highlights. developing - country production growth easing industrial production, ch % (3 mma, saar )...

TRANSCRIPT

Highlights

Oct-0

9

Oct-0

9

Oct-0

9

Nov-0

9

Nov-0

9

Dec-0

9

Dec-0

9

Jan-

10

Jan-

10

Feb-

10

Feb-

10

Mar

-10

Mar

-10

Apr-1

0

Apr-1

0

Apr-1

0

May

-10

May

-10

Jun-

10

Jun-

10

Jul-1

00

200

400

600

800

1,000

1,200

CDS spreads for selected economies

Spreads on credit default swaps

Average of Brazil, Russia, China, Turkey, and IndonesiaGreece Portugal Ireland Spain

Source: JP Morgan and World Bank data

basis points

Developing-country production growth easing

industrial production, ch% (3mma, saar)

Jan-08 May-08 Sep-08 Jan-09 May-09 Sep-09 Jan-10 May-10-35

-25

-15

-5

5

15

25

High-income OECD

Developing ex China

Source: DECPG.

World

Developing countries

OECD developments

WEO Update lowers growth outlook

for Europe in 20112009 2010 2011 Difference from April WEO

2010 2011

World GDP -0.6 4.6 4.3 0.4 0.0

Advanced Econ -3.2 2.6 2.4 0.3 0.0

Euro Area -4.1 1.0 1.3 0.0 -0.2

Germany -4.9 1.4 1.6 0.2 -0.1

Spain -3.6 -0.4 0.6 0.0 -0.3

Japan -5.2 2.4 1.8 0.5 -0.2

United States -2.4 3.3 2.9 0.2 0.3

Source: IMF, WEO Update, July 8, 2010.

G-20 agrees to the principle of

“growth friendly” fiscal consolidation

2007 2008 2009 2010F 2011F-12

-10

-8

-6

-4

-2

0

OECD FiscalU.S. FiscalEuro Area FiscalJapan Fiscal

2007 2008 2009 2010F 2011F0

50

100

150

200

250

OECD Debt U.S. DebtEuro Area Debt Japan Debt

Fiscal balances, %GDP Public sector financial liabilities, %GDP

Source: DECPG staff estimates.

Select OECD core CPI moves lower on mutedgoods prices tied to weaker demand core-CPI: OECD, USA, Euro Area, Spain , Japan and Ireland, ch% (3m/3m saar)

Jan-08 May-08 Sep-08 Jan-09 May-09 Sep-09 Jan-10 May-10-4

-2

0

2

4

6USA Euro Area Spain

Japan Ireland

Source: Thomson/Datastream and DECPG calculations

Progress in reducing U.S. layoffs stallsadding downward pressure on retail sales

Jan-08 Jun-08 Nov-08 Apr-09 Sep-09 Feb-10 Jul-10300

350

400

450

500

550

600

650

-18

-12

-6

0

6

12

retail sales (x-autos) volume [R]

unemployment claims [L]

unemployment claims, 4-wk average ‘000 [L] ; retail sales (x-auto) volume, ch% saar [R]

Source: U.S. Departments of Commerce and Labor.

U.S. investment to pick-up in second quarter with orders, exports and output

highercapacity utilization (%) [L], growth of orders, production and export volumes (saar) [R]

Jan-08 May-08 Sep-08 Jan-09 May-09 Sep-09 Jan-10 May-1067.5

70.0

72.5

75.0

77.5

80.0

82.5

-50

-35

-20

-5

10

25

40

cap-goods orders [R]

capacity util [L]

Source: U.S. Department of Commerce.

production [L]

exports [R]

U.S. bank lending continues declinehitting business without access to bond

markets

Jan-08 Jun-08 Nov-08 Apr-09 Sep-09 Feb-10 Jul-101,200

1,300

1,400

1,500

1,600

1,700

-25

-20

-15

-10

-5

0

5

10

percentage change (y/y) [R]

Source: Federal Reserve of St. Louis.

C&I loans [L]

Commercial & industrial loans ($billions) [L] ; percentage change (y/y) [R]

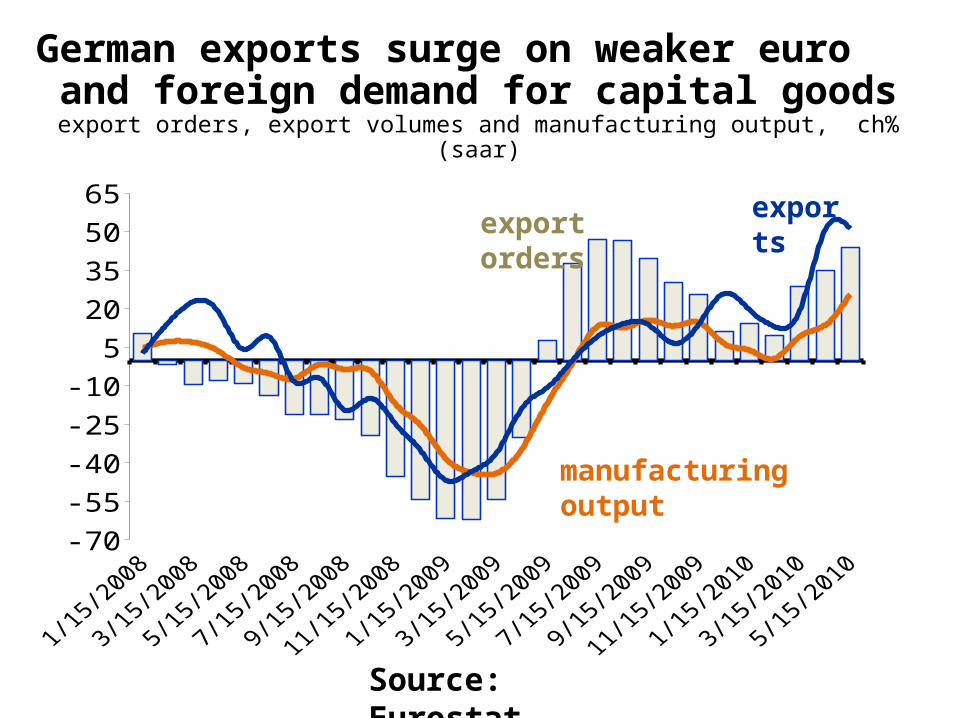

German exports surge on weaker euro and foreign demand for capital goodsexport orders, export volumes and manufacturing output, ch% (saar)

Jan-08 May-08 Sep-08 Jan-09 May-09 Sep-09 Jan-10 May-10-70

-55

-40

-25

-10

5

20

35

50

65

Source: Eurostat.

exports

manufacturing output

export orders

Euro Zone household spending continues in the doldrums

retail sales volumes: Euro Area, Germany, France (mfg gds), Italy, ch% (y/y)

Jan-08 May-08 Sep-08 Jan-09 May-09 Sep-09 Jan-10 May-10-4.5

-3.0

-1.5

0.0

1.5

3.0

4.5

Source: Eurostat.

Germany

France

Euro Area

Italy

Japan sees sobering slump in machinery orders, exports and manufacturing output

machinery orders, export volumes and manufacturing output, ch% (saar)

Jan-08 May-08 Sep-08 Jan-09 May-09 Sep-09 Jan-10 May-10-75

-60

-45

-30

-15

0

15

30

45

60

Source: Japan Cabinet Office.

exportsmanufacturing

output

machinery orders

Industrial production

-5-3-113579

111315

High-income, ex-cl.USA

Global, excl. USA

Developing coun-tries

Growth in retail sales eases on weak labor markets in high-

income countriesRetail sales proxy, ch% (y/y)

Sources: Thomson Datastream and DEC Prospects Group

Recovery continues through April / May but may

be slowing

Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-1050

60

70

80

90

100

110

120

130

ChinaOther developing

Industrial production, index August 2008=100

Sources: Thomson Datastream and DEC Prospects Group

-8-6-4-202468

10

Sources: U.S. Census Bureau and World Bank DEC Prospects Group

Positive contribution to U.S. growth of business inventories

may be coming to an endContribution to total business sales growth (manufacturing, wholesale and retail), seasonally

adjusted

International Trade

Jan-07May-07

Sep-07Jan-08

May-08Sep-08

Jan-09May-09

Sep-09Jan-10

May-1055

60

65

70

75

80

85

90

95

100

105

110

115

120

Export volumes losing momentum across devel-

oping regions

East Asia & Pacific

Europe & Central Asia

Latin America & the Caribbean

Middle East & North Africa

South Asia

Sub-Saharan Africa

U.S. and Japanese exports slow as East Asian demand decelerates

import and export volumes, ch% (3mma, saar)

Dec-09 Jan-10 Feb-10 Mar-10 Apr-10 May-10-20

0

20

40

60

80

100 China M

NIE M

USA exports

JPN exports

EU imports

Source: DEC Prospects Group.

Source: WTO.

Commodity Prices

0

20

40

60

80

100

120

140

2100

2200

2300

2400

2500

2600

2700

2800

2900

Oil price and OECD stocks$/bbl million bbl

Price Stocks

1Q00

2Q00

3Q00

4Q00

1Q01

2Q01

3Q01

4Q01

1Q02

2Q02

3Q02

4Q02

1Q03

2Q03

3Q03

4Q03

1Q04

2Q04

3Q04

4Q04

1Q05

2Q05

3Q05

4Q05

1Q06

2Q06

3Q06

4Q06

1Q07

2Q07

3Q07

4Q07

1Q08

2Q08

3Q08

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

Growth in world oil demand (y/y)

Other

Other Asia

China

OECD

mb/d

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0 OPEC spare capacitymb/d

Non-Commodity Prices

0

50

100

150

200

250

300

350

Agriculture Prices

Food

Raw Materials

Beverages

2000=100

0

10,000

20,000

30,000

40,000

50,000

60,000

0

20

40

60

80

100

120

140

160

180

Nickel price and LME stocks$/ton '000 tons

Price Stocks

Jan-

05

Apr-0

5

Jul-0

5

Oct-0

5

Jan-

06

May

-06

Aug-

06

Nov-0

6

Feb-

07

Jun-

07

Sep-

07

Dec-0

7

Mar

-08

Jun-

08

Oct-0

8

Jan-

09

Apr-0

9

Jul-0

9

Nov-0

9

Feb-

10

May

-10

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000Ocean Bulk Freight - Baltic

Dry Index

International Finance

Subdued June recovery in cross-border debt flows

$ billion 2008 2009 2010

H1Tota

l H1Tota

l H1 Apr May Jun

Total 180 305 77 253 154 39 12 17

Bonds 51 62 35 124 91 29 3 7

Banks 129 243 42 129 63 11 9 9

Lat. America 38 63 31 109 49 15 1 7

E. Europe 84 145 21 65 48 12 4 5

Asia 27 47 14 45 37 8 4 3

Others 32 51 12 34 21 4 4 1

2008 Q1

2008 Q2

2008 Q3

2008 Q4

2009 Q1

2009 Q2

2009 Q3

2009 Q4

2010 Q1

2010 Q2

0

10

20

30

40

50

60

EM corporates increasingly re-lied on international bond

markets in 2010Corporate (Private and Public)

Sovereign

$ billion

Mar.2006

Jun.2006

Sep.2006

Dec.2006

Mar.2007

Jun.2007

Sep.2007

Dec.2007

Mar.2008

Jun.2008

Sep.2008

Dec.2008

Mar.2009

Jun.2009

Sep.2009

Dec.2009

0

500

1,000

1,500

2,000

2,500

3,000

3,500

International banks' claims in developing countries rose in

2009Local currency claims International claims

Foreign exchange / Inflation

Jan-10 Feb-10 Mar-10 Apr-10 May-10 Jun-10 Jul-101.180

1.220

1.260

1.300

1.340

1.380

1.420

1.46086.25

87.50

88.75

90.00

91.25

92.50

93.75

95.00

yen/USD

USD/Euro (inverse)

Euro losses start to dissipate in July yen gains appreciably vs dollar in the month

USD per Euro (inverse) [Left] and Yen per USD [right]

Source: Thomson/Datastream and DECPG calculations.

End of dollar-fix for Chinese RMB

yields modest gains vs U.S. unit

3/1/2

010

3/13/2

010

3/25/2

010

4/6/2

010

4/18/2

010

4/30/2

010

5/12/2

010

5/24/2

010

6/5/2

010

6/17/2

010

6/29/2

010

7/11/2

01097.5

100.0

102.5

105.0

107.5

110.0

112.5

115.0

US dollar Euro Yen

3/1/2010

4/1/2010

5/1/2010

6/1/2010

7/1/20100.1460

0.1465

0.1470

0.1475

0.1480

USD per RMB

Index, RMB cross-rates, March 1, 2010=100 USD per RMB, daily: March 1 to July 16

Source: Thomson/Datastream and DECPG calculations.

LCU per RMB

Net U.S. capital flows show dramatic

“flight to quality” in the 6 months to March

Q1-2009 Q2-2009 Q3-2009 Q4-2009 Q1-2010-300-200-100

0100200300400500600700

Net FDI + Equity U.S. TreasuriesNet Other Flows Financing requirement

Source: Department of Commerce.

net annualized flows in billions U.S. dollars

FOCUS

Jan-

10

Jan-

10

Jan-

10

Feb-

10

Feb-

10

Feb-

10

Mar

-10

Mar

-10

Mar

-10

Apr-1

0

Apr-1

0

May

-10

May

-10

May

-10

Jun-

10

Jun-

10

Jun-

10

Jul-1

0

Jul-1

00.50

0.55

0.60

0.65

0.70

0.75

0.80

0.85

0.90

0.15

0.2

0.25

0.3

0.35

0.4

0.45

0.5

Euro Interbank Offer rates continued to rise, while Eu-

ribor/Eonia spread eased slightly

3-month Euribor (left axis)

percent percent

Source: Bloomberg

Euribor/Eonia spread (right axis)

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

Excess reserves at the ECB declined significantly in recent

weeks

Source: Bloomberg

Oct-0

9

Oct-0

9

Oct-0

9

Nov-0

9

Nov-0

9

Dec-0

9

Dec-0

9

Jan-

10

Jan-

10

Feb-

10

Feb-

10

Mar

-10

Mar

-10

Apr-1

0

Apr-1

0

Apr-1

0

May

-10

May

-10

Jun-

10

Jun-

10

Jul-1

00

200

400

600

800

1,000

1,200

CDS spreads for selected economies

Spreads on credit default swaps

Average of Brazil, Russia, China, Turkey, and IndonesiaGreece Portugal Ireland Spain

Source: JP Morgan and World Bank data

basis points