hiland partners, lp (hlnd) hil d h ldi gp lphiland...

TRANSCRIPT

RBC Capital MarketspMLP ConferenceNovember 2008

Hiland Partners, LP (HLND)Hil d H ldi GP LP (HPGP)Hiland Holdings GP, LP (HPGP)

Joe GriffinChi f E ti OffiChief Executive Officer

Matt HarrisonChief Financial Officer

Robert ShainChief Commercial Officer

Derek GipsonDirector – Business Development & Investor Relations

Risks and Forward-Looking Statements

Investment in the common units of Hiland Partners, LP and Hiland Holdings GP, LP (collectively, “Hiland” or the“Partnership”) involves risks associated with the Partnership’s business, the Partnership’s structure and the taxcharacteristics of the common units. These risks can significantly impact the market value of Hiland’s common units.

The statements made by representatives of Hiland during the course of this presentation that are not historical facts areforward-looking statements. Although Hiland believes that the assumptions underlying these statements are reasonable,investors are cautioned that such forward-looking statements are inherently uncertain and necessarily involve risks thatmay affect Hiland’s business prospects and performance, causing actual results to differ from those discussed during thispresentation. When considering forward-looking statements, you should keep in mind the risk factors and othercautionary statements included in Hiland’s various filings with the Securities & Exchange Commission (“SEC”)cautionary statements included in Hiland s various filings with the Securities & Exchange Commission ( SEC ).

Any forward-looking statements made are subject to all of the risks and uncertainties, many of which are beyondmanagement’s control, involved in gathering, compressing, dehydrating, treating, processing and marketing natural gas,fractionating NGLs and providing air compression and water injection services for oil and gas secondary recoveryoperations These risks include the risks described in the Partnership’s Form 10 K and other documents filed from time tooperations. These risks include the risks described in the Partnership s Form 10-K and other documents filed from time totime with the SEC. Should one or more of these risks or uncertainties occur, or should underlying assumptions proveincorrect, Hiland’s actual results and plans could differ materially from those expressed in any forward-lookingstatements.

The Partnership undertakes no obligation to publicly update any forward looking statements whether as a result of newThe Partnership undertakes no obligation to publicly update any forward-looking statements, whether as a result of newinformation or future events.

2

Non-GAAP Measures

This presentation includes the non-generally accepted accounting principles (“non-GAAP”) financial measure of EBITDA.We define EBITDA, a non-GAAP financial measure, as net income plus interest expense, provisions for income taxes anddepreciation, amortization and accretion expense. EBITDA is used as a supplemental financial measure by ourmanagement and by external users of our financial statements such as investors, commercial banks, research analystsand others to assess: (1) the financial performance of our assets without regard to financial methods capital structure orand others to assess: (1) the financial performance of our assets without regard to financial methods, capital structure orhistorical costs basis; (2) the ability of our assets to generate cash sufficient to pay interest costs and support ourindebtedness; (3) our operating performance and return on capital as compared to those of other companies in themidstream energy sector, without regard to financing and structure; and (4) the viability of acquisitions and capitalexpenditure projects and the overall rates of return on alternative investment opportunities. EBITDA is also a financialmeasurement that, with certain negotiated adjustments, is reported to our banks and is used as a gauge for compliancewith our financial covenants under our credit facility. EBITDA should not be considered as an alternative to net income,operating income, cash flows from operating activities or any other measure of financial performance presented inaccordance with GAAP. Our EBITDA may not be comparable to EBITDA of similarly titled measures of other entities, asother entities may not calculate EBITDA in the same manner as we do.

3

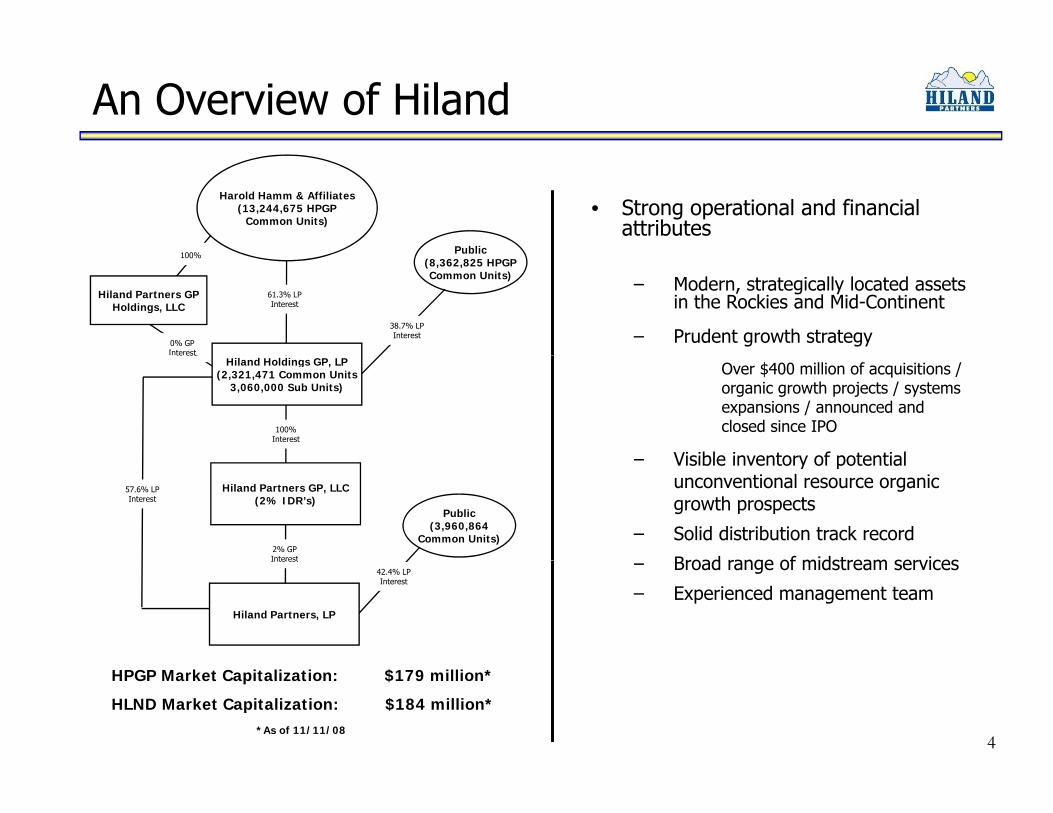

An Overview of Hiland

• Strong operational and financial attributes

Public100%

Harold Hamm & Affiliates(13,244,675 HPGP

Common Units)

– Modern, strategically located assets in the Rockies and Mid-Continent

– Prudent growth strategy

Public(8,362,825 HPGPCommon Units)

Hiland Partners GPHoldings, LLC

61.3% LPInterest

38.7% LPInterest

0% GPInterest

100%

Over $400 million of acquisitions / organic growth projects / systems expansions / announced and closed since IPO

Visible inventory of potential

100%Interest

te estHiland Holdings GP, LP

(2,321,471 Common Units3,060,000 Sub Units)

– Visible inventory of potential unconventional resource organic growth prospects

– Solid distribution track record

Broad range of midstream services

Public(3,960,864

Common Units)

Hiland Partners GP, LLC(2% IDR’s)

2% GPInterest

57.6% LPInterest

– Broad range of midstream services

– Experienced management team

Interest

42.4% LPInterest

Hiland Partners, LP

4

HPGP Market Capitalization: $179 million*

HLND Market Capitalization: $184 million**As of 11/11/08

Hiland Midstream Natural Gas Services

TransmissionTransmission

Hiland Partners’

Midstream LinesLines Midstream Focus

Wellhead

Gathering, Dehydrationand Compression

Processing, Treating and Fractionation

NGL ProductsTransportation− Truck− Y-grade line

5

and Fractionation Y grade line− Rail terminal

Business Strategy

• Engage in construction of organic growth projects and system expansion opportunities

– Unique relationship with Continental Resources, Inc.

Opportunity to gain insight regarding production growth and reserve potential in emerging unconventional resource playsreserve potential in emerging unconventional resource plays

– Expand systems to meet growing demand

• Increase volumes on existing assets while controlling costs• Increase volumes on existing assets while controlling costs

• Pursue complementary acquisitions

T t t iti th t d i i ti i– Target opportunities that expand our presence in existing service territories, offer operational efficiencies and increase utilization

• Reduce exposure to commodity price risk

6

p y p

• Grow distributions to unitholders

Distribution Growth Since IPO

HLND - 96% Growth Since IPO HPGP - 72% Growth Since IPO

$4.00 $1.50

$1 80$1.85

$2.05

$2.50 $2.60 $2.70 $2.80 $2.85 $2.85 $2.93

$3.02 $3.18

$3.31 $3.45 $3.52

$2.00

$2.50

$3.00

$3.50

$0.74

$0.81 $0.83 $0.83 $0.88 $0.92

$1.02 $1.12

$1.22 $1.27

$0.75

$1.00

$1.25

$1.80

$0.50

$1.00

$1.50

$2.00

$0.25

$0.50

$0.00

IPO 2Q05 3Q05 4Q05 1Q06 2Q06 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08 2Q08 2Q08

$0.00

IPO 3Q06 4Q06 1Q07 2Q07 3Q07 4Q07 1Q08 2Q08 3Q08

7

Unique Relationship with Continental Resources, Inc.

• Hiland’s predecessor formed in 1990 to support Continental Resources, Inc.’s (“CLR”) E&P activities

• CLR is a publicly-traded E&P company with an active drilling program– $4.3 billion equity market capitalization (IPO – May 2007)– $663 million drilling capex budget for 2008, $541 million drilling capex budget for 2009 (recently

announced)– EBITDAX of $665 million for the nine months ended 9/30/08– Significant reserve and production growth potentialSignificant reserve and production growth potential– Organic growth strategy focused on unconventional resource plays

− Approximately 1.1 million net undeveloped acres in unconventional plays and growing− Define new shale plays− Take large acreage positions in new and defined shale plays− Embrace and execute horizontal drilling, high psi fracturing and complex drilling and completion of high organic content shale wells

React to and perfect drilling and completion techniques to make each shale well commercial− React to and perfect drilling and completion techniques to make each shale well commercial

• HLND, HPGP and CLR are separate entities with Harold Hamm as the controlling equity holder.

• Hiland’s relationship with CLR has enabled it to significantly expand its asset base– Recently announced North Dakota Bakken organic growth projectRecently announced North Dakota Bakken organic growth project– Montana Bakken acquisition– Badlands system expansion– Woodford Shale organic growth project

8

Overview of Continental Resources, Inc.

$470

$665

$500

$600

$700

EBITDAX ($MM) 2008E Drilling Capex - $663 MM

$184

$53$21

Red River Units

$116

$285

$372

$ 0

$200

$300

$400

$500

$130

Red River Units

Bakken

Other Rockies

Woodford

Other Mid-Con$116

$0

$100

2004 2005 2006 2007 9 Mos. 08

Production (boepd) Announced 2009E Drilling Capex - $541 MM

$245

$30 Gulf Coast

( p ) Announced 2009E Drilling Capex $541 MM

19 751

24,707

29,099

33,297

25,000

30,000

35,000

$101

$99

$14 $12

Red River Units

14,121

19,751

10,000

15,000

20,000

$34

Bakken

Other Areas

Arkoma Woodford

Anadarko Woodford

Atoka

Source: Continental Resources, Inc. – Company Presentations 10/14/2008 and 11/13/2008 and CLR 3Q 2008 earnings press release.9

0

5,000

2004 2005 2006 2007 3Q 08$281

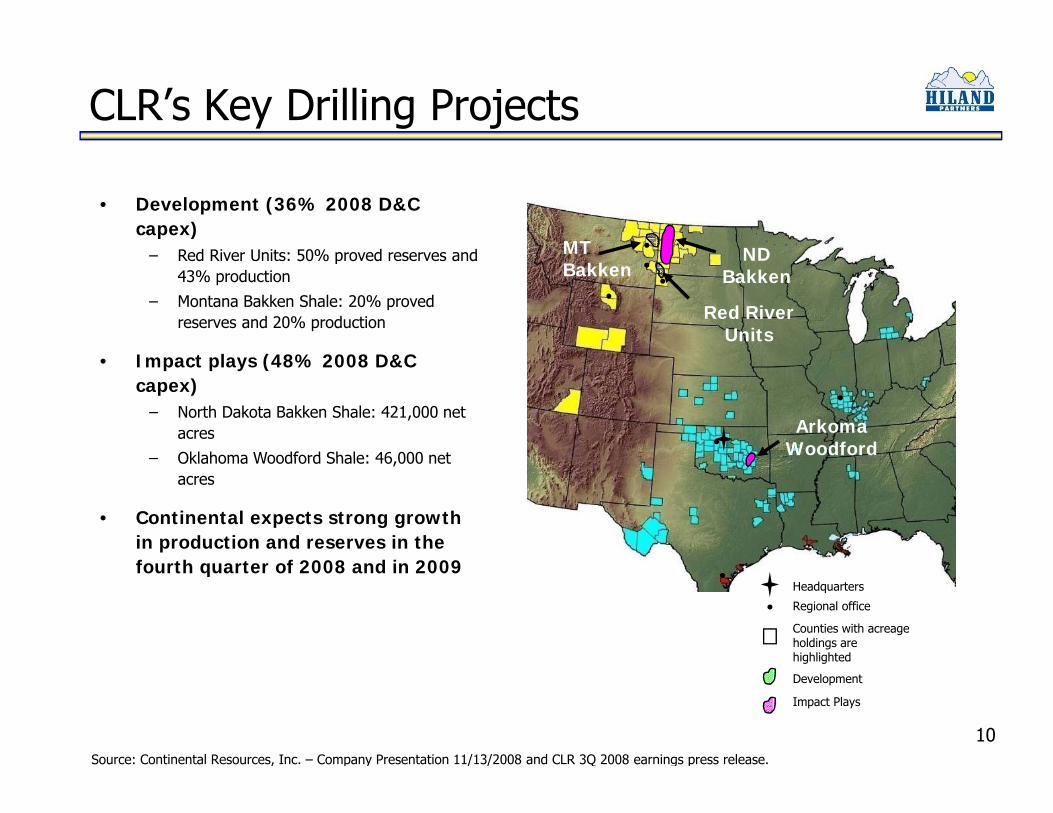

CLR’s Key Drilling Projects

• Development (36% 2008 D&C capex)

Red River Units: 50% proved reserves and MT ND− Red River Units: 50% proved reserves and 43% production

− Montana Bakken Shale: 20% proved reserves and 20% production

I t l (48% 2008 D&C

Red River Units

MT Bakken

ND Bakken

• Impact plays (48% 2008 D&C capex)− North Dakota Bakken Shale: 421,000 net

acres

− Oklahoma Woodford Shale: 46 000 net

Arkoma Woodford− Oklahoma Woodford Shale: 46,000 net

acres

• Continental expects strong growth in production and reserves in the f th t f 2008 d i 2009fourth quarter of 2008 and in 2009

Counties with acreage holdings are highlighted

Regional office

Headquarters

10

g g

Development

Impact Plays

Source: Continental Resources, Inc. – Company Presentation 11/13/2008 and CLR 3Q 2008 earnings press release.

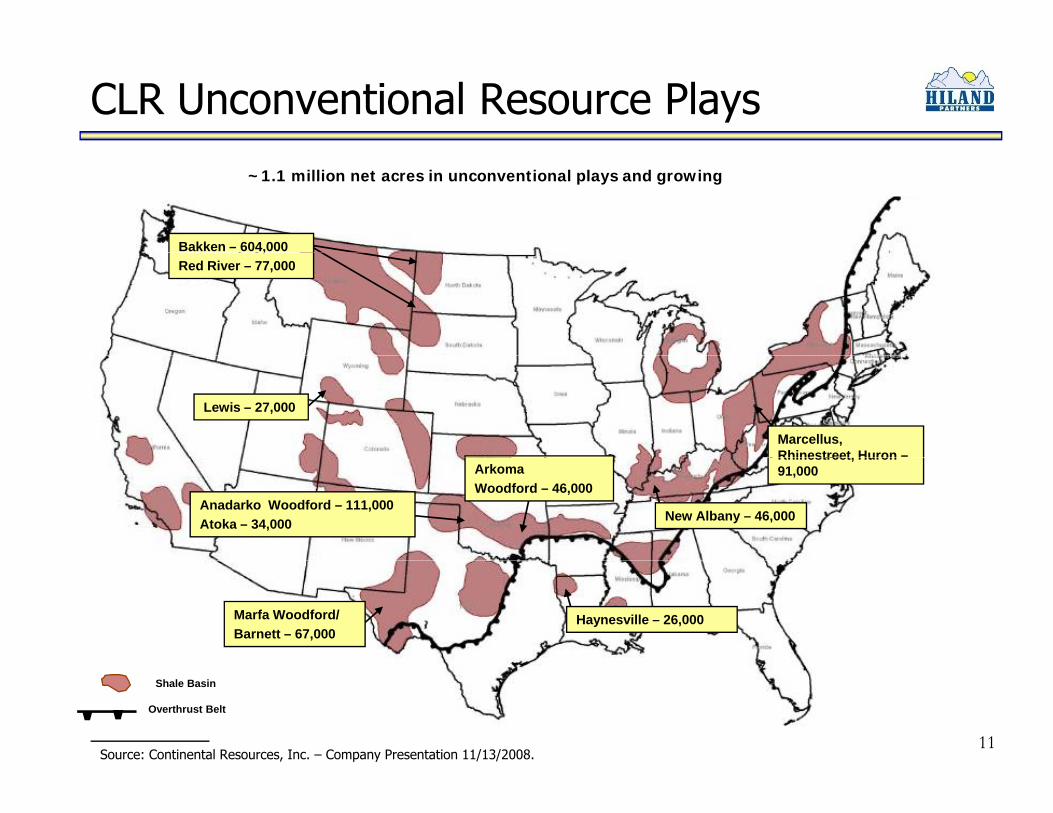

CLR Unconventional Resource Plays

~1.1 million net acres in unconventional plays and growing

Bakken – 604,000,Red River – 77,000

Marcellus, Rhinestreet, Huron –

Lewis – 27,000

Rhinestreet, Huron 91,000

New Albany – 46,000

ArkomaWoodford – 46,000

Anadarko Woodford – 111,000Atoka – 34,000

Haynesville – 26,000Marfa Woodford/Barnett – 67,000

Shale Basin

Overthrust Belt

Source: Continental Resources, Inc. – Company Presentation 11/13/2008.11

CLR’s Rocky Mountain Operations

ND Bakken

12Source: Continental Resources, Inc. – Company Presentation 11/13/2008.

Bakken Shale

Mon

t

Nort

Williston Basin• Largest unconventional oil resource

play in the lower 48− ~4B boe technologically recoverable

reserves (USGS)

Mon ND

Williston Basin

tana

thD

akota

reserves (USGS)

− Play is being developed through horizontal drilling and advanced fracture stimulation

• CLR is the largest leaseholder with ntan

a

North

Dakota

604,000 net acres− 9,631 net boepd in 3Q 2008

− 70+ rigs operating− ConocoPhillips

EOG Reso ces

Outline of potential

− EOG Resources

− Hess

− Marathon

• CLR has allocated $281 million of its

CLR H i t l B kk d

Bakken production 2009 capex budget for the Bakken shale

• 52% of drilling capex budget

• Drill 131 gross (44.1 net) wells

13

CLR acreage Horizontal Bakken producer

Source: Continental Resources, Inc. – Company Presentation 11/13/2008 and CLR 3Q 2008 earnings press release.

CLR - ND Bakken - Recent Activity

CLR-operated wells Gross wells completedN t ll l t d

3Q0816

5 3

1H0846

12 4

• 9 Three Forks/Sanish wells completed with

Net wells completedGross 7-day avg. IP rate

5.3602 boepd

12.4493 boepd

stronger average production than Middle Bakken wells in the play

• Completion process improving overall

• Drilling program now primarily targetingDrilling program now primarily targeting TFS

New acreage

THREE FORKS HORIZONTAL

CLR OPERATED

CLR NON-OPERATED

14

CLR NON OPERATED

NO CLR INTEREST

Source: Continental Resources, Inc. – Company Presentation 11/13/2008.

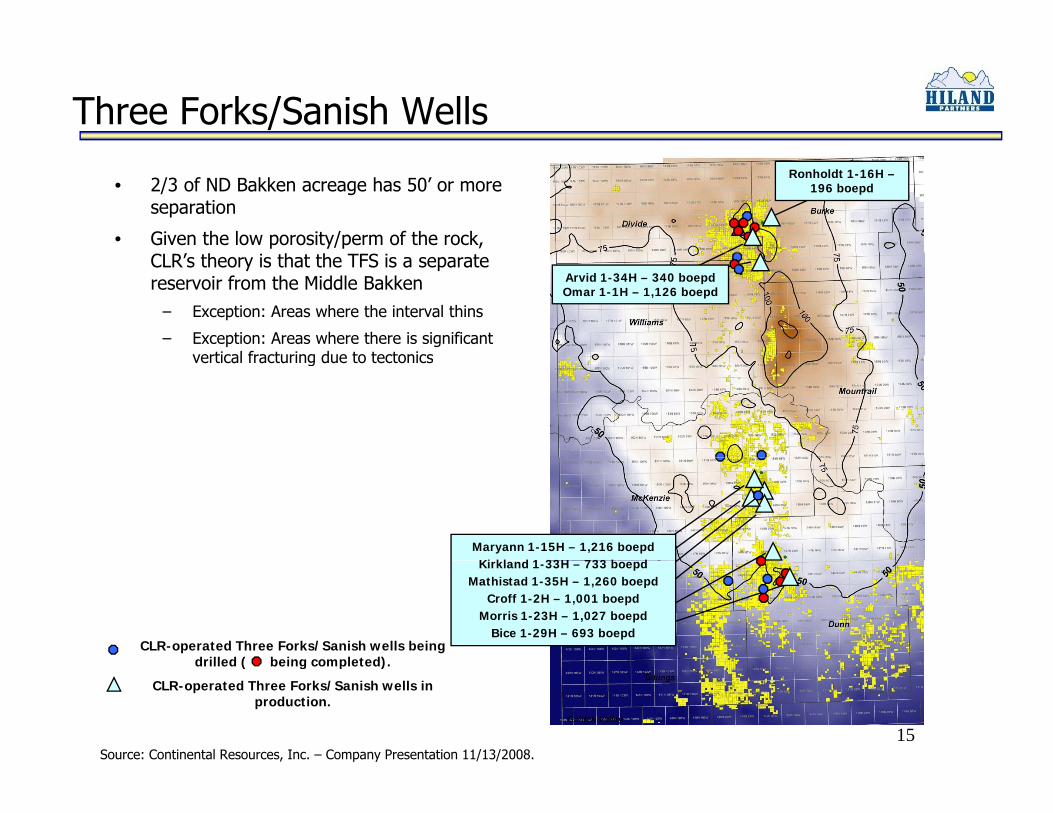

Three Forks/Sanish Wells

• 2/3 of ND Bakken acreage has 50’ or more separation

• Given the low porosity/perm of the rock,

Ronholdt 1-16H –196 boepd

CLR’s theory is that the TFS is a separate reservoir from the Middle Bakken

– Exception: Areas where the interval thins

– Exception: Areas where there is significant vertical fracturing due to tectonics

Arvid 1-34H – 340 boepdOmar 1-1H – 1,126 boepd

vertical fracturing due to tectonics

Maryann 1-15H – 1,216 boepdKi kl d 1 33H 733 b dKirkland 1-33H – 733 boepd

Mathistad 1-35H – 1,260 boepdCroff 1-2H – 1,001 boepd

Morris 1-23H – 1,027 boepdBice 1-29H – 693 boepd

CLR-operated Three Forks/Sanish wells being drilled ( being completed)

15

drilled ( being completed).

CLR-operated Three Forks/Sanish wells in production.

Source: Continental Resources, Inc. – Company Presentation 11/13/2008.

CLR’s Montana Bakken Shale

• Significant unconventional oil resource play

Mon

Nort

Dako

Williston Basin

– Represents ½ of Montana’s oil production – ~50,000 boepd

– 6,187 net boepd in 3Q 2008– Developed through horizontal drilling

and advanced fracture stimulation

tana

thotaRichland Co., MT Bakken

and advanced fracture stimulation

• CLR’s 3Q08 infield wells averaged 391 boepd in their 7-day production test (33% higher than 2Q08)( g Q )

• CLR recently began drilling its first Three Forks/Sanish test well in MT

• CLR and other producers are initiating a C02 injection pilot program in Richland County

– Start by end of 2008

Outline of potential Bakken production

yCLR acreage Horizontal Bakken producer Vertical Bakken producer

16Source: Continental Resources, Inc. – Company Presentation dated 4/10/2008 and 3Q 08 earnings press release.

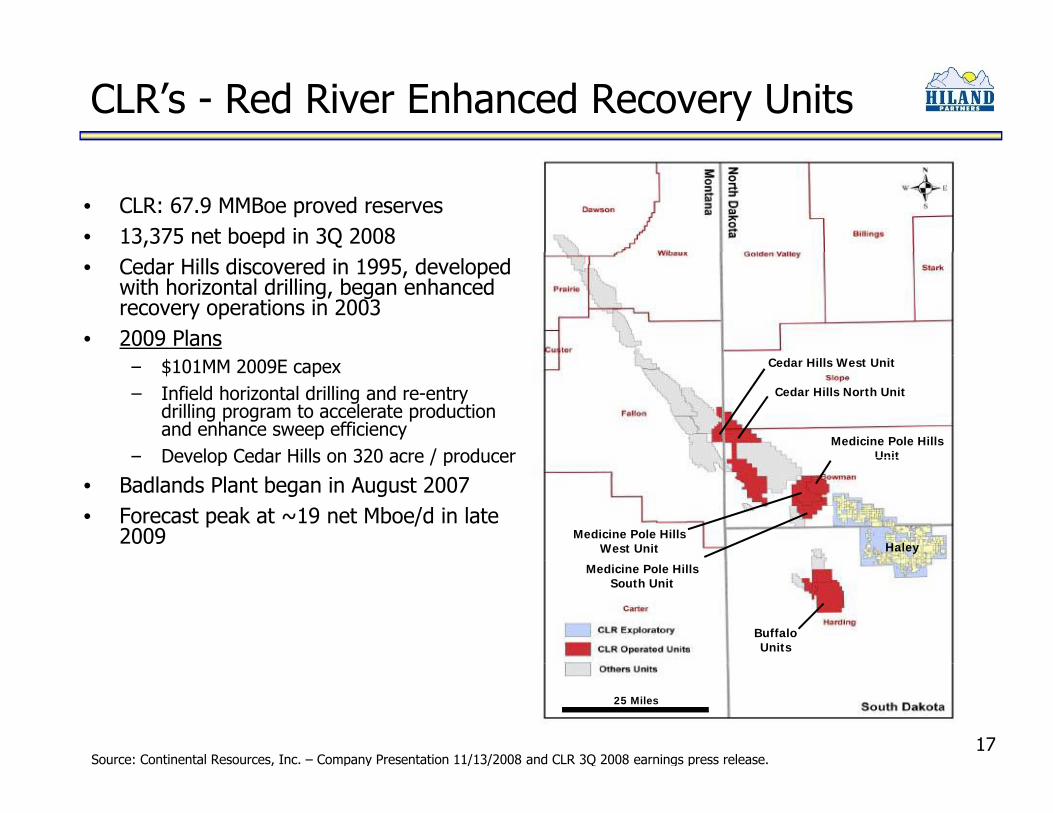

CLR’s - Red River Enhanced Recovery Units

• CLR: 67.9 MMBoe proved reserves• 13,375 net boepd in 3Q 2008• Cedar Hills discovered in 1995, developed

with horizontal drilling, began enhanced recovery operations in 2003

• 2009 Plans– $101MM 2009E capex– Infield horizontal drilling and re-entry

drilling program to accelerate production and enhance sweep efficiency

– Develop Cedar Hills on 320 acre / producer

Cedar Hills North Unit

Cedar Hills West Unit

Medicine Pole Hills UnitDevelop Cedar Hills on 320 acre / producer

• Badlands Plant began in August 2007• Forecast peak at ~19 net Mboe/d in late

2009 Medicine Pole Hills West Unit

Unit

Haley

Buffalo Units

Medicine Pole Hills South Unit

17

25 Miles25 Miles

Source: Continental Resources, Inc. – Company Presentation 11/13/2008 and CLR 3Q 2008 earnings press release.

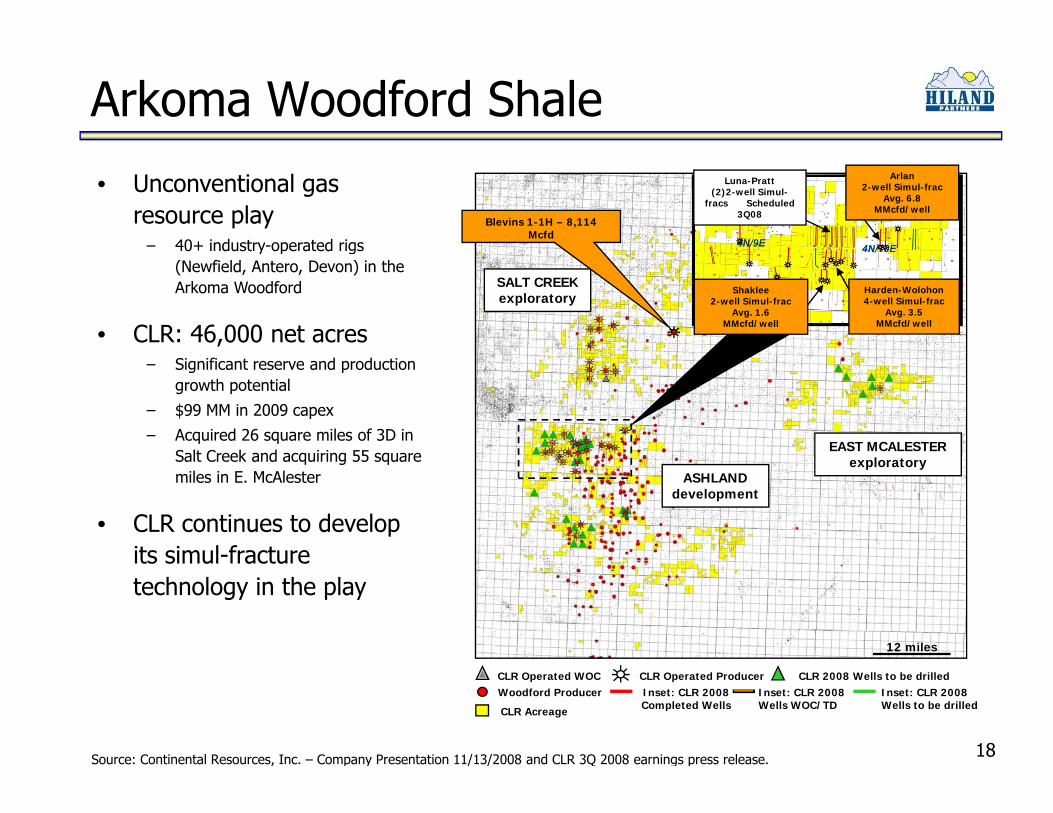

Arkoma Woodford ShaleArlan

2-well Simul-frac Avg. 6.8

MMcfd/wellBlevins 1-1H – 8,114

Mcfd

Luna-Pratt (2)2-well Simul-

fracs Scheduled 3Q08

• Unconventional gas resource play − 40+ industry-operated rigs

SALT CREEK exploratory

Harden-Wolohon 4-well Simul-frac

Avg. 3.5 MMcfd/well

Shaklee 2-well Simul-frac

Avg. 1.6 MMcfd/well

y p g(Newfield, Antero, Devon) in the Arkoma Woodford

• CLR: 46,000 net acres

EAST MCALESTER l t

− Significant reserve and production growth potential

− $99 MM in 2009 capex

− Acquired 26 square miles of 3D in Salt Creek and acquiring 55 square exploratory

ASHLANDdevelopment

Salt Creek and acquiring 55 square miles in E. McAlester

• CLR continues to develop its simul-fracture

12 miles

its simul fracture technology in the play

18

CLR Operated WOC CLR Operated Producer CLR 2008 Wells to be drilledWoodford Producer

CLR Acreage

Inset: CLR 2008 Wells WOC/TD

Inset: CLR 2008 Wells to be drilled

Inset: CLR 2008 Completed Wells

Source: Continental Resources, Inc. – Company Presentation 11/13/2008 and CLR 3Q 2008 earnings press release.

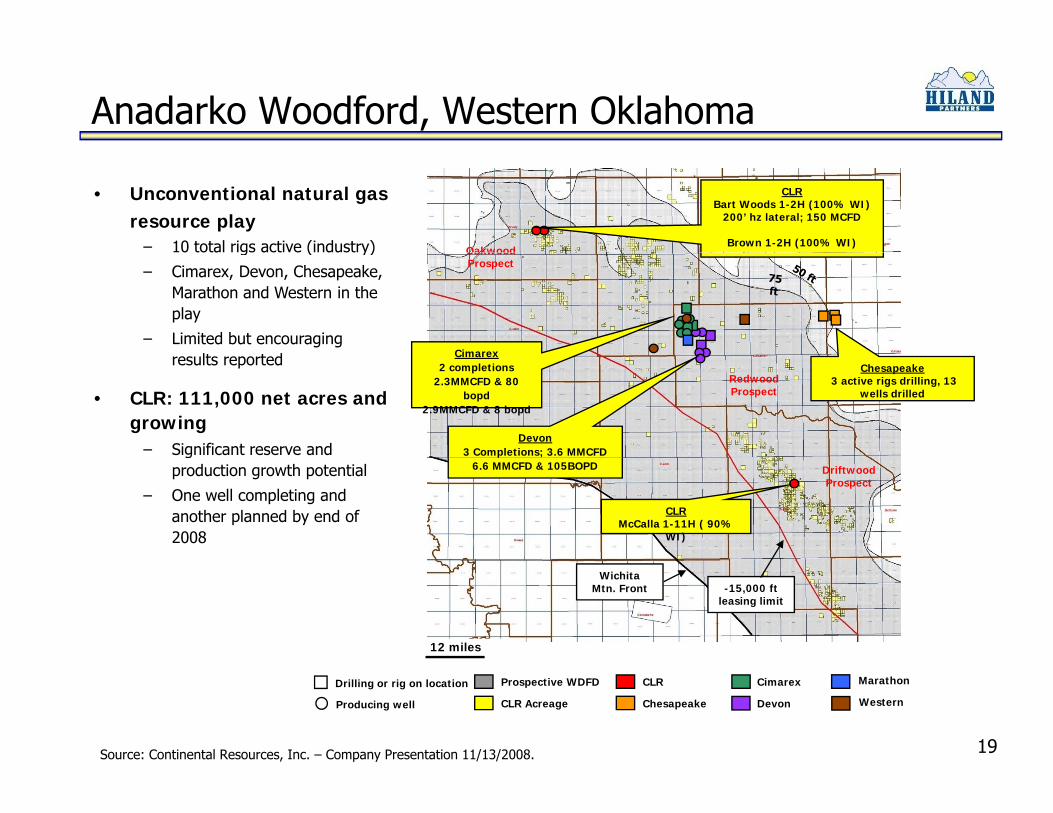

Anadarko Woodford, Western Oklahoma

• Unconventional natural gas resource play− 10 total rigs active (industry) Oakwood

CLR Bart Woods 1-2H (100% WI)

200’ hz lateral; 150 MCFD

Brown 1-2H (100% WI) g ( y)

− Cimarex, Devon, Chesapeake, Marathon and Western in the play

− Limited but encouraging lt t d

Oakwood Prospect

Cimarexresults reported

• CLR: 111,000 net acres and growing − Significant reserve and

Redwood Prospect

Chesapeake3 active rigs drilling, 13

wells drilled

Cimarex2 completions

2.3MMCFD & 80 bopd

2.9MMCFD & 8 bopd

Devon3 Completions; 3.6 MMCFD g

production growth potential

− One well completing and another planned by end of 2008

Driftwood Prospect

6.6 MMCFD & 105BOPD

CLR McCalla 1-11H ( 90%

WI)

12 miles

Wichita Mtn. Front -15,000 ft

leasing limit

19

Marathon

Western

Drilling or rig on location

Producing well

Prospective WDFD

CLR Acreage

CLR

Chesapeake

Cimarex

Devon

Source: Continental Resources, Inc. – Company Presentation 11/13/2008.

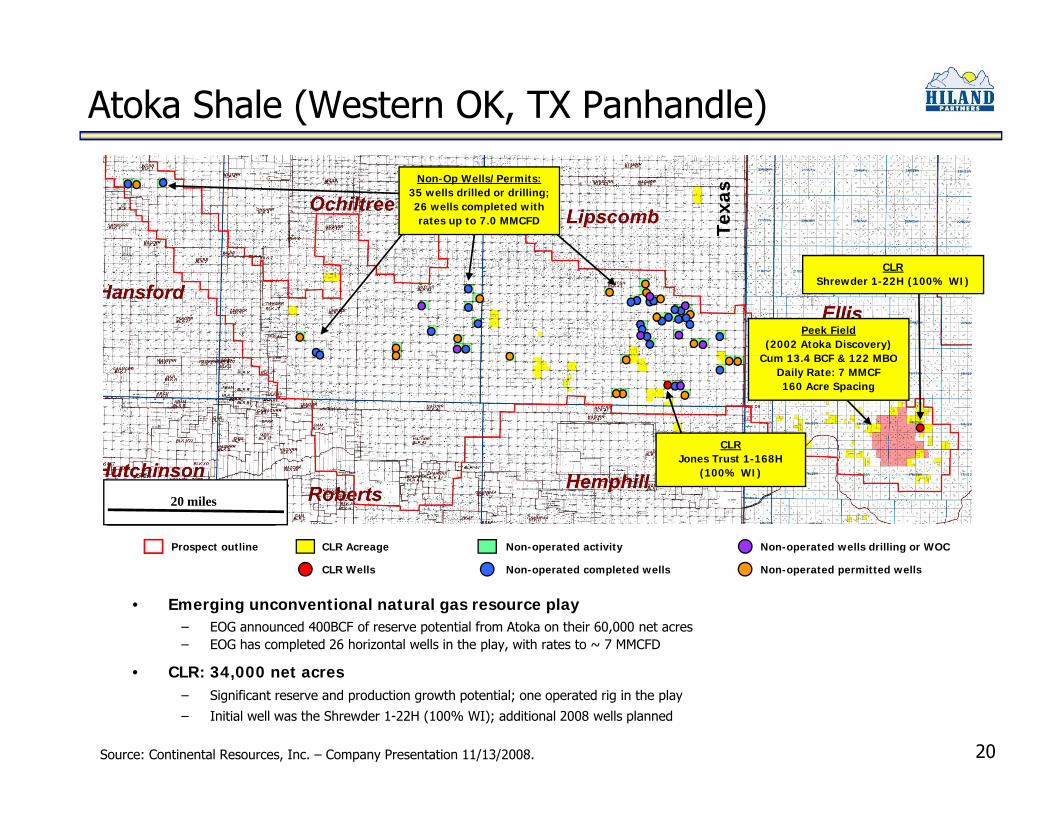

Atoka Shale (Western OK, TX Panhandle)

Non-Op Wells/Permits:35 wells drilled or drilling;26 wells completed with rates up to 7.0 MMCFD Te

xas

Peek Field(2002 Atoka Discovery)

C 13 4 BCF & 122 MBO

CLRShrewder 1-22H (100% WI)

Cum 13.4 BCF & 122 MBODaily Rate: 7 MMCF160 Acre Spacing

CLRJones Trust 1 168H

20 miles

Prospect outline CLR Acreage Non-operated wells drilling or WOCNon-operated activity

Jones Trust 1-168H (100% WI)

20 miles

• Emerging unconventional natural gas resource play − EOG announced 400BCF of reserve potential from Atoka on their 60,000 net acres − EOG has completed 26 horizontal wells in the play, with rates to ~ 7 MMCFD

CLR Wells Non-operated permitted wellsNon-operated completed wells

20

• CLR: 34,000 net acres− Significant reserve and production growth potential; one operated rig in the play

− Initial well was the Shrewder 1-22H (100% WI); additional 2008 wells planned

Source: Continental Resources, Inc. – Company Presentation 11/13/2008.

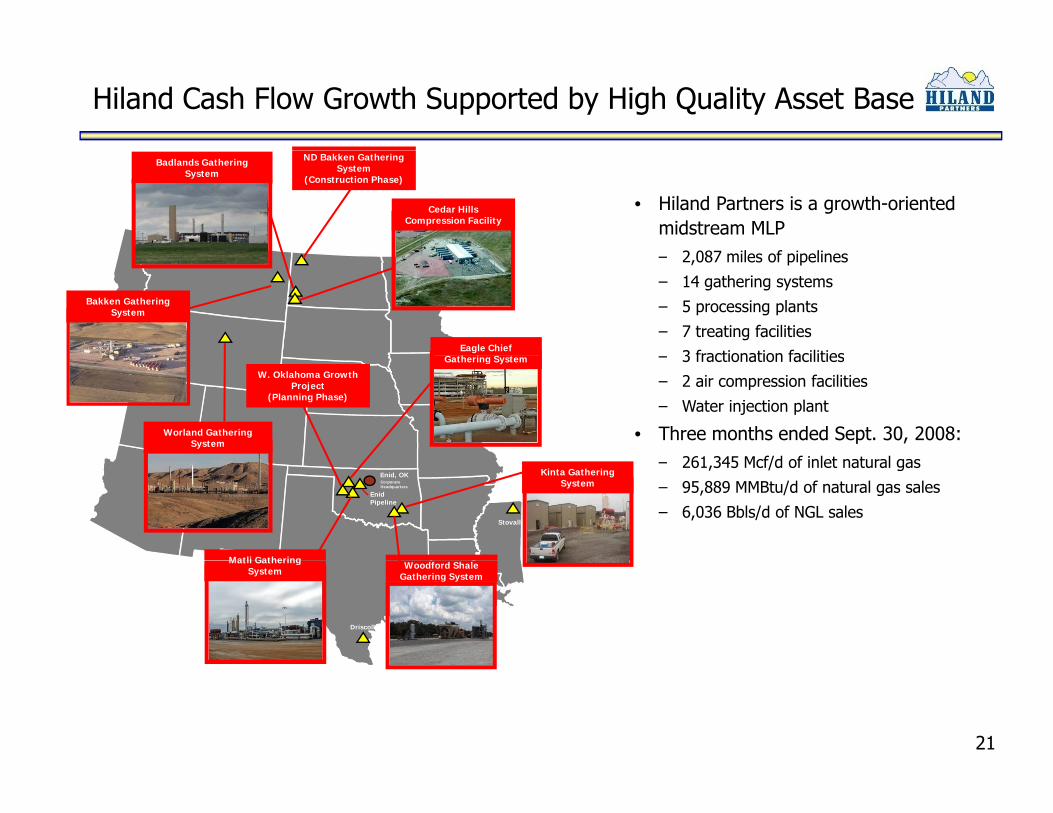

Hiland Cash Flow Growth Supported by High Quality Asset Base

• Hiland Partners is a growth-oriented midstream MLP

2 087 il f i li

Cedar Hills Compression Facility

Badlands Gathering System

ND Bakken Gathering System

(Construction Phase)

– 2,087 miles of pipelines

– 14 gathering systems

– 5 processing plants

– 7 treating facilities

3 fractionation facilities

Bakken Gathering System

Eagle Chief G h i S – 3 fractionation facilities

– 2 air compression facilities

– Water injection plant

• Three months ended Sept. 30, 2008:261 345 M f/d f i l t t l

Gathering System

Worland Gathering System

W. Oklahoma Growth Project

(Planning Phase)

– 261,345 Mcf/d of inlet natural gas

– 95,889 MMBtu/d of natural gas sales

– 6,036 Bbls/d of NGL salesStovall

Enid Pipeline

CorporateHeadquarters

Enid, OK

Matli Gathering

Kinta Gathering System

Driscoll

Matli Gathering System Woodford Shale

Gathering System

21

Execution of Business Strategy

• 129,000 gross acres dedicated

ND Bakken Gathering System – Organic Growth Project

dedicated

• $10 million capex in 2008; additional $17 million over next three years

• 10 year agreement with Continental Resources

• Install field gathering, compression treating andcompression, treating and processing facilities

• “NGL Only” sales via JT processing expected to

l 1Q09commence early 1Q09

22

Execution of Business Strategy

• Operating Highlights

MT Bakken Gathering System - Acquisition

– 365 miles of pipelines

– 273 wells connected

– 25,000 Mcf/d processing plant capacity

– 6,500 Bbl/d Fractionation facility

• Expansion of NGL fractionation facilitiesfractionation facilities

– Increased volumes from Bakken and Badlands Plants

– Potential 3rd party volume

• Major Gas Suppliers:Major Gas Suppliers:– Enerplus– Continental Resources– ConocoPhillips

23

Execution of Business Strategy

• Start up of 40,000 Mcf/d nitrogen rejection plant and

Badlands Gathering System – Significant System Expansion

Solid Volume Growth g j ptreating facilities in August 2007

• Recently announced plans to expand gathering system

Inlet System Mcf/d

September ‘07 13,219 expand gathering system– Continental Resources –

Cedar Hills Looping and Compression Project

• Operating highlights:

December ’07 17,727

March ’08 21,979

June ’08 26,315 Operating highlights:– 214 miles of pipeline– 163 wells connected

• Major Gas Suppliers:C i l R

September ’08 26,582

– Continental Resources– Luff

24

Execution of Business Strategydf d Sh l G h S O G hWoodford Shale Gathering System – Organic Growth Project

• 35,000 gross acres dedicated from Continental Resourcesfrom Continental Resources

• Start up of Phase I in April 2007

• 25,000 Mcf/d capacity as of March 2008

• Recently completed expansion to over 65,000 Mcf/d

Solid Volume Growth

Inlet System Mcf/dMcf/d

Mid-May 2008 – 35,000 Mcf/d

June 2008 – 48,000

June ’07 2,304

September ’07 8,247

D b ’07 12 358 Mcf/d

Early August 2008 –65,000 Mcf/d

December ’07 12,358

March ’08 18,371

June ’08 24,078

September ’08 31 139

25

September ’08 31,139

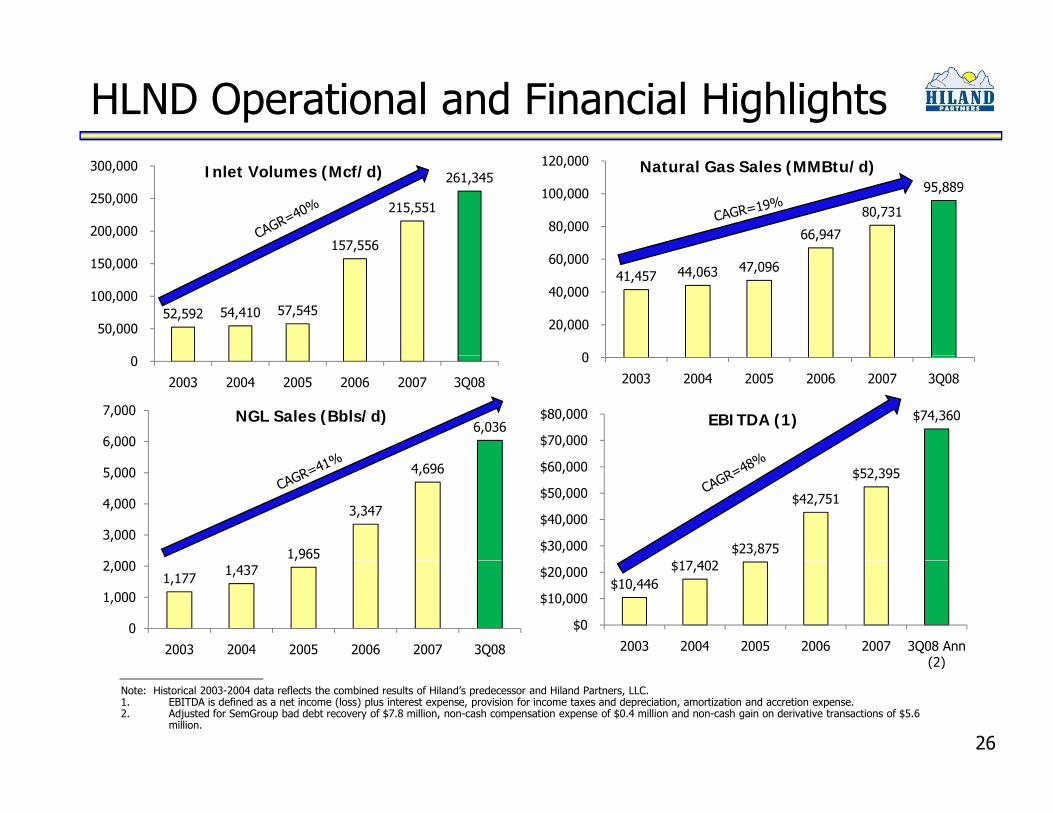

HLND Operational and Financial Highlights

157,556

215,551

261,345

200,000

250,000

300,000 Inlet Volumes (Mcf/d)

66,947

80,731

95,889

80,000

100,000

120,000 Natural Gas Sales (MMBtu/d)

52,592 54,410 57,545 50,000

100,000

150,000 41,457 44,063 47,096

0

20,000

40,000

60,000

0

2003 2004 2005 2006 2007 3Q08

0

2003 2004 2005 2006 2007 3Q08

6,0366,000

7,000 NGL Sales (Bbls/d) $74,360

$70,000

$80,000 EBITDA (1)

1,965

3,347

4,696

3,000

4,000

5,000

$ 02$23,875

$42,751

$52,395

$30,000

$40,000

$50,000

$60,000

1,177 1,437,

0

1,000

2,000

2003 2004 2005 2006 2007 3Q08

$10,446 $17,402

$0

$10,000

$20,000

2003 2004 2005 2006 2007 3Q08 Ann (2)

26

Note: Historical 2003-2004 data reflects the combined results of Hiland’s predecessor and Hiland Partners, LLC.1. EBITDA is defined as a net income (loss) plus interest expense, provision for income taxes and depreciation, amortization and accretion expense.2. Adjusted for SemGroup bad debt recovery of $7.8 million, non-cash compensation expense of $0.4 million and non-cash gain on derivative transactions of $5.6

million.

__________________(2)

Hiland’s Contract Mix

3Q 08 Midstream Margin by Contract Type

13%

POP w/ Incremental

22%

/FeesPOI - Keep Whole

I d Mi F K

7%

Index Minus Fees - Keep WholeFixed Fee - Gathering

59%

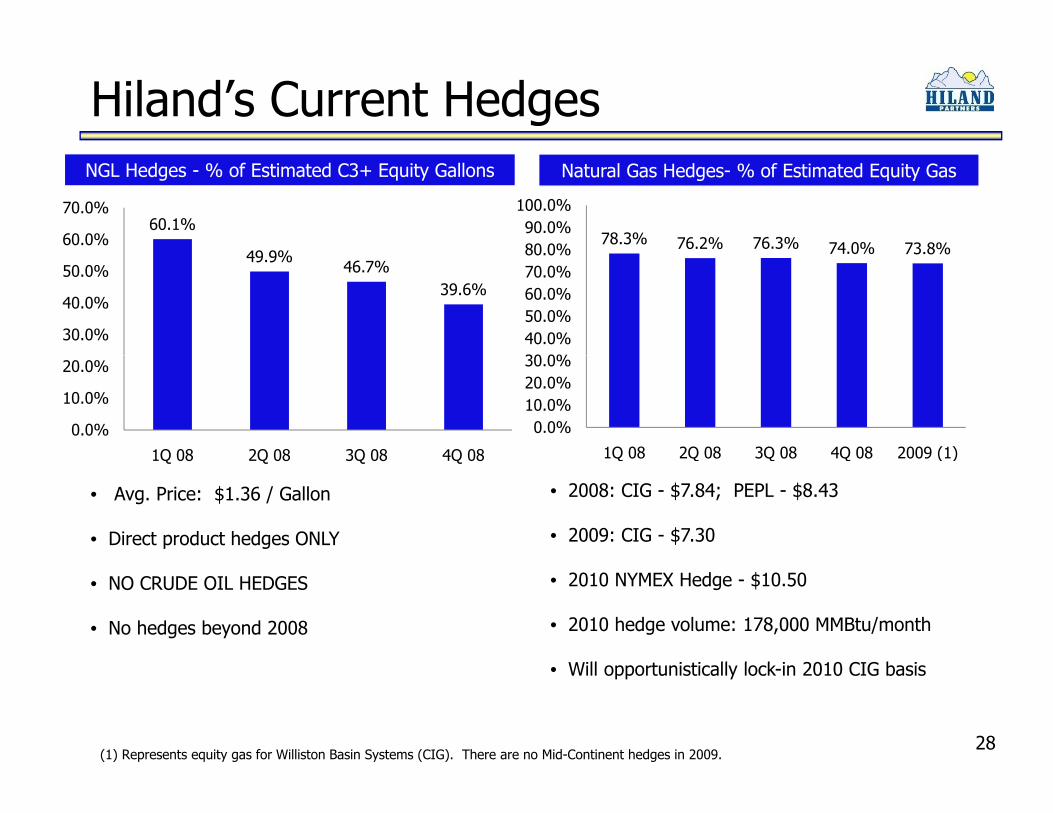

27

Hiland’s Current HedgesNatural Gas Hedges- % of Estimated Equity GasNGL Hedges - % of Estimated C3+ Equity Gallons

78.3% 76.2% 76.3% 74.0% 73.8%80 0%90.0%

100.0%60.1%

49 9%60.0%

70.0%

74.0% 73.8%

30 0%40.0%50.0%60.0%70.0%80.0%49.9%

46.7%39.6%

30.0%

40.0%

50.0%

0.0%10.0%20.0%30.0%

1Q 08 2Q 08 3Q 08 4Q 08 2009 (1)0.0%

10.0%

20.0%

1Q 08 2Q 08 3Q 08 4Q 08

• Avg. Price: $1.36 / Gallon

• Direct product hedges ONLY

• 2008: CIG - $7.84; PEPL - $8.43

• 2009: CIG - $7.30

1Q 08 2Q 08 3Q 08 4Q 08 2009 (1)1Q 08 2Q 08 3Q 08 4Q 08

• NO CRUDE OIL HEDGES

• No hedges beyond 2008

• 2010 NYMEX Hedge - $10.50

• 2010 hedge volume: 178,000 MMBtu/month

Will t i ti ll l k i 2010 CIG b i

28

• Will opportunistically lock-in 2010 CIG basis

(1) Represents equity gas for Williston Basin Systems (CIG). There are no Mid-Continent hedges in 2009.

Financial Flexibility

• HLND had $37.9 million of available capacity under its existing $300 million credit facility at September 30 2008$300 million credit facility at September 30, 2008

• $50 million accordion feature

• Hiland currently has adequate capital resources to fund its announced expansion projects and ongoing system expansionsannounced expansion projects and ongoing system expansions without having to access the debt or equity markets

29

Questions and AnswersQ