hints for assignments from chapters 3, 4, 5 and 6 for... · homework hints for assignments from...

TRANSCRIPT

Homework Hints for Assignments from Chapters 3, 4, 5 and 6.Don’t use the hints before working on the questions first.

Assignment For Chapter 3: Exercises 1, 2, 6, 7, 10.

Arbitrage: Transactions intended to take advantage of observed pricing discrepancies, and earn profits with little or no exposure to risk (have arbitrage opportunities diminished due to the issue of the single European currency €?)

· Spatial arbitrageFor a single currency, spatial arbitrage refers to price differences across market locations or dealers.$/€ (NY) $/€ (London) or $/€ (Dealer A) $/€ (Dealer B)· Triangular arbitrageFor three currencies, triangular parity implies: SF/MP = SF/$ x $/MP MP: Mexican PesoImportance of triangular parity for constructing “cross rates”Direct markets in €/£ were observed, but prices constrained by €/£ = €/$ x $/£

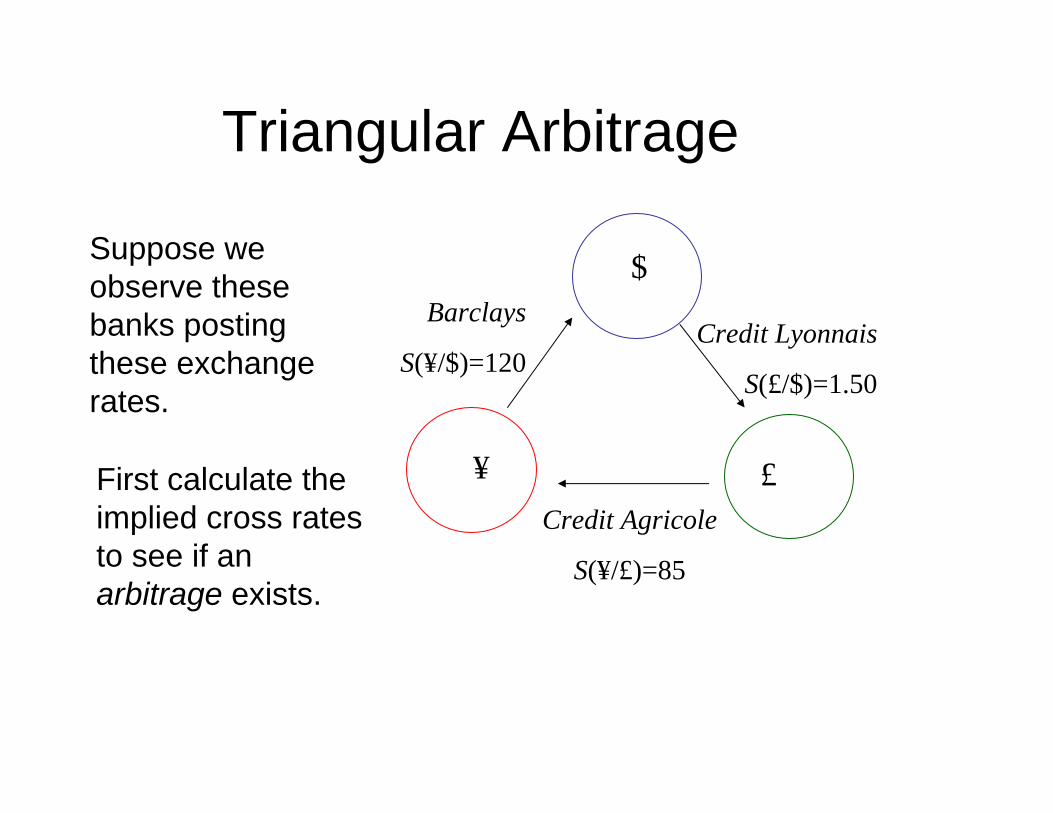

Triangular Arbitrage

$

£¥

Credit Lyonnais

S(£/$)=1.50

Credit Agricole

S(¥/£)=85

Barclays

S(¥/$)=120

Suppose we observe these banks posting these exchange rates.

First calculate the implied cross rates to see if an arbitrage exists.

Triangular Arbitrage

$

£¥

Credit Lyonnais

S(£/$)=1.50

Credit Agricole

S(¥/£)=85

Barclays

S(¥/$)=120

80¥1£

120¥1$

1$50.1£

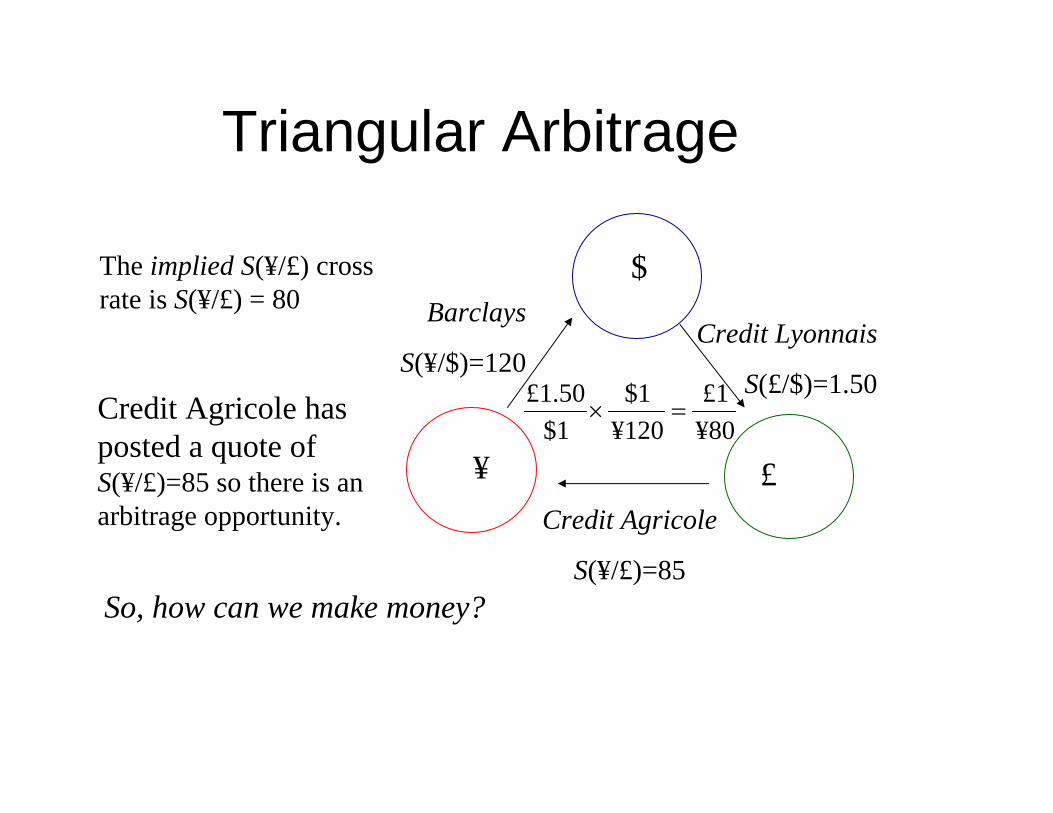

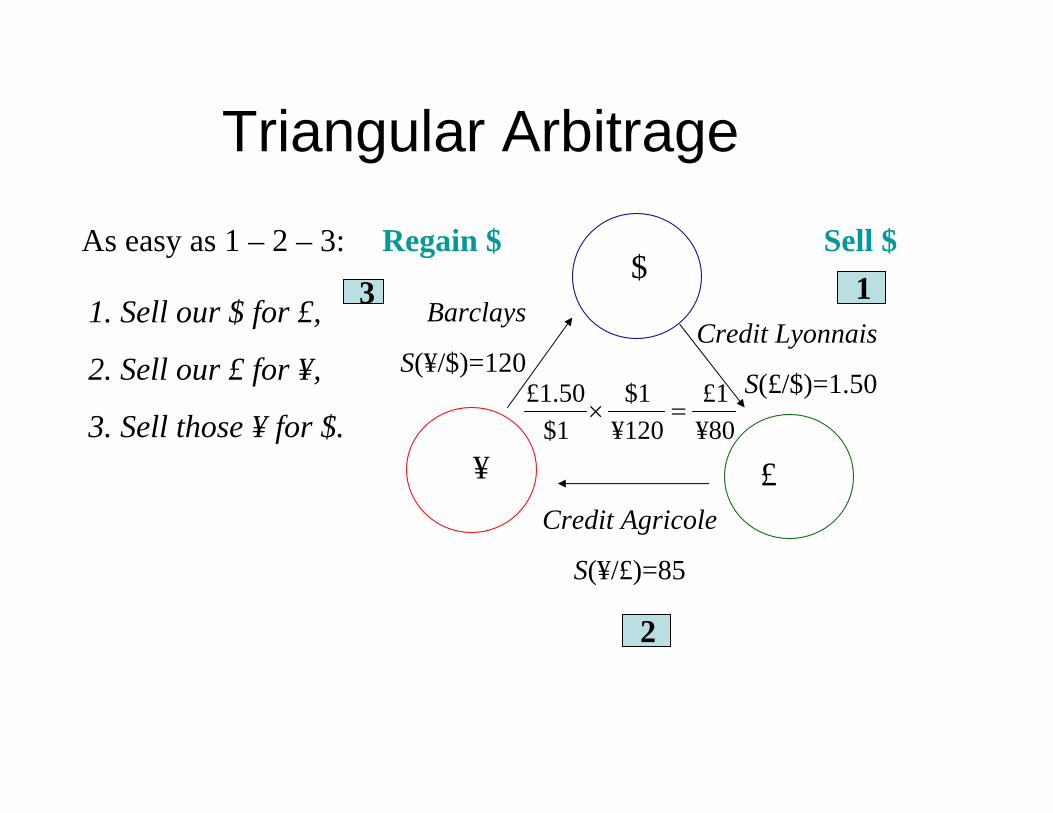

The implied S(¥/£) cross rate is S(¥/£) = 80

Credit Agricole has posted a quote of S(¥/£)=85 so there is an arbitrage opportunity.

So, how can we make money?

Triangular Arbitrage

$

£¥

Credit Lyonnais

S(£/$)=1.50

Credit Agricole

S(¥/£)=85

Barclays

S(¥/$)=120

80¥1£

120¥1$

1$50.1£

As easy as 1 – 2 – 3:

1. Sell our $ for £,

2. Sell our £ for ¥,

3. Sell those ¥ for $.

1

2

3Sell $Regain $

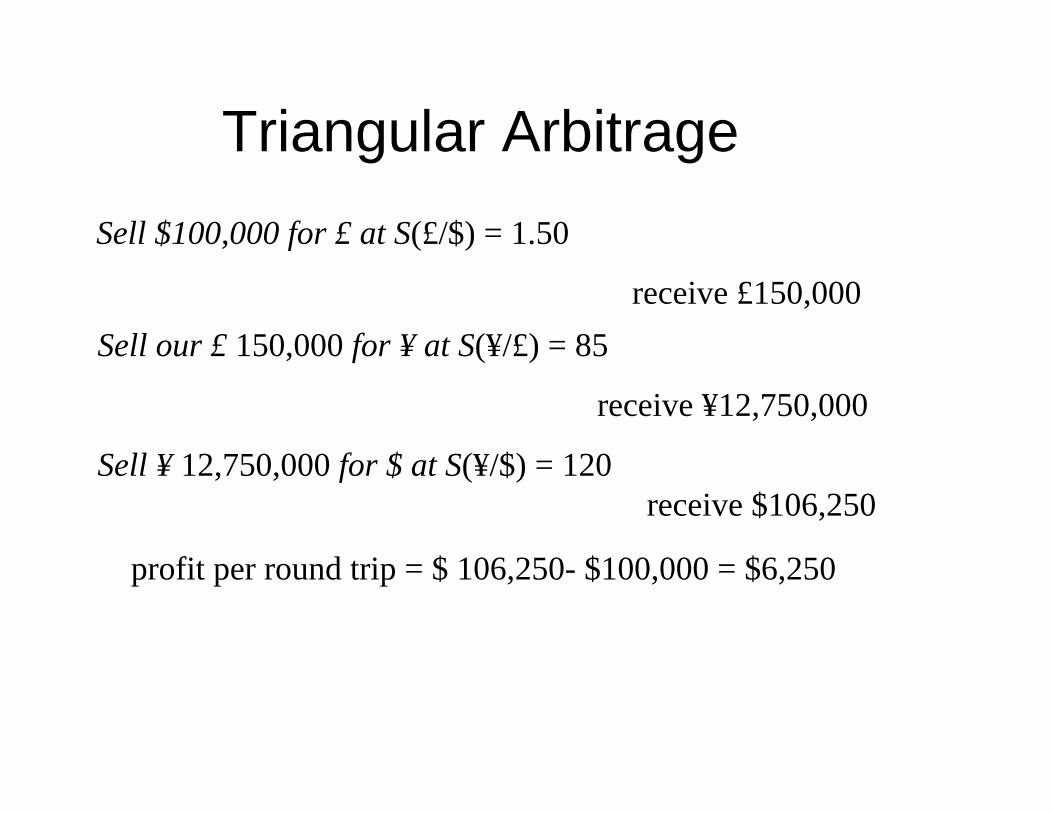

Triangular ArbitrageSell $100,000 for £ at S(£/$) = 1.50

receive £150,000 Sell our £ 150,000 for ¥ at S(¥/£) = 85

receive ¥12,750,000

Sell ¥ 12,750,000 for $ at S(¥/$) = 120receive $106,250

profit per round trip = $ 106,250- $100,000 = $6,250

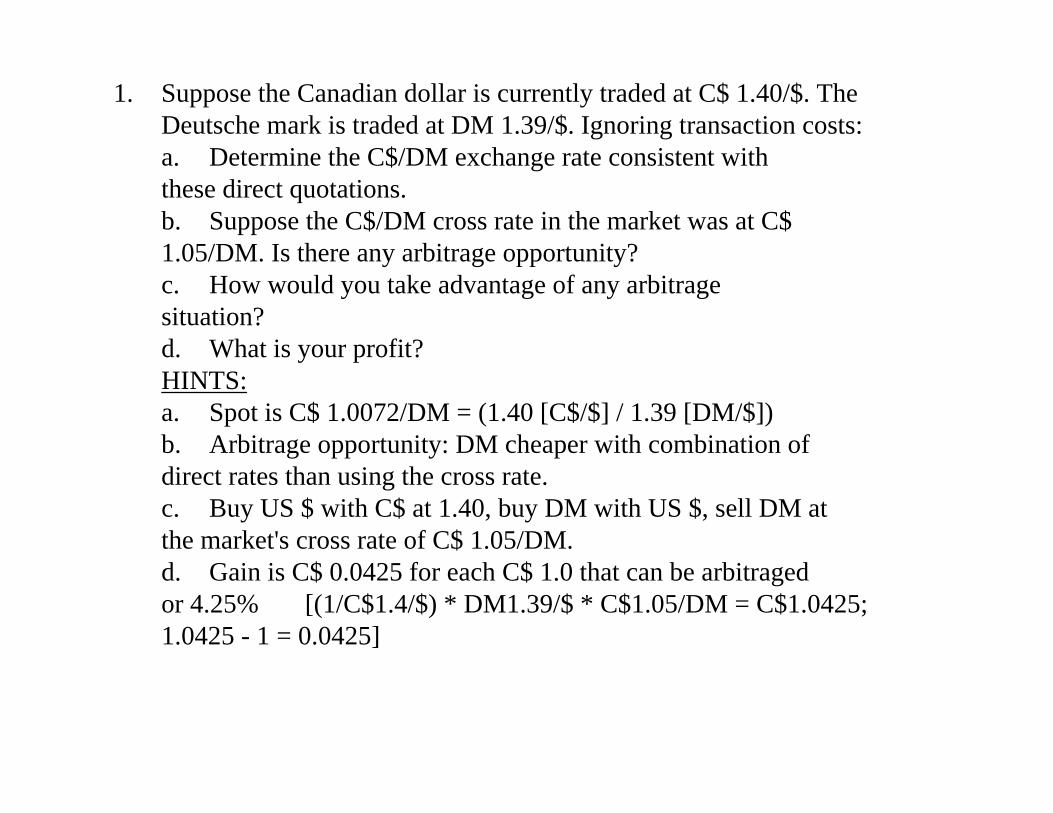

1. Suppose the Canadian dollar is currently traded at C$ 1.40/$. The Deutsche mark is traded at DM 1.39/$. Ignoring transaction costs:a. Determine the C$/DM exchange rate consistent with these direct quotations.b. Suppose the C$/DM cross rate in the market was at C$ 1.05/DM. Is there any arbitrage opportunity?c. How would you take advantage of any arbitrage situation?d. What is your profit?HINTS:a. Spot is C$ 1.0072/DM = (1.40 [C$/$] / 1.39 [DM/$])b. Arbitrage opportunity: DM cheaper with combination of direct rates than using the cross rate. c. Buy US $ with C$ at 1.40, buy DM with US $, sell DM at the market's cross rate of C$ 1.05/DM. d. Gain is C$ 0.0425 for each C$ 1.0 that can be arbitraged or 4.25% [(1/C$1.4/$) * DM1.39/$ * C$1.05/DM = C$1.0425; 1.0425 - 1 = 0.0425]

2. Suppose the Mexican Peso is currently traded at 7 MP/$. The yen is traded at Yen 90/$. a. Determine the MP/Yen cross rate. b. Suppose the MP/Yen cross rate in the market was at

MP 0.1/Yen. Is there any arbitrage opportunity? c. How would you take advantage of any arbitrage

situation?d. What is your profit?HINTS:a. Spot is MP 0.078/Yen = (MP7/$ / Yen90/$)b. Arbitrage opportunity: Yen cheaper using the direct

rates than the cross rate. c. Buy $ with MP, sell $ for Yen, sell Yen at the market's

cross rate of 0.1 MP/Yen.d. Gain is MP 0.2857. [ (1/MP7/$) * Yen90/$ *

MP0.1/Yen = MP1.2857; 1.2857 - 1 = 0.2857]

6. Suppose the spot rate is $ 0.60/DM, i$,6 is 6.5% per annum and iDM,6 is 9% per annum. a. What is your estimate of today's six-month forward $/DM

rate? b. Suppose the six-month forward is quoted at $ 0.60/DM.

What would you do to take advantage of the arbitrage opportunity? Where would you borrow and lend?

HINTS:a. Ft = St * (1 + i$,6/2) / (1 + iDM,6/2) = $0.60/DM * (1 +

.065/2) / (1 + .09/2) = $ 0.5928/DMb. Borrow in US$, buy DM, invest in DM security, sell DM

forward. Profit: ($1 / $0.60/DM) (1 + 0.09/2) * $0.60/DM - $1 * (1 + 0.065/2) = $0.0125; or 1.25% gain on transaction

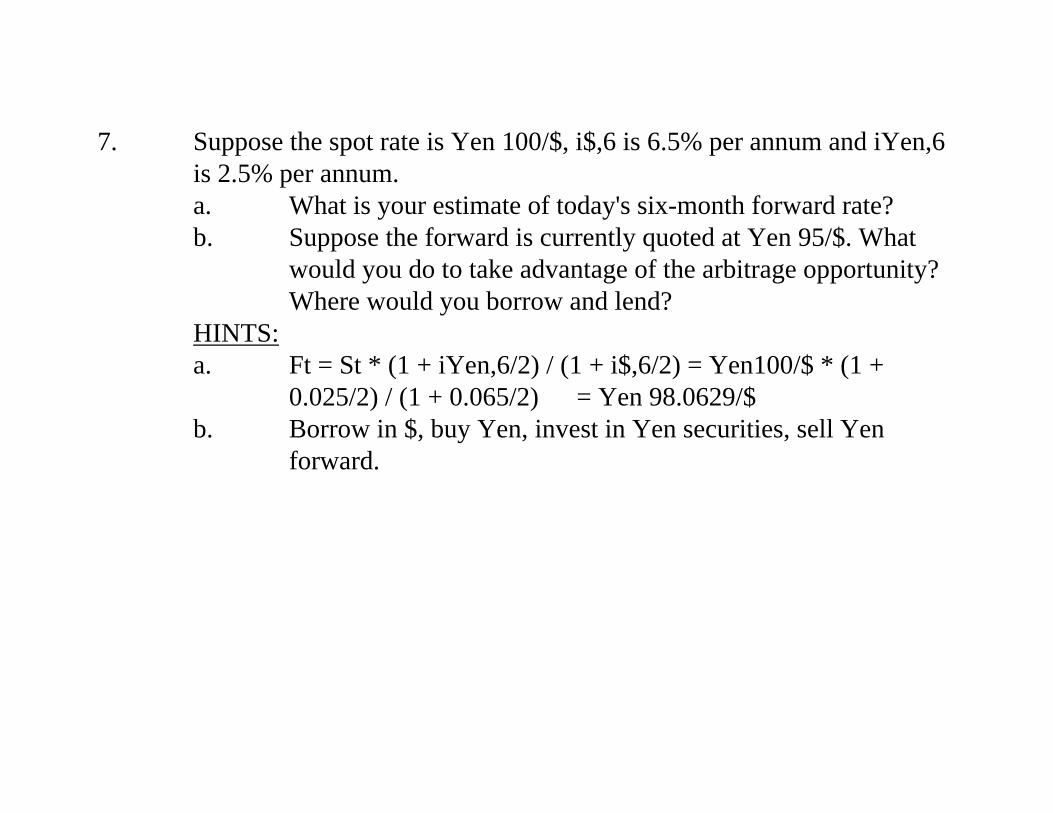

7. Suppose the spot rate is Yen 100/$, i$,6 is 6.5% per annum and iYen,6 is 2.5% per annum. a. What is your estimate of today's six-month forward rate?b. Suppose the forward is currently quoted at Yen 95/$. What

would you do to take advantage of the arbitrage opportunity? Where would you borrow and lend?

HINTS:a. Ft = St * (1 + iYen,6/2) / (1 + i$,6/2) = Yen100/$ * (1 +

0.025/2) / (1 + 0.065/2) = Yen 98.0629/$b. Borrow in $, buy Yen, invest in Yen securities, sell Yen

forward.Profit: $1 * Yen100/$ * (1 + .025/2) / Yen95/$ - $1 * (1 + 0.065/2) = $0.0333; or 3.33% gain on transaction

10. Suppose a German firm wishes to issue commercial paper in DM, but it is unable to do so in the German market. a. What can the firm do to replicate commercial paper (CP)

securities without using German securities? Describe the transactions.

b. Assume that the spot rate is $0.60/DM. The three-month forward rate is $0.58/DM. The three-month US$ CP rate is 8%. At what rate can the German firm expect to issue synthetic DM three-month CP?

HINTS:a. The German firm could borrow in the US$ CP market and

swap its dollar obligation into DM, that is by buying US$ forward to match its future CP payments (principal plus interest) and selling DM forward.

b. The German firm can secure the following rate: 1 + iDM/4 = St/Ft * (1 + i$/4); 1 + iDM/4 = 0.60/0.58 * (1 + .08/4); which implies that iDM = 22.07%

Assignment for Chapter 4 Exercises 5, 6, 7.

Question: How to measure inflation "financially"?

Answer: Yields of TIPS "minus" Yields of regular treasury securities

Note that TIPs are Treasury Inflation Protected Securities. Investors may purchase TIPs at http://www.publicdebt.treas.gov/sec/seciis.htm

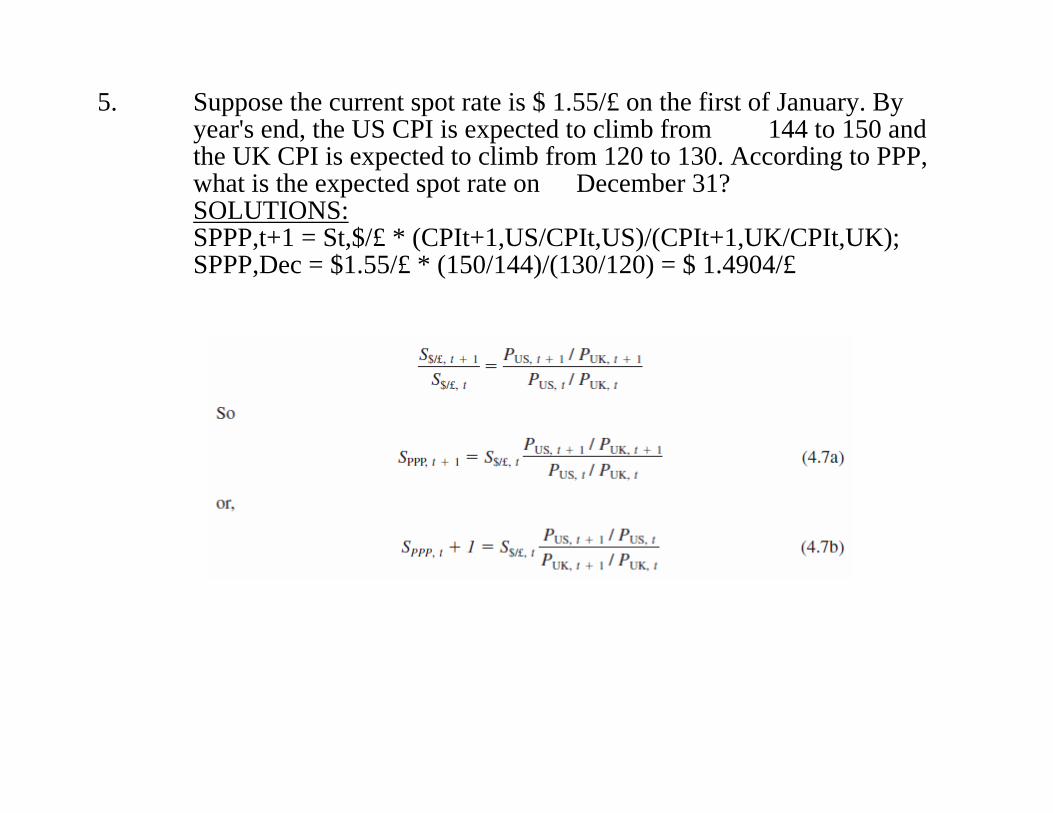

5. Suppose the current spot rate is $ 1.55/£ on the first of January. By year's end, the US CPI is expected to climb from 144 to 150 and the UK CPI is expected to climb from 120 to 130. According to PPP, what is the expected spot rate on December 31? SOLUTIONS:SPPP,t+1 = St,$/£ * (CPIt+1,US/CPIt,US)/(CPIt+1,UK/CPIt,UK);SPPP,Dec = $1.55/£ * (150/144)/(130/120) = $ 1.4904/£

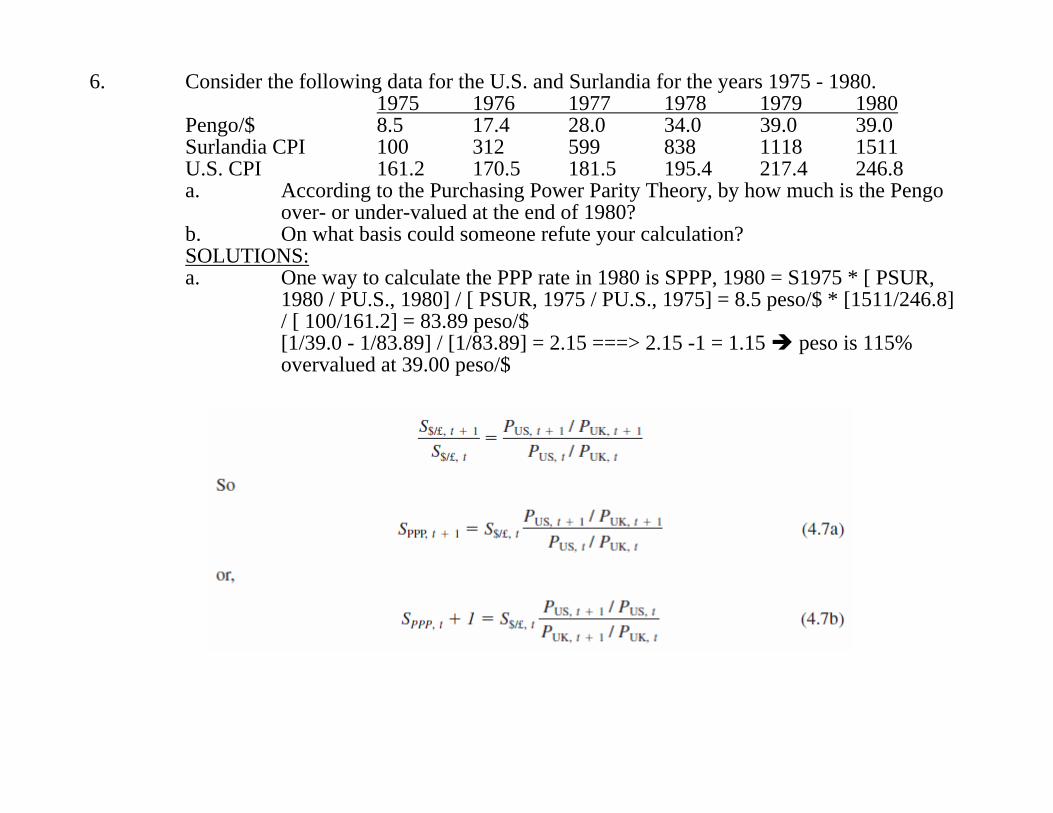

6. Consider the following data for the U.S. and Surlandia for the years 1975 - 1980.1975 1976 1977 1978 1979 1980

Pengo/$ 8.5 17.4 28.0 34.0 39.0 39.0Surlandia CPI 100 312 599 838 1118 1511U.S. CPI 161.2 170.5 181.5 195.4 217.4 246.8a. According to the Purchasing Power Parity Theory, by how much is the Pengo

over- or under-valued at the end of 1980?b. On what basis could someone refute your calculation?SOLUTIONS:a. One way to calculate the PPP rate in 1980 is SPPP, 1980 = S1975 * [ PSUR,

1980 / PU.S., 1980] / [ PSUR, 1975 / PU.S., 1975] = 8.5 peso/$ * [1511/246.8] / [ 100/161.2] = 83.89 peso/$[1/39.0 - 1/83.89] / [1/83.89] = 2.15 ===> 2.15 -1 = 1.15 peso is 115% overvalued at 39.00 peso/$

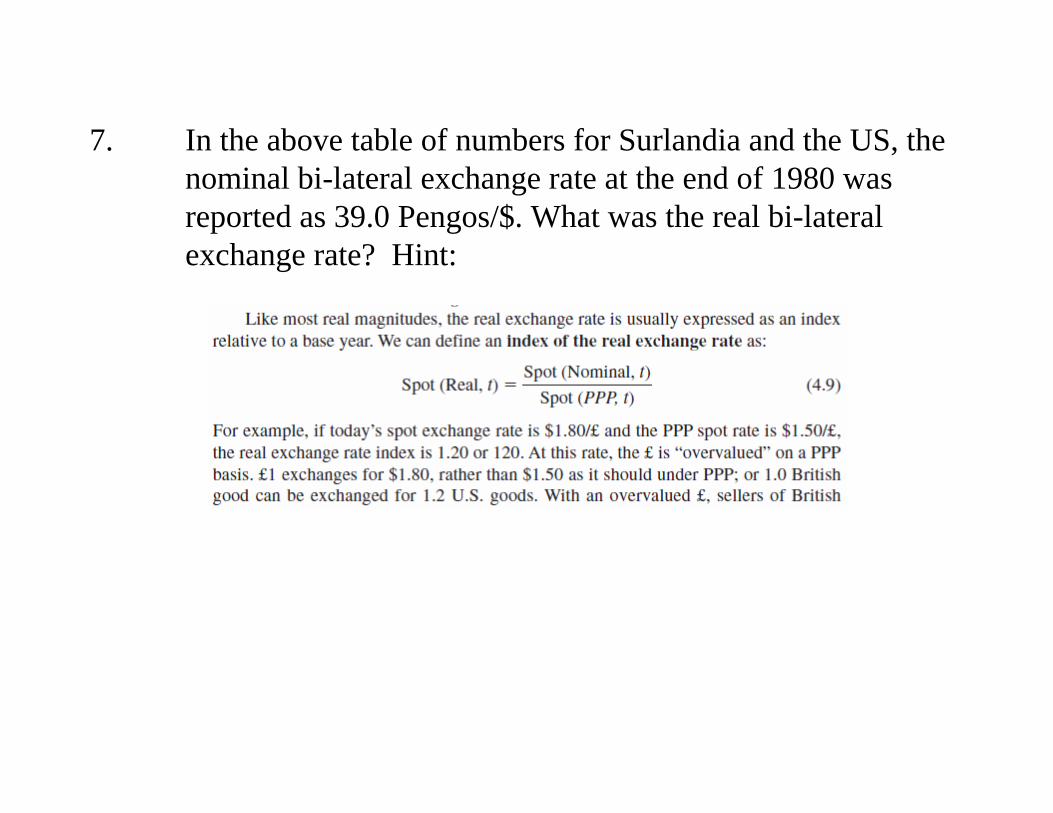

7. In the above table of numbers for Surlandia and the US, the nominal bi-lateral exchange rate at the end of 1980 was reported as 39.0 Pengos/$. What was the real bi-lateral exchange rate? Hint:

Assignment for Chapter 5Exercises 1, 4, 5, 6.

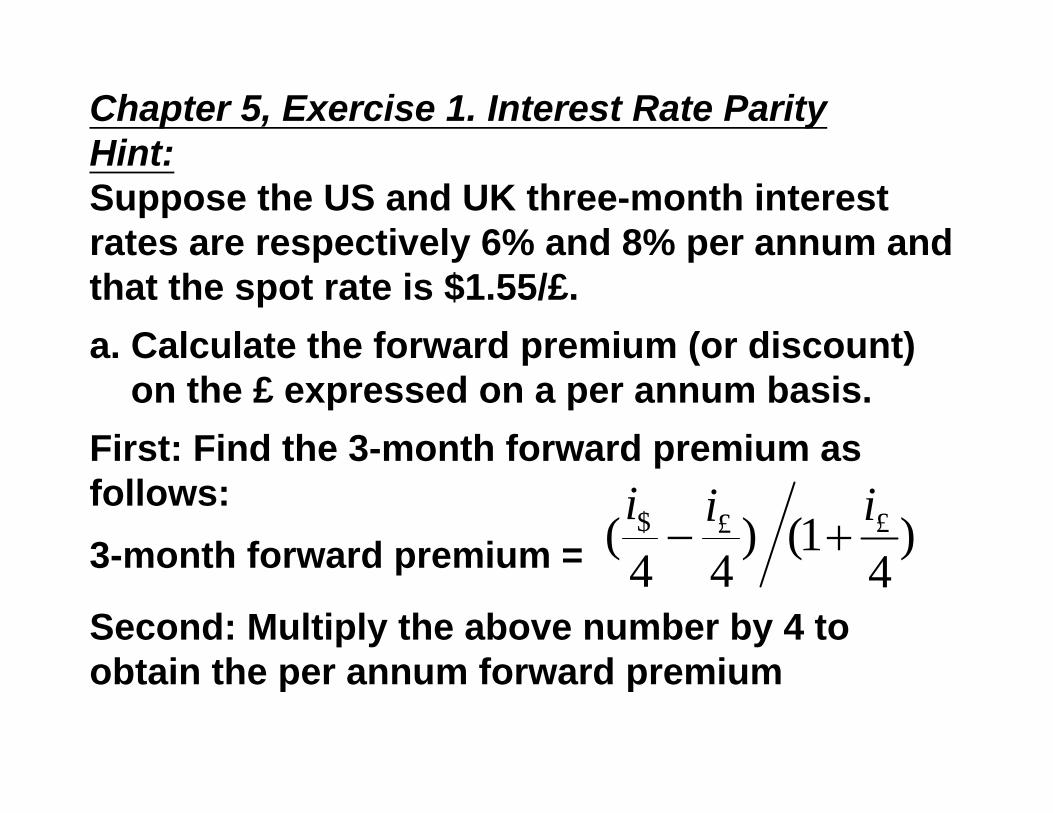

Chapter 5, Exercise 1. Interest Rate ParityHint:Suppose the US and UK three-month interest rates are respectively 6% and 8% per annum and that the spot rate is $1.55/£.a. Calculate the forward premium (or discount)

on the £ expressed on a per annum basis.First: Find the 3-month forward premium as follows:3-month forward premium = )

41()

44( ££$ iii

Second: Multiply the above number by 4 to obtain the per annum forward premium

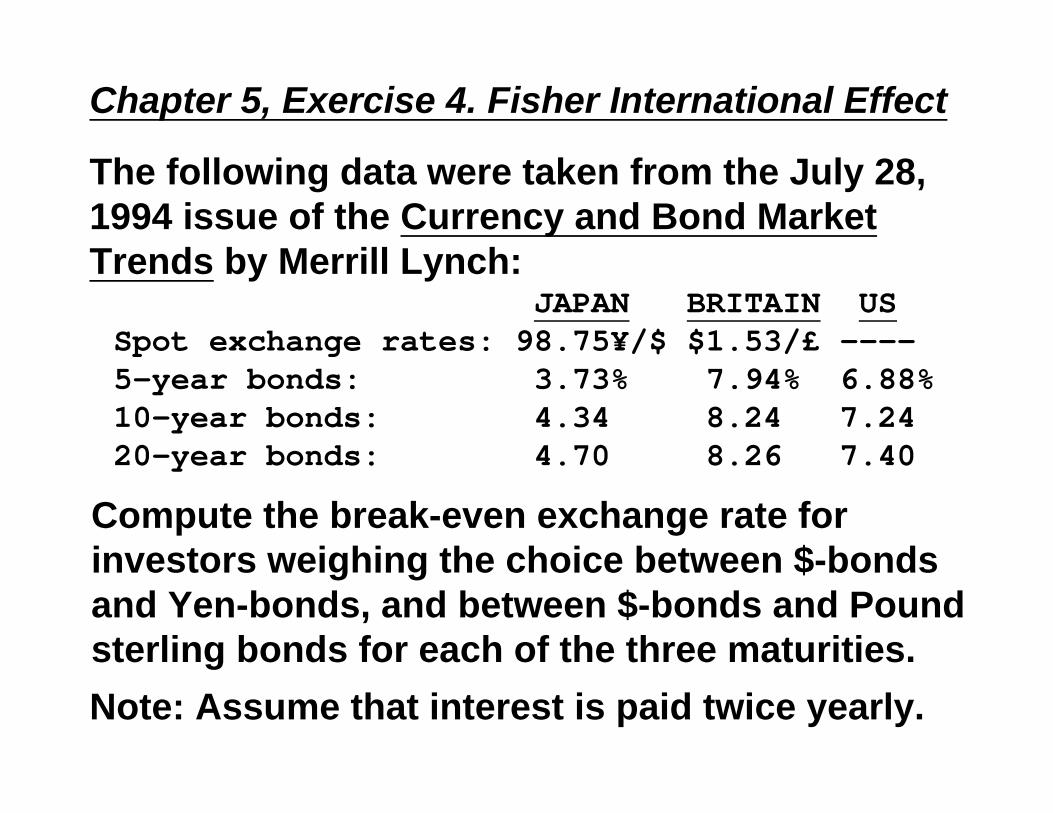

Chapter 5, Exercise 4. Fisher International Effect

The following data were taken from the July 28, 1994 issue of the Currency and Bond Market Trends by Merrill Lynch:

JAPAN BRITAIN USSpot exchange rates: 98.75¥/$ $1.53/£ ----5-year bonds: 3.73% 7.94% 6.88%10-year bonds: 4.34 8.24 7.2420-year bonds: 4.70 8.26 7.40

Compute the break-even exchange rate for investors weighing the choice between $-bonds and Yen-bonds, and between $-bonds and Pound sterling bonds for each of the three maturities. Note: Assume that interest is paid twice yearly.

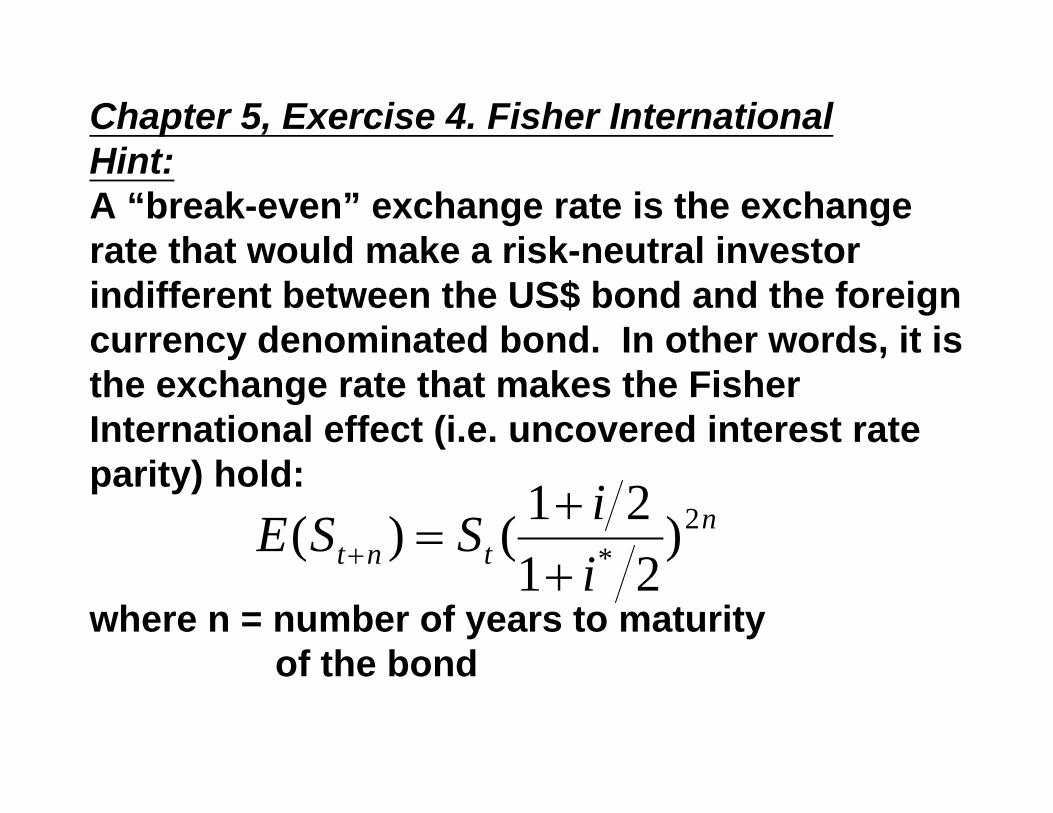

Chapter 5, Exercise 4. Fisher InternationalHint:A “break-even” exchange rate is the exchange rate that would make a risk-neutral investor indifferent between the US$ bond and the foreign currency denominated bond. In other words, it is the exchange rate that makes the Fisher International effect (i.e. uncovered interest rate parity) hold:

ntnt i

iSSE 2* )

2121()(

where n = number of years to maturityof the bond

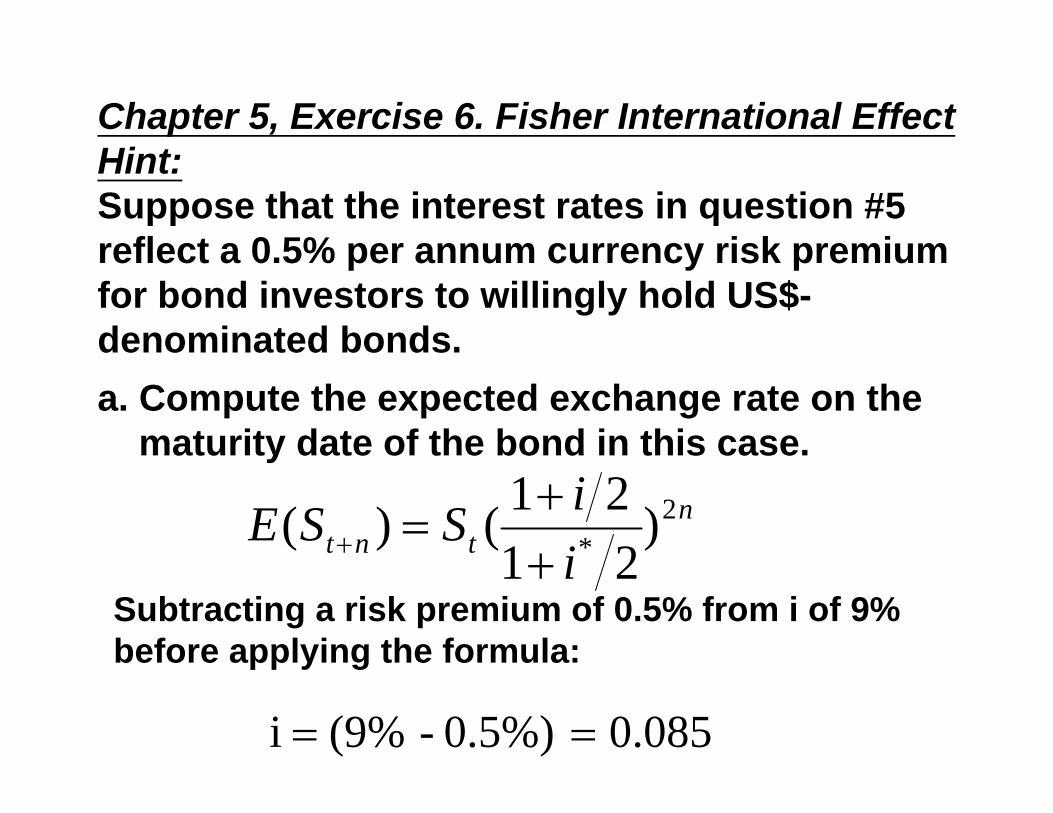

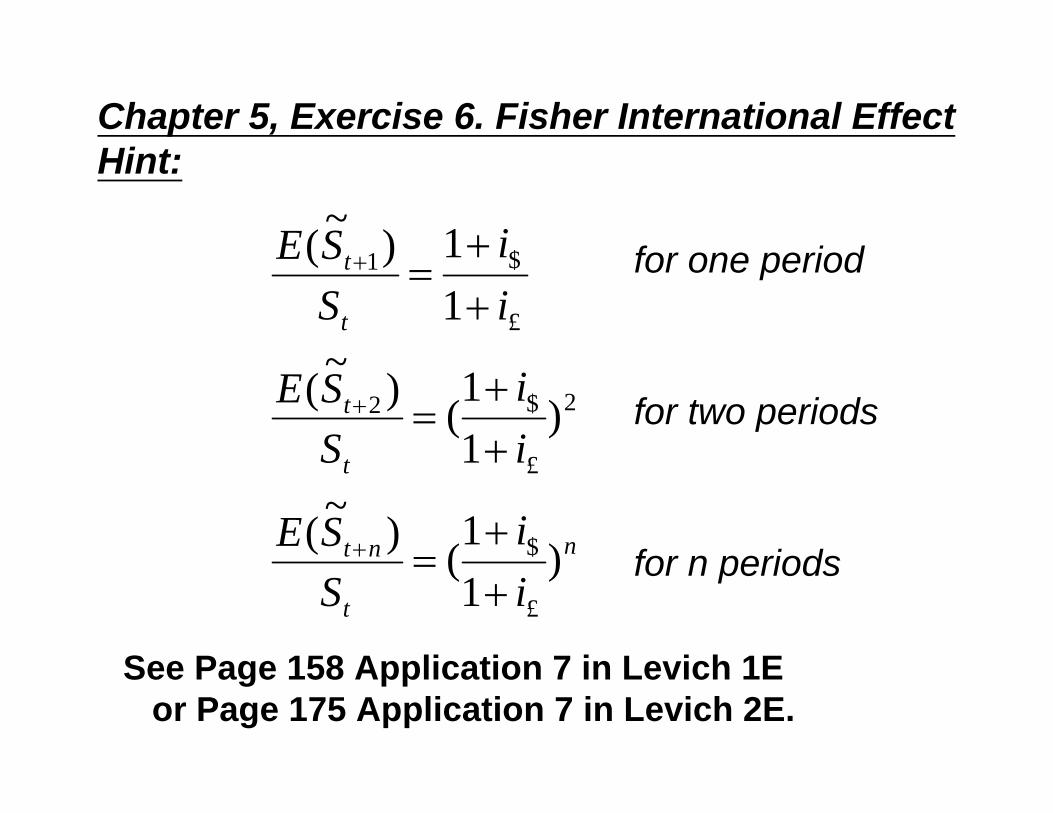

Chapter 5, Exercise 6. Fisher International Effect Hint:Suppose that the interest rates in question #5 reflect a 0.5% per annum currency risk premium for bond investors to willingly hold US$-denominated bonds.a. Compute the expected exchange rate on the

maturity date of the bond in this case.n

tnt iiSSE 2* )

2121()(

Subtracting a risk premium of 0.5% from i of 9% before applying the formula:

0.085 0.5%) - (9% i

£

$1

11)~(

ii

SSE

t

t

for one period

2

£

$2 )11

()~(ii

SSE

t

t

for two periods

n

t

nt

ii

SSE )

11

()~(

£

$

for n periods

See Page 158 Application 7 in Levich 1Eor Page 175 Application 7 in Levich 2E.

Chapter 5, Exercise 6. Fisher International Effect Hint:

Assignment for Chapter 6 Exercises 3, 7, 10, 14.

http://www.mhhe.com/business/finance/levich2e/-or-

http://pages.stern.nyu.edu/~rlevich/links.htmlhttp://pages.stern.nyu.edu/~rlevich/datafile.html

Question #3. "The stock models of foreign exchange pricing sees foreign exchange primarily as a medium of exchange for executing international trade transactions." Is this statement true or false? Explain.

Hint: False. The stock model of foreign exchange pricing views foreign exchange as an asset …

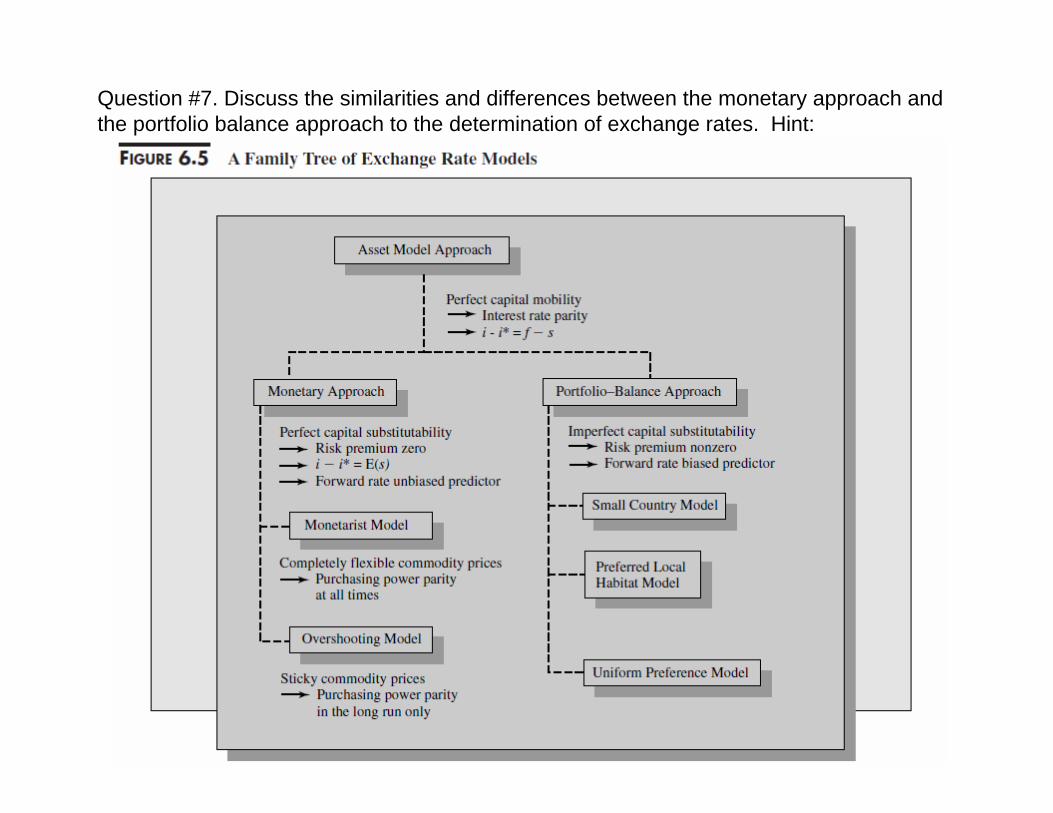

Question #7. Discuss the similarities and differences between the monetary approach and the portfolio balance approach to the determination of exchange rates. Hint:

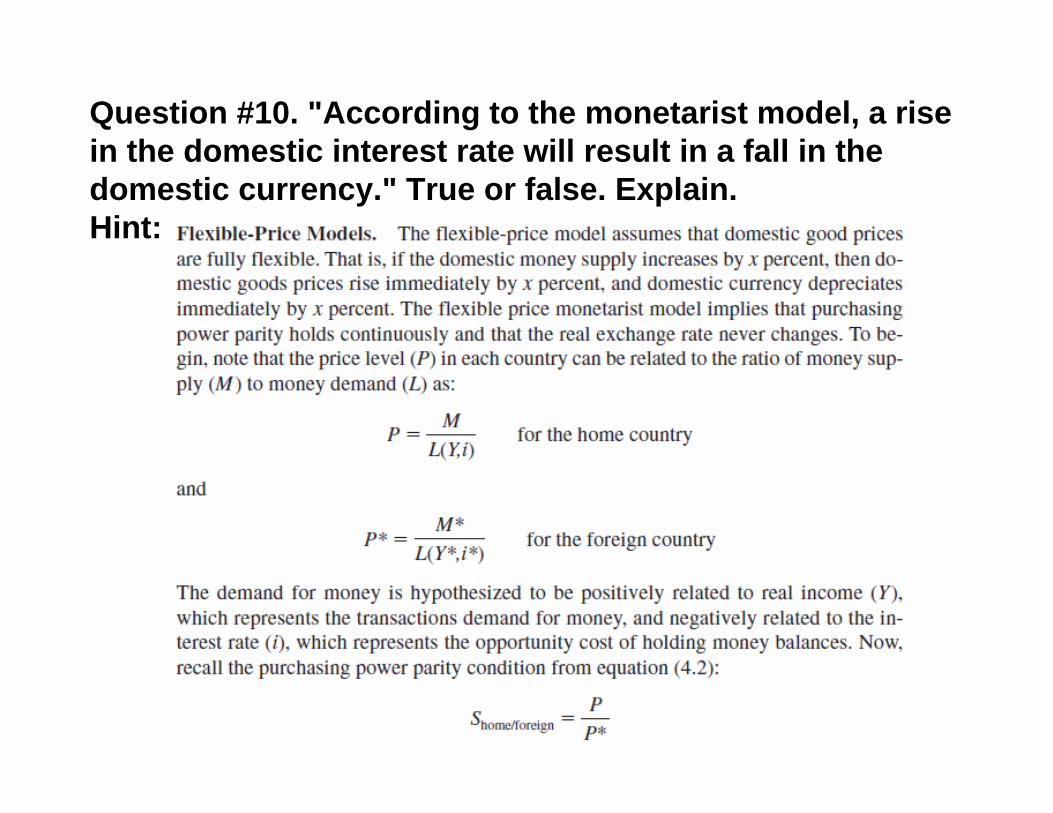

Question #10. "According to the monetarist model, a rise in the domestic interest rate will result in a fall in the domestic currency." True or false. Explain.Hint:

Question 14. Define the term "speculative bubble." Explain how a speculative bubble could develop in the foreign exchange market.Hint: Pages 217-8 of text –or– pages 256-7 of course reader

A speculative bubble is measured by the difference between the present spot rate and the fundamental equilibrium rate.A speculative bubble could develop if traders buy a currency not based on a determination that it is undervalued on the basis on fundamentals, but solely on the basis that the currency is expected to appreciate in tomorrow’s market.If other traders also think and behave so...

¤ Indeed, the Big Mac has had several forecasting successes.

¤ When the euro was launched at the start of 1999, most forecasters predicted that it would rise. But the euro has instead tumbled -exactly as the Big Mac index had signaled. At the start of 1999, euro burgers were much dearer than American ones.

An example of rosy prospect which didn’t realize as expected ...