hedging under ifrs - world banksiteresources.worldbank.org/extcenfinrepref/resources/4152117... ·...

TRANSCRIPT

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation.

International Financial Reporting Standards

Hedging under IFRS Executive IFRS Workshop for

Regulators

3-6 June 2014, Vienna

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Darrel Scott IASB Board Member

2

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Applicable standards

• IAS 39 hedging standard (general and portfolio hedging)

currently required

• IFRS 9 general hedging standard published:

– Early adoption allowed

– Mandatory adoption after 1 January 2018

– However entity can elect to continue applying IAS 39 until

Macro hedging introduced

• Macro Hedging model at discussion paper stage

Grandfathering of IAS 39 3

IFRS 9 HA

model

IAS 39 HA

model

‘macro

FVH’

‘macro

FVH’ Scope-out

‘macro

CFH’

‘macro

CFH’

Accounting

policy choice

Early application

No early application

‘Status quo’ pending completion of the project on accounting for macro hedging:

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

IAS 39

5

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Introduction

• ‘Hedging’ and ‘hedge accounting’ are two different things

• What is hedging?

– managing risks by using one financial instrument

(‘hedging instrument’) purposely to offset the variability in

FV or cash flows of a recognised asset or liability, firm

commitment, or future cash flows (‘hedged item’)

6

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Hedge Accounting

• Matching the change in FV of the hedging instrument and

the hedged risk in profit or loss

• Arises when normal accounting puts changes in

economic values in different periods - ‘accounting

mismatch’

• Hedge accounting subject to strict conditions:

– Formal designation and documentation of a hedge,

– the hedging instrument must be expected to be highly

effective in achieving offsetting changes in fair value or

cash flows of the hedged item that are attributable to the

hedged risk.

7

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Requirements

• Hedge accounting:

– Is an election

– Can only be applied prospectively

– Effectiveness testing must be performed each reporting

date and offset of fair value changes must be within 80–

125% of each other

• Hedging instrument must be a derivative but not be

written option (except for hedges of FX risk)

• Hedged item

– Entire item, group of items, or a hedged risk that is reliably

measurable

8

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Types of Hedge Accounting Fair value hedge accounting

• Hedge exposure to fair value changes of asset or liability

or firm commitment (or portion attributable to a particular

risk)

• Recognise of gains and losses on hedged item and

hedging instrument in profit and loss and adjust the

carrying amount of the hedged item

• Examples

– Fixed-rate debt

– Inventory

– Firm commitment to buy a commodity at a fixed price

9

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Types of Hedge Accounting Cash flow hedge accounting

• Hedge of exposure to variability in cash flows of:

– a recognised asset or liability or

– a highly probable forecast transaction

• Hedge of the foreign currency risk of a firm commitment

• Gains and losses on effective portion of hedge in OCI

• Gains and losses on ineffective portion of hedge in P&L

• Examples

– Forecast purchases/sales at prevailing commodity prices

– Floating-rate debt

– Forecast debt issuance

10

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Types of Hedge Accounting Net investment in foreign operation

• Hedge of a net investment in a foreign operation

– As defined in IAS 21

– Accounted for similarly to cash flow hedges

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

IFRS 9

12

• Greater alignment with risk management including:

– Eligibility criteria based on more economic assessment of

hedging relationship

– Expansion of risk components for non-financial items

– Introduction of ‘costs of hedging’

– Ability to hedge aggregated exposures (combination of

derivative and non-derivative)

• Enhanced disclosures

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Introduction

Hedged items 13

Qualifying

hedged item

Entire item Component

Risk component (separately identifiable and reliably

measurable)

Nominal component or

selected contractual CFs

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Hedged items: risk components

Benchmark

(eg interest

rate or

commodity

price)

Benchmark

(eg interest

rate or

commodity

price)

Variable

element

Fixed element

Benchmark

(eg interest

rate or

commodity

price)

Benchmark

(eg interest

rate or

commodity

price)

Variable

element

Fixed element

IAS 39 New model

14

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Hedged items: aggregated exposures

Aggregated exposure—combination of: (a) another exposure and

(b) a derivative

[non-derivative]

exposure derivative

Hedging

instrument

Hedged item

First level

relationship

Second

level

relationship

15

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Hedged items: aggregated exposures

Example: hedging commodity price & FX risk

Aggregated

exposure

Manufacturer

Commodity

futures

contract

Commodity

supplier US$

US$

€

FX forward

contract

Not an eligible

hedged item

under IAS 39

US$

US$

16

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Hedging instruments 17

Qualifying hedging

instruments

Entire item Partial designation

FX risk component Proportion of nominal

amount

• Intrinsic value

• Spot element

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Costs of hedging 18

Time value

of options

Transaction

related

hedged item

Time period

related hedged

item

Costs of hedging

Forward element

of forward

contract

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

19 Option: time value

Treatment as a cost of hedging

reflects economics

Accounting if the hedged item is transaction related

Life of option

Cumulative

gain in OCI

T0 Expiry

t

Cumulative

loss in OCI

Release from

accumulated OCI

to P/L or as a

basis adjustment

Time

value

paid

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

20

Treatment as a cost of hedging

reflects economics

Accounting if the hedged item is time period related

Life of option

Cumulative

gain in OCI

Cumulative loss

in OCI

Time

value

paid

T0 Expiry

Cumulative amortisation

of initial time value

t

Time value is

amortised to

P/L over life

Option: time value

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Hedge effectiveness 21

Hedge

effectiveness

Hedge effectiveness test:

1. Economic relationship

2. Effect of credit risk

3. Hedge ratio

Measuring and recognising

hedge ineffectiveness

Rebalancing Discontinuation

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Disclosures 22

Hedge accounting

disclosures

Risk

management

strategy

Amount, timing

and uncertainty

of future

cash flows

Effects of hedge

accounting on

the primary

financial

statements

Specific

disclosures for

dynamic

strategies and

credit risk

hedging

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

International Financial Reporting Standards

The views expressed in this presentation are those of the presenter,

not necessarily those of the IASB or IFRS Foundation

Macro Hedging

24

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

At a glance

• The IASB explores an accounting approach to better

reflect dynamic risk management (RM) activities in

entities’ financial statements.

• The Discussion Paper (DP) uses dynamic interest rate

risk management by banks for illustrative purposes.

However, the approach considered in the DP is intended

to be applicable to other risks (for example, commodity

price risk and FX risk).

25

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

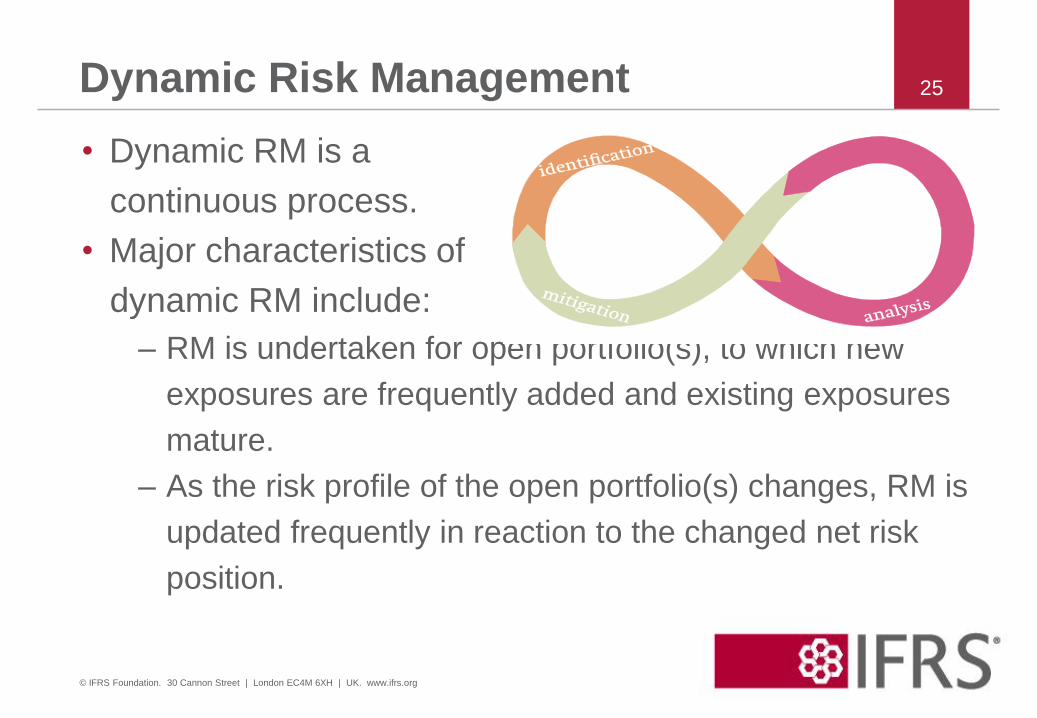

Dynamic Risk Management

• Dynamic RM is a

continuous process.

• Major characteristics of

dynamic RM include:

– RM is undertaken for open portfolio(s), to which new

exposures are frequently added and existing exposures

mature.

– As the risk profile of the open portfolio(s) changes, RM is

updated frequently in reaction to the changed net risk

position.

Dynamic interest rate RM in banks 26

The purpose of dynamic RM is usually to

manage Net Interest Income

Portfolio Revaluation Approach (PRA)

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

27

• Exposures within open portfolios are revalued with respect to

the managed risk (for example, interest rate risk).

• Not a full fair value model.

• The net effect between the revaluation adjustment of the

managed exposures and the fair value changes of the risk

management instruments (for example, interest rate swaps)

is reflected in profit or loss.

The PRA (continued)

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

28

29

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Expected improvements with the PRA

• Enhances information about dynamic RM;

• Reduces operational complexities such as tracking and

amortisations;

• Captures the dynamic nature of RM on a net basis;

• Considers behavioural factors;

• Considers different types of risks managed in open

portfolios.

30

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Scope of the application of the PRA

• The scope has significant implications on the information

provided to users of financial statements and on how

operationally feasible the application of the PRA will be

for an entity.

• The DP considers two scope alternatives:

– Focus on dynamic risk management

– Focus on risk mitigation (sub-portfolio approach,

proportional approach)

31

© IFRS Foundation. 30 Cannon Street | London EC4M 6XH | UK. www.ifrs.org

Questions