helena s. valderrama, ph.d. professor, cesar e. a. virata ... · university of the philippines...

TRANSCRIPT

Helena S. Valderrama, Ph.D. Professor, Cesar E. A. Virata School of Business

University of the Philippines Diliman

BSP – UP Professorial Chair Lectures 14 May 2014

Study Objectives Assess the financial reporting practices of GSIS and

the information available for outsiders to evaluate the fund’s financial condition and performance

Estimate the financial return earned by members on

their GSIS contributions

Methodology and Limitations Methodology Studied the financial statements available in the

website of the GSIS; checked compliance with relevant accounting standards

Developed a simple model to estimate the return on GSIS contributions for retirement benefits; attempted to obtain benchmarks from private sector

Limitations Relied completely on information provided in the

financial statements No direct benchmark for GSIS retirement plan

Background SSL 3 – salary increases of 34-69% granted to

government employees (implemented in tranches from 2009 to 2012)

Role of pension systems in social security and protection

Reforms needed in Philippine pension systems Financial reporting as an important governance

mechanism

The GSIS Created by Commonwealth Act No. 186 in 1936 to implement

the laws that govern the social security and insurance benefits of all government employees

Other laws defining GSIS’ mandate, authority and functions: RA No. 656 (1951) and PD No. 626 (1975) mandated the GSIS to

administer the Employees Compensation and State Insurance Fund and the General Property Insurance Fund, respectively

PD No. 1146 (1977) and RA No. 8291 (1997) amended CA 186 and enhanced the social security coverage of the GSIS

RA No. 10149 (2011) identifies the GSIS as a government-owned or -controlled corporation (GOCC), particularly a government financial institution (GFI), and prescribes mechanisms to strengthen the governance of all GOCCs

GSIS Governance and Supervision INTERNAL - GSIS Board of Trustees 3 representatives from government employee organizations

or associations (including President of PPSTA or PASS) Lawyer (should be a GSIS member) 4 members coming from the banking, finance, investment,

and insurance sectors GSIS President and General Manager (ex-officio Vice

Chairman)

EXTERNAL Commission on Audit Insurance Commission Governance Commission for Government-Owned or -

Controlled Corporations

GSIS Governance and Supervision Commission on Audit

has exclusive authority to examine and audit the accounts of all government entities, including GOCCs

Has exclusive authority to promulgate the accounting rules and regulations for government entities (Art IX, 1987 Philippine Constitution)

Do special audit of 30 biggest GOCCs to determine compliance with generally accepted accounting principles and standards and whether financial statements “present fairly and comprehensively the GOCC’s financial position and the results of its financial operations” (RA 10149, GOCC Act of 2011)

GSIS Governance and Supervision Insurance Commission

make an examination of the financial condition and methods of transacting business of the GSIS at least once every three (3) years (RA 8291 para 48)

Governance Commission for GOCCs Central advisory, monitoring and oversight body for

GOCCs

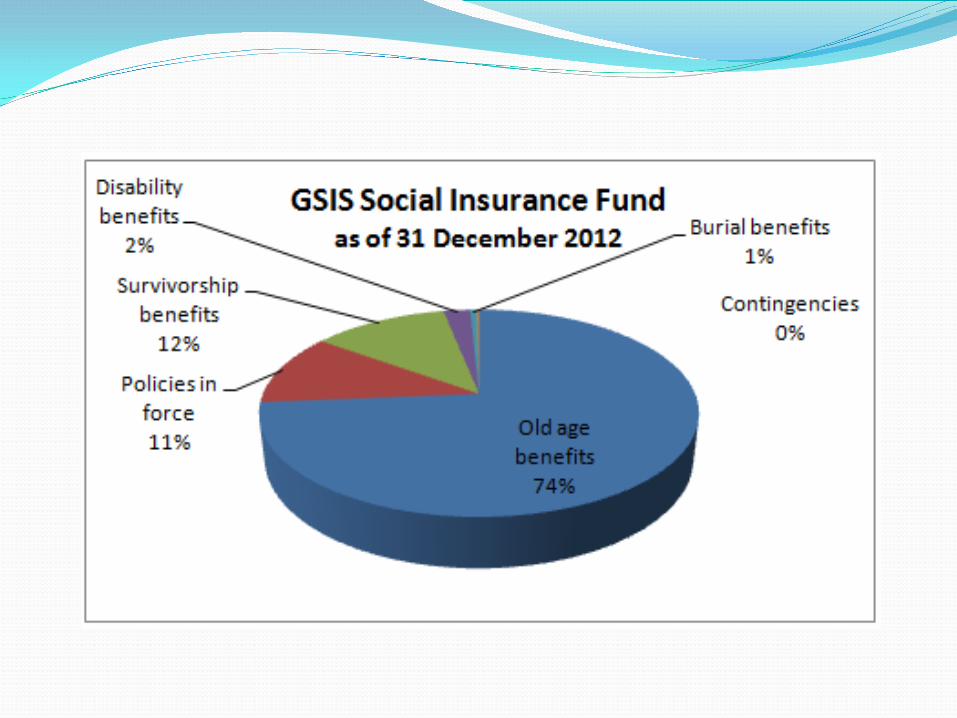

GSIS Social Security Benefits 1. Separation 2. Retirement 3. Permanent disability benefits 4. Survivorship 5. Funeral benefit 6. Life Insurance 7. Optional insurance – life, health, hospitalization,

education, memorial plans

GSIS Contributions and Retirement Benefits GSIS members contribute 21% of their monthly

compensation to the Social Insurance Fund (SIF) – 9% personal share, 12% employer share; 4% life insurance coverage, 17% for retirement benefits

Basic monthly pension upon retirement depends on – 1. Average monthly compensation during last 36 months

of service 2. Length of service

Retiring employees have 2 options: (a) 5-year lump sum payment + monthly pension beginning year 6 and (b) 18-month lump sum payment + monthly pension immediately after retirement

Quality of Financial Reporting Source of financial reporting standards Financial reporting objectives

Information regarding quality and sufficiency of assets Information regarding the fund’s estimated current and

future obligations Information regarding the risks the fund is exposed to,

and how management is addressing these risks Information regarding the institution’s operating

efficiency

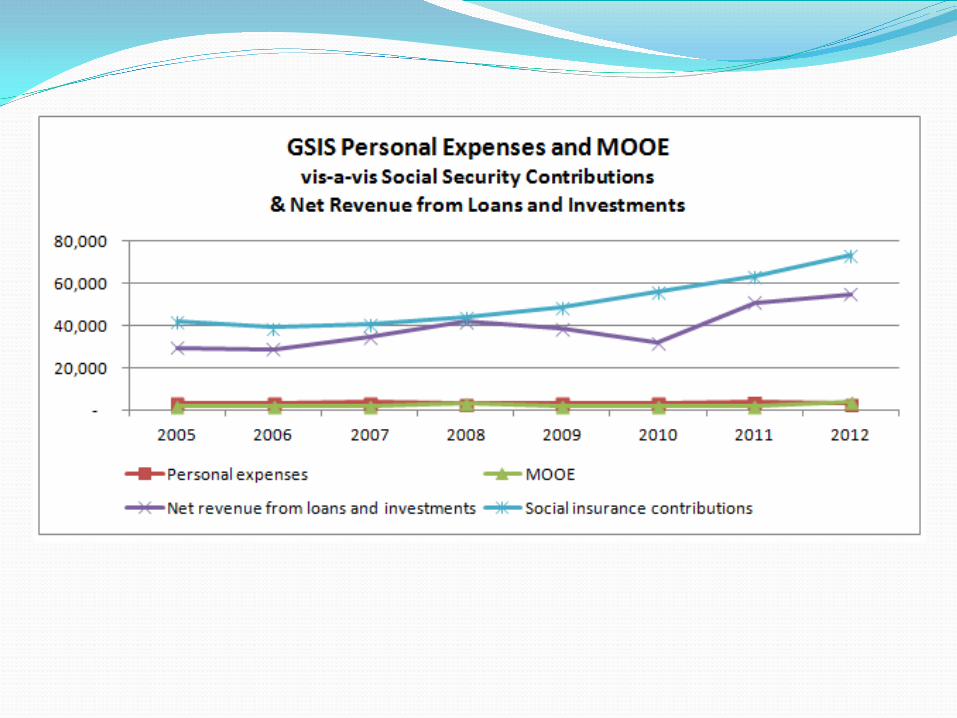

Ave return on loans = 11%

Ave return on investments = 9%

Findings in the Reporting of Liabilities Actuarial Reserves and Financial Reserves

Actuarial reserves are the estimated amount of the obligations of the System under RA 8291.

Financial reserves are the amounts set aside and appropriated from the surplus of a fund to ensure the payment of future obligations as estimated by actuarial reserves”

Source: GSIS 2012 Annual Report, Note 16 of the Notes to the Financial Statements

GSIS recognises financial reserves, not actuarial reserves in its Statement of Financial Condition.

Findings in the Reporting of Liabilities For its insurance activities, GSIS is governed by PFRS 4

(standard on Insurance Contracts) that requires the annual conduct of a liability adequacy test.

“An insurer shall assess at each reporting date whether its recognised insurance liabilities are adequate, using current estimates of future cash flows under its insurance contracts. If that assessment shows that the carrying amount of its insurance liabilities... is inadequate in the light of the estimated future cash flows, the entire deficiency shall be recognised in profit or loss.” [PFRS 4 para 15]

The GSIS disclosed that a liability adequacy test was conducted for the Social Insurance Fund in 2010. The same note was repeated in 2011. No disclosure on the conduct of a LAT is made in the 2012 financial statements.

Estimating the Returns on GSIS Contributions Under SSL3

PENSION

What rate of return is earned by the contributions to make its future value equal to the present value of the member’s pension benefits?

Assumptions 1. Member starts making contributions at age 24, and does

this continuously until the compulsory retirement age in government of 65.

2. The member starts at SG 16 (P28,080/month). This is the starting SG of an Instructor IV at the UP Virata School of Business and, consistent with GSIS actuarial assumptions, the member enjoys a 5% salary rate increase annually.

3. Upon retirement, the member chooses the 18month lump sum + immediate monthly pension option. The basic monthly pension is pegged at the ceiling of 90% of the average monthly compensation.

4. The member retires “permanently” at age 70. Based on the World Health Organization, as of 2012, the life expectancy at birth is 65 years for Filipino men and 72 years for women.

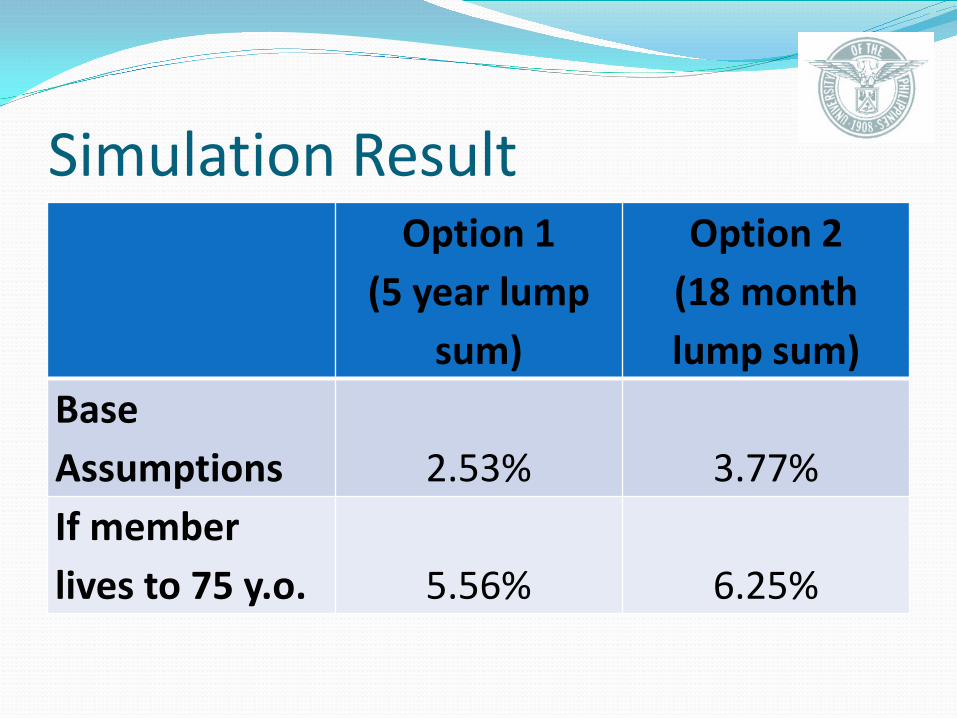

Simulation Result

Option 1 (5 year lump

sum)

Option 2 (18 month lump sum)

Base Assumptions 2.53% 3.77% If member lives to 75 y.o. 5.56% 6.25%

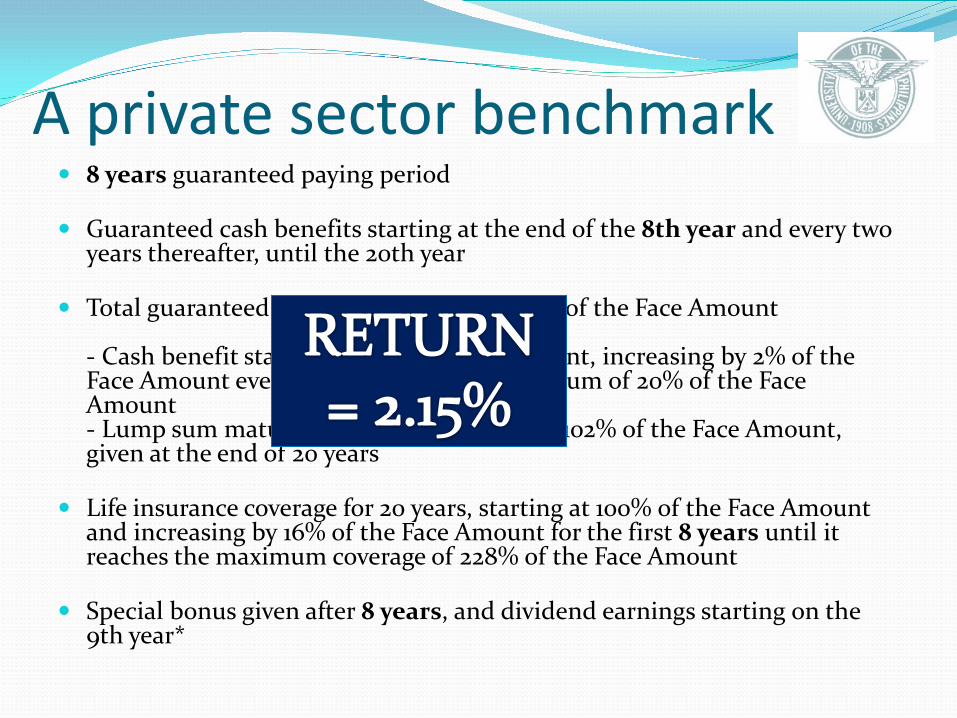

A private sector benchmark 8 years guaranteed paying period

Guaranteed cash benefits starting at the end of the 8th year and every two

years thereafter, until the 20th year

Total guaranteed cash benefits equals 200% of the Face Amount - Cash benefit starts at 8% of the Face Amount, increasing by 2% of the Face Amount every two years, up to a maximum of 20% of the Face Amount - Lump sum maturity benefit amounting to 102% of the Face Amount, given at the end of 20 years

Life insurance coverage for 20 years, starting at 100% of the Face Amount and increasing by 16% of the Face Amount for the first 8 years until it reaches the maximum coverage of 228% of the Face Amount

Special bonus given after 8 years, and dividend earnings starting on the 9th year*

Concluding Remarks For the most part, the financial reporting practices of

the GSIS are compliant with Philippine Financial Reporting Standards. GSIS management is to be commended for the detailed and informative disclosures on the fund’s assets, revenues, and expenses.

Non-compliance is found in the reporting of estimated liabilities relating to its issued insurance contracts and members’ retirement benefits.

Concluding Remarks Based on current data, if a member does not exceed

the life expectancy age, the financial return on his contributions is less than the opportunity cost of capital as measured by the risk-free rate.

Issue of the accountability of the GSIS