gtuc conference powerpoint: demand for cross border payments in west africa

TRANSCRIPT

Demand for Cross Border Payments in West Africa – Lessons from GILA

Public Presentation1

A 2-DAY CONFERENCE ON MOBILE MONEY UPTAKE IN GHANADate: 12th – 13th March, 2013 Venue: Ghana Technology University College

Ghana Technology University College (GTUC) in partnership with the Institute for Money, Technology and Financial Inclusion (IMTFI) USA, hosts a two-day conference aimed at creating awareness and increasing the uptake of Mobile Money Services in Ghana.

Funding from2

Why GILA?3

Present economic activity and future projected economic growth largely follows the Gulf of Guinea coastline.

Who is Involved in Cross Border Transactions?

4

We conducted a modest research project in Sept. 2012 and interviewed 214 travelers crossing one of three borders: Aflao-Lome, Savicodji-Hillacodji and Seme-Badagary.

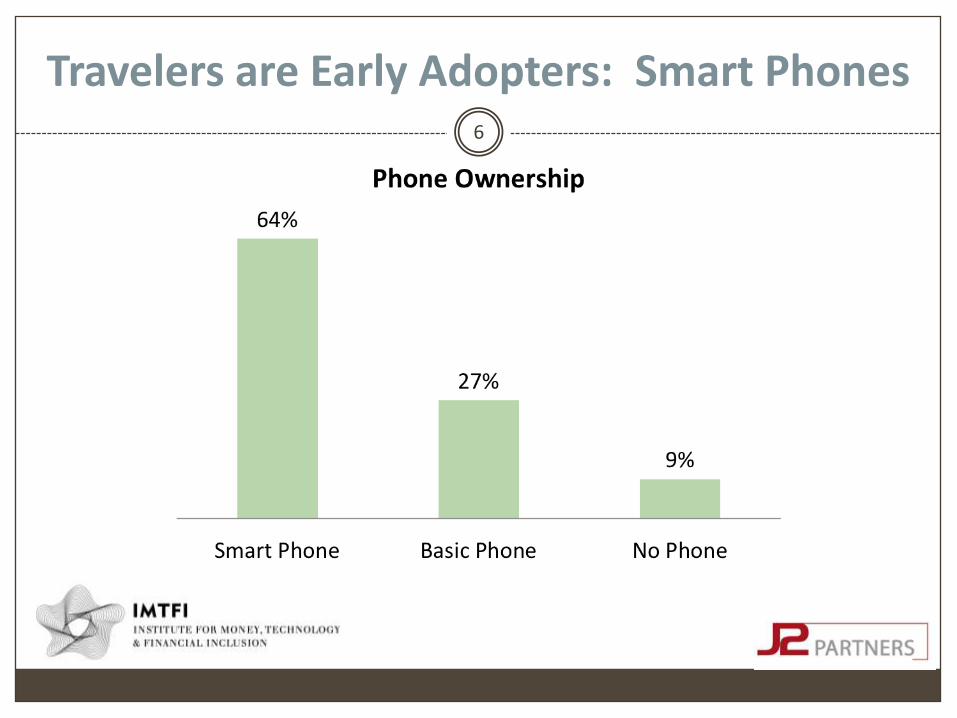

Respondents were more likely to be banked, to have bank cards, and to have mobile money accounts than national averages. Most everyone carries one or more phones and multiple SIM cards.

Who is Involved in Cross Border Transactions? cont’d

5

Togo, 22%

Benin, 22%

Ghana, 23%

Nigeria, 29%

Other, 3%

Citizenship of Survey Participants:

Travelers are Early Adopters: Smart Phones6

Travelers are Early Adopters: Banking7

• Throughout GILA, far more people are unbanked and underbanked than banked, yet 46% of survey respondents reported carrying bank cards.

• Only 1/3 of these 46% reported use, or planned use, of an ATM. More were carrying whatever cash they needed for the trip.

• 14% of respondents had mobile money accounts

Yet Travelers Remain Dependent on Cash8

• Overall most everyone depends on cash. The largest group of travelers, traders, were slightly more likely to be reliant on carrying cash, less likely to use ATMs, than other travelers.

• 4% of respondents were carrying airtime they planned to resell

• Problems with Cash -- 29% of respondents had experience with significant non-trivial theft and this group was less likely to have either a bank card or mobile money account than those who have not had this negative experience.

Opportunity: Platform, Audience & Demand

9

Summary

• The technology is in people’s hands now;

• The characteristics of those traveling is they are relatively more sophisticated than the overall population and this may represent solid footing for launching services;

• Those is the BOP in particular experiences difficulties associated with cash.

Who Moves Money Cross Borders?10

A few regional banks, Ecobank, UBA offer cross-border payment and remittance products and platforms and are agents of money transfer firms such as Western Union and MoneyGram.

Two regional upstarts based in Senegal, Groupe Chaka (Money Express) and Cellular Systems International (WARI), have a particularly strong presence in Togo and Benin.

Still not much consumer or institutional choice. Informal foreign exchange is big business. Transactions can involve millions of dollars and are based on trust. These businesses evade regulations and have the political connections to do this effectively.

• Most cash movement is non-commercial. Cash is carried, either on one’s person, or via a “carrier”.

Informal Money Changer at Seme, Benin11

“Informal” is the norm12

Within GILA, most economic activity is informal, widely used by all, banked and non-banked alike. This occurs for good reasons:

Informal businesses are less costly than formal services, in an environment of tremendous price sensitivity.

People trust informal services and distrust formal for reasons of habit, familiarity and education.

Informal services are also more convenient, with better hours and better coverage than offered at banks.

For traders, especially, informal system anonymity is crucial.

Moving from Informal to Semi-Formal or Formal13

Can the present informal sector actors be encouraged to participate in new formal structures, or must they be disintermediated?

Can privacy replace anonymity?

Education and awareness. Payment service providers must provide offerings that meet needs. Those who are deeply unbanked are most likely to follow their peers.

Active involvement of enforcement agents. JP Morgan: “if the government does not know how to collect taxes, then a man is a fool to pay them.”

Banks don’t want very low value transactions so there is no competing business model for cash. Formal sector actors historic prerogative to have their price, must be reinvented. Traders, maybe poorly educated, understand their businesses well and they recognize value. Price almost always wins – can the mobile money industry deliver?

Long Term Infrastructure Investments14

Integrating national bank switches for ATM, card and mobile interoperation. Fast-track World Bank project now underway. Phase One pilots will be tailored around existing regulations, lowest common denominators and launch later in 2013.

Pioneering work to digitize (and allow payment for) customs, immigration, and foreign exchange processes is ahead.

Coordination between telecoms serving adjacent markets to ensure data coverage.

Possible ways forward: Test & Learn Pilots15

Pilot #1

Extend mobile money agents across borders.

Ghana has five mobile money services, Benin has one and Nigeria has more than a dozen. These services might be permitted to engage agents across their borders. East Africa may prove a model.

Benin to Togo

Ghana to Togo

Nigeria and Ghana

Etc.

Any cross border pilot would require regulatory approval

Possible ways forward: Test & Learn Pilots16

Pilot #2

Facilitate cross-border airtime sales.

Airtime is tricky.

Mobile money agents might be permitted to sell pins back into the system.

Multiple currency universal airtime sales – technically feasible, but there are practical barriers.

Any cross border pilot would require regulatory approval

Possible ways forward: Test & Learn Pilots17

Pilot #3

Permit a Peer to Peer foreign exchange service.

A service branded KlickEx has piloted very successfully in the south Pacific islands, where there are many micro-currencies.

Soon to launch worldwide with http://www.passportfx.com. All are invited to the private beta.

Any cross border pilot would require regulatory approval

Possible ways forward: Test & Learn Pilots18

Pilot #4: Federate Identity Tokens

Financial exclusion is often associated with an inability to provide proof of identity. Experiments in other countries use mobile phones as instruments of identity.

Privacy is extremely important – and must be guaranteed – if it is to effectively replace anonymity.

Are there private sector approaches to privacy that can work on any handset? Can this innovation come out of Africa?

Any cross border pilot would require regulatory approval

Thank you19

Joel PatenaudeManaging Partner

J2 Partners Inc. 183 Park Street, Montclair, NJ 07042 USA

Email: [email protected] | Office: 973.509.0101 | Mobile: 973.650.4162Web: http://www.j2partnerscoaching.com |Twitter: http://twitter.com/J2Partners