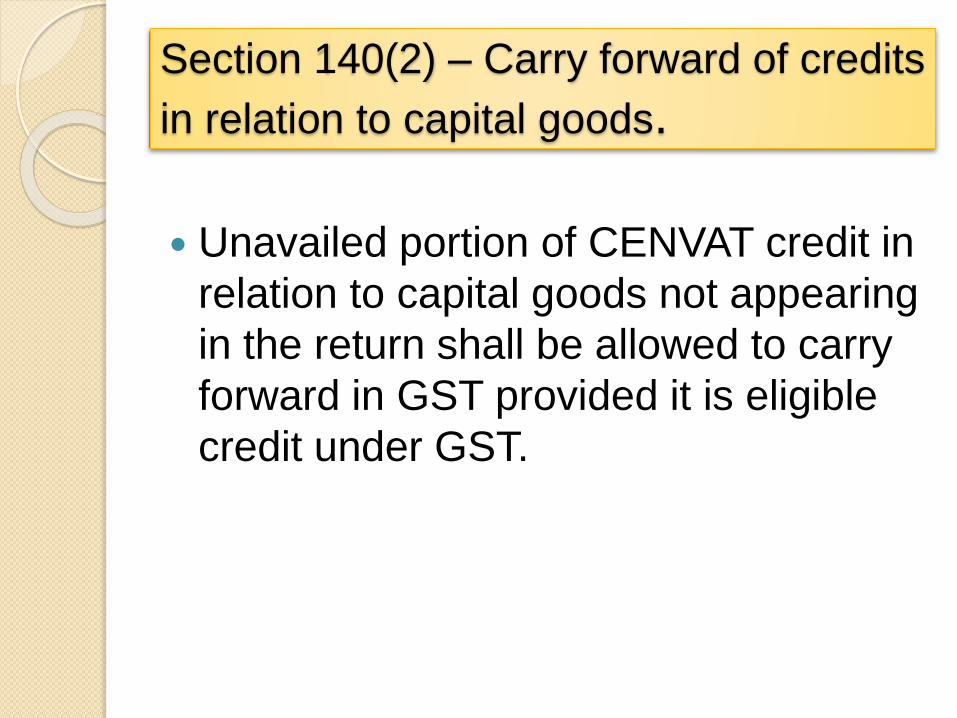

Section 140(2) – Carry forward of credits

in relation to capital goods.

Unavailed portion of CENVAT credit in

relation to capital goods not appearing

in the return shall be allowed to carry

forward in GST provided it is eligible

credit under GST.

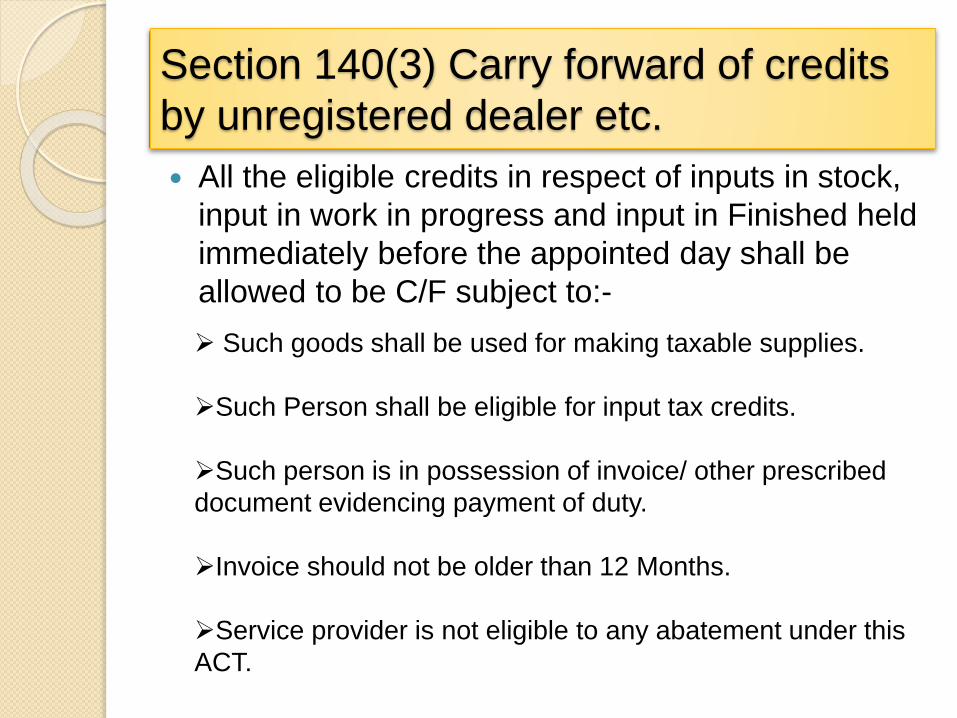

Section 140(3) Carry forward of credits

by unregistered dealer etc.

All the eligible credits in respect of inputs in stock,

input in work in progress and input in Finished held

immediately before the appointed day shall be

allowed to be C/F subject to:-

Such goods shall be used for making taxable supplies.

Such Person shall be eligible for input tax credits.

Such person is in possession of invoice/ other prescribed

document evidencing payment of duty.

Invoice should not be older than 12 Months.

Service provider is not eligible to any abatement under this

ACT.

Section 140(4) carry forward of credit by

manufacturer of exempted goods.

Manufacturer of exempted goods or

provider of exempted services which

are eligible to tax under GST shall

take credit of:-

◦ All the eligible duties in respect of inputs

held in stock, inputs held in work in

progress and inputs held in finished

goods as on the appointed day.

Section 140(5) Credits for inputs and

inputs services in transit.

All the inputs and inputs services received for

which taxes were paid under the previous law but

invoice received after the appointed day.

Credits in respect of such shall be allowed if the

invoice has been recorded within 30 days from the

appointed in books. (This period may be extended

by commissioner)

A statement in TRAN -1 is required to be filled.

Section 140(6) Credits by Manufacturer

paying fixed rate of duty All the eligible credits in respect of inputs in stock, input

in work in progress and input in Finished held immediately before the appointed day shall be allowed to be C/F subject to:-

Such inputs or goods are used or intended to be used for supply of taxable supply under GST.

Such person has not opted for composition scheme (GST)

Such registered person is eligible for ITC under GST

Invoices evidencing payment of duty are available.

Invoices shall not be older than 12 months.

Section 140(7) Input credits of Input

service distributor

Input tax credit on account of services

received before the appointed day by

ISD shall be eligible for distribution by

ISD even if invoices are received after

appointed day.

140(8) Credits of person having

centralized registration.

A person having centralised

registration may distribute credits

allowed to be carry forward between

registered persons having same

PAN(i.e. to branches in each state)

140(9) Credits of Input service reversed

earlier

Cenvat credit which were reversed

due to non payment within three

months shall be reclaimed under this

act subject to the condition that

payment has been made within 3

months of the appointed day.

Section 141(1) input sent to job worker

before appointed day

Inputs sent to job worker before the appointed day

and is received back from job worker after the

appointed day, NO GST shall be payable if

received within 6 months from appointed day which

may further be extended to 2 months by

commissioner.

If goods are not received back in 6 + 2 months

CCR claimed on such inputs in previous shall also

be recovered.

Section 141(2) Semi finished goods sent

to job worker before appointed day

Semi finished goods sent to job worker before the appointed day and is received back from job worker after the appointed day, NO GST shall be payable if received within 6 months from appointed day which may further be extended to 2 months by commissioner.

If goods are not received back in 6 + 2 months CCR claimed on inputs contained in such semi finished goods in previous shall also be recovered.

Goods may cleared from the job worker premises to any other registered person on payment of GST or may be exported without payment of GST.

Section 141(3) Finished goods sent to

job worker before appointed day

Finished goods sent to job worker before the appointed day and is received back from job worker after the appointed day, NO GST shall be payable if received within 6 months from appointed day which may further be extended to 2 months by commissioner.

If goods are not received back in 6 + 2 months CCR claimed on inputs contained in such semi finished goods in previous shall also be recovered.

Goods may cleared from the job worker premises to any other registered person on payment of GST or may be exported without payment of GST.

Condition for Section 141(1),

141(2) & 141(3) Both Job worker and principal

manufacture have to declare the stock

held by job worker on the appointed

day in such form and time as may be

prescribed.

Sec 142(1) Goods returned by Sold prior

to appointed day

Goods sold 6 months prior to the appointed date were returned within 6 months of the appointed day by person other than registered person, registered person (Seller ) shall be eligible for refund of duty.

If goods are returned by registered person, such return shall be treated as supply under GST.

Section 142(2) Revision in price for

supplies made earlier. Where there is any upward revision in price of supplies

made prior to the appointed date, registered person shall issue supplementary invoice within 30 days of such revision, such supplementary invoice shall be deemed to be invoice issued for supply under this act.

Where there is any downward revision in price of supplies made prior to the appointed date, registered person may issue credit note within 30 days of such revision, such credit shall be deemed to be Credit note issued for supply under this act.

On the basis of such credit note registered person shall be allowed to reduce its output tax liability provided recipient of credit note has reduced its credit

Section 142(3)- 142(5) Refund claim for

previous CCR, Duty etc

Any refund claim filed after the appointed day shall

be disposed of in accordance with the provision of

existing law and any amount accruing shall be paid

in cash.

If any claim is rejected the amount so rejected shall

lapse.

No claim for CCR carry forward under this act shall

be available.

Section 142(6) -142(9) - Proceeding

of Appeal review or Reference

Any appeal proceeding review or reference relating

to CENVAT credit or output tax liability initiated

before on or after the appointed day shall be

disposed of in accordance with the provisions of

existing law.

Sec 142(10)

Goods Supplied on or after the

appointed in pursuant to contract

entered before the appointed day shall

be chargeable to GST.

142(12) Goods sent on Approval

Basis Goods sent on approval basis

received back with in 6 months shall

not be chargeable to tax

142(13) TDS on supply of

Goods Where any TDS was required to be

deducted under any law for supply

made before the appointed day, no

TDS shall be deducted if payment is

made on or after the appointed Day.

THANK YOU