hardman & co€¢rhetoric to target value/recovery investors corporate reporting ......

TRANSCRIPT

YOUR LOGO

Hardman & Co

Independent Equity Advice

Client Presentation

Contents

3. How companies fail to attract long-term investors

4. Three examples of how not to attract long-term investors

5. The competition for equity capital

6. How Hardman & Co add value

7. Client breakdown

8. Growth clients:8. What to expect

9. How to measure us

10. Value/recovery clients10. What to expect

11. How to measure us

12. Pre IPO Clients12. What to expect

13. How to measure us

15. Example of where IEA made a difference

17. Hardman Independent Equity Advice

18. Credentials

20. The Hardman & Co Team

21. Disclaimer

Page 2

Page 3

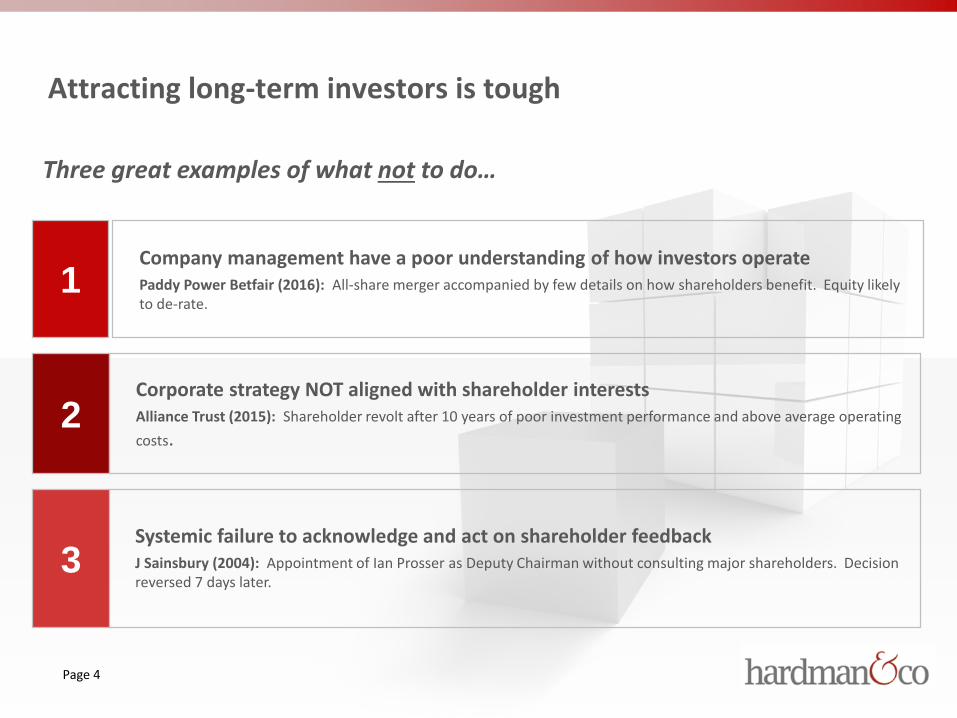

Attracting long-term investors is tough

Companies fail to attract long-term investors because…

Company management have a poor understanding of how investors operate“It takes 20 years to build a reputation and five minutes to ruin it. If you think about that, you'll do things

differently.”

Warren Buffet

Systemic failure to acknowledge and act on shareholder feedback“There should be a dialogue with shareholders based on the mutual understanding of objectives. The board as

a whole has responsibility for ensuring that a satisfactory dialogue with shareholders takes place.”

FCA Corporate Governance Code

1

2

3

Corporate Strategy NOT aligned with shareholder interests“A company’s track record has to be delivered with integrity so that a trusting relationship between investor

and investee can be established….”

QCA Investor Survey 2016

Page 4

Attracting long-term investors is tough

Company management have a poor understanding of how investors operatePaddy Power Betfair (2016): All-share merger accompanied by few details on how shareholders benefit. Equity likely to de-rate.

Systemic failure to acknowledge and act on shareholder feedbackJ Sainsbury (2004): Appointment of Ian Prosser as Deputy Chairman without consulting major shareholders. Decision reversed 7 days later.

1

2

3

Corporate strategy NOT aligned with shareholder interestsAlliance Trust (2015): Shareholder revolt after 10 years of poor investment performance and above average operating

costs.

Three great examples of what not to do…

Page 5

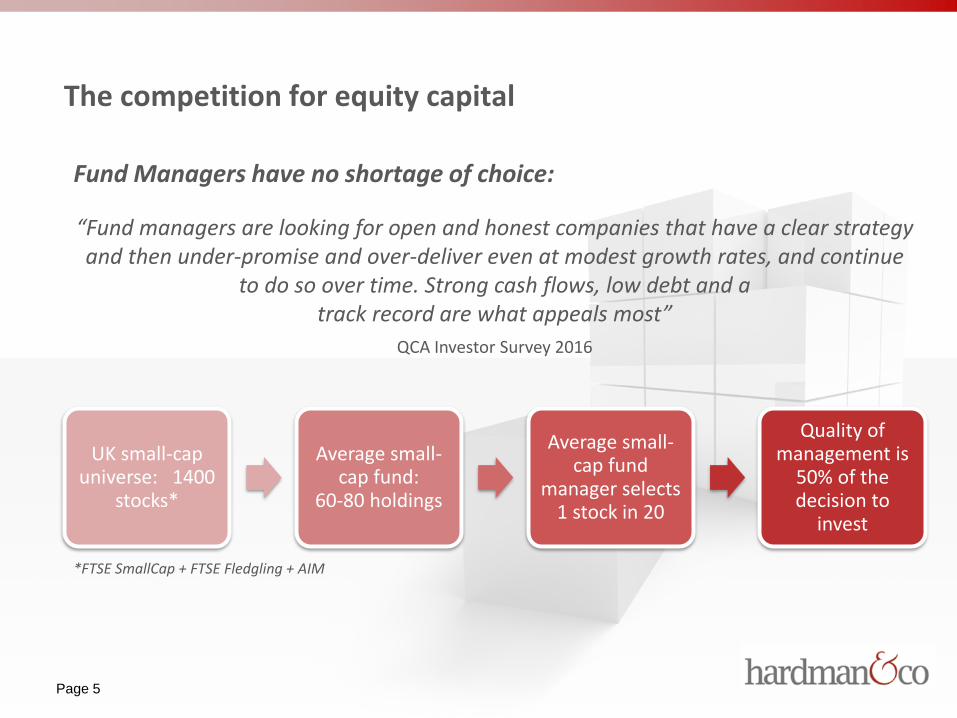

The competition for equity capital

UK small-cap universe: 1400

stocks*

Average small-cap fund:

60-80 holdings

Average small-cap fund

manager selects 1 stock in 20

Quality of management is

50% of the decision to

invest

“Fund managers are looking for open and honest companies that have a clear strategy and then under-promise and over-deliver even at modest growth rates, and continue

to do so over time. Strong cash flows, low debt and a track record are what appeals most”

QCA Investor Survey 2016

*FTSE SmallCap + FTSE Fledgling + AIM

Fund Managers have no shortage of choice:

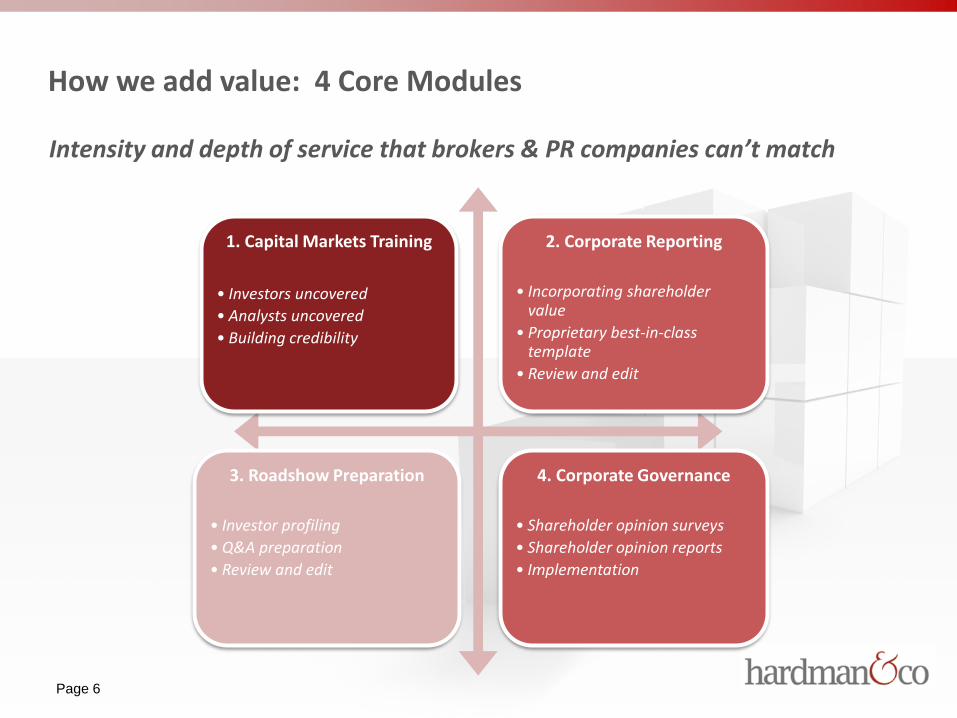

1. Capital Markets Training

• Investors uncovered

• Analysts uncovered

• Building credibility

2. Corporate Reporting

• Incorporating shareholder value

• Proprietary best-in-class template

• Review and edit

3. Roadshow Preparation

• Investor profiling

• Q&A preparation

• Review and edit

4. Corporate Governance

• Shareholder opinion surveys

• Shareholder opinion reports

• Implementation

Intensity and depth of service that brokers & PR companies can’t match

How we add value: 4 Core Modules

Page 6

Client breakdown

Growth

Pre-IPO

Value/ Recovery

Our clients typically fall into one of three categories

Page 7

Growth clients

Page 8

What to expect…

• Bespoke education sessions for CEO and CFO

• Focus on targets, shareholder value & ‘growth traps’ Capital Markets Training

• Results reported using best-in-class template

• Results demonstrate progress on targets Corporate Reporting

• We help roadshow organisers target suitable investors

• ‘Devil’s advocate’ Q&A ahead of investor meetingsRoadshow Preparation

• Independent & comprehensive shareholder opinion surveys

• Conducted at your request & presented to wider boardCorporate Governance

Growth clients

Page 9

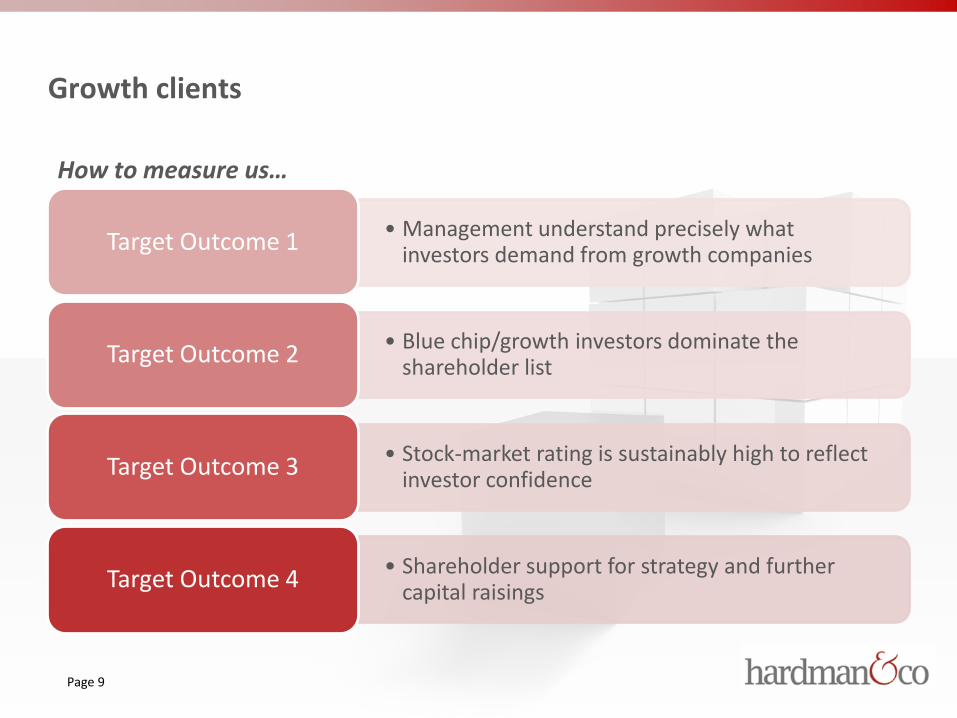

How to measure us…

• Management understand precisely what investors demand from growth companies

Target Outcome 1

• Blue chip/growth investors dominate the shareholder list

Target Outcome 2

• Stock-market rating is sustainably high to reflect investor confidence

Target Outcome 3

• Shareholder support for strategy and further capital raisings

Target Outcome 4

Value/Recovery clients

Page 10

What to expect…

• Bespoke education sessions for CEO and CFO

• Focus on the DNA of value investors Capital Markets Training

• Results reported using best-in-class template

• Rhetoric to target value/recovery investors Corporate Reporting

• We help roadshow organisers target suitable investors

• ‘Devil’s advocate’ Q&A ahead of investor meetingsRoadshow Preparation

• Independent & comprehensive shareholder opinion surveys

• Conducted at your request & presented to wider boardCorporate Governance

Value/Recovery clients

Page 11

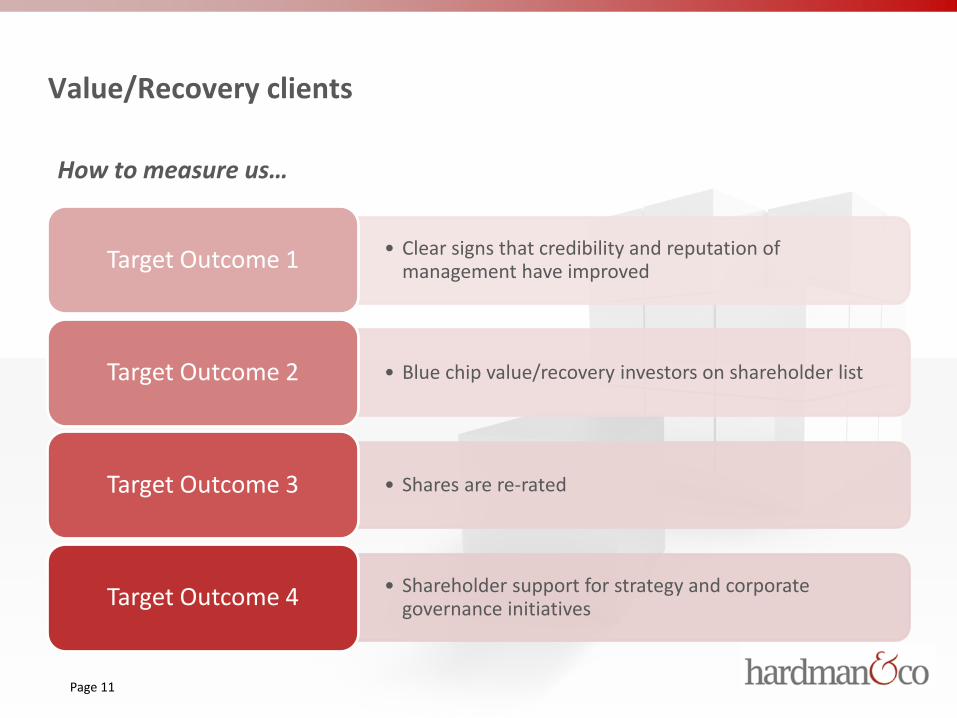

How to measure us…

• Clear signs that credibility and reputation of management have improved Target Outcome 1

• Blue chip value/recovery investors on shareholder listTarget Outcome 2

• Shares are re-ratedTarget Outcome 3

• Shareholder support for strategy and corporate governance initiativesTarget Outcome 4

Pre-IPO clients

What to expect…

• Bespoke education sessions for CEO and CFO

• Focus on the spectrum of IPO subscribers Capital Markets Training

• 1st plc results reported using best-in-class template

• Rhetoric is consistent with IPO investment case Corporate Reporting

• Independent input into IPO roster

• Continual support including ‘Devil’s advocate’ Q&A sessionsRoadshow Preparation

• Independent & comprehensive shareholder survey

• Conducted at your request & presented to wider boardCorporate Governance

Page 12

Pre-IPO clients

How to measure us…

• Management quickly build credibility during investor meetings Target Outcome 1

• Post-IPO interest generated in shares Target Outcome 2

• High quality IPO book Target Outcome 3

• Post-IPO share stability

• Shareholder support for strategic initiativesTarget Outcome 4

Page 13

Pre-IPO clients

IEA service covers BOTH pre-IPO and post-IPO periods

Buy-side experience: A huge advantage

• 17 years’ experience investing in IPOs

• 17 years’ experience rejecting IPOs!

12-month structured program

• Pre-IPO period

• Issuing period

• Post-IPO period

100% independent service

• Commissioned only by corporate client

• No conflicts of interest

Page 14

Shareholder additions since IEA appointed (Oct 2010)

Aviva, Henderson, JO Hambro, Schroders, Utilico,

IEA appointedroadshow

Legal challenge M&A New CEO

Minor profit warning

Augean plc – AIM listed waste management company – share price

Example where IEA made a difference

Page 15

The problem

IEA appointed

Ongoing IEA input

The difference

Small market cap (£30m) and low valuation (P/BV=0.5x) Discontented and transient shareholder base Long history of shareholder value destruction

Training programme designed & implemented for CEO and FD (Module 1) Corporate results reviewed & edited prior to release (Module 2) Management prep’d for investor roadshow (Module 3)

Buy-side appraisal of capital investments (Module 1) Training programme designed for new CEO and new FD (Module 1) Shareholder opinion feedback and advice (Module 4)

Share price doubled over 5 years Shareholder list now dominated by quality long-term names Exceptional management credibility with investors and analysts

Augean plc – AIM listed waste management company – IEA process

Example where IEA made a difference

Page 16

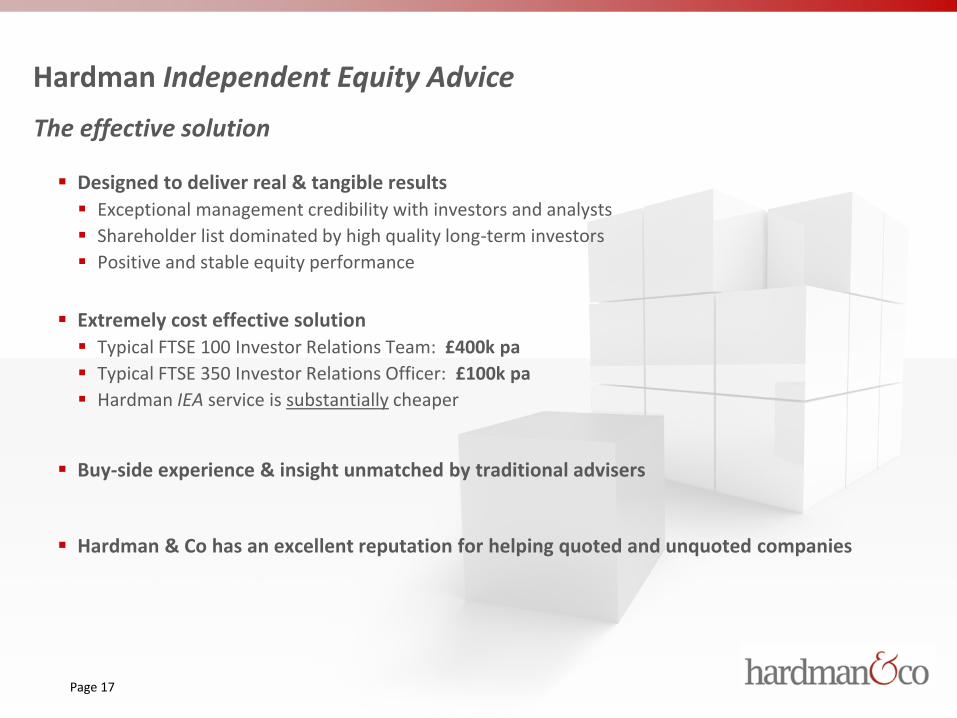

Designed to deliver real & tangible results

Exceptional management credibility with investors and analysts

Shareholder list dominated by high quality long-term investors

Positive and stable equity performance

Extremely cost effective solution

Typical FTSE 100 Investor Relations Team: £400k pa

Typical FTSE 350 Investor Relations Officer: £100k pa

Hardman IEA service is substantially cheaper

Buy-side experience & insight unmatched by traditional advisers

Hardman & Co has an excellent reputation for helping quoted and unquoted companies

Hardman Independent Equity Advice

Page 17

The effective solution

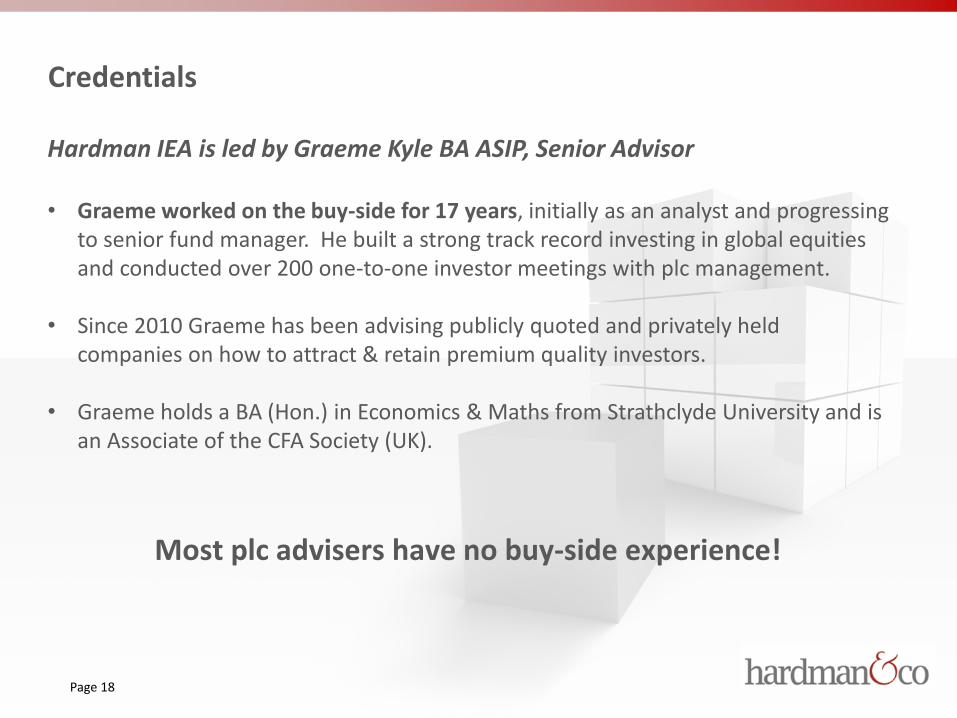

Hardman IEA is led by Graeme Kyle BA ASIP, Senior Advisor

• Graeme worked on the buy-side for 17 years, initially as an analyst and progressing to senior fund manager. He built a strong track record investing in global equities and conducted over 200 one-to-one investor meetings with plc management.

• Since 2010 Graeme has been advising publicly quoted and privately held companies on how to attract & retain premium quality investors.

• Graeme holds a BA (Hon.) in Economics & Maths from Strathclyde University and is an Associate of the CFA Society (UK).

Most plc advisers have no buy-side experience!

Credentials

Page 18

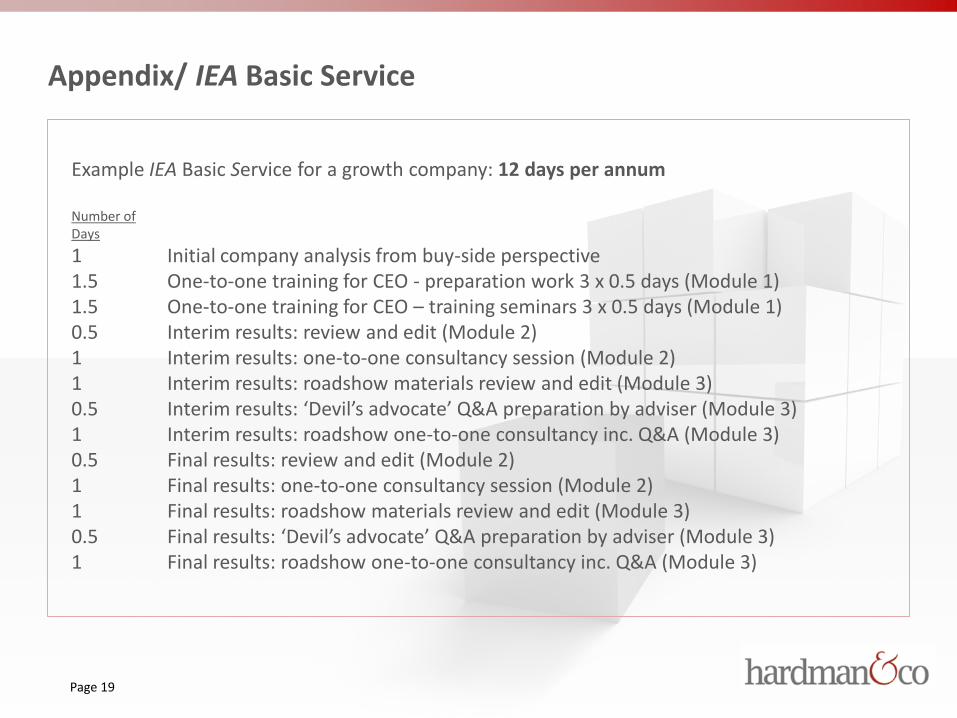

Example IEA Basic Service for a growth company: 12 days per annum

Number ofDays

1 Initial company analysis from buy-side perspective 1.5 One-to-one training for CEO - preparation work 3 x 0.5 days (Module 1)1.5 One-to-one training for CEO – training seminars 3 x 0.5 days (Module 1)0.5 Interim results: review and edit (Module 2)1 Interim results: one-to-one consultancy session (Module 2)1 Interim results: roadshow materials review and edit (Module 3)0.5 Interim results: ‘Devil’s advocate’ Q&A preparation by adviser (Module 3)1 Interim results: roadshow one-to-one consultancy inc. Q&A (Module 3)0.5 Final results: review and edit (Module 2)1 Final results: one-to-one consultancy session (Module 2)1 Final results: roadshow materials review and edit (Module 3)0.5 Final results: ‘Devil’s advocate’ Q&A preparation by adviser (Module 3)1 Final results: roadshow one-to-one consultancy inc. Q&A (Module 3)

Appendix/ IEA Basic Service

Page 19

Page 20

Management Team+44 (0)20 7929 3399John Holmes [email protected] +44 (0)207 148 0543 ChairmanKeith Hiscock [email protected] +44 (0)207 148 0544 CEO

Marketing / Investor Engagement+44 (0)20 7929 3399Richard Angus [email protected] +44 (0)207 148 0548Max Davey [email protected] +44 (0)207 148 0540Antony Gifford [email protected] +44 (0)7539 947 917Neil Pidgeon [email protected] +44 (0)207 148 0504Vilma Pabilionyte [email protected] +44 (0)207 148 0546

Analysts+44 (0)20 7929 3399Agriculture BondsDoug Hawkins [email protected] Brian Moretta [email protected]

Yingheng Chen [email protected]

Meghan Sapp [email protected]

Building & Construction Consumer & LeisureTony Williams [email protected] Mike Foster [email protected] Foster [email protected] Steve Clapham [email protected]

Financials Life SciencesBrian Moretta [email protected] Martin Hall [email protected] Thomas [email protected] Gregoire Pave [email protected]

Media MiningDerek Terrington [email protected] Ian Falconer [email protected]

Oil & Gas PropertyStephen Thomas [email protected] Mike Foster [email protected] Parfitt [email protected]

Services Special SituationsMike Foster [email protected] Steve Clapham [email protected]

Paul Singer [email protected]

Technology UtilitiesMike Foster [email protected] Nigel Hawkins [email protected]

The Hardman & Co Team

Page 21

Disclaimer

Hardman & Co provides professional independent research services. Whilst every reasonable effort has been made to ensure that the information in the research is correct, this cannot be guaranteed.

The research reflects the objective views of the analysts named on the front page. However, the companies or funds covered in this research may pay us a fee, commission or other remuneration in order for this research to be made available. A full list of companies or funds that have paid us for coverage within the past 12 months can be viewed at http://www.hardmanandco.com/

Hardman & Co has a personal dealing policy which debars staff and consultants from dealing in shares, bonds or other related instruments of companies which pay Hardman for any services, including research. They may be allowed to hold such securities if they were owned prior to joining Hardman or if they were held before the company appointed Hardman. In such cases sales will only be allowed in limited circumstances, generally in the two weeks following publication of figures.

Hardman & Co does not buy or sell shares, either for its own account or for other parties and neither does it undertake investment business. We may provide investment banking services to corporate clients.

Hardman & Co does not make recommendations. Accordingly, we do not publish records of our past recommendations. Where a Fair Value price is given in a research note this is the theoretical result of a study of a range of possible outcomes, and not a forecast of a likely share price. Hardman & Co may publish further notes on these securities/companies but has no scheduled commitment and may cease to follow these securities/companies without notice.

Nothing in this report should be construed as an offer, or the solicitation of an offer, to buy or sell securities by us.

This information is not tailored to your individual situation and the investment(s) covered may not be suitable for you. You should not make any investment decision without consulting a fully qualified financial adviser.

This report may not be reproduced in whole or in part without prior permission from Hardman &Co.

Hardman Research Ltd, trading as Hardman & Co, is an appointed representative of Capital Markets Strategy Ltd and is authorised and regulated by the Financial Conduct Authority (FCA) under registration number 600843. Hardman Research Ltd is registered at Companies House with number 8256259. However, the information in this research report is not FCA regulated because it does not constitute investment advice (as defined in the Financial Services and Markets Act 2000) and is provided for general information only.

Hardman & Co Research Limited (trading as Hardman & Co)

11/12 Tokenhouse Yard

London

EC2R 7AS

T +44 (0) 207 929 3399

Follow us on Twitter @HardmanandCo (Disclaimer Version 2 – Effective from August 2015)