has the west...2018/04/02 · world class global receives a$69 mil from handover of units at avant...

TRANSCRIPT

Has the westbeen forgotten?

The Jurong Lake District has seen little action in the recent en bloc cycle,but upcoming launches could offer opportunities

to ride the growth of Singapore’s second CBD. See our Cover Story on Pages 8 and 9.

PROPERTY PERSONALISED

Visit EdgeProp.sg to nd properties, research market trends and read the latest news The week of April 2, 2018 | ISSUE 824-45

MCI (P) 136/08/2017 PPS 1519/09/2012 (022805)

New LaunchOxley previews The

Verandah Residences, its fi rst launch in 2018 EP3

Property TakeChinese investment to continue, even as

pace slows down EP4

PersonalityKishore Buxani,

investor extraordinaire EP6

Deal WatchTownhouse at The

Teneriffe on the market for $2.77 mil EP15

View across Jurong Lake Gardens, Lakeside Apartments (left) and Lakeside Towers (centre)

ALBE

RT C

HUA/

THE

EDG

E SI

NG

APO

RE

EP2 • EDGEPROP | APRIL 2, 2018

E

HOMEE-application for Rivercove Residences EC starts on April 1The 628-unit Rivercove Residences

(above, left) executive condominium

on Anchorvale Lane — the only new

EC project expected to be launched this

year — will be open for e-applications

from April 1 to 11. Booking of units will

commence on April 14.

The project is located within walk-

ing distance of the Tongkang LRT sta-

tion and developed jointly by Singa-

pore-based, privately held property

developer Hoi Hup Realty and Malay-

sian developer Sunway Developments.

Rivercove Residences is expected

to be completed by September 2020.

The EC comprises 10 blocks of 16 sto-

reys each. About 77% of the units (484

units) are three-bedders that range

from 904 to 1,163 sq ft and are priced

from $830,000 to $1.13 million. An-

other 112 units (18%) are four-bed-

room apartments ranging from 1,184

to 1,281 sq ft and priced from $1.1

million to $1.3 million. Prices range

from $1.34 million to $1.47 million

for the 32 five-bedroom units that are

1,485 sq ft each.

Hoi Hup is the developer of Hun-

dred Palms Residences, the 531-unit

EC on Yio Chu Kang Road that was

launched last July and sold out in

seven hours.

SPH and Kajima break ground on The Woodleigh Residences and The Woodleigh MallThe groundbreaking ceremony for the

mixed-use project The Woodleigh Resi-

dences and The Woodleigh Mall (above,

right) was held on March 28. Locat-

ed in Bidadari, the project comprises

680 residential units, a retail mall with

301,392 sq ft of gross floor area (GFA),

a 64,584 sq ft community club and a

23,681 sq ft police centre.

Jointly developed by media organ-

isation Singapore Press Holdings and

Japanese property developer Kajima

Development, the project will have

direct access to the Woodleigh MRT

station and Singapore’s first under-

ground, air-conditioned bus inter-

change.

The Woodleigh Residences will have

two-, three- and four-bedroom apart-

ments, while The Woodleigh Mall will

comprise a supermarket, enrichment

centres and medical suites.

The project, which marks the part-

ners’ first joint venture, is slated for

completion in 2H2022. The JV partners

paid $1,132 million, or $1,181 psf per

plot ratio (ppr), for the 99-year lease-

hold site in a state tender in June 2017.

Oxley buys Ampas Apartment en bloc for $95 mil, 10% below asking priceSingapore Exchange-listed property de-

veloper Oxley Holdings has bought the

43-unit, freehold Ampas Apartment on

Jalan Ampas, off Balestier Road. The

30,239 sq ft en bloc site was sold by

private treaty for $95 million, 10% be-

low the asking price of $105 million.

The land price translates into $1,073

psf ppr, based on a GFA of 84,669 sq

ft, which includes a 10% bonus balco-

ny area. Ampas Apartment has a 2.8

plot ratio under the 2014 Master Plan.

The purchase is subject to, among

other things, written confirmation that

a Pre-Application Feasibility Study

is not required to redevelop the site.

The en bloc sale was brokered by

Huttons Asia.

Freehold property at 96 Owen Road for sale at $24 milOn March 27, 96 Owen Road (below),

a freehold mixed residential and com-

mercial site, was launched for sale with

an asking price of $24 million, accord-

ing to sole marketing agent Edmund

Tie & Co (ET&Co).

The property has a 25m frontage

on Owen Road and is close to the

junction with Race Course Road. It

has a land area of 6,021 sq ft and a

GFA of 16,824 sq ft. The asking price

reflects a land rate of $1,329 psf ppr,

or $1,427 psf on its existing GFA. Un-

der the 2014 Master Plan, the site is

zoned “residential with commercial

at first storey”, with a gross plot ratio

of 3.0. This part two-storey and part

four-storey building is strata subdi-

vided into six units.

The ground floor, which has ap-

proval for F&B use, is currently leased

to a restaurant and gym, while a stu-

dent hostel occupies the upper floors,

notes ET&Co.

Subject to authorities’ approval, the

property may be redeveloped into a

five-storey building with a maximum

GFA of 18,064 sq ft.

The expression of interest exercise

for the site closes on April 27.

JTC launches two Industrial Government Land Sales sitesOn March 27, JTC Corp announced

the launch of two sites under the In-

dustrial Government Land Sales pro-

gramme. One is a confirmed list site at

Woodlands Industrial Park E7/E8, and

the other is a reserve list site at Tuas

South Link 3 (Plot 19).

The 94,990 sq ft site at Woodlands

Industrial Park E7/E8 is zoned “Busi-

ness 2” and has a 20-year tenure, with

a maximum gross plot ratio of 2.5.

Meanwhile, the 47,921 sq ft site

at Tuas South Link 3 (Plot 19) is also

zoned “Business 2” and has a 20-year

tenure, with a maximum gross plot

ratio of 1.4.

Under the reserve list system, a land

parcel will only be released for sale if

it receives an offer of a minimum price

that is acceptable to the government,

or when there is sufficient market in-

terest in the site. A site is considered

to have received sufficient market in-

terest if more than one unrelated party

submits minimum prices that are close

to the government’s reserve price for

the site within a reasonable period.

The tender for the Woodlands Indus-

trial Park E7/E8 site will close on May 22.

For the site at Tuas South Link 3 (Plot 19),

applications may be submitted to JTC.

OVERSEAS

HLH sells hotel component of D’Seaview in Cambodia for $15.7 milSingapore-listed real estate compa-

ny HLH Group is selling the 98-room,

10-storey hotel component of the free-

hold mixed-use project D’Seaview for

$15.7 million. With a 105,680 sq ft site

area, D’Seaview is HLH’s first develop-

ment in Cambodia.

Besides the hotel, the project has

737 one-, two- and three-bedroom

units and 67 commercial units. Locat-

ed in Sihanoukville province, the de-

velopment is 1km from the popular

Sokha Beach.

As at March 26, the commercial

units were 80% sold, while the resi-

dential units were 60% sold, with buy-

ers including those from Cambodia,

Singapore, Malaysia and China, ac-

cording to HLH. The commercial and

residential components are slated for

completion in 2Q2018 and 1H2019,

respectively.

HLH Group also holds land rights

to a 237,497 sq ft, freehold plot adja-

cent to D’Seaview.

World Class Global receives A$69 mil from handover of units at AVANTSGX-listed real estate company World

Class Global, the international prop-

erty arm of jeweller Aspial Corp, has

received A$69 million ($69.6 million)

from the handover of 134 completed

residential units at its 456-unit Mel-

bourne project, AVANT.

The developer will continue to re-

alise settlements of A$35.8 million

from the handover of 69 complet-

ed residential units at the freehold,

56-storey residential tower over the

next few weeks.

Ninety-seven per cent of AVANT

(444 units) were sold as at March 27,

with sales totalling A$256.4 million.

The residential development is located

in Melbourne’s CBD, within walking

distance of RMIT University.

According to World Class Global,

it has two other residential projects in

Australia that have yet to be launched.

Ho Bee Land invests €90 mil in European fund and Munich propertySingapore-listed property company

Ho Bee Land is investing €90 million

($145.8 million) in a Credit Suisse Eu-

ropean property fund, as well as a com-

mercial property adjacent to Munich

Central Station in Germany.

The company will invest €40 mil-

lion in the CS Real Estate SICAV-SIF

I — Credit Suisse (Lux) European

Property Fund II. Incorporated in

Luxembourg, the Credit Suisse fund

invests in real estate or real estate

investment structures in key Euro-

pean cities.

Ho Bee Land will also purchase €50

million worth of notes in Clouse SA,

Compartment 29, a public limited li-

ability company under Luxembourg

law. The proceeds from the notes will

be invested in the Munich commercial

property, which comprises a medical

centre, retail outlets and offices. Occu-

pying a site area of 484,380 sq ft, the

commercial complex was completed in

1992. — Compiled by Bong Xin Ying

and Angela Teo

PROPERTY BRIEFS

EDITORIALEDITOR | Cecilia ChowDEPUTY EDITOR | Lin ZhiqinWRITERS | Angela Teo, Timothy Tay, Bong Xin YingDIGITAL WRITER | Fiona Ho

COPY-EDITING DESK | Elaine Lim, Evelyn Tung, Chew Ru Ju, Shanthi MurugiahPHOTO EDITOR | Samuel Isaac ChuaPHOTOGRAPHER | Albert ChuaEDITORIAL COORDINATOR | Yen TanDESIGN DESK | Tan Siew Ching, Christine Ong, Monica Lim, Tun Mohd Zafi an Mohd Za’abah

ADVERTISING + MARKETING ADVERTISING SALES

DIRECTOR, COMMERCIAL OPERATIONS | Cowie TanASSOCIATE ACCOUNT DIRECTOR | Diana LimSENIOR ACCOUNT MANAGER |Janice ZhuACCOUNT MANAGERS |James Chua, Bernard WongSALES STRATEGIST |Han YaoGuang

CIRCULATIONDIRECTOR | Victor TheEXECUTIVE | Malliga Muthusamy, Ashikin Kader

CORPORATE CHIEF EXECUTIVE OFFICER | Bernard Tong

PUBLISHERThe Edge Property Pte Ltd150 Cecil Street #13-00Singapore 069543Tel: (65) 6232 8688Fax: (65) 6232 8620

PRINTERKHL Printing Co Pte Ltd57 Loyang DriveSingapore 508968Tel: (65) 6543 2222Fax: (65) 6545 3333

PERMISSION AND REPRINTSMaterial in EdgePropmay not be reproduced in any form without the written permission of the publisher

We welcome your commentsand criticism: [email protected]

Pseudonyms are allowed but please state your full name, address and contact number for us to verify.

ERA REALTY SPH AND KAJIMA

ET&CO

NEW LAUNCH

EDGEPROP | APRIL 2, 2018 • EP3

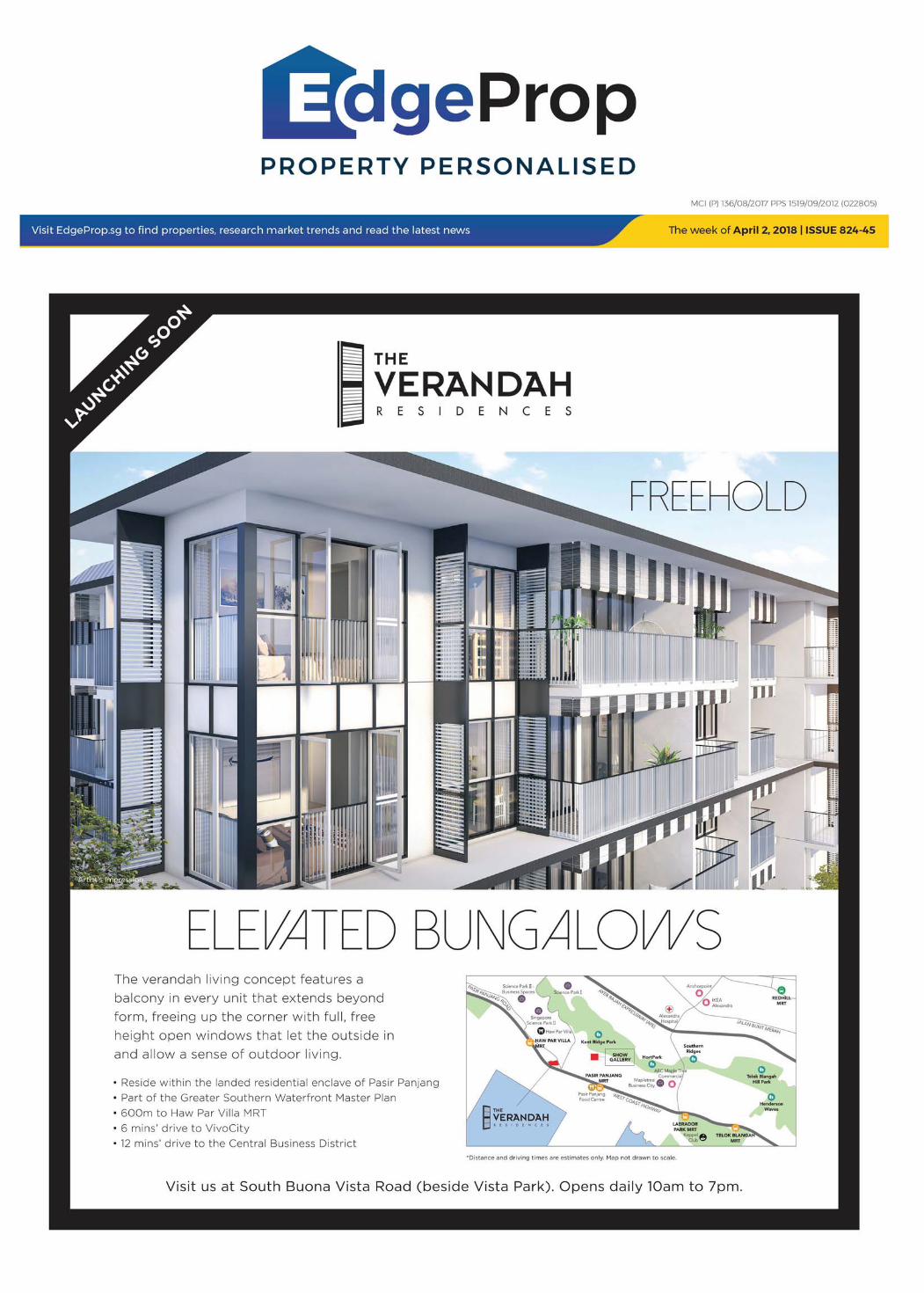

Oxley previews The Verandah Residences, its first launch in 2018

| BY TIMOTHY TAY |

Singapore-listed property de-

veloper Oxley Holdings pre-

viewed its newest residential

development, the freehold The

Verandah Residences in Pasir

Panjang, over the Good Friday week-

end (March 30 to April 1). The 170-

unit development is Oxley’s first in

a series of seven new residential pro-

jects to be launched in 2018.

The Verandah Residences will set

the benchmark in terms of design and

product features for Oxley’s upcom-

ing developments. Designed by DP

Architects, The Verandah Residences

has a theme inspired by the black-

and-white colonial bungalows that

used to dot the area. Given its loca-

tion at the junction of Pasir Panjang

and South Buona Vista Road, it is

expected to be the new icon in the

neighbourhood.

“Both investors and homebuyers

have expressed interest in the devel-

opment,” says Eugene Lim, Oxley

Holdings director of marketing and

sales. “It’s the timelessness of the

black-and-white concept that appeals

to a vast majority of the population.”

Oxley intends to release 100 units

in the first phase at an average price

of $1,800 psf. The project is priced

“realistically”, says Eric Low, deputy

CEO of Oxley Holdings. “It’s even be-

low the replacement cost of some of

the aggressive bids at en bloc tenders

that closed recently.”

The 89,620 sq ft, freehold site is

occupied by four 5-storey blocks with

a range of one- to four-bedroom apart-

ments as well as three strata hous-

es. To cater for a wide range of in-

vestors and future homeowners, the

project has a variety of unit types:

57 one-bedroom units starting from

463 sq ft and 10 one-bedroom-plus-

study units of 603 sq ft each. There

are also 11 two-bedroom units of 646

sq ft each and 21 two-bedroom pre-

mium units starting from 689 sq ft.

Three- and three-bedroom premium

types make up 48 units, with sizes

starting from 904 sq ft. Families that

want more space can choose from

20 four-bedroom units starting from

1,249 sq ft as well as three strata

houses of 2,174 sq ft each.

The Ver andah Residences is a re-

development of the former 231 Pa-

sir Panjang Road, which Oxley pur-

chased for $121 million, or $964 psf

per plot ratio, last July.

Oxley is not new to the area. It

developed the mixed-use develop-

ment Viva Vista located just across

the road. Launched and fully sold

in 2010, Viva Vista was completed

in 2014. Meanwhile, last December,

Oxley purchased the 209-unit Vista

Park en bloc for $418 million ($1,096

psf ppr). In fact, the sales gallery of

The Verandah Residences is adjacent

to Vista Park.

“Pent-up demand has been build-

ing up since 3Q2017,” says Ching

Chiat Kwong, executive chairman

of Oxley Holdings. “There haven’t

been many new launches, as devel-

opers have been holding back some

of their new projects. With the re-

cent bullish tender prices for both

government land sale sites and col-

lective sale sites, this creates an ur-

gency for buyers to purchase now

instead of later.”

Thus, Ching foresees new-home

sales in 2018 surpassing the previous

year’s 10,682 units. “This is certainly

a very exciting year for the market,”

he adds.

The 170-unit The Verandah

Residences is inspired by the stately black-

and-white colonial-era bungalows

The living room of a 1,249 sq ft, four-bedroom unit One of the en-suite bedrooms in the four-bedroom unit

The master bedroom of a four-bedder has a ‘Juliet balcony’ with windows that open outwards The enclosed kitchen of a four-bedroom unit with a yard and utility room

E

PICTURES: ALBERT CHUA/THE EDGE SINGAPORE

EP4 • EDGEPROP | APRIL 2, 2018

PROPERTY TAKE

Chinese outbound investment to continue,even as pace of capital deployment slows down

China has been a major driver

of global investment flows

into real estate in recent

years. CBRE Research data

shows that Chinese out-

bound investment in real estate rose

from around US$8 billion in 2013 to

just over US$35 billion ($45.7 bil-

lion) in 2017 (Chart 1).

Following a government clamp-

down on debt-fuelled offshore invest-

ment and tighter scrutiny of overseas

real estate acquisitions, buying ac-

tivity slowed significantly in 2H2017

and is expected to weaken further

this year as additional restrictions

take effect.

China’s global real estate shopping spreeChinese investors have purchased

more than US$100 billion worth of

overseas commercial real estate over

the past five years, making headlines

with numerous eye-catching deals in-

volving trophy assets in global gate-

way cities.

High-profile transactions in 2015

included Anbang Insurance’s pur-

chase of the Waldorf Astoria New

York hotel for US$1.95 billion, and

Evergrande’s acquisition of Mass Mu-

tual Tower in Hong Kong’s Wan Chai

district for US$1.6 billion (Table 1).

After eclipsing Singapore as the

largest source of Asian outbound cap-

ital in 2016, completing US$26 billion

worth of overseas real estate acquisi-

tions, Chinese investors maintained

their strong momentum in 1H2017,

with several deals inked during that

period considered among the costli-

est recorded that year.

Regulatory change promptsa step backChinese authorities began clamping

down on overseas investment at end-

2016 in a move designed to stabilise

the renminbi, restrict capital flight

and reduce financial risk.

Capital outflows subsequently

weakened significantly. Data quoted

at a news conference hosted by the

Ministry of Commerce in July 2017

showed that overseas direct invest-

ment in the property sector fell 82%

y-o-y in 1H2017, with discrepancies

between official data and actual in-

vestment turnover reflecting the sig-

nificant volume of Chinese capital al-

ready circulating outside the country. CONTINUES ON EP6

High-profile transactions included Anbang Insurance’s purchase of the Waldorf Astoria New York hotel for US$1.95 billion in 2015

BLOOMBERG

| BY SAM XIE |

This new wave was followed by

Beijing publicly naming several of the

country’s largest private conglomer-

ates as having engaged in excessive

borrowing for foreign acquisitions.

Subsequently, in August 2017, the

State Council and the National Devel-

opment and Reform Commission for-

malised restrictions on Chinese com-

panies engaging in overseas mergers

and acquisitions in certain sectors.

NDRC listed three categories of

overseas investment including those

that are banned (for example, indus-

tries related to gambling); those that

are restricted (for example, property,

film and sports); and those that are

to be encouraged (for example, in-

vestments that support the Belt and

Road Initiative).

The inclusion of property on the

list of restricted sectors subjected pro-

posed overseas acquisitions by Chi-

nese companies to additional layers

of scrutiny, ensuring that buying ac-

tivity slowed significantly in 2H2017,

led by a fall in activity by insurance

companies (Chart 2).

While many Chinese investors have

turned cautious towards making new

acquisitions, others are taking a ma-

jor step back by selling offshore real

estate to repay lenders and repatri-

ate capital back to China (Table 2).

New restrictions further dampen investor appetiteAlthough Asian outbound investment

continues to eclipse previous records

and Chinese investors still comprise

the largest source of capital, CBRE

Research expects to see a continua-

tion of the slowdown in Chinese out-

bound investment first witnessed in

2H2017, following the introduction

of new capital controls.

This year’s CBRE Investor Inten-

tions Survey, which focuses on the

forward-looking views of real estate

investors in Asia-Pacific, indicates

that Chinese investors are less keen

to invest overseas in 2018. While

overall interest remains reasonably

firm, fewer investors intend to invest

more than they did in 2017.

At the forefront of investors’ con-

cerns is another set of outbound in-

vestment regulations, effective March

2018, that classify real estate as a “sen-

sitive sector” and therefore subject to

an additional layer of examination.

The measures, unveiled by NDRC

in December 2017, categorise out-

bound investment into “sensitive”

and “non-sensitive” projects. While

real estate is not specifically catego-

rised as a “sensitive industry”, the

previous guidance document released

Chinese outbound real estate investment

(2013 to 2017)

Chinese outbound real estate investment by investor type*

Note: Transactions include deals in the offi ce, retail, industrial, hotel,mixed-use and other commercial sectors. Development sites are excluded.

Note: Transactions include deals in the offi ce, retail, industrial, hotel, mixed-use

and other commercial sectors. Development sites are excluded.

*Sovereign wealth funds are excluded

40

30

20

10

0

16

12

4

0

US$ bil

US$ bil

2H

1H

20172016201520142013

1H2016 1H20172H2016 2H2017

Chart 1

Chart 2

DATE MARKET PROPERTY NAME SECTOR PRICE (US$ MIL) SELLER

March 2018 Hong Kong Kai Tak Site (Lot no 6564) Site 813 HNA

February 2018 New York 19-21 East 64th Street Offi ce 90 HNA

February 2018 Hong Kong Kai Tak Site (Lot no 6562) Site 898 HNA

February 2018 Hong Kong Kai Tak Site (Lot no 6565) Site 1,148 HNA

February 2018 New York 1180 6th Avenue Offi ce 305 HNA

January 2018 Sydney One York Street Offi ce 161 HNA

January 2018 London One Nine Elms Mixed-use 590 Dalian Wanda

December 2017 Sydney 73 Miller Street Offi ce 114 Fosun

November 2017 London Lloyds Chambers Offi ce 133 Fosun

Recent overseas property sales by Chinese companies

Table 2CHARTS: RCA, CBRE RESEARCH

Insurance company Property company Conglomerate Other

PERIOD MARKET PROPERTY NAME SECTOR PRICE (US$ MIL) INVESTOR TYPE

2Q2017 Cities across Europe Logicor portfolio Logistics 13,247 Sovereign wealth fund

3Q2016 Cities across the US Starwood Hotel portfolio Hotel 5,500 Insurance

1Q2017 New York 245 Park Avenue Offi ce 2,210 Conglomerate

1Q2017 Cities across Japan Residential portfolio Residential 2,210 Conglomerate

1Q2015 New York Waldorf Astoria Hotel 1,950 Insurance

1Q2014 Dubai Residential and hotel project Mixed-use 1,876 Sovereign wealth fund

3Q2015 Cities across Australia Offi ce portfolio Offi ce 1,682 Sovereign wealth fund

4Q2015 Hong Kong Mass Mutual Tower Offi ce 1,613 Property company

4Q2016 Seoul IFC Seoul Offi ce 1,595 Sovereign wealth fund

1Q2017 London Leadenhall Building Offi ce 1,425 Sovereign wealth fund

Top 10 Chinese outbound real estate investment transactions (2013 to 2017)

Table 1 TABLES: RCA, CBRE RESEARCH

EDGEPROP | APRIL 2, 2018 • EP5

EP6 • EDGEPROP | APRIL 2, 2018

| BY CECILIA CHOW |

Kishore Buxani gets excited when

he is shown an old building.

“It’s because there’s an oppor-

tunity to turn it around,” says

the CEO and founder of real

estate investment firm Buxani Group.

He is considerably less enthusiastic

when shown a shiny new building

unless he can buy it at a price below

market value.

That opportunity came about in

early 2007: It was when Buxani and

Seychelles-based private investment

firm, Capital Management Group, pur-

chased six strata floors of Grade-A

office space at Samsung Hub at 3

Church Street. Capital Management,

founded by Mukesh Valabhji, has

been a partner with Buxani on sev-

eral acquisitions.

The vendor of the six strata floors

at Samsung Hub was OCBC Properties

and the total strata area was 78,490

sq ft. The joint-venture partners, Bux-

ani and Capital Management, paid

$122.4 million for it, which trans-

lated to $1,560 psf.

It was a brand-new 999-year lease-

hold, 30-storey Grade-A office build-

ing with a six-storey podium in the

CBD. Joint owners in the development

were CapitaLand, OCBC Properties

and the Singapore Chinese Chamber

of Commerce.

A tilt in timeIn 2002, when the building was still

under construction, it was discov-

ered to be tilting by 0.1 degree, and

the problem was rectified by main

contractor, Samsung.

The building was completed and

received its Temporary Occupation

Permit (TOP) in 2006, and Samsung

even became an anchor tenant. Thus,

the building became known as Sam-

sung Hub.

While other investors were initially

cautious about the building’s history,

Buxani saw it as a buying opportu-

nity. He requested for a report on

the soundness of the building from

a structural engineer, even while he

was negotiating to purchase the six

floors from OCBC Properties. “The

report wasn’t completed yet, but

the structural engineer said, ‘Trust

me, it’s probably the safest build-

ing in Singapore now,’” says Buxani.

“Based on that trust, I went ahead.”

The deal was struck in late 2006 and

completed in early 2007.

When Samsung Hub finally ob-

tained its Certificate of Structural

Completion (CSC) in 2011, Buxani

decided to put some of the floors up

for sale, and they were sold at more

than $3,000 psf. The only unit he

kept is the office he currently occu-

pies. “We had 90% financing, and

so when we sold, we made seven

times equity,” says Buxani.

He still considers Samsung Hub

one of the best investment deals in

his portfolio.

Early startOne could say Buxani, who is in his

mid-40s, had an early start in buy-

ing property: When he was 12, he

and his brother helped their mother

purchase a condominium on Meyer

Road. On weekends, he worked at a

relative’s shop in Far East Plaza, ped-

dling T-shirts and jeans. “I wanted to

earn some pocket money,” he says.

His father, a civil servant, had

passed away when he was 11. His

mother then moved the family from

Johor Bahru to Singapore. “We didn’t

come from money,” says Buxani. It

seems that real estate investing ran

in his blood. His mother, Indra, is

the sister of property magnates Raj

and Asok Kumar of Royal Broth-

ers Group. The brothers have since

gone their separate ways with their

respective sons: Raj and son, Kishin

R K, who heads RB Capital; and Asok,

with his son Bobby Hiranandani,

co-chairman of Royal Group Holdings.

Buxani emphasises that his com-

pany is a separate entity from that

of his uncles and cousins.

Prior to becoming a full-time real

estate investor and developer, Buxani

joined Goldman Sachs’ investment

banking division when he was 24. His

job was to start an asset management

business by helping private families,

family offices and corporate entities

invest in global equities, fixed-in-

come instruments and currencies.

“I focused on undervalued stocks,

which was very research-based,

and tried to understand long-term

[investment] themes,” he says. “It’s

very much like investing in real es-

tate. You have to understand the un-

derlying fundamentals.”

Buxani bought his first proper-

ty in 2000 while still an investment

banker at Goldman Sachs. It went

on to make him his first million. He

was 28 then. “Perhaps it’s because

I worked in one of the shops when

I was a kid that the first property I

bought was a strata shop unit at Far

East Plaza,” he muses. “It was on

the third level, facing the escalators,

and 380 sq ft. I paid $880,000, about

$2,700 psf.”

From that one unit, he bought

more strata shops in Far East Plaza

and Lucky Plaza, as well as strata of-

fice units in the CBD, including at Ma-

lacca Centre, adjacent to RB Capital

Building (the former Royal Brothers

Building). He also invested in con-

servation shophouses in Chinatown

and Little India. “I’ve bought and

sold some over the years,” he says.

He founded Buxani Group in 2003

to hold his assets, and decided to

leave Goldman Sachs in 2005 when

China still plays critical role in global commercial real estate market

PERSONALITY

PROPERTY TAKE

by NDRC in August 2017 included real estate

on the list of restricted sectors, meaning that

it meets the fourth criterion of a “sensitive in-

dustry” and that proposed overseas real estate

acquisitions by Chinese companies will be sub-

ject to NDRC approval.

There will also be regulation of financial

institutions, partnership business entities and

Chinese individuals investing via offshore spe-

cial-purpose vehicles or pledging domestic as-

sets against foreign exchange loans to finance

investments.

The start of a new chapter,not the end of the storyChina still accounts for the largest source of

capital in Asia-Pacific and will continue to play

a critical role in the global commercial real es-

tate investment market. CBRE Research believes

Chinese outbound investment will continue,

but the pace of capital deployment is likely

to slow as investors adjust to the new rules.

Chinese outbound investment this year

will be characterised by the following trends:

Focus on Belt and Road: There will be a strong-

er focus on Belt and Road countries and logis-

tics and industrial-related asset classes such as

warehouses, industrial parks and ports, sup-

ported by more flexible regulatory treatment.

CBRE Research’s China Investor Intentions Sur-

vey shows that although Chinese investors are

less keen to invest overseas in 2018, interest in

Belt and Road-related regions continues to rise.

CBRE Research has already observed a signif-

icant jump in the number of Chinese inves-

tors purchasing logistics assets in recent years.

Large portfolio deals: Transactions involving the

purchase of large portfolios are expected to be-

come more frequent in Belt and Road countries

as investors shift their focus from traditional

gateway markets in Asia-Pacific and the West.

Alternative sectors: Healthcare and data cen-

tres are likely to attract stronger interest from

Chinese investors, as investment in these niche

sectors can support the government’s policy of

improving China’s technological R&D. Trans-

actions will take the form of equity stakes or

partnerships with local investors.

Changing composition of capital: The compo-

sition of Chinese outbound capital will change

from property companies and insurance com-

panies to sovereign wealth funds (SWFs) such

as the China Investment Corp and the State

Administration of Foreign Exchange. While

outbound investment demand from several

sources of Chinese capital is set to weaken,

SWFs will retain a strong appetite for real es-

tate, particularly for stabilised assets in ma-

jor cities. However, acquisitions are very like-

ly to be confined to markets allied to the Belt

and Road Initiative. Corporations, particularly

those engaged in e-commerce and manufac-

turing, are also expected to be active and ac-

quire assets — especially logistics properties

— to facilitate their global expansion.

Early Chinese buyers become sellers: Many Chi-

nese buyers at the forefront of the early wave

of outbound investment are expected to dis-

pose of some of their assets to repay loans, or

because they have already reached their ex-

pected returns for core assets. Conglomerates

that have been the subject of the recent gov-

ernment clampdown will continue to liquidate

major overseas real estate holdings to recapi-

talise or repatriate capital home. Some of this

capital could be reinvested abroad, though.

Investment via offshore financial institutions:

Large investors already have money in circula-

tion via the balance sheets of insurance com-

panies and other investment management plat-

forms they have acquired. They are likely to use

these offshore platforms to engage in proper-

ty acquisitions, although these will have to be

closely aligned with the Belt and Road Initiative.

Redeploying offshore capital: With capital con-

trols making outbound direct investment more

difficult, redeploying offshore capital is expect-

ed to drive some investment transactions this

year. Given that they will also be subject to

closer scrutiny by NDRC, however, such pur-

chases will be considered very carefully.

Other routes: Other potential options for Chi-

nese outbound investors could include tak-

ing positions as limited partners, purchasing

smaller equity stakes of below US$50 million

and participating in joint ventures.

Above all, it must be stressed that while

Chinese outbound investment will be subject

to tighter regulation, it has not been forbidden.

CBRE Research expects to see Chinese buyers

engage in low-profile, selective and strategic real

estate purchases that align with their broader

business objectives, eschewing the high-profile

and speculative plays that characterised much of

their previous activity. This will ultimately result

in smaller transactions and slower deal flow.

Sam Xie is CBRE head of research, China.

Jonathan Hills, CBRE director of Asia Pacific

Research, and Leo Chung, CBRE associate

director of Asia Pacific Research, collaborated

on the report.

FROM EP4

Kishore Buxani, investor extraordinaire

CONTINUES ON EP10

Buxani: In Singapore, once you sell something, it’s hard to find a replacement property

E

ALBERT CHUA/THE EDGE SINGAPORE

EDGEPROP | APRIL 2, 2018 • EP7

COVER STORY

EP8 • EDGEPROP | APRIL 2, 2018

| BY LIN ZHIQIN |

An area that seems to have

escaped notice amid the

en bloc fever is the Jurong

Lake District, which spans

360ha in the west of Sin-

gapore and is being developed into

the city state’s second CBD. While

51 sites have been sold for a total

of $14.6 billion since 2017, none of

them are located in JLD. And among

the collective sale sites launched for

tender, only Park View Mansions is

located in the district.

Alice Tan, head of consultancy and

research at Knight Frank Singapore,

says that, over the last 10 years, the

stock of private residential units in

the West Region grew the least among

all the planning regions in Singapore.

This means inherent advantages for

new residential developments in the

region, especially in JLD, compared

with those elsewhere, says Tan. It

also means that the ageing develop-

ments in the area have high redevel-

opment potential.

Adjacent to Park View Mansions

is the 120-unit Lakeside Apartments,

which is next to the 144-unit Lake-

side Towers. Both are 99-year lease-

hold properties completed in 1981

and 1983, respectively.

Located across Jurong Lake from

Park View Mansions is privatised

HUDC estate Ivory Heights, which

is in the process of gathering ap-

proval from the owners for an en

Has the west BEEN FORGOTTEN?The Jurong Lake District has seen little action in the recenten bloc cycle, but upcoming launches could offer opportunities to ride the growth of Singapore’s second CBD

The successful collective sale of Park View Mansions will lift prices of private homes in JLD

bloc sale, according to marketing

agent SLP International in October

2017. The site, located near the Ju-

rong East MRT station, has not been

launched for sale, although a reserve

price of $1.34 billion has been set.

The land rate is $979 psf per plot ra-

tio, based on the existing gross floor

area (GFA), which translates into a

plot ratio of 1.86, and including an

estimated $160 million for a fresh

99-year lease. Ivory Heights is also

close to Jurong Country Club, which

was closed at end-2016 to make way

for the upcoming High Speed Rail

(HSR) terminus.

According to marketing agent

Huttons Asia, the owners of the

160-unit Park View Mansions have

set a reserve price of $320 million,

or a land rate of $1,183 psf ppr, in-

cluding an estimated $157 million

payable to the government to inten-

sify the GFA and for a fresh 99-year

lease. The tender closes on April 20

and, if a deal is struck, the redevel-

opment project could be sold at be-

tween $1,800 and $1,900 psf, which

will lift prices of private homes in

JLD, says Tan.

Existing developmentsThe master plan for JLD, previous-

ly known as Jurong Regional Centre,

was released in 2008 as part of the

government’s push to grow employ-

ment outside the CBD. A new mas-

ter plan was unveiled last August to

transform JLD into a smart and sus-

PICTURES: ALBERT CHUA/THE EDGE SINGAPORE

tainable mixed-use business district

to support Singapore’s next phase of

economic transformation.

In addition to IMM Mall, which

has 961,281 sq ft of retail space, four

new malls — JCube, Jem, West-

gate and Big Box — have sprung up

around the Jurong East MRT station

in recent years.

A redevelopment of the previ-

ous Jurong Entertainment Centre,

JCube was opened in April 2012. It

has 210,000 sq ft of retail space and

houses Singapore’s first Olympic-size

ice skating rink.

Jem, which houses 241 shops

across its 818,000 sq ft of retail space,

opened a year later, in June 2013.

That was followed by the opening

of Westgate in December that year.

The integrated development compris-

es a seven-storey mall with 410,000

sq ft of retail space and a 20-storey

office tower.

Located on a 5.6ha site, Big Box

is the largest project built under the

Economic Development Board’s Ware-

house Retail Scheme, which allows

industrial land to be used for retail

and warehousing. The mall houses

400,000 sq ft of retail space, includ-

ing a hypermart on the ground floor,

which is home to Singapore’s biggest

indoor wet market.

Located between IMM Mall and

Big Box is the Jurong Health Cam-

pus, comprising the 700-bed Ng Teng

Fong General Hospital and the 400-

bed Jurong Community Hospital.

Ageing develop-ments in JLD include the 120-unit Lakeside Apartments (above) and the 144-unit Lake-side Towers

COVER STORY

EDGEPROP | APRIL 2, 2018 • EP9

Panorama taken by a drone at Twin Vew’s site

CSC LAND

The most recent transaction at J Gateway involved a 678 sq ft, two-bedroom unit that changed hands at a 15% profit

Four new malls — JCube, Jem (pictured), Westgate and Big Box — have sprung up around Jurong East MRT station in recent years

Artist’s impression of Twin Vew, which is expected to be launched in April

THE EDGE SINGAPORE

URA REALIS (AS AT 13 MARCH 2018), KNIGHT FRANK RESEARCH

Av

era

ge

pri

ce (

$ p

sf)

1,400

1,200

1,000

800

600

400

200

0

3,000

2,500

2,000

1,500

1,000

500

0

No

of u

nits

New sale Resale Sub sale New sale average price (psf) Resale average price (psf)

1Q2008

1Q2009

1Q2010

1Q2011

1Q2012

1Q2013

1Q2014

1Q2015

1Q2016

1Q2017

3Q2008

3Q2009

3Q2010

3Q2011

3Q2012

3Q2013

3Q2014

3Q2015

3Q2016

3Q2017

Opened in 2015, they are the first

hospitals in Singapore to be designed

and built together as an integrated

development to complement each

other and offer better patient care,

efficiency and convenience.

Conceptualised as a “hotel in a

garden”, the 15-storey Genting Ho-

tel Jurong, which is within walking

distance of the Jurong East MRT sta-

tion, opened in April 2015. It offers

557 rooms and is home to 70 species

of shrubs and 20 species of trees and

palms. Its facilities include a ballroom

that can accommodate 300 people

and five meeting rooms. There is

also a sky terrace where guests can

take in views of JLD.

New projects fully soldMost of the new projects launched

in the area over the last few years

have been fully sold, says Tan. Ad-

jacent to Westgate is J Gateway, a

99-year leasehold condominium by

MCL Land. Riding the development

of JLD and as the first condo to be

launched in the area in 10 years, J

Gateway sold all of its 738 units in

a single day when the project was

previewed in June 2013. The average

selling price was $1,480 psf, and a

484 sq ft one-bedroom unit fetched

$1,778 psf — a record for the area.

J Gateway was completed in 2016

and the most recent transaction in-

volved a 678 sq ft, two-bedroom unit

that changed hands for $1.25 million

($1,843 psf) on March 9. The price

is 15% higher than the $1.09 million

($1,605 psf) paid by the seller in 2013.

Another project that is fully sold

is the 696-unit Lakeville, where de-

veloper MCL Land moved 180 units

at an average price of $1,300 psf on

its first day of sales in April 2014.

Lake ville sits on a 99-year leasehold

site located across Boon Lay Way

from Jurong Lake.

Adjacent to Lakeville is the 710-

unit Lake Grande, also developed by

MCL Land. Over its launch weekend

in July 2016, 436 units were sold at

an average price of $1,368 psf. The

condo overlooks Jurong Lake and is

within walking distance of the Lake-

side MRT station. It was fully sold

in less than two years and is slated

for completion in 2020.

Those keen to buy in the area

this year can consider the upcom-

ing launch of Twin Vew, says Tan.

The 520-unit condo at West Coast

Vale will be the first development

by CSC Land, a subsidiary of con-

glomerate China State Construction

Engineering Corp. In February 2017,

the developer submitted the winning

bid of $292 million ($592 psf ppr)

for the hotly contested Government

Land Sales site that drew nine bids.

Its bid for the 176,295 sq ft site was

just 0.7% above the second highest.

CSC Land is expected to launch the

project in April.

Twin Vew is adjacent to EL Devel-

opment’s Parc Riviera, which has a

total of 752 units. The 99-year lease-

hold project was launched for sale

in November 2016 and fully sold in

less than a year.

Across the road from Parc Riviera

is a another GLS site whose tender

closed on Jan 30. City Developments

submitted the top bid of $472.4 mil-

lion ($800 psf ppr) for the 210,881 sq

ft site, which can yield an estimated

730 units. The project is likely to be

launched for sale next year.

Catalysts for growthThe completed JLD, which is set to

transform the west of Singapore, will

offer more than 100,000 new jobs

and 20,000 new homes, says URA.

It will also be home to the largest

local collection of water lilies. More

than 140 varieties will be showcased

at the Jurong Lake Gardens, which

is undergoing further development

that is set to be completed progres-

sively from 2020.

Slated for completion by 2025, the

20km Jurong Region Line will provide

better connectivity both within the

region and with the rest of the island.

Billed as a game changer that will

affect the way Singaporeans and Ma-

laysians live, work and play, the HSR

project is expected to be completed

in 2026. It will take just 90 minutes

to travel the 350km separating Kuala

Lumpur’s Bandar Malaysia and Sin-

gapore’s Jurong East, opening up new

possibilities for business and leisure

in both countries.

The Cross Island Line (CRL), ex-

pected to be completed in 2030, will

provide a faster commute from Ju-

rong to Changi and serve an estimat-

ed 600,000 riders daily. It will also

connect all of the existing MRT lines,

with about half of the 30-plus CRL

stations being interchange stations.

The next phase of JLD’s develop-

ment, including new offices, hous-

ing, hotels, retail, F&B and other lei-

sure offerings, will take place around

the HSR station, according to URA.

The HSR and Jurong East MRT sta-

tions will be connected by a pedes-

trian mall, which will form the main

commercial spine along which the

second CBD will grow. The Minis-

try of Transport and the Land Trans-

port Authority have also announced

plans to be housed together in a new

building adjacent to the Jurong East

MRT station.

First announced in 2012, the Tuas

mega port will be opened progres-

sively from 2021 and eventually con-

solidate operations from the current

Pasir Panjang, Tanjong Pagar, Keppel

and Brani container terminals. When

fully completed by 2040, it will be

twice the size of Ang Mo Kio town

and be able to handle up to 65 mil-

lion twenty-foot equivalent units of

cargo yearly, about double the 33.7

TEUs handled in Singapore last year.

The developments are expected to

catalyse the growth of the JLD when

they are completed, says Tan.

According to Tan, prices for both

new sale and resale non-landed pri-

vate residential properties in the West

Region of Singapore more than dou-

bled between the trough in 1Q2009

and the peak in 3Q2013, but they

have been flattish since (see chart).

Last year, the average transacted

price in the West Region was $1,112

psf, putting it in third place after the

Central Region’s $1,610 psf and North

East Region’s $1,129 psf. Although the

figure is higher than the $1,090 psf

in the East Region and $1,067 psf in

the North Region, “the West Region

presents a more optimistic investment

opportunity for buyers, in view of the

government’s plans for JLD, construc-

tion of new infrastructure such as the

Jurong Region Line and Cross Island

Line, as well as the upcoming High

Speed Rail”, says Tan.

CSC LAND

E

Transaction volume versus average price in the West Planning Region

EP10 • EDGEPROP | APRIL 2, 2018

PERSONALITY

he realised he was enjoying his extra-curric-

ular activities — property investing — more

than his full-time job as an investment banker.

‘Accidental’ en bloc beneficiaryBuxani is a walking testament of how child-

hood experiences and impressions shape us

as adults. “When I was young, I saw so many

people lose their pants in real estate from

1985 to 1987 and, again, in the Asian finan-

cial crisis in 1997/98. And these were usual-

ly the same people who had claimed, ‘Sure to

make money,’ when they bought their prop-

erties,” he recalls. “So, now, whenever I hear

someone say something is guaranteed to make

money, I cringe.”

As such, Buxani is not about to bet on the

en bloc boom. “The perception is that the res-

idential market is recovering,” he says. “I be-

lieve there’s pent-up demand, and it will con-

tinue for a while. But, for me, I will stick with

commercial property in Singapore.”

Nevertheless, he benefited when Thong

Sia Building was sold en bloc for $380 mil-

lion. “Honestly, we didn’t think of going en

bloc when we bought it, although I knew it

had en bloc potential, given its location just

off Orchard Road, and the fact that it’s free-

hold,” he says.

In August 2013, Buxani purchased Raffles

Medical Management, an entity of Raffles Medi-

cal Group, which owned the commercial po-

dium of Thong Sia Building, for $120 million.

The seven-storey commercial podium contained

eight retail and office units, with sizes ranging

from 710 to 8,826 sq ft. Raffles Medical Group

had purchased the commercial podium in Feb-

ruary 2011 for $92.08 million to convert it into

a specialist medical centre. When it failed to

obtain the necessary government approvals for

the conversion, it put the commercial podium

up for sale by tender.

Following the purchase, Buxani had plans

to reposition and rename the building. Thong

Sia Co was the distributor of Seiko watches

and the building was famous for its promi-

nent Seiko watch boutique fronting Bideford

Road. “We thought of changing the name to

Times Square Building — it was a play on the

acronym TSB of Thong Sia Building,” explains

Buxani. “We even had an architect draw pic-

tures of what the building would will look like

with a big clock.”

When Buxani joined Thong Sia Building’s

Management Council of Strata Title (MCST)

board as its chairman, at the very first man-

agement meeting in January 2014, about half

a dozen members suggested that the owners

attempt a collective sale. A collective sale com-

mittee (CSC) was set up, and a request for pro-

posals was called to appoint a property con-

sultant and a lawyer.

Higher GFAThong Sia Building, which was built in 1981,

occupies a freehold site of 21,602 sq ft. In ad-

dition to the seven-storey commercial podi-

um, it had a 19-storey residential block with

37 apartments. Prior to the collective sale, its

owners had verified with URA that the gross

floor area (GFA) of the building was 156,300

sq ft, which reflects a plot ratio of 7.23. “This

was 10% higher than what most people had

initially estimated,” says Buxani.

Although the commercial podium account-

ed for just 30% of the strata area at Thong Sia

Building, it had a higher share value of 75.2%.

This is because commercial units have a high-

er share value than residential units. “But we

arrived at an apportionment that was agreea-

ble to everyone,” says Buxani.

The original reserve price was $400 million.

There were expressions of interest but no firm

buyers even after two tenders were held. When

the second private treaty was called, a buyer

emerged, but with a lower offer of $380 mil-

lion. The CSC proceeded to collect signatures

all over again and managed to obtain 80%

consensus to sell at the lower price. The col-

lective sale was done in July 2015 and com-

pleted in April 2016.

The building is being redeveloped into Bid-

eford Hills by Sin Capital Group, an Asian pri-

vate investment group. It will be a mixed-use

development with serviced apartments man-

aged by Oakwood Asia Pacific, and branded

Oakwood Studios.

The sale of the former Thong Sia Building

was brokered by JLL, and marked the only

collective sale in 2015. It was also considered

the largest mixed-use collective sale in Singa-

pore. The sale price of $380 million reflected a

price of $2,430 psf based on the existing GFA

of the building.

Opportunistic buys, long-term hold Buxani has made several opportunistic deals

over the past decade. In 2006, the former GMG

Building at 108 Robinson Road was put up

for sale by expression of interest. The asking

price was $48 million, or $875 psf, yet there

were no bidders.

Buxani smelt an opportunity, however, as

the building was freehold and on Robinson

Road in the CBD. It was an old building de-

veloped in the 1970s. As it was the result of

two buildings merged together, there were two

lobbies, and there were pillars within the of-

fices. “It was a bit odd, but I could see its po-

tential,” says Buxani.

After acquiring the building for $48 million,

Buxani and his partner, Capital Management,

spent another $6 million to refurbish it, then

renamed it Finexis Building. In 2011, they sold

a 50% stake in the 12-storey building to an

offshore fund managed by Sin Capital for $110

million, or $2,043 psf. In 2014, the remaining

50% stake in the building was sold to another

offshore fund managed by Sin Capital for $120

million, or $2,300 psf.

In April 2012, Buxani and Capital Manage-

ment jointly purchased 51 strata office units at

Parkway Centre in Marine Parade for $53.375

million. The strata area totalled 51,191 sq ft,

which means the purchase price translated to

$1,043 psf. The building had 68 years left on

its 99-year lease.

Once again, Buxani got himself on the MCST

committee and elected chairman. When he

called for an extraordinary general meeting

and suggested upgrading Parkway Centre, he

was told that the sinking fund had only about

$300,000. It would cost about $500,000 to up-

grade the toilets and common corridors and to

repaint the building. Buxani suggested going

ahead with upgrading works, and his compa-

ny would pay the difference.

In 2012, the strata commercial market

was hot. Because of the imposition of the

additional buyer’s stamp duty and seller’s

stamp duty in the residential sector in 2011,

many investors switched from buying resi-

dential to strata commercial units. “We start-

ed receiving offers from interested parties,”

says Buxani.

From September 2012, he started selling strata

units from $1,600 psf to as high as $1,820 psf.

Buxani is still holding on to 20 units at Parkway

Centre, which are fully leased. The area is being

rejuvenated with the upcoming Thomson-East

Coast Line, and Parkway Centre should bene-

fit from its proximity to the future Marine Pa-

rade MRT station.

In late 2012, Buxani and Capital Manage-

ment also jointly purchased the former Katong

Junction, a four-storey freehold commercial

building on Joo Chiat Road. They paid $55.28

million for the building, and proceeded with

addition and alteration works. The building

has been renamed Katong Point.

The three upper levels have been taken up

by MOX, a collaborative work space for those

in the creative industry, with a retail store-

front on the first level. “I’m still holding on to

the building because it’s a freehold commer-

cial property,” says Buxani. “We would like

to keep it for the long term unless we receive

an offer we can’t refuse. In Singapore, once

you sell something, it’s hard to find a replace-

ment property.”

HospitalityGiven that the Singapore property market is

on an uptrend, it is becoming “a challenge”

for Buxani to hunt for undervalued or under-

appreciated assets in Singapore. As such, he

has been looking abroad since 2013.

He believes the current boom in the tour-

ism and travel industry will be a long-term

trend, driven by millennials and the growth in

Chinese tourists abroad. He therefore started

Buxani Hotels to invest in hospitality assets.

Particularly bullish about the UK and Europe,

he recently purchased a hotel in Scotland and

is doing due diligence for its possible conver-

sion into a four-storey boutique hotel.

Buxani is also a shareholder in a luxury resort

and residential development on the 268ha Fe-

licite island in Seychelles, which is being deve-

loped by Capital Management. The Six Senses

Zil Pasyon, a 30-villa resort that opened in

October 2016, has been enjoying an occupancy

rate in the 70%-to-80% range.

There are plans to develop 28 luxury vil-

las on the island. So far, four of the residences

have been completed. Two have been sold to

buyers who had purchased the units off-plan,

and another two will be used as show villas

for a global launch slated for later this year.

To increase his chances of securing big-

ger hospitality assets in the UK and Europe,

Buxani Capital was launched recently. “It’s

a platform to create a vehicle for larger hos-

pitality acquisition opportunities in Europe

with like-minded co-investors,” he says, add-

ing that the focus will be on the acquisition

of hotel portfolios.

Commercial focus locally, targeting hospitality assets in Europe

FROM EP6

Buxani purchased six strata floors of the Grade-A, 30-storey Samsung Hub in 2006, and sold most of them at more than $3,000 psf

Thong Sia Building was sold en bloc in 2015 for $380 million. Buxani had purchased the commercial podium for $120 million in 2013.

The former GMG Building at 108 Robinson Road was renamed Finexis Building

Buxani still owns 20 strata office units at Parkway Centre

PICTURES: BUXANI GROUP

E

SAMUEL ISAAC CHUA/THE EDGE SINGAPORE

OFFSHORE

EDGEPROP | APRIL 2, 2018 • EP11

Mixed-use project in JB with mall and theme park to draw international crowd

| BY LIN ZHIQIN |

Siow Chien Fu, executive director and

CEO of Capital World, expects Singa-

poreans to make a beeline to Capital

21 mall in Johor Bahru when it opens

in August. “We are building a one-stop

entertainment and shopping haven in the heart

of Johor Bahru,” he says.

The mall is part of the 1.2 million sq ft Cap-

ital City being developed by Capital World,

which was listed on Catalist last year via a re-

verse takeover of marble producer Terra tech

Group. The project occupies a 439,726 sq ft

site on Jalan Tampoi — a 15-minute drive from

Woodlands Causeway and 30 minutes from

Senai International Airport. It will consist of

a six-storey theme-park-and-mall, 315-room

Hilton Garden Inn, 630 hotel-style serviced

suites and 690 serviced apartments.

When completed, the indoor theme park

will rank among the world’s five biggest and be

the largest in Southeast Asia. “An indoor theme

park is a very good niche,” says Siow. “We are

adapting to the local weather condition by hav-

ing it indoors.” He reckons the entertainment

element injected by the theme park will help

the integrated development compete against on-

line retail and the other malls in Johor Bahru.

Billed as a mall within a theme park, the

retail component comprises 1,655 units, of

which Capital World is retaining 242 for recur-

ring income. Seventy per cent of these units

have been leased out, says Siow. Meanwhile,

of the 1,413 units available for sale, the devel-

oper has sold about 65% at an average price

of RM2,600 psf.

The serviced apartments, which are priced

from RM500 to RM600 psf, will be launched

for sale later this year. The price level is aimed

at local buyers, says Siow, but Singaporeans

would also be able to invest, as the quantum

will cross RM1 million ($337,592).

Despite concerns of an oversupply in Jo-

hor, Siow is confident that the apartments

will be well received. “As long as the location

and product are good, there will be demand

regardless of the oversupply in the larger mar-

ket,” he explains.

The entire project is spearheaded by the

theme park, he adds. Spanning Levels Three

and Four of the retail podium, it will feature

several theme attractions, including Movie Plan-

et, Cartoon Planet and Music Planet. The Mov-

ie and Cartoon attractions will integrate aug-

mented reality and virtual reality, while Music

Planet will have circus, musical and theatrical

performances. The retail component will also

feature thematic zones inspired by five conti-

nents — the Americas, Europe, Australia, Asia

and the Middle East.

Coupled with affordable ticket prices, the

attractions will ensure a steady stream of re-

peat customers. That is the key to a success-

ful theme park, notes Siow.

The theme park will cater for people from

all walks of life. In addition to the discounted

rates offered to senior citizens, children who

are handicapped or from less-privileged back-

grounds will enjoy complimentary access. “It

will be a theme park for everyone,” he says.

Ahead of its opening in August, Capital

World is also working with tour agencies and

organisations such as the Express & Excursion

Bus Association to promote the theme park

and mall. “We want to have busloads of peo-

ple visiting,” says Siow.

The groups he is targeting include day trip-

pers from Singapore, local Malaysians, as well

as other nationalities via Senai International

Airport, which receives international flights

from China, Indonesia, Macau, South Korea

and Thailand.

When fully completed in 2020, Capital City

will be a destination where people can live,

shop and play. It will also be a showcase of

Capital World’s capabilities as a developer and

a stepping stone into other markets. Accord-

ing to Siow, having a completed project un-

der its belt would make it easier to secure joint

ventures with partners who own land, which

is the company’s preferred business strategy.

Capital World’s development pipeline in-

cludes Austin City, another mixed-use pro-

ject in Johor Bahru; Sitiawan Wellness Hub,

a mixed-use project in Perak with a health

and wellness focus; and Pengerang Project, a

207.5 acre landed housing township in Kota

Tinggi, Johor.

The developer is keen to expand beyond

Malaysia, where its current projects are lo-

cated. “The market is vibrant in Singapore,

where we are listed,” says Siow. “We wish we

could be there.”

Siow: As long as the location and product are good, there will be demand

Capital City occupies a 439,726 sq ft site located 15 minutes from Woodlands Causeway

The theme park will feature several attractions, including Movie Planet (pictured), Cartoon Planet and Music Planet

Capital City’s retail component will also feature thematic zones inspired by five continentsCapital World’s development pipeline includes Aus-tin City, another mixed-use project in Johor Bahru

PICTURES: CAPITAL WORLD

ALBERT CHUA/THE EDGE SINGAPORE

E

EP12 • EDGEPROP | APRIL 2, 2018

Singapore — by postal district LOCALITIES DISTRICTSCity & Southwest 1 to 8

Orchard/Tanglin/Holland 9 and 10

Newton/Bukit Timah/Clementi 11 and 21

Balestier/MacPherson/Geylang 12 to 14

East Coast 15 and 16

Changi/Pasir Ris 17 and 18

Serangoon/Thomson 19 and 20

West 22 to 24

North 25 to 28

District 1 MARINA ONE RESIDENCES Apartment 99 years March 16, 2018 1,518 3,553,530 - 2,341 2017 New SaleTHE SAIL @ MARINA BAY Apartment 99 years March 19, 2018 678 1,250,000 - 1,843 2008 ResaleDistrict 2 DORSETT RESIDENCES Apartment 99 years March 15, 2018 484 1,000,000 - 2,064 2013 ResaleSKYSUITES@ANSON Apartment 99 years March 16, 2018 958 2,230,000 - 2,328 2014 ResaleWALLICH RESIDENCE AT TANJONG PAGAR CENTRE Apartment 99 years March 16, 2018 614 2,255,820 - 3,677 2017 New SaleWALLICH RESIDENCE AT TANJONG PAGAR CENTRE Apartment 99 years March 14, 2018 1,722 6,600,000 - 3,832 2017 New SaleDistrict 3 ARTRA Apartment 99 years March 13, 2018 1,227 2,159,800 - 1,760 Uncompleted New Sale

QUEENS Condominium 99 years March 14, 2018 915 1,200,000 - 1,312 2002 ResaleQUEENS PEAK Condominium 99 years March 18, 2018 1,001 1,751,000 - 1,749 Uncompleted New SaleQUEENS PEAK Condominium 99 years March 15, 2018 850 1,636,000 - 1,924 Uncompleted New SaleTHE CREST Condominium 99 years March 14, 2018 1,539 2,996,000 - 1,946 2017 ResaleTHE REGENCY AT TIONG BAHRU Condominium Freehold March 20, 2018 1,270 2,040,000 - 1,606 2010 ResaleDistrict 4 REFLECTIONS AT KEPPEL BAY Condominium 99 years March 19, 2018 1,012 1,500,000 - 1,482 2011 ResaleTHE OCEANFRONT @ SENTOSA COVE Condominium 99 years March 16, 2018 1,216 2,120,000 - 1,743 2010 ResaleDistrict 5 EALINE PARK Terrace Freehold March 14, 2018 2,282 3,080,000 - 1,348 1990 ResaleONE-NORTH RESIDENCES Apartment 99 years March 16, 2018 570 925,000 - 1,621 2009 ResaleREGENT PARK Condominium 99 years March 15, 2018 958 958,000 - 1,000 1997 ResaleTHE CLEMENT CANOPY Apartment 99 years March 16, 2018 990 1,477,000 - 1,491 Uncompleted New SaleTHE CLEMENT CANOPY Apartment 99 years March 15, 2018 990 1,426,000 - 1,440 Uncompleted New SaleTHE ORIENT Apartment Freehold March 18, 2018 721 1,380,300 - 1,914 2017 New SaleTHE ORIENT Apartment Freehold March 16, 2018 721 1,380,300 - 1,914 2017 New SaleTHE ORIENT Apartment Freehold March 13, 2018 990 1,845,000 - 1,863 2017 New SaleTHE PARC CONDOMINIUM Condominium Freehold March 14, 2018 2,174 1,980,000 - 911 2010 ResaleDistrict 7 BURLINGTON SQUARE Apartment 99 years March 13, 2018 732 910,000 - 1,243 1998 ResaleCONCOURSE SKYLINE Apartment 99 years March 19, 2018 861 1,711,320 - 1,987 2014 ResaleSOUTHBANK Apartment 99 years March 16, 2018 958 1,480,000 - 1,545 2010 ResaleDistrict 8 CITYLIGHTS Condominium 99 years March 13, 2018 560 975,000 - 1,742 2007 ResaleFLANDERS SQUARE Apartment Freehold March 19, 2018 1,335 1,180,000 - 884 Unknown ResaleKENTISH COURT Apartment 99 years March 19, 2018 1,259 1,220,000 - 969 1999 ResaleMERGUI MANSIONS Apartment Freehold March 15, 2018 1,389 1,330,000 - 958 1995 ResaleDistrict 9 ESPADA Apartment Freehold March 15, 2018 355 985,000 - 2,773 2013 ResaleILLUMINAIRE ON DEVONSHIRE Apartment Freehold March 15, 2018 441 939,000 - 2,128 2011 ResaleMARTIN MODERN Condominium 99 years March 13, 2018 764 2,131,200 - 2,789 Uncompleted New SaleMARTIN MODERN Condominium 99 years March 13, 2018 764 1,998,000 - 2,614 Uncompleted New SaleMARTIN MODERN Condominium 99 years March 13, 2018 764 2,158,240 - 2,824 Uncompleted New SaleMARTIN MODERN Condominium 99 years March 13, 2018 764 2,155,420 - 2,820 Uncompleted New SaleMARTIN MODERN Condominium 99 years March 13, 2018 764 2,129,100 - 2,786 Uncompleted New SaleMARTIN MODERN Condominium 99 years March 13, 2018 764 2,115,000 - 2,767 Uncompleted New SaleMARTIN MODERN Condominium 99 years March 13, 2018 764 2,115,000 - 2,767 Uncompleted New SaleMARTIN MODERN Condominium 99 years March 13, 2018 764 2,034,000 - 2,661 Uncompleted New SaleORCHARD SCOTTS Condominium 99 years March 16, 2018 2,174 3,450,000 - 1,587 2007 ResaleSUITES AT ORCHARD Apartment 99 years March 19, 2018 753 1,600,000 - 2,123 2014 Resale

| BY TIMOTHY TAY |

Sales at Wallich Residence at

Tanjong Pagar Centre have

picked up pace in March. So

far this month, four units were

sold at the ultra-luxury condo

perched on top of the 38-storey Guo-

co Tower at GuocoLand’s $3.2 billion

Tanjong Pagar Centre integrated devel-

opment, which is linked underground

to the Tanjong Pagar MRT station.

It is not just the 614 sq ft, one-bed-

room units that found buyers, but the

larger units on the higher floors too. In

fact, the highest psf price achieved so

far this year — $3,832 psf — was for

the 1,722 sq ft, three-bedroom unit on

the 57th floor, which fetched $6.6 mil-

lion. In the latest transaction, a one-bed-

room unit on the 48th floor was sold

for $2.26 million ($3,677 psf), accord-

ing to a caveat lodged on March 16.

Soaring 290m at its apex, Wallich

Residence is Singapore’s tallest tower.

The 181 units, which are a mix of one-

to four-bedroom types as well as pent-

houses, span the 39th to 64th floors.

Prices look like they are inch-

ing their way towards the $4,000 psf

threshold. That was the price achieved

for a 958 sq ft, two-bedroom unit on

the 55th floor; it was sold for $3.83

million last November. It is the high-

est psf price achieved at Wallich Res-

idence so far and has set a new price

benchmark for the CBD area.

Nearby, a 958 sq ft, three-bed-

room unit on the 70th floor of Sky-

suites @ Anson was sold for $2.23

million ($2,328 psf). The 360-unit,

99-year leasehold condominium was

developed by Allgreen Properties and

completed in 2014.

At the newly completed Marina One

Residences, which is part of an inte-

grated development by M+S, a joint

venture between Malaysia’s Khazan-

ah Nasional and Singapore’s Temasek

Holdings, a 1,518 sq ft, three -bedroom

unit on the sixth floor fetched $3.55

million ($2,341 psf).

Wallich Residence at Tanjong Pagar

Centre is not the only luxury develop-

ment where prices are reaching their

all-time highs. At Ardmore Park con-

do, a 2,885 sq ft, four-bedroom unit

on the 17th floor of one of the three

33-storey towers recently changed

hands for $10.4 million ($3,605 psf).

It last changed hands at the peak of

the property boom in August 2007 for

$8.2 million ($2,843 psf), according

to a caveat lodged then.

The latest price of $3,605 psf

achieved at Ardmore Park is close to

the all-time high of $3,688 psf, when

a four-bedroom unit on the 27th floor

changed hands for $10.64 million in

January 2010.

Unit at Wallich Residence sold for $3,832 psf

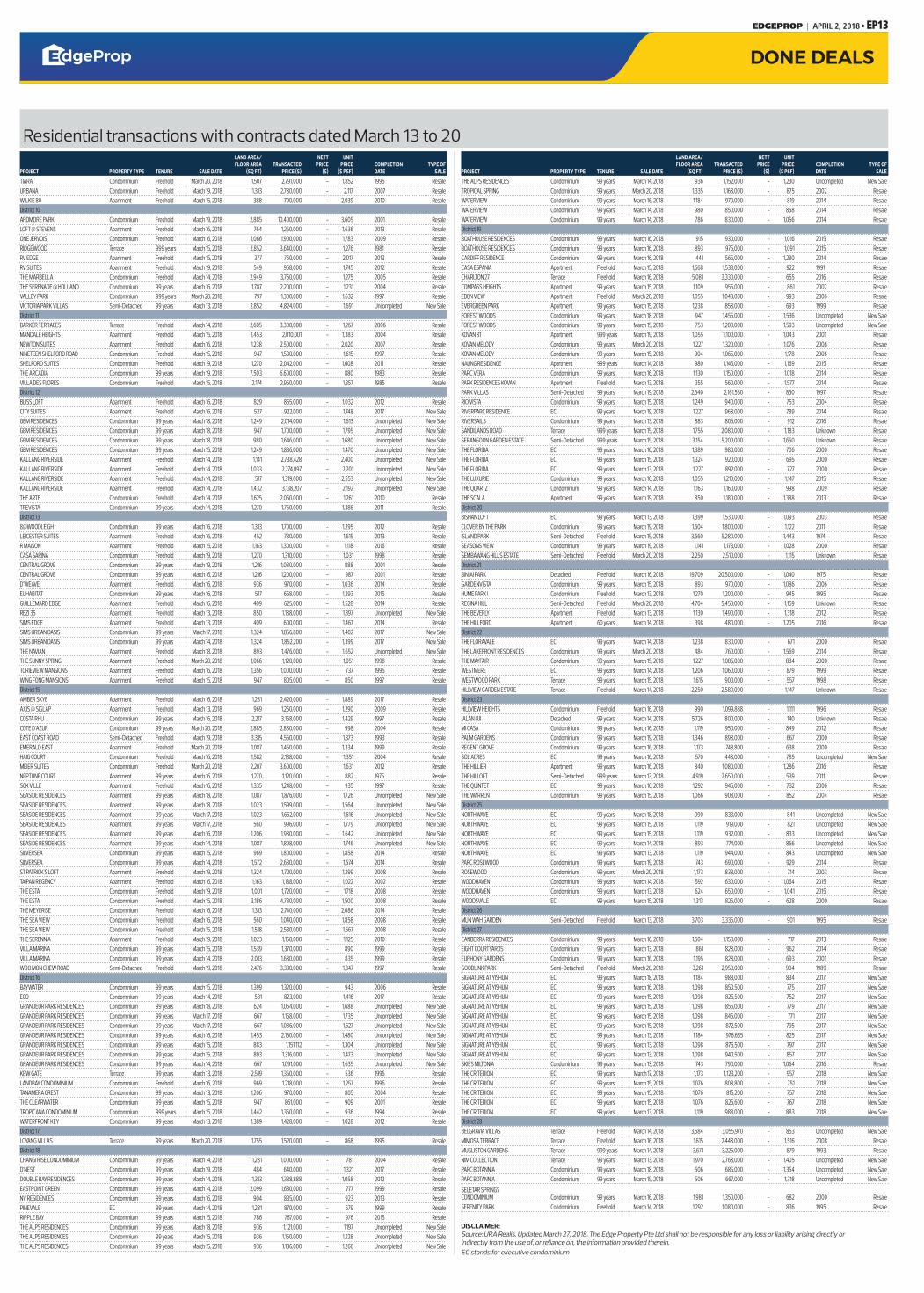

DONE DEALS

Residential transactions with contracts dated March 13 to 20

LAND AREA/ NETT UNIT FLOOR AREA TRANSACTED PRICE PRICE COMPLETION TYPE OFPROJECT PROPERTY TYPE TENURE SALE DATE (SQ FT) PRICE ($) ($) ($ PSF) DATE SALE

LAND AREA/ NETT UNIT FLOOR AREA TRANSACTED PRICE PRICE COMPLETION TYPE OFPROJECT PROPERTY TYPE TENURE SALE DATE (SQ FT) PRICE ($) ($) ($ PSF) DATE SALE

The 181-unit Wallich Residence sits atop the 38-storey Guoco Tower at Tanjong Pagar Centre

GUOCOLAND

E

EDGEPROP | APRIL 2, 2018 • EP13

LAND AREA/ NETT UNIT FLOOR AREA TRANSACTED PRICE PRICE COMPLETION TYPE OFPROJECT PROPERTY TYPE TENURE SALE DATE (SQ FT) PRICE ($) ($) ($ PSF) DATE SALE

LAND AREA/ NETT UNIT FLOOR AREA TRANSACTED PRICE PRICE COMPLETION TYPE OFPROJECT PROPERTY TYPE TENURE SALE DATE (SQ FT) PRICE ($) ($) ($ PSF) DATE SALE