hindalco industries ltd board meeting · switch yard esp mahan cpp . utkal refinery 23 erection of...

TRANSCRIPT

Q3 FY12

February 9, 2012

Hindalco Industries Ltd.

Investor Presentation

Financial Highlights

2

Projects Update

Performance Review & Outlook

Presentation Structure

Highlights and Financial

Performance

3

4

Q3 FY12: Highlights

Steady performance despite severe cost pressures

Novelis – Solid Performance in tough quarter, further

impacted by seasonal demand slow down

Aluminium – Robust operational performance in the

face of severe cost inflation

Portfolio strategy depicted its benefits as upstream

businesses witnessed severe margin squeeze

Copper – Strong all-round performance

Financial Performance (Standalone, Q3)

5

` Cr Q3 FY11 Q3 FY12 Change (%)

Net Sales 5,975 6,647 11

PBITDA 801 805 1

PBT 579 551 (5)

PAT 460 451 (2)

EPS (`) 2.41 2.35 (2)

` Cr 9M FY11 9M FY12 Change (%)

Net Sales 17,013 18,950 11

PBITDA 2,483 2,695 9

PBT 1,807 1,958 8

PAT 1,429 1,597 12

EPS (`) 7.47 8.34 12

Performance Review & Outlook

6

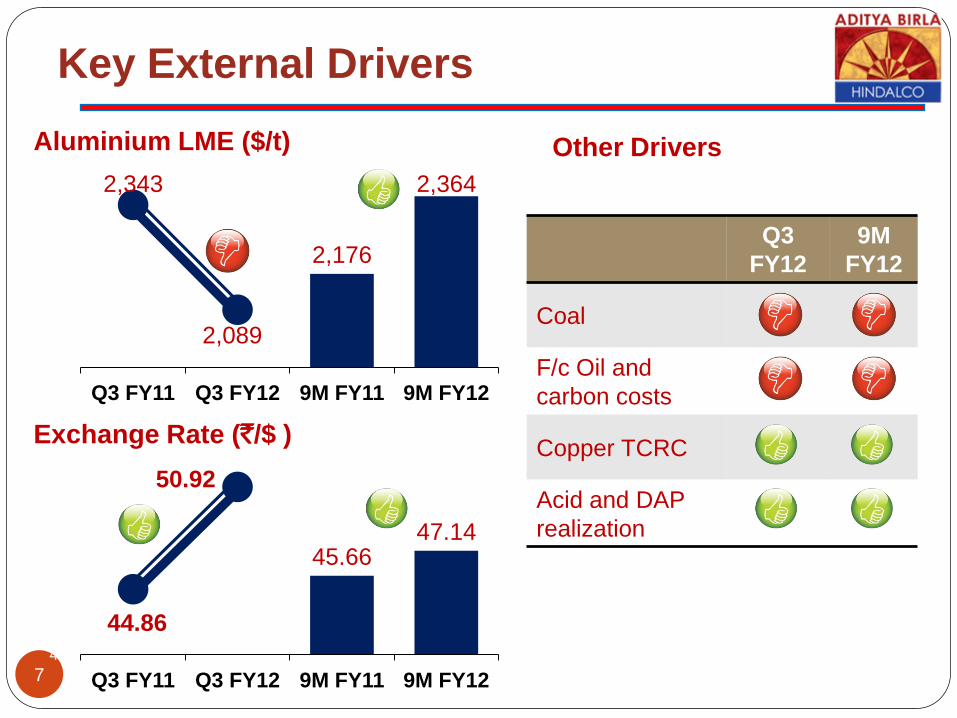

Key External Drivers

7

Aluminium LME ($/t)

2,176

2,364 2,343

2,089

1950

2000

2050

2100

2150

2200

2250

2300

2350

2400

Q3 FY11 Q3 FY12 9M FY11 9M FY12

Exchange Rate (`/$ )

45.66 47.14

44.86

50.92

41 42 43 44 45 46 47 48 49 50 51 52

Q3 FY11 Q3 FY12 9M FY11 9M FY12

Other Drivers

(vis-à-vis year-ago period)

Q3

FY12

9M

FY12

Coal

F/c Oil and

carbon costs

Copper TCRC

Acid and DAP

realization

0

500

1000

1500

2000

2500

3000

3500

4000

0% 50% 100%

8

Tough Phase for the Aluminium Industry

2,026

1500

1700

1900

2100

2300

2500

2700

2900

Ap

r-11

May-1

1

Jun-1

1

Jul-11

Aug-1

1

Sep-1

1

Oct-

11

Nov-1

1

Dec-1

1

LME ($/t)

Macro risks and overhang of stocks have pushed LME below

cost for many smelters Industry Cash Cost Curve ($/t)

Percentage of capacity

Alcoa, Rio Tinto, Hydro, Zalco, Rusal have announced closure of >1

mn ton capacity in recent announcements; more may follow ...

LME @ 2,026

Nearly half production at cash cost

above the Dec-11 LME

(Q4, 2011)

_____________

Source: Industry

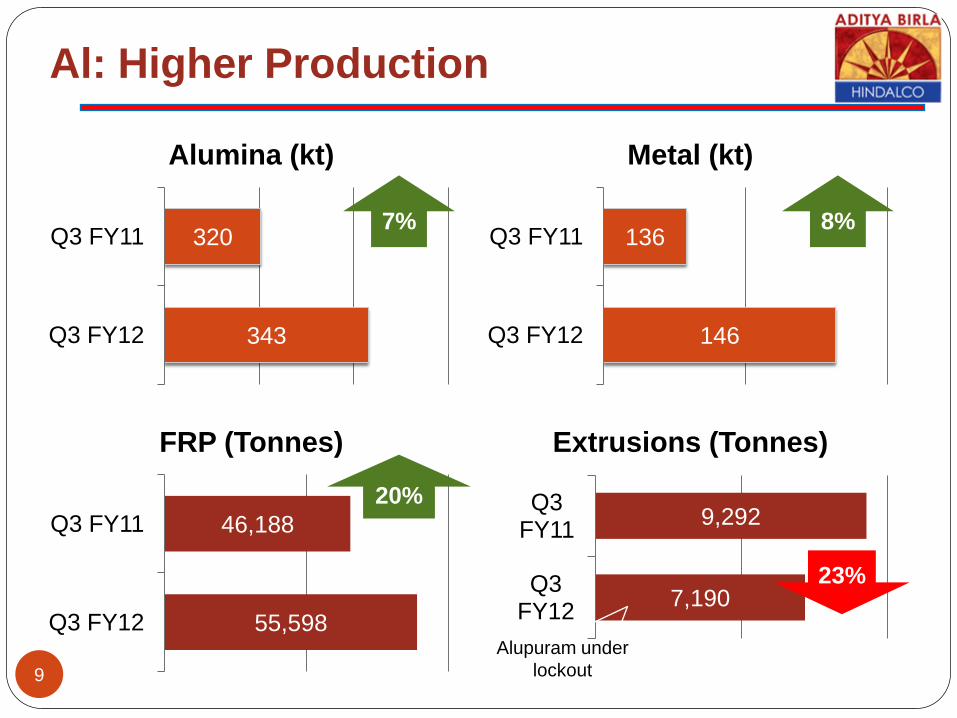

Al: Higher Production

9

343

320

Q3 FY12

Q3 FY11

Alumina (kt)

7%

146

136

Q3 FY12

Q3 FY11

Metal (kt)

8%

55,598

46,188

Q3 FY12

Q3 FY11

FRP (Tonnes)

20%

7,190

9,292

Q3 FY12

Q3 FY11

Extrusions (Tonnes)

23%

Alupuram under

lockout

Al: Sales Performance and Mix

10

9.6

6.8

8.6 7.9

7.0

3.0

0.5

India IIP (%, yoy)

Soft patch in Indian growth

story

But we managed to sell more

metal and more VAP

58

55

87

79

0 100 200

Q3 FY12

Q3 FY11

VAP Others

9% 133 kt

146 kt

Q3 FY11 Q3 FY12

87% 83%

Export Domestic

Resulting in lower domestic

sales

Cost pressures

Soft LME

Adverse mix

Aluminium Financials

11

` Cr 9M FY11 9M FY12 Change (%)

Net

Sales 5,754 6,543 13.7

EBIT 1,441 1,338 (7.2)

` Cr Q3

FY11 Q3

FY12 Change (%)

Net Sales 1,977 2,236 13.1

EBIT 465 310 (33.4)

12

Al. LME: Volatility may continue …

2009 2010 2011 2012 (Proj)

3.3

1.0 0.7 0.5

Al Market Balance (Mn ton) Softer demand and smelter closures

are expected to leave market in a

small surplus in 2012

Dec-end global stocks ~101 days of

consumption (vs. 88 days at end-

Sep)

Financing deals viable so far

Cost curve warrants higher LME for

viability of nearly one-third of

smelters

___________

Source: Industry

While cost curve calls for a higher LME floor, macro

risks may test it from time to time

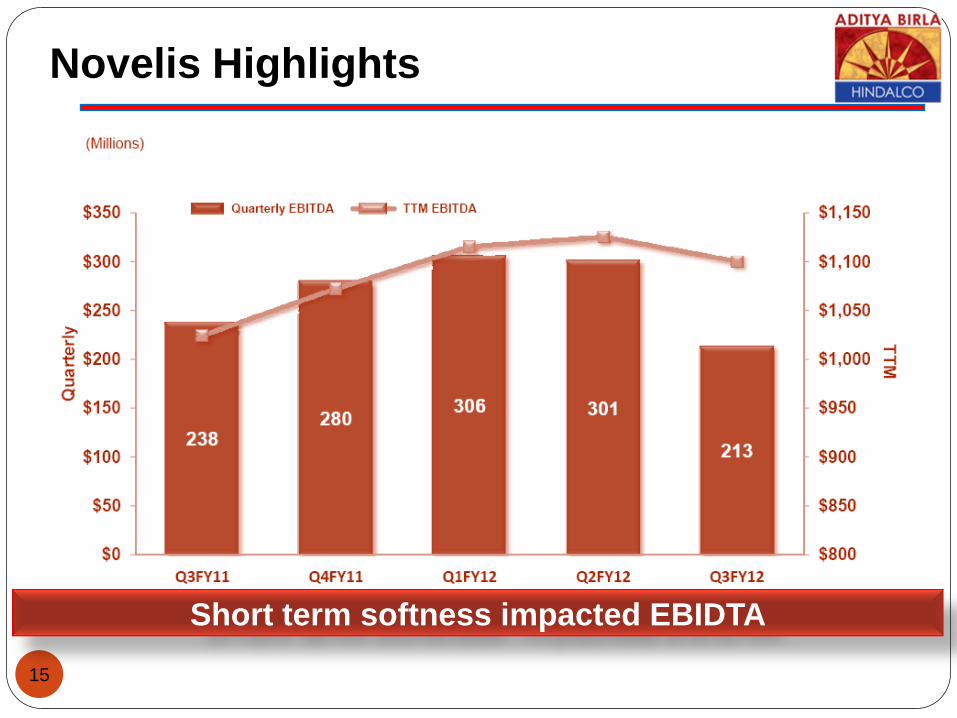

Performance Highlights (Novelis)

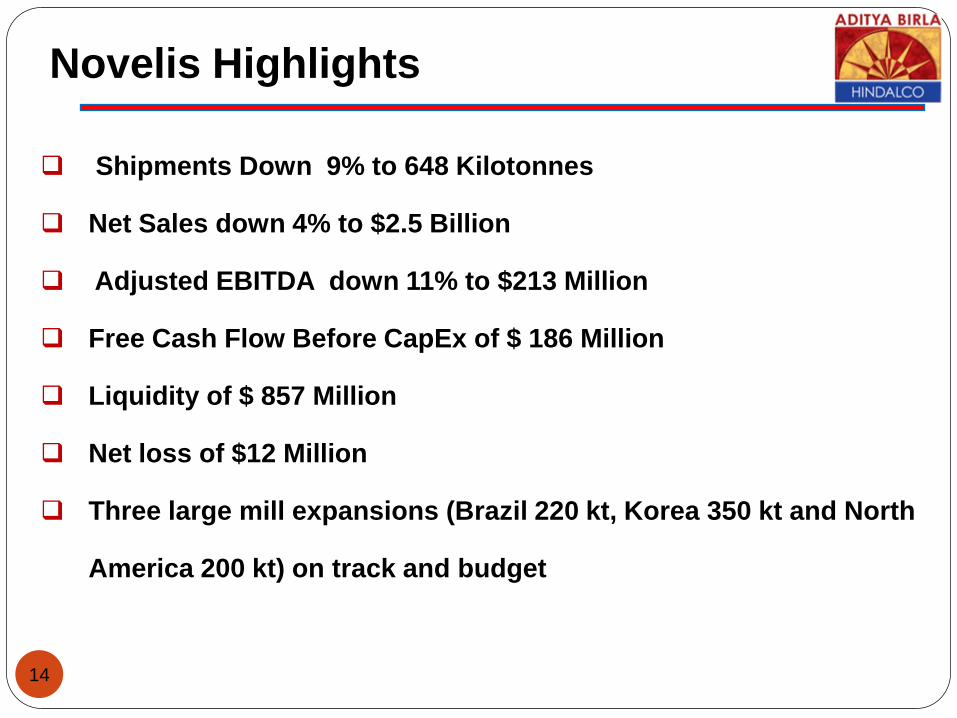

Novelis Highlights

14

Shipments Down 9% to 648 Kilotonnes

Net Sales down 4% to $2.5 Billion

Adjusted EBITDA down 11% to $213 Million

Free Cash Flow Before CapEx of $ 186 Million

Liquidity of $ 857 Million

Net loss of $12 Million

Three large mill expansions (Brazil 220 kt, Korea 350 kt and North

America 200 kt) on track and budget

Novelis Highlights

15

Short term softness impacted EBIDTA

Novelis Highlights – Q3 comparisons

16

Evident Strength of Improved Business Model

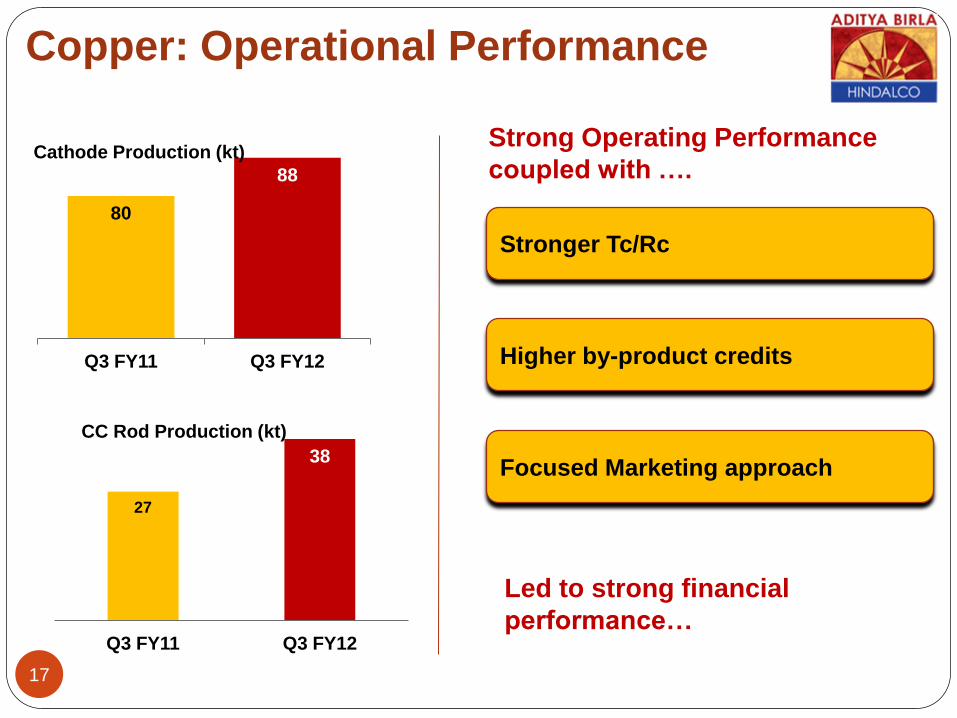

Copper: Operational Performance

Strong Operating Performance

coupled with ….

80

88

Q3 FY11 Q3 FY12

Cathode Production (kt)

17

Stronger Tc/Rc

Higher by-product credits

Focused Marketing approach

27

38

Q3 FY11 Q3 FY12

CC Rod Production (kt)

Led to strong financial

performance…

Copper Financials

18

` Cr 9M FY11 9M FY12 Change (%)

Net Sales 11,265 12,420 10.3

EBIT 396 509 28.4

` Cr Q3 FY11 Q3 FY12 Change (%)

Net Sales 4,000 4,418 10.5

EBIT 143 216 51.1

TCRC, Higher output, better Mix, improved recovery, By product

revenues

Cost Pressures, declining grades

19

ABML Performance

Decline in Nifty Grade (%)

Q3 FY11 Q3 FY12

2.92 2.41

Production subdued

Cu in conc. (Tonnes)

15077 11617

Q3 FY11 Q3 FY12

Nifty Mt Gordon

15,077 15,414

Drop in LME (A$/t)

8,724

7,416

Q3 FY11 Q3 FY12

Challenging times, especially in

the face of cost pressures &

subdued LME

Projects

20

21

Pot Lines Smelter Pot Tending Machine

Cathode Sealing Shop Fume Treatment Center

Mahan Smelter

22

Power Plant View Power House Building

ESP Switch Yard

Mahan CPP

Utkal Refinery

23

Erection of Rod Mill

Power Plant under erection

Digestor and Heat Exchanger

Coal Mill

Aditya Smelter & CPP

24

Pot Room Cathode Sealing Shop

Power Plant Chimney

Power House Building

Other Projects under implementation

25

Project

Hirakud Expansion Brownfield expansion from 161ktpa to 213 ktpa

Hirakud FRP First Can body stock Project in India

Aditya Refinery 1.5 Mn tpa alumina refinery

Jharhand smelter Third fully backwardly integrated smelter in

pipe line

Hirakud FRP facility

Cold Mill Cold Mill Erection

Hot Mill Control Panel Hot Mill

Novelis Projects…

27

Project

Brazil Expansion 220 KT incremental capacity for can body stock

190 KT Recycling line & 100 KT CES coating line

Korea Expansion 350 KT incremental FRP capacity

North America 200 KT incremental capacity to target Auto

segment

Summing Up

28

Macro environment may continue to remain adverse for

the next few quarters

Cost pressures continuing, especially w.r.t. coal and crude-

derivatives

Conversion businesses’ contribution will become critical if

macro risks affect metal prices

Managing projects and their ramp-up to be a key priority

for the coming year

Thank you

29

30

Certain statements in this report may be “forward looking statements”

within the meaning of applicable securities laws and regulations. Actual

results could differ materially from those expressed or implied.

Important factors that could make a difference to the company’s

operations include global and Indian demand supply conditions,

finished goods prices, feed stock availability and prices, cyclical

demand and pricing in the company’s principal markets, changes in

Government regulations, tax regimes, economic developments within

India and the countries within which the company conducts business

and other factors such as litigation and labour negotiations. The

company assume no responsibility to publicly amend, modify or revise

any forward looking statement, on the basis of any subsequent

development, information or events, or otherwise.

Forward Looking & Cautionary Statement

30

Aluminium Production

In Tonnes Q3FY11 Q3FY12 Variance

Alumina

320,310

343,086

7%

Metal

135,829

146,374

8%

FRP

46,188

55,598

20%

Extrusions

9,292

7,190

-23%

Wire Rods

23,672

25,247

7%

31

Copper Production

Strong Operational Performance

Production Units Q3 FY11 Q3 FY12 variance

Copper Cathodes MT 80,224 87,748 9%

CC Rods : Own MT 26,996 38,426 42%

32

Novelis