guidance regarding the commission’s rules relating to ... regarding the commission's...

TRANSCRIPT

JFSC.Basel II.M5TB Trading Book Guide – February 2008 1

Guidance regarding the Commission’s rules relating to Trading Books:

Including the Commission’s prudential reporting

requirements for Jersey incorporated deposit takers that have a trading book

Issued February 2008

JFSC.Basel II.M5TB Trading Book Guide – February 2008 2

CONTENTS SECTION 1 Introduction ................................................................................................................... 4 SECTION 2 Trading book rules: General ........................................................................................ 6

Definition of the trading book ..................................................................................... 6 Internal hedges .............................................................................................................. 7 Systems and controls for the trading book ................................................................ 8 Bank’s trading book policies ....................................................................................... 8

SECTION 3 FX and Gold ................................................................................................................. 10 Introduction ................................................................................................................. 10 Foreign exchange positions ....................................................................................... 10 Gold ............................................................................................................................... 11 Capital charge .............................................................................................................. 11

SECTION 4 Interest Rate Risk ........................................................................................................ 13 Introduction ................................................................................................................. 13 Specific interest rate risk ............................................................................................ 13 Large Exposures: Interest rate and equity risk; policy and incremental capital charge ............................................................................................................... 15 Capital charge .............................................................................................................. 16 General interest rate risk ............................................................................................ 17 Capital charge .............................................................................................................. 19

SECTION 5 Equity Risk ................................................................................................................... 20 Introduction ................................................................................................................. 20 Specific and general equity risk ................................................................................ 20 Equity derivatives ....................................................................................................... 20

SECTION 6 Commodity Risk ......................................................................................................... 23 Introduction ................................................................................................................. 23 Reporting and calculation of capital charge ............................................................ 23 Capital charge .............................................................................................................. 23 Top five commodities ................................................................................................. 24

SECTION 7 Settlement Risk ............................................................................................................ 25 Introduction ................................................................................................................. 25 Failed DvP trades ........................................................................................................ 25 Treatment ..................................................................................................................... 25 Free deliveries .............................................................................................................. 26 Summary of settlement risk ....................................................................................... 27

SECTION 8 OTC Derivatives .......................................................................................................... 28 Introduction ................................................................................................................. 28 Treatments that are the same as in the banking book ........................................... 28

JFSC.Basel II.M5TB Trading Book Guide – February 2008 3

Treatment of credit derivatives booked in the trading book ................................ 29 SECTION 9 Repo, Reverse-repo and Other Counterparty Risk ................................................ 31

Introduction ................................................................................................................. 31 SECTION 10 Trading Book Risk Summary .................................................................................... 32

Trading book risk – capital charges .......................................................................... 32 Appendix A: Treatment of Options ................................................................................................. 33 Appendix B: Incremental Capital for Large Exposures: Example............................................... 37 Appendix C: Allowable Offsetting of Matched Positions ............................................................ 39 Appendix D: Qualifying Indices ....................................................................................................... 40

JFSC.Basel II.M5TB Trading Book Guide – February 2008 4

SECTION 1 INTRODUCTION

Overview

1.1 The trading book of a bank consists of all positions in financial instruments and commodities held either with trading intent or in order to hedge other elements of the trading book and which are either free of any restrictive covenants on their tradability or are able to be hedged. Section 2 sets out the Commission’s general rules relating to trading books, whilst Sections 3 to 9 address the Commission’s reporting requirements for banks that have adopted the standardised approach to market risk under Basel II.

1.2 Trading book activity gives rise to market risk and counterparty risk and Sections 3 to 9 set out the appropriate treatments for both. Section 10 explains how the summary sheet is laid out in the return; no input is required on this sheet.

1.3 Market risk is defined as the risk of losses in on and off-balance sheet positions arising from movements in market prices. The risks subject to a capital requirement in Jersey for all banks are: • Foreign exchange risk; • Interest rate risk; • Equity risk; and • Commodities risk.

1.4 Counterparty risk covers: • Settlement risk; the risk that arises through failed trades and non delivery

versus payment (“DvP”) transactions. This treatment is the same as for banking book transactions, as set out in “Guidance regarding the completion of the Market Risk (Subsidiaries) prudential reporting module”, issued in September 2007;

• Counterparty risk in respect of OTC derivatives in the trading book; • Sale and repurchase (“repo”) transactions and reverse-repo transactions; and • Other counterparty risk, including fees and margins receivable.

1.5 The rules set out in Sections 3 to 9 relate to the completion of standardised approach reporting forms. These are:

• Section 3 - FX & Gold

• Section 4 –Interest rate risk

• Section 5 – Equity risk

• Section 6 – Commodity risk

• Section 7 – Settlement Risk

• Section 8 – OTC derivatives

• Section 9 – Repo, Reverse-repo and other counterparty risk.

JFSC.Basel II.M5TB Trading Book Guide – February 2008 5

1.6 Throughout the guidance in Sections 3 to 9, references to “Table X” refer to the relevant section “X” of the appropriate spreadsheet in the Module.

1.7 Subsidiaries are reminded of the requirement to ensure that they adhere to their minimum risk asset ratio requirement at all times. This must include a daily assessment of the capital required to support their trading book.

JFSC.Basel II.M5TB Trading Book Guide – February 2008 6

SECTION 2 TRADING BOOK RULES: GENERAL

Definition of the trading book

2.1 The trading book of a bank consists of all positions in financial instruments and commodities held either with trading intent or in order to hedge other elements of the trading book and which are either free of any restrictive covenants on their tradability or able to be hedged. The term “position” includes proprietary positions and positions arising from client servicing (see paragraph 2.2) and market making.

2.2 Positions arising from client servicing include those arising out of contracts where a bank acts as principal (even in the context of activity described as 'broking' or 'customer business'). Such positions should be allocated to a bank's trading book if the intent is trading (see paragraph 2.6). This applies even if the nature of the business means that generally the only risks incurred by the bank are counterparty risks (i.e. no market risk charges apply).

2.3 Fixed-term trading-related repo-style transactions that a bank accounts for in its banking book may be included in the trading book for capital requirement purposes so long as all such repo-style transactions are included. For this purpose, fixed-term trading-related repo-style transactions are defined as those that meet the requirements of paragraphs 2.2, 2.6 and 2.7, and both legs are in the form of either cash or securities includable in the trading book.

2.4 Capital requirements for fixed-term trading-related repo-style transactions are the same for the standardised approaches whether the risks arise in the trading book as counterparty risk or in the banking book as credit risk.

2.5 “Financial instrument” means any contract that gives rise to both a financial asset of one party and a financial liability or equity instrument of another party and includes both primary financial instruments (or cash instruments) and derivative financial instruments, the value of which is derived from the price of an underlying financial instrument, a rate, an index or the price of another underlying item. Generally, for the purpose of this definition: • A financial asset means cash, the right to receive cash or another financial

asset, the contractual right to exchange financial instruments on potentially favourable terms or an equity instrument; and

• A financial liability means the contractual obligation to deliver cash or another financial asset or to exchange financial instruments under conditions that are potentially unfavourable.

2.6 Positions held with trading intent for the purpose of the definition of the trading book are those held intentionally for short-term resale and/or with the intention of benefiting from actual or expected short-term price differences between buying and selling prices, or from other price or interest rate variations. Trading intent must be evidenced on the basis of the strategies, policies and procedures set up by the bank to manage the position or portfolio in accordance with paragraph 2.7.

JFSC.Basel II.M5TB Trading Book Guide – February 2008 7

2.7 Positions/portfolios held with trading intent must comply with the following requirements: • There must be a clearly documented trading strategy for the

position/instrument or portfolios, approved by senior management, which must include the expected holding horizon;

• There must be clearly defined policies and procedures to monitor the position against the bank's trading strategy including the monitoring of turnover of positions in the bank’s trading book and positions that have not been traded recently but are included in the bank's trading book; and

• There must be clearly defined policies and procedures for the active management of the position, which must include the following: (a) Each position must be entered into by a trading desk1; (b) Position limits are set and monitored for appropriateness; (c) Dealers have the autonomy to enter into/manage the position within

agreed limits and according to the approved strategy; (d) Positions are reported to senior management as an integral part of the

bank's risk management process; and (e) Positions are actively monitored with reference to market information

sources and an assessment made of the marketability or hedge-ability of the position or its component risks, including the assessment of the quality and availability of market inputs to the valuation process, level of market turnover and sizes of positions traded in the market.

Internal hedges

2.8 Internal hedges, where one leg is booked in the banking book whilst the other is booked in the trading book, may be included in the trading book, in which case the following paragraphs apply: • An internal hedge is a position that materially or completely offsets the

component risk element of a banking book position or a set of positions. Positions arising from internal hedges are eligible for trading book capital treatment, provided that they are held with trading intent and that the general criteria on trading intent and prudent valuation specified in 2.7 and the trading book systems and controls rules (2.11 to 2.14) are complied with. In particular: (a) Internal hedges must not be primarily intended to avoid or reduce

capital requirements; (b) Internal hedges must be properly documented and subject to particular

internal approval and audit procedures; (c) The internal transaction must be dealt at the market rate for such a deal

given prevailing market conditions; (d) The bulk of the market risk that is generated by the internal hedge

must be dynamically managed in the trading book within authorised limits; and

1A desk where transactions for trading financial instruments occur. Trading desks can be either large or small depending on the firm and a firm may have one or more trading desks, usually each specialising in certain types of trading activity. Each trading desk will be manned by one or more traders and will have appropriate systems, including those required to deliver pricing, dealing with counterparties and deal capture.

JFSC.Basel II.M5TB Trading Book Guide – February 2008 8

(e) Internal transactions must be carefully monitored. • Monitoring must be ensured by adequate procedures. • The treatment applies without prejudice to the capital requirements

applicable to the "banking book leg" of the internal hedge.

2.9 However, notwithstanding the above, when a bank hedges a banking book credit risk exposure using a credit derivative booked in its trading book (using an internal hedge), the banking book exposure is not deemed to be hedged for the purposes of calculating capital requirements unless the bank purchases from an eligible third party protection provider a credit derivative meeting the requirements with regard to the banking book exposure (as set out in “Guidance regarding the completion of the prudential reporting module for banks using the standardised approach to credit risk“). Where such third party protection is purchased and is recognised as a hedge of a banking book exposure for the purposes of calculating capital requirements in the banking book, neither the internal nor external credit derivative hedge may be included in the trading book for the purposes of calculating capital requirements.

Systems and controls for the trading book

2.10 A bank must implement policies and procedures for the measurement and management of all material sources and effects of market risk.

2.11 A bank must establish and maintain systems and controls to manage its trading book, in accordance with the trading book systems and controls rules and other rules contained within this Section.

2.12 A bank must establish and maintain systems and controls sufficient to provide prudent and reliable valuation estimates.

2.13 Systems and controls must include at least the following elements: • Documented policies and procedures for the process of valuation (including

clearly defined responsibilities of the various areas involved in the determination of the valuation, sources of market information and review of their appropriateness, frequency of independent valuation, timing of closing prices, procedures for adjusting valuations, month end and ad-hoc verification procedures); and

• Reporting lines for the department accountable for the valuation process that are clear and independent of the front office. The reporting line in relation to these matters must ultimately be to an executive director on the bank's governing body.

Banks’ trading book policies

2.14 A bank must have clearly defined policies and procedures for determining which positions to include in the trading book for the purposes of calculating its capital requirements, consistent with the criteria set out in this Section and taking into account the bank's risk management capabilities and practices. Compliance with these policies and procedures must be fully documented and subject to periodic internal audit.

2.15 A bank must have clearly defined policies and procedures for overall management of the trading book. As a minimum, these policies and procedures must address:

JFSC.Basel II.M5TB Trading Book Guide – February 2008 9

• The activities the bank considers to be trading and as constituting part of the trading book for capital requirement purposes, including: (a) The financial instruments and commodities that the bank proposes to

trade in, including the currencies, maturities, issuers and quality of issues; and

(b) Any instruments to be excluded from its trading book. • The extent to which a position can be marked-to-market daily by reference to

an active, liquid two-way market; • For positions that are marked-to-model, the extent to which the bank can:

(a) Identify all material risks of the position; (b) Hedge all material risks of the position with instruments for which an

active, liquid two-way market exists; and (c) Derive reliable estimates for the key assumptions and parameters used

in the model; • The extent to which the bank can, and is required to, generate valuations for

the position that can be validated externally in a consistent manner; • The extent to which legal restrictions or other operational requirements

would impede the bank's ability to effect a liquidation or hedge of the position in the short term;

• The extent to which the bank can, and is required to, actively risk manage the position; and

• The extent to which the bank may transfer risk or positions between the banking book and trading book and the criteria for such transfers.

2.16 The policies and procedures referred to above must be recorded in a single written document. A bank may record these policies and procedures in more than one written document if the bank has a single written document that identifies: • All those other documents; and • The parts of those documents that record those policies and procedures.

2.17 A bank must notify the Commission as soon as is reasonably practicable when it adopts a trading book policy. A bank must notify the Commission as soon as is reasonably practicable if the trading book policy becomes subject to significant changes. A significant change for the purpose of this rule includes new types of customers or business.

2.18 There is likely to be an overlap between what the trading book policy should contain and other documents such as dealing or treasury manuals. A cross reference to the latter in the trading book policy is adequate and material in other documents need not be set out again in the trading book policy. However, where this is the case, the matters required to be included in the trading book policy should be identified in the trading book policy.

2.19 The trading book policy may be prepared on either a consolidated or a solo basis. It should be prepared on a consolidated basis when a group either manages its trading risk centrally or employs the same risk management techniques in each group member. A trading book policy prepared on a consolidated basis should set out how it applies to each bank in the group and should be approved by each bank's governing body.

JFSC.Basel II.M5TB Trading Book Guide – February 2008 10

SECTION 3 FX AND GOLD

Introduction

3.1 The risks arising from foreign currency and gold exposures are similar and hence this form addresses both. In both cases, current and future exposures may be offset so as to arrive at a net figure. Banks using options should read Appendix A, which addresses how these should be reported.

Foreign exchange positions

3.2 Positions in the reporting currency of the submitting bank should not be reported; the return calculates a balancing item corresponding to the effective position in this currency. For most submitting banks this means that row A.1 (Pounds Sterling) should be blank.

3.3 The major currencies should be reported separately, namely Pounds Sterling (“GBP”), US Dollars (“USD”), Euros (“EUR”), Swiss Francs (“CHF”), Canadian Dollars (“CAD”), Japanese Yen (“JPY”) and Australian Dollars (“AUD”). Other currencies should be split into two groups according to whether the bank is long or short, which is in turn based on whether the net overall position in that currency is positive.

• Other – Long Currencies: Group together currencies where the net overall position in that individual currency is positive; or

• Other – Short Currencies, where the net overall position in that individual currency is negative.

3.4 Note that the net overall position is the sum of all balance sheet assets less balance sheet liabilities plus/minus net forward purchases/sales.

3.5 All input figures should correspond to the gross amount.

3.6 Table A: Foreign Currency Positions ITEM DESCRIPTION COMPLETION NOTES

A.1 to A.9

Gross Assets Total balance sheet assets denominated in the foreign currency in question or group of currencies.

Gross Liabilities Total balance sheet liabilities denominated in the foreign currency in question or group of currencies.

Net spot position A calculated field, being equal to “gross assets” less “gross liabilities”.

Gross forward purchases

All forward purchases of the foreign currency or group of currencies.

Gross forward sales All forward sales of the foreign currency or group of currencies.

JFSC.Basel II.M5TB Trading Book Guide – February 2008 11

ITEM DESCRIPTION COMPLETION NOTES

A.1 to A.9 (cont.)

Net forward purchases A calculated field, being equal to “gross forward purchases” less “gross forward sales”.

Net overall position A calculated field, being the sum of the “net spot position” and the “net forward purchases” entries. NB a negative value here indicates a short position; a positive value indicates a long position.

A.10 Balancing item A calculated field, being the position required to make the overall total of net long and short positions in all currencies, taken together, equal to zero.

A Aggregate net long position

A calculated field being the sum of all “long” positions including the entry for the “sterling balancing item” if it is positive. This aggregate of net long open positions, which will be positive or zero, is included in the risk asset ratio calculation.

Gold

3.7 Report any position for gold. Note that the net overall position in gold is the sum of all balance sheet gold assets less balance sheet gold liabilities plus/minus net forward purchases/sales of gold.

3.8 All input figures should correspond to the gross amount.

3.9 Table B: Gold:

ITEM DESCRIPTION COMPLETION NOTES

B Gross Assets Total balance sheet gold assets.

Gross Liabilities Total balance sheet gold liabilities.

Net spot position A calculated field, being equal to “gross assets” less “gross liabilities”.

Gross forward purchases

All forward purchases of gold.

Gross forward sales All forward sales of gold.

Net forward purchases

A calculated field, being equal to “gross forward purchases” less “gross forward sales”.

Net overall position A calculated field, being the sum of the “net spot position” and the “net forward purchases “entries.

Capital charge

3.10 Table C calculates the risk capital charge, being 8% of the sum of the “Aggregate net long position” from Table A and 8% of the absolute value for the “Net overall position” in gold from Table B.

JFSC.Basel II.M5TB Trading Book Guide – February 2008 12

3.11 Table D calculates the total foreign exchange risk requirement, being the total from Table C plus the amount calculated by the bank and input in D.1 as representing the additional capital charge for options, as calculated in accordance with Appendix A.

JFSC.Basel II.M5TB Trading Book Guide – February 2008 13

SECTION 4 INTEREST RATE RISK

Introduction

4.1 This section describes the standardised approach for measuring the risk of holding or taking positions in debt securities and other interest rate related instruments in the trading book. The instruments covered include all fixed-rate and floating-rate debt securities and instruments that behave similarly, including non-convertible preference shares. Convertible bonds, i.e. debt issues or preference shares that are convertible, at a stated price, into common shares of the issuer, will be treated as debt securities if they trade in a manner similar to debt securities and as equities if they trade in a manner similar to equities.

4.2 The minimum capital requirement is expressed in terms of two separately calculated charges, one applying to the “specific risk” of each security, whether it is a short or a long position, and the other applying to the interest rate risk in the portfolio (termed “general risk”). Long and short positions in different securities or instruments can be offset but banks should be familiar with Appendix C, which covers the offsetting of positions more fully.

Specific interest rate risk

4.3 Complete Tables A to C by entering the “Gross Amount” for each “Specific Risk Charge %” category, being the sum of all positions that attract that “Specific Risk Charge %”.

4.4 The “Specific Risk Charge %” is determined by the type, rating and maturity of the position and can be found from the following table:

Categories External credit assessment

Specific Risk Charge %”

Government AAA to AA- 0%. A+ to BBB- 0.25% (residual term to final maturity 6 months or less).

1.00% (residual term to final maturity greater than 6 and up to and including 24 months). 1.60% (residual term to final maturity exceeding 24 months).

BB+ to B- 8%. Below B- 12%. Unrated 8%.

Qualifying 0.25% (residual term to final maturity 6 months or less). 1.00% (residual term to final maturity greater than 6 and up to and including 24 months).

1.60% (residual term to final maturity exceeding 24 months). Other Determined as 8% of the risk weight for a corporate exposure with the

same rating as the position, according to the standardised approach to credit risk (“SAC”) guide published by the Commission (i.e. 8% for a 100% risk weight item and 12% for a 150% risk weight item).

JFSC.Basel II.M5TB Trading Book Guide – February 2008 14

4.5 The category “Government” will include all forms of government paper, including bonds, Treasury bills and other short-term instruments.

4.6 The “Qualifying” category includes securities issued by public sector entities and multilateral development banks, plus other securities that: • Are rated BBB- or higher by at least two external credit assessment

institutions (“ECAIs”) that are in the list of eligible ECAIs published by the Commission. As of February 2008 these comprised: (a) Moody’s; (b) Standard & Poor’s; and (c) Fitch; or

• Are only rated by one eligible ECAI and this rating is BBB- or higher.

4.7 For banks using a Commission approved advanced approach for credit risk for a portfolio, unrated securities can be included in the “Qualifying” category if both of the following conditions are met: • The securities are rated equivalent to investment grade under the reporting

bank’s internal rating system; and • The issuer has securities listed on a recognised stock exchange.

4.8 The “Net Amount” reported should be the “Gross Amount” less offsetting allowed for positions hedged by credit derivatives. A full allowance will be recognised when the values of two legs (i.e. long and short) always move in the opposite direction and broadly to the same extent. This would be the case in the following situations: • The two legs consist of completely identical instruments, or • A long cash position is hedged by a total rate of return swap (or vice versa)

and there is an exact match between the reference obligation and the underlying exposure (i.e. the cash position).

4.9 In these cases, no specific risk capital requirement applies to both sides of the position.

4.10 An 80% offset will be recognised when the value of two legs (i.e. long and short) always moves in the opposite direction but not broadly to the same extent. This would be the case when a long cash position is hedged by a credit default swap or a credit linked note (or vice versa) and there is an exact match in terms of the reference obligation, the maturity of both the reference obligation and the credit derivative, and the currency of the underlying exposure. In addition, key features of the credit derivative contract (e.g. credit event definitions, settlement mechanisms) should not cause the price movement of the credit derivative to materially deviate from the price movements of the cash position. To the extent that the transaction transfers risk (i.e. taking account of restrictive payout provisions such as fixed payouts and materiality thresholds), an 80% specific risk offset will be applied to the side of the transaction with the higher capital charge, while the specific risk requirement on the other side will be zero.

4.11 Partial allowance (as set out in paragraph 4.12) will be recognised when the value of the two legs (i.e. long and short) usually moves in the opposite direction. This would be the case in the following situations: • The position would be captured by 4.8, but there is an asset mismatch

between the reference obligation and the underlying exposure;

JFSC.Basel II.M5TB Trading Book Guide – February 2008 15

• The position would be captured by 4.8 or 4.10 but there is a currency or maturity mismatch between the credit protection and the underlying asset; or

• The position would be captured by 4.10 but there is an asset mismatch between the cash position and the credit derivative. However, the underlying asset is included in the (deliverable) obligations in the credit derivative documentation.

4.12 In each of the cases in 4.11, the following rule applies: rather than adding the specific risk capital requirements for each side of the transaction (i.e. the credit protection and the underlying asset) only the higher of the two capital requirements will apply.

4.13 In cases not captured in 4.8 to 4.11, a specific risk capital charge will be assessed against both sides of the position.

4.14 With regard to banks’ first-to-default and second-to-default products in the trading book, the basic concepts developed for the banking book will also apply. Banks holding long positions in these products (e.g. buyers of basket credit linked notes) would be treated as if they were protection sellers and would be required to add the specific risk charges or use the external rating if available. Issuers of these notes would be treated as if they were protection buyers and are therefore allowed to off-set specific risk for one of the underlying reference exposures, i.e. the asset with the lowest specific risk charge.

Large Exposures: Interest rate and equity risk; policy and incremental capital charge

4.15 The Commission’s Large Exposure policy recognises that positions held in a bank’s trading book are not subject to the pre-approval requirements applicable to “Large Exposures” in the banking book.

4.16 If a bank with a trading book has an exposure to an issuer arising from the inclusion of holdings of tradable securities in its trading book which exceeds 25% of its agreed capital base, the use of soft limits should be agreed in writing with the Commission. The soft limit agreed with the Commission for an individual counterparty/issuer is an overall limit on the total exposure to that counterparty/issuer. Soft limits are not subject to the Commission’s limits for large exposures, such as the 800% rule for the total of approved large exposures.

4.17 When soft limits have been agreed, the bank’s agreed capital base may be amended to include any tier 3 capital eligible to support risks in the bank’s trading book. This is the trading book capital base (“TBCB”).

4.18 Any exposure, other than an exempt exposure, in excess of 25% of the bank’s TBCB held in the bank’s trading book should only arise as a result of normal holdings of tradable securities.

4.19 Incremental capital in respect of an exposure’s excess over 25% of the TBCB should be calculated (as set out in paragraph 4.20). The capital amount calculated should be included in the calculation for determining how much trading book capital a bank should have.

4.20 However, an exposure need not be further pre-notified to the Commission if it is within an agreed soft limit. It should still be post-notified to the Commission by the close of business on the date when the total exposure first exceeds 25% of the bank’s TBCB and again when it falls back within 25% of the bank’s TBCB.

JFSC.Basel II.M5TB Trading Book Guide – February 2008 16

Furthermore, it should be reported in the “Other Prudential” Module within the Large Exposures sheet. Banks are also required to hold incremental capital against these trading book exposures, and this should be computed as follows and reported in Table D:

(a) Net any short securities positions against long securities positions; netting the short items against the highest specific risk weighted long items. The specific risk weights of netted items need not be identical; the rules are set out earlier in this Section for interest rate risk and in Section 5 for equity risk.

(b) Rank the remaining net long securities positions in order, according to specific risk weighting factors.

(c) Taking the lowest weighted items first, apply these exposures to the difference between the non-securities exposure to the counterparty and 25% of the TBCB i.e. the ‘headroom’ up to 25% of the TBCB is used to cover the lowest weighted exposures first.

(d) Incremental capital should be calculated for the remaining net long securities exposures as follows: • If the excess exposure has been outstanding for 10 days or less, the

specific risk charges for the exposures in excess of 25% of the amended agreed capital base should be entered in D.1 and the resultant incremental charge will be 200% of this amount.

• If the excess exposure has been outstanding for more than 10 days, the specific risk charges for the exposures in excess of 25% of the amended agreed capital base should be entered in D.2.1 to D.2.6. where they are multiplied by a factor dependent on the total amount by which the exposure exceeds the amended capital base.

• The period that an exposure has been outstanding is calculated in relation to the length of time that the total has been above a particular threshold even though the components of the exposure may have changed within that time.

4.21 In any event, the Commission considers that the following limits on excess exposures should not be exceeded: • The trading book exposure to a counterparty should not exceed 500% of the

bank’s TBCB, where the excess exposure has been extant for 10 days or less; and

• The aggregate trading book excess exposures which have persisted for more than 10 days should not exceed 600% of the bank’s TBCB.

4.22 Appendix B gives an example of the calculation.

4.23 Please note that this charge relates to equity and interest rate exposures; the placement of the form within the interest rate schedules reflects the desire of the Commission to have a single report and calculation for Large Exposures and the expectation that most such exposures will be interest rate, rather than equity, in nature.

Capital charge

4.24 Table E calculates the total specific interest rate risk requirement, being the total from Tables A-C plus the amount for Large Exposures (Table D).

JFSC.Basel II.M5TB Trading Book Guide – February 2008 17

General interest rate risk

4.25 The capital requirements for general market risk are designed to capture the risk of loss arising from changes in market interest rates. The capital charge is the sum of four components: • The net short or long position in the whole trading book; • A small proportion of the matched positions in each time-band (the “vertical

disallowance”); • A larger proportion of the matched positions across different time-bands (the

“horizontal disallowance”); • A net charge for positions in options, where appropriate (see Appendix A).

4.26 For the accounting currency, the methodology is replicated within the reporting form 5.2.2A and the correct completion of this form will allow the form to calculate the charge.

4.27 For other currencies, where the total gross positions held exceed 10% of the total trading book gross positions, separate maturity ladders should be used for each currency and capital charges should be calculated for each currency separately and then summed with no offsetting between positions of opposite sign in different currencies. These should mirror the calculation performed for the accounting currency, with the outputs recorded in rows A.2 to A.12 of Table A within the sheet “Interest Rate Risk: General Charge”.

4.28 For those currencies in which gross positions are insignificant (less than 10% of total gross positions), separate maturity ladders for each currency are not required. Rather, the bank may construct a single maturity ladder and slot, within each appropriate time-band, the aggregate of the long and the short positions for these currencies. The outputs should be recorded in row A.13 of Table A within the sheet “Interest Rate Risk: General Charge”.

4.29 In completing the maturity ladder, long or short positions in debt securities and other sources of interest rate exposures, including derivative instruments, are slotted into a maturity ladder. Fixed-rate instruments should be allocated according to the residual term to maturity and floating-rate instruments according to the residual term to the next repricing date. Opposite positions of the same amount in the same issues (but not different issues by the same issuer), whether actual or notional, can be omitted from the interest rate maturity framework, as well as closely matched swaps, forwards, futures and FRAs which meet the conditions set out in Appendix C.

4.30 The first step in the calculation is to weight the positions in each time-band by a factor designed to reflect the price sensitivity of those positions to assumed changes in interest rates. The weights for each time-band are set out in the Table 5.2.2A (and this calculation is done by the worksheet for this currency, the accounting currency).

4.31 The next step in the calculation is to offset the weighted longs and shorts in each time-band, resulting in a single short or long position for each band. Since, however, each band would include different instruments and different maturities, a 10% capital charge to reflect basis risk and gap risk will be levied on the smaller of the offsetting positions, be it long or short. Thus, if the sum of the weighted longs in a time-band is £100 million and the sum of the weighted shorts £90 million, the so-called “vertical disallowance” for that time band

JFSC.Basel II.M5TB Trading Book Guide – February 2008 18

would be 10% of £90 million (i.e. £9.0 million). This is computed by the worksheet for the accounting currency and displayed in Table 5.2.2A. For other currencies the total “vertical disallowance” should be entered in the column for “Capital requirements – Vertical” in Table A within the sheet “Interest Rate Risk: General Charge”.

4.32 The result of the above calculations is to produce two sets of weighted positions, the net long or short positions in each time-band (£10 million long in the example above) and the vertical disallowances. In addition, however, banks will be allowed to conduct two rounds of “horizontal offsetting”, first between the net positions in each of three zones (zero to one year, one year to four years and four years and over), and subsequently between the net positions in the three different zones. The offsetting will be subject to a scale of disallowances expressed as a fraction of the matched positions, as set out in the table below. The weighted long and short positions in each of three zones may be offset, subject to the matched portion attracting a disallowance factor that is part of the capital charge. The residual net position in each zone may be carried over and offset against opposite positions in other zones, subject to a second set of disallowance factors.

4.33 All of the above calculations are carried out by the worksheet for the accounting currency and displayed in Table 5.2.2A. For other currencies the net weighted positions for Zones 1, 2 & 3 and the total “horizontal disallowance” should be entered in the relevant columns (i.e. those for the net weighted position and the “Capital requirements – Horizontal”) in Table A within the sheet “Interest Rate Risk: General Charge”.

Zone Time band Within the Zone

Between Adjacent Zones

Between Zones 1 and 3.

Zone 1

0 – 1 month

40%

40%

40%

100%

1 – 3 months 3 – 6 months 6 – 12 months

Zone 2

1 – 2 years

30%

2 – 3 years 3 – 4 years 4 – 5 years

Zone 3

5 – 7 years

30%

7 – 10 years 10 – 15 years 15 – 20 years Over 20 years

4.34 Note that for all time bands the upper limit is inclusive and the lower limit exclusive.

4.35 The total capital charge is then calculated as the sum of the overall net position, the vertical disallowance and the horizontal disallowance.

JFSC.Basel II.M5TB Trading Book Guide – February 2008 19

4.36 In summary, the data that the bank must calculate and input in Table A within the sheet “Interest Rate Risk: General Charge” is:

ITEM COMPLETION GUIDANCE Currency Enter the accounting currency and specify any

significant currencies not denoted in the sheet. Net weighted position

Zone 1 Enter the net weighted position for Zone 1. Zone 2 Enter the net weighted position for Zone 2. Zone 3 Enter the net weighted position for Zone 3.

Capital requirements

Overall Position Enter the net weighted overall position. Vertical Enter the amount of vertical disallowances.

Horizontal Enter the amount of horizontal disallowances.

Total Charge Calculated by the sheet, being the sum of the previous three items.

Capital charge

4.37 Table B calculates the total general interest rate risk requirement, being the total from Table A plus the amount calculated by the bank and input in B.2 as representing the additional capital charge for options, as calculated in accordance with Appendix A.

JFSC.Basel II.M5TB Trading Book Guide – February 2008 20

SECTION 5 EQUITY RISK

Introduction

5.1 This section sets out a minimum capital standard to cover the risk of holding or taking positions in equities in the trading book. It applies to long and short positions in all instruments that exhibit market behaviour similar to equities, but not to non-convertible preference shares (which are covered by the interest rate risk requirements described in Section 4). Long and short positions in the same issue may be reported on a net basis. The instruments covered include common stocks, whether voting or non-voting, convertible securities that behave like equities, and commitments to buy or sell equity securities. The treatment of derivative products, stock indices and index arbitrage is described in paragraphs 5.4 to 5.12 below.

Specific and general equity risk

5.2 As with debt securities, the minimum capital standard for equities is expressed in terms of two separately calculated charges for the specific risk of holding a long or short position in an individual equity and for the general risk of holding a long or short position in the market as a whole. Specific risk is defined as the bank’s gross equity positions (i.e. the sum of all long equity positions and of all short equity positions) and general market risk as the difference between the sum of the longs and the sum of the shorts (i.e. the overall net position in an equity market). The long or short position in the market must be calculated on a market-by-market basis, i.e. a separate calculation has to be carried out for each national market in which the bank holds equities.

5.3 The capital charge for specific risk will be 8%, unless the portfolio is both liquid and well-diversified, in which case the charge will be 4%. Given the different characteristics of national markets in terms of marketability and concentration, the rules of the local regulator should be used if the local regulator is deemed to be equivalent, as agreed with the Commission. If no such regulator exists, or no such rules have been published, then the bank may apply the 4% charge to a share that is a constituent of a qualifying index (see Appendix D), providing that it is held as part of a portfolio where: • No individual position exceeds 10% of the portfolio’s gross value; and • The sum of positions (ignoring the sign) which individually represent

between 5% and 10% of the portfolio’s gross value does not exceed 50% of the latter.

Equity derivatives

5.4 Except for options, which are dealt with in Appendix A, equity derivatives and off-balance-sheet positions which are affected by changes in equity prices should be included in the standard measurement system. This includes futures and swaps on both individual equities and on stock indices. The derivatives are

JFSC.Basel II.M5TB Trading Book Guide – February 2008 21

to be converted into positions in the relevant underlying equity or stock index. The treatment of equity derivatives is summarised in paragraph 5.12 below.

5.5 In order to calculate the standard formula for specific and general market risk, positions in derivatives should be converted into notional equity positions: • Futures and forward contracts relating to individual equities should, in

principle, be reported at current market prices; • Futures relating to stock indices should be reported as the marked-to-market

value of the notional underlying equity portfolio; • Equity swaps are to be treated as two notional positions; • Equity options and stock index options should be either “carved out”

together with the associated underlying hedged position or be incorporated in the measure of general market risk described in this section according to the delta-plus method (see Appendix A).

5.6 Matched positions in each identical equity or stock index in each market may be fully offset, resulting in a single net short or long position to which the specific and general market risk charges will apply. For example, a future in a given equity may be offset against an opposite cash position in the same equity.

5.7 Besides general market risk, a further capital charge of 2% will apply to the net long or short position in an index contract comprising a diversified portfolio of equities. Contracts relating to qualifying indices (see appendix D) count for this purpose, otherwise the bank must assure itself that the criteria in 5.3 would be satisfied. This specific risk capital charge is intended to cover factors such as execution risk.

5.8 In the case of the futures-related arbitrage strategies described below, the additional 2% specific risk capital charge described above may be applied to only one index with the opposite position exempt from a capital charge. The strategies are: • When the bank takes an opposite position in exactly the same index at

different dates or in different market centres; and • When the bank has an opposite position in contracts at the same date in

different but similar indices, subject to supervisory oversight that the two indices contain sufficient common components to justify offsetting.

5.9 Where a bank engages in a deliberate arbitrage strategy, in which a futures contract on a broadly-based index matches a basket of stocks, it will be allowed to carve out both positions from the standardised methodology on condition that: • The trade has been deliberately entered into and separately controlled; and • The composition of the basket of stocks represents at least 90% of the index

when broken down into its notional components.

5.10 In such a case, the capital requirement will be 4% (i.e. 2% of the gross value of the positions on each side) to reflect divergence and execution risks. This applies even if all of the stocks comprising the index are held in identical proportions. Any excess value of the stocks comprising the basket over the value of the futures contract or excess value of the futures contract over the value of the basket is to be treated as an open long or short position.

5.11 If a bank takes a position in depository receipts against an opposite position in the underlying equity or identical equities in different markets, it may offset the

JFSC.Basel II.M5TB Trading Book Guide – February 2008 22

position (i.e. bear no capital charge) but only on condition that any costs on conversion are fully taken into account.

5.12 The table below summarises the regulatory treatment of equity derivatives for market risk purposes:

Instrument Specific Risk General Risk Exchange-traded or OTC-Future - Individual equity

Yes, as per the underlying equity.

Yes, as per the underlying equity.

- Index 2%. Yes, as per the underlying index. Options - Individual equity

Yes, as per the underlying equity.

Either: (a) Carve out together with associated

hedging positions - simplified approach; or

(b) Apply the general market risk charge according to the delta-plus method (gamma and vega should receive separate capital charges).

See Appendix A for further details.

- Index 2%.

JFSC.Basel II.M5TB Trading Book Guide – February 2008 23

SECTION 6 COMMODITY RISK

Introduction

6.1 All commodity positions should be reported using this part of the form except gold, which is treated as a currency and reported within “FX & Gold” – see Section 3. The bank is allowed to offset current and future exposures to arrive at a net position, and the capital charge is made up of elements for the net and gross positions.

Reporting and calculation of capital charge 6.2 The groupings are:

• A.1: Precious metals (excluding gold); • A.2: Base metals; • A.3: Energy contracts; and • A.4: Other contracts.

6.3 All input figures should correspond to the gross amount.

6.4 Table A: Commodity Positions ITEM Description COMPLETION NOTES

A.1 to A.4

Gross Long Report all long positions for each commodity group.

Gross Short Report all short positions for each commodity group.

Net Open Position A calculated field, being equal to “Gross Long” less “Gross Short”.

Simplified Approach A calculated field, being equal to 15% of the “Net Open Position” plus 3% of “Gross Long” plus 3% of “Gross Short”.

A (Total) Gross Long A calculated field, being a sum of A.1 to A.4, as applicable.

Gross Short A calculated field, being a sum of A.1 to A.4, as applicable.

Net Open Position A calculated field, being a sum of the absolute values of A.1 to A.4.

Simplified Approach A calculated field, being equal to 15% of the “Net Open Position” plus 3% of “Gross Long” plus 3% of “Gross Short”.

Capital charge

6.5 Table B calculates the total commodity risk requirement, being the total from Table A plus the amount calculated by the bank and input in B.1 as representing

JFSC.Basel II.M5TB Trading Book Guide – February 2008 24

the additional capital charge for options, as calculated in accordance with Appendix A.

Top five commodities

6.6 Table C is completed in the same manner as Table A, except that, instead of reporting all positions, split by group, the bank need only report the five commodities that produce the largest “Simplified Approach” charge.

6.7 The Commission does not require a breakdown if the charge is less than 1% of the bank’s Agreed Capital Base.

JFSC.Basel II.M5TB Trading Book Guide – February 2008 25

SECTION 7 SETTLEMENT RISK

Introduction

7.1 Settlement risk arises through failed DvP trades and all non DvP trades (free deliveries).

Failed DvP trades

7.2 Whether or not a transaction involving the delivery of an instrument against the receipt of cash attracts a counterparty risk charge during its life, a capital charge should apply in cases of unsettled transactions as defined below: • An unsettled transaction is one where delivery of the instrument is due to

take place against the receipt of cash, but which remains unsettled five business days after the due settlement date.

• As an example of where this is applicable, if Bank A sells shares in Company C to Bank B and Bank A fails to deliver on time, Bank B should hold capital for counterparty risk on Bank A in addition to capital for specific risk on Company C. This is because if the price moves in Bank B’s favour, its profit can only be realised once Bank A has delivered the instruments to Bank B.

7.3 In principle, banks’ systems should be set up in such a manner that, where a deal attracts a counterparty risk charge, this charge continues to apply when settlement is due but has not been completed. Banks are expected to adopt this for all such transactions.

7.4 No capital charges in respect of settlement risk on spot and forward foreign exchange transactions are considered necessary.

Treatment

7.5 Unsettled transactions should attract a capital cost based upon the difference between the amount due and the current market value of the instrument, if this has a potential loss. The capital requirement should be this potential loss multiplied by the factor in the table below.

7.6 This applies only to trades where a loss may arise for the bank if the trade fails to settle. Failed trades must be reported once the date is more than four days after the agreed settlement date.

7.7 Note that the capital requirement for such transactions is not multiplied by the counterparty risk weight.

Number of working days after due settlement date

Item Factor

5 – 15 A.1 8%

16 – 30 A.2 50%

31 – 45 A.3 75%

46 or more A.4 100%

JFSC.Basel II.M5TB Trading Book Guide – February 2008 26

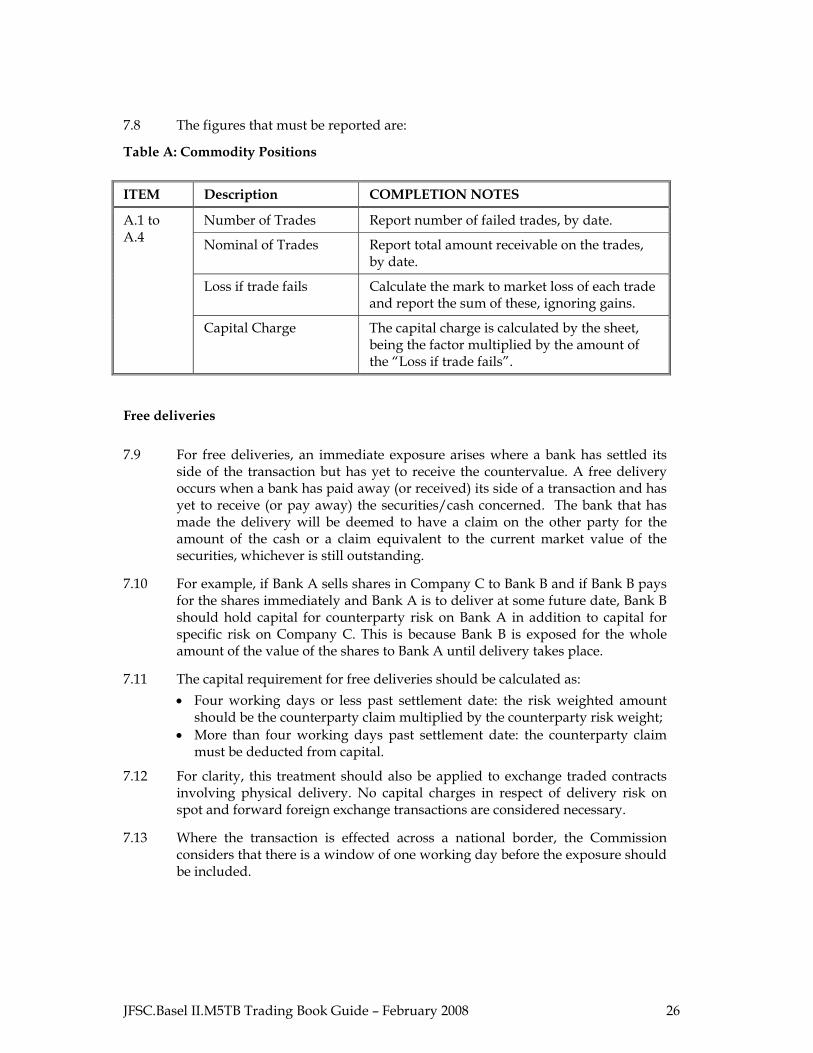

7.8 The figures that must be reported are:

Table A: Commodity Positions ITEM Description COMPLETION NOTES

A.1 to A.4

Number of Trades Report number of failed trades, by date.

Nominal of Trades Report total amount receivable on the trades, by date.

Loss if trade fails Calculate the mark to market loss of each trade and report the sum of these, ignoring gains.

Capital Charge The capital charge is calculated by the sheet, being the factor multiplied by the amount of the “Loss if trade fails”.

Free deliveries

7.9 For free deliveries, an immediate exposure arises where a bank has settled its side of the transaction but has yet to receive the countervalue. A free delivery occurs when a bank has paid away (or received) its side of a transaction and has yet to receive (or pay away) the securities/cash concerned. The bank that has made the delivery will be deemed to have a claim on the other party for the amount of the cash or a claim equivalent to the current market value of the securities, whichever is still outstanding.

7.10 For example, if Bank A sells shares in Company C to Bank B and if Bank B pays for the shares immediately and Bank A is to deliver at some future date, Bank B should hold capital for counterparty risk on Bank A in addition to capital for specific risk on Company C. This is because Bank B is exposed for the whole amount of the value of the shares to Bank A until delivery takes place.

7.11 The capital requirement for free deliveries should be calculated as: • Four working days or less past settlement date: the risk weighted amount

should be the counterparty claim multiplied by the counterparty risk weight; • More than four working days past settlement date: the counterparty claim

must be deducted from capital.

7.12 For clarity, this treatment should also be applied to exchange traded contracts involving physical delivery. No capital charges in respect of delivery risk on spot and forward foreign exchange transactions are considered necessary.

7.13 Where the transaction is effected across a national border, the Commission considers that there is a window of one working day before the exposure should be included.

JFSC.Basel II.M5TB Trading Book Guide – February 2008 27

ITEM Description COMPLETION NOTES

B.1: 4 days or less

Number of Trades Number of trades four days or less past settlement, by counterparty weight.

Mark-to-market receivable

Report receivable mark-to-market, by counterparty weight.

Counterparty Weight Weights are in accordance with the credit risk approach used by the entity.

Risk Weighted Assets A calculated field, being equal to the “mark-to-market receivable” multiplied by the “Counterparty weight”.

Capital Charge A calculated field, being 8% of the Risk Weighted Assets.

B.2 More than 4 days

Number of Trades Number of trades more than four days past settlement.

Mark-to-market receivable

Report mark-to-market of the receivable.

Capital Charge Automatically calculated, equal to the “Mark-to-market receivable”.

Summary of settlement risk

7.14 Table A calculates the total equivalent Risk Weighted Asset figures from Table A for DvP failed trades and Table B for all non DvP trades (free deliveries).

JFSC.Basel II.M5TB Trading Book Guide – February 2008 28

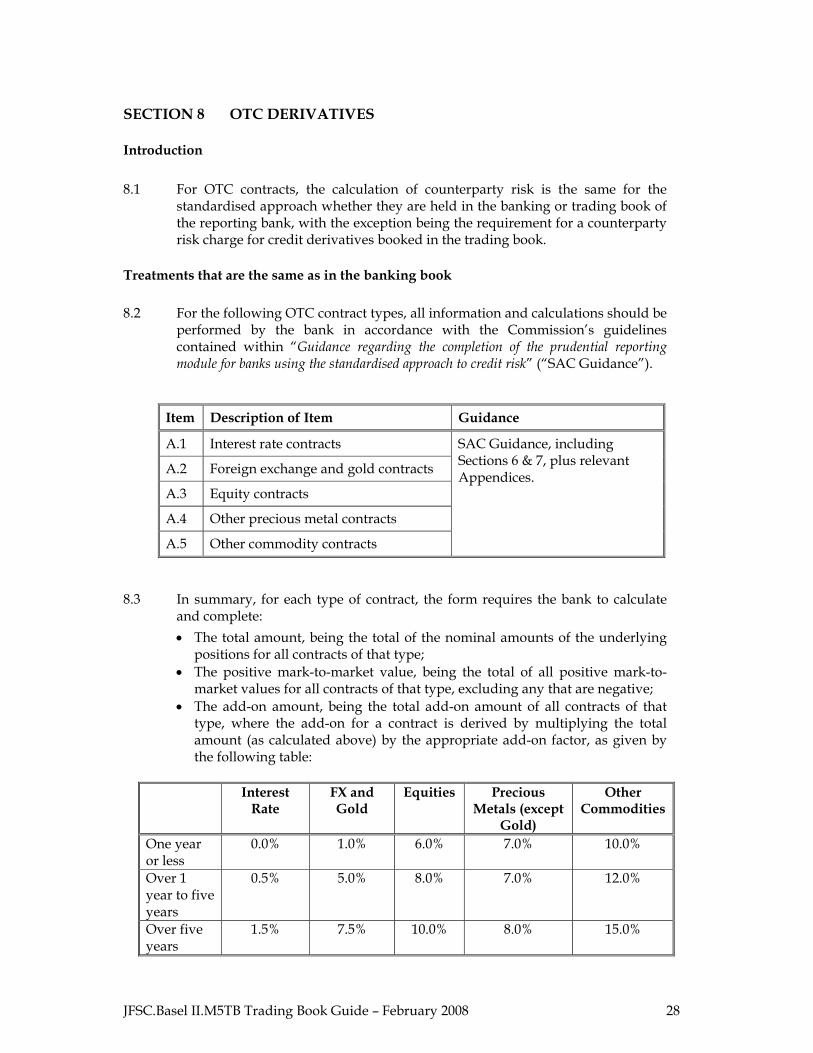

SECTION 8 OTC DERIVATIVES

Introduction

8.1 For OTC contracts, the calculation of counterparty risk is the same for the standardised approach whether they are held in the banking or trading book of the reporting bank, with the exception being the requirement for a counterparty risk charge for credit derivatives booked in the trading book.

Treatments that are the same as in the banking book

8.2 For the following OTC contract types, all information and calculations should be performed by the bank in accordance with the Commission’s guidelines contained within “Guidance regarding the completion of the prudential reporting module for banks using the standardised approach to credit risk” (“SAC Guidance”).

Item Description of Item Guidance

A.1 Interest rate contracts SAC Guidance, including Sections 6 & 7, plus relevant Appendices. A.2 Foreign exchange and gold contracts

A.3 Equity contracts

A.4 Other precious metal contracts

A.5 Other commodity contracts

8.3 In summary, for each type of contract, the form requires the bank to calculate and complete: • The total amount, being the total of the nominal amounts of the underlying

positions for all contracts of that type; • The positive mark-to-market value, being the total of all positive mark-to-

market values for all contracts of that type, excluding any that are negative; • The add-on amount, being the total add-on amount of all contracts of that

type, where the add-on for a contract is derived by multiplying the total amount (as calculated above) by the appropriate add-on factor, as given by the following table:

Interest

Rate FX and Gold

Equities Precious Metals (except

Gold)

Other Commodities

One year or less

0.0% 1.0% 6.0% 7.0% 10.0%

Over 1 year to five years

0.5% 5.0% 8.0% 7.0% 12.0%

Over five years

1.5% 7.5% 10.0% 8.0% 15.0%

JFSC.Basel II.M5TB Trading Book Guide – February 2008 29

• The form calculates the credit equivalent amount, before credit risk mitigation; and

• Finally, the bank should input the amount after credit mitigation in accordance with the guidance in Section 7 of the Commission’s SAC Guidance.

Treatment of credit derivatives booked in the trading book

8.4 Basel II requires that counterparty risk is also calculated for credit derivatives in the trading book. The calculation and disclosure is the same as for other OTC contracts, except that the add-on is calculated as set out in the following paragraphs.

8.5 The add-ons to be applied for the calculation of potential exposure for single name transactions are as follows:

Protection buyer

Protection Seller

Total Return Swap

“Qualifying” reference obligation 5% 5%

“Non-Qualifying” reference obligation

10% 10%

Credit Default Swap

“Qualifying” reference obligation 5% 5%*

“Non-Qualifying” reference obligation

10% 10%*

* The protection seller of a credit default swap is only subject to the add-on factor where the swap is subject to closeout upon the insolvency of the protection buyer while the reference obligation is still solvent. The add-on should then be capped to the amount of unpaid premium.

8.6 The definition of “Qualifying” is the same as for the “Qualifying” category for the treatment of specific interest rate risk in Section 4, and includes all securities issued by public sector entities and multilateral development banks, plus other securities that: • Are rated BBB- or higher by at least two external credit assessment

institutions (“ECAIs”) that are in the list of eligible ECAIs published by the Commission. As of February 2008 these comprised: (c) Moody’s; (d) Standard & Poor’s; and (e) Fitch; or

• Are only rated by one eligible ECAI and this rating is BBB- or higher. 8.7 Where the credit derivative is a first-to-default transaction linked to a basket of

items, the add-on of “Non-Qualifying” reference obligations will be used if there is at least one “Non-Qualifying” reference obligation in the basket, otherwise, the add-on of “Qualifying” reference obligations should be used. For second-to-default transactions, the add-on of “Non-Qualifying” reference obligations will be used if there are at least two “Non-Qualifying” reference obligations in the basket, otherwise, the add-on to be used will be that of

JFSC.Basel II.M5TB Trading Book Guide – February 2008 30

“Qualifying” reference obligations. The same principle applies to other subsequent-to-default transactions.

8.8 Hence Table B should be completed by the bank in the same fashion as Table A: • The total amount, being the total of the nominal amounts of the underlying

positions for all contracts of that type; • The positive mark-to-market value, being the total of all positive mark-to-

market values for all contracts of that type, excluding any that are negative; • The add-on amount, being the total add-on amount of all contracts of that

type, where the add-on for a contract is derived by multiplying the nominal underlying that contract by the appropriate add-on factor;

• The form calculates the credit equivalent amount, before credit risk

mitigation; and • Finally, the bank should input the amount after credit mitigation in

accordance with the guidance in Section 7 of the Commission’s SAC Guidance.

8.9 Finally, Table C calculates the total Risk Weighted Assets, being the sum of that calculated for Table A (OTC Contracts) and Table B (Credit Derivatives) and then calculates the total capital charge, being 8% of the total Risk Weighted Assets.

JFSC.Basel II.M5TB Trading Book Guide – February 2008 31

SECTION 9 REPO, REVERSE-REPO AND OTHER COUNTERPARTY RISK

Introduction

9.1 For all other counterparty risk, the calculation of counterparty risk is the same for the standardised approach whether the instruments are held in the banking or trading book of the reporting bank.

9.2 The forms should be completed for the following categories: • Table A: Margins/Fees due; • Table B: Repos; • Table C: Reverse-repos; and • Table D: Other Counterparty risk.

9.3 For each, the treatment follows that set out in the Commission’s guidelines contained within “Guidance regarding the completion of the prudential reporting module for banks using the standardised approach to credit risk” (“SAC Guidance”).

9.4 In summary, the bank should report the amount before and after credit mitigation, classified by risk weight of the counterparty, in accordance with the SAC Guidance, with the amount after credit risk mitigation being determined by the simple or comprehensive approach to credit risk mitigation.

9.5 In particular, the reporting bank should note the guidelines contained in the SAC Guidance, within Appendix D: Criteria for Preferential Treatment of Repo-Style Transactions.

9.6 Finally, Table E calculates total Risk Weighted Assets, being the sum of that calculated for Tables A to D, and then calculates the total capital charge, being 8% of the total Risk Weighted Assets.

JFSC.Basel II.M5TB Trading Book Guide – February 2008 32

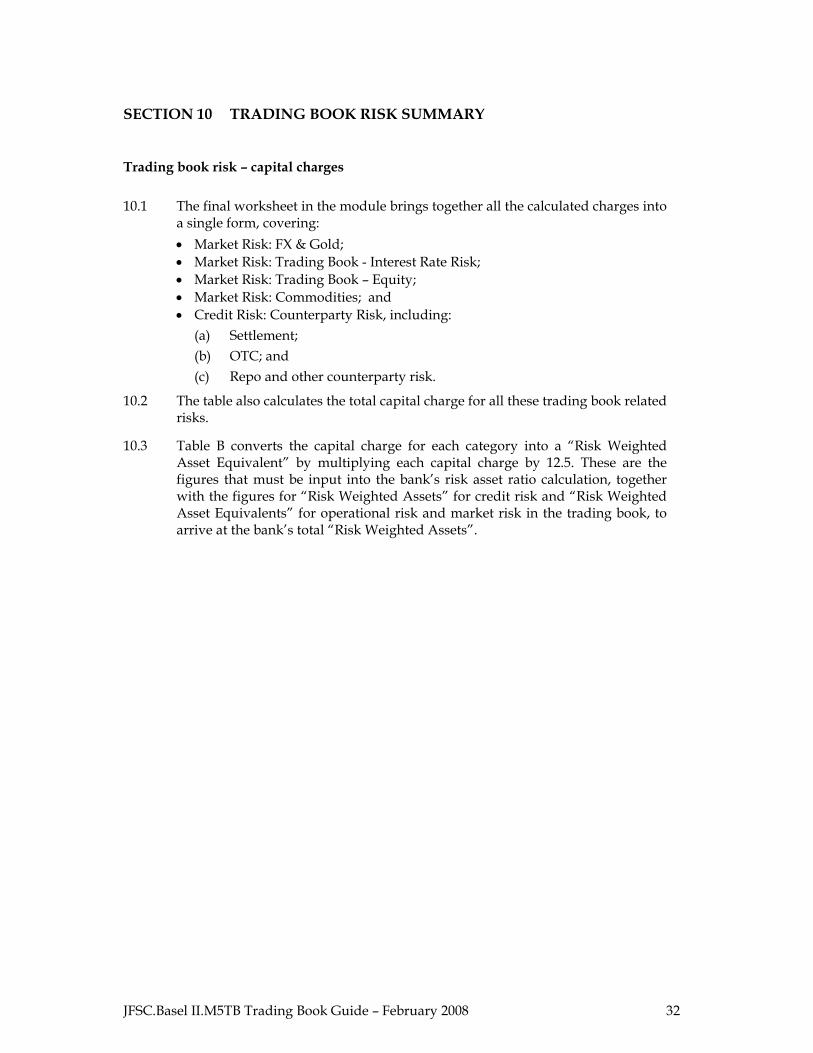

SECTION 10 TRADING BOOK RISK SUMMARY

Trading book risk – capital charges

10.1 The final worksheet in the module brings together all the calculated charges into a single form, covering: • Market Risk: FX & Gold; • Market Risk: Trading Book - Interest Rate Risk; • Market Risk: Trading Book – Equity; • Market Risk: Commodities; and • Credit Risk: Counterparty Risk, including:

(a) Settlement; (b) OTC; and (c) Repo and other counterparty risk.

10.2 The table also calculates the total capital charge for all these trading book related risks.

10.3 Table B converts the capital charge for each category into a “Risk Weighted Asset Equivalent” by multiplying each capital charge by 12.5. These are the figures that must be input into the bank’s risk asset ratio calculation, together with the figures for “Risk Weighted Assets” for credit risk and “Risk Weighted Asset Equivalents” for operational risk and market risk in the trading book, to arrive at the bank’s total “Risk Weighted Assets”.

JFSC.Basel II.M5TB Trading Book Guide – February 2008 33

APPENDIX A: TREATMENT OF OPTIONS

A.1 Overview

A.1.1 In recognition of the wide diversity of banks’ activities in options and the difficulties of measuring price risk for options, alternative approaches will be permissible, as set out below: • Those banks which solely use purchased options will be free to use the

simplified approach described in A.2; • Those banks which also write options will be expected to use the

“delta-plus” approach as set out A.3.

A.1.2 A bank that conducts significant trading activity, especially regarding options, will be expected to consider using an advanced approach. This will require the Commission’s approval and will impact all aspects of calculating and reporting trading book risk, not just the treatment of options.

A.1.3 In the simplified approach, positions for options and the associated underlying position (cash or forward) are not subject to the standardised methodology but rather are “carved-out” and subject to separately calculated capital charges that incorporate both general market risk and specific risk. The risk numbers thus generated are then added to the capital charges for the relevant category, i.e. interest rate related instruments, equities, foreign exchange and commodities as described in Sections 3 to 6.

A.1.4 The “delta-plus” method uses the sensitivity parameters or “Greek letters” associated with options to measure their market risk and capital requirements. Under this method, the delta-equivalent position of each option becomes part of the standardised methodology set out in Sections 3 to 6 with the delta-equivalent amount subject to the applicable general market risk charges. Separate capital charges are then applied to the gamma and vega risks of the option positions. For the “delta-plus” method the specific risk capital charges are determined separately by multiplying the delta-equivalent of each option by the specific risk weights set out in Sections 3 to 6.

A.2 Simplified approach

A.2.1 Banks which handle a limited range of purchased options only will be free to use the simplified approach set out in the table below for particular trades. As an example of how the calculation would work, if a holder of 100 shares currently valued at £10 each holds an equivalent put option with a strike price of £11, the capital charge would be: £1,000 x 16%(i.e. 8% specific plus 8% general market risk) = £160, less the amount the option is in the money (£11 - £10) x 100 = £100, i.e. the capital charge would be £60. A similar methodology applies for options where the underlying position is a foreign currency, an interest rate related instrument or a commodity.

JFSC.Basel II.M5TB Trading Book Guide – February 2008 34

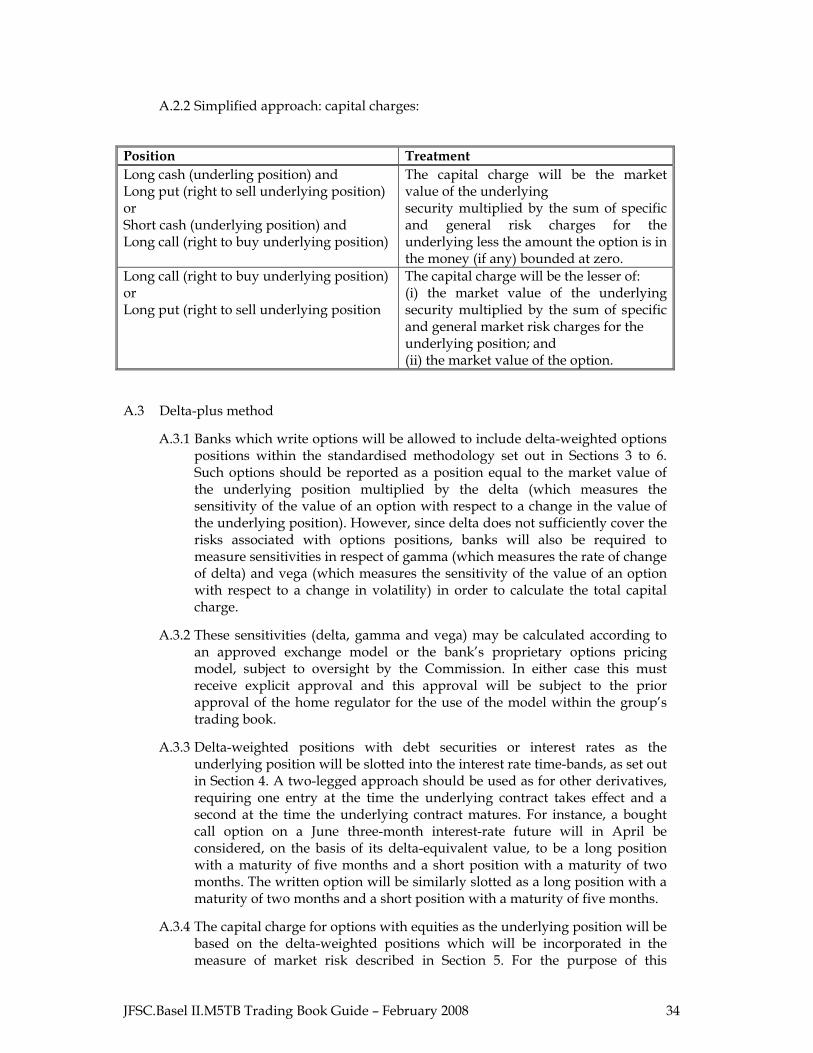

A.2.2 Simplified approach: capital charges:

Position Treatment Long cash (underling position) and Long put (right to sell underlying position) or Short cash (underlying position) and Long call (right to buy underlying position)

The capital charge will be the market value of the underlying security multiplied by the sum of specific and general risk charges for the underlying less the amount the option is in the money (if any) bounded at zero.

Long call (right to buy underlying position) or Long put (right to sell underlying position

The capital charge will be the lesser of: (i) the market value of the underlying security multiplied by the sum of specific and general market risk charges for the underlying position; and (ii) the market value of the option.

A.3 Delta-plus method

A.3.1 Banks which write options will be allowed to include delta-weighted options positions within the standardised methodology set out in Sections 3 to 6. Such options should be reported as a position equal to the market value of the underlying position multiplied by the delta (which measures the sensitivity of the value of an option with respect to a change in the value of the underlying position). However, since delta does not sufficiently cover the risks associated with options positions, banks will also be required to measure sensitivities in respect of gamma (which measures the rate of change of delta) and vega (which measures the sensitivity of the value of an option with respect to a change in volatility) in order to calculate the total capital charge.

A.3.2 These sensitivities (delta, gamma and vega) may be calculated according to an approved exchange model or the bank’s proprietary options pricing model, subject to oversight by the Commission. In either case this must receive explicit approval and this approval will be subject to the prior approval of the home regulator for the use of the model within the group’s trading book.

A.3.3 Delta-weighted positions with debt securities or interest rates as the underlying position will be slotted into the interest rate time-bands, as set out in Section 4. A two-legged approach should be used as for other derivatives, requiring one entry at the time the underlying contract takes effect and a second at the time the underlying contract matures. For instance, a bought call option on a June three-month interest-rate future will in April be considered, on the basis of its delta-equivalent value, to be a long position with a maturity of five months and a short position with a maturity of two months. The written option will be similarly slotted as a long position with a maturity of two months and a short position with a maturity of five months.

A.3.4 The capital charge for options with equities as the underlying position will be based on the delta-weighted positions which will be incorporated in the measure of market risk described in Section 5. For the purpose of this

JFSC.Basel II.M5TB Trading Book Guide – February 2008 35

calculation, each national market is to be treated as a separate underlying position.

A.3.5 The capital charge for options on foreign exchange and gold positions will be based on the method set out in Section 3. For delta risk, the net delta-based equivalent of the foreign currency and gold options will be incorporated into the measurement of the exposure for the respective currency (or gold) position.

A.3.6 The capital charge for options on commodities will be based on the approach set out in Section 6. The delta-weighted positions will be incorporated into the categories described in that section.

A.3.7 In addition to the above capital charges arising from delta risk, there will be further capital charges for gamma and for vega risk. Banks using the delta-plus method will be required to calculate the gamma and vega for each option position (including hedge positions) separately. The capital charges should be calculated in the following way: • For each individual option a “gamma impact” should be calculated

according to a Taylor series expansion as:

Gamma impact = ½ x Gamma x VU²

where VU = Variation of the underlying position of the option. • VU will be calculated as follows:

(a) For interest rate options if the underlying position is a bond, the market value of the underlying position should be multiplied by the applicable weight for its maturity. An equivalent calculation should be carried out where the underlying position is an interest rate;

(b) For options on equities and equity indices: the market value of the underlying position should be multiplied by 8%;

(c) For foreign exchange and gold options: the market value of the underlying position should be multiplied by 8%; and

(d) For options on commodities: the market value of the underlying position should be multiplied by 15%.

• For the purpose of this calculation, the following underlying positions should be treated as the same underlying position: (a) For interest rates, each time-band as set out in Section 4; (b) For equities and stock indices, each national market; (c) For foreign currencies and gold, each currency pair and gold; and (d) For commodities, each individual commodity as defined in

Section 6. • Each option on the same underlying position will have a gamma

impact that is either positive or negative. These individual gamma impacts will be summed; resulting in a net gamma impact for each underlying position that is either positive or negative. Only those net gamma impacts that are negative will be included in the capital calculation. The total gamma capital charge will be the sum of the absolute value of the net negative gamma impacts, as calculated above.

JFSC.Basel II.M5TB Trading Book Guide – February 2008 36

• For volatility risk, banks will be required to calculate the capital charges by multiplying the sum of the vegas for all options on the same underlying position, as defined above, by a proportional shift in volatility of ± 25%.

• The total capital charge for vega risk will be the sum of the absolute value of the individual capital charges that have been calculated for vega risk.

JFSC.Basel II.M5TB Trading Book Guide – February 2008 37

APPENDIX B: INCREMENTAL CAPITAL FOR LARGE EXPOSURES: EXAMPLE

B.1 The following is only an example and as such does not purport to cover every eventuality.

B.2 Suppose that a bank’s trading book capital base (“TBCB”) comprises: • Capital base (tier 1 and tier 2) = £1,000,000 • Eligible tier 3 capital = £100,000 • And hence the TBCB = £1,100,000

B.3 The components of the Large Exposure comprise: £ Amount Counterparty exposure: 200,000 Mark to market value of trading book securities:

Specific risk weight % Short: Qualifying bond (20,000) 1.00 Long: Qualifying Commercial paper

100,000 0.25

Long: Equity 150,000 4.00 Long: Qualifying Convertible bond

330,000 1.60

Total net long securities position

560,000

Total net large exposures position

760,000

B.4 The short position in the qualifying bond is offset against the highest specific risk weight items - in this case equities: • Net long equity position (£150,000 - £20,000) = £130,000

B.5 The remaining items are ranked according to specific risk weight. % Specific risk Security £ Amount 0.25 Qualifying commercial

paper 100,000

1.60 Qualifying convertible bond

330,000

4.00 Equity 130,000

B.6 The “headroom” between the non securities exposure and 25% of the TBCB is calculated: • 25% of TBCB (£1,100,000)= £275,000 • Non securities exposures = £200,000 • Headroom = £75,000

JFSC.Basel II.M5TB Trading Book Guide – February 2008 38

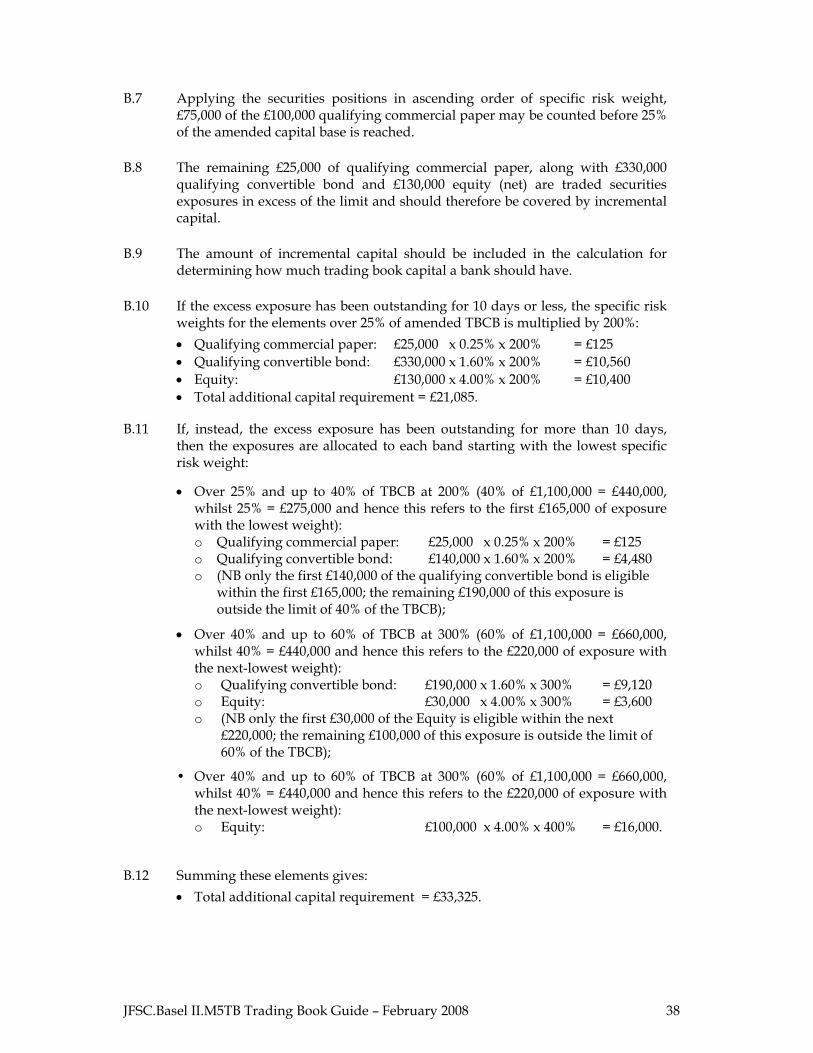

B.7 Applying the securities positions in ascending order of specific risk weight, £75,000 of the £100,000 qualifying commercial paper may be counted before 25% of the amended capital base is reached.

B.8 The remaining £25,000 of qualifying commercial paper, along with £330,000 qualifying convertible bond and £130,000 equity (net) are traded securities exposures in excess of the limit and should therefore be covered by incremental capital.

B.9 The amount of incremental capital should be included in the calculation for determining how much trading book capital a bank should have.