h floor, gst bhavan, nr. polytechnic, ambavadi, …

TRANSCRIPT

~£W1 JfT<jCffi cpr Cf51 tlT<.1 [j, 2p rsn [j "cit, tt."Qt1. Ji Q l""l (II iSll (I - ~ \9cft~, \3fttt."Qt1.~ ,qlf?!2Cf5~Cf5 ~Lffi1,JiiiSllql;g) ,JiQl""l~liSllC( -~~

OFFICE OF THE PRINCIPAL COMMISSIONER OF CENTRAL GST, AHMEDABAD-SOUTH ih FLOOR, GST BHAVAN, NR. POLYTECHNIC, AMBAVADI,

AHMEDABAD-380015

~1::fTCfCft~~/ By REGISTERED POST A.D. "CfiT .ti / STC/4-114/0&AI1S-16 DIN: 20200864WSOOOOliCADB

3-1R9T ;f,t ~/Date of Order : 25-08-2020 m B ;f,t ~/Date of Issue : 25-08-2020

~ ~/Passed by:- ~ cp=rR fiiQ ,)("'UIr{" ~

SUNIL KUMAR SINGH, PRINCIPAL COMMISSIONER :rq 3lR!<T~ / Order-In-Original No. : AHM-EXCUS-001-COM-008-009-20-21 Dated 25-08- 2020

1. R-B" ~)m (ciT ~ ~ ~ \iffift ~,~ ~ Rh~1 d ~ ~ ~ f.f:~ ~ eft \iffift ~I This copy is granted free of charge for private use of the person(s) to whom it is sent.

2. ~ 3lR!<T it ~ m m ~ ~ 3lR!<T eft mm it m liTQ" ~ ~"ffi11T ~ ,~9ycF ~ fl cwf;Z 31 qrhA £I ~ ,31 'Q 11 ~ I Cl I ~ flo cf.T ~ 3lR!<T ~ ~ 3f1:fh;r Cf,T ~ ~I 3f1:fh;r '8QI£lCfl Z~f~l( ,"ffi11T ~ ,~ ~ ~ flCllcf,J W:fl41£l ~ ,0-20, i4'Cl1 oA"PIZ ,r<J ~ 'Q1f\:flG~1 CfllOq 1\3'-6 ,3i'Ql1~ICl I~ 016 380-cf.T ~$1 ~ ~I Any person deeming himself aggrieved by this Order may appeal against this Order to the Customs, Excise and Service Tax Appellate Tribunal, Ahmedabad Bench within three months from the date of its communication. The appeal must be addressed to the Assistant Registrar, Customs, Excise and Service Tax Appellate Tribunal, 0-20, Meghani Nagar, Mental Hospital Compound, Ahmedabad-380 016.

3. ~ 3f1:fh;r ~ B" .~.~ 3.it ~ eft 0lT'""fT ~I ~ ~ ~ 9p) ~ ( H £ll1l q ffi 2001,~ f.nn:t 3 ~:zq f.nn:t (2) it Rl H Re ~ Rvii "[Tn ~e{T ~ ~I j-i=f,

3f1:fh;r ciT 'i'fR mm it ~ I ru ~ m-r ~ ~m Rl1 3lRQT ~ ~ 3f1:fh;r eft 'li ~ ,~ m ~ tr ~ ~ efT~) mit Cfi11 if Cfi11 ~ ~ ~l1lfiJld ~ ~(I ~ if ~~m~fdl~\J1 m'i'fR~it~~m~1 The Appeal should be filed in Form No. E.AJ. It shall be signed by the persons specified in sub-rule (2) of Rule 3 of the Central Excise (Appeals) Rules, 2001. It shall be filed in quadruplicate and shall be accompanied by an equal number of copies of the order appealed against (one of which at least shall be certified copy). All supporting documents of the appeal should be forwarded in quadruplicate .

.4 ~~~?.-mCfiT Rlq{OI ~ ~~ 3lT~9~~ ,'i'fR~it~lru~ efT~~m ~m?_"f~3lRQT~~~efT'li~,~m~tr~~efT~ )m if Cfi11 if Cfi11 ~ ~ 111 fiJI d ~ ~(I The Appeal including the statement of facts and the grounds of appeal shall be filed in quadruplicate and shall be accompanied by an equal number of copies of the order appealed against (one of which at least shall be a certified copy.)

.5 ~CfiTm~2{~~it~~~~~fcf;ID"dCf; 31~ RlClJ.UI ~ffiT ~~~~mQfTqT~~~~~~Ttir~cf.T#,'l1lj;gIJ #"qif?t,('j ~~I The form of appeal shall be in English or Hindi and should be set forth concisely and under distinct heads of the grounds of appeals without any argument or narrative and such grounds should be numbered consecutively.

Brief facts of the case

M/s Shiv Carriers situated at 323, Vanijya Bhawan, Kankaria Road, Ahmedabad (hereinafter referred to as the assessee) is a coastal freight forwarding firm engaged in doing business of more than 500 containers per month in West Coastal Region and through Railways. The firm has got itself registered under Goods Transport Agency (GT A) bearing registration No. ACZPC0823EST003 issued by Service tax, Ahmedabad dated 18.8.2005.

2. Intelligence was gathered that the assessee is providing service of delivery of cargo from the place of Consignor in Gujarat to the place of Consignee anywhere in India (i.e Customers) under a composite scheme and charging for the same from its Customers, but is not discharging its Service Tax liability properly. To evade payment of Service Tax, the firm splits the whole transaction into three parts i.e. from the place of Consignor to Port/Rail yard by road. from Port/railways in Gujarat to Cochin Portslrail yard anywhere in India by sea/rail route & from there to the place of Consignee by road. If the firm had been registered under "Cargo Handling Services", no abatement would have been admissible and the whole of transaction from Consignor to Consignee would be covered under the taxable service.

2.1 For ease of comprehension, an Executive Summary of the investigations is given below:

(i) The assessee is providing service of delivery of cargo from the place of Consignor in Gujarat to the place of Consignee anywhere in India (i.e. Customers) under a composite scheme and charging for the same from its Customers, but are not discharging its Service Tax liability.

(ii) The services being provided by the assessee includes:

);> arranging for vehicles/containers from the nearest Port to the place of consignor;

);> loading of goods at the place of Consignor in Gujarat by them;

);> transportation of containerized cargo to Port/railway yard, Gujarat;

» unloading of containerized cargo at Port/railway yard;

);> handling of containerized cargo at Port/railway yard including payment of vanous port/rail charges;

);> loading of containerized cargo in coastal vessel/rail by Shipping/railway Companies on behalf of the assessee;

);> transportation of containerized cargo by sea/rail route by Shipping Companies Irailways on behalf of the assessee;

);> unloading & handling of containerized cargo at Port/ Railway yard Shipping Companies/Railways on behalf of the assessee;

);> transportation of containerized cargo from Port/railway yard to the place of Consignee; and

);> delivery of empty containers to the Shipping Companies after the goods are unloaded at the place of the Consignee

(iii) The assessee provides service of delivery of cargo to its customers till the destination by taking the services of various other intermediaries like Shipping Companies and Railways, Lorry Providers (GT A), etc.

(iv) The Rate Contracts recovered during the Search and produced by the Proprietor in his Statement dated 12.10.2015 reveals that the assessee has the composite rate contract with each of their clients for delivery of cargo from the Consignor's place in Gujarat to the place of Consignee anywhere in India through Rail/Sea & Road for which they are charging the freight per ton of the cargo consigned in the lumpsum manner.

3

Q. 8 Who is responsible for loading of containerized cargo In coastal "esse Is at Port and

Railway Yard?

unloaded at yard/port from where the goods are carried on by railways to the various destinations such as Patna, Kolkatta, Hyderobad. Bengaluru. Raipur and Kanpur. By sea route the goods are consigned for the destination of Cochin only. Thereafter, we again take the delivery of goods at the destined Railway station/yard or unload port from where the goods are transported to the place of consignee as undertook or entrusted to us. We are as transporter responsible for taking the delivery of goods from the Consignors place to the Consignee's place as per mutual agreement.

Q.4 Who is responsible for arrangement (~florries/trucksfor loading of goods at the place of

Consignor?

A. Myfirm is responsible for arrangement of lorries to the place of Consignor.

Q.5 Who is responsible for loading of goods at the place of Consignor

A. Consignor undertakes the responsibility for loading oj'goods.

Q.6 Who is responsible for offloading of containerized cargo at Kandlain'illncira Port

or at Railway yard?

A. My firm approaches the surveyors of Shipping Companies which undertake the responsibility of ojjloading the containerized cargo at load port and my firm is responsible for off-loading the goods at the railway yard

Q. 7 Who is responsible for looking after the containerized cargo at Port or at Railway

yard?

A. Shipping Companies and Railways are responsible for looking after the containerized cargo once the goods are handed over to them.

5

A. Shipping Companies and Railways are responsible for loading of containerized cargo in coastal vessels and in Rail.

Q. 9 Who is responsible for movement of containerized cargo from. Port and Railway yard to the discharge Port/yard at the destination point?

A. Shipping Companies and Railways are responsible for movement of containerized cargo from Port and Railway yard to the discharge Port/station.

Q. 10 Who is responsible for offloading of containerized cargo at discharge Port/Railway

station?

A. Shipping Companies arid Railways are responsible for offloading of containerized cargo at discharge Port and at destined railway yard/station.

Q.II Who is responsible for looking after the containerized cargo at discharge

Port/Railways?

AiShipping Companies and Railways are responsible for looking after the containerized cargo at discharge Port/Railway yard.

Q.12 Who is responsible for loading of containerized cargo on lorries/trucks at discharge

Port/Rail yard?

A. Generally, Shipping Companies and Railways undertake the responsibility of loading of containerized cargo on lorries/trucks at discharge Port/Rail yard.

Q.13 Who is responsible for providing of lorries/trucks for further transportation of goods at unload port, and Rail yard?

A. No sir, our business does not, include loading, packing or unpacking of cargo. We have taken services of other intermediaries such as Railways & Shipping Companies and we perform the activity of road transportation only. We also issue lorry receipts.

Q. 19 In response to the questions asked today, you have asserted that the work carried upon by you is nothing but, CTA. The definition ofGTA as provided in the Finance Act, 1994 reads as

follows: "Goods Transport Agency" means any person "who provides service in relation to transport of goods by road and issues consignment note, by whatever name called. Going through the aforesaid definition of GTA, it is more than clear that GTA covers only transportation through road and not by any other means like sea/rail, which means that your assertions are not at all supported by facts and legal position. What do you want say in this regard?

A. Sir, our activity is GTA only and as GTA, our firm is regularly issuing Lorry Receipts/Consignment Note.

Q. 20 Please provide the manner & method of quoting rates to your Customers.

A . Generally, our firm quote rates to the Customers through telephonic conversation, on firm'S letter pad, in some cases, our firm quote rates through e-mails also. 1 produce such correspondence mail, letters onfirm's letter head, etc marked as Exh-1 containing page nos. 1 to 201 which are our sample copies agreements with consignors/consignees for whom we have undertaken transportation work on cornposite manner of Road-Rail-Road and Road Sea-Road, duly signed by me. It contains the composite rate of transportation made by Shiv Carriers through road first, then by rail or sea and again by road. However. in our bills issued to our customers 'we have made (I single hill showing separately road transport and sea/rail transport. The rates are quoted either in full or per tonnage to the Customers depending upon the work desired by them. The door to door delivery charges quoted under composite rate contract are also contained in the seized file no. A/25 from my premises on 14.8.2015 under the panchnama. In token of having seen/lie A/25 today, I sign the first and last page of the same.

Q. 21 As per your above statement you have admitted that yourfirm has raised Bills/Invoices in the name of your Customers for the entire service from the place of Consignor at Gujarat to the place of Consignee anywhere in India. Please provide the details of gross income/amount of composite services provided to your customers for the lastfive years.

A. Sir, the details regarding composite payments received from our customers i. e. Consignor/Consignee for the ensuring delivery oj'goods from the place of Consignor in Gujarat to the place of Consignee anywhere in India is as follows.

(i) (ii) (iii) (iv) (v)

2010-11 (from 1110/2010 to 31/3/2011): 2011-12: 2012-13: 2013-14: 2014-15:

Rs. 220-156460/ Rs. 352379487/ Rs. 262761714/ Rs. 178697702/ Rs. 208130812/-

Thus, the total payment receivedfrom the customers i.e. Consignor/Consignee towards providing of composite service comes out to be Rs.1223326175/- (approximately) from 2010-11(Oct-10 onwards) to 2014-15.

Q.22 Whether you have shown any income through transportation by road or under composite services of Road-sea/rail-road in the ST 3 returns filed by you? Are you availing any cenvat credit on inputs or input services?

A. No 'we have not shown any type of income/receipts in the ST 3 returns [il ed by Shiv Carriers and have also not availed any type of cenvat credit. We have till date regularly filed NIL returns only.

3.3 The Statement of the Proprietor of the assessee dated 12.10.2015 reveals that services being provided by the assessee includes arranging for vehicles/containers from the nearest Port/Rail Yard

7

5.2 It appeared that due Service Tax is not being paid on movement of goods by the aforesaid the assessee. Since, it is the assessee which undertakes the responsibility of delivery of goods from Consignor to Consignee, it is the assessee which is providing the services, maybe with the help of other Service Providers, but, taking of services from other Service Providers does not alter the nature of services being provided by the assessee to its Customers. Moreover, the assessee is getting composite payment for ensuring delivery of goods from the place of Consignor in Gujarat to the place of Consignee (i.e. Customers).

5.3 The assessee appeared to have not paid the service tax on the above composite services viz. Cargo Handling Service and accordingly, they have wilfully suppressed the fact of providing said taxable services and its taxable value by not correctly filing periodical ST-3 returns with an ulterior motive to defraud the Government Revenue. Even from the perusal of ST -3 Returns filed by the assessee from the period 2010-11 to 2014-15, it transpires that till date they have filed all NIL returns and have not shown any income or receipts under any category of service. They failed to show the correct gross receipt of taxable services provided in the ST -3 Returns which appears to have been done with the intent to evade payment of Service Tax. Thus, the assessee has wilfully suppressed the above facts with intent to evade payment of Service Tax leviable thereon and as such it appears that the extended period specified in the proviso to subsection (1) of Section 73 of the Finance Act, 1994 is invokable to demand & recover the Service Tax due from them.

6. It is claimed by the assessee, they are acting as "Goods Transport Agency" but they failed to take into cognizance that as per the definition laid down under Sec. 65(50b) of the Finance Act, 1994, to fall under "GTA", the service provided by goods carriage should be in relation to transportation of goods by road [emphasis supplied) and not by any other means. In case of the assessee, there are a number of services involved including transportation by coastal waterways/railways and so, going by the provisions regarding "GT A" as contained in Sec. 65 (50b) of the FA, 1994 as well as Rule 4A & 4B of the Service Tax Rules, 1994. the services provided by the assessee may not fall under the category "GTA".

6.1 Another argument put forth in its support by the assessee is that as GT A it is issuing "Consignment Note/Lorry Receipt". In this regard, it is to be noted that the document issued by the assessee show the place of origin as HimatnagariSanand/Bhavnagar and the place of destination as Cochin, Kolkatta, Patna,etc or. any other place anywhere in India but, that may not be considered as "Consignment Note" for the purposes of Sec. 65 (50b) of the Finance Act, 1994 as well as Rule 4A & 48 of the Service Tax Rules, 1994. 1994 for the simple reason that transportation of goods from Morbi, Himmatnagar, Bhavnagar, Ahmedabad.etc or any other place in India to Cochin, Kolk atta, Patna, etc or any other place in India cannot be done merely through road by the assessee and issuance of Consignment Note is a condition attached with the primary condition of transportation of goods by road [emphasis supplied} as is evident from the Consignment Note No. 71119 dated 26.07.2012 (shown below as sample) wherein the place of origin is shown as Himmatnagar and the place of destination is shown as Cochin which makes it amply clear that the transportation of goods has not been done merely by road, so as to make the assessee eligible to fall under "GT A". t:t;k, ,::"- .. :;-:"".': ~., ":. :":""

_ i"~~,,,"~~t~J!,~~rs~~~~"!"A,,' , . _ \,'.' <"/'i:'.~'~':':""'!'::':C:'!:::.:' I~n', ,±:td::'-~l~~'1~!:' ~~i~~d~~{;:~t~~ ..• 0:~)\~A1·;·'~J~ ~', .. ~ _, I ' , ,--, ,'_, '." ;-" -'-, " f:t( - - lr,,·~i~'f ,,';- -"-;; :-: - i .' ~ '~.' ';'," .: /l_~~f(~J;;;;~v·~/I~::f.l:. ~'d/: I •• A'" U.de~J~ (';.',fI());}IJ,:1{'~'.}.cl_" :~."~'" J'~'!~' j«~~ I:!):·1~kt;:~l~·I-:I~1 t '. ~),.~""j.~'rt-'l.r,<"; .....•.. ";!: ~ ! : j' ) -~...:~ .~i:'" or ;~,' I

" ~ - v ~,' .~~~.:~~~~Y~if)_:~'::.;_l~::::~r !,to( 11 t:t-."S(f," ..;~~~t97t1;~1.l . ·.~i "r ,.. •• f·C"·( •• ,.n )\~~S~~,"I''..1~~r<I.\~~~1''ii'''' ~IC'.N~ !~!';;f)')~ 1~~,:;":'.~.i-;l:'1;{:t ~I'· i

~ --- _v_.~_' --'.~ • _ ' f'r' v' ;;. J :.;.o;:-::~J(I 'I .,', "'~l)(l-)'~; ~ "<~'1f~ ,,~,r .•. T,'·"f.:':~~!·'<:'-'H;:.-r·r'i"'''';<~~' '..11"'-";;-' 1 ...• 1;0,: ;':r:"l"h'J

, - -- - •. 'd'~ t -r,,,.'· -, ,.~,-.,~ ',r -:-l 'l'- .' I '::"')71..,,1.:.( - ... ·,··/~I I "r.'h~·H(·t!~r.j)~_:.. .•. I~'· , I .,} ~ r \., ,."''_' j ,'" . ~ ~ _. d" •• "'-.. ' ••.• - III 1

: ,'.- ':>. '.' >':'1 ':_" t' 'r"t"C'T-~"T'-~'~r

9

goods, with or without one or more other services like loading, unloading. unpacking, under cargo handling service. With this amendment, packing with transportation will be classifiable under cargo handling service only.

7.4 A conjoint reading of provisions of Section 65( 1 05)(zr) and 65(23) of the Finance Act, 1994 show that Cargo Handling Agencies are taxable entities. Cargo Handling Services provided by such entities attract the levy of Service Tax. Section 65(23) has a wide amplitude and has brought all like nature activities to its fold expressly and by inclusion of such like nature activities under the class 'Cargo Handling Services'. However classification of service under this category is subject to two exceptions/exclusions: viz.: (1) handling of export cargo or passenger baggage and (2) mere transportation of goods. These two activities are beyond the scope of such class from taxation for rationale behind them. Accordingly. Cargo Handling Services provided in respect of domestic cargo only are liable to be taxed. Event of levy arises when service relating to or in relation to handling of cargo is provided by a cargo handling agency irrespective of mode of transport used for movement of such cargo. Precisely, following activities which are contemplated to be taxed as cargo handling service are:

(1) By express terms: (A) Loading, unloading, packing or unpacking of cargo; (2) By inclusive terms: (B) Handling service relating to cargo: (i) Provided for freight in special containers or for non-containerized freight; (ii) Provided by a container freight terminal or, by any other freight terminal; and (3) Cargo handling service provided which is incidental to freight.

7.5 From the above it appears that necessity of law for taxation under the class "Cargo Handling Service" is that the service provided should be relating to or in relation to cargo handling by a cargo handling agency. The service provided should be integrally or inseparably connected with handling of cargo or attributable thereto without being a mere activity of transportation of such cargo since transport service independent of cargo handling is an exception under the scheme of levy by Section 65(23) of the-Act and it may be said that loading, unloading, packing or unpacking of cargo and handling of cargo for freight in special containers or non-containerized freight and service provided by container freight terminal or other freight terminal for all modes of transport are subject matter of taxation under the class "Cargo Handling Service". That apart, any activity incidental to freight of cargo is also liable to be taxed under such class. Mode of transport is irrelevant for incidence of levy once the service provided meets the test of handling of cargo in the manner as envisaged bylaw. It is also appears that it is not necessary that the cargo should only be meant for transport either by vessel in ships or aircrafts.

7.6 In view of the aforementioned facts and legal provisions. it appears that the for the period prior to 01.07.2012, the service being provided by the assessee which includes arranging for vehicles/containers, loading of goods at the place of Consignor in Gujarat by them, transportation of containerized cargo to Port/railway yard, Gujarat; unloading of containerized cargo at Port/railway yard; handling of containerized cargo at Port/railway yard including payment of various port/rail charges, loading of containerized cargo in coastal vessel by Shipping Companies/railways on behalf of them. transportation by sea/rail route. unloading & handling of containerized cargo at Port/railway yard by Shipping Companies/railways on behalf of them; transportation of containerized cargo from Port/railway yard to the place of Consignee and delivery of empty containers to the Shipping Companies after the goods are unloaded at the place of Consignee may not appear to be classified as GTA rather it may be suitably classified under "Cargo Handling Services" prior to 01.07.2012.

7.7 After 01.07,2012, the word "Service" has been defined under Section 65 B (44) of the Finance Act, 1994 which reads as under:

"service" means any activity carried out by a personfor anotherfor consideration, and includes a declared service, .

This means- any activity

II

• loading of goods at the place of Consignor in Gujarat by them; • transportation of containerized cargo to Portirailway yard;

unloading of containerized cargo at Port/railway yard; • handling of containerized cargo at Port/railway yard including payment of various

port/rail charges; • loading of containerized cargo in coastal vessel/rail by Shipping

Companies/Railways on behalf of the assessee; transportation of containerized cargo by sea/rail route by Shipping Companies/Railways on behalf of the assessee;

• unloading & handling of containerized cargo at Port/railway yard by Shipping Companies/rail ways on behalf of the assessee;

• transportation of containerized cargo from Port/railway yard to the place of Consignee; and delivery of empty containers to the Shipping Companies after the goods are unloaded at the place of Consignee.

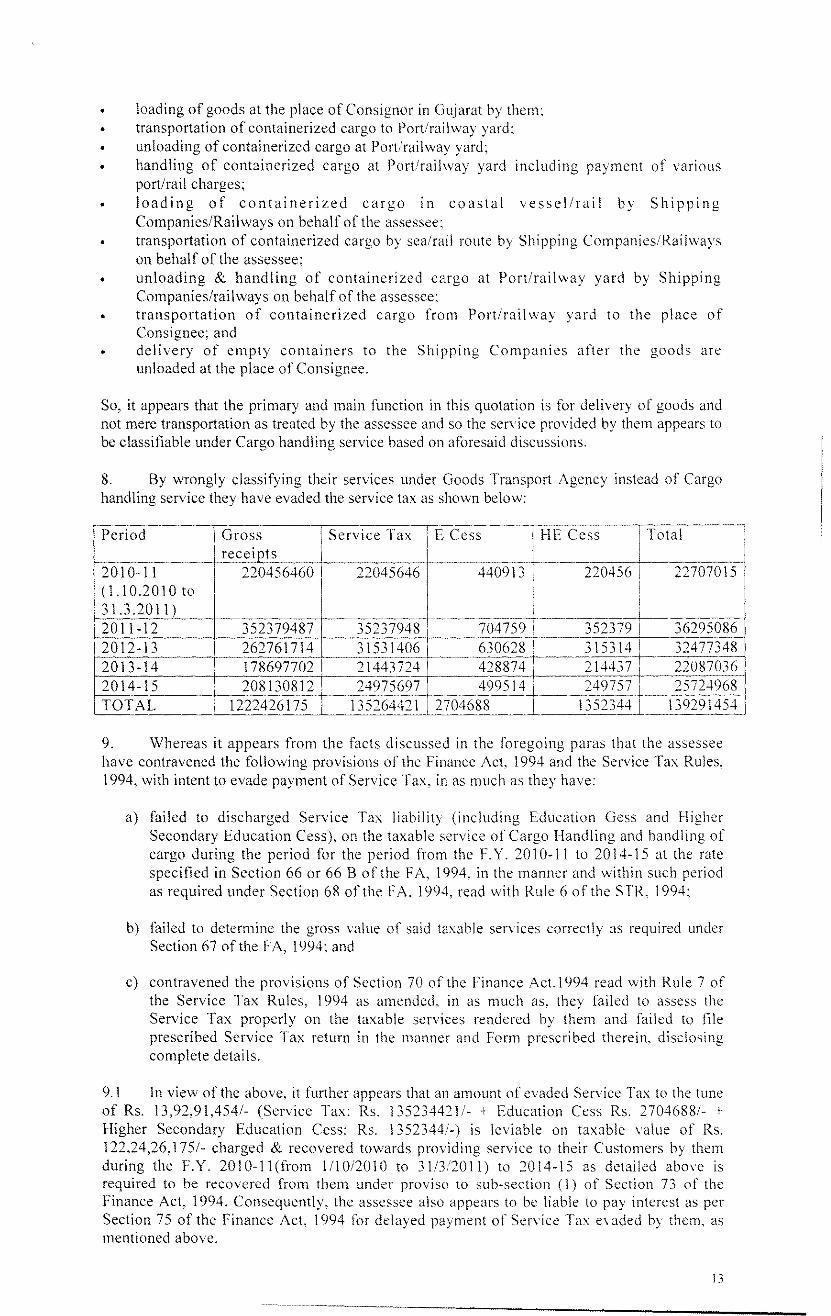

So, it appears that the primary and main function in this quotation is for delivery of goods and not mere transportation as treated by the assessee and so the service provided by them appears to be classifiable under Cargo handling service based on aforesaid discussions.

8. By wrongly classifying their services under Goods Transport Agency instead of Cargo handling service they have evaded the service tax as shown below:

Period Gross Service Tax E Cess HE Cess Total receipts

12010-11 220456460 22045646 440913 220456 22707015 I (1.10.2010 to 31.3.2011) 2011-12 352379487 35237948 704759 352379 36295086 2012-13 262761714 31531406 630628 315314 32477348 2013-14 178697702 21443724 428874 214437 22087036 2014-15 208130812 24975697 499514 249757 25724968 TOTAL 1222426175 135264421 2704688 1352344 139291454

9. Whereas it appears from the facts discussed in the foregoing paras that the assessee have contravened the following provisions of the Finance Act, 1994 and the Service Tax Rules, 1994, with intent to evade payment of Service Tax, in as much as they have:

a) failed to discharged Service Tax liability (including Education Gess and Higher Secondary Education Cess), on the taxable service of Cargo Handling and handling of cargo during the period for the period from the F. Y. 2010-11 to 2014-15 at the rate specified in Section 66 or 66 B of the FA, 1994, in the manner and within such period as required under Section 68 of the FA, 1994, read with Rule 6 of the STR, 1994;

b) failed to determine the gross value of said taxable services correctly as required under Section 67 of the FA, 1994; and

c) contravened the provisions of Section 70 of the Finance Act.1994 read with Rule 7 of the Service Tax Rules, 1994 as amended, in as much as, they failed to assess the Service Tax properly on the taxable services rendered by them and failed to file prescribed Service Tax return in the manner and Form prescribed therein, disclosing complete details.

9.1 In view of the above, it further appears that an amount of evaded Service Tax to the tune of Rs. 13,92,91,454/- (Service Tax: Rs. 135234421/- + Education Cess Rs. 2704688/- + Higher Secondary Education Cess: Rs. 1352344/-) is leviable on taxable value of Rs. 122,24,26,175/- charged & recovered towards providing service to their Customers by them during the F.Y. 2010-11(from 1110/2010 to 31/3/2011) to 2014-15 as detailed above is required to be recovered from them under proviso to sub-section (1) of Section 73 of the Finance Act, 1994. Consequently, the assessee also appears to be liable to pay interest as per Section 75 of the Finance Act, 1994 for delayed payment of Service Tax evaded by them, as mentioned above.

13

Ahmedabad South. The said show cause notice was a subsequent notice issued in terms of the provisions of Sec. 73(1 A) of the Finance Act, 1994 which reads as under:

(1 A) Notwithstanding anything contained in sub-section (J) (except the period of thirty months of serving the notice for recovery of service tax), the Central Excise Officer may serve, subsequent to any notice or notices served under that sub-section, a statement, containing the details of service tax not levied or paid or short levied or short paid or erroneously refunded for the subsequent period, on the person chargeable to service tax. then. service of such statement shall be deemed to be service of notice on such person, subject to the condition that the grounds relied upon for the subsequent period are same as are mentioned in the earlier notices

The grounds relied upon in the said show cause notice were the same as of the earlier show cause notice it was alleged that the assessee had provided Cargo Handling Service under the guise of GTA services and had not paid the service tax leviable thereon. Under the said SCN, the assessee were called upon to show cause as to why:

(i) The total amount of evaded service tax to the tune of Rs. 4,20,48,276/- (Four crores Twenty Lakhs Forty Eight Thousand Two Hundred Seventy Six only) leviable on taxable value of Rs. 29,38,51,539/- charged & recovered toward providing service to their customers by them during the Financial Year 2015-16 to June 2017 should not be demanded and recovered from them under the provision of Section 73 of the Finance Act, 1994;

(ii) Interest at the appropriate rate on delayed payment of service tax liability as mentioned at (i) above should not be demanded and recovered from them from the due date of payment of service tax evaded by them as mentioned at (i) above, under provisions of Section 75 of the Finance Act, 1994

(iii) Penalty should not be imposed upon them with intent to evade payment of service tax, as mention hereinabove, under the provision of Section 76 of the Finance Act, 1994;

(iv) Penalty should not be imposed upon them under Section 77 of the Finance Act. 1994 separately for the above mentioned contraventions;

(v) Penalty should not be imposed under Section 70 of the Finance Act, 1994 for not disclosing correct gross receipt/ income in their ST-3 returns

13. The assessee was earlier registered under the jurisdiction of the Commissioner of Service Tax, Ahmedabad. Consequent to the issue of Notfn No 12/2017 to 14/2017-Central Excise (NT), all dated 9.6.2017, appointing the Officers of various ranks as Central Excise Officers re allocating the jurisdiction of the Central Excise Officers and Trade Notice No 001/2017 dated 16.6.2017 issued by the Chief Commissioner, Central Excise & Service Tax, Ahmedabad Zone, the assessee is now registered under the jurisdiction of Commissioner, Central Goods and Services Tax, Ahmedabad (South). Further, the provisions of the repealed Central Excise Act. 1944 and amendment of the Finance Act, 1994 have been saved under Section 174(2) of the Central Goods and Services Tax Act, 2017 and therefore, the provisions of the repealed/amended Acts and Rules made thereunder enforced for the purpose of demand of duty, interest and imposition of penalty under both the above notices would be applicable to the case.

Written submission of the assessee

14. The assessee filed their written submissions under their letter dated 23.6.2020 wherein they submitted that:

);- The customer was aware at the time of giving the contract that a particular shipping line or railways had been appointed for transportation of goods by sea or rail. That the railways raised the invoice in the name of the customer and the railways/ shipping lines paid the service tax on the services.

Y They had mainly undertaken the activities of (1) Transportation of goods by road from

15

and Mis Usha Martin Industries reported at 1997 (94) EL T 460 (SC).

);;> Service tax had been paid on the entire transaction i.e. the railwayl shipping lines had paid the service tax on the activity of transportation of goods by rail! sea and the service recipient had paid the service tax on the transportation of goods by road under the reverse charge mechanism.

);;> They had complied with all the conditions specified under Rule 5(2) of the Service Tax (Determination of Value) Rules and as such the value of reimbursement expenses would be excluded from the taxable value.

);;> In terms of the principle laid down by the Supreme Court in the case of Mis Intercontinental Consultants and Technocrats P Ltd. reported at 2018 (10) GSTL 401, reimbursement of expenses was not includible in the taxable value prior to 14.5.2015.

);;> The benefit of cum-tax-va1ue had not been extended to them. They placed reliance on the case laws of Mis ABN Amro Bank reported at 2011 (23) STR 529 and Mis Prompt and Smart Security reported at 2008 (9) STR 237.

);;> The facts of the case involved revenue neutrality in as much as they would have been eligible for cenvat credit of the service tax paid by the railwayl shipping lines.

);;> The extended period of limitation was not applicable to the facts of the case since they had disclosed all the facts in their ST -3 returns. They placed reliance on the case laws of Mis Singh Brothers reported at 2009 (14) STR 552, Mis Continental Foundation Jt. Venture reported at 2007 (216) ELT 177 and Mis Tamil Nadu Housing Board reported at 1994 (74) ELT9

);;> Penalty under Sec. 78 could be imposed only when the tax was not paid by reasons of fraud, collusion or willful mis-statement or suppression of facts, or contravention of any of the provisions of law with an intent to evade tax. None of the above ingredients was present and as such penalty was not imposable. Reliance was placed on the case law of Mis DD Industries Ltd. reported at 2002 (142) EL T 256 (T)

);;> Penalty could be waived off under Section 80 of the Finance Act. 1994 in case of reasonable cause. Reliance was placed on the case laws of Mis Vinay Bele & Associates reported at 2008 (9) STR 350 and Mis Ashish Vasantrao reported at 2008 (10) STR 8

);;> Simultaneous penalty under Sec. 76 and 78 could not be imposed. Reliance was placed on the case law of Mis Raval Trading Co. reported at 2016 (42) STR 210

Record of Personal Hearing

15. Personal hearing in the matter was held on 31. 7 .2020 wherein Shri Hardik Modh, Advocate, Shri Vipul Kothari, CA and Shri Awadheshsingh S Chaudhary. Prop. of the assessee appeared and they reiterated the contentions raised under their written submissions. It was argued that they are essentially providing GT A services and not Cargo Handling Services. That since they did not undertake packing activity, the service cannot be classified as Cargo Handling Service in view of Board's clarification.

Discussion & Findings

16. I have carefully gone through the SCNs. relevant case records and the assessee's submissions, both in written and in person. The subsequent SCN F.No. STCI04-57/0A/ShivIl7- 18 dated 27.03.2018 involves the same issue i.e. proposal for classifying the service under Cargo Handling Service and demanding service tax on the same. Further the said show cause notice has been issued for the subsequent period i.e. period from April 15 to June 17 in terms of the provisions of Sec. 73(lA) of the Finance Act, 1994. As the issue in both the SCNs is same and the grounds of raising the demand is emanating from the same set of facts. I take up both the SCNs for adjudication together.

17

18.3 It is the argument of the assessee that they are issuing Consignment Note. Before. verifying the fact whether the Consignment Note has been issued or otherwise it is incumbent that the assessee should be providing services in relation to transport of goods by road. The assessee has not produced any evidence to establish that they are solely engaged in providing services in relation to transport of goods by road. At this juncture it becomes necessary to assess the actual activities undertaken by the assessee. The actual nature of activity undertaken by the assessee has been explained by Shri A wadheshsing Chaudhary. Prop. of the assessee in his statement dated 12.10.2015 at answer to question no. 1 as under:

"In Shiv Carriers we are basically doing the work of transportation of goods. In Shiv Carriers we undertake the responsibility of transportation of goodsfrom our consignor's premises to the consignee 's premises through road, sea or rail as per the destination entrusted to us."

The above version indicates that the services rendered by the assessee consists of transportation of goods by multiple methods viz. by road, sea! rail. Shri Awadheshsing Chaudhary has further elaborated the activities undertaken by them at answer to question no. 3 as under:

"We are sending empty containers by our own lorries/trucks as well as lorries owned by others also to the place of Consignor in Gujarat where the cargo gets stuffed by them, then, we arrange delivery of containerized cargo through road to the nearest port like Mundra Port/rail yard. Further. we hand over the containerized cargo to the Shipping Companies/Railways and they perform the necessary formalities at the Port/railways and then. they connect the containers on ship/rail, then the Shipping Companies/railways take the containerized cargo to the discharge port/station and at discharge port/station again, they go through the necessary formalities and hand over the containerized cargo to us and then by road we deliver the containerized cargo to the place of Consignee as per their request in certain cases where he gets the goods de-stuffed and then, we hand over the empty containers to the Shipping Companies again. For this the consignor usually calls on phone at our Ahmedabad office for booking/transportation of goods from their premises to the defined destination. Thereafter, we send them the truck for loading of the goods from the consignor's premises, from where the goods are carried to railway yard or to the port of loading by the truck. The goods are then unloaded at yard/port from where the goods are carried on by railways to the various destinations such as Patna, Kolkatta, Hyderabad, Bengaluru, Raipur and Kanpur. By sea route the goods are consigned for the destination of Cochin only. Thereafter. we again take the delivery of goods at the destined Railway station/yard or unload portfrom where the goods are transported to the place of consignee as undertook or entrusted to us. We are as transporter responsible for laking the delivery of goods from the Consignors place to the Consignee's place as per mutual agreement.

The above detailed explanation given by the Proprietor of the assessee indicates that the assessee is not merely engaged in providing services in relation to transportation of goods by road but is engaged in various activities in respect of End-to-End delivery of the cargo from the premises of the consignor to the premises of the consignee.

18.4 The various activities undertaken by the assessee are dissected as under:

y Arrangement of vehicles/containers from the nearest Port to the place of consignor;

y Loading of the goods in the vehicle/ container at the place of Consignor in Gujarat;

y Transportation of such containerized cargo to the nearest Port/railway yard located 111

Gujarat;

Y Unloading of such containerized cargo at the Port/railway yard;

Y Handling of containerized cargo at Port/railway yard including payment of various port/rail charges;

19

question of classification of the activity undertaken by the assessee under the category of Transport of Goods by road (GTA services) is ruled out.

18.8 Now coming to the alleged classification of the service under the head of Cargo Handling Services it needs to be analysed whether the activities undertaken by the assessee fall within the ambit of the definition at Sec. 65(23) of the Finance Act, 1994. The definition of the term 'Cargo Handling Service' has been reproduced hereinabove and it is seen that the said definition is in 3 parts viz. 1) the main definition, 2) inclusive definition and 3) exclusive definition. The main definition indicates that the activities of loading, unloading, packing or unpacking of cargo is covered under the category of Cargo Handling Services. Two inclusions have also been made of which clause (a) pertains to the activities undertaken by a container freight terminal or other freight terminal and clause (b) pertains to the combined activity of packing with transportation of cargo. The exclusion clauses debar three activities from the definition of Cargo Handling Services viz. 1) Handling of Export Cargo, 2) Handling of Passenger Baggage and 3) Mere Transportation of Goods.

18.9 The main definition clearly specifies that the activity of loading/ unloading is covered under the Cargo Handling Services. In the instant case, the activities undertaken by the assessee, as discussed above, clearly include the acts of loading and unloading of cargo amongst the other activities. Thus, the services are covered under the main part of the definition of Cargo Handling Services and there is no room for doubt in this regard.

19. Period from 1.7.2012 to 30.6.2017 (Negative-list regime)

19.1 With effect from 1.7.2012, the concept of classification of services as specified under Sec. 65 was dispensed with and the concept of 'service' as defined under Sec. 65B(44) of the Finance Act, 1994 was introduced. Thus, there was no definition of the term 'Cargo Handling Service' w.e.f. 1.7.2012. However, the term 'Goods Transport Agency' has been defined at Sec. 65B(26) of the Finance Act, 1994 as under:

"goods transport agency" means any person 'who provides service in relation to transport of goods by road and issues consignment note, hy whatever name calIed

The definition of Goods Transport Agency under Sec. 65B(26) of the Finance Act, 1994 is identical to the definition under Sec. 65(50b) of the Finance Act, 1994 as applicable to the period prior to l.7.2012. Thus, the same principle as applicable prior to 1.7.2012 would apply for the period from 1.7.2012 onwards. In other words, the twofold condition of the person engaged in providing service in relation to transport of goods by road and issuance of consignment note would apply for the post negative-list regime also. It has been elaborately discussed in the foregoing paras that the assessee is not solely engaged in the activity of transport of goods by road but the delivery of goods involves movement by rail! sea as well as by road. Therefore, the assessee does not qualify as a Goods Transport Agency during the post negative-list regime too.

19.2 Further, the service tax leviable under the reverse charge mechanism in respect of services of transport of goods by road has been specified under Rule 2( d) of the Service Tax Rules, 1994 which reads as under:

"person liable for paying service tax ". -

A) ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ B) in relation to service provided or agreed to he provided bv a goods transport agencv in respect of transportation o[goods by road. where the person liable to pay freight is,-

(1) ~~~~~~~~~ any person who pays or is liable to payfreight either himself or through his agent for the transportation of such goods by road in a goods carriage

The above statute indicates that the threefold condition as applicable to the pre-negative list regime is still in force viz. 1) Service provider should be a GT A, 2) service should be in relation to transport of goods by road and 3) Goods should be transported in a goods carriage. It has been discussed at length at the foregoing paras that none of the three conditions stand fulfilled in the nature of transaction under consideration. Therefore, the question of shifting of the person liable

21

(c) gross amount charged" includes payment by cheque, credit card. deduction from account and any form of payment by issue of credit notes or debit notes and book adjustment, and any amount credited or debited, as the case may be, to any account, whether called "Suspense account" or by any other name, in the books of account of a person liable to pay service tax, where the transaction of taxable service is with any associated enterprise.

In the instant case the provision of service is for a consideration in money and as such the value shall be the gross amount charged for providing such services. In the instant case it is an undisputed fact that the assessee has charged the gross amount from their clients which has been reflected in the books of accounts of the assessee as income. The gross amount received from the customers towards the said services, for the period from 1.10.2010 to 31.5.2015, has been admitted by Shri Awadheshsingh Chaudhary in his statement dated 12.10.15 at answer to question no. 21. For the period from 1.4.2015 to 30.6.2017, the gross amount received towards rendering the said services has been reflected in the accounting ledgers of the assessee which have been relied upon in SCN dated 27.3.2018. The service tax liability has been computed on such gross amount received towards the services. The assessee have also not disputed the fact that they have received the said amount from their customers against the agreement of delivery of cargo from the consignor'S place to the consignee's premises.

20. It has been contended that by the assessee that the loading and unloading of goods at factory of the consignor and at the consignee's place was being undertaken by the customers and they had only provided services for transportation by road from factory of the supplier to port/ railway yard at loading point and from port/ railway yard at discharge point upto factory of the buyer. However, the said averment is totally in contradiction to the statement dated 12.10.2015 of Shri Awadheshsingh Chaudhary, Proprietor of the assessee wherein he has described the nature of activities undertaken by them at answer to question no. 3. The point-wise activities under-taken have also been listed at para 18.4 hereinabove. The said activities also stand admitted by Shri Awadheshsingh Chaudhary, Prop. of the assessee at answer to question No. 16 of his statement dated 12.10.2015 which is reproduced under for ease of reference:

Q. i6 From the replies made in respect to Q. 0-1-15, don't you think that the your business activity include; (i) arrangingfor vehicles/containers by yourfirm; (ii) loading of goods at the place of Consignor by them: (iii) transportation of containerized cargo at Port/Railways; (iv) unloading of containerized cargo at Port/Railway yard by Shipping

Companies/your firm: (v) handling of containerized cargo at Port/yard including payment ofvarious

port/railway charges: (vi) loading of containerized cargo in coastal vessel by Shipping

Companies/railways; (vii) transportation by sea route, unloading & handling ofcontainerized cargo

at Ports/railways by Shipping Companies and rail-way authorities; (viii) transportation of containerized cargo from off load Ports/rail yards to the

place of Consignee hy the Customers or hy your firm. in certain cases & as per request ofthe Customers: and,

(ix) delivery ofempty containers to the Shipping Companies by your Company after the goods are unloaded at the place of Consignee.

This proves that the 'whole work is being carried upon either by your firm or by other intermediariesfor yourfirm. Do ),011 agree?

A. Yes, to support our transportation services to different individuals/ Business Entities we are performing the activities of transportation of their choice seal rail

The above clearly indicates that the assessee is also involved in the activities of loading and unloading amongst the other activities undertaken by them. Further, the assessee have not submitted any evidence to establish that they have not engaged themselves in the activity of loading or unloading of goods. In absence of any evidence to that effect, the admission of the Proprietor would hold good since the statement recorded under Sec. 14 of the Central Excise

were made to the effect that they would be providing merely Road Transportation services and would act as a pure agent in respect of transportation by sea or rail. An image of the rate contract withdrawn during the course of panchnama dated 12.10.2015 is reproduced under:

( t, \ . \~

orr. : 2~i,:545<19, 2S'!')(),)c,r)

1.10. : 9f!79G120G1, (ifj. 'Hi/S0071 i'. -_ -"~ - ------ - ~-- - - -- ~--- - - ~.,' .;:.:. \',\Nl.'YA BHAVi\N lliD FLO .. . ... - _. -.

_ .• , on. OPi'. [lIWMI Bt.LLUBHAI SCHOOL, KMIKflnlA nOf-D, AfH.'EADMlAD.381 Gil

NO.SCfHnt('/l :~·1.1/1.1!) '1\,. Dt.lG.Ol.2011

~\rm:\ Ltd "Xirrnu House" Ashram Road Aluucdn bad.

EiIl(t,·\ttn.:' Shri Nnrlibi .Ji

Sub: R:ltt'~ ex Fnct ory at Bhnvnngar via Bhavnagar Railway siding to Fl.l'l' -Pal 11:\ door delivery at Nirma Ltd Godown at sipara Patna

~ Through Railway wauone>

\\' c are quo! ing our Hates for Transportation of Nirrna Ltd Vltl Salt Ex Factory Y1a Bhavnagar to Patna up to Nirrnn Ltd Depot at Sipara as mentioned bellow>

I Ex Factory Salt Rate P_(!r :\rCB:<;=j1 Bhnvnaznr I 2G05 ~ ~~~~~ L_____ ~~~----~

f

We hope you will find our Rates competitive enough to fulfill your requirement. We arc

waiting for your kind approval.

,- ;;~ With Regards,

Yours truly,

For: sHr;v~RIERS Ii <

AutJ ignatory

BRANCH OFFICE:

~OLKATA P~ot ~~o 23 ,06 "~ FiOOI Ra-, K~m.Jf Gan1,1Uly Laroe. ?C~! 9: Ga"jfln, H~r3h·3 To: ~a' OJ3·2~8803-l' •.• C9~J':";SJS57

COCHIN Cro Dr, RJmson R Ntlir Hou~C No 1 ZlS93A Krish,'13\n.;pa.Coct""" CcHrgc 2"1d Street Land, KooyaC'a1d~. Coc~"o·2 M 09-l47722763

GANDHIOHAM r.4 9~2SC32S~G

PATNA

B •• nglore M 9879;;12C6'

tj,l,ll PJt"''' Ty'!' F":'!r P.1o~:1~·i M C~JJ~l1J)1J

The above rate contract indicates that the goods were to be delivered on door delivery basis to Patna and the goods were to be loaded from the factory at Bhavnagar. The entire activity of delivery also included movement of goods by Railways. However, it is seen that lump-sum rate has been quoted for the entire composite activity of delivery of goods from Bhavnagar to Patna and the rate contract nowhere indicates that the customer had a clear understanding that the railway freight had to be exactly reimbursed to the assessee. There is no bifurcation of the

25

Supreme Court had upheld the interpretation of the High Court and rendered the decision in light of such interpretation. The relevant text of the said judgment is reproduced under:

6. The High Court, on the interpretation of the aforesaid Entry, has observed that two conditions for considering any service to be 'Cargo Handling Service' need to be satisfied, namely: (J) there must be a cargo i.e. a packed or unpacked commodity accepted by a transporter or carrier for carrying the same from one destination to another. It is only after the commodity becomes a cargo, its loading and unloading at the freight terminal for being transported by any mode becomes a cargo handling service, if it is provided by an independent agency and: (2) the service provider must independently be involved in loading-unloading or packing unpacking of the cargo. 7. The aforesaid meaning given by the High Court while interpretating Entry 23 of Section 65 is perfectly in order and justified. On that has is. we have to see whether the twin conditions mentioned therein are satisfied in the present case or not.

What that appears to be necessity of law for taxation under the class cargo handling service is that the service provided should he relating to or in relation to cargo handling by a cargo handling agency. The service provided should be integrally or inseparably connected with handling of cargo or attributable thereto without being a mere activity of transportation of such cargo since transport service independent of cargo handling is an exception under the scheme of levy by Section 65(23) of the Act. Thus it can be said that loading. unloading, packing or unpacking of cargo and handling of cargo {or freight in special containers or non-containerized freight and service prOVided hy container (i-eight terminal or other freight terminal (or all modes of'transport are suhject matter of taxation under the class "cargo handling service ".

From the above it is evident that the underlying principles have been specified that there should be a cargo and the service provider must be independently involved in loading/ unloading or packing/ unpacking of cargo. In the instant case, both the elements are present i.e. there is a cargo and the assessee have admittedly engaged themselves in loading/ unloading of the cargo. Thus, the charges leveled in the SCN are not being contradicted by the above judgment of the Hon'ble Apex Court.

Further the judgment of M/s Gajanand Agarwal supra relied upon the assessee completely supports the allegations made in the present show cause notice and the relevant text of the findings of the Tribunal is reproduced under:

In the instant case, the activities undertaken by the assessee have been categorized hereinabove and it is seen that the activities of loading/ unloading as discussed under the judgment supra have been undertaken by the assessee. Therefore, the said judgment supports the case of the department rather than the case of the assessee.

20.5 It has been argued that the activity of transportation was specifically excluded from Cargo Handling Services and as such the exclusion should be given effect as held in the case law of Dr. Lal Path Lab (P) Ltd. Reported at 2006 (4) STR 527 as upheld by High Court in 2007 (8) STR 337. A reference to the definition of Cargo Handling Service as defined under Sec. 65(23) of the Finance Act, 1994 indicates that the exclusion portion from the definition is the activity of 'mere transportation of goods'. As already discussed above, it is an admitted fact that the assessee are not merely engaged in transportation of goods but are undertaking a combination of various activities interalia comprising of loading/ unloading of goods alongwith transportation of goods by Road as well as Sea/Rail. Therefore, the exclusion clause of the definition would not apply to the facts of the case in as much as the activity undertaken by the assessee is not merely transportation of goods. Resultantly the case law relied upon by the assessee also is not applicable to the facts of the case.

20.6 The assessee has also cited the case laws of M/s Konkan Marine Agencies reported at 2009 (13) STR 7, M/s Balmer Lawrie & Co. Ltd. reported at 2014 (35) STR 800 and Mr. Dalveer Singh reported at 2008 (9) STR 491 to emphasize that their activity was not covered under Cargo Handling Services. In the case of M/s Konkan Marine Agencies the issue under

27

made by them through road first, then by rail or sea and again by road. The said admission clearly indicates that the rate quoted was for the entire activity and there was no agreement to the effect that the assessee was to incur the expenditure of transport by rail! sea on behalf of the service recipient. Thus, the provisions of Rule 5(2) of the Service Tax (Determination of Value) Rules do not come into play in the instant case. Resultantly, the reliance on the case law of Mis Intercontinental Consultants and Technocrats P Ltd. reported at 2018 (10) GSTL 401 is inconsequential since the same deals with a situation of reimbursable expenses.

20.10 It has been further submitted that the benefit of cum-tax-value had not been extended to them. In this regard, I find that the assessee have mis-classified the services as GTA services which are liable to service tax under the reverse charge mechanism. Thus. the assessee have shifted the onus of payment of service tax on the service recipient in respect of such services and as such the it cannot be said that the consideration is inclusive of the service tax payable. Further, it is on record that the assessee have not shown the said consideration in their ST -3 returns even under the category of GT A and thereby, they have resorted to gross suppression of facts. In such cases, the benefit of cum-tax-value cannot be extended to the assessee. My views are supported by the case law of Mis Asian Alloys Ltd. v. CCE, Delhi-III reported at 2006 (203) E.L.T. 252 (Tri.-Del.), which has been affirmed by the Supreme Court as reported at 2012 (278) EL T A 143 (SC), and the relevant portions of the order are reproduced below:

"18. It was contended that the amounts 'Forked out for the values of job work, clandestine removal, and shortage, totalling Rs. 28,92,32,7531-, even if taken to be true and correct should be considered as the total price received by the said unit of the appellant company inclusive of duty. In other words, the said amount should be considered, as "cum-duty" price and the duty liahility should he worked out on that hasis. In this context, it appears from the decision of the Mumbai Bench of the Tribunal in Nagreeka Exports Ltd. v. Commissioner of Central Excise, Pune reported in 2003 (159) E. L. T. 891 (Tri. -Mumbai), that in Paragraph 1 I of the judgment it has been held that if duties and taxes have not been realized separately, the sale price has to be treated as cum-duty price and duties and faxes have to be deducted to arrive at the assessable value in such case. The Tribunal was dealing with the contention that the price which was realized by the appellants on DTA sales he taken as cum-duty price and the assessable value and the duty amount have to he worked out ./i'OI71 the same. It however, appears that the issue of clandestine removal and its impact on the claim for treating price as cum-duty was neither raised nor considered by the Tribunal in that order. In the present case, there is absolutely no material on record to indicate that the price charged by the 100% EOU unit of the appellant was a cum-duty price. Even in the decision of the Hon 'ble Supreme Court in Commissioner of Central Excise, Delhi v. Maruti Udyog Ltd. reported in 2002 (141) E.L.T. 3 (S.c.) (supra}, in Paragraph 5 of the judgment the Honble Supreme Court held as under :- "A reading of the aforesaid section clearly indicates that the wholesale price which is charged is deemed to be the value for the purpose of levy (~f excise duty, but the element of excise duty, sales tax or other taxes which is included in the 'wholesale price is to be excluded in arriving at the excisable value. This section has been so construed by this Court in Asstt. Collector of Central Excise and Others v. Bata India Ltd. - 1996 (4) SCC 563, and it is thus clear that when cum duty price is charged, then in arriving at the excisable value of the goods the element of duty which is payable has to be excluded. The Tribunal has, therefore. rightly proceeded on the basis that the amount realized by the respondent from the sale of scrap has to be regarded as a normal wholesale price and in determining the value on which excise duty is payable the element of excise duty which must be regarded as having been incorporated in the sale price, must be excluded. There is nothing to show that once the demand was raised by the Department, the respondent sought to recover the same from the purchaser of scrap. The facts indicate that after the sale transaction was completed, the purchaser was under no obligation to pay any extra amount to the seller, namely, the respondent. In such a transaction, it is the seller who takes on the obligation of paying all taxes on the goods sold and in such a case the said taxes on the goods sold are to be deducted under Section 4(4)(d)(ii) and this is precisely what

29

therefore the department would come to know about such non-payment of duty/service tax only during audit or preventive/other checks. In the instant case, the assessee have failed to reflect the taxable income in their ST - 3 returns and have concealed such income from the department deliberately, consciously and purposefully to evade payment of service tax. Had it not been for the investigation by the officers of the DOOL the case would never have seen the light of the day. In the case of Mahavir Plastics versus CCE Mumbai, 2010 (255) EL T 24 L it has been held that if facts are gathered by department in subsequent investigation extended period can be invoked. In 2009 (23) STT 275, in case of Lalit Enterprises vs. CST Chennai, it is held that extended period can be invoked when department comes to know of service charges received by appellant on verification of his accounts. Therefore. I find that the all essential ingredients exist to invoke the extended period under proviso to Section 73 (l) of Finance Act, 1994 in the case at hand. Accordingly, I find that the service tax is liable to be recovered by invoking the extended period of limitation as provided for under Sec. 73 of the Finance Act, 1994 along with interest in terms of the provisions of Sec. 75 of the Finance Act, 1994.

22.1 With regard to SCN F.No. STC/04-57/0A/ShivIl7-18 dated 27.03.2018, penalty under Section 76 of the Finance Act, 1994 has been proposed. In this regard I find that the assessee have failed to discharge the service tax on the services provided by them and therefore they are liable to penalty under Sec. 76 of the Finance Act, 1994.

22. Further, the assessee have contended that there was no intention to evade payment of service tax and as such penalty under Sec. 78 cannot be imposed. However, the discussion at the foregoing paras clearly indicates that the assessee have resorted to suppression of facts and contravention of the provisions of law with an intent to evade payment of service tax and as such I find that penalty under Sec. 78 of the Finance Act 1994 is imposable.

23. The assessee have made pleas of waiver of penalty in terms of the provisions of Sec. 80 of the Finance Act, 1994. However, the discussion at the foregoing paras indicate that the service tax has not been paid by reason of suppression of facts and contravention of the provisions of the law with an intent to evade payment of service tax and as such the provisions of Sec. 80 of the Finance Act, 1994 will not come into play.

24. It has been contended that Sec. 76 and 78 are mutually exclusive and simultaneous penalty under both is contradictory. In this regard I find that the argument is out of context in as much as simultaneous penalty has not been proposed in either of the two SCNs. The SCN dated 31.3.2016 proposes penalty under Sec. 78 of the Finance Act. 1994 whereas the subsequent SCN dated 27.3.2018, being a protective demand under Sec. 73(IA) of the Finance Act, 1994, proposes penalty under Sec. 76 of the Finance Act, 1994 which provides for imposition of penalty not exceeding ten per cent of the amount of such service tax.

25. Penalty under Section 77 of the Finance Act 1994 has been proposed in both the SCNs. The contraventions alleged in the SCN are failure to discharge the service tax in the time and manner as prescribed under law and failure to determine gross value of the said taxable services. In this regard, I find that the act of non-payment of service tax by due date is not covered under the provisions of Sec. 77(1) of the Finance Act. 1994. As regards. the provisions of Sec. 77(2) is concerned, the same is imposable in cases where no other penalty has been provided for under the law. In the instant case, I find that for non-payment of service tax, penalty under Sec. 78 has already been proposed and I have also found that penalty under Sec. 78 is imposable and therefore the provisions of Sec. 77(2) would also not be applicable to the instant case. For ease of reference, the provisions of Sec. 77 are reproduced under:

SECT/ON /77. Penalty for contravention of rilles and provisions of Act for which no penalty is specified elsewhere. - (l ) Any person. -

"(a) who is liable to pay service tax or required to lake registration. jails to take registration in accordance with the provisions of section 69 or rules made under this Chapter shall be liable to a penalty which may extend to ten thousand rupees;

(b) who jails to keep, maintain or retain books of account and other documents as required in accordance with the provisions of this Chapter or the

31

f) I confirm the demand of service tax to the tune of Rs. 4,20,48,276/- (Four crores Twenty Lakhs Forty Eight Thousand Two Hundred Seventy Six only) and order recovery of the same in terms of the provisions of Section 73 of the Finance Act, 1994;

a) I confirm the demand of service tax to the tune of Rs. 13,92,91,454/- (Service Tax Rs. 1352344211- + Education Cess: Rs. 2704688/- + Higher Secondary Education Cess Rs. 1352344/-) {Rs. Thirteen Crore Ninety Two Lakhs Ninety One Thousand Four Hundred Fifty Four only} and order recovery of the same in terms of the provisions Section 73 of the Finance Act, 1994, by invoking extended period of limitation;

b) Interest at the appropriate rate shall be charged and recovered from the assessee in terms of the provisions of Section 75 of the Finance Act, 1994;

c) I impose a penalty of Rs. 13,92,91,454/- (Rs. Thirteen Crore Ninety Two Lakhs Ninety One Thousand Four Hundred Fifty Four only) on the assessee in terms of the provisions of the Section 78 of the Finance Act, 1994. However, in view of clause (ii) of the second proviso to Section 78 (1), if the amount of Service Tax confirmed and interest thereon is paid within period of thirty days from the date of receipt of this Order, the penalty shall be twenty five percent of the said amount, subject to the condition that the amount of such reduced penalty is also paid within the said period of thirty days.

d) I refrain from imposing penalty under Section 77 of the Finance Act. 1994 for the reasons given above.

e) I vacate the proposal of imposition of penalty under Section 70 of the Finance Act. 1994 for the reasons given above.

With respect to SCN F.No. STC/04-57/0A/ShivIl7-18 dated 27.03.2018

g) Interest at the appropriate rates shall be charged and recovered from the assessee in terms of the provisions of Section 75 of the Finance Act, 1994;

h) I impose a penalty of Rs. 42,04,827/- (Rs. Forty Two lakhs Four Thousand Eight Hundred Twenty Seven only) on the assessee in terms of the provisions of Section 76 of the Finance Act, 1994;

i) I refrain from imposing penalty under Section 77 of the Finance Act, 1994 for the reasons given above.

j) I vacate the proposal of imposition of penalty under Section 70 of the Finance Act, 1994 for the reasons given above.

.~. L. r

~ ).~.-.)"'. N (Sunil Kumar Singh)

Principal Commissioner Date: 25/08/2020

F.No. STC/4-114/0&Al15-16

BY R.P.A.D.

To, M/s Shiv Carriers, 323, Vanijya Bhavan, Kankaria Road, Ahmedabad

Copy to:- 1) The Principal Chief Commissioner, Ahmedabad Zone. 2) ADG, DGGI, AZU, 6th & ih Floor, '1' The Address Building, Opp. HCG Hospital, Nr.

Sola Overbridge, Sola, Ahmedabad. 3) The Deputy/Assistant Commissioner, CGST, Division-I, Ahmedabad-South.

33