half year results presentation - ophir-energy.com · 11,400 boepd average daily production $102...

TRANSCRIPT

HALF YEAR RESULTS PRESENTATIONLondon, 13 September 2018

STRATEGIC PRIORITIES

2018 Half Year Results Presentation Slide 2

SUSTAINABILITY ANDFREE CASH FLOW

To drive NAV growth and returns

to shareholders

LNG ASSETS

Unlock potential value and ensure our shareholders share appropriately

in value realised

CONSOLIDATION

Evaluate opportunities that can accelerate delivery of

business objectives

MINMISE FRONTIER EXPLORATION

Focus on near field exploration

COSTS

Downsize London office* and establish an Asian HQ

*Subject to consultation

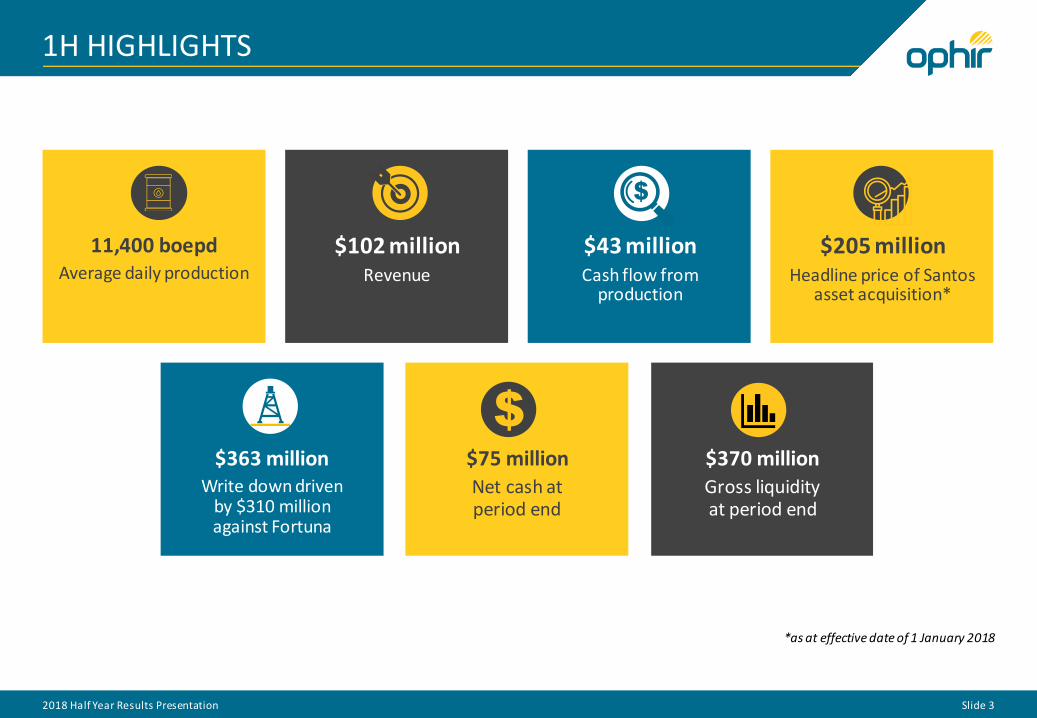

11,400 boepdAverage daily production

$102 millionRevenue

$43 millionCash flow from

production

$205 millionHeadline price of Santos

asset acquisition*

1H HIGHLIGHTS

2018 Half Year Results Presentation Slide 3

$363 millionWrite down driven

by $310 million against Fortuna

$75 millionNet cash at period end

$370 millionGross liquidity at period end

*as at effective date of 1 January 2018

First step towards reaching goal of material free cash generation

SANTOS ACQUISITION

Key metrics

• Production up 18.5% against forecast at acquisition

• Cash flow up 36% against forecast at acquisition

• Recovered 30% of acquisition costs already

• Payback reduced by 6 months

• $13 million per annum of synergies

65

72

60

62

64

66

68

70

72

74

At acquisition Average YTD

$ p

er

bb

l

Oil Price

13,500

16,000

12,000

14,000

16,000

At acquisition Actual

Bo

ep

d

1H Production

45

61

0

10

20

30

40

50

60

70

At acquisition On completion

$ m

illio

ns

Cash flow YTD

36

30

2728293031323334353637

At acquisition On completion

Mo

nth

s

Payback

2018 Half Year Results Presentation Slide 4

Deal rationale

• Further grow and diversify production base

• Increase cash generative base of business

• Move closer to financial sustainability

Forward plan to maximise value creation

ACQUIRED ASSETS

2018 Half Year Results Presentation Slide 5

Madura Offshore/Sampang, Indonesia

• HSE- Continue safe production operations

• Incremental reserves growth- Paus Biru-1 exploration well - Review/sanction Meliwis FID

• Longer term upside

- Negotiate licence extensions

- Enable delivery of longer term near field exploration strategy

Block 12W

• Continue to build relationship with PetroVietnam

• Maximise value creation from assets- Further strengthen relationship with operator (Premier) and JV

- Ensure active contribution to technical and commercial discussions

Synergies

• Combine Indonesian offices, generate at least $13 million per annum of synergies*- Appointed a new Indonesian GM, Pak Tenny Wibowo (ex-Santos)*- Opportunity to high grade the team in Indonesia

*subject to regulator approval

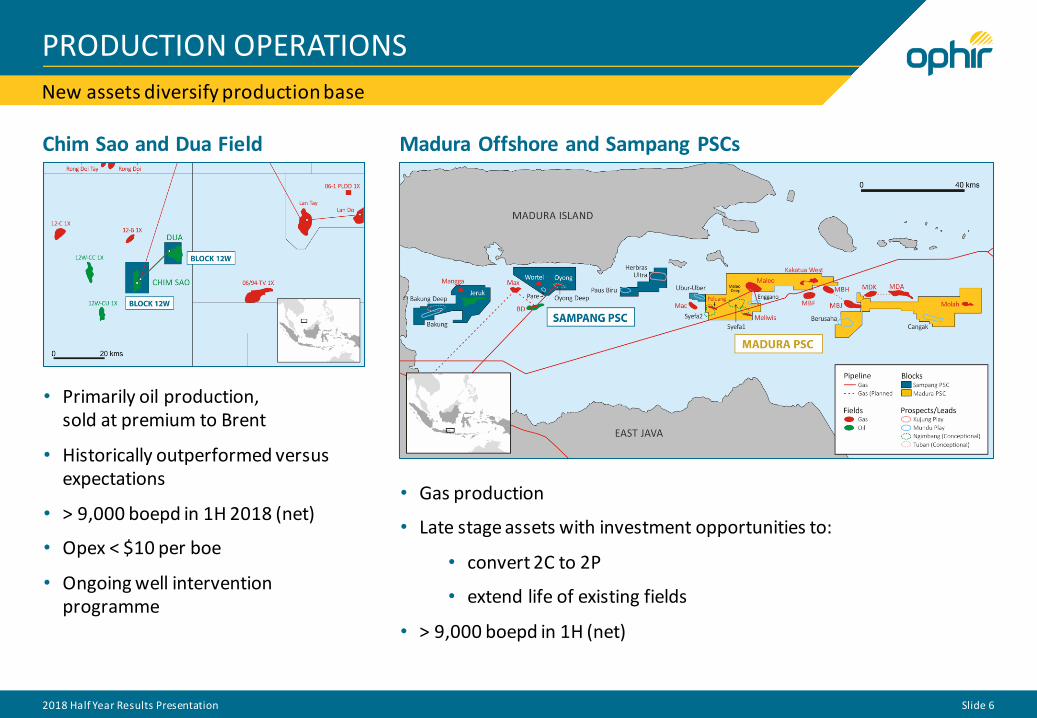

New assets diversify production base

PRODUCTION OPERATIONS

2018 Half Year Results Presentation Slide 6

Madura Offshore and Sampang PSCs

• Primarily oil production, sold at premium to Brent

• Historically outperformed versus expectations

• > 9,000 boepd in 1H 2018 (net)

• Opex < $10 per boe

• Ongoing well intervention programme

• Gas production

• Late stage assets with investment opportunities to:

• convert 2C to 2P

• extend life of existing fields

• > 9,000 boepd in 1H (net)

Chim Sao and Dua Field

Existing assets performing in line with expectations

PRODUCTION OPERATIONS

Bualuang Field Kerendan field

2018 Half Year Results Presentation Slide 7

• Reliable production asset

• 7,800 bopd during 1H

• Opex ~ $13 / bopd

• Development drilling in 2H 2018 to increase production to over 9,000 bopd

• New platform with 12 new slots to be installed in 2019 driving production up to over 11,000 bopd

• Stable production under GSA 1 at 17.5 MMsfcd

• Opex ~ $13 / boepd

• 3D seismic acquired in 2017 highlights material upside potential which could support new routes to market

• Commenced negotiations for GSA 2 to monetise next phase of contingent resource

High value barrels, rapid payback

BUALUANG PHASE 4

Slide 8

Project Scope

• A third platform (Charlie) with 12 slots

• Expansion of water disposal to 100k bwpd

• Additional crude fired power generation capacity

• Additional water disposal well on Bravo platform

• 10 slots allocated in the Phase 4 development phase

• 2 slots for near field exploration success or additional contingent resources

Progress Report

• Brownfield work has commenced offshore Construction work onshore has commenced

- schedule for installation and hook up in June 2019

• Total capex of $138 MM

• Development drilling from July 2019

• First oil in October 2019

Charlie platform and associated brownfield

modifications

2018 Half Year Results Presentation

IRR > 40%Payback within 18 months

T2.6 Depth Map Original Velocity Solution

T2.6 Reservoir

Closure above OWC

Revised depth solution has potential to

bring

North Bualuang into

main field closure above

OWC

B8/38 Bualuang North Prospect

EXPLORATION: NEAR FIELD THE FOCUS

2018 Half Year Results Presentation Slide 9

• Step-out well 5km north of Bualuang platforms

• Targeting reservoirs already producing in main field

• Well cost US$4.8MM on a dry hole basis (US$1.5 million post-tax)

• Spud October 2018

• Pmean STOIIP 36.7 MMSTB with 50% GPOS

• Development drilling in mid-2020 at end ofCharlie drilling programme

• First oil Q3 2020

Kerendan Gas Field

B8/38 OPHIR 100%

BualuangOil Field

Bualuang North Prospect

T2.6 Depth Map Revised Velocity Solution

T2.6 Reservoir

Closure above OWC

with revised velocity

model

FORWARD PRODUCTION PROFILE

Slide 10

0

20000

40000

2017 2018 2019 2020

Production Profile*

Base case Upside

Current investment programme delivers 25,000 boepd in 2019/2020

Delivery of risked upside could drive production over 25,000 boepd

Upside opportunities include:

• Bualuang Phase 5

• Bualuang North

• Kerendan Phases 2 and 3

• Meliwis development

• Paus Biru nearfield exploration

2018 Half Year Results Presentation

*2018 numbers on a pro-forma basis from effective date of 1 January 2018

HALF YEAR FINANCIAL SUMMARY

2018 Half Year Results Presentation Slide 11

Units HY 2018 HY 2017 COMMENTS

NET SOURCES OF FUNDS:

Revenue (including hedges) $’millions 102.1 88.3 ― Bualuang $67/bbl (HY17: $50/bbl) and Kerendan $5.43/Mscf (HY17: $5.23/Mscf)

Kerendan take-or-pay $’millions (0.1) 2.0 ―

Cost of production (operating expenses, royalty and inventories)

$’millions (30.5) (36.0) ― Unit opex $11/boe (HY17: $12/boe)

Investment Income $’millions 1.8 2.6 ― Net income from Sinphuhorm $2m (HY17: $3m)

Income Tax Charge $’millions (30.4) (17.0) ― Increase in SRB (lower capex) and higher revenue from Bualuang

Total net sources of funds from production

$ ‘millions 42.9 39.9 ― Income from production $23/boe (HY17: $21/boe)

NET USES OF FUNDS:

Capex (including pre-licence costs)(1) $’millions 49.7 45.4 ― Exploration $35m (HY17: $26m) and P&D $14m (HY17: $19m)

Net administration cost $’millions 6.5 5.8 ― Minimising corporate cost base - gross reduction of 60% in three years

Net finance costs $’millions 6.5 7.0 ― Interest in 1H18 only relates to NOK bond. 1H 17 included old RBL

Total net uses of funds $’millions 62.7 58.2 ―

FINANCING:

Closing net cash $’millions 75.3 129.9 ― Net cash outlay $42m (HY17: $30m)

Closing borrowings $’millions 104.7 106.6 ―

Undrawn facilities $’millions 190.7 177.5 Available facility of $191m (YE17: $204m; HY17: $178m)

Closing gross liquidity $’millions 370.7 414.0 ― Total liquidity with undrawn RBL $371m (YE17: $427m, HY17: $414m)

Note 1 - capex is adjusted to eliminate non-cash movements for decommissioning of $0.5m (HY17: $0.5m)

Focus on delivering free cash flow

2018 GUIDANCE

2018 Half Year Results Presentation Slide 12

Production: 27,500 boepd*

Fund flow from production: $210 million*

2018 Hedging Programme

• Purchased swap at average of $60/bbl for 3,200 bpd

• Purchased call at average of $68/bbl for 3,200 bpd

• Post 6 Sept additional hedging includes

- Swap at average of $70/bbl for 2,000 bpd

- Call at an average of $78/bbl for 2,000 bpd

Capital expenditure: $145 million*

• Bualuang Phase 4: $45 million

• Mexico exploration: $24 million

• Kerendan civil works & water wells: $10 million

• New Asian assets: $25 million

Net debt: $110 million

Gross liquidity: $260 million

*on a pro-forma basis for Santos assets from effective date of 1.1.18

Net Operating Cash Flow 41%

Operating Costs 24%

Royalty 5%

Taxation 28%

Administration 2%

REVENUE (BRENT ASSUMPTION: $73/BBL)

CAPITAL EXPENDITURE (EXCLUDING ACQUISITION COSTS)

Exploration 46%

Pre-development 8%

Production 45%

Investment Fortuna 1%

Strong balance sheet, low cost sustainable production and limited commitments

FREE CASH GENERATING ASIAN PRODUCTION BASE

2018 Half Year Results Presentation Slide 13

Significant cash position & liquidity• Closing net cash $75 million; Liquidity $371 million

• $130 million Bridge facility to be rolled into RBL

• Planned refinance of Nordic bond

Robust operating cash flow from high margin assets• Solid production base generating c. $300 million free

cash flow p.a, post investment, between 2019-2021

Funded work programme for next few years

• Focus on investing in existing assets to grow production and cash flow

• Reduce balance sheet exposure to frontier exploration

• Up to $150 million investment into Fortuna (not assumed in current forecast)

$50/bbl

$50/bbl $50/bbl

$60/bbl

$60/bbl$60/bbl

$70/bbl

$70/bbl

$70/bbl

$0m

$100m

$200m

Op Cash Flow(1) P&DCapex (2)

Op Cash Flow(1) P&DCapex

Op Cash Flow(1) P&DCapex

2018 2019 2020

Investment Capex Maintenance Capex

Note 1 - Operating cash flow before working adjustmentsNote 2 - Pre-acquisition expenditure

Cash flow v P&D capex forecast

OUTLOOK

Slide 14

Asia will become the hub of our operations

Expanding productionbase

Monetise LNG assets

Reducing exposure to frontier exploration

Generating free cash flow

2018 Half Year Results Presentation

For further information contact:

Head of IR and Corporate [email protected]

Geoff Callow

Level 4123 Victoria StreetLondon SW1E 6DEUNITED KINGDOM

Tel: +44 (0)29 7811 2400Fax: +44 (0)20 7811 2421

Slide 15