h2 2012 results - capgemini capgemini investors en · onepathtm: sap as-a-service products and...

TRANSCRIPT

2012 Half Year Results

July 26, 2012

2012 Half Year Results

2 Copyright © Capgemini 2012. All Rights Reserved

Paul Hermelin Chairman and CEO

2012 Half Year Results

3 Copyright © Capgemini 2012. All Rights Reserved

€5,150M revenue in H1 2012, +8.3% +2.3% organically, in line with guidance

Positive net cash position €27M Business model under control

6.4% of revenue, in line with FY guidance

121,000+ headcount Continuous increase of our offshore basis, 38.1% (+1pt vs YE 2011)

Growth

Operating

margin

Sales activity

Offshore

Good booking level, BBR at 1.09, 1.16 in Q2 2012

Price pressure resistance thanks to high-value offer development

Cash

Strong resilience demonstrated again

2012 Half Year Results

4 Copyright © Capgemini 2012. All Rights Reserved

We execute our strategy

Sell new offerings bringing higher value to clients

and higher margins (eg. Cloud based offers - Salesforce.com)

Develop solutions and new business models

(eg. SAP Mobility)

Accelerate offshore expansion (e.g. XRIM)

Reshape onshore pyramids, hire more freshers

Develop a strong industrialized network of AM factories

Improve cost position leveraging Lean methods

and standardization

Portfolio

Pyramid

Industrialization & Cost cutting

2012 Half Year Results

5 Copyright © Capgemini 2012. All Rights Reserved

Client appetite for our cloud-based portfolio strategy

Customer

experience

Operational

Process Business model

SAAS

PAAS

IAAS

"Cloud"

Digital Transformation MIT framework

Cloud is everywhere!

Mobility

Big Data

2012 Half Year Results

6 Copyright © Capgemini 2012. All Rights Reserved

SAP as-a-service, innovative cloud-based solutions

PartnerEdge

Channel

Program

RapidPath for

Medical Devices

EnergyPath

CRESCENT

Consumer retail

IBX platform

Procurement

CHROME

Manufacturing

Financials and

Accounting

BPO

Procurement

BPO

Public Cloud

Private Cloud

SAP Managed

Mobility Partner

Program

Illustration with SAP

business in North America

5% of bookings

are “As a Service”

25% of bookings

are “Solutions based”

For 100% of bookings,

solutions were part of the

discussions

License Build Host Operate

Solutions

Products

Services Support for

Solutions

IAAS SAAS PAAS

OnePathTM : SAP as-a-service Products and Solutions

2012 Half Year Results

7 Copyright © Capgemini 2012. All Rights Reserved

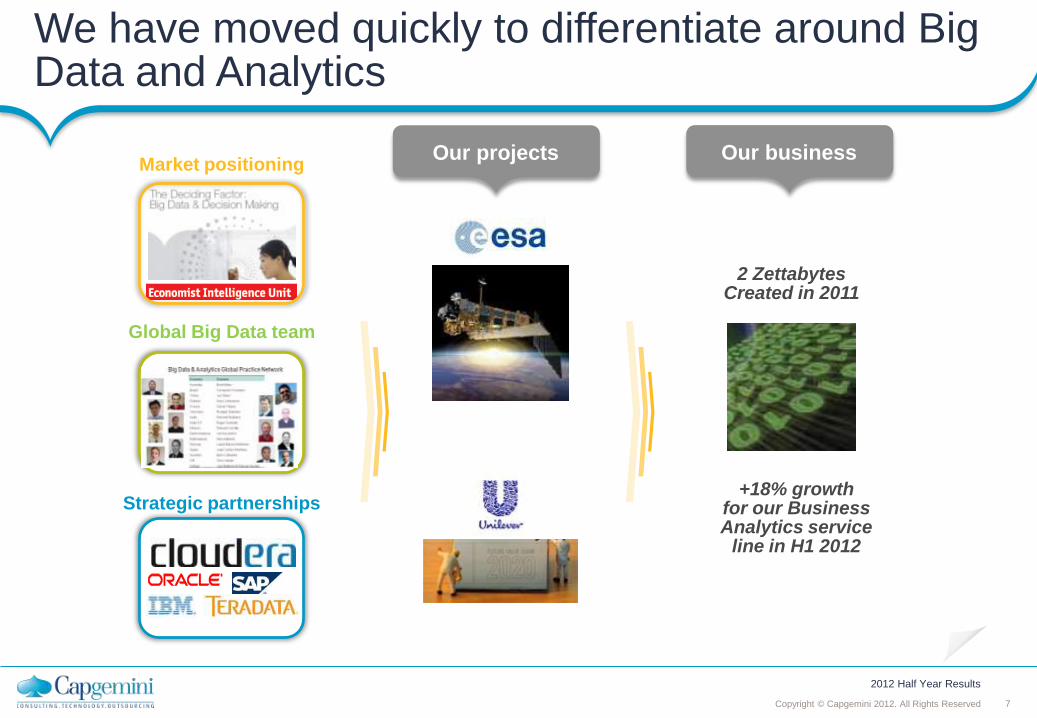

We have moved quickly to differentiate around Big Data and Analytics

Market positioning

Global Big Data team

Strategic partnerships

Our projects Our business

2 Zettabytes Created in 2011

+18% growth for our Business Analytics service

line in H1 2012

2012 Half Year Results

8 Copyright © Capgemini 2012. All Rights Reserved

Re-shaping fast our pyramid

Offshore expansion

75K

44 k (35k in India)

80 K

YE 2011 Target 2015

46 k (near 37k in India)

H1 2012

End-to-end pyramid

40% freshers out of H1 2012 total recruits, +3pts versus 2011

Objective of 47% freshers out of total H2 recruits with the

upcoming recruitment season in September

Strengthening senior positions offshore: +19% increase this

year

2012 Half Year Results

9 Copyright © Capgemini 2012. All Rights Reserved

2012 2015

Major deals including large offshore components

Recent major deals validate our Rightshore® strategy

2011

550 FTEs

80 FTEs 250 FTEs

230 FTEs

The champion in Continental Europe

with a share of 10% of total offshored

resources serving Europe

Several Banking

Deals

2012 Half Year Results

10 Copyright © Capgemini 2012. All Rights Reserved

Globalization agenda Winning clients are engaged

in a globalization journey

We entered the elite world of global players

Global delivery network Demanding customers want global

delivery networks, including industrialized onshore centers

Global consistency Alliance partners require global

coverage and alignment

(1) : IBM, Accenture, Indian pure players

€20m+ deal pipeline up 42% vs January

We are increasingly bidding against global players (1) : 71% of our bids

(versus 58% in 2011)

2012 Half Year Results

11 Copyright © Capgemini 2012. All Rights Reserved

A tangible shift of the Group in H1 2012

Group

momentum

Sustained growth in North America

Top accounts strategy & reference clients

New geographies expansion

Demonstrated resilience in troubled Europe

+9.7% H1 YoY

20.8% of the Group revenue in Q2

Caixa multi-year deal in Brazil

ANZ deal in Australia

Double-digit growth in Nordic and in the UK, excl. Aspire Turnaround program in NL

Portfolio management to offset price pressure

Limited price decrease +29% growth of our Top Line Initiatives

+10% growth on strategic accounts for

the second year

Acquisition of reference customers

New business models uptake

+30% SAP business As a service/ solutions in the US Significant Prosodie deal with CNAM

1

3 6

4

2 5

Successful combination

of organic growth and accretive acquisitions

2012 Half Year Results

12 Copyright © Capgemini 2012. All Rights Reserved

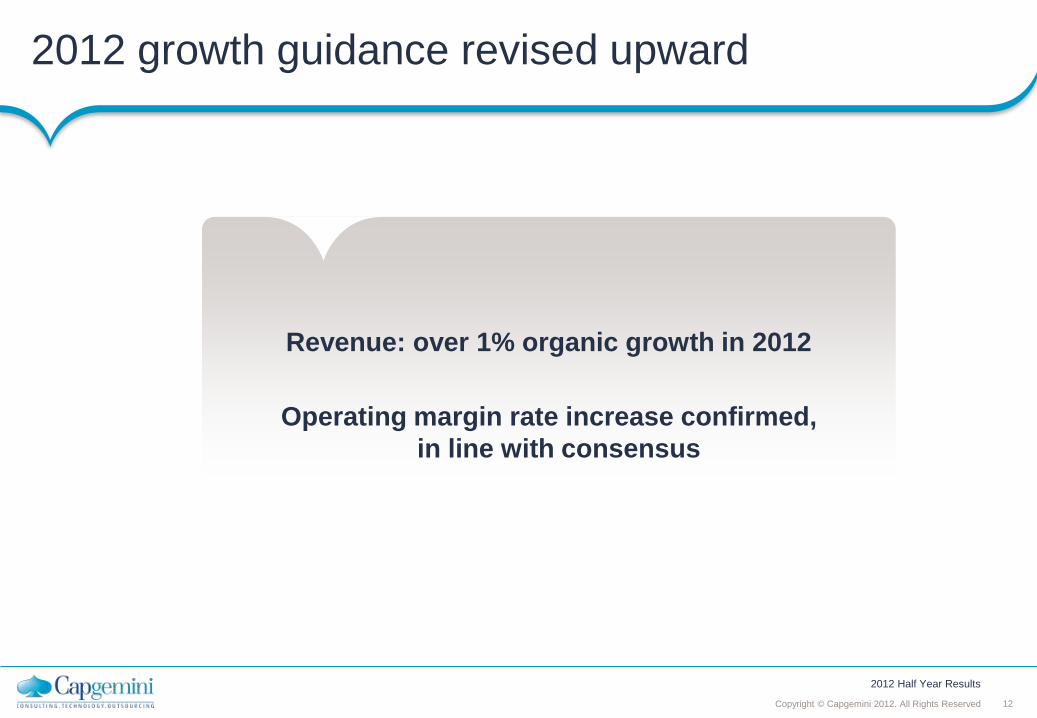

2012 growth guidance revised upward

Revenue: over 1% organic growth in 2012

Operating margin rate increase confirmed,

in line with consensus

2012 Half Year Results

13 Copyright © Capgemini 2012. All Rights Reserved

Paul Nannetti Group Sales and Portfolio Director

2012 Half Year Results

14 Copyright © Capgemini 2012. All Rights Reserved

At budget rates and constant perimeter

H1 2012 revenue by sector

H1 2012

H1 2012

vs. 2011

Revenue

Financial services -5.6%

Energy, utilities & chemicals 5.3%

MALS 0.7%

CPRDT 9.8%

Public sector -0.9%

Telecom, Media & entertainment 0.0%

Total 2.3%

19.0%

23.9%

17.3%

13.7%

10.9%

9.0%

6.2%

External revenue

Financial services Public sector

MALS CPRDT

Energy, utilities & chemicals Telecom, media & entertainment

Others

2012 Half Year Results

15 Copyright © Capgemini 2012. All Rights Reserved

Bookings evolution by business

M€

1639 1754 1371

1713 1586 1749

784

1004

815

764

559

1219

0

500

1000

1500

2000

2500

3000

3500

Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12

CS / TS / LPS Outsourcing

2423

2758

2186

2477

2145

2968

At budget rates and constant perimeter

2012 Half Year Results

16 Copyright © Capgemini 2012. All Rights Reserved

Book to Bill evolution

Q2 2012

Consulting/Technology/Local professional services

M€ Booking Revenue BBR

North America 390 343 1.14

Rest of the World 1 359 1 163 1.17

Total 1 749 1 506 1.16

At budget rates

H1 2012

Consulting/Technology/Local professional services

M€ Booking Revenue BBR

North America 739 679 1.09

Rest of the World 2 596 2 383 1.09

Total 3 335 3 062 1.09

At budget rates

2012 Half Year Results

17 Copyright © Capgemini 2012. All Rights Reserved

Major H1 2012 deals

IT partner

Smart metering

+ Customer experience

ALS

ALS

Service Integration

Testing

€MMM years

€130M

€80M

~€50M

€MM

€MM

TCV figures

2012 Half Year Results

18 Copyright © Capgemini 2012. All Rights Reserved

How we see the market

Geographies

Digital Transformation

Multi Channel Exp.

Cloud, Big Data, Mobility

Offers

CPR

EU

FS outside Continental

Europe

Sectors

Benelux

Iberia

Mega, multi-tower deals FS in Continental

Europe

Public Sector

“Hot”

“Cold”

Overall, transition from Capex to Opex, caution on long-term investments

but appetite for new technologies… and a good flow of larger deals

North America

Nordic

Asia Pacific

France, Germany,

UK, Italy, Latam

Mid size offshore

AM/IM/BPO

TME

MALS

Stable

=

2012 Half Year Results

19 Copyright © Capgemini 2012. All Rights Reserved

Nicolas Dufourcq Deputy General Manager and CFO

2012 Half Year Results

20 Copyright © Capgemini 2012. All Rights Reserved

(in M€)

H1 2011 H2 2011 H1 2012 H1 2012

vs

H1 2011

Revenues 4 756 4 937 5 150 + 8.3%

Operating expenses - 4 467 - 4 513 - 4 822

Operating Margin before amortization of intangible assets acquired through business combinations

301 437 347

(% Revenues) 6.3% 8.9% 6.7% + 0.4 pt

Amortization of intangible assets acquired through business combinations

- 12 -13 -19

Operating Margin 289 424 328

(% Revenues) 6.1% 8.6% 6.4% + 0.3 pt

Other operating expenses - 49 - 69 - 91

Operating Profit 240 355 237

(% Revenues) 5.1% 7.2% 4.6% - 0.5 pt

Net financial expense - 51 - 54 - 49

Income tax expense - 70 - 31 - 55

Share of profit of associates - - -1

Non-controlling interests 8 7 11

Net Profit (Group Share) 127 277 143

Normalized Net Profit (Group Share) (*) 158 321 211

Net cash (end of period) 169 454 27

Number of employees (end of period) 114 274 119 707 121 026

Income Statement: Overview

+ 2.3 % Organic

(*) Normalized net profit (Group share) equal Net profit (Group share) corrected for the impact of restructurings costs and amortization of

intangible assets acquired through business combination, net of tax.

2012 Half Year Results

21 Copyright © Capgemini 2012. All Rights Reserved

Current Organic

Current Sequential Year on

year Sequential

Year on year

(in M€) Q2 2011 Q1 2012 Q2 2012 Q2 12 /

Q1 12

Q2 12 /

Q2 11

Q2 12 /

Q1 12

Q2 12 /

Q2 11

North America 445 505 536 6.1% 20.2% 4.3% 7.2%

UK & Ireland 508 510 559 9.5% 9.9% 6.3% 0.9%

France 515 578 538 -7.1% 4.5% -7.1% -4.3%

Benelux 319 298 278 -6.9% -12.9% -6.9% -13.0%

Rest of Europe, Asia & Latin America

619 674 674 0.3% 9.1% 1.5% 5.6%

TOTAL 2 406 2 565 2 585 0.8% 7.4% 0.2% 0.4%

Benelux

North America

UK &

Ireland

France

Rest of Europe,

Asia & Latin

America

20.8%

21.6%

10.7%

20.8%

26.1%

Q2 2012 Revenues by Main Geography

2012 Half Year Results

22 Copyright © Capgemini 2012. All Rights Reserved

At constant rates and perimeter

Q2 2012 Growth by Discipline

5.2%

39.9%

40.3%

14.6%

Consulting

Services

Technology

Services

Local Professional

Services

Outsourcing Services

Sequential Year on year

Q2 12 / Q1 12 Q2 12 / Q2 11

Consulting Services 1.3% 1.4%

Technology Services -0.2% 3.1%

Local Professional Services

-7.2% -3.0%

CS / TS / LPS -1.9% 1.4%

Outsourcing Services 3.4% -1.0%

TOTAL GROUP 0.2% 0.4%

2012 Half Year Results

23 Copyright © Capgemini 2012. All Rights Reserved

Current Organic

Current Sequential Year on

year Sequential

Year on year

(in M€) H1 2011 H2 2011 H1 2012 H1 12 /

H2 11

H1 12 /

H1 11

H1 12 /

H2 11

H1 12 /

H1 11

North America 869 936 1 041 11.3% 19.7% 4.5% 9.7%

France 1 039 1 099 1 116 1.6% 7.4% 2.0% - 1.6%

UK & Ireland 987 958 1 069 11.6% 8.3% 5.8% 2.3%

Benelux 642 624 576 - 7.6% - 10.3% - 7.7% - 10.4%

Rest of Europe, Asia & Latin America

1 219 1 320 1 348 2.1% 10.6% 0.4% 6.8%

TOTAL 4 756 4 937 5 150 4.3% 8.3% 1.6% 2.3%

Benelux

North America

UK &

Ireland

France

Rest of Europe,

Asia & Latin

America

20.2%

20.8%

11.2%

21.7%

26.1%

H1 2012 Revenues by Main Geography

2012 Half Year Results

24 Copyright © Capgemini 2012. All Rights Reserved

At constant rates and perimeter

H1 2012 Growth by Discipline

5.2%

39.3% 40.3%

15.2%

Consulting

Services

Technology

Services Local

Professional

Services

Outsourcing

Services

Sequential Year on year

H1 12 / H2 11 H1 12 / H1 11

Consulting Services 6.3% -0.5%

Technology Services 3.3% 4.8%

Local Professional Services

2.8% 0.6%

CS / TS / LPS 3.4% 3.3%

Outsourcing Services - 1.0% 0.9%

TOTAL GROUP 1.6% 2.3%

5.3%

39.8% 39.4%

15.5%

Consulting

Services

Technology

Services Local

Professional

Services

Outsourcing

Services

H1 2012

H1 2011

2012 Half Year Results

25 Copyright © Capgemini 2012. All Rights Reserved

50

60

70

80

90

8284 84 83

8283

7978

7980 80 80

656867

7168 67

Consulting Services Technology Services Local Professional Services

At constant perimeter

Q1 Q2 Q2 Q4

2011 2012

Q3 Q1

(%)

Q1 Q2 Q2 Q4

2011 2012

Q3 Q1 Q1 Q2 Q2 Q4

2011 2012

Q3 Q1

Utilization Rates by Business

2012 Half Year Results

26 Copyright © Capgemini 2012. All Rights Reserved

Charge-out Rates

Year on year

Variation

Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12

Consulting Services

Local Professional Services

Technology Services

Weighted average

0.4%

0.1%

- 2.2%

- 1.8 %

-0.7%

1.1%

- 3.0%

- 1.6%

0.8%

1.3%

- 3.7 %

- 1.9%

- 1.3%

1.9%

- 1.0%

0.0%

- 1.6%

2.2%

- 1.0%

- 0.1%

- 1.6%

1.1%

- 1.1%

- 0.5%

Pricing Evolution (onshore)

2012 Half Year Results

27 Copyright © Capgemini 2012. All Rights Reserved

Headcount as of Dec. 31, 2011 119 707

Recruits (*) 14 570

Acquisitions / Outsourcing Deals 104

Disposals - 65

Layoffs - 2 993

Leavers - 10 297

Headcount as of June 30, 2012 121 026

(*) out of which 1 571 in Sogeti (excl. India)

5 625 in India

1 899 in other offshore centers

52% offshore

Attrition YTD June

2011

Dec

2011

June

2012 YoY Var.

Consulting services 21.3% 20.5% 17.1% - 4.2 pts

Technology services 17.0% 18.4% 16.7% - 0.3 pt

Local Professional

services 17.3% 18.0% 16.3% - 1.0 pt

Outsourcing services 17.7% 16.6% 17.0% - 0.7 pt

Total Business 17.7% 18.2% 17.0% - 0.7 pt

Headcount Evolution

2012 Half Year Results

28 Copyright © Capgemini 2012. All Rights Reserved

“Pyramid Effect” Improving

ONSHORE (cost of 2 899 M€ in H1 2012)

OFFSHORE (cost of 274 M€ in H1 2012)

in % Year on Year H1 2010 H2 2010 H1 2011 H2 2011 H1 2012

Salary increase 1.3 1.5 2.7 3.3 2.4 Average remuneration increase 2 3.6 2.8 0.4 -1

Pyramid effect 0.7 2.1 0.1 -2.9 -3.4

Continuous

effect in

H1 2012

Favorable pyramid effect continues into H1 2012, group average remuneration is down 3.1% in H1 2012

In % Year on Year H1 2010 H2 2010 H1 2011 H2 2011 H1 2012

Salary increase 6.6 7.8 7.4 9.2 7.1 Average remuneration increase 1.7 7.3 5 0.8 3.1

Pyramid effect -4.9 -0.5 -2.4 -8.4 -4

2012 Half Year Results

29 Copyright © Capgemini 2012. All Rights Reserved

Evolution of Group Remuneration Cost from H1 2011 to H1 2012

At current rates

& perimeter

At constant rates

& perimeter

Group average remuneration costs evolution - 1.2% - 3.1%

2012 Average salary increase onshore : 2.4%

2012 Average salary increase offshore : 7.1%

2012 Half Year Results

30 Copyright © Capgemini 2012. All Rights Reserved

H1 2011 H2 2011 H1 2012

Revenues 4 756 4 937 5 150

Personnel costs - 2 958 - 2 858 - 3 173

% of Revenues 62.2% 57.9% 61.6%

Purchases and subcontracting expenses - 1 052 - 1 179 - 1 129

% of Revenues 22.1% 23.9% 21.9%

Travel expenses - 192 - 199 - 208

% of Revenues 4.0% 4.0% 4.0%

Rent and local taxes - 158 - 166 - 162

% of Revenues 3.3% 3.4% 3.2%

Depreciation, amortization, provisions and proceeds from asset disposal - 107 - 111 - 150

% of Revenues 2.3% 2.2% 2.9%

Total operating expenses - 4 467 - 4 513 - 4 822

% of Revenues 93.9% 91.4% 93.6%

Operating margin 289 424 328

% of Revenues 6.1% 8.6% 6.4%

Operating Margin before amortization of intangible assets acquired through business combinations

301 437 347

% of Revenues 6.3% 8.9% 6.7%

77.3% Cost of

services

rendered

Operating

Margin

Selling

8.6% 8.0% 6.1%

G&A

At current rates and perimeter (in M€)

Operating Margin Analysis

H1 2011

Operating

Margin 7.9% 7.8%

77.9%

6.4%

G&A

Cost of

services

rendered

Selling

H1 2012

2012 Half Year Results

31 Copyright © Capgemini 2012. All Rights Reserved

H1 2011 H2 2011 H1 2012

Consulting Services

Technology Services

Local Professional Services

CS / TS / LPS

Outsourcing Services

11.8%

5.8%

9.9%

7.4%

5.7%

12.2%

7.7%

12.0%

9.1%

9.6%

10.8%

6.7%

9.5%

7.7%

5.9%

Total Operations (*) 6.8% 9.3% 7.0%

GROUP 6.1% 8.6% 6.4%

At current rates and perimeter

(*) before headquarters’ expenses

Operating Margin by Discipline

2012 Half Year Results

32 Copyright © Capgemini 2012. All Rights Reserved

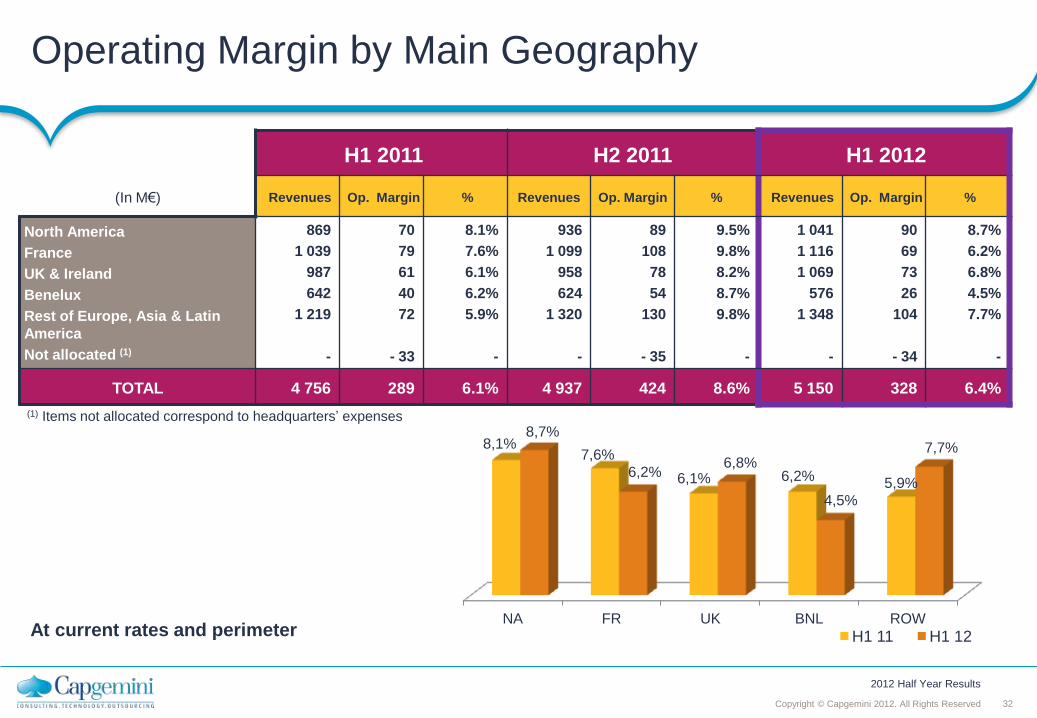

H1 2011 H2 2011 H1 2012

(In M€) Revenues Op. Margin % Revenues Op. Margin % Revenues Op. Margin %

North America

France

UK & Ireland

Benelux

Rest of Europe, Asia & Latin

America

Not allocated (1)

869

1 039

987

642

1 219

-

70

79

61

40

72

- 33

8.1%

7.6%

6.1%

6.2%

5.9%

-

936

1 099

958

624

1 320

-

89

108

78

54

130

- 35

9.5%

9.8%

8.2%

8.7%

9.8%

-

1 041

1 116

1 069

576

1 348

-

90

69

73

26

104

- 34

8.7%

6.2%

6.8%

4.5%

7.7%

-

TOTAL 4 756 289 6.1% 4 937 424 8.6% 5 150 328 6.4%

At current rates and perimeter

(1) Items not allocated correspond to headquarters’ expenses

Operating Margin by Main Geography

NA FR UK BNL ROW

8,1% 7,6%

6,1% 6,2% 5,9%

8,7%

6,2% 6,8%

4,5%

7,7%

H1 11 H1 12

2012 Half Year Results

33 Copyright © Capgemini 2012. All Rights Reserved

(in M€) H1 2011 H1 2012

Operating Margin 289 328

Other operating expenses - 49 - 91

of which Restructuring costs

Stock options and performance shares

-32 - 9

-75 - 7

Net financial expense - 51 - 49

Income tax expense - 70 - 55

Share of profit of associates - - 1

Non-controlling interests 8 11

Net Profit (Group share) 127 143

Normalized Net Profit (Group share) (*) 158 211

Earnings per share as of June 30 (non diluted) – in €

Normalized Net Profit per share at June 30 (non diluted) – in €

0.82

1.03

0.92

1.37

Net Profit Analysis

(*) Normalized net profit (Group share) equal Net profit (Group share) corrected for the impact of restructurings costs and amortization of

intangible assets acquired through business combination, net of tax.

2012 Half Year Results

34 Copyright © Capgemini 2012. All Rights Reserved

(in M€) H1 2011 H1 2012

Interest on bonds (29) (32)

Other interest expenses (10) (9)

Income from cash and cash equivalents 13 12

Net finance costs (26) (29)

Other financial income Other financial expenses

22 (47)

30 (50)

Net financial expense (51) (49)

Net Financial Expense

2012 Half Year Results

35 Copyright © Capgemini 2012. All Rights Reserved

(in M€) H1 2011 H1 2012

Current income tax (45) (56)

Tax payable on profit (23) (32)

Tax not based on taxable income (22) (24)

Deferred income tax (25) 1

Tax losses

• Net utilization of deferred tax assets on tax losses (30) (24)

France (26) (19)

Other regions (4) (5)

• Net reassessment of deferred tax assets on tax losses 18 13

Temporary differences and reassessments of deferred tax assets (13) 12

INCOME TAX EXPENSE (70) (55)

Effective tax rate 37.2% 29.6%

Income Tax Expense

2012 Half Year Results

36 Copyright © Capgemini 2012. All Rights Reserved

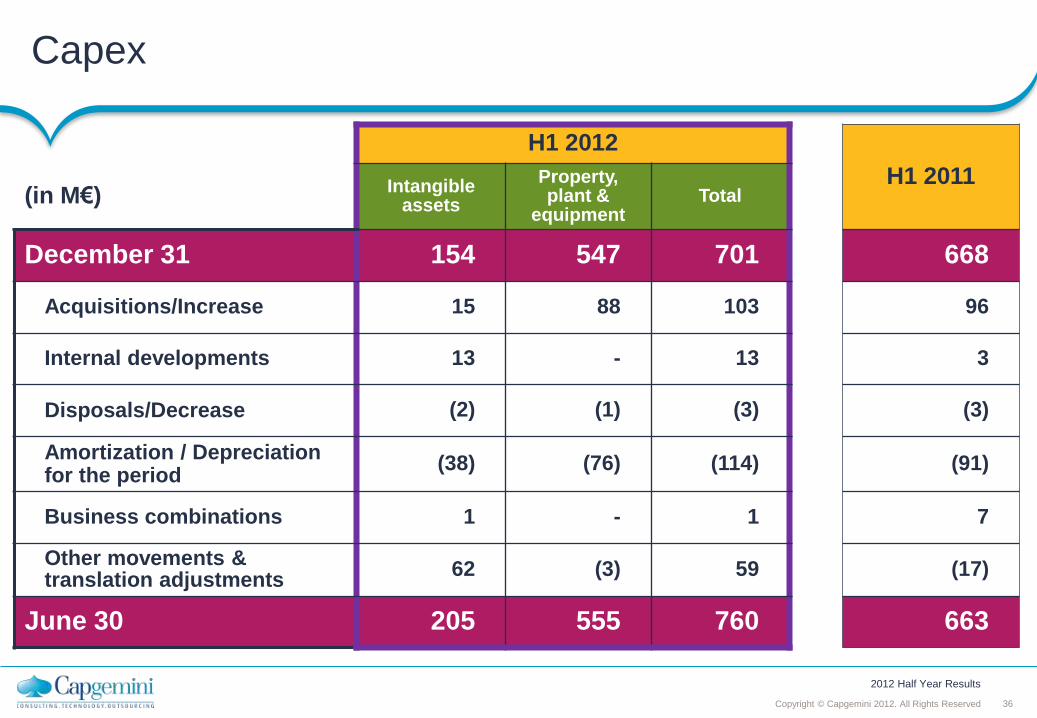

H1 2012

H1 2011 (in M€) Intangible

assets

Property, plant &

equipment Total

December 31 154 547 701 668

Acquisitions/Increase 15 88 103 96

Internal developments 13 - 13 3

Disposals/Decrease (2) (1) (3) (3)

Amortization / Depreciation for the period

(38) (76) (114) (91)

Business combinations 1 - 1 7

Other movements & translation adjustments

62 (3) 59 (17)

June 30 205 555 760 663

Capex

2012 Half Year Results

37 Copyright © Capgemini 2012. All Rights Reserved

289 164 77 -329 -39 -42 -607 -21 -68 -151 H1

2011

Compa-

rable

-104

Net Cash Evolution

-31 -32

Cash net of Debt

Opening

YtD Operat. margin

YtD Bonus

provision

Amorti- zation and

provisions

Bonus Payment For last

year

Payment of

Restruc- turing

Tax paid

Other working capital

evolution

Acqui- sitions

Cash Net of Debt Closing

Net interest

CAPEX, Net of

disposals

Increase in

Capital from minority

interests

Exchange rates diff.

Cash net of debt bef. investing

and financial activities

(in M€)

Dividends &

Treasury shares

Debt increase & others

1 063

68 454

328

182

84

336

72

84

289

21

101

145

50 149

17

-187M€ cash flows from operating

activities vs -487M€ in H1 2011

-309M€ free cash flows vs -576M€ in H1 2011 4 2

0

27

2012 Half Year Results

38 Copyright © Capgemini 2012. All Rights Reserved

Organic Free cash flow generation

Back to normal seasonality of FCF in H1 2012

-309 M€ in H1 2012,

vs -576 M€ in H1 2011,

and -319 M€ in H1 2010

-800

-600

-400

-200

0

200

400

600

800

1000

H1 2010 H2 2010 H1 2011 H2 2011 H1 2012

2012 Half Year Results

39 Copyright © Capgemini 2012. All Rights Reserved

One of the best revenue into collection conversion in recent years. DSO has been improving following action plans launched in H2 2011… without penalizing further our suppliers

H1 2008 H1 2009 H1 2010 H1 2011 H1 2012

Revenue

Conversion 110.7% 114.2% 106.3% 107.4% 112.8%

DSO 73 70 79 80 76

Supplier days 108 103 120 111 105

2012 Half Year Results

40 Copyright © Capgemini 2012. All Rights Reserved

Back up

2012 Half Year Results

41 Copyright © Capgemini 2012. All Rights Reserved

2 350

2 4062 378

2 559 2 565 2 585

1 800

2 000

2 200

2 400

2 600

Q1 11 Q2 11 Q3 11 Q4 11 Q1 12 Q2 12

Q1 2011 Q2 2011 H1 2011 Q3 2011 Q4 2011 H2 2011 FY 2011 Q1 2012 Q2 2012 H1 2012

In M€ (Published) 2 350 2 406 4 756 2 378 2 559 4 937 9 693 2 565 2 585 5 150

Sequential Current Growth 2.4 % - 1.2 % 7.6 % 0.3 % 0.8 % 4.3 %

Sequential Organic Growth 4.1 % - 4.3 % 6.2 % - 1.3 % 0.2 % 1.6 %

Year-on-Year Current Growth 9.2 % 7.4 % 8.3 %

Year-on-Year Organic Growth 4.3 % 0.4% 2.3%

(in M€)

Revenues Quarterly Evolution

2012 Half Year Results

42 Copyright © Capgemini 2012. All Rights Reserved

Current Current Organic

Q2 2011 Q1 2012 Q2 2012

Sequential Year on year Sequential Year on year

(in M€) Q2 12/

Q1 12

Q2 12/

Q2 11

Q2 12/

Q1 12

Q2 12/

Q2 11

North America 445 505 536 6.1% 20.2% 4.3% 7.2%

Europe and Asia

of which : 1 961 2 060 2 049 - 0.5% 4.5% - 0.9% - 1.2%

UK & Ireland 508 510 559 9.5% 9.9% 6.3% 0.9%

France 515 578 538 - 7.1% 4.5% - 7.1% - 4.3%

Benelux 319 298 278 - 6.9% - 12.9% - 6.9% - 13.0%

Southern Europe & Latin America

236 246 241 - 1.5% 2.2% 1.1% - 2.7%

Nordic 161 181 182 0.9% 13.7% 1.2% 11.8%

Germany & Central Europe

155 169 163 - 3.4% 5.0% -3.4% 4.8%

Asia Pacific 67 78 88 13.2% 32.5% 14.7% 21.5%

TOTAL 2 406 2 565 2 585 0.8% 7.4% 0.2% 0.4%

Q2 2012 Revenues by Geography

2012 Half Year Results

43 Copyright © Capgemini 2012. All Rights Reserved

Current Current Organic

H1 2011 H2 2011 H1 2012

Sequential Year on year Sequential Year on year

(in M€) H1 12 /

H2 11

H1 12 /

H1 11

H1 12 /

H2 11

H1 12 /

H1 11

North America 869 936 1 041 11.3% 19.7% 4.5% 9.7%

Europe and Asia

of which : 3 887 4 001 4 109 2.7% 5.7% 0.9% 0.6%

France 1 039 1 099 1 116 1.6% 7.4% 2.0% - 1.6%

UK & Ireland 987 958 1 069 11.6% 8.3% 5.8% 2.3%

Benelux 642 624 576 - 7.6% -10.3% - 7.7% - 10.4%

Southern Europe & Latin America

461 539 487 -9.7% 5.6% - 10.9% - 0.1%

Nordic 319 316 363 14.7% 14.0% 12.5% 12.4%

Germany & Central Europe

312 314 332 5.7% 6.2% 5.5% 5.9%

Asia Pacific 127 151 166 10.0% 31.0% 4.6% 19.8%

TOTAL 4 756 4 937 5 150 4.3% 8.3% 1.6% 2.3%

H1 2012 Revenues by Geography

2012 Half Year Results

44 Copyright © Capgemini 2012. All Rights Reserved

Q2 Revenues by Geography

At constant rates and perimeter

Q2 2011

6,3%12,4%

6,0%

21,5%

19,5%

21,8%

2,8%

9,7%

Benelux

North

America

UK

& Ireland

Nordic

Germany

& Central

Europe

France

Southern

Europe

& Latin

America

Asia

Pacific

7,1%10,7%

6,3%

21,6%

20,8%

20,8%

3,4%

9,3%

Q2 2012

Benelux

North

America

UK

& Ireland

Nordic

Germany

& Central

Europe

France

Southern

Europe

& Latin

America

Asia

Pacific

2012 Half Year Results

45 Copyright © Capgemini 2012. All Rights Reserved

H1 Revenues by Geography

7,1%11,2%

6,3%

20,8%

20,2%

21,7%

3,2%

9,5%

At constant rates and perimeter

Benelux

North

America

UK

& Ireland

Nordic

Germany

& Central

Europe

France

Southern

Europe

& Latin

America

Asia

Pacific

H1 2011

Benelux

North

America

UK

& Ireland

Nordic

Germany

& Central

Europe

France

Southern

Europe

& Latin

America

Asia

Pacific

6,4%12,8%

6,1%

20,8%

18,9%

22,5%

2,8%

9,7%

H1 2012

2012 Half Year Results

46 Copyright © Capgemini 2012. All Rights Reserved

H1 Revenues by Discipline

5,2%

40,3%39,3%

15,2%

At constant rates and perimeter

H1 2011

39,4%

15,5%

39,8%

5,3%

Consulting

Services

Technology

Services

Local

Professional

Services

Outsourcing

Services H1 2012

Consulting

Services

Technology

Services Local

Professional

Services

Outsourcing

Services

2012 Half Year Results

47 Copyright © Capgemini 2012. All Rights Reserved

10.9%

19.0%

6.2%

23.9%

9.0%

13.7%

Energy, Utilities &

Chemicals

Financial

Services

Others

Public Sector

Telecom,

Media &

Entertainment

Customer products,

retail, distribution &

transportation

H1 Revenues by Sector

At budget rates and constant perimeter

10.5%

20.6%

4.6%

24.7% 9.2%

17.6%

Energy, Utilities &

Chemicals

Financial

Services

Others

Public Sector

Telecom,

Media &

Entertainment

12.8%

17.3% Manufacturing

Customer products,

retail, distribution &

transportation

Manufacturing

H1 2011

H1 2012

2012 Half Year Results

48 Copyright © Capgemini 2012. All Rights Reserved

June 11 Sept 11 Dec 11 Mar 12 June 12 June 12 /

June 11

June 12 /

Dec. 11

Consulting Services 3 333 3 410 3 431 3 229 3 164 - 5.1% - 7.8%

Technology Services 52 096 53 050 54 304 53 441 53 498 2.7% - 1.5%

Outsourcing Services 39 252 41 156 42 124 44 008 44 524 13.4% 5.7%

Local Professional Services 19 295 19 511 19 553 19 575 19 549 1.3% 0.0%

TOTAL GROUP* 114 274 117 428 119 707 120 542 121 026 5.9% 1.1%

* including not classified headcount

Evolution of Headcount by Business

2012 Half Year Results

49 Copyright © Capgemini 2012. All Rights Reserved

Group Headcount by Geography

UK & IRELAND :

• Opening: 8 977

• Closing: 8 985

• Change in Person: +8

• Change in %: +0.1%

Southern Europe & Latin America:

• Opening: 16 499

• Closing: 16 603

• Change in Person: +104

• Change in %: +0.6%

FRANCE :

• Opening: 21 738

• Closing: 21 529

• Change in Person: -209

• Change in %: -1.0%

BENELUX :

• Opening: 10 391

• Closing: 9 832

• Change in Person: -559

• Change in %: -5.4%

ASIA PACIFIC :

• Opening: 39 097

• Closing: 40 478

• Change in Person: +1 381

• Change in %: +3.5%

CENTRAL EUROPE :

• Opening: 8 962

• Closing: 9 295

• Change in Person: +333

• Change in %: +3.7%

TOTAL GROUP:

Opening: 119 707 Closing: 121 026 D in P: +1 319 D in %: +1.1%

NORDIC :

• Opening: 4 538

• Closing: 4 518

• Change in Person: -20

• Change in %: -0.4%

NORTH AMERICA :

• Opening: 9 505

• Closing: 9 786

• Change in Person: +281

• Change in %: +3.0%

2012 Half Year Results

50 Copyright © Capgemini 2012. All Rights Reserved

H1 2011 H2 2011 H1 2012

(in M€) Revenues Op.

Margin % Revenues

Op.

Margin % Revenues

Op.

Margin %

North America 869 70 8.1% 936 89 9.5% 1 041 90 8.7%

France 1 039 79 7.6% 1 099 108 9.8% 1 116 69 6.2%

UK & Ireland 987 61 6.1% 958 78 8.2% 1 069 73 6.8%

Benelux 642 40 6.2% 624 54 8.7% 576 26 4.5%

Southern Europe & Latin America

461 3 0.7% 539 27 4.9% 487 5 1.0%

Nordic 319 19 5.8% 316 27 8.6% 363 26 7.2%

Germany & Central Europe

312 19 6.0% 314 24 7.7% 332 30 8.9%

Asia Pacific 127 31 N/A 151 52 N/A 166 43 N/A

Not allocated (1) - - 33 - - -35 - - -34 -

TOTAL 4 756 289 6.1% 4 937 424 8.6% 5 150 328 6.4%

(1) Items not allocated correspond to headquarters’ expenses

At current rates and perimeter

Operating Margin by Geography

2012 Half Year Results

51 Copyright © Capgemini 2012. All Rights Reserved

Operating Margin Analysis by Destination

(in M€) H1 2011 H2 2011 H1 2012

Revenues 4 756 4 937 5 150

Cost of services rendered - 3 679 - 3 746 - 4 011

% of Revenues 77.3% 75.9% 77.9%

Gross Margin 1 077 1 191 1 139

% of Revenues 22.7% 24.1% 22.1%

Selling Expenses - 378 - 368 - 403

% of Revenues 8.0% 7.5 % 7.8%

General & Administrative Expenses - 410 - 399 - 408

% of Revenues 8.6% 8.1% 7.9%

Operating Margin 289 424 328

% of Revenues 6.1% 8.6% 6.4%

At current rates and perimeter

2012 Half Year Results

52 Copyright © Capgemini 2012. All Rights Reserved

(in M€) FY 2010 H1 2011 H2 2011 FY 2011 H1 2012

Restructuring costs Of which :

(71) (32) (49) (81) (75)

Workforce reduction (44) (29) (45) (74) (69)

Real estate assets streamlining (19) (1) (3) (4) (5)

Rightshoring (8) (2) (1) (3) (1)

Integration costs related to acquired companies (11) (3) (6) (9) (4)

Acquisition-related costs (4) (4) (3) (7) (1)

Expenses relating to share subscriptions, share grants and stock options

(16) (9) (8) (17) (7)

Other operating income 6 - - - -

Other operating expense (2) (1) (3) (4) (4)

Other operating income and expense (98) (49) (69) (118) (91)

Other Operating Income and Expense

2012 Half Year Results

53 Copyright © Capgemini 2012. All Rights Reserved

(In M€) H1 2011 H2 2011 H1 2012

Profit for the period Depreciation, amortization and impairment of fixed assets Net charges to provisions Gains and losses on disposals of assets Net finance costs Income tax expense Other non-cash items

119 92

(15) 7

26 70

4

270 96

(18) 6

39 31 16

132 114 (16)

2 29 55 23

Cash flows from operations before net finance costs and income tax Income tax paid Change in restructuring debt Changes in operating working capital

303

(42)

(7) (741)

440

(62)

6 452

339

(84)

5 (447)

Operating cash flows Capital expenditure (net of proceeds) Net investments Dividends paid Net proceeds/payments relating to treasury shares transactions Translation, perimeter changes & other

(487) (68)

(104) (154)

3 (84)

836 (87)

(450) -

(10) (4)

(187) (101)

(4) (154)

5 14

Change in net cash and cash equivalents (894) 285 (427)

Opening net cash and cash equivalents 1 063 169 454

Closing net cash and cash equivalents 169 454 27

Net Cash Evolution

2012 Half Year Results

54 Copyright © Capgemini 2012. All Rights Reserved

ASSETS Dec. 31, 2011

June 30, 2012 EQUITY & LIABILITIES Dec. 31,

2011 June 30,

2012

Equity (attributable to owners of the company) Non-controlling interests

4 256

27

4 072

39

Goodwill 3 768 3 762 Total equity 4 283 4 111

Intangible assets 154 205 Long-term borrowings 1 135 1 133

Property, plant & equipment 547 555 Deferred taxes 183 207

Deferred taxes 1 020 1 096 Provisions for pensions and other post-employment benefits 1 099 1 362

Other non-current assets 119 111 Non-current provisions 15 19

Other non-current liabilities 322 338

Total non-current assets 5 608 5 729 Total non-current liabilities 2 754 3 059

Accounts & notes receivable 2 685 2 959 Short-term borrowings and bank overdrafts 702 219

Income tax receivable 55 70 Accounts and notes payable 2 340 2 214

Other receivables 370 400 Advances from customers and billed in advance 661 664

Cash management assets 73 74 Current provisions 48 49

Cash and cash equivalents 2 223 1 310 Income tax payables 89 70

Other payables 137 156

Total current assets 5 406 4 813 Total current liabilities 3 977 3 372

Total Assets 11 014 10 542 Total Equity & Liabilities 11 014 10 542

(in M€)

Balance Sheet

2012 Half Year Results

55 Copyright © Capgemini 2012. All Rights Reserved

(in M€) Equity (attributable

to owners of the Company)

Non-controlling interests

Total Equity

Total equity as of January 1, 2012 4 256 27 4 283

Dividends paid out for 2011 (154) - (154)

Valuation of stock options and performance shares grants 7 - 7

Treasury shares 5 - 5

Put CPM-Braxis and change in percentage of interest (30) 25 (5)

Income and expenses recognized in equity of which :

Actuarial gains & losses on defined benefit plans Remeasurement of hedging derivatives Deferred tax related to items recognized in equity Exchange differences on translating foreign operations

(155)

(249) (10)

64 40

(2)

0 0 0

(2)

(157)

(249) (10)

64 38

Profit for the period 143 (11) 132

Total equity as of June 30, 2012 4 072 39 4 111

Equity

2012 Half Year Results

56 Copyright © Capgemini 2012. All Rights Reserved

Commitments given

• Non cancelable leases (mainly offices, vehicles, computers)

€ 823M

• Other commitments:

• Covenants on OCEANE bonds and syndicated credit facilities Compliant

• Limited financial guarantees granted to customers € 925M

• Bank guarantees granted to customers € 72M

• Other commitments € 104M

• Parent performance and/or financial guarantees provided in various large clients contracts

Off Balance Sheet Commitments as of June 30, 2012:

Off Balance Sheet Commitments

2012 Half Year Results

57 Copyright © Capgemini 2012. All Rights Reserved

Charge-out Rates (onshore)

Consulting Services Technology Services onshore

Local Professional Services

(in €)

Q1 Q2 Q2 Q4

2011 2012

Q3 Q1

At constant perimeter Q1 Q2 Q2 Q4

2011 2012

Q3 Q1

Q1 Q2 Q2 Q4

2011 2012

Q3 Q1

615629

600

631

609

622

500

600

700

479

487485

498490 492

300

400

500

1169 11791153

11861149 1160

300

400

500

600

700

800

900

1000

1100

1200

1300

2012 Half Year Results

58 Copyright © Capgemini 2012. All Rights Reserved

Offshore Leverage

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

CS APPS1 APPS2 Infra Sogeti BPO Group Total (*)

5,0%

61,4%

20,3%

43,7%

11,1%

90,5%

38,6%

6,5%

60,8%

21,4%

45,6%

13,2%

93,3%

39,7%

January 12 June 12

Offshore penetration per SBU (billable headcount)

(*) Group Total includes Emerging Markets

2012 Half Year Results

59 Copyright © Capgemini 2012. All Rights Reserved

Labor Cost Evolution Onshore

H1 11 Salary increase

Pyramid effect

FX impact Perimeter Volumes Others H1 12

2 899

84 - 2

65

2 708

- 91 68

67

2012 Half Year Results

60 Copyright © Capgemini 2012. All Rights Reserved

Labor Cost Evolution Offshore

H1 11 Salary increase

Pyramid effect FX impact Volumes Others H1 12

18

250

- 10

- 14

30

274

0

The information contained in this presentation is proprietary.

© 2012 Capgemini. All rights reserved.

www.capgemini.com

About Capgemini

With more than 120,000 people in 40 countries, Capgemini is one

of the world's foremost providers of consulting, technology and

outsourcing services. The Group reported 2011 global revenues

of EUR 9.7 billion.

Together with its clients, Capgemini creates and delivers

business and technology solutions that fit their needs and drive

the results they want. A deeply multicultural organization,

Capgemini has developed its own way of working, the

Collaborative Business ExperienceTM, and draws on Rightshore ®,

its worldwide delivery model.

Rightshore® is a trademark belonging to Capgemini