highlights from the q1 2015 experian-oliver wyman market intelligence report

TRANSCRIPT

1

© 2015 Experian Information Solutions, Inc. All rights reserved. Experian and the marks used herein are service marks or registered trademarks of Experian Information Solutions, Inc. Other product and company names mentioned herein are the trademarks of their respective owners. No part of this copyrighted work may be reproduced, modified, or distributed in any form or manner without the prior written permission of Experian. Experian Public.

Unique insights on the consumer credit market

Highlights from the Q1 2015 Experian–Oliver Wyman Market Intelligence Report

2 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Experian-Oliver Wyman Market Intelligence Report Introduction

Linda Haran

Senior Director Experian Decision Sciences

Alan Ikemura

Senior Product Manager Experian Decision Sciences

Today’s Speakers:

3 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

2015 Economic Outlook

Origination and Delinquency Trends

► Mortgage

► Home Equity

► Bankcard

► Automotive

Experian-Oliver Wyman Market Intelligence Report Agenda

4 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Economic Trends

5 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

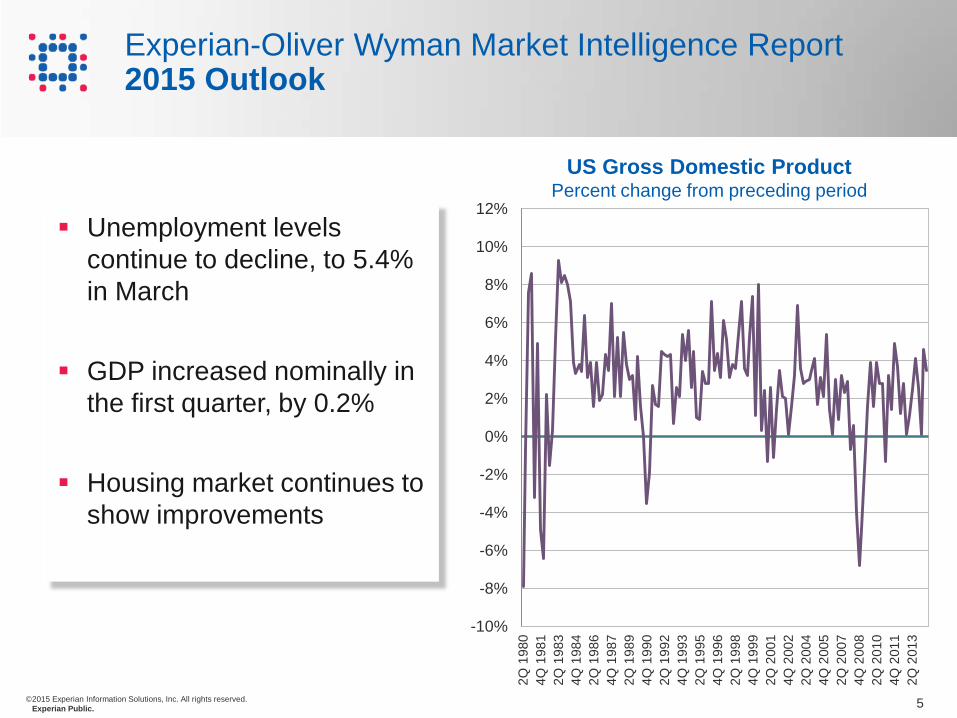

Experian-Oliver Wyman Market Intelligence Report 2015 Outlook

Unemployment levels continue to decline, to 5.4% in March

GDP increased nominally in the first quarter, by 0.2%

Housing market continues to show improvements

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

2Q 1

980

4Q 1

981

2Q 1

983

4Q 1

984

2Q 1

986

4Q 1

987

2Q 1

989

4Q 1

990

2Q 1

992

4Q 1

993

2Q 1

995

4Q 1

996

2Q 1

998

4Q 1

999

2Q 2

001

4Q 2

002

2Q 2

004

4Q 2

005

2Q 2

007

4Q 2

008

2Q 2

010

4Q 2

011

2Q 2

013

US Gross Domestic Product Percent change from preceding period

6 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Mortgage Trends

7 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

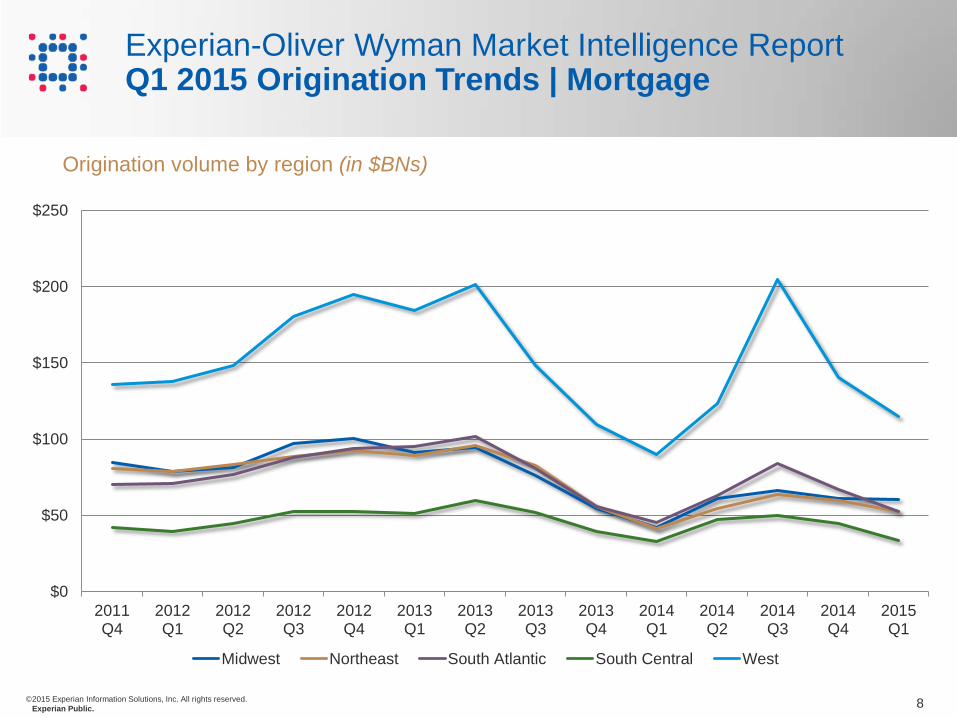

Experian-Oliver Wyman Market Intelligence Report Q1 2015 Origination Trends | Mortgage

$0

$100

$200

$300

$400

$500

$600

2011Q4

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

$416 $407 $436 $508 $537 $515 $555 $441 $317 $253 $350 $386 $374 $316

Mortgage origination volume (in $BNs)

YoY increase of 25%

8 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

$0

$50

$100

$150

$200

$250

2011Q4

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

Midwest Northeast South Atlantic South Central West

Experian-Oliver Wyman Market Intelligence Report Q1 2015 Origination Trends | Mortgage

Origination volume by region (in $BNs)

9 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

2011Q4

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

30-59 60-89 90-180

Mortgage delinquency rates as % of balances

Experian-Oliver Wyman Market Intelligence Report Q1 2015 Delinquency Trends | Mortgage

10 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Experian-Oliver Wyman Market Intelligence Report Q1 2015 Delinquency Trends | Mortgage

30+ dpd balance exposure (in $BNs)

$7.0

$7.2

$7.4

$7.6

$7.8

$8.0

$8.2

$8.4

$8.6

$8.8

$9.0

$0

$100

$200

$300

$400

$500

$600

2011Q4

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

30+ dpd Exposure Balances O/S

30+ delinquency exposure continues to decline while balances see steady increases

11 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

0%

1%

2%

3%

4%

5%

6%

3 6 9 12 15 18 21 24

Months after origination

2008 Q2 2009 Q2 2010Q2 2011Q2 2012Q2 2013Q2 2014Q2

Experian-Oliver Wyman Market Intelligence Report Q1 2015 Delinquency Trends | Mortgage

Vintage performance | 30+ delinquency rates as % of trades

12 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Home Equity Trends

13 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

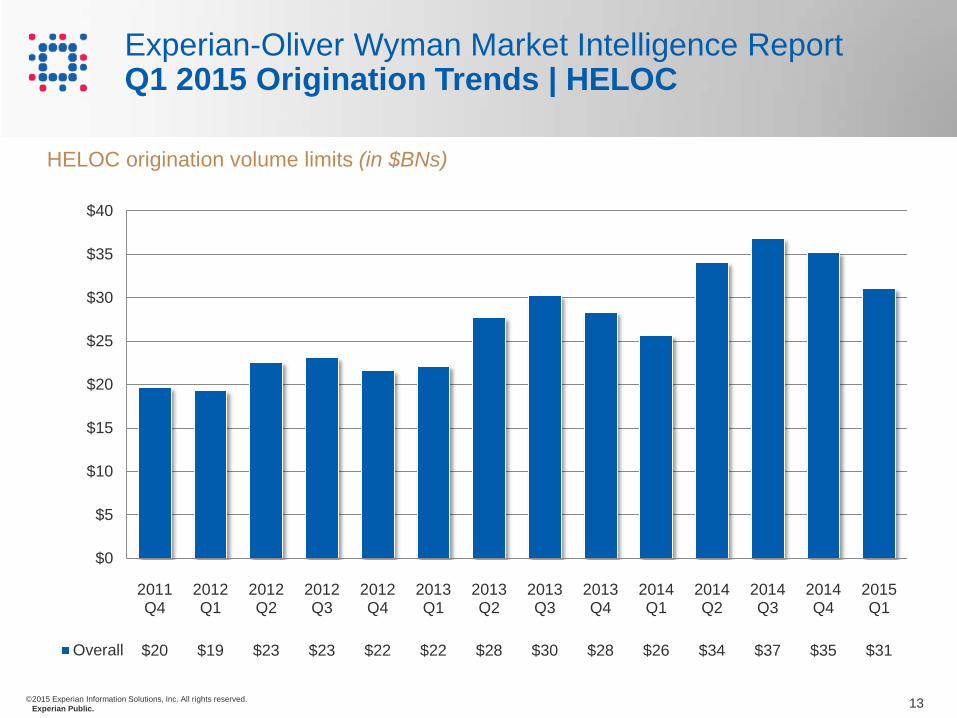

$0

$5

$10

$15

$20

$25

$30

$35

$40

2011Q4

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

Overall $20 $19 $23 $23 $22 $22 $28 $30 $28 $26 $34 $37 $35 $31

HELOC origination volume limits (in $BNs)

Experian-Oliver Wyman Market Intelligence Report Q1 2015 Origination Trends | HELOC

14 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

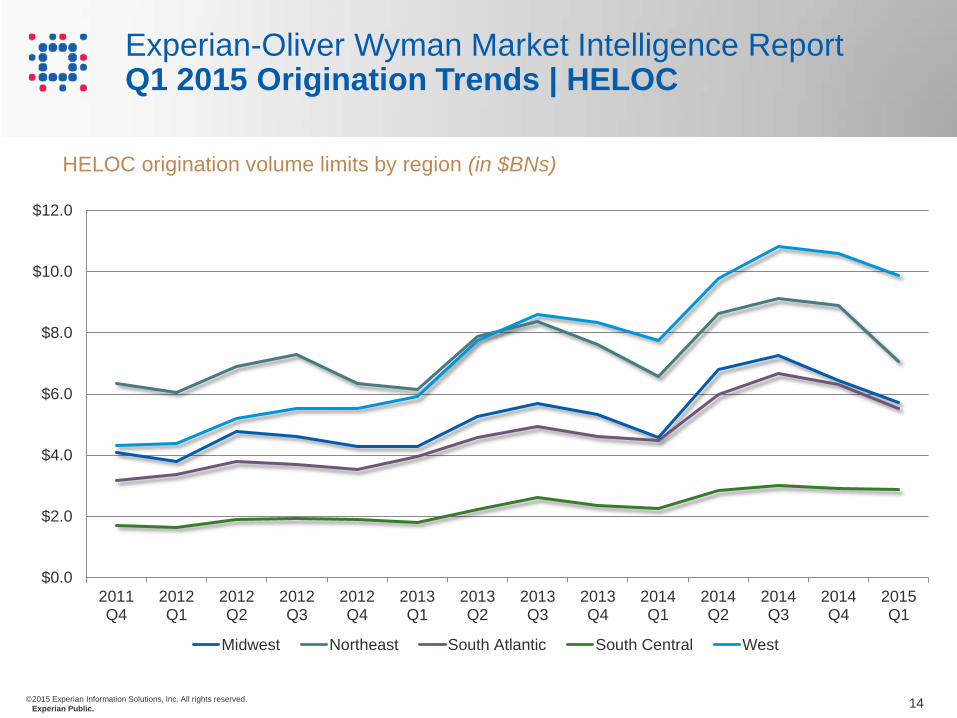

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

2011Q4

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

Midwest Northeast South Atlantic South Central West

Experian-Oliver Wyman Market Intelligence Report Q1 2015 Origination Trends | HELOC

HELOC origination volume limits by region (in $BNs)

15 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

2011Q4

2012Q1

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

30-59 60-89 90-180

HELOC delinquency rates as % of balances

Experian-Oliver Wyman Market Intelligence Report Q1 2015 Delinquency Trends | HELOC

16 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

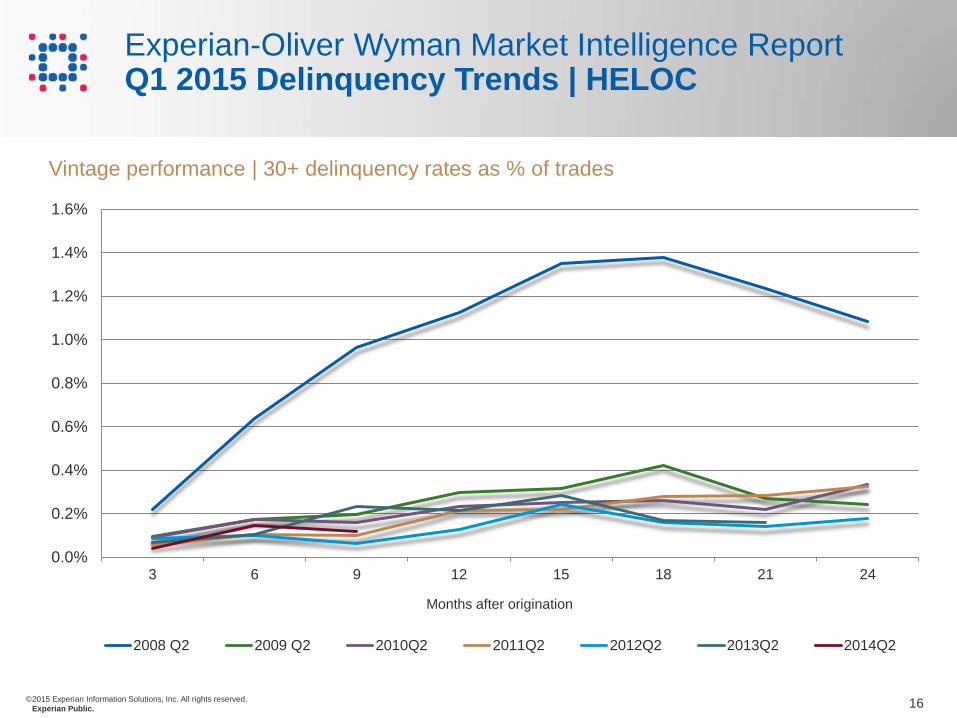

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

3 6 9 12 15 18 21 24

Months after origination

2008 Q2 2009 Q2 2010Q2 2011Q2 2012Q2 2013Q2 2014Q2

Experian-Oliver Wyman Market Intelligence Report Q1 2015 Delinquency Trends | HELOC

Vintage performance | 30+ delinquency rates as % of trades

17 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Bankcard Trends

18 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

$57 $57 $61 $59 $63 $68 $77 $71 $77 $81 $80 $77

Bankcard origination volume (in $BNs)

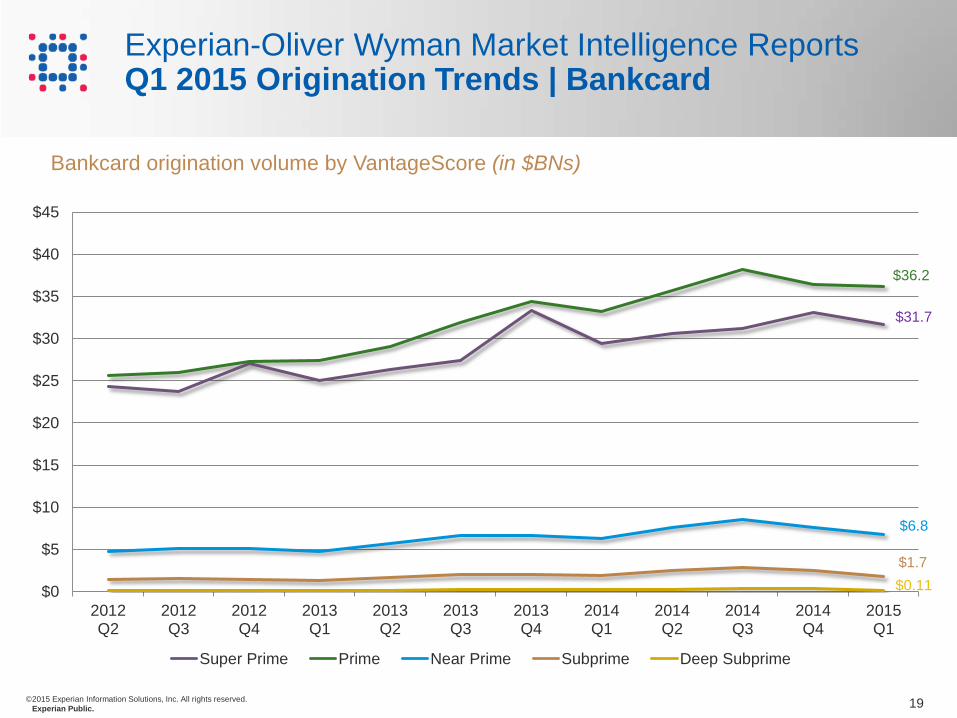

Experian-Oliver Wyman Market Intelligence Reports Q1 2015 Origination Trends | Bankcard

19 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

$36.2

$6.8

$1.7

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

Super Prime Prime Near Prime Subprime Deep Subprime

Experian-Oliver Wyman Market Intelligence Reports Q1 2015 Origination Trends | Bankcard

Bankcard origination volume by VantageScore (in $BNs)

$0.11

$31.7

20 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

SuperPrime

Prime NearPrime

Subprime DeepSubprime

Q1 2014 Q1 2015

Average limit per new trade by VantageScore (in $s)

-30.0%

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

Super Prime Prime Near Prime

Subprime Deep Subprime

-0.6% -3.2%

-17.5%

-8.8%

-25.9%

Experian-Oliver Wyman Market Intelligence Reports Q1 2015 Origination Trends | Bankcard

YoY % change in average limit by VantageScore

$9,604

$5,209

$2,277

$966 $509

$9,543

$5,382

$2,497

$1,171 $686

21 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

550

560

570

580

590

600

610

620

630

640

650

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

Balances O/S Unemployment

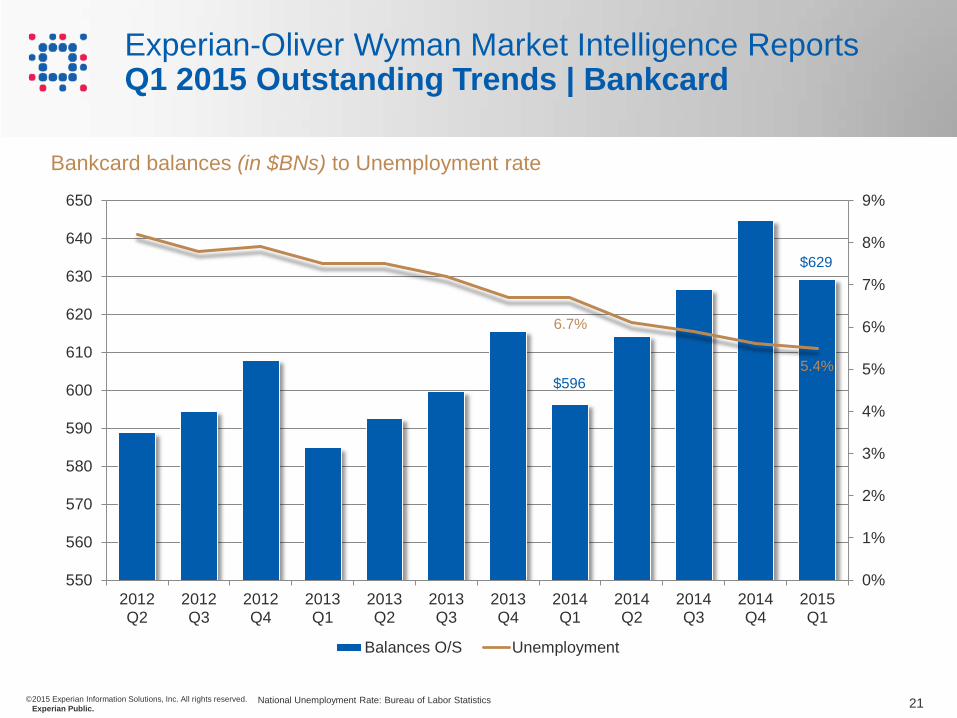

Experian-Oliver Wyman Market Intelligence Reports Q1 2015 Outstanding Trends | Bankcard

Bankcard balances (in $BNs) to Unemployment rate

National Unemployment Rate: Bureau of Labor Statistics

6.7%

$629

5.4% $596

22 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

30-59 DPD 60-89 DPD 90-180 DPD Charge-offs

Bankcard delinquency rates as % of balances

Experian-Oliver Wyman Market Intelligence Reports Q1 2015 Delinquency Trends | Bankcard

4.33%

1.28%

0.78%

0.48%

23 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Auto Trends

24 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

$0

$20

$40

$60

$80

$100

$120

$140

$160

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

$107 $116 $109 $115 $132 $135 $121 $127 $142 $146 $133 $134

Auto origination volume (in $BNs) $555BN

+8%

Experian-Oliver Wyman Market Intelligence Reports Q1 2015 Origination Trends | Auto Loans

$515BN

25 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

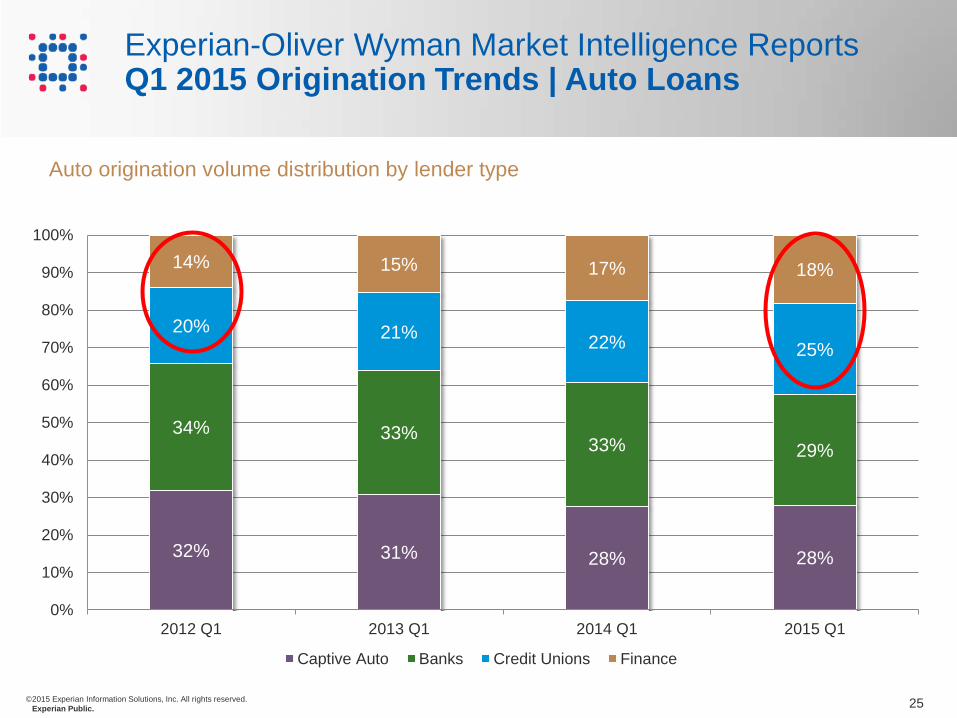

32% 31% 28% 28%

34% 33% 33% 29%

20% 21% 22% 25%

14% 15% 17% 18%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2012 Q1 2013 Q1 2014 Q1 2015 Q1

Captive Auto Banks Credit Unions Finance

Experian-Oliver Wyman Market Intelligence Reports Q1 2015 Origination Trends | Auto Loans

Auto origination volume distribution by lender type

26 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

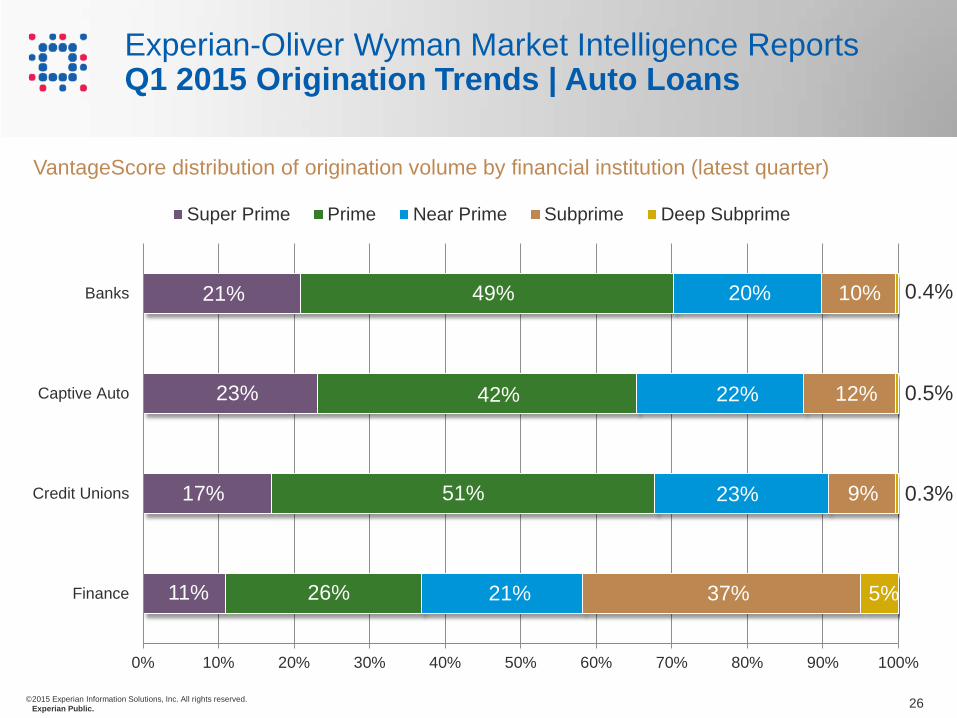

Finance

Credit Unions

Captive Auto

Banks

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Super Prime Prime Near Prime Subprime Deep Subprime

Experian-Oliver Wyman Market Intelligence Reports Q1 2015 Origination Trends | Auto Loans

VantageScore distribution of origination volume by financial institution (latest quarter)

21% 10% 20% 49%

42% 23% 22% 12%

17% 51% 23% 9%

11% 26% 21% 37% 5%

0.4%

0.5%

0.3%

27 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

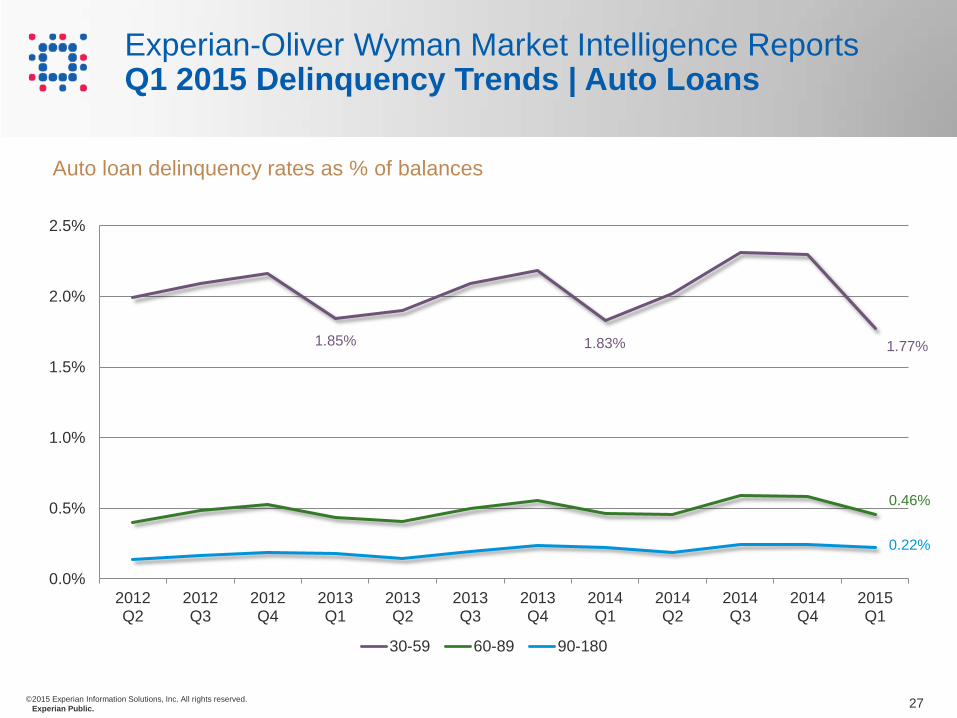

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

2012Q2

2012Q3

2012Q4

2013Q1

2013Q2

2013Q3

2013Q4

2014Q1

2014Q2

2014Q3

2014Q4

2015Q1

30-59 60-89 90-180

Auto loan delinquency rates as % of balances

1.83% 1.85% 1.77%

Experian-Oliver Wyman Market Intelligence Reports Q1 2015 Delinquency Trends | Auto Loans

0.46%

0.22%

28 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Experian-Oliver Wyman Market Intelligence Report Q1 2015 Summary

Economy slowed in the quarter, but steady ► Unemployment continues to decline ► GDP relatively flat; consumer confidence stable

Real estate showing signs of life ► 1st Mortgage: 25% increase YoY ► HELOC originations: still generating over $30BN/quarter ► Strong loan performance for both portfolios

Bankcard increases, but slower than prior quarters ► 8% YoY and 6% YoY for originations and balances, respectively ► Delinquency remains near all-time lows

Auto growing through continuing channel diversification ► 6% YoY growth; Credit Unions and Finance categories now

represent over 40% of originations ► Delinquency back in check after slight upticks in previous

quarters

29 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

Experian-Oliver Wyman Market Intelligence Report IntelliView

*NEW* Segment by Experian-exclusive scores

*NEW* Overlay key macroeconomic indicators

A unique combination of industry leading assets from Experian and Oliver Wyman

Benchmark your portfolio performance against peers and industry to gain a competitive advantage

Quickly and easily respond to what-if scenarios and run multiple iterations as needed

IntelliView v1.2 now available!

30 © 2015 Experian Information Solutions, Inc. All rights reserved. Experian Public.

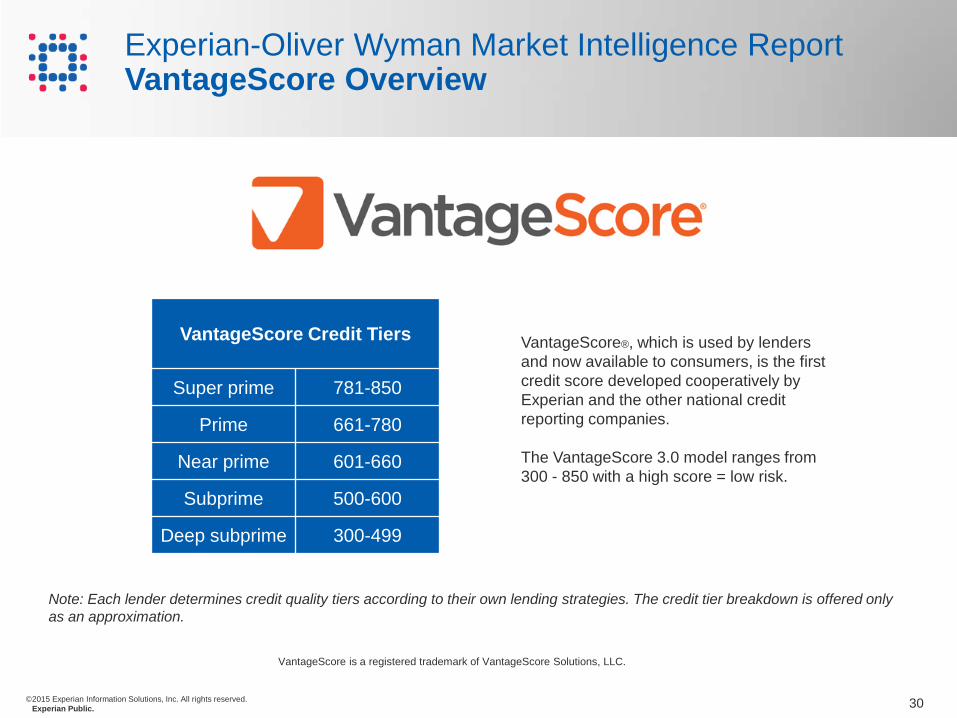

Experian-Oliver Wyman Market Intelligence Report VantageScore Overview

VantageScore Credit Tiers

Super prime 781-850

Prime 661-780

Near prime 601-660

Subprime 500-600

Deep subprime 300-499

VantageScore®, which is used by lenders and now available to consumers, is the first credit score developed cooperatively by Experian and the other national credit reporting companies. The VantageScore 3.0 model ranges from 300 - 850 with a high score = low risk.

Note: Each lender determines credit quality tiers according to their own lending strategies. The credit tier breakdown is offered only as an approximation.

VantageScore is a registered trademark of VantageScore Solutions, LLC.