health benefits 2007: a usa and california update jon r. gabel senior fellow national opinion...

Post on 19-Dec-2015

214 views

TRANSCRIPT

Health Benefits 2007:A USA and California Update

Jon R. Gabel

Senior Fellow

National Opinion Research Center

Presentation Objectives

To document the state of employer-based health benefits, 2007, in the US and California

To examine changes in benefits over the last year and five years

To examine trends in underlying health care expenses To examine the affordability of individual and small group

health insurance in California

• Telephone survey of 1,997 randomly selected public and private employers

• National Research conducts interviews with employee benefit managers from Jan. 2007 to May 2007

• Response rate of 49 percent in 2007• Survey conducted by HIAA 1987-1991 and KPMG 1991-1998• Use of statistical weights• Employer-based statistics• Employee-based statistics

KFF/HRET Health Benefits Survey

2007 California HealthCare Foundation/NORC Employer Health Benefits Survey

• Telephone survey of 805 randomly selected private employers with three or more workers.

• National Research conducts interviews with employee benefit managers from April 2007 to July 2007.

• Questionnaire is similar to KFF/HRET national survey.• Margin of error for responses among all employers is +/_

3.5 percent.

14.0%

8.5%7.70%

6.10%

12.0%

18.0%

9.2% *

0.8%

11.2% *

5.3% *

8.2% *

10.9% *

12.9% *

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Health Insurance PremiumsOverall InflationWorkers Earnings

Increases in Health Insurance Premiums Compared to Other Indicators, 1988-2007

* Estimate is statistically different from the previous year shown at p<0.05. No statistical tests were conducted for years prior to 1999.† Estimate is statistically different from the previous year shown at p<0.1. No statistical tests were conducted for years prior to 1999.

Note: Data on premium increases reflect the cost of health insurance premiums for a family of four.

Source: KFF/HRET Survey of Employer-Sponsored Health Benefits, 1999-2005; KPMG Survey of Employer-Sponsored Health Benefits, 1993, 1996; The Health Insurance Association of America (HIAA), 1988, 1989, 1990; Bureau of Labor Statistics, Consumer Price Index (U.S. City Average of Annual Inflation (April to April), 1988-2005; Bureau of Labor Statistics, Seasonally Adjusted Data from the Current Employment Statistics Survey (April to April), 1988-2005.

13.9%†

Cumulative Changes in Health Insurance Premiums, Overall Inflation, and Workers’ Earnings 2000 - 2007

0%

11%

25%

43%

60%

73%

87%

98%

0%3% 5%

7%10%

14%18%

20%

0%4%

7%10%

12%15%

20%24%

0%

20%

40%

60%

80%

100%

2000 2001 2002 2003 2004 2005 2006 2007

Health Insurance Premiums Overall Inflation Workers' Earnings

Source: KFF/HRET Survey of Employer-Sponsored Health Benefits, 2001-2006; Bureau of Labor Statistics, Consumer Price Index, U.S. City Average of Annual Inflation (April to April), 2001-2006; Bureau of Labor Statistics, Seasonally Adjusted Data from the Current Employment Statistics Survey (April to April), 2001-2006.

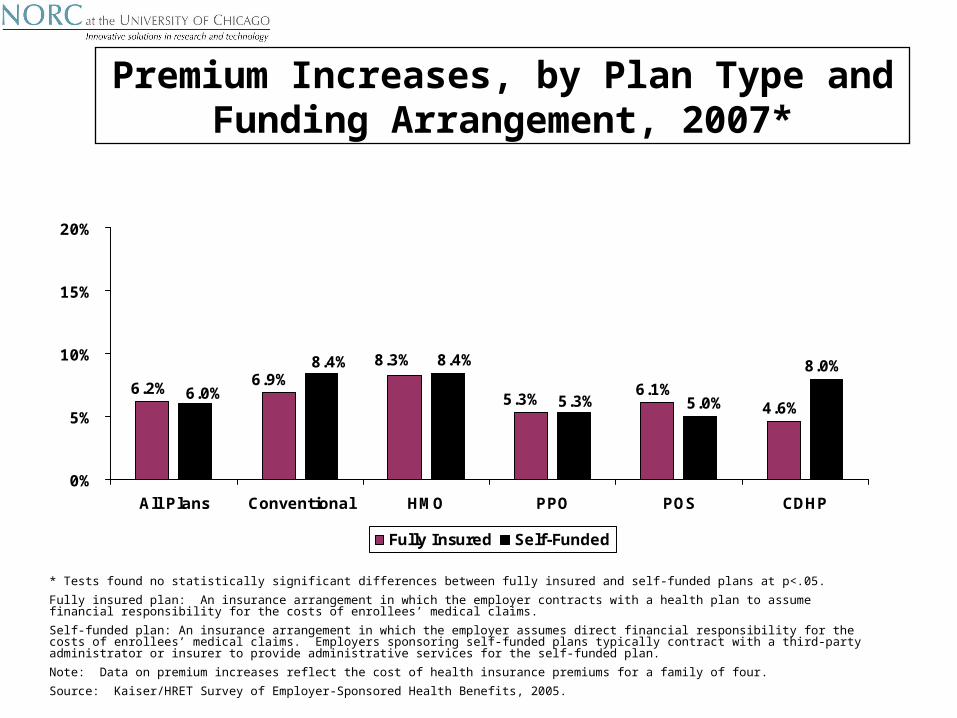

6.2% 6.1%4.6%

8.0%8.3%6.9%

5.3% 5.0%5.3%

8.4%8.4%

6.0%

0%

5%

10%

15%

20%

All Plans Conventional HMO PPO POS CDHP

Fully Insured Self-Funded

Premium Increases, by Plan Type and Funding Arrangement, 2007*

* Tests found no statistically significant differences between fully insured and self-funded plans at p<.05.

Fully insured plan: An insurance arrangement in which the employer contracts with a health plan to assume financial responsibility for the costs of enrollees’ medical claims.

Self-funded plan: An insurance arrangement in which the employer assumes direct financial responsibility for the costs of enrollees’ medical claims. Employers sponsoring self-funded plans typically contract with a third-party administrator or insurer to provide administrative services for the self-funded plan.

Note: Data on premium increases reflect the cost of health insurance premiums for a family of four.

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 2005.

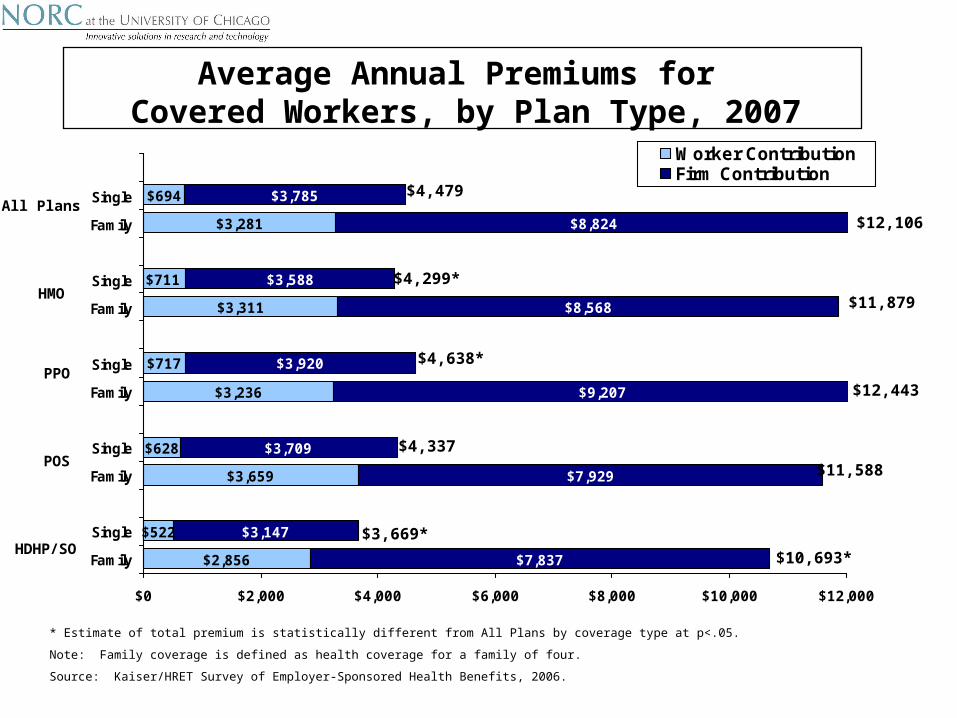

$694

$3,281

$3,311

$717

$3,236

$628

$3,659

$522

$2,856

$3,785

$3,588

$3,920

$3,709

$3,147

$711

$7,837

$7,929

$9,207

$8,568

$8,824

$0 $2,000 $4,000 $6,000 $8,000 $10,000 $12,000

Single

Family

Single

Family

Single

Family

Single

Family

Single

Family

Worker ContributionFirm Contribution

HDHP/SO

HMO

PPO

POS

All Plans

Average Annual Premiums for Covered Workers, by Plan Type, 2007

* Estimate of total premium is statistically different from All Plans by coverage type at p<.05.

Note: Family coverage is defined as health coverage for a family of four.

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 2006.

$4,479

$12,106

$4,299* $11,87

9

$4,638*

$12,443

$4,337

$11,588

$3,669* $10,693*

Increases in California Health Insurance Premiums Compared to National Trends,

1999-2007

8.3%

6.1%

8.7%

6.7%

4.8%

8.2%

11.4%

15.8%

13.4%

10.0%

7.7%

13.9%

12.9%

9.2%11.2%

5.3%

8.2%

10.9%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1999 2000* 2001 2002 2003* 2004 2005 2006* 2007

California Health Insurance Premiums National Health Insurance Premiums

• Health insurance premiums in California grew by 8.3% in 2007, significantly higher than the 6.1% rate of increase nationally.

Sources: CHCF/HSC California Employer Health Benefits Survey: 2005-2006; CHCF/HRET California Employer Health Benefits Survey: 2004; Kaiser/HRET California Employer Health Benefits Survey: 1999-2003; Kaiser/HRET Survey of Employer-Sponsored Health Benefits. 1999-2006.

* Estimates are statistically different between California and US.

Chart #9

Chart #10

Source: CHCF/HSC California Employer Health Benefits Survey: 2006

Average Percentage Increase in Health Insurance Premiums in California, by Firm Size, 2007

* Estimate is statistically different from all other firms.

8.3%

12.7%

11.0%

8.1%

10.0%

8.2%

7.3%

7.0%

0% 2% 4% 6% 8% 10% 12% 14%

All Large (200 orMore Workers)

(1000 or MoreWorkers)

(200-999 Workers)

All Small (3-199Workers)

(50-199 Workers)

(10-49 Workers)

(3-9 Workers)

All Firms

• Premium increases were greater for small employers than for large employers in 2007: small firms (3 to 199 workers) experienced average premium increases of 10.0%, compared with 7.3% for large firms (200 or more workers).

Note: Data are worker weighted.

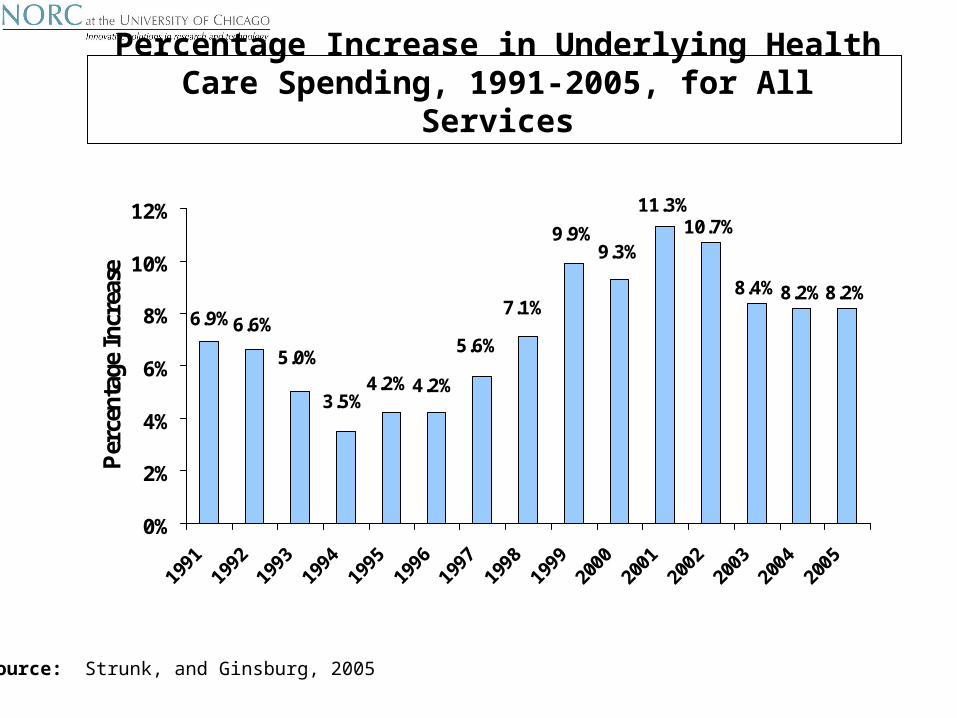

10.7%

8.4%8.2%8.2%

11.3%

9.3%9.9%

7.1%

5.6%

4.2%4.2%3.5%

5.0%

6.6%6.9%

0%

2%

4%

6%

8%

10%

12%

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

Per

cent

age

Incr

ease

Source: Strunk, and Ginsburg, 2005

Percentage Increase in Underlying Health Care Spending, 1991-2005, for All Services

-10

-5

0

5

10

15

20

Per

cen

tage

Hosp. Inpat. Hosp. Outpatient Physician Prescription Drug

Trends in Provider Revenues from Non-Medicare Patients, 1991 – 2005,

(Annual Percent Change Per Capita)

Health Plan Enrollments for Covered Workers, by Plan Type, 2001 – 2007, in California and the USA

7%

21%

20%

21%

25%

24%

27%

24%

47%

50%

49%

50%

52%

54%

54%

57%

60%

61%

55%

54%

52%

46%

35%

34%

34%

36%

29%

30%

25%

13%

13%

15%

15%

17%

18%

23%

13%

14%

17%

12%

17%

16%

21%

5%

4%

4%

2%

3%

3%

3%

5%

5%

4%

1%

1%

1%

1%

0% 20% 40% 60% 80% 100%

2007

2006

2005*

2004

2003*

2002*

2001

2007*

2006

2005*

2004*

2003

2002*

2001

Conventional HMO PPO POS HDHP/SO

• The percentage of covered workers enrolled in HMOs in California was considerably higher than nationally. Conversely, enrollment in PPOs in 2007 remained far lower in California than nationally.

• Enrollment in high-deductible plans with a savings option among California workers has increased from 2% in 2006 to 4% in 2007, a level comparable to the proportion nationally.

California

U.S.

Sources: CHCF/NORC California Employer Health Benefits Survey: 2007; CHCF/HSC California Employer Health Benefits Survey: 2005-2006; CHCF/HRET California Employer Health Benefits Survey: 2004; Kaiser/HRET California Employer Health Benefits Survey: 2001-2003; Kaiser/HRET Employer Health Benefits Survey: 2001-2007.

Note: Conventional plan enrollment in California in 2001, 2005 and 2007 is less than 1%. Due to the addition of HDHP in 2006, no test was conducted comparing 2006 with 2005.

* Distribution is statistically different from previous year shown.

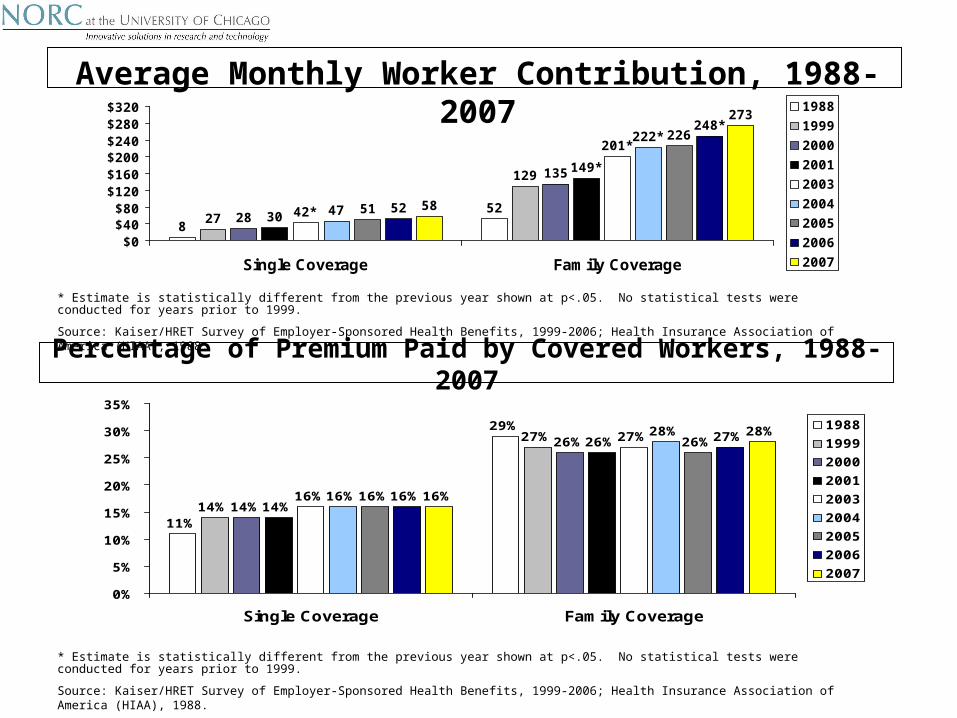

Average Monthly Worker Contribution, 1988-2007

852

129

28

135

30 47 51

226

52 58

273

27

149*

201*

42*

222*248*

$0$40$80

$120$160$200$240$280$320

Single Coverage Family Coverage

1988

1999

2000

2001

2003

2004

2005

2006

2007

* Estimate is statistically different from the previous year shown at p<.05. No statistical tests were conducted for years prior to 1999.

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 1999-2006; Health Insurance Association of America (HIAA), 1988.

11%

29%27%

14%

26%

14%

26%

16%

27%

16%

28%

16%

26%

16%

27%

16%

28%

14%

0%

5%

10%

15%

20%

25%

30%

35%

Single Coverage Family Coverage

1988

1999

2000

2001

2003

2004

2005

2006

2007

Percentage of Premium Paid by Covered Workers, 1988-2007

* Estimate is statistically different from the previous year shown at p<.05. No statistical tests were conducted for years prior to 1999.

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 1999-2006; Health Insurance Association of America (HIAA), 1988.

$186

$49

$204

$275

$44

$71

$323

$42

$72

$298

$92

$275*

$384*

$287

$210$220

$175

$327$327

$0

$100

$200

$300

$400

HMO PPO POS

1999

2001

2003

2004

2005

2006

2007

* Estimate is statistically different from the previous year shown at p<.05.

^ Information was not obtained for HMO single coverage prior to 2003.

Note: Average deductibles for PPO and POS plans are for in-network services. Averages include covered workers who do not have a deductible. If covered workers with no deductible are excluded from the calculation, the average deductibles for single coverage for 2005 are as follows: conventional - $671; HMO - $568; PPO -$445; POS - $495.

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 1999-2005.

Average Annual Deductibles for Single Coverage, by Plan Type, 1999-2007

^ ^

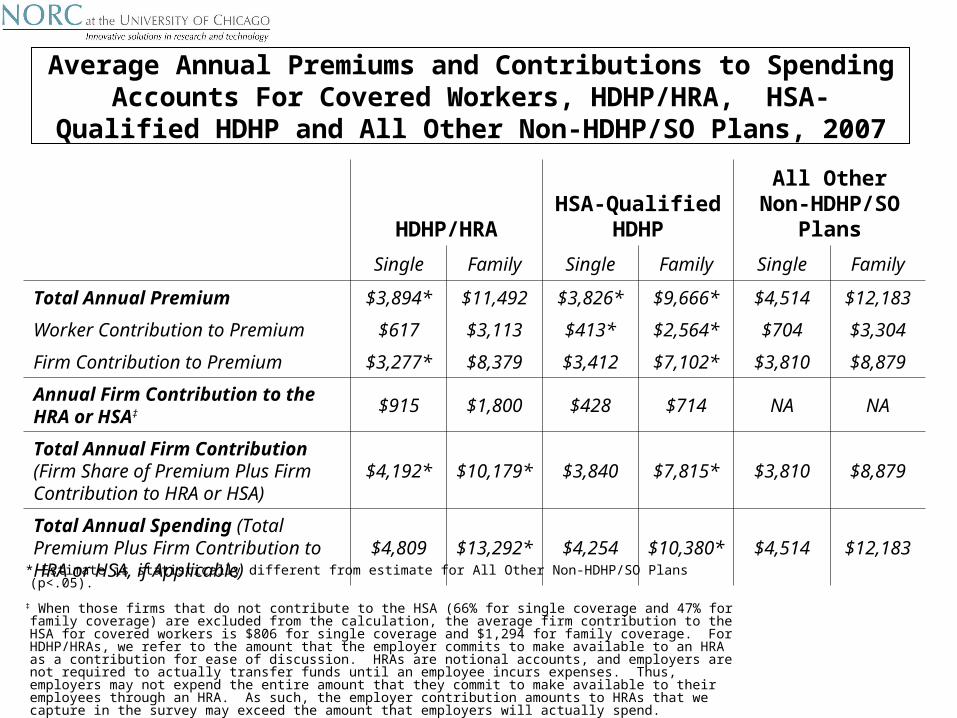

* Estimate is statistically different from estimate for All Other Non-HDHP/SO Plans (p<.05).

‡ When those firms that do not contribute to the HSA (66% for single coverage and 47% for family coverage) are excluded from the calculation, the average firm contribution to the HSA for covered workers is $806 for single coverage and $1,294 for family coverage. For HDHP/HRAs, we refer to the amount that the employer commits to make available to an HRA as a contribution for ease of discussion. HRAs are notional accounts, and employers are not required to actually transfer funds until an employee incurs expenses. Thus, employers may not expend the entire amount that they commit to make available to their employees through an HRA. As such, the employer contribution amounts to HRAs that we capture in the survey may exceed the amount that employers will actually spend.

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 2007.

Average Annual Premiums and Contributions to Spending Accounts For Covered Workers, HDHP/HRA, HSA-Qualified HDHP

and All Other Non-HDHP/SO Plans, 2007

HDHP/HRAHSA-Qualified

HDHPAll Other Non-

HDHP/SO Plans

Single Family Single Family Single Family

Total Annual Premium $3,894* $11,492 $3,826* $9,666* $4,514 $12,183

Worker Contribution to Premium $617 $3,113 $413* $2,564* $704 $3,304

Firm Contribution to Premium $3,277* $8,379 $3,412 $7,102* $3,810 $8,879

Annual Firm Contribution to the HRA or HSA‡ $915 $1,800 $428 $714 NA NA

Total Annual Firm Contribution (Firm Share of Premium Plus Firm Contribution to HRA or HSA)

$4,192* $10,179* $3,840 $7,815* $3,810 $8,879

Total Annual Spending (Total Premium Plus Firm Contribution to HRA or HSA, if Applicable)

$4,809 $13,292* $4,254 $10,380* $4,514 $12,183

55%57%

58%

54% 53%

50%

53%

50%

66% 67%69% 69%

68% 68%66%

63%65%

62%63%

65%63%

62%61%

59% 59%

50% #

60% #

40%

45%

50%

55%

60%

65%

70%

75%

80%

1999 2000 2001 2002 2003 2004 2005 2006 2007

All Small Firms (3-199 Workers)

All Large Firms (200 or More Workers)

All Firms

Percentage of Workers Covered by Their Employer’s Health Benefits, in Firms Both Offering and Not Offering Health

Benefits, by Firm Size, 1999-2007

# Year-to-year estimates are not significantly different at p<.05. However, there is a significant change between 2000 and 2005 for All Firms and All Small Firms at p<.05.

Source: KFF/HRET Survey of Employer-Sponsored Health Benefits, 1999–2005.

Increase in Productivity Growth versus Real Wage Growth, 1970-2006

100

120

140

160

180

200

220

Cumulative productivity growth Cumulative median real wage growth

1970 2006

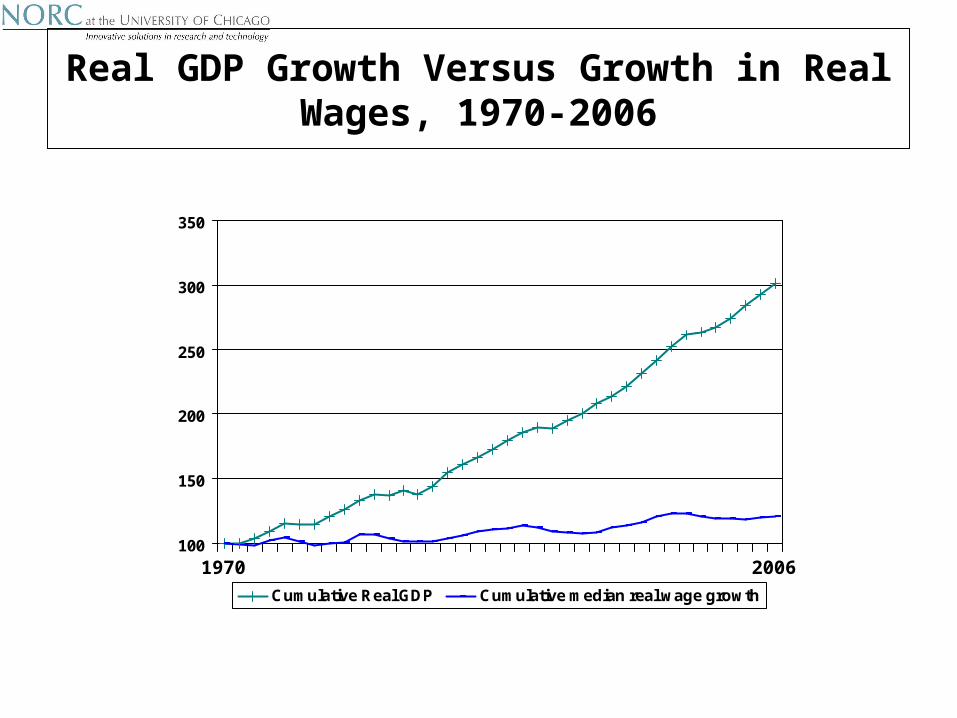

Real GDP Growth Versus Growth in Real Wages, 1970-2006

100

150

200

250

300

350

Cumulative Real GDP Cumulative median real wage growth

1970 2006

Percentage of Income Spent on Premiums and Expected out-of-pocket Medical Expenses, 2006, for Single Persons in Small

Group and Individual Insurance Market in California

3.5%

11.0%

5.5%

2.8%

7.7%

16.1%

50.3%

25.2%

12.6%

35.1%

0% 10% 20% 30% 40% 50% 60%

Median Income

100% of Poverty

200% of Poverty

400 Percent ofPoverty

FT MinimumWage

Individual

Small Group

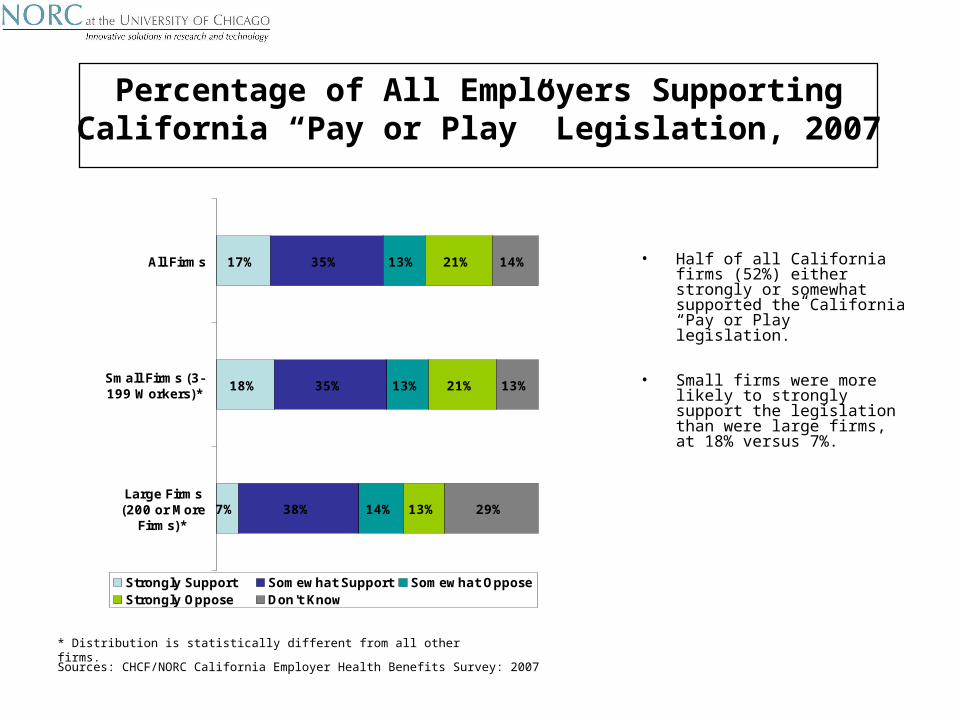

Percentage of All Employers Supporting California “Pay or Play” Legislation, 2007

7%

18%

17%

38%

35%

35%

14%

13%

13%

13%

21%

21%

29%

13%

14%

Large Firms(200 or More

Firms)*

Small Firms (3-199 Workers)*

All Firms

Strongly Support Somewhat Support Somewhat OpposeStrongly Oppose Don't Know

• Half of all California firms (52%) either strongly or somewhat supported the California “Pay or Play” legislation.

• Small firms were more likely to strongly support the legislation than were large firms, at 18% versus 7%.

Sources: CHCF/NORC California Employer Health Benefits Survey: 2007

* Distribution is statistically different from all other firms.

Distribution of Firms’ Opinions on the Effectiveness of the Following Cost Containment Strategies, 2007

*Distributions are statistically different between All Small Firms and All Large Firms within category (p<.05).

Note: Distributions are among all firms both offering and not offering health benefits.

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 2007.

Tighter Managed Care Networks*

35%

28%

14%

12%

17%

15%

4%

16%

50%

43%

47%

46%

52%

53%

42%

39%

9%

12%

26%

18%

19%

13%

35%

4%

13%

12%

19%

8%

12%

17%

15%

4%

11%19%

7%

2%

2%

4%

2%

5%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

All Large Firms

All Small Firms

All Large Firms

All Small Firms

All Large Firms

All Small Firms

All Large Firms

All Small Firms

Very Effective Somewhat Effective Not Too Effective Not At All Effective Don't Know

Higher Employee Cost Sharing*

Consumer-Driven Health Plans

Disease Management Programs*

Summary, Conclusions, and Projections

• Economic slowdown will greatly affect health care.– Continued moderation in expenses and premiums– Substantial decline in employer-based coverage

• High cost of coverage makes both health care unaffordable to many Americans, but also makes the solution unaffordable.

• CDHP growth modest, but not meeting expectations.• Economic slowdown may boost CDHP and more

restrictive managed care.• More aggressive wellness efforts on the part of

employers.

Percentage of California Employers Agreeing That All Firms Bear Some Responsibility For Providing Health

Benefits, 2007

• Two-thirds of all California firms agreed that employers bear some responsibility for providing health benefits.

• Eighty-eight percent of all large firms (200 or more workers) agreed that all firms bear some responsibility for providing health benefits, with nearly half (48%) strongly supporting that statement.

48%

33%

33%

40%

33%

33%

13%

13%

18%

18%

7%

3% 2%

3%

3%

Large Firms ( 200+Workers)*

Small Firms (3-199Workers)*

All Firms

Strongly Agree Somewhat Agree Somewhat DisagreeStrongly Disagree Don't Know

Sources: CHCF/NORC California Employer Health Benefits Survey: 2007

* Distribution is statistically different from all other firms.

Mean versus Median Income Growth, 1970-2006

100

110

120

130

140

150

160

170

Median Income Mean Income1970 2006

Percentage of Workers with Single/Single Plus One/Family Coverage in California, Massachusetts,

and Nationally, 20071

44%

45%

46%

18%

8%

19%

38%

47%

35%

0% 20% 40% 60% 80% 100%

U.S.

Massachusetts*

California

Single Single Plus One Family

• The percentage of California workers enrolled in single, single plus one, and family coverage is similar to the national distribution.

• However, when compared to Massachusetts, a state experiencing changes to its employer-sponsored health system by legislative mandate, the enrollment distribution is significantly different. In particular, there appears to be little differentiation between single plus one and family coverage in Massachusetts as compared to California.

Source: CHCF/NORC California Employer Health Benefits Survey: 2007; RWJF/KSC Massachusetts Employer Health Benefits Survey: 2007; Kaiser/HRET Employer Health Benefits Survey: 2006.

* Distribution is statistically different from California. 1 U.S. estimates are from 2006.

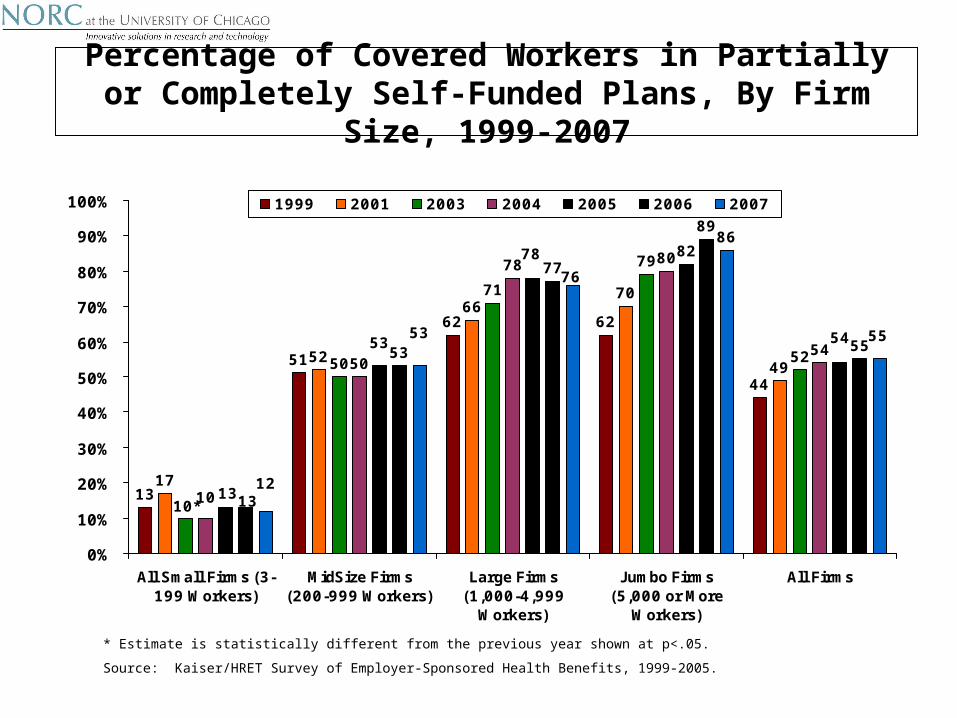

Percentage of Covered Workers in Partially or Completely Self-Funded Plans, By Firm Size, 1999-2007

44

6262

51

13

49

7066

52

17

52

79

71

50

10*

54

8078

50

10

54

8278

53

13

55

89

77

53

13

55

86

76

53

12

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

All Small Firms (3-199 Workers)

MidSize Firms(200-999 Workers)

Large Firms(1,000-4,999

Workers)

Jumbo Firms(5,000 or More

Workers)

All Firms

1999 2001 2003 2004 2005 2006 2007

* Estimate is statistically different from the previous year shown at p<.05.

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 1999-2005.

Percentage of California Firms Offering Health Benefits to Domestic Partners such as Unmarried Opposite Sex

and Same Sex Couples, 2007

69%

66%

47%

37%

0% 10% 20% 30% 40% 50% 60% 70% 80%

UnmarriedHeterosexual

Couples Eligible forHealth Benefits*

Unmarried Same-sex Couples Eligible

for HealthBenefits*

California U.S.

• Nearly seven of every ten firms in California offered health benefits to domestic partners in 2007.

• Firms in California were more likely to offer health benefits to domestic partners than in the rest of the US.

Sources: CHCF/NORC California Employer Health Benefits Survey: 2007; Kaiser/HRET Survey of Employer-Sponsored Health Benefits: 2007

* Estimates are statistically different between California and US.

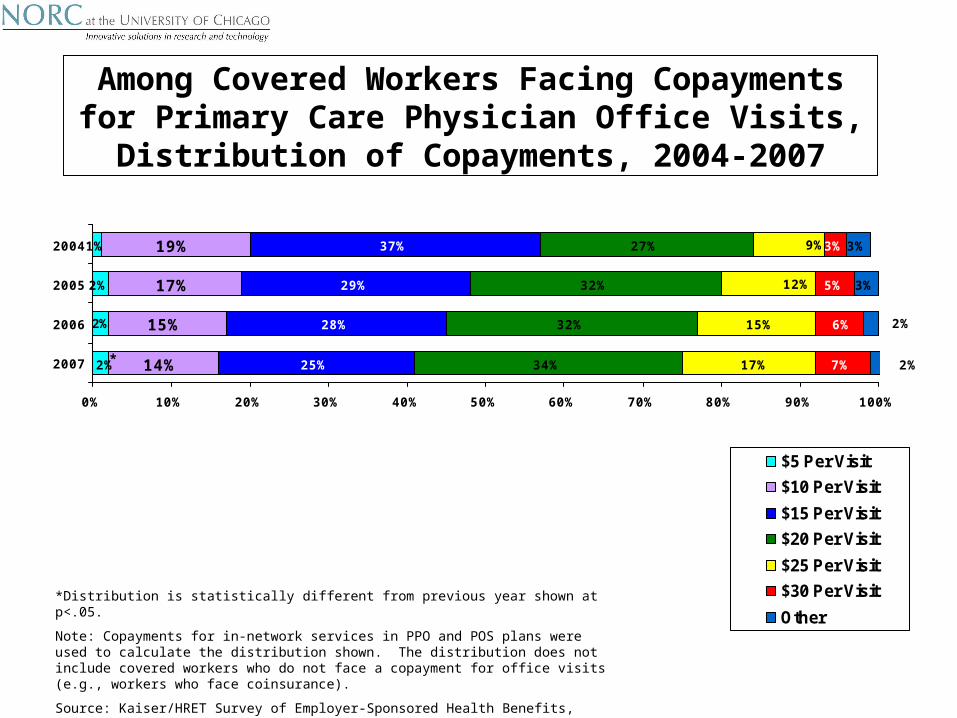

2%

1%

14%

17%

19%

25%

28%

29%

37%

34%

32%

32%

27%

7%

5%

3%

3%

3%

2%

2%

15%

17%

15%

12%

9%

6%

2%

2%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

2007

2006

2005

2004

$5 Per Visit

$10 Per Visit

$15 Per Visit

$20 Per Visit

$25 Per Visit

$30 Per Visit

Other

Among Covered Workers Facing Copayments for Primary Care Physician Office Visits, Distribution of

Copayments, 2004-2007

*Distribution is statistically different from previous year shown at p<.05.

Note: Copayments for in-network services in PPO and POS plans were used to calculate the distribution shown. The distribution does not include covered workers who do not face a copayment for office visits (e.g., workers who face coinsurance).

Source: Kaiser/HRET Survey of Employer-Sponsored Health Benefits, 2004 - 2005.

*