henri poupart-lafarge president, alstom grid docu… · henri poupart-lafarge president, alstom...

TRANSCRIPT

0 ALSTOM © 2010 Confidential

Henri Poupart-LafargePresident, Alstom Grid

22 September 2010

Grid Overview

1 ALSTOM © 2010 Confidential

2 ALSTOM © 2010 Confidential

Agenda

Alstom Grid Today

Strategic Priorities

Conclusion

Market Overview

3 ALSTOM © 2010 Confidential

A third Sector alongside Power and Transport

A decisive step in Alstom’s development

Sales: Over €23 billion*Workforce: 96,000 employees

• Power • Transport

Sales: €19.7 billion* Workforce: 76,500 employees

POWER TRANSPORT POWER TRANSPORTGRID

*pro forma 2009/10*2009/10

Until May 2010: 2 Sectors Today: 3 Sectors

4 ALSTOM © 2010 Confidential

Alstom acquires Transmission &

power electronicsbusiness

of Areva T&D

The launch of Alstom Grid’s

Transformation Plan « Spark »

Signature of the agreement for the

acquisition of Areva T&D

Alstom Grid: A new name in the industry

November 2009 January 2010 7 June 2010 30 June 2010

Acquisition and integration progressing smoothly

A pioneer and leader since the earliest days of electricity over 100 years ago

Alstom and Schneider Electric offer retained by

Areva’s supervisoryboard

5 ALSTOM © 2010 Confidential

Among the Top 3 in electrical Transmission with a ~ 12% global market shareOver €3.5 billion in annual sales20,000 employeesOver 90 manufacturing and engineering sites worldwide4 main businesses: Products, Systems, Automation, ServiceStrong positions in key markets and fast-growing technologies (Network Management, GIS, HVDC, Disconnectors, Instrument Transformers…)

Alstom Grid

Ready to address the market needs

6 ALSTOM © 2010 Confidential

Alstom Grid offer across 4 Business Units – grid specialists

ProductsA comprehensive range of equipment covering the high toultra-high voltage up to 1,200 kV (AC) and 1,000 kV (DC):

- Power transformers

- Gas-insulated substations and air-insulated switchgear: circuit breakers, disconnectors, instrument transformers…

SystemsTurnkey high voltage substations (onshore and offshore)

Grid interconnection for all types of generation

HVDC (high voltage direct current) substations using LCCand VSC technologies

Specialist in Flexible AC Transmission Systems (FACTS)Special power systems for industry and infrastructureElectrical balance-of-plant (eBOP)

35%

5%

50%

10%

35%5%

50%

10%

Sales 2009

Sales 2009

7 ALSTOM © 2010 Confidential

AutomationMission critical solutions to protect, control & manage power systems and electrical grids

N°1 in Network Management Solutions (e-terra)

A Market leader in Substation Automation Solutions with full range (MiCOM and PACIS)

ServiceMaintenance: Inspection, repair, support, spare parts…

Optimization of equipment usage:Consultancy, expertise, training, refurbishment, extension, upgrade…

Alstom Grid offer across 4 Business Units – grid specialists

35%

5%

50%

10%

35%

5%

50%

10%

Sales 2009

Sales 2009

8 ALSTOM © 2010 Confidential

From products to integrated solutions

P

P

P

P

P

Provided by Alstom Power

Provided by Alstom TransportProvided by Alstom Grid

Provided by Schneider Electric (MV / LV)

New integrated solutions (example)

G

G

T

G

G

PGG

G

G

T Wind farmRail transport

Gas-fired plant

Factory

Steam plant

HVDCSubstation

Solar plant

P

G

S

S

T

Network Management System

Substation

Hydro plant

G

9 ALSTOM © 2010 Confidential

Competition

Alstom Grid, Siemens and ABB are the 3 global leaders of the transmission industry− Technological leadership (Power

electronics, Grid management solutions…)

− Global industrial footprint

Emerging players from Korea, China, India are extending their offer coverage and their geographical reach

ABB

Siemens

AlstomGrid

Local Players

Main Emerging PlayersXian, TBEA, Hyundai,

Hyosung, Crompton and Greaves

Either specialists or generalists

10 ALSTOM © 2010 Confidential

Agenda

Alstom Grid Today

Strategic Priorities

Conclusion

Market Overview

11 ALSTOM © 2010 Confidential

A unprecedented time in history: increasing challenges driving change & new technologies

1

2

3Larger Grid

Smarter Grid

Fast growing energy needs, especially electricity

Energy world consumption 2007-2030: ~+45%Share of electricity in total energy consumption: from 9% in 1973, 16% in 2004 to more than 20% in 2030

Race for a low carbon energy mixObjectives 20/20/20 of the European Union: -20% of CO2 emissions, -20% of energy consumption, 20% of energy coming from renewable energy sources

Strong constraints on primary resourcesEurope dependency on fossil fuels imports: 70% in 2030

Source: IEA 2009 – EU Commission

12 ALSTOM © 2010 Confidential

Return to robust medium and longer term growthafter impact of the economic downturn

Market recovery in 2010 after 2009 crisis boosted by major HVDC projects

Mid term (2009-14) market growth estimated around 3% per year

Continued shift towards turnkey

Source: Alstom

Alstom Grid Market (€ billion) Key Dynamics

20142013

Worldwide market

2008 2012201120102009

45

40

35

0

13 ALSTOM © 2010 Confidential

17%

Europe: driven by the 20/20/20 directiveLarge HVDC projects being deployed and planned:

- DC offshore wind connections (UK, Germany)

- HVDC Interconnections

Recurring business volume increasing due to infrastructure renewal

Grid market: Europe and Russia show greater potentials

Percentage of the total Grid Market 2009Source: Alstom

X%

Russia: a strong recoveryGrid modernization a key objective of the government in

`the short to mid term3%

14 ALSTOM © 2010 Confidential

Grid market: Middle East and Africa, Asia Pacific

Eastern Asia and Pacific: catching up after the slow downDeveloped countries consolidating and improving their grid (Korea, Australia…)Developing countries need investment to sustain their industrial growth

Middle-East and Africa: a consolidating market due toGeneral slow down of grid investment in Middle Eastern countriesSustained investment in specific markets e.g. Saudi ArabiaFuture interconnections between renewable resources in North Africa and Europe

18%

13%

15 ALSTOM © 2010 Confidential

Grid market: Americas, new infrastructure and upgrades

Latin America: Brazil taking the lead in Latin AmericaStrong investment in generation and transmission capacity planned in BrazilLarge infrastructure projects in Argentina and Chile9%

12%

North America: gearing upElectrical infrastructure upgrade plannedMajor interconnection project to access additional

capacity (wind and hydro) in the planning

16 ALSTOM © 2010 Confidential

India: a growth story

Continuous increase in recurring business and additional opportunities due to deployment of new generation capability

9%

Grid market: Asia still the place for the largest investment

China: the biggest individual marketRecurring business to sustain growth in consumptionInvestment in large HVDC and Ultra High Voltage (UHV)interconnections

19%

17 ALSTOM © 2010 Confidential

Transmission 54%

Power Generation

15%

Industries13%

Distribution 18%

Transmission and Distribution markets sustained by large governmental investment programs

Transmission needs driven by wind generation and large hydro investments in emerging countries

After a slow down in industrial investment, recovery expected in the short/mid term

Split of the Grid market by end-usersSource: Alstom

Grid market: end-customers

18 ALSTOM © 2010 Confidential

Grid market: HVDC large growth potential

Rapid short term HVDC market increase (to reach an average of €4billion per year by 2012) driven by:

Need to connect massive amount of power away from the consumption centers (China, India, Brazil)

Integration of offshore wind capacity far from the shore (Germany, UK)

Need for interconnection between national/regional grids to increase the stability of the grid and optimize generation capacity (Europe, Russia, Africa, Latin America)

Two thirds of the overall market growth between 2008 and 2014 will come from HVDC

AndréCanelhas

19 ALSTOM © 2010 Confidential

Smart Grid: a driver of Grid market growth

Global market expected to grow from 16b€ to 50b€

Power Plant and Grid Segments will represent 60%

Grid growth driven by Power Electronics and Automation

Generation Grid Demand & Storage

0

5

10

15

20

25b€Global market estimate

2020

2010

Source: LEK, BCG, Alstom

Jean-Michel Cornille

20 ALSTOM © 2010 Confidential

Agenda

Alstom Grid Today

Strategic Priorities

Conclusion

Market Overview

21 ALSTOM © 2010 Confidential

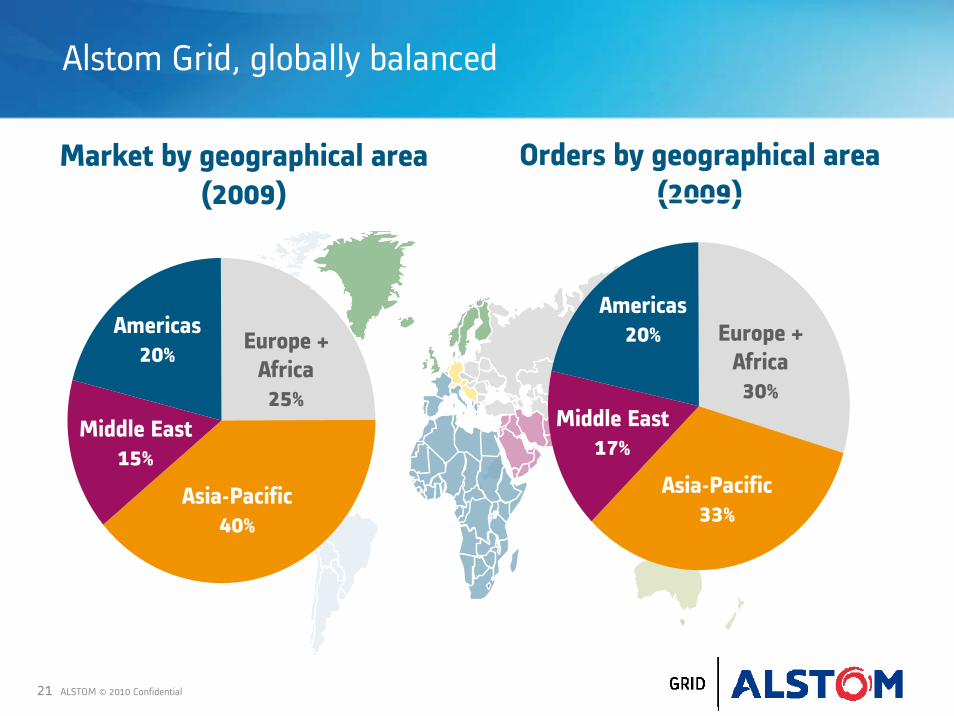

Alstom Grid, globally balanced

Market by geographical area (2009)

Orders by geographical area (2009)

Asia-Pacific 40%

Europe + Africa25%

Middle East15%

Americas20%

Asia-Pacific 33%

Europe + Africa30%

Middle East17%

Americas20%

22 ALSTOM © 2010 Confidential

Global industrial footprint to enable global competitiveness

Over 90 manufacturing and engineering sites worldwide

Main Manufacturing SitesMain Engineering SitesR&D Competence CentresTechnology Centres

Wuhan, ChinaThe world’s first power transformer factory to receive green certification

Aix-les-Bains, FranceGIS & Technical Institute

765 kV TransformerVadodara, India

Redmond, USA. Network Management Systems

23 ALSTOM © 2010 Confidential

Manufacturing Units: 8Employees: approx. 3,500

PALLAVARAM

NAINI

VADODARA

PADAPPAI

India: Overall market leader with full local scope5 Product Lines in leadership positions

NOIDAHOSURNOIDANOIDA

Vadodara - Power Transformers

Hosur - Instrument Transformers

Noida (Suburb of Delhi) -Country Office, Sales, Systems, Automation, Service

Naini - Power Transformers

Pallavaram -Substation Automation,Protection Relays

Padappai - Circuit Breakers, Gas-Insulated Substations,Disconnectors

24 ALSTOM © 2010 Confidential

Deploying expertise and innovation

R&D investment equal to 4% of sales

Main R&D Technology CentresStafford, UKMassy, FranceRedmond, USAVilleurbanne, France (CERDA Laboratory)Shanghai, China (China Technology Centre)

Several R&D Competency Centres in 12 countries worldwide

Shanghai Technology Centre, China

Stafford, UKVilleurbanne, FranceMassy, France

25 ALSTOM © 2010 Confidential

Moving towards Ultra High Voltage (UHV)

33~110kV

220kV AC

400kV AC

500kV DC

765kV AC

800kVHVDC

1200kV AC

19901950 1960 1970 1980 2000 2005 2010 2013

kV

33~110kV

220kV AC

400kV AC

500kV DC

765kV AC

800kVHVDC

1200kV AC

33~110kV

220kV AC

400kV AC

500kV DC

765kV AC

800kVHVDC

1200kV AC

19901950 1960 1970 1980 2000 2005 2010 2013

kV

19901950 1960 1970 1980 2000 2005 2010 2013

kV India’s progression towards UHV

As a market leader, Alstom Grid is well positioned to capitalize on growth in India

Sipat: India’s first 765 kV substation for NTPC Inaugurated on 20 January 2007

26 ALSTOM © 2010 Confidential

Moving towards the digital substation

Digital SubstationControl System “PACiS”: (IEC 61850)

Digital Protection Relay:(IEC 61850)

Online monitoring

27 ALSTOM © 2010 Confidential

Moving towards smarter energy management

Example: Energinet.dk

Denmark - 1980 Denmark - 2010

Central power plantDCHP unitWind turbine

Solutione-terra Renewable Desk integrated in Energinetcontrol center

Customer challengeManage large portfolio of intermittent and distributed generation units

YA-8

28 ALSTOM © 2010 Confidential

Moving towards power electronics – from 100 to 800 kV

kV

0100200300400500600700800900

1000

1950s 1960s 1970s 1980s 1990s 2010

29 ALSTOM © 2010 Confidential

Operational priorities

Excel in the basics 2

Take a step in cost competitiveness 1

Further develop smart grid value proposition 4

Capture key growth opportunities 5Work together 6

Develop customer-valued differentiated offering 3

Streamline direct costs of our products/projectsStreamline structure costs

Establish a leadership position on smart grid

Customer satisfactionOn-time deliveryQuality

Monetize value of current offeringPrepare future differentiation of our offering

Establish strong positioning on HVDCSecure path for growth in key geographiesOptimize sales model

Enforce cooperation at all levelsDefine the grid way

« GAIN »The Alstom costs optimisation plan

APS « Alstom Production System »Deploying lean manufacturingworldwide

30 ALSTOM © 2010 Confidential

Agenda

Market Overview

Strategic Priorities

Conclusion

Alstom Grid Today

31 ALSTOM © 2010 Confidential

A turning point in our industry : the Grid is back

- increasing need for high level electro-technical expertise

Alstom Grid ideally placed to benefit from this evolution

- well positioned worldwide – commercially and industrially

- at the leading edge for key technologies

- benefiting from synergies with Alstom Power and Alstom Transport

Operational plan in place to improve Alstom Grid performance and create value

Conclusion

32 ALSTOM © 2010 Confidential

www.grid.alstom.com