half-year 2011 results presentation - ugl limited · 2017-08-10 · half-year 2011 results...

TRANSCRIPT

Half-Year 2011 Results PresentationMonday, 21 February 2011Sofitel Wentworth, Sydney

OverviewRichard Leupen, Managing Director & CEO

3

Group Highlights

• healthy financial performance• record contributions from 3 of 4 divisions• increased interim dividend

Business Diversity Delivering

• financial flexibility• robust risk management• consistent focus - growth, market leadership,

sustainability and earnings stability

Strong Strategic Position

• near record $8.9b order book• expanding tender pipeline• market conditions generally improving

Growth Momentum Continuing

4

Financial Highlights

Operating revenue, EBIT, Tax, NPAT & EPS in this presentation refer to underlying results. A reconciliation to reported results is detailed on slide 13.

Operating revenue

Operating cash flow

NPAT

EPS

Capex

Gearing

DPS

$2.3b - up 7%

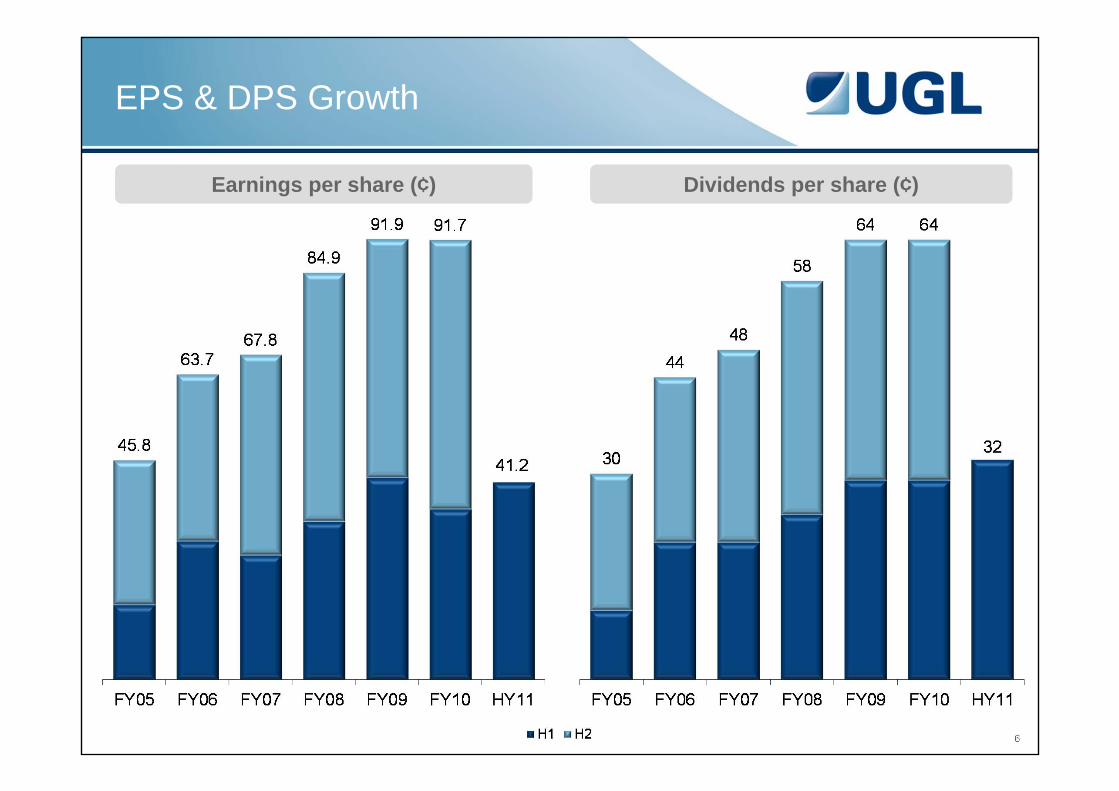

32¢ fully franked

14% flexibility for growth

$65.9m

$68.1m - up 16%

41.2¢ - up 16%

$22m low capital intensity

5

Revenue & Profit Growth

Operating Revenue Net profit after tax ($m)

6

EPS & DPS Growth

Earnings per share (¢) Dividends per share (¢)

7

Drivers for Growth

Sustainable Earnings

Market Leadership

RiskManagement

FinancialStrength

BusinessPositioning

Sector Leadership

• Balanced recurring revenues• Long term capital works alliances• Diverse earnings streams• Strong order book• Solid opportunity pipeline

• Robust systems and processes• Alliance and cost-plus contracts• Blue chip and government clients• Sensible, balanced trading terms

• People• Safety• Technology partnerships • Intellectual property • Outstanding customer service

• LNG, iron ore and coal• Transport and rail engineering• Infrastructure and

the environment• Property management

• Strong balance sheet• Low capital intensity• Robust cash flow• Flexibility to grow

• Exposure to long term growth trends• Significant market opportunities• Strong technical component• World class technology

8

-

5

10

15

20

25

30

Dec-03 Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10

Freq

uenc

y ra

te p

er m

illio

n m

an h

ours

wor

ked*

Lost time incident frequency rate Total recordable case frequency rateLTIFR Excluding US TRCFR Excluding US

Safety

*rolling 12-month average

9

Our People

Employee numbers* Breakdown by division

2,198 (5%)2,822 (6%)5,125 (12%)

33,571 (76%)266 (1%)54 (0%)

*includes contractors

8% growth

10

Divisional Overview

UGL Infrastructure

• Record half year earnings• Strong water and power performance • Ramping up on DTRS and Airport Link• Continuing opportunities in power and communications

• Record half year earnings• Strong water and power performance • Ramping up on DTRS and Airport Link• Continuing opportunities in power and communications

UGL Rail

• Strong growth in sales and earnings• Solid contribution from rolling stock• Commenced Oscar 3 deliveries• Texmaco JV signed• Improving market conditions

• Strong growth in sales and earnings• Solid contribution from rolling stock• Commenced Oscar 3 deliveries• Texmaco JV signed• Improving market conditions

UGLResources

• RGP5 project completed• Growing maintenance services• Pluto nearing completion• Aurora and Lynas contributing in second half

• RGP5 project completed• Growing maintenance services• Pluto nearing completion• Aurora and Lynas contributing in second half

UGLServices

• All regions performing well• Continued turnaround in CRE and ANZ operations• Singapore Sports Hub financial close• Business development activity strong

• All regions performing well• Continued turnaround in CRE and ANZ operations• Singapore Sports Hub financial close• Business development activity strong

Financial AnalysisRob Bonaccorso, Chief Financial Officer

12

Results Overview

Constant currency: translating results in AUD dollars at the exchange rate applicable during the prior corresponding period.

$m HY11 HY10 Change ConstantCurrency

Operating revenue 2,273.7 2,119.7 7% 10%

EBIT 104.6 91.3 15% 17%

EBIT margin 4.6% 4.3%

NPAT 68.1 58.6 16% 18%

NPAT margin 3.0% 2.8%

EPS 41.2 35.6 16% 17%

13

Reconciliation to Underlying Results

$m HY11 HY10 Change

Consolidated revenue 2,140.5 2,073.5 67.0Add: Revenue from joint ventures & associates 135.6 47.9 87.7Less: Interest income (2.4) (1.7) (0.7)Total segment revenue 2,273.7 2,119.7 154.0

EBIT 98.3 85.8 12.5Add: Amortisation of acquired intangibles 5.2 5.5 (0.3)Add: Tax on equity accounted income 1.1 - 1.1Underlying EBIT 104.6 91.3 13.3

Tax (23.0) (20.1) (2.9)Less: Tax on amortisation of acquired intangibles (2.1) (2.2) 0.1Less: Tax on equity accounted income (1.1) - (1.1)Underlying tax (26.2) (22.3) (3.9)

NPAT (attributable to owners of the company) 65.0 55.3 9.7Add: Amortisation of acquired intangibles (after tax) 3.1 3.3 (0.2)Underlying NPAT 68.1 58.6 9.5

14

Operational Report - Infrastructure

• Favourable project completions

• Order book steady

• Expanding pipeline

• Major projects supporting growth in second half

$m HY11 HY10 Change

Sales - $m 495.6 582.6 (15%)

EBIT - $m 40.3 39.0 3%

EBIT / Sales 8.1% 6.7%

Order book - $m 1,912.5 2,139.4 (11%)

EBIT $m

15

Operational Report - Rail

• Growth driven by locomotives and wagons

• Expanding freight and passenger activity

• Strong order book

• Bidding activity high

$m HY11 HY10 Change

EBIT $m

Sales - $m 638.4 556.1 15%

EBIT - $m 38.5 13.7 182%

EBIT / Sales 6.0% 2.5%

Order book - $m 3,085.0 3,164.1 (2%)

16

Operational Report - Resources

• Strong top line growth

• Major projects division impacting performance

• Asset services continues to grow

• Growing order book

• Elevated bidding activity

Sales - $m 479.7 320.3 50%

EBIT - $m 11.6 23.6 (51%)

EBIT / Sales 2.4% 7.4%

Order book - $m 868.5 741.4 17%

$m HY11 HY10 Change

EBIT $m

17

Operational Report - Services

• Sales growth 6% (constant currency)

• US, ANZ and Asia performing well

• Discretionary spend supporting margins

• FX impacting EBIT and order book

$m HY11 HY10 Change

EBIT $m

Sales - $m 667.7 673.1 (1%)

EBIT - $m 35.6 34.8 2%

EBIT / Sales 5.3% 5.2%

Order book - $m 3,054.8 2,728.7 12%

18

Operating Cash Flow

• Underlying cash realisation steady

• New projects driving working capital growth

Operating Cash flow $m

Note: Cash Realisation = Operating cash flow / NPAT add back depreciation and amortisation

EBITDA 126.3

Financing costs & Tax (33.6)

Other non-cash items 2.9

Movement in working capital (29.7)

65.9Reported cash flow from operations

19

Financial Position

• Average term 4.9 years

• No refinancing obligations until 2012

• $141m available bank capacity

20

Financial Position

• Strong financial position

• Financial flexibility

• Positioned for growth

$m HY11 FY10

Net debt 189 234

Net debt to net debt plus equity 14.3% 16.8%

Interest cover (rolling 12 months) 14.2x 11.0x

Net debt to EBITDA 0.7x 0.8x

Total assets 2,320 2,505

OutlookRichard Leupen, Managing Director & CEO

22

Order Book • Reported $8.9b• Constant Currency $9.2b

Order Book

Historic growth ($m) Order book excludes significant value

Preferred tender status $0.2b• Property services• Locomotive delivery

and maintenance

Options in existing contracts $2.8b• Rail maintenance• Property services• Locomotive orders

Recurring maintenance $6.5b• Historic renewal rate 90-95%• Value over five years• Excludes fixed term contracts

23

By year ($m)

Order Book Breakdown

By type By division

Alliance style projects $1,432m

24

Pipeline

Weighted and Qualified ($m) Status

FY08 FY09 FY10 FY11

Note: Weighted & Qualified – excludes any opportunities with a go-get less than 25%

25

New Contract Wins & Extensions

• Murrumbidgee Irrigation• North Auckland and

Northland Grid Upgrade• Western Downs to Halys

275kV powerline

UGL Infrastructure

• Oscar 3 extension• Various freight orders

- RIO, Freightliner Australia and GE• Long term locomotive service

and support programs

UGL Rail

• Asset services mechanical shutdowns

• CITIC Pacific Mining Sino Iron project

• Brockman Marillana Iron Ore FEED

UGL Resources

• Singapore Sports Hub• RTA and Foster’s• US higher education, automotive

and pharmaceutical sectors

UGL Services

$2.3b in New Wins and Extensions

26

Divisional Outlook

• Major projects supporting growth in second half

• Sector outlook steadily improving• Power, Transport and Communications

to remain resilient

UGL Infrastructure

• Freight market recovery to continue• Ongoing passenger rail demand• MTM performance improving• Maintenance markets remain healthy

UGL Rail

Order Book

27

Divisional Outlook

• Recovery anticipated across second half

• Continuing asset services growth• Bidding activity robust and expanding• Changing customer needs

• Strong business platform• US economy recovering• Energy and environment focus• Evaluating global JV opportunities

UGL Resources

UGL Services

Order Book

28

Group Outlook

• focussed strategic intent• exposure to long term trends• significant market opportunities• sector and market leadership

Strong growth opportunities

• robust systems and processes• strong financial position• blue chip and government clients • diverse earnings streams

Flexibility to grow

• majority of revenue secured• expanding order book• record pipeline of opportunities• continuing to target 10-15% NPAT growth in FY11

On-track for growth

29

Important Notice

This presentation and any oral presentation accompanying it:

• is not an offer, invitation, inducement or recommendation to purchase or subscribe for any securities in UGL Limited (“UGL”) or to retain any securities currently held;

• is for information purposes only, is in summary form and does not purport to be complete;

• is not intended to be relied upon as advice to investors or potential investors and does not take into account the investment objectives, financial situation or needs of any particular investor, potential investor or any other person. Such persons should consider seeking independent financial advice depending on their specific investment objectives, financial situation or needs when deciding if an investment is appropriate or varying any investment;

• may contain forward looking statements. Any forward looking statements are not guarantees of future performance. Any forward looking statements have been prepared on the basis of a number of assumptions which may prove to be incorrect or involve known and unknown risks, uncertainties and other factors, many of which are beyond the control of UGL, which may cause actual results, performance or achievements to differ materially from those expressed or implied in such statements. There can be no assurance that actual outcomes will not differ materially from these statements. Any forward looking statement reflects views held only as of the date of this presentation. Subject to any continuing obligations under applicable law or any relevant stock exchange listing rules, UGL does not undertake any obligation to publicly update or revise any of the forward looking statements or any change in events, conditions or circumstances on which any such statement is based.

No representation or warranty, express or implied, is made as to the fairness, accuracy, completeness or correctness of the information, opinions and conclusions contained in this presentation and any oral presentation accompanying it. To the maximum extent permitted by law, UGL and its related bodies corporate, and their respective directors, officers, employees, agents and advisers, disclaim and exclude all liability (including, without limitation, any liability arising from fault or negligence) for any loss, damage, claim, demand, cost and expense of whatever nature arising in any way out of or in connection with this presentation and any oral presentation accompanying it, including any error or omission therefrom, or otherwise arising in connection with any reliance by any person on any part of this presentation and any oral presentation accompanying it.