high value adding services e-commerce

TRANSCRIPT

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

High Value-Adding Services; E-Commerce

Global Transfer Pricing Course (Adv. Topics), Oct.10,2016

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

2

CONTENTS

• Contemporary trends in services

• Low value services

• Types of high value services

• Location savings

• E-Commerce

• Case studies

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

3

Contemporary trends in Services

Low value and high value services – With increasing flow of services within MNEs, the debate of value attributable to services between entities is gaining focus

Location of performance of services – Services performed out of developing economies and low cost locations give rise to Locational advantages

Taxable presence - Permanent establishment (“PE”) issues

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

4

Contemporary trends in Services

Core and non-core services - While developed nations are taking a view that non-core services should be attributed a lower return and have introduced safe harbours for such services, various developing nations like India on the other hand expect a higher return for support services on the premise that they create significant value for the group (through location savings, talent pool etc.)

Concept of hard to value intangibles – Services that have an element of intangible embedded in it and for which reliable comparables’ data is not available in public domain

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

5

Contemporary trends in Services

Increasing focus on substance – Substance of an intercompany arrangement is being scrutinised during audits thereby going beyond the legal flow in order to arrest any erosion of tax base

Growth of Digital economy – Growth in transactions through e-commerce poses new challenges in understanding the elements in the virtual supply chain and thereby the taxing rights of countries involved

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

6

Country measures

Countries are increasingly adopting the following to provide guidance to taxpayers on profitability expected from services

Safe harbours (e.g. US, Singapore, India) Circulars providing guidance on services (e.g. India) Advance Pricing Agreements

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

7

Country measures

OECD efforts to develop action plans to tackle Base Erosion and Profit Shifting

Identify and address arrangements which involve use of intangibles, risks, capital and other high risk transactions that result in artificially shifting profits from one jurisdiction to another

Counter treaty abuse resulting in double non-taxation

Address various tax issues relating to digital economy, intangibles, strengthening CFC rules and tackle aggressive tax planning schemes

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

8

Service models in an MNE set up (illustrative)

Administrative support services Routine technology development services

Joint development arrangements

Returns

Contract R&D services

Full fledged R&D

KPO services

Functions Risks

Assets

Procurement services

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

9

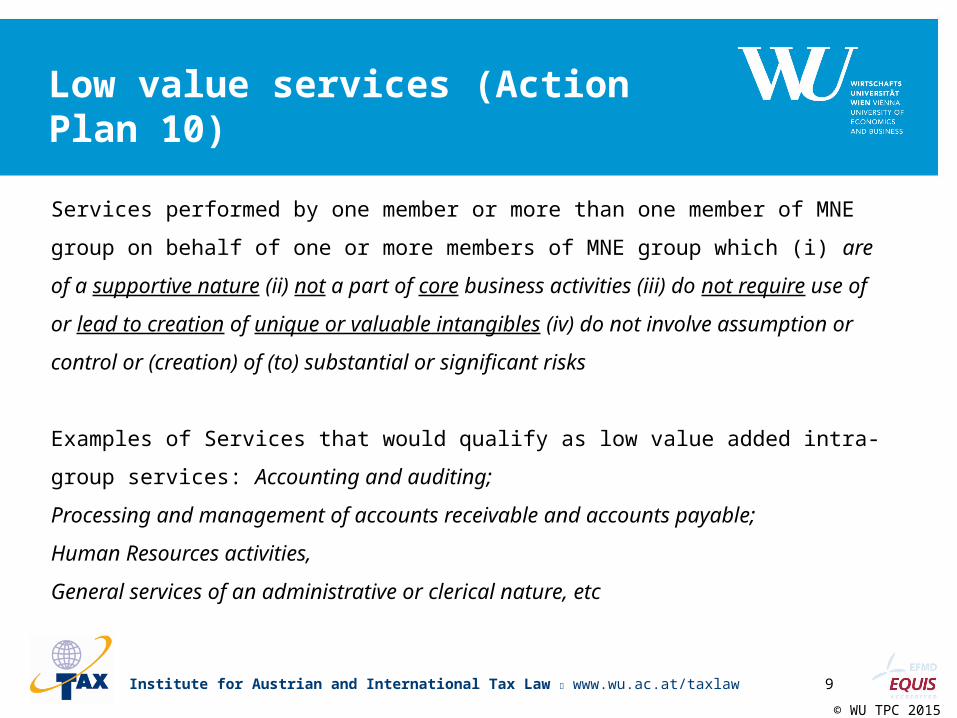

Low value services (Action Plan 10)

Services performed by one member or more than one member of MNE group on behalf

of one or more members of MNE group which (i) are of a supportive nature (ii) not a part

of core business activities (iii) do not require use of or lead to creation of unique or

valuable intangibles (iv) do not involve assumption or control or (creation) of (to)

substantial or significant risks

Examples of Services that would qualify as low value added intra-group services:

Accounting and auditing;

Processing and management of accounts receivable and accounts payable;

Human Resources activities,

General services of an administrative or clerical nature, etc

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

10

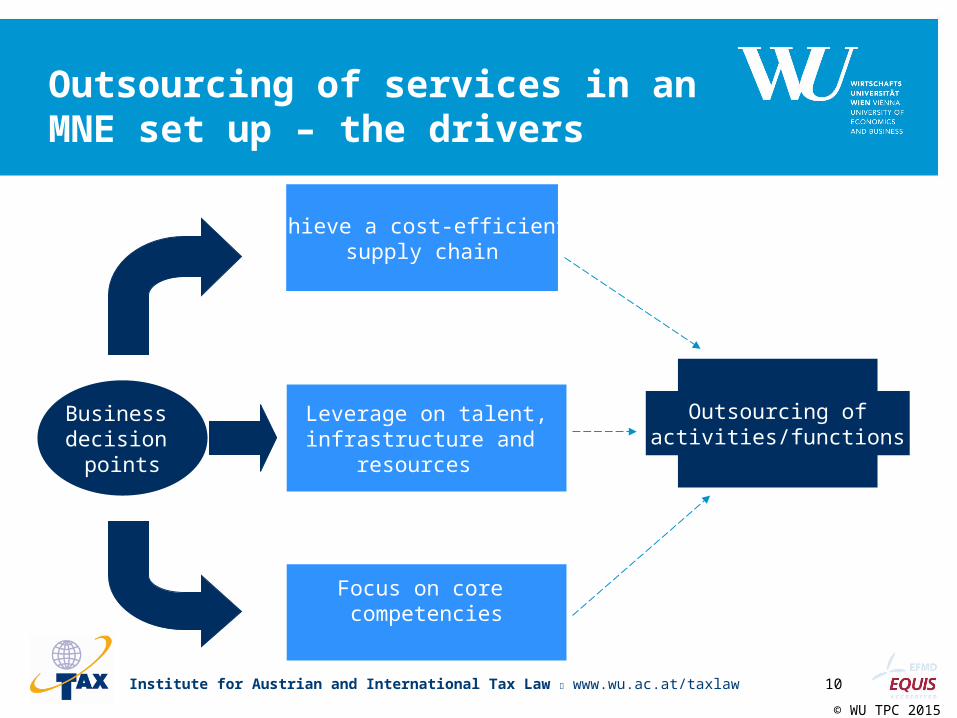

Outsourcing of services in an MNE set up – the drivers

Business decision

points

Outsourcing of activities/functions

Achieve a cost-efficient supply chain

Focus on core competencies

Leverage on talent,infrastructure and

resources

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

11

Fiscal effects of outsourcing

Location savings: Identification and allocation

Withholding tax: Application in the State of the service provider on the fees paid by the service recipient on:

– Service fees– Royalties

Benefit of double tax treaty: Advantage to claim the benefit of a double tax treaty between the State of the service recipient and the State of the service provider– Avoid the withholding tax– Reduce the withholding tax rate– Avoid potential double taxation

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

12

Location savings – defined

Net cost savings from relocation to a low cost jurisdiction

All factors and associated costs to be considered (e.g. termination costs for the existing operation, possibly higher infrastructure costs in the new location, possibly higher transportation costs if the new operation is more distant from the market, training costs of local employees etc)

Economically significant functions resulting in creation of location savings

Location specific advantage

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

13

Location specific advantages (“LSAs”) Location savings (i.e. cost savings) coupled with the following additional

geographical/business advantages can lead to creation of LSAs:

Highly specialised skilled manpower and knowledge;

Closeness to market;

Large customer base

Developed infrastructure

Market premium

Incremental profits derived from LSAs lead to “location rent”

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

14

The location savings (“LS”) issue – identification and allocation

Whether locationsavings exist?

Determine quantum of LS?

Whether LS retained by MNE or passed on to

customers

How would independent parties allocate LS under arm’s length conditions

• Market and industry factors to be considered for establishing existence of LS

• In contract manufacturing and services arrangements, an adjustment for LS may not be warranted where reliable local market comparables are available for determination of arm’s length returns for these arrangements

• Allocation of LS, if any, according to relative bargaining strength of the respective entities – depends on their access to LSAs

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

15

Location savings - illustrated

Entity A (high cost jurisdiction)

Cost of manufacture US$100

End customerSelling price = US$ 150

Scenario BEFORE outsourcing

Entity B – Contract manufacturer

Cost of manufacture US$60

End customer

Selling price = US$ 150

Scenario AFTER outsourcing

Entity A – Outsourcer

High cost jurisdiction

Selling price = US$ 80

Location savings for the Group: US$ (150 – 60 = 90)Location savings for Entity A: US$ (150 – 80 = 70)

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

16

Location savings – the jurisprudenceOECD

The OECD first acknowledged and addressed the issue of location savings in the new Ch IX on TP issues associated with business restructurings

Acknowledges the presence of LSAs in MNE operations whose quantification and allocation should be in accordance with arm’s length principle

Sharing of LSAs between group companies is best done through comparability analysis if the savings are not passed on to third party customers

UN

Views consistent with the OECD.

Concludes that allocation of benefits will depend on competitive factors relating to access to LSAs, alternatives available to the parties and their relative bargaining power

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

17

Guidance as per OECD – BEPs Action plan 8-10 Final Report

Do location savings and / or other local

market features affect the prices or margins or provide

other market advantages or

disadvantages, vs the foreign

comparables ?

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

18

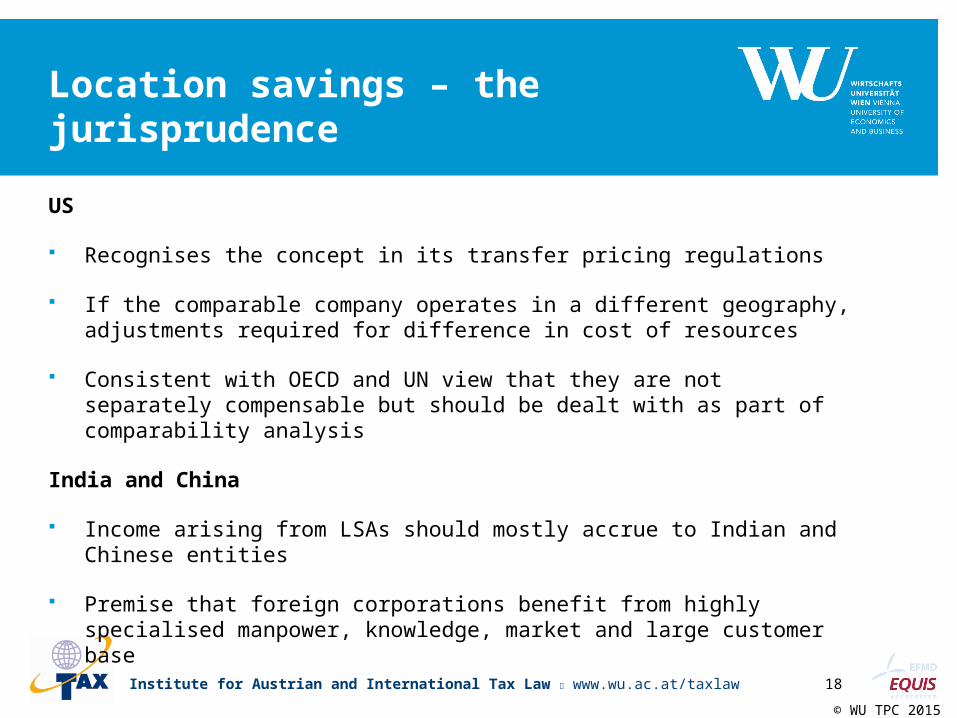

Location savings – the jurisprudenceUS

Recognises the concept in its transfer pricing regulations

If the comparable company operates in a different geography, adjustments required for difference in cost of resources

Consistent with OECD and UN view that they are not separately compensable but should be dealt with as part of comparability analysis

India and China

Income arising from LSAs should mostly accrue to Indian and Chinese entities

Premise that foreign corporations benefit from highly specialised manpower, knowledge, market and large customer base

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

19

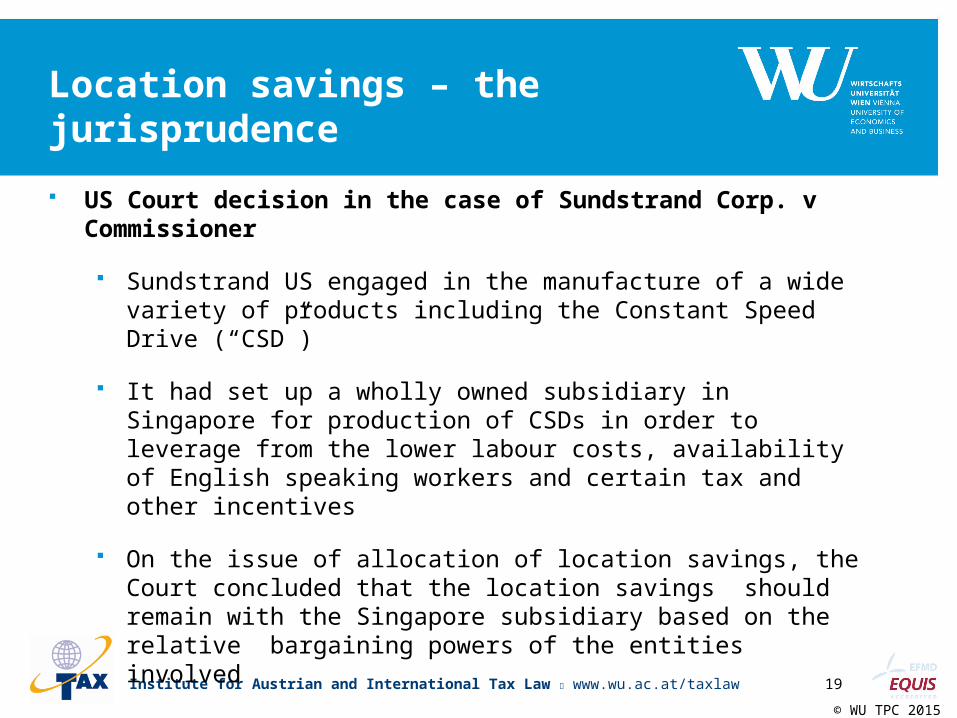

Location savings – the jurisprudence US Court decision in the case of Sundstrand Corp. v Commissioner

Sundstrand US engaged in the manufacture of a wide variety of products including the Constant Speed Drive (“CSD”)

It had set up a wholly owned subsidiary in Singapore for production of CSDs in order to leverage from the lower labour costs, availability of English speaking workers and certain tax and other incentives

On the issue of allocation of location savings, the Court concluded that the location savings should remain with the Singapore subsidiary based on the relative bargaining powers of the entities involved

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

20

Location savings – the jurisprudence

In the United Nations Transfer Pricing Manual for Developing Countries (India Chapter), the Indian authorities have advocated that, in the quantification and allocation of location savings amongst the parties, the profit split method (PSM) can be used wherein the functional analysis and bargaining power of the parties to the transaction would be relevant factors for consideration – benchmarking against local comparables does not take into account the benefit of location savings.

The OECD, UN and US transfer pricing regulations on the other hand are of the view that location savings cannot be said to exist where there are comparables

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

21

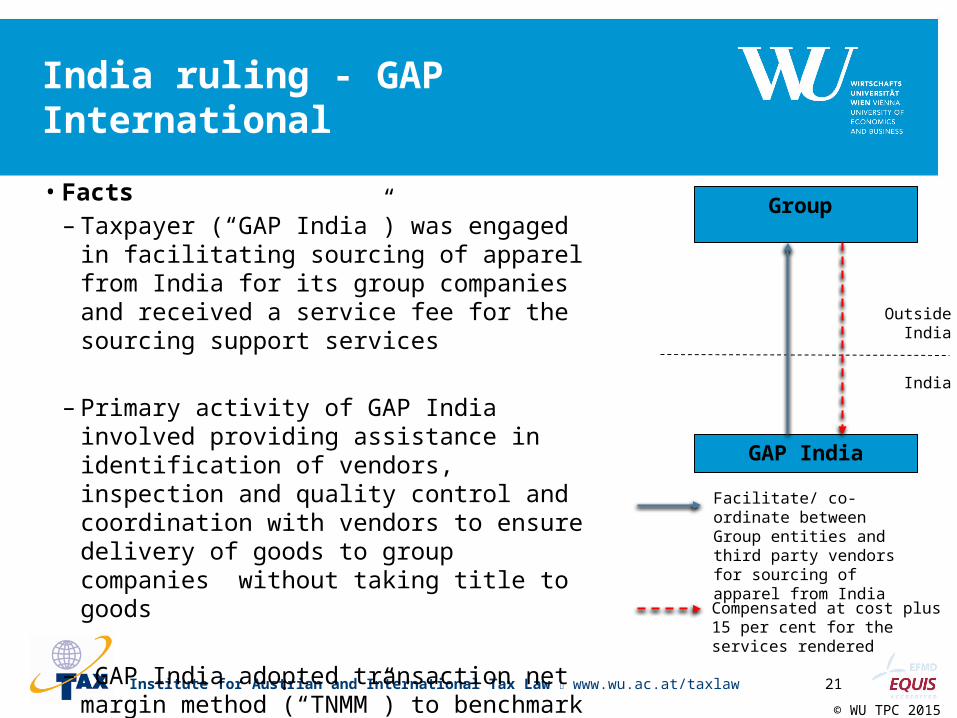

India ruling - GAP International • Facts

– Taxpayer (“GAP India”) was engaged in facilitating sourcing of apparel from India for its group companies and received a service fee for the sourcing support services

– Primary activity of GAP India involved providing assistance in identification of vendors, inspection and quality control and coordination with vendors to ensure delivery of goods to group companies without taking title to goods

– GAP India adopted transaction net margin method (“TNMM”) to benchmark the service fee determined at full cost plus 15 per cent from its group company

Group

GAP India

Outside India

India

Facilitate/ co-ordinate between Group entities and third party vendors for sourcing of apparel from IndiaCompensated at cost plus 15 per cent for the services rendered

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

22

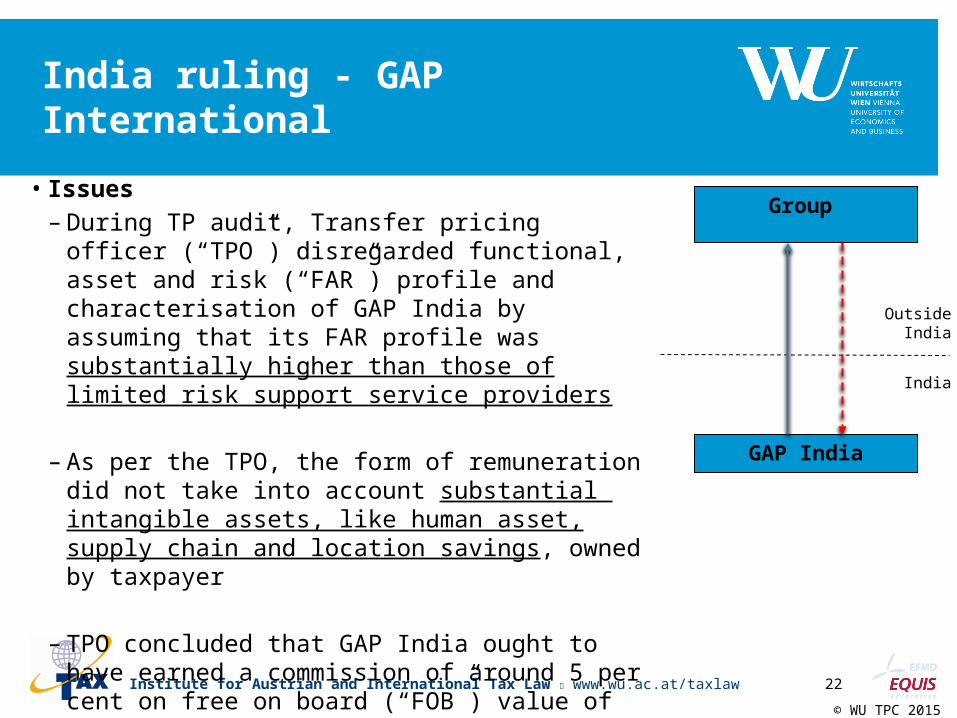

India ruling - GAP International

• Issues– During TP audit, Transfer pricing officer (“TPO”) disregarded

functional, asset and risk (“FAR”) profile and characterisation of GAP India by assuming that its FAR profile was substantially higher than those of limited risk support service providers

– As per the TPO, the form of remuneration did not take into account substantial intangible assets, like human asset, supply chain and location savings, owned by taxpayer

– TPO concluded that GAP India ought to have earned a commission of around 5 per cent on free on board (“FOB”) value of goods procured by group companies, thereby making a TP adjustment.

Group

GAP India

Outside India

India

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

23

India ruling - GAP International

• Contentions of the Revenue– GAP India performed all critical functions, assumed

significant risks and used unique intangibles developed by it over a period of time.

– Functions like quality management, involve great care to be taken at sourcing stage and any defect may result in huge adverse impact on whole supply chain.

– GAP India had proprietary information of supply chain, such as knowledge of vendors, products and designs, acquisition and supply, quality control, storage and logistic involved

Group

GAP India

Outside India

India

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

24

India ruling - GAP International

• Contentions of the Revenue (contd)– Independent enterprises, for similar services, would use a

charging basis as a percentage of value of goods procured rather than cost plus.

Group

GAP India

Outside India

India

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

25

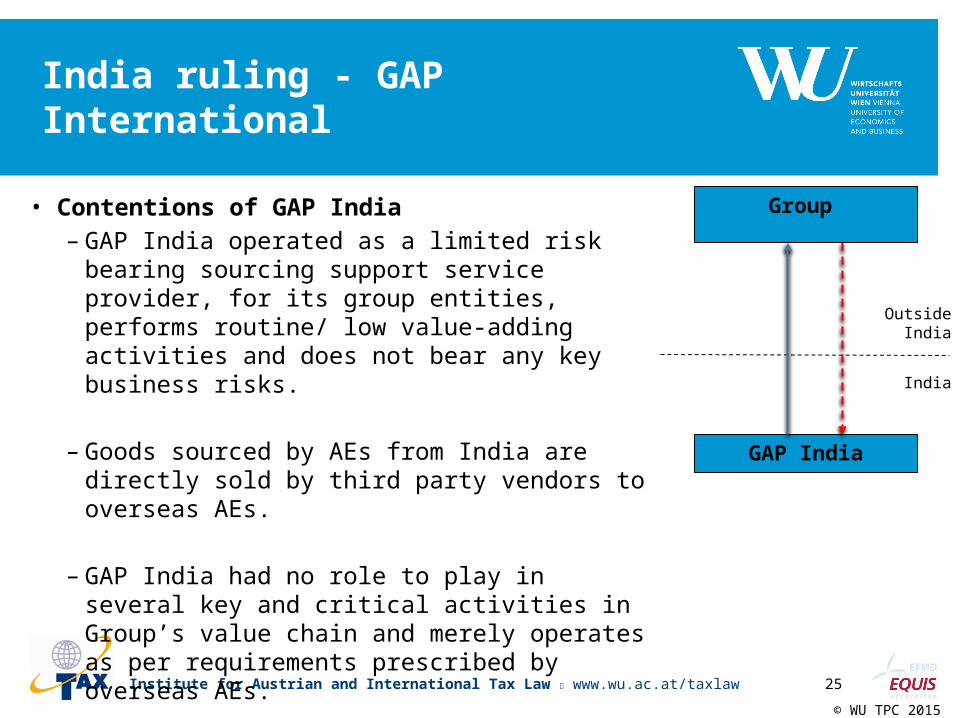

India ruling - GAP International

• Contentions of GAP India– GAP India operated as a limited risk bearing sourcing

support service provider, for its group entities, performs routine/ low value-adding activities and does not bear any key business risks.

– Goods sourced by AEs from India are directly sold by third party vendors to overseas AEs.

– GAP India had no role to play in several key and critical activities in Group’s value chain and merely operates as per requirements prescribed by overseas AEs.

Group

GAP India

Outside India

India

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

26

India ruling - GAP International

• Contentions of GAP India (contd)– Location savings generated by Group entities are

passed on to end customers in the form of lower prices

– Due to lack of comparable sourcing support service providers in databases, taxpayer had to identify distributor companies and make suitable working capital adjustment

– TPO selected same comparables and merely

changed the PLI, without appreciating that the intensity of functions of such comparables were more than that of taxpayer

Group

GAP India

Outside India

India

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

27

India ruling - GAP International

• Tribunal ruling– Determination of ALP to be based on

characterisation of GAP India and its Group entity

– Location savings arise to the industry as a whole and not taxpayer alone. The objective of sourcing from low cost countries is to survive in stiff competition by providing a lower cost to its end-customers

– Procurement support service providers work on various models and remuneration model followed would depend on the facts.

Group

GAP India

Outside India

India

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

28

India ruling - GAP International

• Tribunal ruling– GAP India did not assume any significant business

risks, no human resource or supply chain intangibles were developed

– On the basis of the above, the PLI as a percentage of FOB value of goods procured by AE (as applied by the TPO for computing the TP adjustment) resulted in absurd and distorted results.

– Based on the characterisation of GAP India and the facts of the case, the cost plus form of compensation adopted by GAP India was upheld

Group

GAP India

Outside India

India

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

29

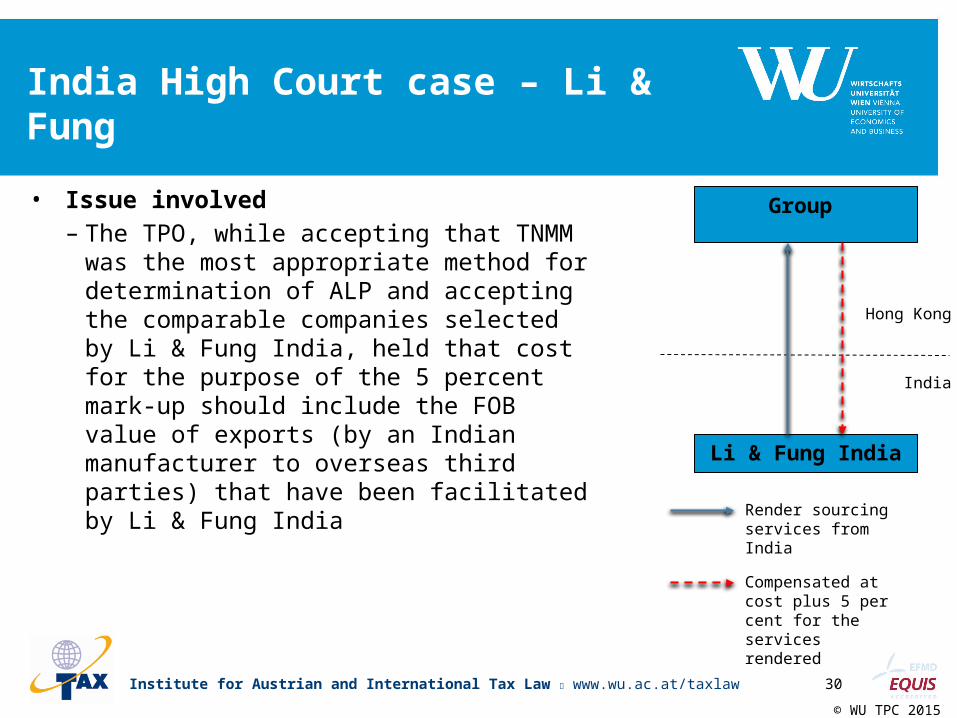

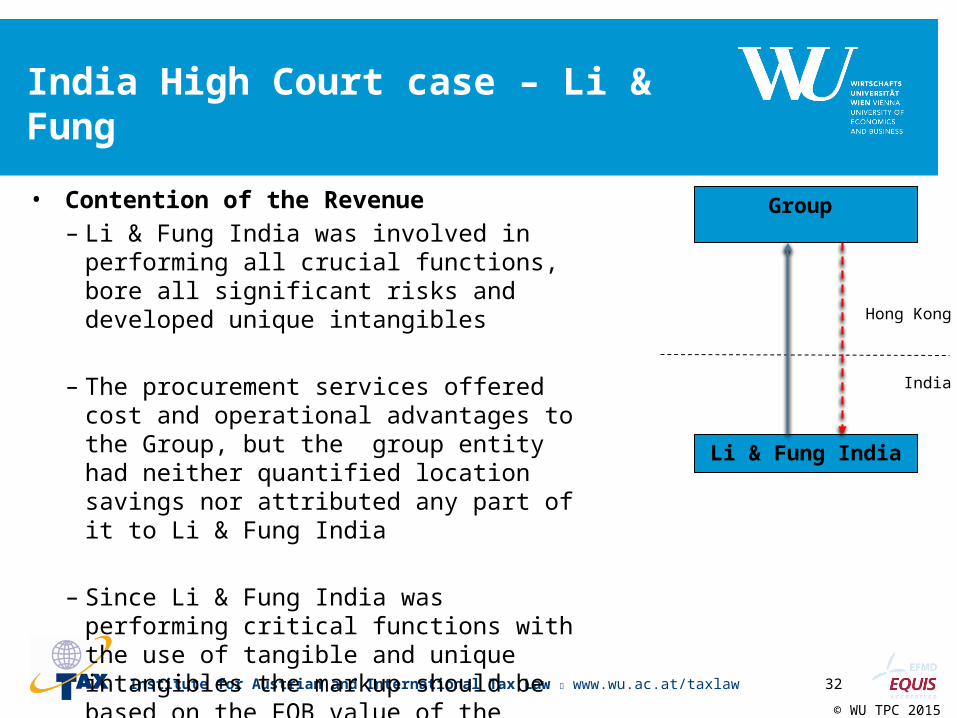

India High Court case – Li & Fung • Facts

– Li & Fung India was engaged in rendering sourcing support services to its Hong Kong based Group entity, for which it received a remuneration of cost plus 5 percent

– Li & Fung India applied TNMM to determine the ALP of such remuneration, considering Operating Profit/Total Cost (OP/TC) as the PLI.

Group

Li & Fung India

Hong Kong

India

Render sourcing services from India

Compensated at cost plus 5 per cent for the services rendered

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

30

• Issue involved– The TPO, while accepting that TNMM was the most

appropriate method for determination of ALP and accepting the comparable companies selected by Li & Fung India, held that cost for the purpose of the 5 percent mark-up should include the FOB value of exports (by an Indian manufacturer to overseas third parties) that have been facilitated by Li & Fung India

Group

Li & Fung India

Hong Kong

India

Render sourcing services from India

Compensated at cost plus 5 per cent for the services rendered

India High Court case – Li & Fung

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

31

• Question before the High Court– Whether assessment of Revenue authorities of ALP

applying the TNMM method was contrary to the provisions in the Indian TP law?

– Whether the TPO’s apportionment by considering the cost plus mark up of 5 percent on FOB value of goods transacted between third party enterprises, sourced through the taxpayer, is in compliance with the law?

Group

Li & Fung India

Hong Kong

India

India High Court case – Li & Fung

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

32

• Contention of the Revenue– Li & Fung India was involved in performing all crucial

functions, bore all significant risks and developed unique intangibles

– The procurement services offered cost and operational advantages to the Group, but the group entity had neither quantified location savings nor attributed any part of it to Li & Fung India

– Since Li & Fung India was performing critical functions with the use of tangible and unique intangibles the markup should be based on the FOB value of the exports

Group

Li & Fung India

Hong Kong

India

India High Court case – Li & Fung

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

33

• Contention of Li & Fung India– Rendered buying or sourcing support services and

operated with limited risk.

– Did not develop any unique intangibles or undertake supply chain management

– Location savings is attributed to the end purchaser only. The transaction of export of finished goods is being undertaken by third party vendors neither taxpayer nor the Group entity were parties to such contracts and none of them have gained any advantage on account of location saving

– TPO’s application of TNMM is contrary to provision of law

Group

Li & Fung India

Hong Kong

India

India High Court case – Li & Fung

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

34

• High Court verdict– Li & Fung India operated as a low risk contract

service provider exclusively rendering sourcing support to its group entities. It did not bear any significant operational risks for its functions.

– TPO’s determination of the arm’s length price for sourcing support services based on markup on FOB value contrary to the provisions of the law.

– of law

Group

Li & Fung India

Hong Kong

India

India High Court case – Li & Fung

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

35

India Tribunal – Watson Pharma• Facts

– Watson Pharma India engaged in provision of contract manufacturing and contract R&D services for its parent company – Watson Labs, US

– Watson Pharma India reported an operating mark up on cost of 17.43% and 15.66% for contract R&D services and contract manufacturing services respectively

– The TPO determined the arm’s length mark up at a higher rate and proposed a TP adjustment for the contract R&D services segment

Watson Labs

Watson Pharma

US

India

Render contract R&D services and contract manufacturing

Compensated with service fee

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

36

India Tribunal – Watson Pharma• Facts

– In respect of the contract manufacturing and contract R&D segment, the TPO also made an adjustment for location savings

– Adjustment for LS computed on the basis that the transfer of manufacturing process from US and Europe to India resulted in cost savings

– The Revenue relied upon international research publications stating cost differentials for similar activities between countries to support the LS adjustment

Watson Labs

Watson Pharma

US

India

Render contract manufacturing and contract R&D services

Compensated with service fee

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

37

India Tribunal – Watson Pharma• Ruling by Tribunal

– The companies – both the Indian company and the US Co operated in a perfectly competitive market

– If at all there were location savings, they were passed on to customers

– Any attribution to the Indian company of a share of the location savings (rent) should be on the basis of relative bargaining power and characterisation

– Where local comparables are available for similar services, no adjustment for LS required

Watson Labs

Watson Pharma

US

India

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

38

High value services

Customer delivery and relationships

Local market insights

Administration

Commercial risk

Business analysis and solutions

Commercial judgement/experience

IP (Brand etc)

Routine return(Cost plus return)

High value return

Shared return

Potentially involvingHigh value services

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

39

Allocation of profits

Tested party

Return attributable to functions, assets and risks

Service Provider

Cost+

Principal

Residual

Profi

t

Control of capital Economically significant functions

Contractual risks

Management of Assets and Risks

Key determinants for arm’s length reward• Key people functions – economically significant functions• Supervision and control• Capital funding• Investment of economically significant assets

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

40

High value services?

Procurement services

Research and development services

KPO/LPO services

Engineering design services

Brand/market promotion

Financial services

Technical services

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

41

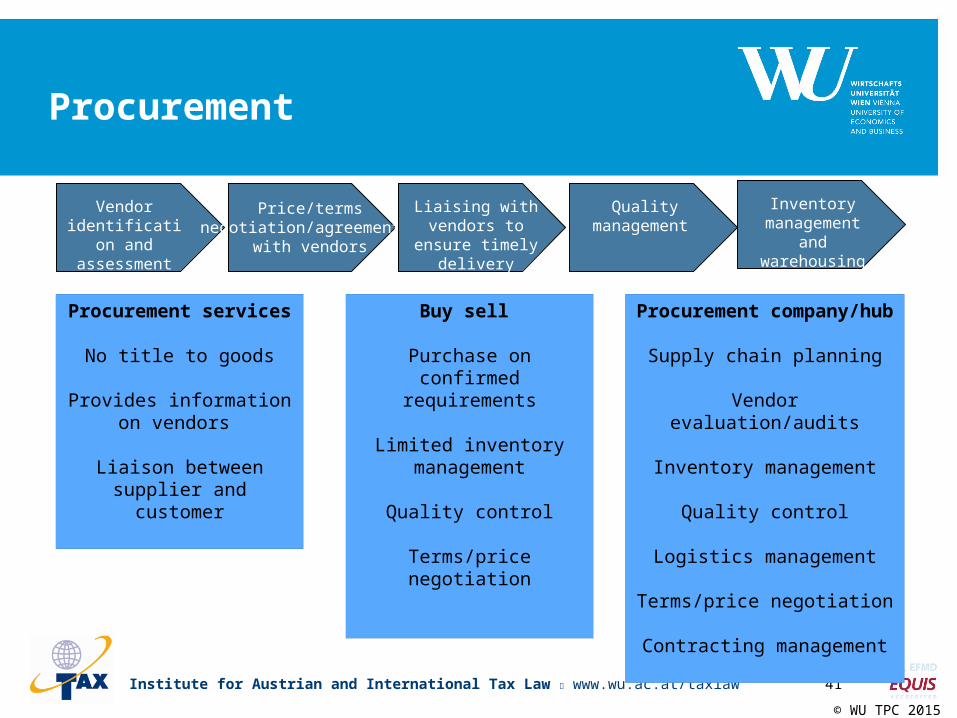

Procurement

Vendor identification

and assessment

Price/termsnegotiation/agreement

with vendors

Liaising with vendors to ensure

timely delivery

Quality management

Procurement company/hub

Supply chain planning

Vendor evaluation/audits

Inventory management

Quality control

Logistics management

Terms/price negotiation

Contracting management

Buy sell

Purchase on confirmed requirements

Limited inventory management

Quality control

Terms/price negotiation

Procurement services

No title to goods

Provides information on vendors

Liaison between supplier and customer

Inventory management and

warehousing

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

42

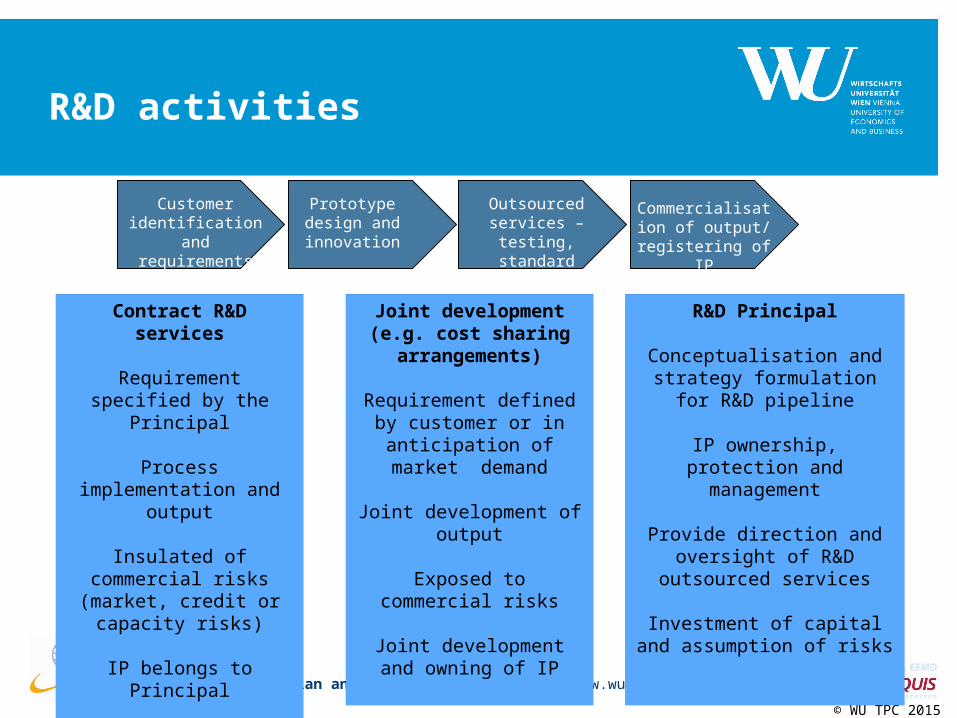

R&D activities

Customer identification and

requirementsanalysis

Prototype design and innovation

Outsourced services – testing,

standard processes

Commercialisation of output/

registering of IP

R&D Principal

Conceptualisation and strategy formulation for R&D pipeline

IP ownership, protection and management

Provide direction and oversight of R&D outsourced services

Investment of capital and assumption of risks

Joint development (e.g. cost sharing

arrangements)

Requirement defined by customer or in anticipation

of market demand

Joint development of output

Exposed to commercial risks

Joint development and owning of IP

Contract R&D services

Requirement specified by the Principal

Process implementation and output

Insulated of commercial risks (market, credit or

capacity risks)

IP belongs to Principal

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

43

Issues on R&D services

Relative role of entities involved in the services i.e. conduct of parties

Legal v Economic ownership

Value creation and location savings

Comparables

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

44

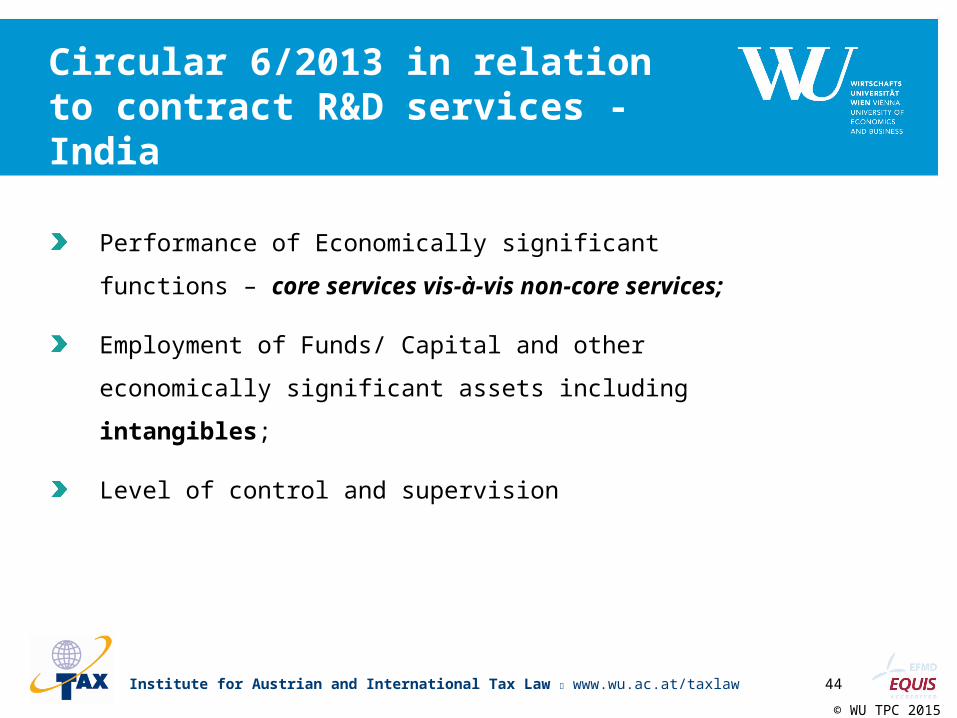

Circular 6/2013 in relation to contract R&D services - India

Performance of Economically significant functions – core services vis-

à-vis non-core services;

Employment of Funds/ Capital and other economically significant

assets including intangibles;

Level of control and supervision

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

45

Circular 6/2013 in relation to contract R&D services - India

Strategic decision making capability and overseeing /monitoring

activities performed;

Assumption of Risks;

Ownership rights (legal or economic) of outcome of

research/development/spend

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

46

Circular 6/2013 in relation to contract R&D services - India

Economically significant functions would include the following:

Conceptualization and design of a product/solution;

Providing strategic direction and framework in relation to an R&D

activity

Key people functions

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

47

Circular 6/2013 in relation to contract R&D services - India

The following functions may also be considered to be illustrative of

economically significant functions:

Research into new products/applications either collaborative with

the Principal or independently;

Significant people functions in relation to planning and execution of

design/development of a solution independent of any direction or

supervision of a foreign principal.

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

48

Circular 6/2013 in relation to contract R&D services - India

Usage of Funds/ Capital and other economically significant assets including intangibles – responses to the following questions would help:

Whether the operations involve significant R&D and innovation?

Whether there are investments leading to creation or development of any intangibles;

What is basis of compensation to the entity performing the services – compensation should reflect contribution

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

49

Marketing/brand promotion

Market research and pre-sales

activities

Conceptualization of advertising and market promotion

campaigns

Implementation of market

promotion plans

Brand management and registering of IP

Principal/Brand owner

Formulating strategy for brand management

Provide direction and oversight for brand promotion activities

Managing and assuming brand budget

Investment of capital and assumption of risks

IP protection and management

Exposed to commercial risks

Distributor/licensed manufacturer

Participation in developing and implementing market

promotion plans

Customization of brand/products for local

markets through advertising and packaging

Spend in brand promotion activities

Exposed to commercial risks

Contract market support services

Contracted to the Principal

Market research support and sharing local market insights on a need-basis

Insulated of commercial risks (market, credit or

capacity risks)

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

50

Issues on marketing/brand promotion

Assessment of excessive advertising, marketing promotional expenses relative

to comparables – bright line test;

Distributors and licensed manufacturers – key considerations

Whether sufficient to be compensated in an aggregated manner (i.e. as a

reduction in import price of products) or separate compensation required for

AMP services?

Will any compensation be due upon termination of intercompany agreement?

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

51

Technical services

• Model conventions do not contain a specific Article for fees for technical services (“FTS”).

• Taxability of FTS has to be considered either under Article 7 or Article 14 or Article 21, depending on facts.

• For example, most Indian tax treaties have specific provision for taxing FTS with common operating provisions as for “royalties”.

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

52

Technical services

Consideration (including lump sum) for rendering

Managerial Technical Consultancy

Provision of services

of other personnel

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

53

Technical services

Contemplates high value service to the service recipient due to knowledge and

human involvement

The service must be one which requires skills/acts which is to be performed

when the service is being performed

Distinguished from administrative, commercial support services

Technical services vis-à-vis technology driven services

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

54

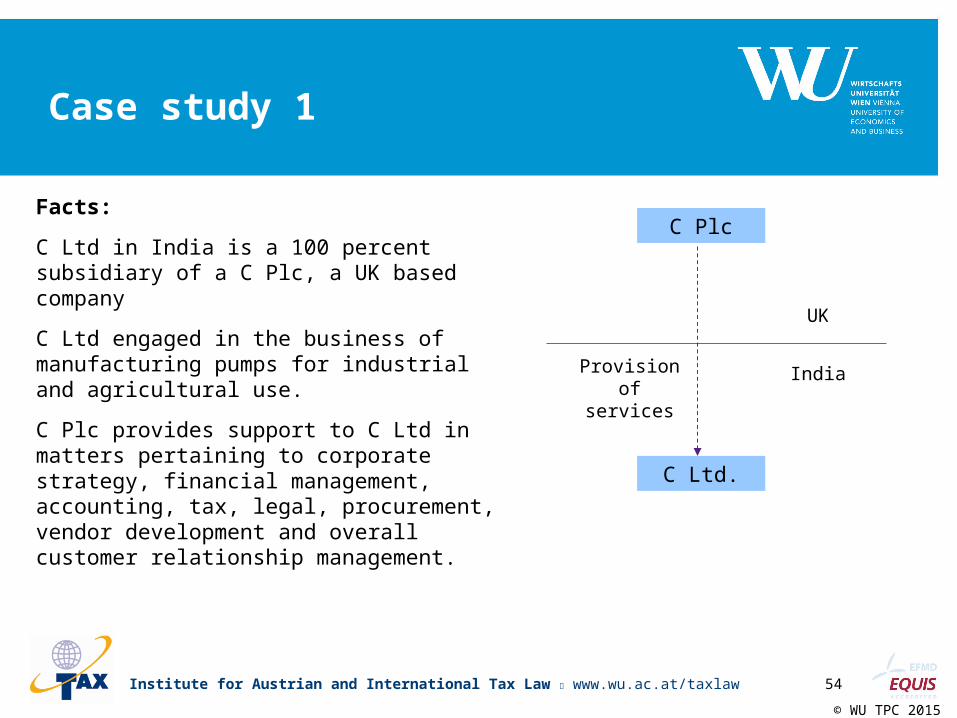

Case study 1

Facts:

C Ltd in India is a 100 percent subsidiary of a C Plc, a UK based company

C Ltd engaged in the business of manufacturing pumps for industrial and agricultural use.

C Plc provides support to C Ltd in matters pertaining to corporate strategy, financial management, accounting, tax, legal, procurement, vendor development and overall customer relationship management.

C Plc

C Ltd.

UK

IndiaProvision of services

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

55

Case study 1

Facts (contd. )

C Plc has been charging a sum of GBP 10 million per annum to C Ltd by way of management service fees.

C Plc and C Ltd have an intercompany agreement for provision of services. One of the clauses in the agreement indicates that the services would be provided on “request”.

In the course of the TP audit, the Revenue asks C Ltd to produce documentary evidence in support of the “high” or “low” value of the services.

C Plc

C Ltd.

UK

IndiaProvision of services

How would you go about with setting out the information request for the Company management for the evaluation process?

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

56

E-Commerce

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

57

Hard to value intangibles

Public discussion draft issued by the OECD on BEPS Action Plan 8 defines HTVI as

intangibles or right in intangibles involved in a transaction of transfer between

associated enterprises;

Where no comparable transactions exist in public domain;

Lack of reliable financial projections to estimate future probable cash flows;

Assumptions used in valuation of intangibles are highly uncertain

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

58

Hard to value intangibles

HTVI in the context of services may be seen in the following arrangements within

an MNE Group:

Joint development of a breakthrough IP by entities within an MNE involved in

R&D services;

Partially developed IP (say technology) at the time of a transfer between

entities within an MNE

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

59

CONTENTS

• What is e-commerce?

• Tax and transfer pricing considerations

• Work done internationally

• Case studies

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

60

What is E-Commerce?

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

61

E-commerce - defined

Referred to as use of electronic means to buy / sell goods or services - settlement may or may not happen electronically

Australian Taxation Office has defined e-commerce narrowly as ‘the buying and selling of goods and services on the internet’

Scope of e-commerce is constantly enlarging as more and more sectors adopt ICT – Retail, Financial Services, Education, Healthcare…

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

62

Scoping e-commerce…

•Commercial transactions involving both organisations and individuals that are based upon the processing and transmission of digitized data, including text, sound and visual images and that are carried out over open networks (like the Internet) or closed networks (like AOL or Minitel) that have a gateway onto an open marketOECD•Commercial transactions in which the order is placed electronically and goods are delivered in tangible or intangible form and there is ongoing commercial relationshipIFA•All business activity conducted using a combination electronic communication and information processing technology

The Asia Pacific Economic Cooperation

•The process of using electronic methods and procedures to conduct all forms of business activity

The United Nations Economic and Social Commission for

Asia and the Pacific

•Transactions where both the offer for sale and acceptance of offer are made electronicallyNASSCOM

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

63

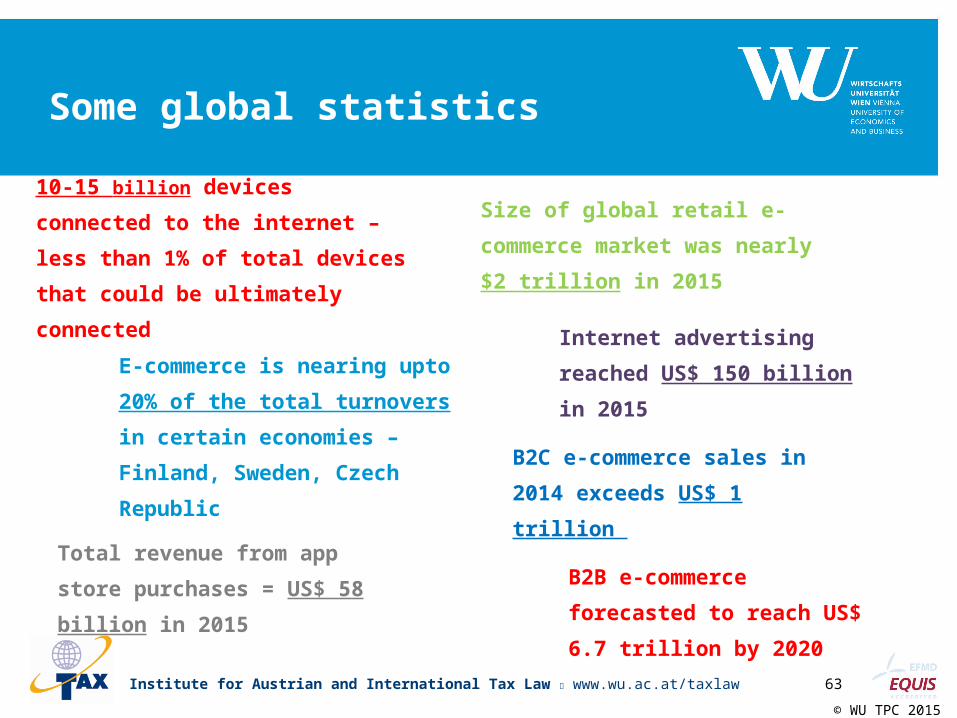

Some global statistics

10-15 billion devices connected to the internet – less than 1% of total devices that could be ultimately connected

E-commerce is nearing upto 20% of the total turnovers in certain economies – Finland, Sweden, Czech Republic

B2C e-commerce sales in 2014 exceeds US$ 1 trillion

B2B e-commerce forecasted to reach US$ 6.7 trillion by 2020

Size of global retail e-commerce market was nearly $2 trillion in 2015

Internet advertising reached US$ 150 billion in 2015

Total revenue from app store purchases = US$ 58 billion in 2015

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

64

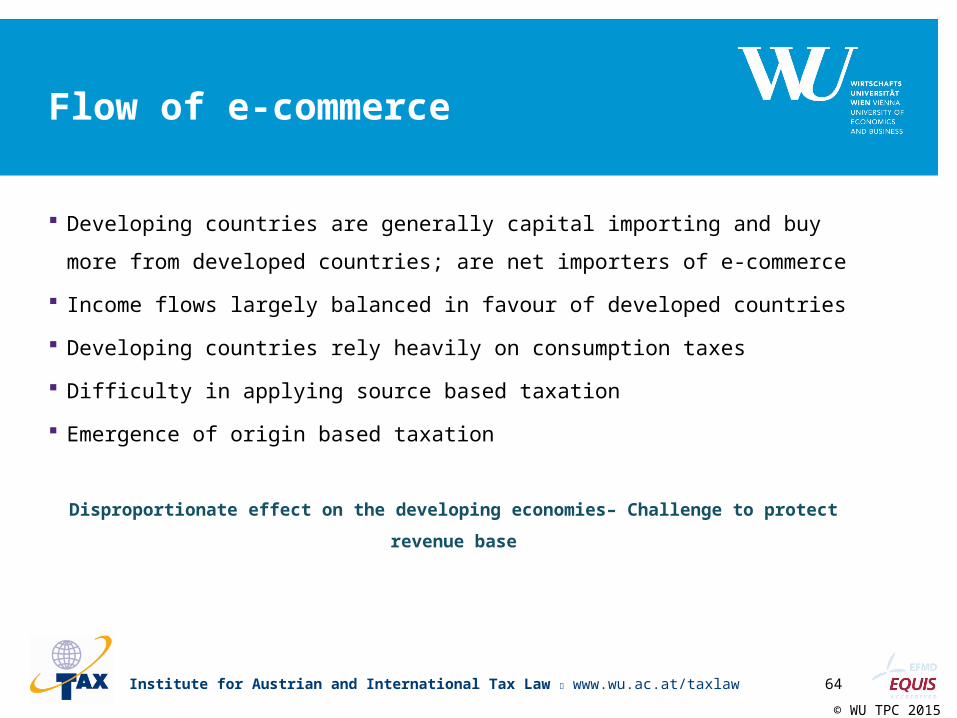

Flow of e-commerce

Developing countries are generally capital importing and buy more from developed countries; are net importers of e-commerce

Income flows largely balanced in favour of developed countries Developing countries rely heavily on consumption taxes Difficulty in applying source based taxation Emergence of origin based taxation

Disproportionate effect on the developing economies– Challenge to protect revenue base

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

65

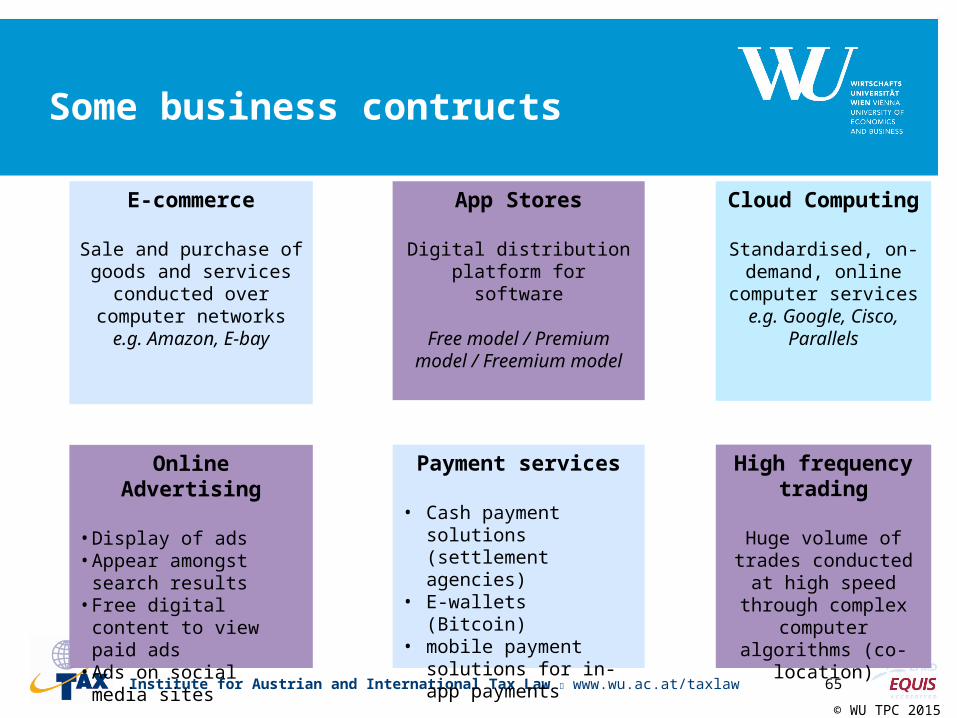

Some business contructs

E-commerce

Sale and purchase of goods and services

conducted over computer networkse.g. Amazon, E-bay

App Stores

Digital distribution platform for software

Free model / Premium model / Freemium

model

Online Advertising

• Display of ads• Appear amongst

search results• Free digital content to

view paid ads• Ads on social media

sites

Cloud Computing

Standardised, on-demand, online

computer servicese.g. Google, Cisco,

Parallels

Payment services

• Cash payment solutions (settlement agencies)

• E-wallets (Bitcoin)• mobile payment

solutions for in-app payments

High frequency trading

Huge volume of trades conducted at high speed through complex computer

algorithms (co-location)

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

66

Adaptive business models in e-commerce

Manufacturing:

Outsourcing and remote monitoring of manufacturing activities

Direct just-in-time sales

Electronic web based inventory management and ordering

Sales/distribution:

Outsource logistics to specialists for faster deliveries

Cash flow improvements through online payments

Marketing, customer relationship management:

Digital marketing

Call centres

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

67

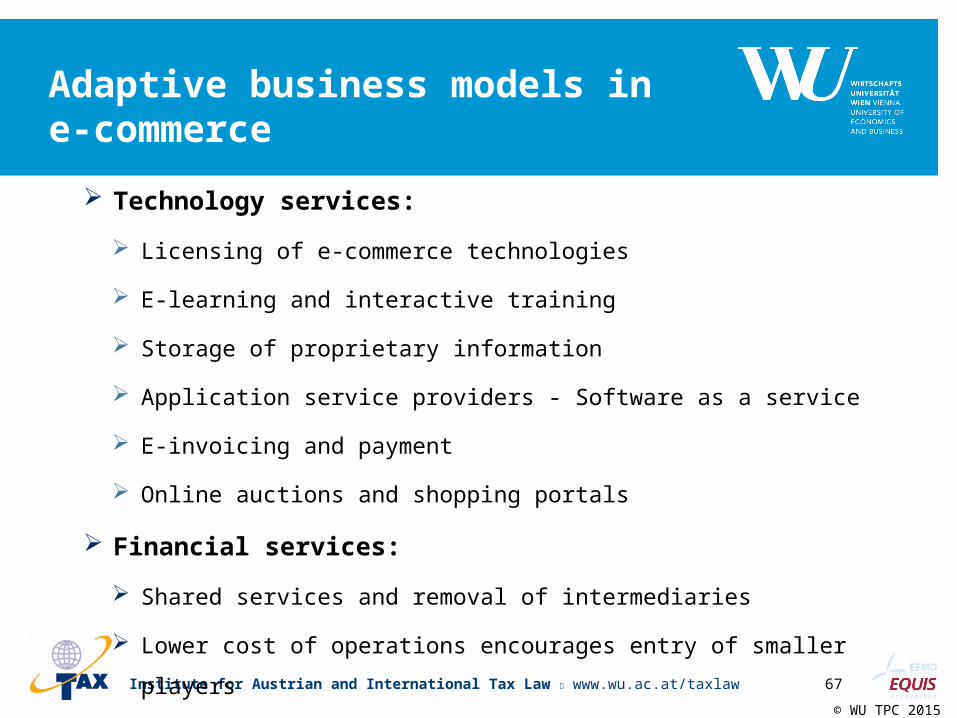

Adaptive business models in e-commerce

Technology services:

Licensing of e-commerce technologies

E-learning and interactive training

Storage of proprietary information

Application service providers - Software as a service

E-invoicing and payment

Online auctions and shopping portals

Financial services:

Shared services and removal of intermediaries

Lower cost of operations encourages entry of smaller players

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

68

Tax considerations

New business models

Online market – digitized market place

Taxability of services vis-à-vis product sales

Place of business – permanent establishment issues

Assessment of market factors having a bearing on intercompany

transaction prices/results

Intangibles – technology, content and marketing

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

69

Transfer pricing issues

Functional analysis

Allocation of economically significant functions and risks

Identification of key value drivers

Understanding of supply chain

Characterization

Application of transactional approach to determination of arm’s length price

Identifying the actual transaction and similar third party transactions

Assignment of risks between entities

Comparability factors

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

70

Transfer pricing issues

Intangibles

Who/what creates value?

Legal and economic ownership of intangibles

Technological obsolescence raises questions on intangible valuation

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

71

Taxable presence in e-commerce

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

72

Taxable presence in e-commerceReduced need of physical presence and human intermediaries

E-commerce activity with no substantial presence - only offices undertaking activities (purchase, storage) falling within preparatory and auxiliary

No need for branch offices staffing people – interaction can be undertaken remotely

People replaced by software – eg co-location

Artificial avoidance

Locating server in low-tax jurisdiction

Splitting of automated functions to different locations / servers – all within the threshold of ‘preparatory and auxiliary’

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

73

Taxable presence in e-commerceAvoiding taxable presence (noted in BEPS)

Remote interaction

Reliance on automated processes

Artificial segmentation of activities

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

74

Taxable presence in e-commerce

Is there a need to reconceptualize source for e-commerce? Is source-based taxation justifiable for income arising in e-commerce environment?

Should source countries have right to tax business income only if they have physical presence (PE)?

Where should income be regarded to be generated if all the value of what is sold is created in the residence country, but the customers that determine that value are in the source country?

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

75

Google tax

UK introduced levy on company profits that are routed through “contrived arrangements”

Popularly known as “google tax”

Tax at 25 percent of taxable diverted profits

Australia similar to UK levied tax and penalty focusing on arrangements that attempt to avoid establishing PE in australia

Equalisation levy

India recently introduced an equalisation levy on online advertising revenue earned by non-resident e-commerce companies from India

Rate of tax is 6 per cent on the consideration received from online advertising by a non-resident from a resident or non-resident having a PE in India

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

76

OECD BEPS initiative

Public Discussion Draft – BEPS Action 1: Address the tax challenges of the digital economy (March 2014 – April 2014)

Action 1: 2014 Deliverable – Addressing the Tax Challenges of the Digital Economy (September 2014)

Public Discussion Draft - BEPS Action 7: Preventing the Artificial Avoidance of PE status(October 2014 – January 2015)

Discussion Draft for Public Consultation – International VAT/GST Guidelines (December 2014 – February 2015

Revised Discussion Draft – BEPS Action 7: Preventing the Artificial Avoidance of PE status (May 15, 2015 to June 12, 2015)

Final Report – BEPS Action Plan 1 and 7 (October 2015)

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

77

Key tax challenges of Digital business models

Nexus

Ability to operate in source country without extensive physical presence – digital infrastructure is sufficient

Are current rules which hinge on physical presence sufficient? Is there a need for reformulation?

Usage of data cross border

Businesses have developed ways to collect, analyse and ultimately monetize data

Self created intangibles usually not accounted for

Value attribution to such data – challenging to anlayse the functions, assets and risks

Characterisation

Development of new products and services and new means to deliver these products and services

No clarity or precedents on characterization – especially payments for cloud computing

Levy of value added tax

Challenges related to where goods, services and intangibles are acquired by private consumers from suppliers abroad

No international framework for VAT collection

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

78

BEPS Initiative: Options Proposed for Digital Economy

No ring fencing

Digital economy is becoming the economy itself

Isolating digital economy will involve drawing arbitrary lines

The challenges faced by digital economy are also faced in traditional economy – only risk in digital economy is exacerbated due to its very nature

Modification to Exception from PE status [Article 5(4)]

Exceptions no longer serve their intended purpose

Make all activities referred to in Article 5(4) subject to the overall exception of being “preparatory or auxiliary” or remove exceptions in 5(4) completely

Report on Action Plan 7 proposes that all activities be made subject to the overall exception

New nexus based on Significant digital presence

Targeting those businesses which require minimal physical elements

An enterprise undertaking “fully dematerialized digital activities” could be deemed to have a taxable presence

Fully dematerialized digital activities could include (eg – core business is to sell digital goods and services, contracts generally concluded remotely, payments generally made online, websites are the only means of relationship with consumers).

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

79

BEPS Initiative: Options Proposed for Digital Economy

Creation of a withholding tax on digital transactions

Impose a final withholding tax on certain payments made by residents of a country for digital goods and services to a foreign e-commerce provider

Introducing equalization levy

Levy on transactions concluded with in-country customers. Applicable only where business maintains significant business presence

Feasible only where no / low tax in home jurisdiction or availability of credit against corporate tax

Transfer pricing rules

Appropriate allocation of profits – not based on legal ownership but performance of important functions and contribution of important assets

CFC rules • Definition of CFC income to include income from Digital economy• Income from Digital economy to be taxable in ultimate home jurisdiction

The Task Force on Digital Economy will monitor developments in the digital economy and other Action Plans and will determine if future work on 3 options is required, viz, equalisation levy, significant digital presence and withholding tax. The report on outcome of the

continued work will be presented in 2020

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

80

Summary

Growth in services and e-commerce are creating new challenges for taxpayers and tax administrations seeking certainty of tax policy and its administration

Stratification of services into various categories – low value/high value, core/non core

In the post-BEPS era, MNE businesses are expected to focus even more on substance and conduct

New approaches to comparability and profit attribution

…..its a small world after all….

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

81

Case studies

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

82

Case study - 2

U Co based in UK is engaged in research, development and manufacturing of forrmulated medicines at its UK facility.

Due to availability of talent and competitive pressures, it seeks to locate the research activity in India and China continuing its manufacturing operations in the UK;

Having done the feasiblity studies in these locations, U Co organises the research centre through acquisition of third party manufacturing/research entities in India and China thereby forming its subsidiaries - I Co (India) and C Co (China) which would be engaged in contract research services for U Co

U Co

I Co

UK

Contract research services

C Co

Contract research services

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

83

Case study - 2

I Co and C Co were existing businesses in India and China respectively which were historically manufacturing for third party customers in their respective markets

Whilst I Co and C Co would undertake contract research services for U Co‘s portfolio of products, they would also continue to carry out manufacturing activity for their erstwhile third party customers

The feasibility analysis shows that U Co has been able to achieve significant cost savings on account of the shifting of the research activity to India and have been able to achieve a faster pipeline growth of R&D product portfolio and patent applications

U Co

I Co

UK

Contract research services

C Co

Contract research services

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

84

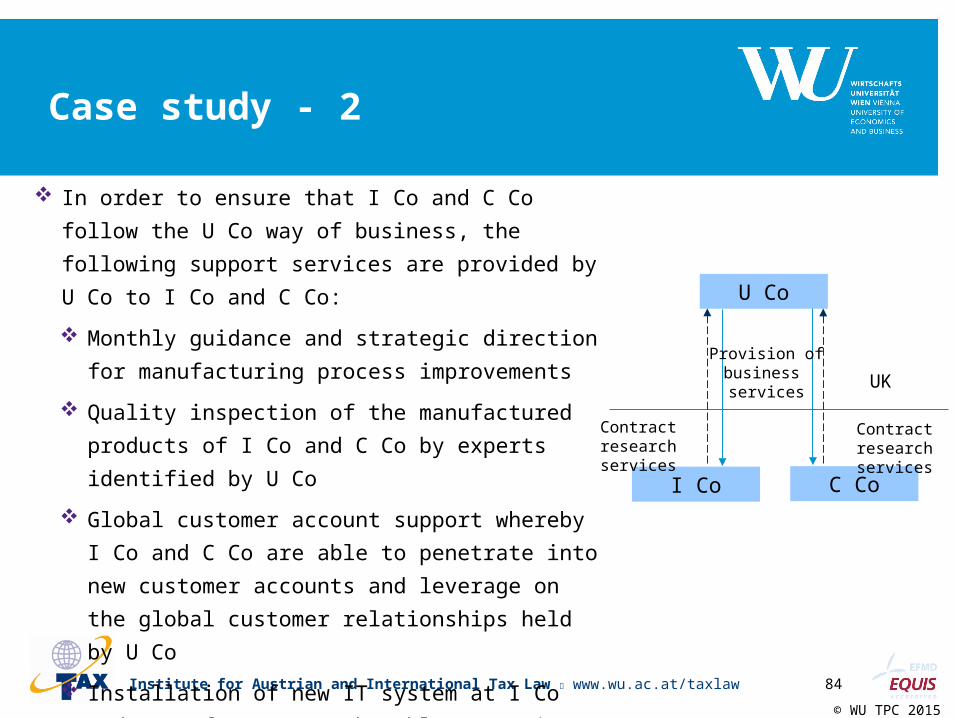

Case study - 2

In order to ensure that I Co and C Co follow the U Co way of business, the following support services are provided by U Co to I Co and C Co:

Monthly guidance and strategic direction for manufacturing process improvements

Quality inspection of the manufactured products of I Co and C Co by experts identified by U Co

Global customer account support whereby I Co and C Co are able to penetrate into new customer accounts and leverage on the global customer relationships held by U Co

Installation of new IT system at I Co and C Co for U Co to be able to monitor the performance and reporting of the respective companies

U Co

I Co

UK

Contract research services

C Co

Contract research services

Provision of business services

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

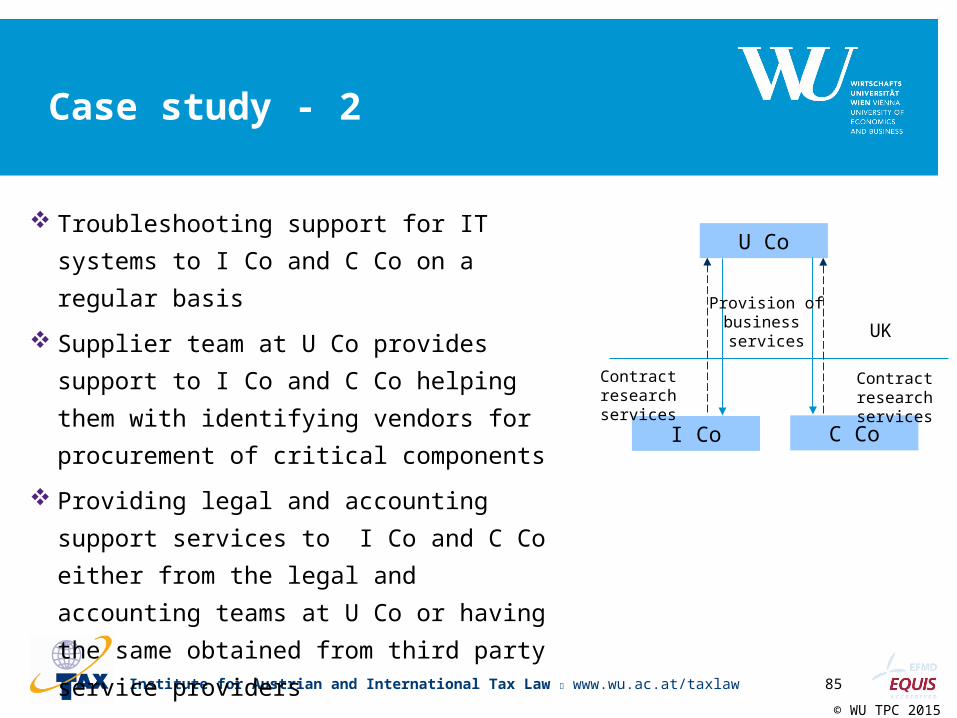

85

Case study - 2

Troubleshooting support for IT systems to I Co and C Co on a regular basis

Supplier team at U Co provides support to I Co and C Co helping them with identifying vendors for procurement of critical components

Providing legal and accounting support services to I Co and C Co either from the legal and accounting teams at U Co or having the same obtained from third party service providers

U Co

I Co

UK

Contract research services

C Co

Contract research services

Provision of business services

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

86

Case study - 2

Issues for consideration:

Whether I Co and C Co can be said to be entitled to a share of the location savings generated by U Co as a result of the shift of the research activities from the UK to India and China?

How would you categorise the nature of services provided by I Co and C Co to U Co as well as the services received by them from U Co?

What pricing policy can be considered as an appropriate compensation to the parties for the services?

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

87

Case study - 3

Facts

E Co headquartered in the US provides online training and exams in the field of engineering, medical and management. Its course includes the following:

Access to online study material

Facility of online interactive chart with other students, faculty and external experts

Appearing for online tests

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

88

Case study - 3

Issues for consideration:

Whether payments made can be considered to be in the nature of royalties, FTS or

Business Profits?

Difference between online training courses and retrieval or access to online

database

Institute for Austrian and International Tax Law www.wu.ac.at/taxlaw© WU TPC 2015

89

Case study - 3

Variation in facts

E Co establishes a subsidiary in India – I Co and wholesales the bundled

services to I Co which in turn onward sells to Indian customers

Can I Co be considered to be a “reseller” of services? What would be the other

considerations from a business, tax and regulatory standpoint?