guns & ammunition manufacturing in the us - …sanpete.com/downloads/33299a.pdf · guns &...

TRANSCRIPT

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 1

IBISWorld Industry Report 33299aGuns & Ammunition Manufacturing in the USJune 2017 Daniel Longo

Lock and load: After recent sales surge, demand normalizes as fears of gun control subside

2 About this Industry2 Industry Definition

2 Main Activities

2 Similar Industries

3 Additional Resources

4 Industry at a Glance

5 Industry Performance5 Executive Summary

5 Key External Drivers

7 Current Performance

10 Industry Outlook

12 Industry Life Cycle

14 Products & Markets14 Supply Chain

14 Products & Services

15 Demand Determinants

16 Major Markets

17 International Trade

19 Business Locations

21 Competitive Landscape21 Market Share Concentration

21 Key Success Factors

21 Cost Structure Benchmarks

23 Basis of Competition

24 Barriers to Entry

25 Industry Globalization

26 Major Companies26 General Dynamics Corp.

27 Vista Outdoor Operations LLC

28 Remington Outdoor Company

28 American Outdoor Brands Corporation

30 Olin Corp.

31 Orbital ATK Inc.

32 Operating Conditions32 Capital Intensity

33 Technology & Systems

34 Revenue Volatility

34 Regulation & Policy

36 Industry Assistance

38 Key Statistics38 Industry Data

38 Annual Change

38 Key Ratios

39 Industry Financial Ratios

40 Jargon & Glossary

www.ibisworld.com | 1-800-330-3772 | [email protected]

This report was provided toUniversity of Nevada, Reno (2126926196)by IBISWorld on 01 September 2017 in accordance with their license agreement with IBISWorld

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 2

This industry manufactures small arms (including shotguns, rifles, revolvers, pistols, machine guns and grenade launchers), and ammunition, ordnance and accessories.

The primary activities of this industry are

Machine guns manufacturing

Shotguns and rifles manufacturing

Handguns manufacturing

Gun magazines manufacturing

Small arms ammunition manufacturing

Ammunition (except small arms) manufacturing

Grenades manufacturing

Mines manufacturing

Artillery and tank ammunition manufacturing

Howitzers and man-portable and vehicle installed rockets and rocket launchers manufacturing

32592 Explosives Manufacturing in the USThis industry manufacturers blasting caps, detonating caps and safety fuses.

33641a Aircraft, Engine & Parts Manufacturing in the USThis industry manufactures military aircraft, including bombers, fighter jets and attack helicopters.

33641b Space Vehicle & Missile Manufacturing in the USThis industry manufactures guided missiles, which are like ordnance products, such as mortars, rocket launchers and howitzers.

33699b Tank & Armored Vehicle Manufacturing in the USThis industry manufactures complete military armored vehicles, combat tanks and specialized components for combat tanks, including self-propelled weapons.

Industry Definition

Main Activities

Similar Industries

About this Industry

The major products and services in this industry are

Ordnance & accessories

Small arms & machine guns

Small arms ammunition

Other ammunition

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 3

About this Industry

Additional Resources For additional information on this industry

www.atf.gov Bureau of Alcohol, Tobacco, Firearms and Explosives

www.nra.org National Rifle Association

www.nssf.org National Shooting Sports Foundation

www.defense.gov US Department of Defense

IBISWorld writes over 1000 US industry reports, which are updated up to four times a year. To see all reports, go to www.ibisworld.com

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 4

% c

hang

e

10

-10

-5

0

5

2210 12 14 16 18 20Year

Federal funding for defense

SOURCE: WWW.IBISWORLD.COM

% c

hang

e

15

-15

-10

-5

0

5

10

2309 11 13 15 17 19 21Year

Revenue Employment

Revenue vs. employment growth

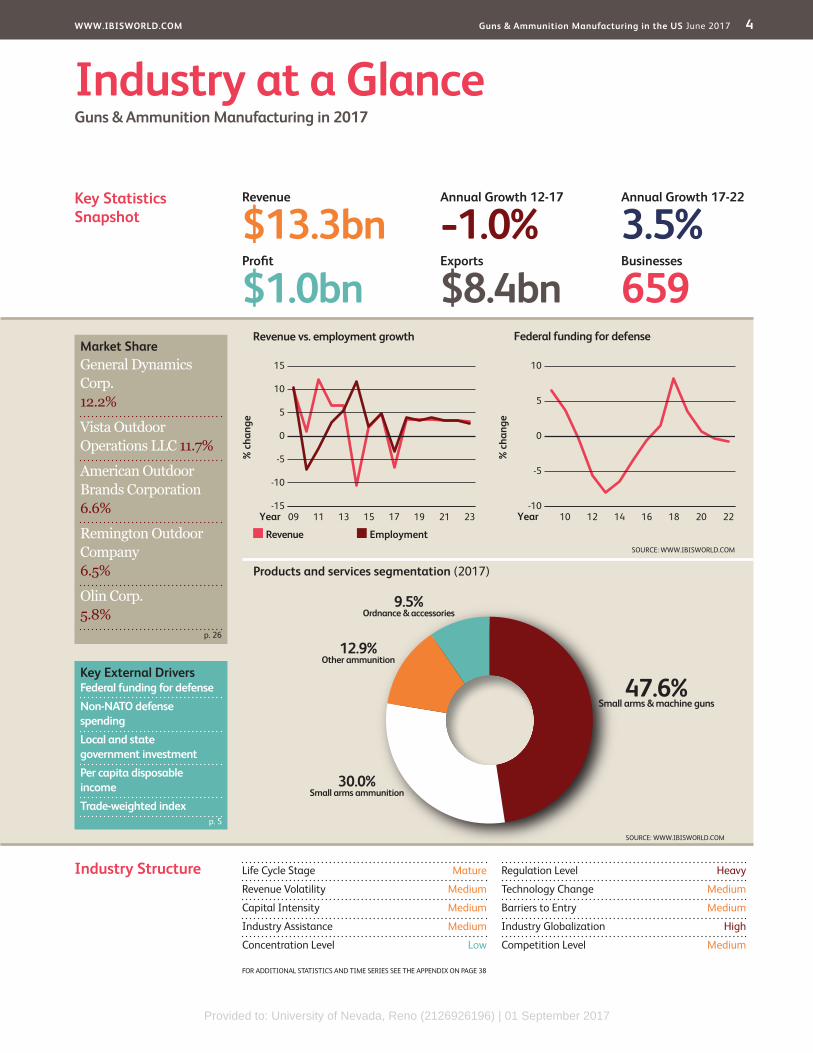

Products and services segmentation (2017)

47.6%Small arms & machine guns

30.0%Small arms ammunition

12.9%Other ammunition

9.5%Ordnance & accessories

SOURCE: WWW.IBISWORLD.COM

Key Statistics Snapshot

Industry at a GlanceGuns & Ammunition Manufacturing in 2017

Industry Structure Life Cycle Stage Mature

Revenue Volatility Medium

Capital Intensity Medium

Industry Assistance Medium

Concentration Level Low

Regulation Level Heavy

Technology Change Medium

Barriers to Entry Medium

Industry Globalization High

Competition Level Medium

Revenue

$13.3bnProfit

$1.0bnExports

$8.4bnBusinesses

659

Annual Growth 17-22

3.5%Annual Growth 12-17

-1.0%

Key External DriversFederal funding for defenseNon-NATO defense spendingLocal and state government investmentPer capita disposable incomeTrade-weighted index

Market ShareGeneral Dynamics Corp. 12.2%

Vista Outdoor Operations LLC 11.7%

American Outdoor Brands Corporation 6.6%

Remington Outdoor Company 6.5%

Olin Corp. 5.8%

p. 26

p. 5

FOR ADDITIONAL STATISTICS AND TIME SERIES SEE THE APPENDIX ON PAGE 38

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 5

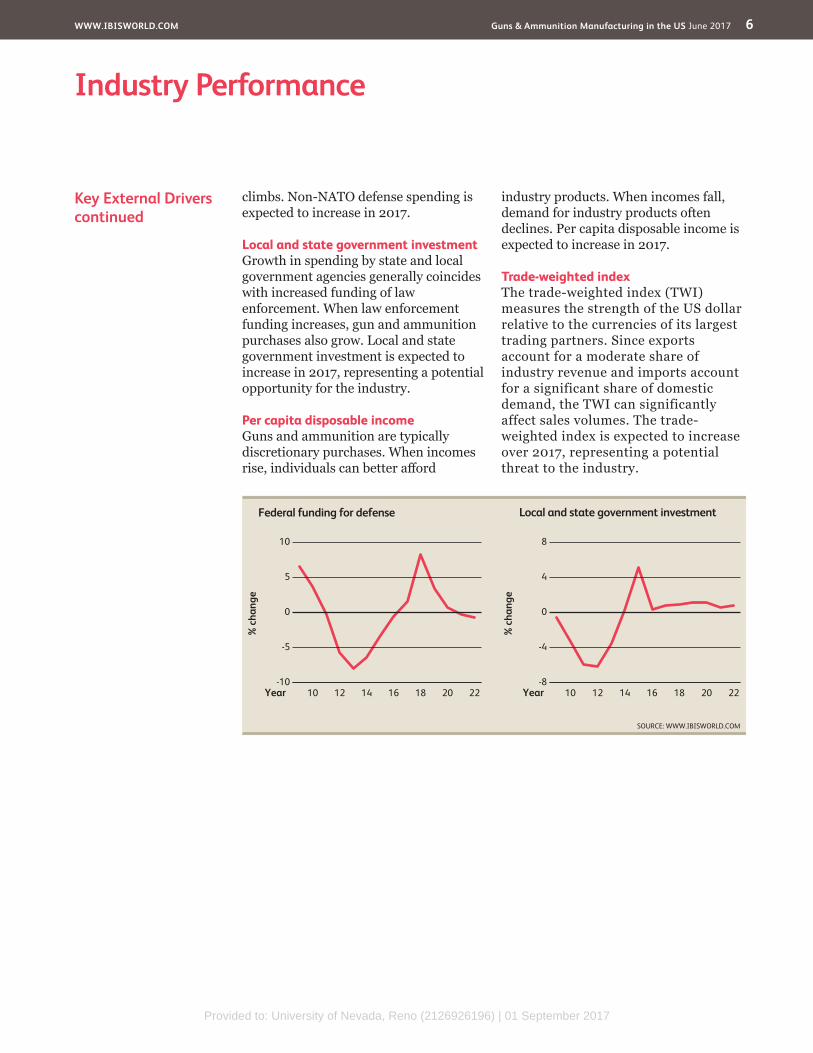

Key External Drivers Federal funding for defenseThe US government, especially the Department of Defense, is a major purchaser of industry products, particularly those of a higher caliber and complexity. As the expenditure allocated for these items increases, sales and revenue typically grow. Government funding for defense is influenced by fears of terrorism, defense expenditures of rival nations, outbreaks of conflict and other geopolitical factors. Federal

funding for defense is expected to increase in 2017.

Non-NATO defense spendingNon-NATO defense spending is the sum of global military spending, excluding the 29 members of the North Atlantic Treaty Organization. Therefore, this driver excludes spending by most Western states, focusing more on non-Western nations. When non-NATO spending increases, the market for industry exports

Executive Summary

The Guns and Ammunition Manufacturing industry has experienced inconsistent growth over the past five years. Industry operators design and manufacture small arms, bombs, ordnances, ammunition, artillery and related parts. Companies in this industry vary between small arms manufacturers to large multibillion-dollar defense contractors, with many companies serving both the civilian and military markets. During the period, often-diverging trends in these two markets drove industry performance. As a result,

over the five years to 2017, industry revenue is expected to decrease at an annualized rate of 1.0% to $13.3 billion, including a 6.8% decline in 2017.

Prior to the five-year period, the expanding US defense budget and combat operations in the Middle East greatly increased demand for military-related small arms, ammunition, bombs, artillery shells, ordnances and other munitions. However, as the United States began to wind down combat operations and Congress attempted to reduce the federal

budget deficit, spending on industry-related products fell. While the defense market lost demand, the civilian small arms and ammunition segment performed very well. Increasing consumer concerns about stricter gun control laws led many to purchase industry products in anticipation of a ban. As a result, despite defense cuts, industry revenue made strong gains. However, as fears of gun regulation subsided following President Trump’s electoral victory in November 2016, demand for industry products fell, negatively impacting industry revenue. In response to a weakening domestic military market, industry players have increasingly sought growth in exports, which have been rising due to geopolitical tensions and global instability.

Over the five years to 2022, industry revenue is forecast to grow at an annualized rate of 3.5% to $15.8 billion. The defense market is anticipated to remain at historically low levels, and the domestic side is also set to remain weaker than average due to allayed fears of national gun control legislation under the Trump administration. As a result, industry operators will increasingly turn to export markets to offset weaker domestic demand. Moreover, industry profit is projected to slightly increase due to increased consumer demand and defense contractor restructuring.

Industry PerformanceExecutive Summary | Key External Drivers | Current Performance Industry Outlook | Life Cycle Stage

Industry operators will increasingly turn to export markets to offset weaker domestic demand

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 6

Industry Performance

Key External Driverscontinued

climbs. Non-NATO defense spending is expected to increase in 2017.

Local and state government investmentGrowth in spending by state and local government agencies generally coincides with increased funding of law enforcement. When law enforcement funding increases, gun and ammunition purchases also grow. Local and state government investment is expected to increase in 2017, representing a potential opportunity for the industry.

Per capita disposable incomeGuns and ammunition are typically discretionary purchases. When incomes rise, individuals can better afford

industry products. When incomes fall, demand for industry products often declines. Per capita disposable income is expected to increase in 2017.

Trade-weighted indexThe trade-weighted index (TWI) measures the strength of the US dollar relative to the currencies of its largest trading partners. Since exports account for a moderate share of industry revenue and imports account for a significant share of domestic demand, the TWI can significantly affect sales volumes. The trade-weighted index is expected to increase over 2017, representing a potential threat to the industry.

% c

hang

e

8

-8

-4

0

4

2210 12 14 16 18 20Year

Local and state government investment

SOURCE: WWW.IBISWORLD.COM

% c

hang

e

10

-10

-5

0

5

2210 12 14 16 18 20Year

Federal funding for defense

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 7

Industry Performance

War and government expenditure

The wars in Iraq and Afghanistan ushered in substantial increases in military spending by the government, resulting in additional purchases of the industry’s products. The industry especially increased sales of its military-grade, high-caliber weapons systems and munitions, such as tank ammo and howitzers.

However, this initial boom has recently become a detriment. In 2011, the United States completed the withdrawal of its troops from Iraq and has more recently begun curtailing combat operations in Afghanistan. The withdrawal of US troops from the Middle East resulted in a sharp

decline in demand for industry products, as warfare requires extensive resupply of ammunition. The United States stationed 90,000 troops in Afghanistan in 2012, compared with 10,000 at the beginning of 2016. In addition, budget sequestration has led to cuts in military spending. IBISWorld expects federal funding for defense to fall from $644.3 billion in 2012 to $540.9 billion in 2017. The military’s decline in gun and ammunition purchases has played a significant role in slowing down industry revenue growth. However, most recently, US military spending on industry products has climbed as bombing

Current Performance

The Guns and Ammunition Manufacturing industry has experienced increased volatility over the past five years. The industry experienced aggressive revenue growth in the years after the recession as fears of more restrictive gun control laws overrode consumers’ financial constraints. However, as the US military began to withdraw from the Middle East and Congress sought to address deficit spending, federal funding for defense dropped, greatly tempering overall revenue growth. In addition, fears of greater gun control subsided in 2014 after a series of measures proposed by the Obama administration failed in the Senate, including a ban on assault weapons. The subsequent combination of falling military and consumer spending caused revenue to fall.

Consumer demand was rekindled following renewed emphasis on gun control in 2016, as well as security fears. The June 2016 mass shooting at a nightclub in Orlando, FL, combined with pollsters’ favored odds of Hillary Clinton winning the November election, stoked fears of impending legislation. On the military side, many manufacturers used growing foreign demand for US arms and

ammunition to partially offset a weakening defense market at home. Even domestic military demand recently picked up as US bombing operations against ISIS intensified.

The 2016 US presidential election may have exerted the greatest impact on the industry. Donald J. Trump’s victory over Hillary Clinton eased concerns over sweeping gun reform. Indeed, his win caused a 6.8% revenue decline in 2017 alone. Therefore, industry revenue is expected to decline at an annualized rate of 1.0% to $13.3 billion over the five years to 2017.

% c

hang

e

15

-15

-10

-5

0

5

10

2309 11 13 15 17 19 21Year

Industry revenue

SOURCE: WWW.IBISWORLD.COM

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 8

Industry Performance

International trade Amid a weakening domestic military market, the industry’s defense contractors have increasingly sought growth in foreign markets. Fortunately for operators, growing geopolitical tensions and instability around the world have boosted military spending in many regions. Over the five years to 2017, non-NATO defense

spending, which excludes most Western military expenditure, is expected to climb an annualized 2.9% to $865.6 billion. Demand for munitions from US allies in the Middle East has surged in recent years as tensions with Iran climbed and conflict and instability proliferated. Tensions in Asia have also increased, creating further

Commercial demand Overall, private-sector demand has been the biggest driver of industry revenue growth, even picking up the slack caused by declining military spending. The past five years’ growth is mainly attributable to fears of potentially tougher gun control legislation. In 2012, with the presidential election looming, many consumers looking to purchase industry products wondered what another four years of the Obama administration might hold for gun laws, and whether purchasing a firearm in the future would prove more difficult. The situation was exacerbated by high-profile mass shootings, such as in Aurora, CO, and Sandy Hook Elementary School in Newtown, CT, both of which took place in 2012. In December 2012, the Obama administration announced its intention to reform gun laws to prevent similar tragedies from occurring.

As a result, consumers purchased firearms and ammunition at record rates, with industry revenue surging through 2013. In 2014, demand began to normalize as it became clear that more stringent gun control laws would not be passed on a

federal level. Therefore, industry revenue fell 10.6% that year. However, this dip was only temporary, as attacks such as the Charleston, SC church shooting and the San Bernardino, CA, terrorist attacks stoked consumer fears of regulation and the need for self-defense, all during a heated presidential campaign. Domestic demand for guns and ammunition surged in the second half of 2015, breaking previous records, with the FBI National Instant Criminal Background Check System (NICS) recording an all-time high for checks during the year. Moreover, in early 2016, President Barack Obama issued an executive order that expanded gun sales licensing and background check coverage, likely further heightening consumer anxiety over regulations. The new administration has rolled back Mr. Obama’s efforts.

operations against ISIS has created demand for bombs and ammunition.

Federal government and local law enforcement agencies’ budgets also grew over the past five years. As a result of the sustained risk of terrorism, the responsibilities of federal, state and local departments have expanded to include

terrorist attack prevention, thereby increasing budgets for guns and ammunition. Nevertheless, falling tax receipts caused by poor economic conditions have put pressure on law enforcement budgets, with local and state government investment growing at a tepid annualized rate of 0.6% over the five years to 2017.

War and government expenditure continued

Private-sector demand has been the biggest driver of industry revenue growth

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 9

Industry Performance

Consolidation Declining demand from the military and the 2014 contraction is expected to cause industry profit to drop from 9.8% of revenue in 2012 to 7.8% in 2017. Overall market share concentration, defined as the top players’ share of industry revenue, has declined over the five years to 2017 due to declining revenue for the industry’s biggest defense suppliers. The military market has high barriers to entry, and its products tend to be more sophisticated and expensive. Therefore, this segment accounts for a large portion of industry revenue and is dominated by a few large companies, including General Dynamics Corporation and BAE Systems PLC. As a result, this segment skews overall industry concentration. When defense spending declined, the resulting loss in revenue among defense contractors caused overall industry concentration to also decline. The industry further fragmented when Alliant Techsystems spun off its commercial business, now called Vista Outdoor, and merged its defense business with Orbital Sciences, creating Orbital ATK.

However, in the consumer market, mergers and acquisitions have been more

prevalent. For example, private equity firm Cerberus Capital went on an acquisition spree for weapons manufacturers prior to gun and ammunition conglomerate Freedom Group’s attempted public offering. This trend toward consolidation indicates that major players within this segment are realizing the benefits of economies of scale and are attempting to gain a competitive advantage through acquisition and growth.

Over the five years to 2017, the number of industry establishments is expected to grow at an annualized rate of 6.0% to 690. However, as defense contractors and some consumer manufacturers restructured, the number of employees expanded at a slower rate and even declined in recent years. Therefore, industry employment is expected to grow at an annualized rate of only 4.0% to 45,308 workers during the five-year period.

Declining demand from the military is expected to cause industry profit to drop

demand for US-made guns and ammunition. As a result, industry exports are expected to grow at an annualized rate of 5.9% to $8.4 billion over the five years to 2017.

Unlike exports, industry imports are much more focused on the consumer

market. Once consumer demand for industry products declined in 2014, imports plunged. However, the recent pickup in demand has helped imports recover. Over the five years to 2017, imports are expected to increase at an annualized rate of 4.9% to $6.9 billion.

International trade continued

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 10

Industry Performance

Demand normalizes After years of surging demand, consumers are expected to slow the pace of their recent gun and ammunition spending. After previous failed attempts to create more stringent gun regulations, it has become clear that the chances of such laws being passed on a federal level are increasingly dim. Consequently, consumers will be less worried about new regulations in the coming years and, after years of stockpiling, less likely to purchase industry products at the same rate as in the previous five years. This will likely help to normalize demand in the near term, causing fewer sales. However, if prospects for federal regulation increase, higher demand may return. Some state governments have already implemented more stringent regulations, potentially driving away demand from those regions.

While demand from consumers moderates, the government segment is anticipated to slightly pick up. Based on President Trump’s fiscal 2018 budget request, US Army, Air Force, Navy and Marine outlays for ammunition, small arms, ordnances and similar munitions are anticipated to increase more than 7.6% between 2018 and 2023. Drivers of this trend include increased combat operations in Iraq and Syria and the eventual implementation of the Modular Handgun Systems (MHS) contract. The MHS is an Army and Air Force attempt to replace their Beretta M9 pistol.

Nonetheless, spending will still be well below rates in previous years. In addition, the overall defense budget is expected to grow over the next five years, particularly in procurement, research and development.

Federal, state and local law enforcement agencies are projected to remain frugal on spending as budgetary constraints persist. For instance, local and state government investment is projected to grow at a mere annualized rate of 0.9% over the next five years. Nonetheless, fears of terrorism are anticipated to lead to continued funding of federal, state and local law enforcement to expand terrorism prevention and response capabilities, bolstering demand for industry products.

As in the previous five years, industry operators will try to increase their exposure to the export market. Geopolitical tensions and instability in the Middle East and Asia will continue to fuel foreign demand for US munitions. However, exports are expected to level off in the near term after the recent surge. Alongside demand normalizing, export growth is expected to slow, growing at an annualized rate of 3.6% to $10.1 billion

Industry Outlook

The Guns and Ammunition Manufacturing industry’s trajectory over the next five years will largely depend on US defense spending and perceptions about the future of firearms legislation. While revenue experienced some volatility over the past five years, it is forecast to grow in a more tempered fashion as consumer demand eventually begins to

normalize. Increased military spending on industry products will help bolster revenue growth, despite overall spending remaining below levels experienced in 2012. Moreover, industry operators will increasingly depend on exports for expansion. Over the five years to 2022, industry revenue is forecast to grow at an annualized rate of 3.5% to $15.8 billion.

Geopolitical tensions will continue to fuel foreign demand for US munitions

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 11

Industry Performance

Other industry trends Over the next five years, profitability is projected to recover and stabilize as demand and revenue grow. Defense contractors and some commercial manufacturers will continue restructuring to improve profitability. Market share is also expected to shift in favor of the industry’s larger participants, mostly through acquisitions. These operators have sizable manufacturing facilities with lower production costs, enabling them to capture an increasing portion of the market at the expense of smaller players.

Over the next five years, the number of establishments is projected to grow an annualized 3.9% to total 836. Similarly, employment is forecast to climb an annualized 3.6% to 54,084 workers during the five-year period.

over the five years to 2022. Nonetheless, average export values over the next five years will be significantly higher compared with the past five years. Similarly, imports will also rise, with

their value projected to rise at an annualized rate of 3.3% to $8.1 billion during the five-year period. A stronger US dollar should make imports more price-competitive with US products.

Demand normalizes continued

Market share is expected to shift in favor of the industry’s larger participants

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 12

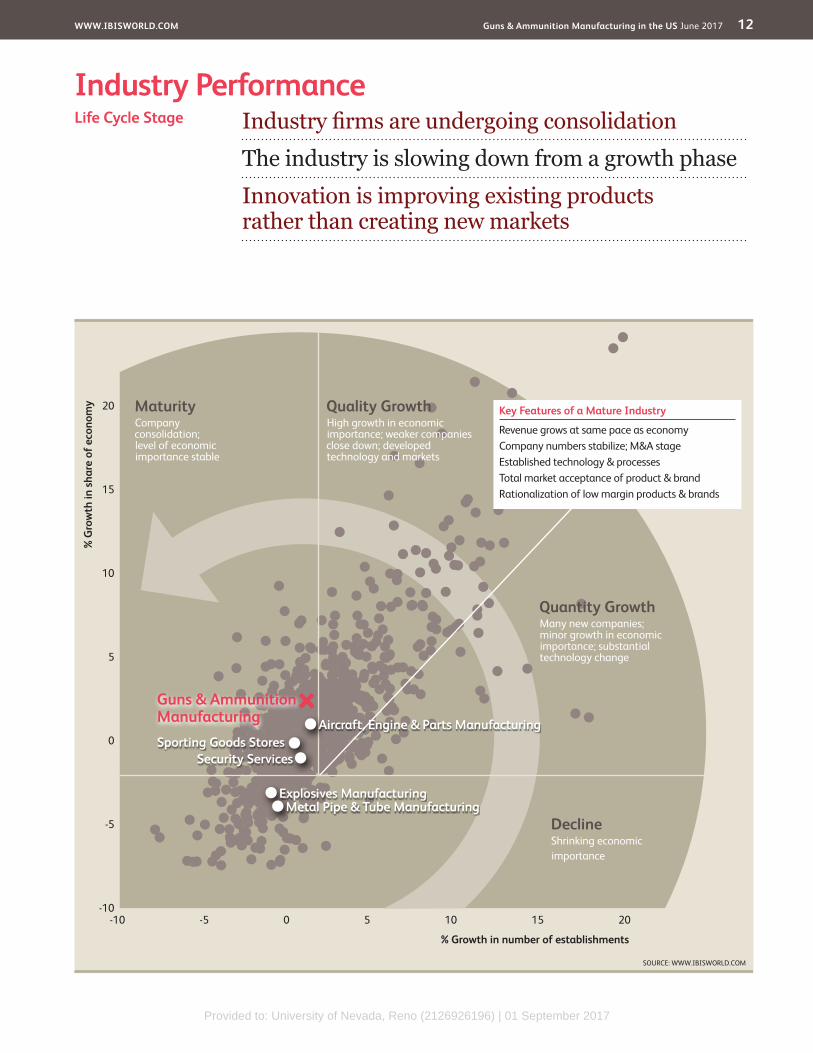

Industry PerformanceIndustry firms are undergoing consolidation

The industry is slowing down from a growth phase

Innovation is improving existing products rather than creating new markets

Life Cycle Stage

SOURCE: WWW.IBISWORLD.COM

20

15

10

5

0

-5

-10

% G

row

th in

sha

re o

f eco

nom

y

% Growth in number of establishments

-10 -5 0 5 10 15 20

DeclineShrinking economicimportance

Quality GrowthHigh growth in economic importance; weaker companies close down; developed technology and markets

MaturityCompany consolidation;level of economic importance stable

Quantity GrowthMany new companies; minor growth in economic importance; substantial technology change

Key Features of a Mature Industry

Revenue grows at same pace as economyCompany numbers stabilize; M&A stageEstablished technology & processesTotal market acceptance of product & brandRationalization of low margin products & brands

Explosives Manufacturing

Sporting Goods Stores

Metal Pipe & Tube Manufacturing

Aircraft, Engine & Parts Manufacturing

Security Services

Guns & Ammunition Manufacturing

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 13

Industry Performance

Industry Life Cycle After years of growth, the industry has entered a mature stage of its life cycle. A resurgence of demand from the civilian sector, among other factors, supported industry revenue over the past few years. Exports and defense spending are expected to offset waning revenue gains on the commercial side of the industry. Over the 10 years to 2022, industry value added (IVA), which measures an industry’s contribution to the economy, is expected to grow an annualized1.8%, compared with 2.1% annualized GDP growth anticipated over the same period.

Over the past five years, significant players have engaged in a multitude of mergers and acquisitions, including Freedom Group’s recent acquisition spree and both Smith & Wesson’s and Sturm, Ruger & Company’s acquisitions of small companies to expand their product lines. Large players within this

industry have experienced the spike in demand and have been scrambling to expand their product lines to accommodate growing customer bases.

While the industry is constantly innovating existing products, its core products and major markets have essentially been established and its participants are mostly focused on winning market share from competing countries and companies. However, over the next five years, technological advancements are expected to begin changing how the industry operates. Smart guns, which use fingerprint or radio-frequency identification (RFID) technology to identify their owners, are anticipated to carve out market share from more conventional firearms manufacturers. Moreover, 3D printing technology could increase the speed and efficiency of industry production.

This industry is Mature

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 14

Products & Services

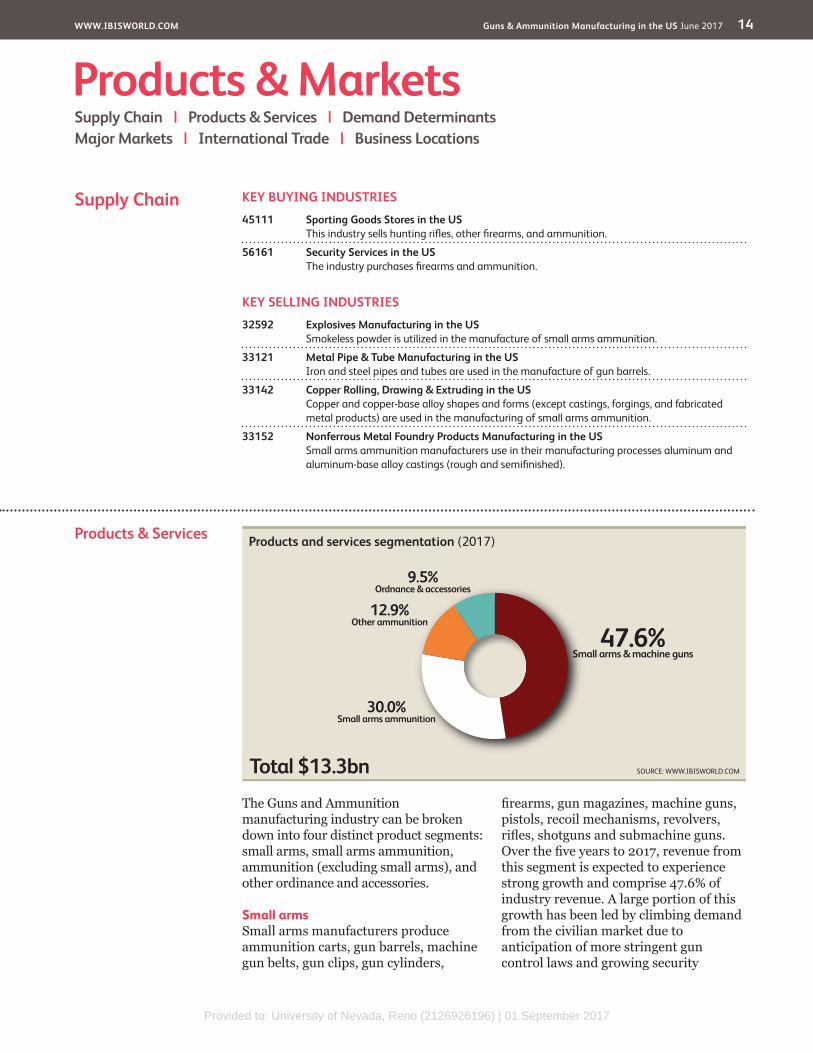

The Guns and Ammunition manufacturing industry can be broken down into four distinct product segments: small arms, small arms ammunition, ammunition (excluding small arms), and other ordinance and accessories.

Small armsSmall arms manufacturers produce ammunition carts, gun barrels, machine gun belts, gun clips, gun cylinders,

firearms, gun magazines, machine guns, pistols, recoil mechanisms, revolvers, rifles, shotguns and submachine guns. Over the five years to 2017, revenue from this segment is expected to experience strong growth and comprise 47.6% of industry revenue. A large portion of this growth has been led by climbing demand from the civilian market due to anticipation of more stringent gun control laws and growing security

Products & MarketsSupply Chain | Products & Services | Demand Determinants Major Markets | International Trade | Business Locations

KEY BUYING INDUSTRIES

45111 Sporting Goods Stores in the US This industry sells hunting rifles, other firearms, and ammunition.

56161 Security Services in the US The industry purchases firearms and ammunition.

KEY SELLING INDUSTRIES

32592 Explosives Manufacturing in the US Smokeless powder is utilized in the manufacture of small arms ammunition.

33121 Metal Pipe & Tube Manufacturing in the US Iron and steel pipes and tubes are used in the manufacture of gun barrels.

33142 Copper Rolling, Drawing & Extruding in the US Copper and copper-base alloy shapes and forms (except castings, forgings, and fabricated metal products) are used in the manufacturing of small arms ammunition.

33152 Nonferrous Metal Foundry Products Manufacturing in the US Small arms ammunition manufacturers use in their manufacturing processes aluminum and aluminum-base alloy castings (rough and semifinished).

Supply Chain

Products and services segmentation (2017)

Total $13.3bn

47.6%Small arms & machine guns

30.0%Small arms ammunition

12.9%Other ammunition

9.5%Ordnance & accessories

SOURCE: WWW.IBISWORLD.COM

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 15

Products & Markets

Demand Determinants

Economic conditionsFor most people, guns and ammunition are expensive discretionary goods. As a result, demand for industry products depends on factors such as disposable income, the unemployment rate and consumer confidence. When unemployment is low and consumers’ income and confidence are high, individuals are more willing to purchase industry products. However, many other factors influence gun purchases, some of which override economic conditions.

RegulationRegulations can have a substantial impact on demand for guns and ammunition. Certain states restrict the types of small arms and ammunition that consumers can purchase, thus limiting

consumption of industry goods. Strict licensing requirements can also reduce the industry’s customer base, as fewer people can make gun purchases. On the other hand, loose firearm regulations in other states increase not only the customer base but also the range of products manufacturers offer.

Public perception of gun laws, politics, security and crimeOver the past few years, a major driver of gun and ammunition consumption has been the public perception of gun regulations. Recent shootings have brought the idea of stricter gun regulations to the national forefront. As a result, many consumers began to fear that they only have a limited amount of time to purchase small arms and ammunition and have

Products & Servicescontinued

concerns. Falling orders from the military market has tampered this growth. However, the recent pick-up in US combat involvement in the Middle East and rising foreign military demand has recently bolstered the defense segment.

AmmunitionThe sale of ammunition is almost as large as the sale of arms. Small arms ammunition (ammo 30mm or less) includes handgun, shotgun, rifle, machine gun and even 30mm autocannon ammunition. It also includes blank cartridges, bullet jackets and percussion caps. Over the past five years, small arms ammunition’s share of industry revenue has reached 30.0%. Because ammo sales generally follow arms sales, their share of revenue changes little. Just like small arms, sales of ammunition to civilians has surged over the past five years, while military grade ammunition declined.

The sale of other ammunition accounts for about 12.9% of industry revenue. This

product category mostly consists of military grade ammunition that is greater than 30mm, including bombs, mortar, tank and artillery shells, fuses, missile warheads, mines, torpedoes and related components. Due to reduced defense spending, other ammunitions’ share of revenue has declined over the past five years (from 15.1% in 2011, closest data available). However, the recent pick-up in US bombing in Iraq and Syria has increased demand for bomb and similar items.

Ordnance and accessoriesOrdnance manufacturing involves more explosive weaponry and includes aircraft and antiaircraft artillery, antitank rocket, cannons, field artillery, gun turrets, howitzers, mortars, naval artillery, rocket projectors, tampions, line-throwing guns, tank artillery, torpedo tubes, flamethrowers and gun turrets. This segment’s products are almost exclusively bought by the military and has thus dropped in value as defense spending fell. It represents 9.5% of industry revenue in 2017.

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 16

Products & Markets

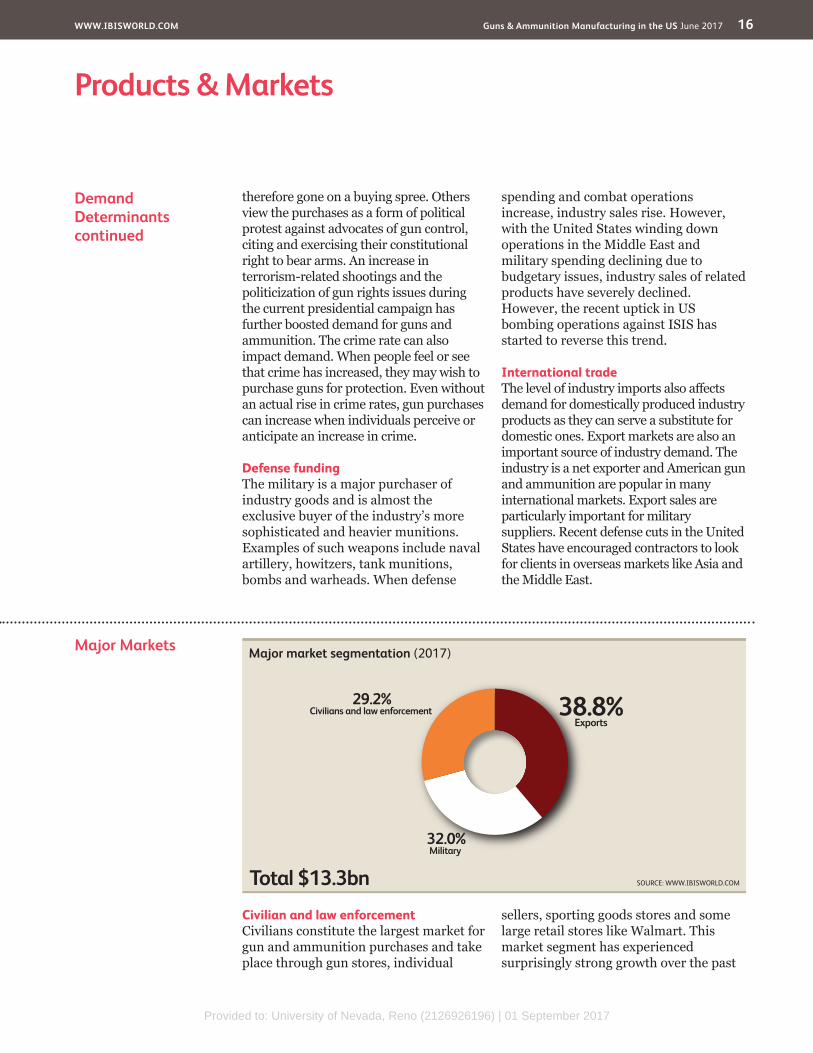

Major Markets

Civilian and law enforcementCivilians constitute the largest market for gun and ammunition purchases and take place through gun stores, individual

sellers, sporting goods stores and some large retail stores like Walmart. This market segment has experienced surprisingly strong growth over the past

Demand Determinantscontinued

therefore gone on a buying spree. Others view the purchases as a form of political protest against advocates of gun control, citing and exercising their constitutional right to bear arms. An increase in terrorism-related shootings and the politicization of gun rights issues during the current presidential campaign has further boosted demand for guns and ammunition. The crime rate can also impact demand. When people feel or see that crime has increased, they may wish to purchase guns for protection. Even without an actual rise in crime rates, gun purchases can increase when individuals perceive or anticipate an increase in crime.

Defense fundingThe military is a major purchaser of industry goods and is almost the exclusive buyer of the industry’s more sophisticated and heavier munitions. Examples of such weapons include naval artillery, howitzers, tank munitions, bombs and warheads. When defense

spending and combat operations increase, industry sales rise. However, with the United States winding down operations in the Middle East and military spending declining due to budgetary issues, industry sales of related products have severely declined. However, the recent uptick in US bombing operations against ISIS has started to reverse this trend.

International tradeThe level of industry imports also affects demand for domestically produced industry products as they can serve a substitute for domestic ones. Export markets are also an important source of industry demand. The industry is a net exporter and American gun and ammunition are popular in many international markets. Export sales are particularly important for military suppliers. Recent defense cuts in the United States have encouraged contractors to look for clients in overseas markets like Asia and the Middle East.

Major market segmentation (2017)

Total $13.3bn

38.8%Exports

32.0%Military

29.2%Civilians and law enforcement

SOURCE: WWW.IBISWORLD.COM

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 17

Products & Markets

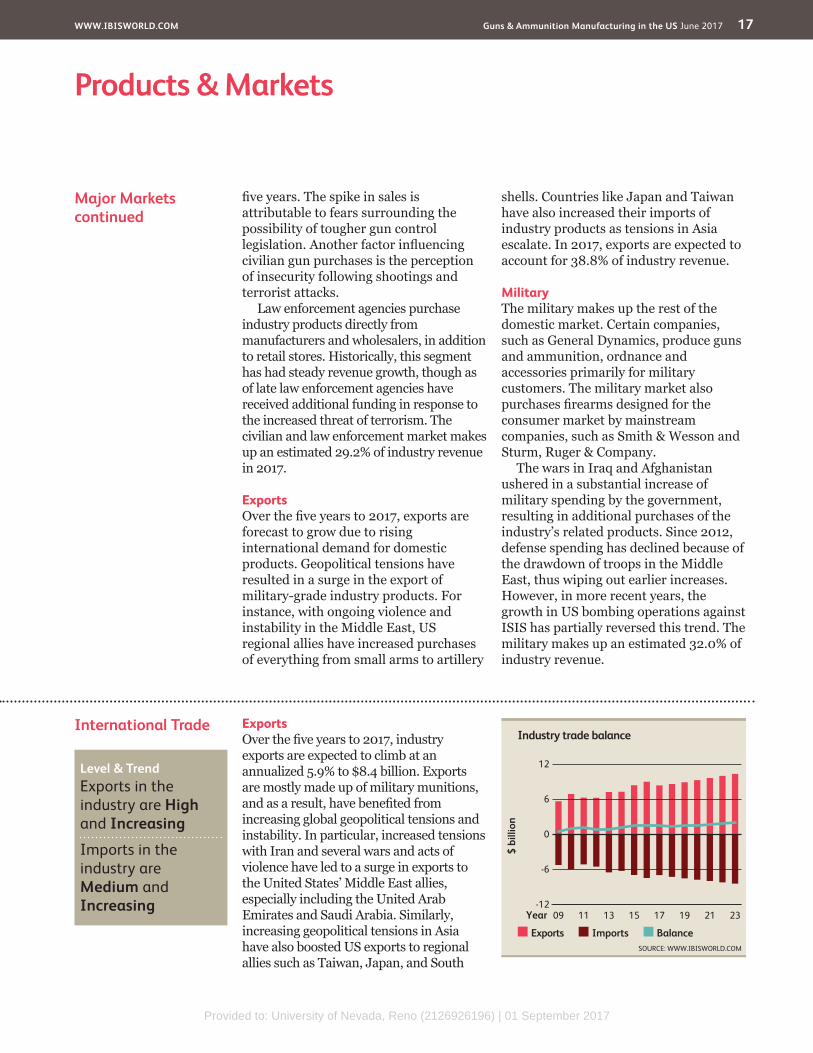

International Trade ExportsOver the five years to 2017, industry exports are expected to climb at an annualized 5.9% to $8.4 billion. Exports are mostly made up of military munitions, and as a result, have benefited from increasing global geopolitical tensions and instability. In particular, increased tensions with Iran and several wars and acts of violence have led to a surge in exports to the United States’ Middle East allies, especially including the United Arab Emirates and Saudi Arabia. Similarly, increasing geopolitical tensions in Asia have also boosted US exports to regional allies such as Taiwan, Japan, and South

Major Marketscontinued

five years. The spike in sales is attributable to fears surrounding the possibility of tougher gun control legislation. Another factor influencing civilian gun purchases is the perception of insecurity following shootings and terrorist attacks.

Law enforcement agencies purchase industry products directly from manufacturers and wholesalers, in addition to retail stores. Historically, this segment has had steady revenue growth, though as of late law enforcement agencies have received additional funding in response to the increased threat of terrorism. The civilian and law enforcement market makes up an estimated 29.2% of industry revenue in 2017.

ExportsOver the five years to 2017, exports are forecast to grow due to rising international demand for domestic products. Geopolitical tensions have resulted in a surge in the export of military-grade industry products. For instance, with ongoing violence and instability in the Middle East, US regional allies have increased purchases of everything from small arms to artillery

shells. Countries like Japan and Taiwan have also increased their imports of industry products as tensions in Asia escalate. In 2017, exports are expected to account for 38.8% of industry revenue.

MilitaryThe military makes up the rest of the domestic market. Certain companies, such as General Dynamics, produce guns and ammunition, ordnance and accessories primarily for military customers. The military market also purchases firearms designed for the consumer market by mainstream companies, such as Smith & Wesson and Sturm, Ruger & Company.

The wars in Iraq and Afghanistan ushered in a substantial increase of military spending by the government, resulting in additional purchases of the industry’s related products. Since 2012, defense spending has declined because of the drawdown of troops in the Middle East, thus wiping out earlier increases. However, in more recent years, the growth in US bombing operations against ISIS has partially reversed this trend. The military makes up an estimated 32.0% of industry revenue.

Level & Trend Exports in the industry are High and Increasing

Imports in the industry are Medium and Increasing

$ bi

llion

12

-12

-6

0

6

2309 11 13 15 17 19 21Year

Exports Imports Balance

Industry trade balance

SOURCE: WWW.IBISWORLD.COM

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 18

Products & Markets

International Tradecontinued

Korea. These countries have close defense relationships with the United States and are dealing with an increasingly powerful China. Canada accounts for a sizable share of exports due to the country’s proximity to the United States, membership in the North American Free Trade Agreement and US defense ties. The surge in industry exports has helped domestic defense contractors partially offset a weak domestic military market, with exports’ share of industry revenue expected to rise from a low of 45.1% in 2012 to 63.3% in 2017.

ImportsUnlike exports, industry imports primarily consist of small arms and ammunition tailored to the consumer and law

enforcement segments. Initially, as demand for civilian industry products surged, many customers have turned to imports to satisfy their needs. In the five years to 2017, imports are expected to climb at an annualized 4.9% to $6.9 billion. But imports’ share of domestic demand has fallen in the last two years to 51.8% in 2017, due to normalization of demand in 2014 and a stronger dollar. European manufacturers such as Italy, Austria, the United Kingdom and Germany dominate the import markets, and all four have close defense ties with the United States. Germany, Austria and Italy are also famous for small arms manufactures such as Heckler & Koch (Germany), Glock (Austria) and Beretta (Italy).

Imports From...

Total $6.9bn

6.1%United

Kingdom

7.5%Germany9.1%

Italy

12.5%Austria

64.8%All others

Exports To...

Total $8.4bn

61.5%All others

17.1%United Arab

Emirates

7.3%Saudi Arabi

7.1%South Korea

7.0%Canada

Year: 2017SIZE OF CHARTS DOES NOT REPRESENT ACTUAL DATA SOURCE: USITC

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 19

Products & Markets

Business Locations 2017

MO1.4

West

West

West

Rocky Mountains Plains

Southwest

Southeast

New England

Great Lakes

VT0.2

MA0.7

RI0.1

NJ0.3

DE0.0

NH0.3

CT22.5

MD0.1

DC0.0

1

5

3

7

2

6

4

8 9

Additional States (as marked on map)

AZ2.3

CA2.0

NV0.6

OR1.4

WA1.5

MT1.9

NE0.5

MN0.6

IA0.8

OH2.2 VA

0.5

FL3.0

KS0.6

CO1.1

UT1.2

ID0.8

TX3.9

OK0.2

NC1.3

AK31.3

WY0.4

TN1.6

KY0.7

GA1.6

IL1.4

ME0.4

ND0.1

WI1.8 MI

1.0 PA2.3

WV0.3

SD0.6

NM0.1

AR1.1

MS0.5

AL0.7

SC0.3

LA0.1

HI0.1

IN0.9

NY1.1 5

67

8

321

4

9

SOURCE: WWW.IBISWORLD.COM

Mid- Atlantic

Establishments (%)

Less than 3% 3% to less than 10% 10% to less than 20% 20% or more

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 20

Products & Markets

Business Locations The location of manufacturing establishments is generally influenced by their proximity to major markets, as well as material and supply industries. Manufacturing establishments also tend to be highly correlated with population density. IBISWorld estimates that the industry is concentrated in the West, New England and Southeast regions of the United States, due to their proximity to major supply industries as well as population centers. These regions combined will account for 72.7% of industry establishments.

The West region will account for 36.8% of industry establishments. This is mostly due to Alaska, which housed 31.3% of industry establishments, the highest concentration in the United States. This region also has easy access to the Pacific Ocean for shipping exports.

The New England region will account for an estimated 24.2% of industry establishments. New England is home to so-called “Gun Valley,” a band of western Massachusetts and Connecticut historically grounded in the production and sale of small firearms.

The Southeast region includes 11.7% of industry establishments and is the most

populous geographic area in the United States. This suggests that many industry operators seek to take advantage of proximity to their domestic customer bases.

Among ammunition manufacturers, Alaska, Florida, Georgia and California have a high concentration of establishments. Arizona, Alaska, Texas, Florida and Ohio have the most gun and ordnance manufacturing establishments.

%

40

0

10

20

30

Sout

hwes

t

Wes

t

Gre

at L

akes

Mid

-Atla

ntic

New

Eng

land

Plai

ns

Rock

y M

ount

ains

Sout

heas

t

EstablishmentsPopulation

Distribution of establishments vs. population

SOURCE: WWW.IBISWORLD.COM

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 21

Cost Structure Benchmarks

The Guns and Ammunition Manufacturing industry has been making the gradual shift toward higher levels of capital investment in manufacturing automation with the goal of creating more efficient and profitable enterprises.

ProfitIndustry profit is based on earnings before interest and taxes recorded by industry operators. Profit will vary between players depending on the size of the manufacturing facility that they

Key Success Factors Having a loyal customer baseThere is a distinct competitive advantage in cultivating and maintaining strong long-term customer relationship.

Access to high quality inputsCompanies within this industry group must be able to source a variety of raw materials, both from within the United States and overseas.

Effective quality controlIn providing high-quality products and services, operators must maintain detailed and extensive quality assurance programs.

Having a good technical knowledge of the productHaving a good technical knowledge of the product is a key success factor within this industry group because companies must provide strong engineering, design and technical support to clients.

Establishment of brand namesStrong brand recognition is considered to be a major basis of competition.

Control of distribution arrangementsThe cultivation, maintenance and control of downstream distribution channels are a distinct advantage.

Market Share Concentration

The Guns and Ammunition Manufacturing industry consists of many small to medium operators. The wide variety of products produced in this industry and the diverse buying markets make it difficult for individual companies to grab a large portion of industry’s entire market share. Overall industry market concentration is low and lost some ground over the last five years before rebounding a bit in 2017. The top four players account for an estimated 37.0% of industry revenue. However, this drop has been primarily led by the huge exposure the top players have to defense spending.

Due to the high barriers to entry and sophistication of the military market, concentration in the defense segment of the industry is very high and is dominated by General Dynamics and

Orbital ATK. Because the military is such a big buyer of guns and ammunition and the increased prices of more complex weapon systems, this segment also represents a large portion of overall industry revenue. Defense bias also explains why concentration decreased when falling military spending caused defense contractors to lose money. Moreover, the 2015 breakup of ATK’s industry-specific operations between Orbital ATK and Vista Outdoor fragmented the industry further.

For most of the past five years, concentration in the civilian market has been increasing. Within this period, major players such as the Freedom Group have undergone acquisition sprees. Smith & Wesson and Sturm, Ruger & Company have also acquired small gun manufacturers to expand their product lines.

Competitive LandscapeMarket Share Concentration | Key Success Factors | Cost Structure Benchmarks Basis of Competition | Barriers to Entry | Industry Globalization

Level Concentration in this industry is Low

IBISWorld identifies 250 Key Success Factors for a business. The most important for this industry are:

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 22

Competitive Landscape

Cost Structure Benchmarkscontinued

operate, with larger operators generally benefiting from economies of scale. IBISWorld estimates that in 2017, the industry will obtain profit equivalent to 7.8% of an average operator’s revenue. Overall, industry profitability has declined as reduced defense spending has squeezed the profit of large defense contractors. Moreover, the recent reversal of the boom in civilian gun and ammunition sales further pressure profitability. Nonetheless, profitability has increased since 2014, amid a resurgence in civilian and eventually military sales.

PurchasesOne of the largest expenses of the average industry player’s cost structure consists of purchases. These principally consist of the cost of raw materials that are used during the manufacturing process. Commonly used production

inputs include metals such as steel, copper tubing, aluminum and iron castings. Fluctuations in the prices of these materials affect operators’ revenue and profitability.

In many cases, companies can pass a significant portion of raw material price increases on to customers in the form of product price increases or surcharges. Most industry operators enter into fixed-price contracts, so short-term fluctuations in raw material prices have little impact on profitability. However, the persistent higher raw material prices experienced during the past five years have placed increasing upward pressure on the cost structure of industry participants.

Across product segments, manufacturing costs associated with raw material expenditure fluctuate due to the differences in the size and density of the product being manufactured. The

Sector vs. Industry Costs

n Profi tn Wagesn Purchasesn Depreciationn Marketingn Rent & Utilitiesn Other

Average Costs of all Industries in sector (2017)

Industry Costs (2017)

0

20

40

60

Perc

enta

ge o

f rev

enue

80

100

SOURCE: WWW.IBISWORLD.COM

7.6 7.8

23.1

5.4 1.03.1

38.8

20.8

19.9

2.3 0.52.5

54.4

12.3

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 23

Competitive Landscape

Basis of Competition InternalAn assortment of competitive factors encourage competition within the Guns and Ammunition Manufacturing industry. Factors like medium barriers to entry increase the threat of competition from firms outside the industry, while low levels of product differentiation encourage direct competition among industry players on the basis of price.

While players in this industry compete primarily based on product pricing, other factors such as product innovation and branding are also important for some product segments. Price competition is particularly evident in product segments where the pace of product development has virtually ground to a halt. This is the case for the majority of industry products. However, price competition

occurs while maintaining a standard level of product quality.

There are also other competitive differentiation strategies used within the industry. These include service quality, brand recognition, effective and timely distribution and technical support. The introduction of new and improved product designs and the acquisition of product lines at different price points is a key to maintaining and increasing product and market share. Products manufactured and developed in the industry also have a high research and development (R&D) component. As a result, technical excellence rather than price can be more important to remaining competitive within certain segments. In technologically advanced segments (i.e. specialized military munitions), R&D is particularly important in developing new

Cost Structure Benchmarkscontinued

complexity, quality and quantity of raw materials used are also factors influencing cost. Shortages and changes in the price of raw materials are common (availability and cost are influenced by, among other factors, political stability in exporting nations). In 2017, purchases are estimated to account for 38.8% of an average operator’s revenue.

WagesThe industry has a high level of capital intensity compared to other industries. Despite this, labor costs are high relative to other manufacturing industries because of the level of skill required to manufacture certain products, especially military grade equipment. IBISWorld estimates that in 2017, wage costs incurred by the industry will account for 20.8% of an average company’s revenue. They comprised 18.5% in 2012, suggesting little change in demand for highly skilled workers.

Depreciation, rent and utilitiesThe cost of depreciation will invariably fluctuate between operators depending on their size and the amount of capital expenses involved. The cost of new plant and equipment used to manufacture industry products is significant and periodic product innovation necessitates regular investment in new capital. In 2017, depreciation is estimated to account for 2.1% of an average operator’s revenue. Companies may reduce facility depreciation by leasing or renting the factories, with rent and utilities accounting for an estimated 5.4% of industry revenue.

OtherOther expenditures include communications, legal, accounting fees. Advertising expenses make up 0.9% of revenue. In 2017, all other expenses are expected to equal about 24.1% of Guns and Ammunition Manufacturing industry revenue.

Level & Trend Competition in this industry is Medium and the trend is Increasing

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 24

Competitive Landscape

Barriers to Entry Several barriers to entry exist in this industry. A significant financial investment is required to acquire, maintain and update plant and equipment. This cost may deter some firms from entering the industry. Machinery operators also need to be trained, but these costs are relatively insignificant. The rising level of unemployment in the United States has lowered some of the difficulty in obtaining a workforce with the required skills.

Research and development (R&D) is necessary for product innovation. To effectively compete, an entrant should be committed to spending a significant amount on R&D. In addition, many incumbent operators in this industry have developed strong relationships with upstream suppliers and downstream markets, making it difficult for other companies to break in. This may be a deterrent to some entrants into the industry.

For certain product segments, establishing a brand for their product represents a barrier to entry. This may require funds to be spent on advertising to establish a market presence. Companies are likely to have trouble entering the industry because of the customer loyalty that the more prominent industry participants already have, including Remington and Smith & Wesson.

Guns and ammunition manufacturers must fully appreciate costs associated

Basis of Competitioncontinued

products and ensuring products are up-to-date and evolving.

Companies that are able to diversify their customer base can also achieve a competitive advantage. Operators that can serve both military and civilian segments can mitigate their exposure to the business cyclicality. On the other hand, companies like BAE Land and Armament, which sells almost exclusively to the military, have seen revenue significantly fall. At the same time, being a supplier to the military can also produce a more secure revenue source as regulations and requirements reduce competition in this segment.

ExternalWhile the industry does not contend with competition from other industries, it does face import competition. Consumers may

find imported firearms and ammunition to be of higher quality and better price. The Austrian Glock and Italian Beretta brands are especially popular in the United States in both the civilian and law enforcement markets. When it comes to suppliers or military guns and ammunition, competition for contract with foreign firms can be strong. However, the nature of military equipment manufacturing and the strength of domestic firms, combined with advantages associated with domestic manufacturing and regulations, means that foreign produced products are not as big a threat in this segment. Yet, competition for foreign contracts is tougher. Domestic manufacturers must deal with foreign firms that can offer cheaper equipment and/or have special connections to local governments.

Level & Trend Barriers to Entry in this industry are Medium and Steady

Barriers to Entry checklist

Competition MediumConcentration LowLife Cycle Stage MatureCapital Intensity MediumTechnology Change MediumRegulation & Policy HeavyIndustry Assistance Medium

SOURCE: WWW.IBISWORLD.COM

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 25

Competitive Landscape

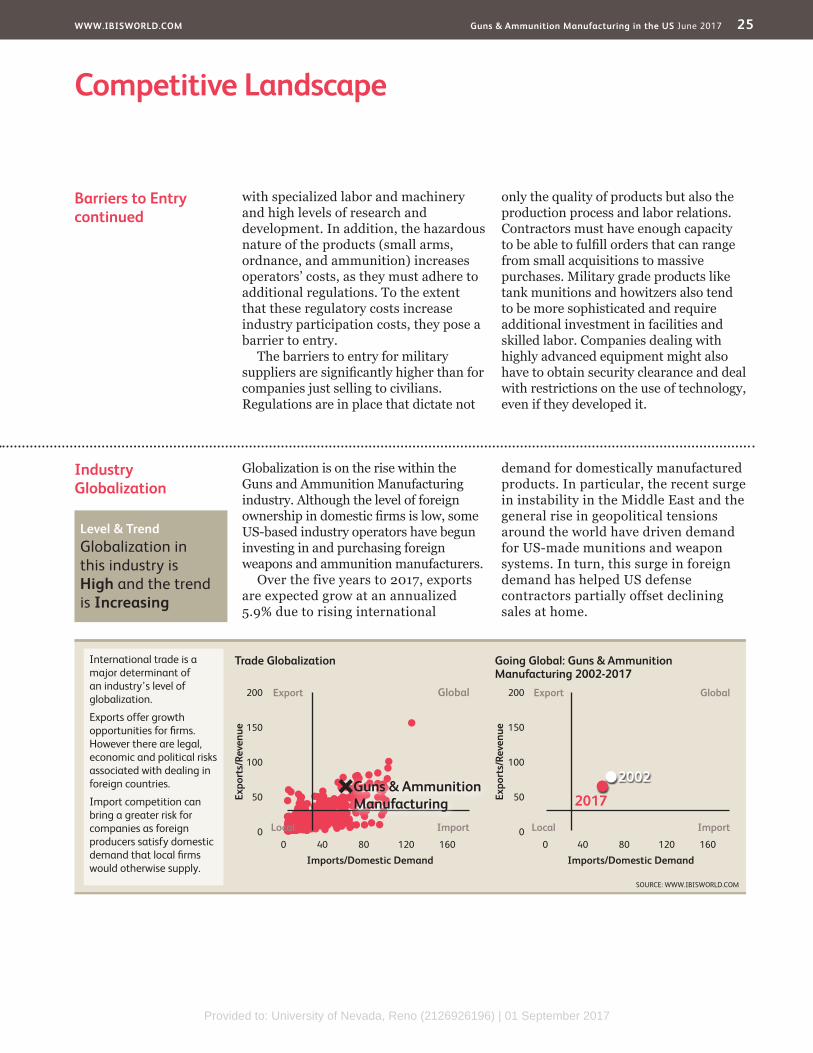

Industry Globalization

Globalization is on the rise within the Guns and Ammunition Manufacturing industry. Although the level of foreign ownership in domestic firms is low, some US-based industry operators have begun investing in and purchasing foreign weapons and ammunition manufacturers.

Over the five years to 2017, exports are expected grow at an annualized 5.9% due to rising international

demand for domestically manufactured products. In particular, the recent surge in instability in the Middle East and the general rise in geopolitical tensions around the world have driven demand for US-made munitions and weapon systems. In turn, this surge in foreign demand has helped US defense contractors partially offset declining sales at home.

Barriers to Entrycontinued

with specialized labor and machinery and high levels of research and development. In addition, the hazardous nature of the products (small arms, ordnance, and ammunition) increases operators’ costs, as they must adhere to additional regulations. To the extent that these regulatory costs increase industry participation costs, they pose a barrier to entry.

The barriers to entry for military suppliers are significantly higher than for companies just selling to civilians. Regulations are in place that dictate not

only the quality of products but also the production process and labor relations. Contractors must have enough capacity to be able to fulfill orders that can range from small acquisitions to massive purchases. Military grade products like tank munitions and howitzers also tend to be more sophisticated and require additional investment in facilities and skilled labor. Companies dealing with highly advanced equipment might also have to obtain security clearance and deal with restrictions on the use of technology, even if they developed it.

SOURCE: WWW.IBISWORLD.COM

Trade Globalization Going Global: Guns & Ammunition Manufacturing 2002-2017

Expo

rts/

Reve

nue

Expo

rts/

Reve

nue

200

150

100

50

0

200

150

100

50

0

Imports/Domestic Demand Imports/Domestic Demand0 040 4080 80120 120160 160

International trade is a major determinant of an industry’s level of globalization.

Exports offer growth opportunities for fi rms. However there are legal, economic and political risks associated with dealing in foreign countries.

Import competition can bring a greater risk for companies as foreign producers satisfy domestic demand that local fi rms would otherwise supply.

Export ExportGlobal Global

ImportLocal ImportLocal

Guns & Ammunition Manufacturing

2002

2017

Level & Trend Globalization in this industry is High and the trend is Increasing

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 26

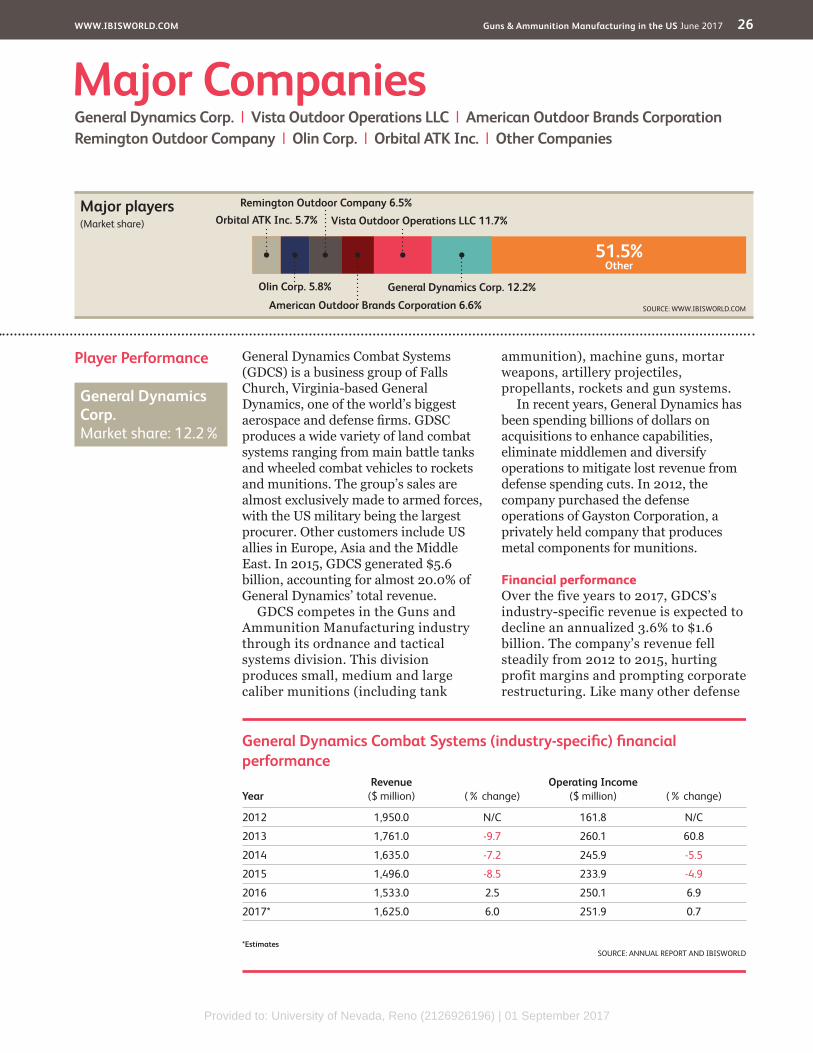

Player Performance General Dynamics Combat Systems (GDCS) is a business group of Falls Church, Virginia-based General Dynamics, one of the world’s biggest aerospace and defense firms. GDSC produces a wide variety of land combat systems ranging from main battle tanks and wheeled combat vehicles to rockets and munitions. The group’s sales are almost exclusively made to armed forces, with the US military being the largest procurer. Other customers include US allies in Europe, Asia and the Middle East. In 2015, GDCS generated $5.6 billion, accounting for almost 20.0% of General Dynamics’ total revenue.

GDCS competes in the Guns and Ammunition Manufacturing industry through its ordnance and tactical systems division. This division produces small, medium and large caliber munitions (including tank

ammunition), machine guns, mortar weapons, artillery projectiles, propellants, rockets and gun systems.

In recent years, General Dynamics has been spending billions of dollars on acquisitions to enhance capabilities, eliminate middlemen and diversify operations to mitigate lost revenue from defense spending cuts. In 2012, the company purchased the defense operations of Gayston Corporation, a privately held company that produces metal components for munitions.

Financial performanceOver the five years to 2017, GDCS’s industry-specific revenue is expected to decline an annualized 3.6% to $1.6 billion. The company’s revenue fell steadily from 2012 to 2015, hurting profit margins and prompting corporate restructuring. Like many other defense

Major CompaniesGeneral Dynamics Corp. | Vista Outdoor Operations LLC | American Outdoor Brands Corporation Remington Outdoor Company | Olin Corp. | Orbital ATK Inc. | Other Companies

51.5%Other

General Dynamics Corp. 12.2%

Vista Outdoor Operations LLC 11.7%

American Outdoor Brands Corporation 6.6%

Remington Outdoor Company 6.5%

Olin Corp. 5.8%

Orbital ATK Inc. 5.7%

SOURCE: WWW.IBISWORLD.COM

Major players(Market share)

General Dynamics Combat Systems (industry-specifi c) fi nancial performance

YearRevenue

($ million) (% change)Operating Income

($ million) (% change)

2012 1,950.0 N/C 161.8 N/C

2013 1,761.0 -9.7 260.1 60.8

2014 1,635.0 -7.2 245.9 -5.5

2015 1,496.0 -8.5 233.9 -4.9

2016 1,533.0 2.5 250.1 6.9

2017* 1,625.0 6.0 251.9 0.7

*Estimates SOURCE: ANNUAL REPORT AND IBISWORLD

General Dynamics Corp. Market share: 12.2%

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 27

Major Companies

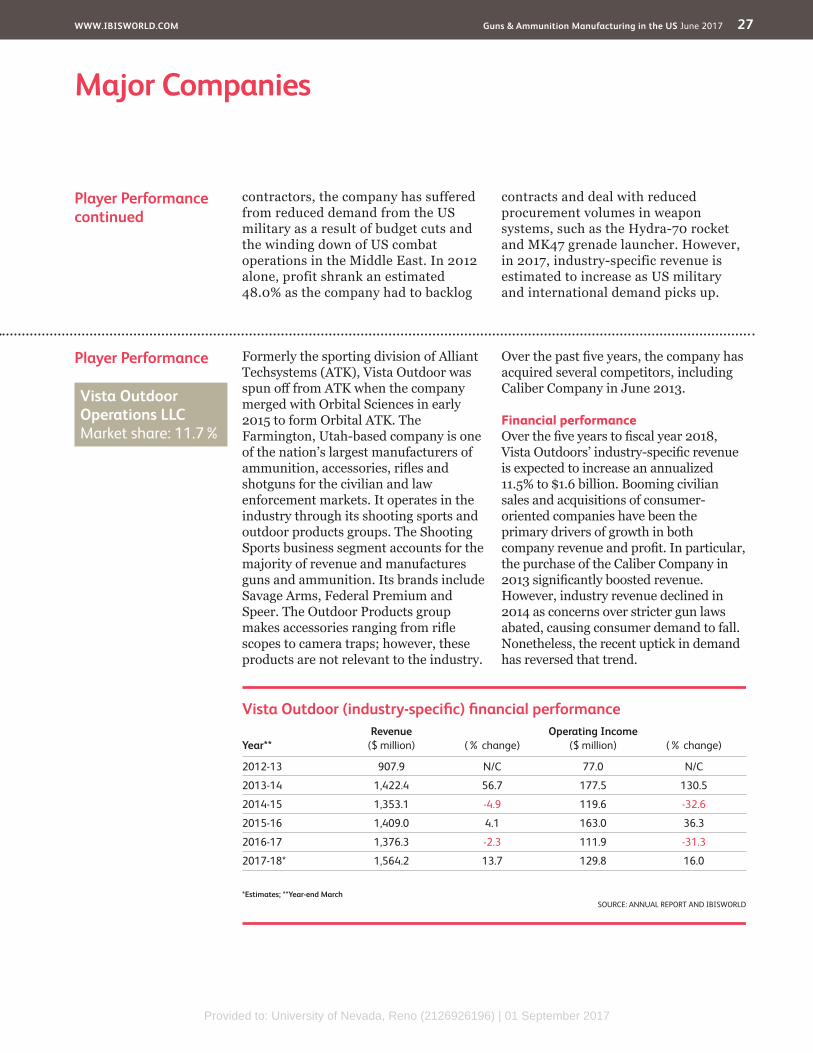

Player Performance Formerly the sporting division of Alliant Techsystems (ATK), Vista Outdoor was spun off from ATK when the company merged with Orbital Sciences in early 2015 to form Orbital ATK. The Farmington, Utah-based company is one of the nation’s largest manufacturers of ammunition, accessories, rifles and shotguns for the civilian and law enforcement markets. It operates in the industry through its shooting sports and outdoor products groups. The Shooting Sports business segment accounts for the majority of revenue and manufactures guns and ammunition. Its brands include Savage Arms, Federal Premium and Speer. The Outdoor Products group makes accessories ranging from rifle scopes to camera traps; however, these products are not relevant to the industry.

Over the past five years, the company has acquired several competitors, including Caliber Company in June 2013.

Financial performanceOver the five years to fiscal year 2018, Vista Outdoors’ industry-specific revenue is expected to increase an annualized 11.5% to $1.6 billion. Booming civilian sales and acquisitions of consumer-oriented companies have been the primary drivers of growth in both company revenue and profit. In particular, the purchase of the Caliber Company in 2013 significantly boosted revenue. However, industry revenue declined in 2014 as concerns over stricter gun laws abated, causing consumer demand to fall. Nonetheless, the recent uptick in demand has reversed that trend.

Player Performancecontinued

contractors, the company has suffered from reduced demand from the US military as a result of budget cuts and the winding down of US combat operations in the Middle East. In 2012 alone, profit shrank an estimated 48.0% as the company had to backlog

contracts and deal with reduced procurement volumes in weapon systems, such as the Hydra-70 rocket and MK47 grenade launcher. However, in 2017, industry-specific revenue is estimated to increase as US military and international demand picks up.

Vista Outdoor (industry-specifi c) fi nancial performance

Year**Revenue

($ million) (% change)Operating Income

($ million) (% change)

2012-13 907.9 N/C 77.0 N/C

2013-14 1,422.4 56.7 177.5 130.5

2014-15 1,353.1 -4.9 119.6 -32.6

2015-16 1,409.0 4.1 163.0 36.3

2016-17 1,376.3 -2.3 111.9 -31.3

2017-18* 1,564.2 13.7 129.8 16.0

*Estimates; **Year-end March SOURCE: ANNUAL REPORT AND IBISWORLD

Vista Outdoor Operations LLC Market share: 11.7%

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 28

Major Companies

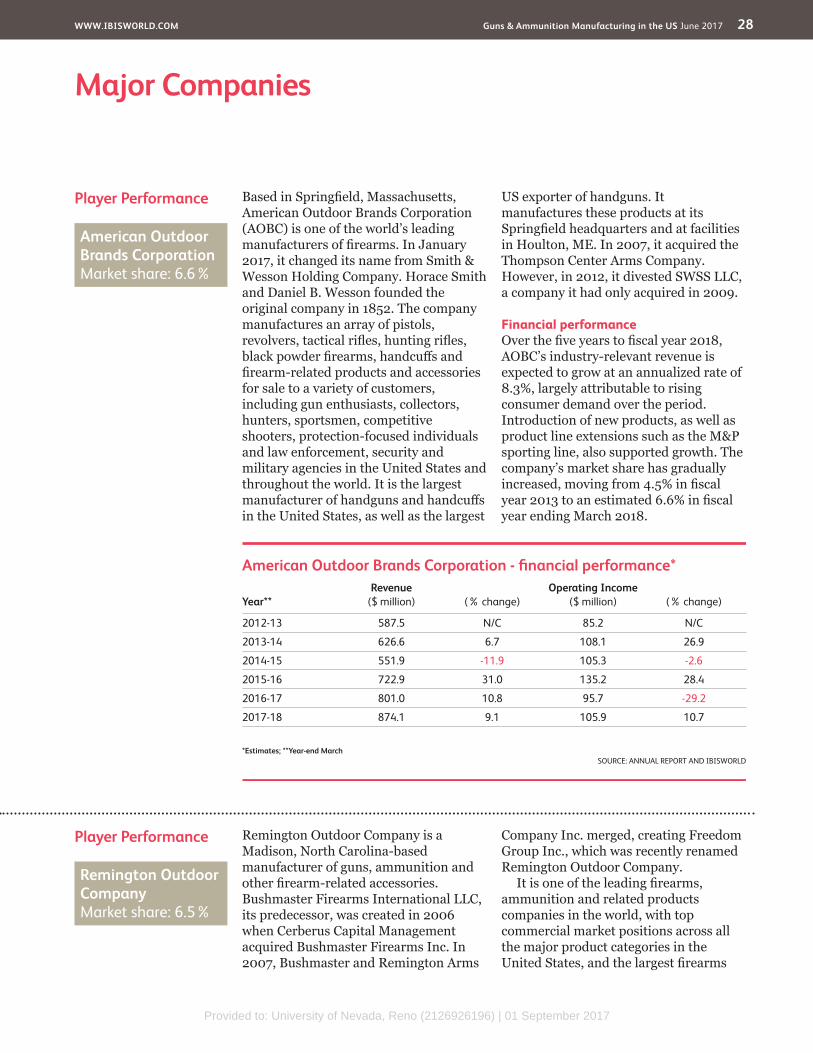

Player Performance Remington Outdoor Company is a Madison, North Carolina-based manufacturer of guns, ammunition and other firearm-related accessories. Bushmaster Firearms International LLC, its predecessor, was created in 2006 when Cerberus Capital Management acquired Bushmaster Firearms Inc. In 2007, Bushmaster and Remington Arms

Company Inc. merged, creating Freedom Group Inc., which was recently renamed Remington Outdoor Company.

It is one of the leading firearms, ammunition and related products companies in the world, with top commercial market positions across all the major product categories in the United States, and the largest firearms

Player Performance Based in Springfield, Massachusetts, American Outdoor Brands Corporation (AOBC) is one of the world’s leading manufacturers of firearms. In January 2017, it changed its name from Smith & Wesson Holding Company. Horace Smith and Daniel B. Wesson founded the original company in 1852. The company manufactures an array of pistols, revolvers, tactical rifles, hunting rifles, black powder firearms, handcuffs and firearm-related products and accessories for sale to a variety of customers, including gun enthusiasts, collectors, hunters, sportsmen, competitive shooters, protection-focused individuals and law enforcement, security and military agencies in the United States and throughout the world. It is the largest manufacturer of handguns and handcuffs in the United States, as well as the largest

US exporter of handguns. It manufactures these products at its Springfield headquarters and at facilities in Houlton, ME. In 2007, it acquired the Thompson Center Arms Company. However, in 2012, it divested SWSS LLC, a company it had only acquired in 2009.

Financial performanceOver the five years to fiscal year 2018, AOBC’s industry-relevant revenue is expected to grow at an annualized rate of 8.3%, largely attributable to rising consumer demand over the period. Introduction of new products, as well as product line extensions such as the M&P sporting line, also supported growth. The company’s market share has gradually increased, moving from 4.5% in fiscal year 2013 to an estimated 6.6% in fiscal year ending March 2018.

American Outdoor Brands Corporation - fi nancial performance*

Year**Revenue

($ million) (% change)Operating Income

($ million) (% change)

2012-13 587.5 N/C 85.2 N/C

2013-14 626.6 6.7 108.1 26.9

2014-15 551.9 -11.9 105.3 -2.6

2015-16 722.9 31.0 135.2 28.4

2016-17 801.0 10.8 95.7 -29.2

2017-18 874.1 9.1 105.9 10.7

*Estimates; **Year-end March SOURCE: ANNUAL REPORT AND IBISWORLD

American Outdoor Brands Corporation Market share: 6.6%

Remington Outdoor Company Market share: 6.5%

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 29

Major Companies

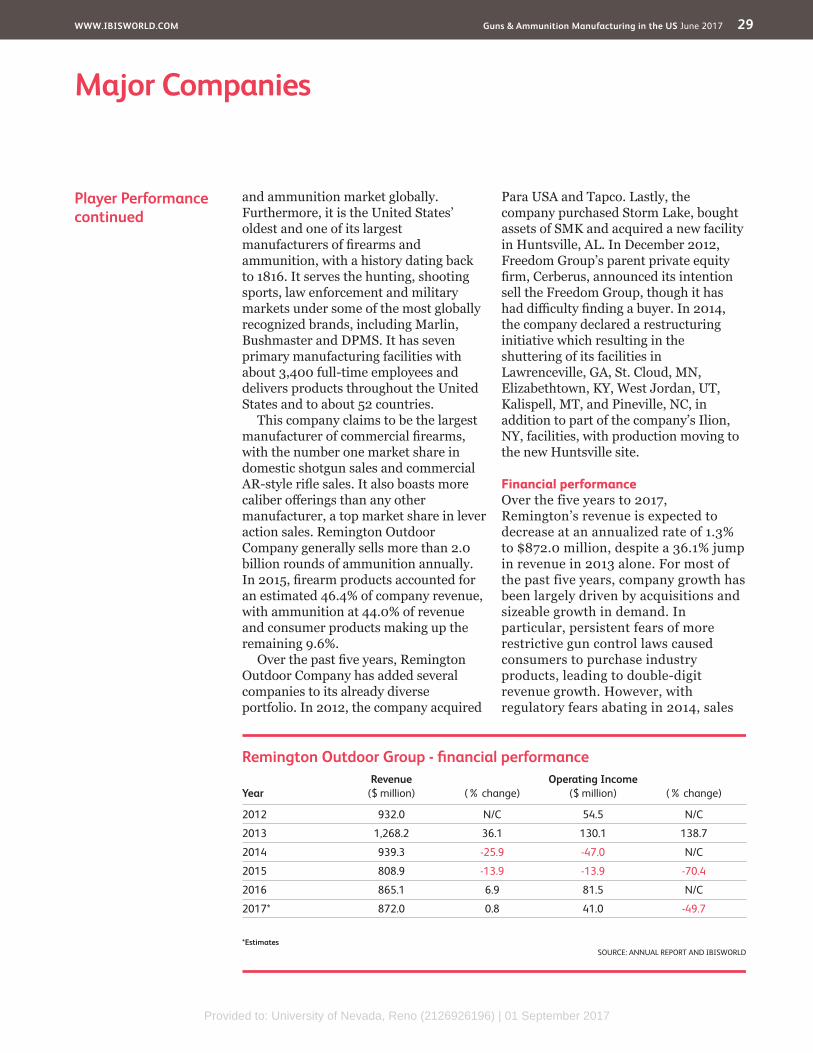

Player Performancecontinued

and ammunition market globally. Furthermore, it is the United States’ oldest and one of its largest manufacturers of firearms and ammunition, with a history dating back to 1816. It serves the hunting, shooting sports, law enforcement and military markets under some of the most globally recognized brands, including Marlin, Bushmaster and DPMS. It has seven primary manufacturing facilities with about 3,400 full-time employees and delivers products throughout the United States and to about 52 countries.

This company claims to be the largest manufacturer of commercial firearms, with the number one market share in domestic shotgun sales and commercial AR-style rifle sales. It also boasts more caliber offerings than any other manufacturer, a top market share in lever action sales. Remington Outdoor Company generally sells more than 2.0 billion rounds of ammunition annually. In 2015, firearm products accounted for an estimated 46.4% of company revenue, with ammunition at 44.0% of revenue and consumer products making up the remaining 9.6%.

Over the past five years, Remington Outdoor Company has added several companies to its already diverse portfolio. In 2012, the company acquired

Para USA and Tapco. Lastly, the company purchased Storm Lake, bought assets of SMK and acquired a new facility in Huntsville, AL. In December 2012, Freedom Group’s parent private equity firm, Cerberus, announced its intention sell the Freedom Group, though it has had difficulty finding a buyer. In 2014, the company declared a restructuring initiative which resulting in the shuttering of its facilities in Lawrenceville, GA, St. Cloud, MN, Elizabethtown, KY, West Jordan, UT, Kalispell, MT, and Pineville, NC, in addition to part of the company’s Ilion, NY, facilities, with production moving to the new Huntsville site.

Financial performanceOver the five years to 2017, Remington’s revenue is expected to decrease at an annualized rate of 1.3% to $872.0 million, despite a 36.1% jump in revenue in 2013 alone. For most of the past five years, company growth has been largely driven by acquisitions and sizeable growth in demand. In particular, persistent fears of more restrictive gun control laws caused consumers to purchase industry products, leading to double-digit revenue growth. However, with regulatory fears abating in 2014, sales

Remington Outdoor Group - fi nancial performance

YearRevenue

($ million) (% change)Operating Income

($ million) (% change)

2012 932.0 N/C 54.5 N/C

2013 1,268.2 36.1 130.1 138.7

2014 939.3 -25.9 -47.0 N/C

2015 808.9 -13.9 -13.9 -70.4

2016 865.1 6.9 81.5 N/C

2017* 872.0 0.8 41.0 -49.7

*Estimates SOURCE: ANNUAL REPORT AND IBISWORLD

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 30

Major Companies

Player Performance Clayton, Missouri-based Olin Corp. is a major chemicals and munitions company. Started in 1892, the company employs about 6,200 people and operates through three divisions. Olin Chlor Alkali Products and Vinyls produces and distributes chlorine and caustic soda, hydrochloric acid, hydrogen, bleach products and potassium hydroxide. The epoxy division manufactures epoxy resins, curing agents and intermediates. Finally, the Winchester division produces sporting ammunition, related components and small caliber military ammunition. In 2015, the company generated $2.9 billion in worldwide revenue.

Financial performanceThe company’s industry-specific operations are conducted exclusively

through its Winchester division, which accounts for about a quarter of the company’s total sales. Winchester is more than 148 years old and is a leading producer of ammunition for the recreational shooter, hunter, law enforcement and military markets. The division operates two facilities in the United States and one in Australia. In 2010, the company announced plans to relocate the Winchester centerfire pistol and rifle ammunition manufacturing operations from East Alton, IL, to Oxford, MS. This relocation was completed in 2014. Olin’s industry-relevant revenue grew at an annualized rate of 6.5% over the period to an estimated $771.4 million in 2017.

Player Performancecontinued

fell 25.9% in 2014, with more declines in 2015. Revenue growth returned in 2016 and 2017 as the recent surge in consumer demand drives sales.

Olin Corp. (industry-specifi c) fi nancial performance

YearRevenue

($ million) (% change)Operating Income

($ million) (% change)

2012 562.0 N/C 50.2 N/C

2013 707.6 25.9 130.3 159.6

2014 671.9 -5.0 115.8 -11.1

2015 647.4 -3.6 105.2 -9.2

2016 663.7 2.5 110.0 4.6

2017* 771.4 16.2 102.3 -7.0

*Estimates SOURCE: ANNUAL REPORT AND IBISWORLD

Olin Corp. Market share: 5.8%

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 31

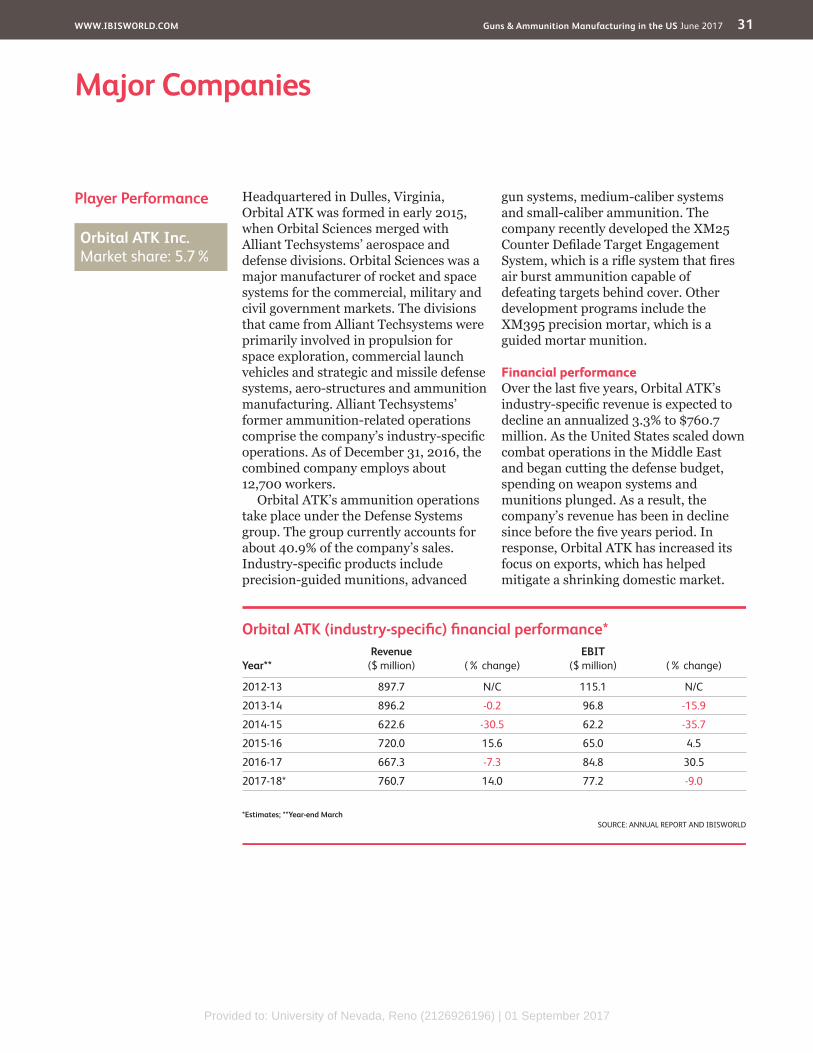

Major Companies

Orbital ATK (industry-specifi c) fi nancial performance*

Year**Revenue

($ million) (% change)EBIT

($ million) (% change)

2012-13 897.7 N/C 115.1 N/C

2013-14 896.2 -0.2 96.8 -15.9

2014-15 622.6 -30.5 62.2 -35.7

2015-16 720.0 15.6 65.0 4.5

2016-17 667.3 -7.3 84.8 30.5

2017-18* 760.7 14.0 77.2 -9.0

*Estimates; **Year-end March SOURCE: ANNUAL REPORT AND IBISWORLD

Player Performance Headquartered in Dulles, Virginia, Orbital ATK was formed in early 2015, when Orbital Sciences merged with Alliant Techsystems’ aerospace and defense divisions. Orbital Sciences was a major manufacturer of rocket and space systems for the commercial, military and civil government markets. The divisions that came from Alliant Techsystems were primarily involved in propulsion for space exploration, commercial launch vehicles and strategic and missile defense systems, aero-structures and ammunition manufacturing. Alliant Techsystems’ former ammunition-related operations comprise the company’s industry-specific operations. As of December 31, 2016, the combined company employs about 12,700 workers.

Orbital ATK’s ammunition operations take place under the Defense Systems group. The group currently accounts for about 40.9% of the company’s sales. Industry-specific products include precision-guided munitions, advanced

gun systems, medium-caliber systems and small-caliber ammunition. The company recently developed the XM25 Counter Defilade Target Engagement System, which is a rifle system that fires air burst ammunition capable of defeating targets behind cover. Other development programs include the XM395 precision mortar, which is a guided mortar munition.

Financial performanceOver the last five years, Orbital ATK’s industry-specific revenue is expected to decline an annualized 3.3% to $760.7 million. As the United States scaled down combat operations in the Middle East and began cutting the defense budget, spending on weapon systems and munitions plunged. As a result, the company’s revenue has been in decline since before the five years period. In response, Orbital ATK has increased its focus on exports, which has helped mitigate a shrinking domestic market.

Orbital ATK Inc. Market share: 5.7%

Provided to: University of Nevada, Reno (2126926196) | 01 September 2017

WWW.IBISWORLD.COM Guns & Ammunition Manufacturing in the US June 2017 32

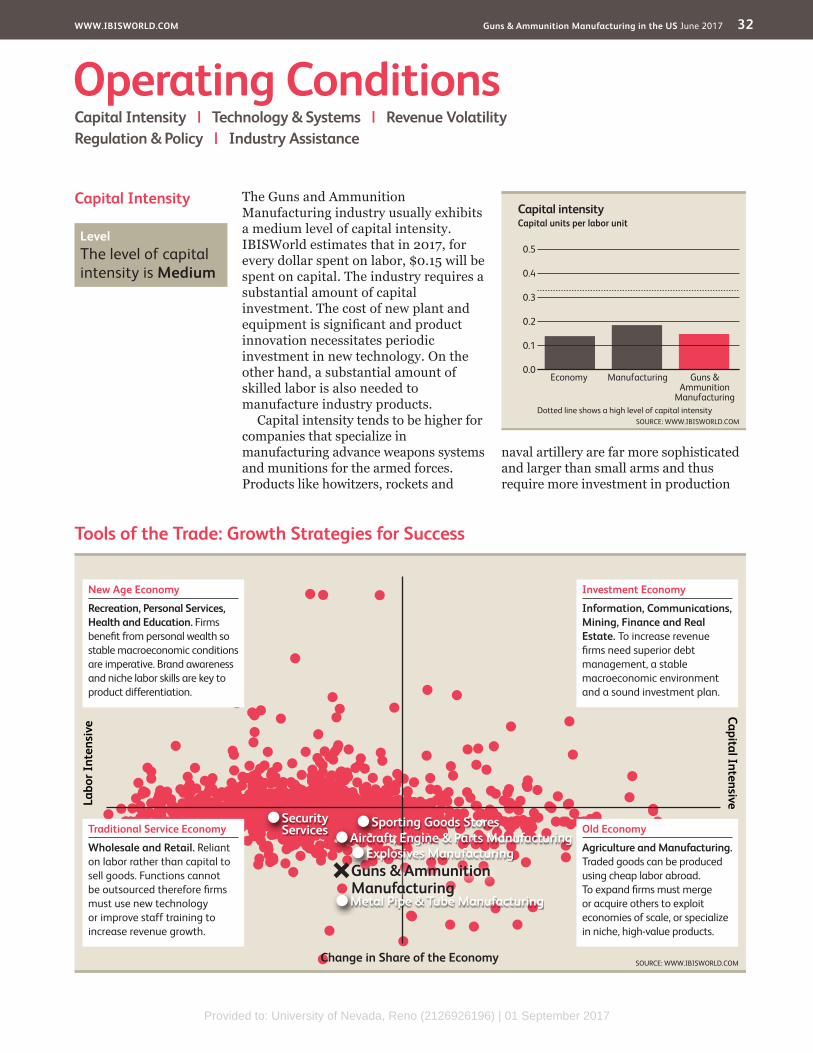

Capital Intensity The Guns and Ammunition Manufacturing industry usually exhibits a medium level of capital intensity. IBISWorld estimates that in 2017, for every dollar spent on labor, $0.15 will be spent on capital. The industry requires a substantial amount of capital investment. The cost of new plant and equipment is significant and product innovation necessitates periodic investment in new technology. On the other hand, a substantial amount of skilled labor is also needed to manufacture industry products.

Capital intensity tends to be higher for companies that specialize in manufacturing advance weapons systems and munitions for the armed forces. Products like howitzers, rockets and

naval artillery are far more sophisticated and larger than small arms and thus require more investment in production

Operating ConditionsCapital Intensity | Technology & Systems | Revenue VolatilityRegulation & Policy | Industry Assistance

Tools of the Trade: Growth Strategies for Success

SOURCE: WWW.IBISWORLD.COM

Labo

r Int

ensi

veCapital Intensive

Change in Share of the Economy

New Age Economy

Recreation, Personal Services, Health and Education. Firms benefi t from personal wealth so stable macroeconomic conditions are imperative. Brand awareness and niche labor skills are key to product differentiation.

Traditional Service Economy

Wholesale and Retail. Reliant on labor rather than capital to sell goods. Functions cannot be outsourced therefore fi rms must use new technology or improve staff training to increase revenue growth.

Old Economy

Agriculture and Manufacturing. Traded goods can be produced using cheap labor abroad. To expand fi rms must merge or acquire others to exploit economies of scale, or specialize in niche, high-value products.

Investment Economy