historic •• downtown laramie

TRANSCRIPT

HISTORIC� DOWNTOWN�

LARAMIE�

RETAIL

MARKET

ANALYSIS

Mareh2007

••••••••••••••••••••••••••••••••••••••••••••�

Dusinetj8 Resource Group, LLC

946 South Ash Street CUSpet', \\'Y

CITY OF LARAMIE (307) 721-52501 P.O. Box C FAX (307) 721-5284

LARAMIE Laramie, WY 82073 TDD (3071 721-5295 [email protected]

June 5, 2007�

Susan Flobeck� Economic Development Program Manager� Wyoming Business Council� 214 West 15th Street� Cheyenne WY, 82002�

Dear Susan,� Enclosed please find the final Retail Market Analysis for Historic Downtown Laramie,� which was prepared by the Business Resource Group, LLC and the final report for this� project.�

Please call or email if you have any questions or concerns.�

Sincerely,�

(-e

Sarah Reese Grants Writer City of Laramie

MAIN STREET� LARAMIE WYOMING

PAGE NUMBEU

••••••••••••••••••••••••••••••••••••••••••••�

• •

•••

•••••

•••••• ••• PROJECT PARTICIPANTS

••Jane Daniels, Executive Director Laramie Main Street Program

•• Board of Directors Laramie Main Street Program

Peter Wysocki, Community Development Director City of Laramie

•••• Downtown Laramie Business Association

••�

Downtown Development Authority�

Laramie Area Chamber of Commerce�

Laramie Economic Development Corporation�

••• Laramie Main Street Design Committee

Laramie Streetscape Committee

•••�University of Wyoming�

Dr. David Hunt & Advanced Marketing Management Students� Dr. Bill Gribb & Downtown Development Area Parking Study Students�

•• University of Wyoming Market & Research Center

•••Wyoming Business Council

Wyoming Community Foundation

•• Wyoming Main Street Program

AmeriCorps *VISTA Volunteers Courtney Stevens, Ellen Smyth, Evan Medley, Diane Mills

1

••�

••••••

•••••••••

•••

••••� CHAPTER I INTRODUCTION

••••••

The National Trust for Historic Preservation, in reaction to economic decline

and threats to traditional commercial architecture, initiated a proactive effort

to revitalize historic downtown commercial areas to address neglected and

threatened commercial architecture. This initiative has since become known

as the Main Street Program. Since the National initiative was launched in

the later 1970's nearly 2,000 communities nationwide have adopted the Main

Street approach to look again to their downtown commercial areas, the heart

of their communities, to revive its commercial core, to strengthen business,

to control community-eroding sprawl, and to keep a sense of place and•••••� community life.

In January 2005 Laramie was selected to be a pilot Main Street community in

Wyoming and created the Laramie Main Street Program (LMSP) to combine

and strengthen the efforts of new and existing downtown organizations. The

mission of the Laramie Main Street Program is to foster the economic and

social vitality of downtown Laramie, while accentuating its unique heritage.

The Laramie Downtown Historic District, listed on the National Register of

Historic Places, is the jewel of Wyoming for its preservation and renovation

of commercial buildings circa 1870 through 1938. The District consists of

ten blocks of the original Union Pacific Railroad plat and is almost

exclusively comprised of two story brick commercial structures. While many

of the buildings reflect a variety of late 19th century commercial trends in

railroad communities, one of the most important is the former Carnegie

Library building.

The City of Laramie is a unique and vibrant community. Wyomingites take

pride in the City as the home of the University of Wyoming and travel

••••� frequently from across the State to alumni and athletic events. Wyoming

Technical Institute (WyoTech) is the largest vocational school in Wyoming,

attracting more than 2,500 students annually. These two educational

institutions provide specialized opportunities to a wide range of young

people and contribute to the overall diversity and focus on advanced learning

that is central to the spirit of the community. Located adjacent to Interstate

80, the City of Laramie draws tourists from around the world attracted to the

City's historic past and western flair. Laramie offers the relaxed, outdoor •••• ••• 2

••••

•••••••

•••Wyoming lifestyle, enhanced by the educational and cultural opportunities

available to the community through the University of Wyoming. ••••• A vibrant downtown is the envy of many communities, large and small,

nationwide as-well-as throughout Wyoming! Even in rural states with small

•••• communities downtowns are often the site of deteriorating or unused

buildings or, in general, do not reflect community pride or economic

viability. The City of Laramie, its residents, business and building owners are

truly fortunate to have this jewel as their downtown and the primary

commercial and retail center of the community.

••• PIU'I)()Se and Scope The Laramie Main Street Program provides economic development•• opportunities within the context of historic preservation of the downtown

commercial district using the national Main Street Program Four-Point

• •••

approach: organization, economic restructuring, design, and promotion. To

address future economic development opportunities, it is first necessary to

understand the current commercial and retail environment within the Laramie

Downtown area and to identify the desires and preferences of the target

audience (consumers; both residents and travelers). FUliher, it is essential for

future planning and development to understand the multi-use capacity and

capability of the Laramie Downtown area, to preserve the unique

characteristics of the area's historic past, and create an inviting and inclusive

community gathering place.

••••• BRG is pleased to offer this Laramie Main Street Market Analysis, following

the guidelines established by the national Main Street Program, as an

assessment of the existing retail and commercial business environment in

Downtown Laramie. Included in this report are recommendations for

consideration as enhancements to the overall market appeal of the Downtown

area.

Organization ofthe Mal'ket Analysis The Laramie Main Street Program Market Analysis is organized into sections•• to enable readers to gain a better sense of the existing business and

community environment in Downtown Laramie, and the potential richness•• that a vibrant downtown contributes to an overall sense of community.

3•••�

••

••

••••••• •••

•••••••�••�•• Chapter Four: Trade Area Analysis

Chapter Five: Consumer Preferences Chapter Six: Market Opportunities•••� Chapter Seven: Observations & Recommendations�

•••�COIllInlulity Pal1:icil)atioll�

Chapter One:� Introduction Chapte.· Two:� Downtown Laramie Building

& Business Survey Chapter Three:� Business Environment

A Market Analysis is a picture, or snap-shot, of the market conditions that

exist at the specific time that the analysis is performed. Business, business

conditions, municipal influences, economic trends are all dynamic influences

which impact market conditions over time. The Main Street Program, while

relatively new to the community, enjoys wide and enthusiastic support from

numerous business organizations, the City of Laramie, the University of•••� Wyoming, and the community at large as represented by the Jist of

participating organizations presented earlier in this document. BRG listened

to business owners in the Study Area, spoke with the City of Laramie

Community Development Director, reviewed previous prepared studies and

plans for the Downtown area, complied and analyzed 112 Laramie

Downtown Building and Business Surveys, and data generated through 103

consumer Intercept Surveys: all contribute to the picture of Laramie

••••�••� Downtown reflected here.

••� StudyAJoea The Study Area is defined as the area of the City of Laramie represented by

the bounders of the Laramie Downtown Development Authority District

••�

(LDDA); a twenty-five (25) block area, commonly referred to as Downtown

Laramie. It is the commercial and retail center of the City of Laramie and

encompasses a large portion of the area listed on the National Register of

Historic Places as the Laramie Commercial Historic District. It is estimated

that the Study Area is the site of approximately 295 business entities

including commercial and retail businesses, County and municipal services,

churches, and nonprofit entities.

4�

•••••••• •••

• ••••••••••••• ••••••••• •••••

••••

5�

•

••••� CIIAPTERII BUILDING & BUSINESS SURVEY

••••••••••••

A comprehensive Building and Business Survey was conducted throughout

the Study Area beginning in late 2006, the aim of which was to gather

information relative to the unique business and building characteristics of the

primary retail and commercial district of the City of Laramie. The

information generated through the survey provides valuable information on

how the business and building owners are contributing to maintaining and

improving the overa] I esthetic of the Downtown Area, a measure of the

current and long term viability of the Downtown retail and commercial area,••• and to broadly define how the needs and desires of the consumer public are

being addressed.

•••Information gathered through the business and building inventory provides a

profile of downtown buildings which can assist in determining existing and

future commercial and multiple-use opportunities within the downtown area,••to define potential improvement or restoration projects to enhance the

historic and commercial appeal, to identify areas of focus for future

••improvement projects, and to create a realistic baseline of knowledge about

the Downtown to create a vision for effective utilization and preservation of

the historic buildings.•• This survey establishes a business and building inventory benchmark for

Downtown Laramie. It is recommended that this same Building and Business•• Survey be conducted every two years to assess changing conditions, and to

expand the data base of distinctive features and characteristics of the

downtown buildings.

••••• Business owners, through their survey participation, provided a "moment-in

time" look at the overall business environment in the Downtown Area,

identified issues which impact business conditions, and their efforts to

address the needs and desires of the local and traveling consumer•• The survey was distributed to businesses in the Study Area in October and

•••November 2006. As a follow-up to those not responding, in January and

February 2007, volunteers visited each the businesses dropping off a survey

form, returning later to pick-up the completed form. Approximately 38%, or

111, of the Downtown businesses responded to the survey.

•• 6••�

·••••••�•••••�•••••••••••••••••••••••••••••••••�

o - Businesses Completing and Returning Survey

7

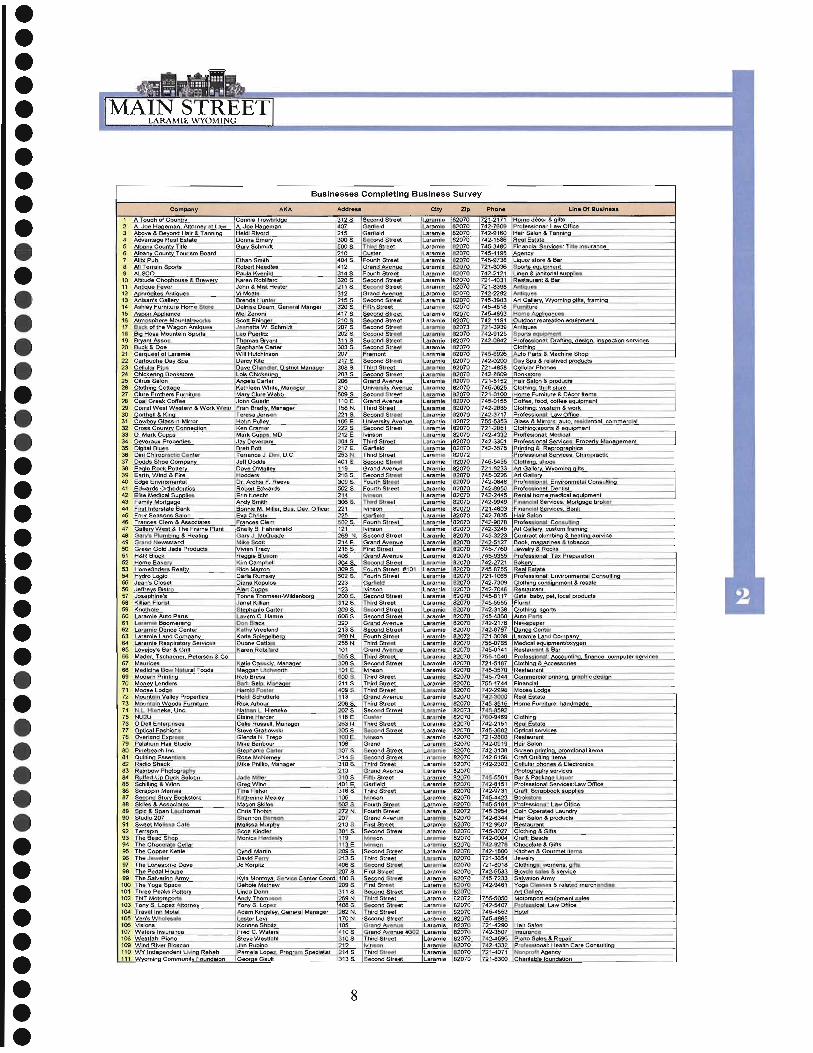

•••••• Businesses Completing Business Survey

Company� AKA Addr... elly line Of Bu.ln...

••••• A Touch of Count Connie Tr ~e

A Joe Hageman Attorney a.L~aYl A. Joe Ha eman� Abov~_BeyondHair & Tanning Heidi Rivard� Advantage Real Estate DonoaEme� Alban Coun-Tit-,.-- Ga Schmidt ~ Coun Tourism Board� ~lbi....f3!b Ethan Smith� All Terrain s~_n, _ Robert Needl_�

9 AlS.£9 P';Gii"""K-;enild� 10 Altitude Chophouso & Brewory Karen Robil~ard

11 Ant" ue Fever John e. Mist HeMer� 12 ~rodit85 Anti ue-. Vi Moats.� 13 Artisan's Galle Brenda...!:::l~~

14 AShiey Furniture Homo StOle Oelnise Deem Ge........1Ma� 15 As n lance�

••••�I. 17� '8� '9� 20� 2,�

••� 22 23 24 25 26 272. John Guerin� 29 (ran Bradl Man� 3<l Teresa Jenso�

Hohn Pu~le

32 Ken Cramer� 33 Mark...Qu~ MD� 34 Ja DevEtf!lux� 35 Brett Bott� 36 Terren<;e J c..1 D.C.� 37 Jeffpodds� 39 Dave O'MaUe� 39 .·i"Cidder;~ Or Arch:e F. Reeve�

3'

Robert EcllNarlh� 42 Enn Knecht� 43 And Smi\h�.. lBonnieM~Miller Bus, De" Omcar� 45 Eva Christ� 46 France~ Clem� 47 SheRy B Fahnllnstid� 48 Gary..L McQuade� 49 Mlko Scott� 50 VrvianTrll� 51 H&R Bloc R ieBhlSom� 52 Home Bakery KirnCampbl!lI� 53 Homefind8f$ Real Rich Marron� 54 ~Iol Ie Carla Rumse� 55 Jean's Croset IDiana Ko oIoa� 56 Jeffre BIslro AI8nG.~

57 _-&!.I!Ebino's Tonna Thomsen-Wildenbor� 58 Killian Florist Janel Killian� 59 ~KnOlhole Sts anle Carter� 60 Laramie Auto Parts LlI'w'ern C. Hamre�

4'

•••••••••••••

61 l.,amlit Boomerang ~BlllGk 62 Loramu! Dance Cenler Kltl:h Vreeland� 63 Laramleland Come!.f:lY. _ Karll!..§.e.Le.:gelber� 64 laramie Res irator Services QUlin", Callie.� 65 Lovo"o 8 Bar & Grill Karen Robillard� 66 ~r Tschacne Peterson & Co.� 67 Maurices atie Cauid Man� 68 MediclneBowN uralFoods M anUt h� 69 "Modern Prmli~ Rob Bross� 70 ~Lend.ers e.rb Selp M.b;;agOl� 71 Moose lod • ~fotIIllII

• 72 Mountsln Valle Pro rtiea HeX1i SchUllcrro� 73 Mounllaln Wood~ Furniture .Rlck&bour� 74~Unc Nathan L Hieneke� 75 NU2U ElaIne Harder�7. Celie Russell Man er� 77 Stove GrabaNll.ki� 76 GfendaN, T,..----o� 79� Mike Banbour 80� 5te aofeCar1Of

Rose McNorne...,Y� 82 ike Phirti Man!Qer� 63� 84� 65� 86� 87� 88� 89� 90� 9'

••• 8'

••• 92 93 The� 94 The� 95 The� 9G The ewelef� 97 The L00~~.Q.QYe 98 The Pedal House� 99 The Salvation ~m

100 The Yoaa 5 ace 101 Three Pe<!.~_E'....ot1ery:� 102 TNT Motors� 103 TonyS Lo..J?£~ltoInO 104 Travel Inn Motel� 105 Ven's Whdn_� 106 Visions� 107 Wat~r5 Insurance� 108 Westfahl Plano109 Wind River Bi~can

, 10 Wy Independent ~ Re ab� 111 W omin Communi! Foundaion�

•••••••� 8�

••••

•••

•• •• •••••

••••

•�••�••�•�

••�•�•�••�••�•�•••�•�

••�•••�

MAIN STREET LARAMIE WYOMING

Downtown Laramie is the primary commercial and retail center of the City

and Albany County. Other retail and commercial properties are clustered in

small strip malls, single site retail locations, or spread along the major traffic

arteries that serve the community. In addition to the numerous attractive and

historic buildings in Downtown, the business climate in the area is supportive

and stable.

It is estimated that the Study Area is the site of approximately 295 business

entities including commercial and retail businesses, County and municipal

services, churches, and nonprofit entities. Approximately 38%, or Ill, of

these Downtown businesses responded to the survey. Not all survey

respondents indicated a response to each question, hence the fluctuation in

number of responses indicated in the following survey analysis.

Survey Question: Date Business Established� Number ofresponses to this question: 94�

The responses to the following survey questions indicates the stability of the

Laramie Downtown businesses and the support the businesses receive from

the consumer community. The national average for longevity of small

businesses indicates that only one out of five new businesses survive more

than three years. The stability and longevity of businesses located in

Downtown is very impressive.

40% 36%=34 Businesses

35% .

en w en 30% en w zt' -z en

25%

::::lC alZ 11. 0 00..

20%

I-~ 15% ~o:: u 0:: 10% w 0..

5%

0% 2000·2006

24"/.=23-Busifiesses.----~---------

-14%=13 Businesses� 11%=10 Businesses�

1999-1990 1989-1980 1979·1970 1969·1960 1959-Prlor

DATE BUSINESS ESTABLISHED

9�

--

- --

-- -- -- --

••••••••�••••�•••�••••••�••••••••••�•••••••••••••�

If it can be assumed that the 94 respondents to the above survey question are

representative of all (295) businesses in Downtown Laramie the following

estimate of business longevity could be applied:

DATE ESTABLISHED ESTIMATED # OF BUSINESSES

2000 - 2006

1999 - 1990

1989 - 1980

1979 - 1970

1969-1960

1959 - Prior

106

71

41

32

18

27

Survey Question: How long has your business been at this location? Number ofresponses to this question: 109

,

25% , ,

o z ,

~ 20% o c.. en w 0::

~ -15% en en w z eniil 10% u. o I

II r

Z

~ 5%0:: w c..

-= 0% ~- -- -- 7I

<1 yr. 1-5 yrs. 6-10 yrs. 11-20 yrs. >20 yrs. YEARS AT THIS LOCATION

25%=27 B-.usmells'e-s23%=25

Bu:ses 20%=22

Businesses

~ 17%=19 Businesses

15%=16 ...Businesses -~

-- -- -- I-~

f--.- 1

A further indicator of the positive business environment which is present in�

Downtown Laramie is the diversity of businesses represented in this�

10�

commercial and retail center of the community. The commercial and retail

mix plus the existing and available residential opportunities in Downtown

offer the services and life style found in many major cities, worldwide. As

the Downtown continues to expand existing businesses, add new businesses,

and the residential oppol1unities become more fully developed, all of the

viable Downtown businesses and the entire community will benefit from the

synergistic atmosphere created.

Survey Question: What type ofbusiness do you have? Number of responses to this question: 111 completed surveys were received. This question received 121 responses due to some businesses indicating a combined retail and service business, or a combined retail and wholesale business.

SURVEY RESPONSES BY BUSINESSS CATEGORY

Other 2%

Professional g%

Note: "Other" category includes: wholesale, nonprofit, religious, fraternal,

and manufacturing entities.

BRG was asked to determine if the businesses responding to the survey by

business category were representative of the business categories for all of the

estimated 295 Downtown Laramie businesses. Following is an analysis based

on the NAICS codes for businesses in the Study Area. An imp0l1ant

distinction between the two charts (above and below) is that the survey

respondents self identified their type of business which may be more

representative of the true nature of the business than the NAICS code

assigned. Therefore, the following graph is considered to be a projection and

••••••••••••••••••••••••••••••••••••••••••••� 11�

MAIN STREET LARAMIE WYOMING

may not truly reflect the entire business population mix within Downtown

Laramie Study Area.

ALL STUDY AREA BUSINESSES BY BUSINESS CATEGORY

Other 6 0/0

Retail 430

/0

•••••••••••••••••••• Professional Estimated Downtown 21% Business Types

Data source: DUIIII & Bradstreet, calculated using survey respolISe percelltages•••••• The Study Area businesses completing the survey further demonstrate the

Downtown Laramie stable business environment through their assessment of

the size of their existing space relative to their requirements, availability of

customer parking, and long terms plans regarding the location, or relocation

of their business.••• Survey Question: Is this space adequate/or your present operation? 107 businesses responded to this question.

Yes: 84%

No: 16%

Survey Question: Do you expect to move/romyour current location? 108 businesses responded to this question.

Within 12 months: 3%

Within 6 months: 0%

Not at aU: 65%

Don't know: 32%

••••••••••••• 12••

MAIN STREET LARAMIE WYOMING

Downtown Pal-king The availability of parking to meet the needs of commercial and retail

businesses, their customers or potential customers within the confines of

downtown area, real or perceived, is a challenge for vibrant downtown

commercial areas everywhere. The City of Laramie is no exception. Parking

studies, traffic flow studies, and city planning resources have been dedicated

over time to address parking in Downtown Laramie. The condition was

summarized best by one of the survey respondents: there is never enough parking in downtown!

The Downtown commercial area offers a mix of on and off-street parking,

estimated as 1750 on-street spaces and 1950 off-street parking spaces, the

majority of which are in designated business parking lots and in public

parking areas. In the central downtown area, diagonal parking provides up to

18 parking spaces per block face. The perceived lack of available parking

might be translated to a lack of parking "in front of the business one intends

to visit."

••••••••••••••••••••••••••••

A recent Parking Study was conducted by Dr. Bill Gribb of the University of

Wyoming and a group of University students (A complete copy of the study

is available at the Main Street Wyoming Office). The Study provides detailed

information regarding the availability and utilization of parking in

Downtown Laramie. According to Dr. Gribb's Study, the weighted average

distance (these) survey respondents had to walk to visit the establishment of

their choice was 121.9 ft. - the equivalent of two building fronts.

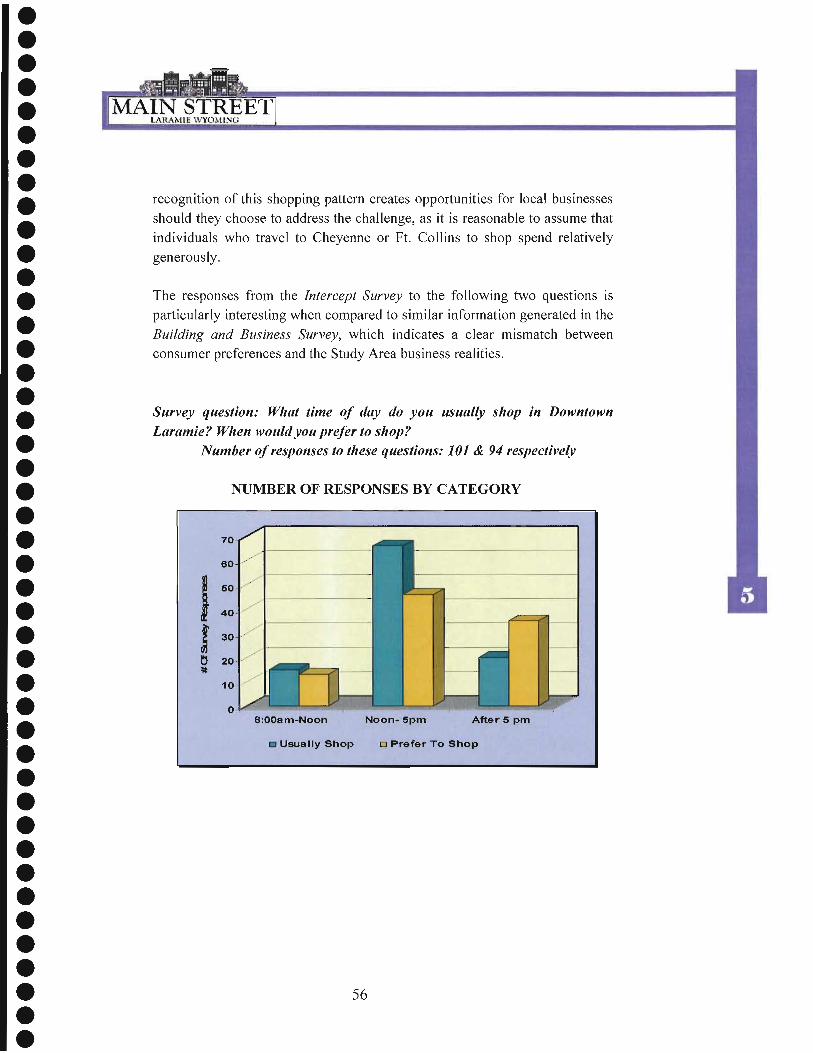

Two questions in the Downtown Building and Business Survey addressed

parking in the Downtown area, both from the business owners and bu iJding

owners' perspective. Parking was also addressed in the consumer Intercept

Survey, discussed in Chapter 5 of this document.

Survey Question: Do you have off-street parking available for your customerslclients?

106 businesses responded to this question. Yes: 42%

No: 58%

13

••••••••••••••••�

••••••

••••••••• Survey Question: Does existing on and of.f-street parking meet the� requirements ofyour husiness?�

99 husinesses responded to this question.�

••� Yes: 69%�

No: 31%�

CustOlner & Client Service Wherever clusters of commercial and retail businesses exist a synergy is

created. If the majority of the businesses in-place are meeting the demands of

the consumer public or a specific target audience; some will thrive, others

will succeed relatively well, and others will be carried along by the most

successful, through the implementation of proven business operating•••� practices. A measure of the viability of a commercial/retail area is not only

the number of customers/clients availing themselves of the products and

services offered, it can be measured by the frequency of consumer visits to

the area, the number of businesses frequented during a visit to the area, and

the number of repeat visits to the same commercial or retail establishment.

Several of the Building and Business Survey questions were designed to

identify consumer traffic patterns, overall viability of the downtown, and to

establish a basel ine from which to measure the success of future programs

designed to stimulate expanded utilization of the downtown by local

residents, visitors, and travelers through southern Wyoming.

••••••••••

•••�

••••••••••• 14

••••• MAIN STREET

• LARAMIE WYOMING

• Survey Question: Estimate the number of customers who enter your store/office each day.

••Number ofbusinesses responding to this question: 97••• ESTIMATED NUMBER OF CUSTOMERS/CLIENTS PER DAY

•• 35 .'.- ..

30! ..

.=Cl I "C 25[c: ...••••~~ -VI 0 20Ql Cl D::,2! - --I VI "' -Ql(,) 15 VI >:gm - .=VI

10 ,.....:::l m 'It 5

• O~ I- t- ~-

•••- 1- -

l-f1-. I-r::b Uncertlan <10 10·20 20·50 50-100 100-200 >200

••Estimated Customers Per Day

•••• • A strong indicator of the overall viability of the Downtown Laramie Area is

that both the commercial and retail businesses indicated a lack of seasonality

of the consumer/shopper utilization. Business owners suggested a relatively

even level of activity throughout the year with the typical retail peaks during

holiday periods, back to school, etc. The summer vacation slump which can

•••• impact retail activity in small or rural communities, is clearly off-set in

Laramie by: an increase in visitors and travelers, an increase in organized

community events designed to increase utilization of the downtown, and

traditional community celebrations which take place entirely or in part in the

Downtown Area. Further, the core population of Laramie, like the population

of most Wyoming towns, appreciates the warm summer weather and if they

are not traveling they are more apt to ride a bike, walk, run or enjoy an

outing in the Downtown Area. •••••••••••�

15�

I

MAIN STREET LARAMIE WYOMING

Survey question: What are your peak business times? Number of responses to this question: 111 completed surveys were received. This question received 133 responses due to some businesses indicating multiple seasons, or all seasons, as their peak time.

NUMBER OF BUSINESSES RESPONDING BY CATEGORY

SPRINGWINTER 2533

ResponsesResponses

•••••••••••••••••••••• FALL 38

Responses

The survey also queried business owners relative to the days of the week and

the hours of the day customer traffic was the highest. The responses are

somewhat atypical of the generally recognized consumer shopping pattern

due to local circumstances. While consumer shopping patterns tend to favor

weekend and evening utilization, in general the Downtown businesses are not

open in the evening, nearly all are closed on Sunday, and Saturday hours of

operation vary widely. The Downtown commercial and retail area represents

the largest shopping district in Laramie and therefore consumers have

adjusted to shopping during the week, most often in the afternoon.

••••••••••••••• Based on the consumer Intercept Survey, discussed in Chapter 5 of this

document, it appears consumers who choose to shop for items not found in

Downtown, local big box stores, or local supermarkets travel out of town to

shop on weekends. Utilization of the Downtown Area on the weekends

(primarily on Saturday) is relatively high due to the popularity of the

restaurants, coffee house, bars, and movie theater. Cultural and athletic•••••••�

events associated with the University of Wyoming also stimulate weekend

utilization of the Downtown establishments. The proposed conference center,

16

currently under construction east of the University, may further stimulate

weekend business activity in the Downtown Area, causing some retail

business to re-evaluate their hours of operation.

Survey question: What are your peak business days ofthe week? Number of responses to this question: 111 completed surveys were received. This question received 142 responses due to some businesses indicating multiple days, or all days, as their peak time.

NUMBER OF BUSINESS RESPONDING BY CATEGORY

Sunday No pattern

7 13 Monday 15

Tuesday 12

Thursday 18

•••••••••••••••••••••••••••••••

Survey question: What are your peak daily business hours? Number of responses to this question: 111 completed surveys were receivelL This question received 65 responses, which may not accurately reflect the busiest times ofday in the Downtown Area.

NUMBER OF BUSINESS RESPONDING BY CATEGORY••••All Day Morning

16 13

•••••••••� 17�

•••• •••••••••••••

••••••• •••••••••••• •••

The businesses located in the Downtown Area enjoy impol1ant consumer

suppol1 from the Laramie community, as is evident from the high number of

customers indicated as being from the community. The businesses also draw

from all of Albany County, as well as from nearby cities. Many have

nationwide loyal customers. The repeat consumer utilization of the

downtown businesses would indicate that they have identified their target

markets well, providing the customers with products and services that meet

their needs/desires.

•••••

The synergy created 111 any commercial/retail business district, as in this

Study Area, benefits all businesses located there. The theory is that if a

customer comes into the business district for a single purpose they may be

tempted, given attractive window displays, special promotions, etc., to visit a

second or third business establishment. Each single business therefore does

not necessarily have to invest in attracting every customer that walks through

the door.

Small retail business owners are by nature independent, risk takers with a

clear concept of how to operate their business successfully. Hours of

operation are a sensitive and critical topic for most small retail business

owners, as each makes his/her related decision based on level of staffing,

cost factors, knowledge of their customer base, and their own personal

considerations.

Survey Question: What are your hours ofoperation? The data generated in response to this question follows on the next two

pages. The tabulated information is astonishing! The 106 businesses

responding to this question indicate approximately 43 different hours of

operation on weekdays (Monday through Friday), the variables increase for

hours of operation on Saturday, and virtually none of the retail businesses are

open on Sunday. The professional services and the food/beverage

establishments indicate a more consistent pattern for hours of operation

throughout the week.

Hours of operation of the Downtown Laram ie businesses was also addressed

in the Consumer Intercept Survey analysis in Chapter 5. Consumers were

queried as to what days and during which times they preferred to shop.

Business owners in the Downtown Area may find the information presented

18

••••

•••••• •

••• ••••

••in Chapter 5 helpful in determining future hours of operation and days of the

week it would be most profitable to be open.

•••••• It is important to recognize that many of the retail businesses in Downtown

Laramie are owner operated, which allows them to provide personal attention

•••••

to their clientele. Everyone needs personal time to maintain the balance in

their life. The illustration of the scope of business hours of operation is

presented to perhaps allow the Downtown Area businesses to, over time,

collectively develop more uniform hours of operation, rather than necessarily

to encourage them to increase hours of operation.

It is recommended when viewing the responses to this question to have an

appreciation that this information is included to illustrate a trend, rather than

to call attention to each of the unique line items.

•••••••

••••••� 19�

•••••

--------

--- -

--

----------

•�•••�•••DOWNTOWN LARAMIE BUSINESS HOURS OF OPERATION••

Sunday Monday Tuesday Wednesday Closed 72 Closed 4 Closed 0 Closed O. ?:00am-11 :OOpm 1 ~..:.Qpam-11 :OOpm__ 6:00am-11 :OOpm 1 6:00am-11 :OOpm 1••

~ •• 6:30am-10:00pm 1 6:00am-6:00pm 1 6:00am-6:00pm 1 6:00am-6:00pm 1

8:00am-3:00pm 1 6:30am-1 O~OOpm 1 6:~.oam-1 0:00pm 1 6:30am-10:00pm 1I --

••8:00am--6:00pm 1 7:30am-4:30pm 2 7:00am-2:30am 1 -iOOam-2:36am- 1 8:00a - 9:00 pm 1 7:30am-5:30pm 1 7:30am-4:39pm 2 7:30am-4:~9pm 2 1-6:00am-5:00pm 2 7:30am-6:00pm 1 7:30am-5:30pm 1 7:30am-5:30pm 1 10:00am-7:00pm 1 8:00am-12:00pm 1 7:30am-6:00pm 1 7:30am-6:00pm 1 10:00am-6:00pm 1 ~~oam-2:0Q.~ 8:00am-12:00pm 1 ~~00am-12:00pm 1•• 10:00-midnght 2 8:00am-4:30pm 1 8:00am-2:00pm 1 8:00am-2:00pm 1 ~_1 :00am-4:00pm 1 8:00am-5:00pm 17 8:00am-4:30pm 1 8:00am-4:30pm 1 11 :00am-6:00pm 1 8:00am-5~_Qpm 2 8:00am-5:00pm 17 8:00am-5:00pm 17

. 11 :00am-2:00am 1 8:00am-6:00pm 1 8:00am-5:30pm 2 -8:00am-5:30p;n- '2 , 12:00-4:00pm I 10 8:00am-7:00pm 4 8:00am-6:00pm 1 }:OOa.!!1~§_:gQP_I11_ 1•••••

I~ ---_. ,12:00-5:00pm 3 8:00am-8:00pm 2 8:00am~ '7jlOpm 4 8:00am-9:00pm 2 1:00pm-5:00pm I 1 8:00 am-9:00pm 1 8:00am-8:00pm 2 8:00am-7:00pm 4

I!:QOpm-6:00am 1 8:00am-2:30am 1 _~00am-9:00pm 2 IOOam-8:00pm 2 24 hr/day 1 8:00 to whenever 1 8:00 to whenever 1 8:00 to whenever 1 -----_ ... ----- ----- - --.-------~ f--

102 8:30am-5:00pm 2 8:30am-?:_Q..°P~ 1 8:30am-5:00pm 2

••• -

8:30am-5:30pm 1 8:30am5:30pm 2 8:30am-5:30pm 2 9:00am-5:00pm 9 _~9.0am-5:00pm 7 9:00am-5:00pm 81

-

9:00am-5:30pm 4 9:00am-5:30pm 4 9:00am-5:30pm 41 9:00am-6:00pm 4 9:00am-6:00pm 4 .Q:_QOam-6:00pm 4i 9:06am-7:00pm 2 9:00am-7:00pm 2 9:00am-7:00pm 2, 9:00am-8:00pm rz 9:00 am-8:00pm 2 9:00am-8:00pm 1 9:30am-6:00pm 2 9:00a m-8:30pm 1 ~~~~~~:.9..Qpm _ 1 9:30am-5:00pm 1 9:30am-5:00pm 1 9:30am-5:30pm 2 9:30am-5:30pm 1 9:30am-6:00pm 2 9:30am-6:00em 2 10:00am-6:00pm 17 9:30am-5:30pm ,10:00am-5:09pm 2~ 1--:10:00am-5:00pm 2 1O:CfOam-5:00pm 2 10:00am-5:30pm 3 .!.O_:Q9~~~5:30pm 2 10:00a~~:3~m 3 10:00am-6:00pm 18

•••••~---

10:00am-7:00pm 2 10:00am-6:00pm 18 10:00am-7:00pm 2 I 10:00am-2:00am 1 10:00am-7:00pm 2 10:00am-2:00am 1 I 11 :00am-1 0:00pm 10:00am-2:00am 1 10:30am-5:00pm 1 I 11 :OOam-~:OQp"2...... 3 -.,0:30am-5:00pm 1 1-1 :00am:9:00pm 2

11 :00am-6:00pm 2 11 :00am-7:00pm 11 :00?m-1 0:00pm 1~

•••1:00pm-1 0:00pm 1 11 :00am-9:00pm 2 11 :00am-5:00pm 1 11 :00am-2:00am 1 11 :00am-10:00pm 1 11 :00am-6:00pm 2 3:00pm-9:-30pm 1 11 :00am-5:00pm 1 11 :00am-2:00am 1 24 hr/day 1 I 11 :00am-6_:QQ£..~ 2 1:00pm-9:00pm 1 .§y Appointment 1 11 :00am-2:00am 1 3:00pm-6:00pm 1

•• ~

,

-1--

••1106 1:00pm-9:00pm 1 3:00pm-9:00pm 1 I

_~~hr/day 1 ~4hr/day~_ 1 I I 1- By Appointment 1 By Appointment 1

I I I 106 106

•• Continued, next page

20�

-----

•••• MAIN STREET LARAMIE WYOMING••••• DOWNTOWN LARAMIE BUSINESS HOURS OF OPERATION

... CONTINUED•• Thursday I Friday Saturday Closed 0 Closed 0 ,Closed _ 27 6:00am-11 :OOpm 1 6:00am-11 :OOpm 1 ,6:00am-11 :O_Qp~ 1 60gam-6:QOpm 1 6:00am-6:00pm 1 6:00am -6:00pm 1•

I

•••••

6:30am-10:Q~~ .§.:-~Q_am -1 0:00pm 1 6:30am-10:00pm 1 7:00am-2:30am 1 7 :OOam -2:30am 1 7:00am-2:30am 1 7:30am-4:30pm 2 7:30am -4:30pm 2 7:30am-2:00pm 1 ' -7:30am-5:30pm~ 7:30am-5:30pm 1 8:00am-12_:QQE~ 1 730am-6:00pm 1 7:30am -6:00pm 1 8:00am-3:00 m 1 8:00am-12:00pm 1 -?:OOam -12:00pm 1 8:0Dam-=5:00pm 1 l~m-4:30pm 1 8:00am-2:00pm 1 8:00am-7:00pm 8:00am -5:00e.-m 8:00am-4:30pm -~1

_~:_QOam-8:00pm 1•h

~ I 8:00am-5:30pm 2 _~~~)Qam-5:00pm 17 ~m-2-':Q.~± 8:00am-6:00pm 1 8:00am-5:30pm 9:00am-? 1••

~

••8:00am-i:OOpm 4 8:00am -6:00pm 1 '9:00am-12:00pm 3 8:00am-8:00pm 2 8:00am-7:00pm 4 9:00am-12:30pm 1 8:00am -9:00pm 2 8:00am-8:00pm 1 9:00am-1 :OOpm 1 8:00am-2:00pm 1 8 :OOam -9:00pm ~ 9:00am -2:00pm 1

•8:00 to whenever 1 8:00 to whenever 1 9:00am-4:00pm 2 8:30am-5:00pm 1 8:30am-5:00pm 2 9:00am -5:00pm 3 8:30am-5:30pm 2 8:30am-5:30pm ~ 9:00am -5: 30pm 1

1-9:00am -5:60pm 7 9:00am-5:00pm 8 9:00a~_~_~Q_Q.em 2

•9:00am-5:30pm 5 9:00~m-5:30pm 5 9:00~m-7:00pm 1 9:00am-6:00pm 4' 9:00am-6:00pm 5 9:00am -8:00pm 1•

9:00am-7:00pm 2 9:00am -7 :OOpm 9:00am -9:00pm 1~ 9:00am-8:00pm 9:00am-8:00pm 1 ~.l0am-12:00pm 1+--~ 9:30am -5:00pm 1 9:30am-5:00pm 1 9:30am 2:30pm 1

• •••••

I

1~:30all1-5:30pm I 1 9:30..a_~ -5:30pm 1 9:30am-5:30pm 1 930am-6:0pm 2 9:30am-6:00pm ~ 10:00am-12:00pm 1 10:00am-5:00pm 2 1~0.9am4:00pm 1 10:00am-1 :Q92m 1 10:00am -5:30pm 3 1O:OOam-~:Opm I i 10~Q.0am-4:00pm ~ 10:00am-6:00pm 18 .lQ.:.Q.Oam-5:3.Qem 3' 10:00am ~5~9pm 7 10:00am-7:00pm 10:00am-6:00pm

i

17 10:00am -5:30pm 4~ 10:00am-2:00am 1 10:00am-7:00pm 10:00am -6:00pm 12I~ -10:30am-5:00pm 1 10:00am -2:00am 1 10:00am-7:00pm 1JJ :00am-5:00pm 1 10:30am -5:00pm 1 10:00pm -1 0:00pm 1

I11 :OOam -6:00pm 2 11 :Oam-9:00pm 2 10:00am-2:00am 1--_._-••• 11 :00am-7:00pm 1 11 :00am-1 0:00pm 1 11:00am-9:00P~ 11 :00am-9:00pm 2 11 :00am-2:00pm 1 11 :00am-3:00pm 1 1100am-10:00pm 1 11 :00am-5:00pm 1 11:00am-6:00pm 2I

I

•� •••�

hOOam-2:00am 1 11 :00am-6:00pm 2 11 :00am-1Q:00PEl~ __1� 3:00pm -6:00pm 1 1:00pm-10:00pm 1 11 :00am-2:00am 1� 1:OOpm-9:00pm 1 3:00pm-6:30pm 1 12:00noon-5:00pm 1� 24 hr/day 1 24hr/day ~ 24 hr/day - 1� ~ Appointment 1 By Appointment 1 By Appointment 3�

f--106 106 Varies 1

1 ~

••••• 21

•

••

- - -

•�•••�••••• Again, the importance of the Downtown commercial and retail area to the entire community is demonstrated by the business owner's knowledge of their customer base. Nearly all of the businesses responding to the following•• questions indicated that their customer is base is primary local, and they

••enjoy a high rate of return customers. This further addresses the service•• provided, as unhappy customers do not return frequently. It is always more cost effective to serve repeat customers than to attract new ones. Successful

businesses know how to sell to retain good customers. It appears that for the

most part, the Downtown Area businesses have incorporated that philosophy.

••• Survey Question: What percent of your customers/clients come from

Laramie? Number ofresponses to this question: 87

••• NUMBER OF BUSINESS RESPONDING BY CATEGORY

,••25

• -.

20

•.= C)

"0 .c:: -0 a.~ 15

••'" 0Q/C)� 0:: Q/�

"' .... -- ,... - - -'" c-aQ/U 10 _I ..c:: >'iii aJ••::l ~ aJ-0

'Ilo

I-- r- ~ I-0

10%-20% 20'/0-30% 30%..40% 40%·60% 60,/,.<;0% 60%-70% 70%-80% 80%·90% 90%,..100% •

5-

LCl-rJ --

~ .L.,..r

% of Customers from Laramie

• Every small business owner, regardless of the type of business or where they

••••are located will suggest a high number of repeat customers or return

business. While the number below may be slightly inflated, the percentage of••

repeat customers is above the norm and therefore, speaks well for the

products and/or services the Downtown Laramie businesses offer.•••• 22••�

--

---

--

-- --

-- ---- -- --

•�••• MAIN STREET LARAMIE WYOMING•••

• Survey Question: What percent ojyour business is repeat business?

Number ojresponses to this question: 97 ••

NUMBER OF BUSINESS RESPONDING BY CATEGORY••• j ...- --1•45- .' !

I

/40· .....- I

./~ 35 ~-

30

•••

~ 25 ~.

-

~- 1•• I.

-- -

20 /' -- I

~ 15- I

~ 10-/1

=I*: 5- ./ i ,- I/ - 7••• 0

-""

<25% 25-50% 51-75% >75%

Percent Repeat Business••Downtown Business Contributions

•••••• The building and business owners in Downtown Laramie serve the

community through their offerings of products and services and, perhaps

even more importantly, their commitment to the renovation, preservation,

and viable reuse of the historic buildings which dominate the Downtown

commercial area. The financial investment and creative reuse of older and•••historic Downtown buildings provide a richness and sense of history that is

reflected in the character of the community.

••In addition to the esthetic value of the Downtown area, the business owners

contribute to the overall economic health of City of Laramie and Albany

County in several important ways. As the businesses promote their products••and services, more consumers are pulled into the community to avail

themselves of these and other available products and services. The

Downtown businesses have created sustainable employment opportunities,•• both full time and part time, for Laramie residents. And as the existing

businesses expand and grow, or new businesses are attracted by the synergy

of the area and choose to locate there, additional jobs will be created.••• 23

••

••••••••••• •••••

••••••••• Sales tax paid by the business owners in the Study Area is important to the

City of Laramie and Albany County. While there are large retailers in

Laramie that are not located within the Downtown commercial area, the•• collective contribution of the Downtown businesses is an imp0l1ant

component to the overall sales tax generated in the county.••• The Building and Business Survey addressed the economic contributions of

the Downtown business: jobs and sales tax.•• Survey question: Including yourself, how many people do you employ at this location?•••� Full Time Jobs:�

Number of responses to this question:�

Total number offull time employees:

Part Time Jobs:� Number of responses to this question:�

Total number of part time employees:�•• Note: It was

81 businesses

402jobs

69 businesses

3IIjobs

the observation of those tabulating the survey data that many of the business owners who responded to this survey question, did not include themselves in the employee count for their business. Therefore, for the number ofbusiness represented below, the actual employee count is slightly understated.

••

BRG was asked to determine, based on the above representative sampling of

the Downtown Area businesses, the number of jobs existing for all of the

businesses in the Downtown Area. To accommodate this request, certain

assumptions must be made: the III survey respondents assigned are a

reflective sampling of all Downtown businesses relative to employment both

ful I and part time, that the job numbers indicated in the survey responses are

accurate, and that all similar businesses employ the same number of

employees.

••• 24••�

•••••

••••••••• ••••••••

•�

•••�

••• 73% (214) Downtown Area Businesses would produce 1,087 FT jobs

100% (295) Downtown Area Businesses produce 1,489 FT jobs

•• Part Time Jobs

23% (69) Downtown Area Businesses produce 311 PT jobs

•• 77% (226) Downtown Area Businesses would produce 1,041 PT jobs

100% (295) Downtown Area Business would produce 1,352 PT jobs

NOTE: Again, this a simple straight-line projection, provided at the request

of a committee member and does not reflect the opinion of BRG, nor is it

••Given the above detailed assumptions, a simple straight-line estimated

projection would indicate:

Full Time Jobs 27% (81) Downtown Area Businesses produce 402 FT jobs

••�

validated by surveys, interviews, or other quantitative data.

••�

••••• 25

•• •••••

•••••�••• Sales Tax

••Sales tax paid by the business owners in the Study Area is important to the

City of Laramie and Albany County. While there are large retailers in Laramie that are not located within the downtown commercial area, the

•

••• collective contribution of the downtown businesses is an important

component to the overall sales tax generated in the county.

Sales tax paid by businesses in Downtown Laramie is difficult to determine

••• accurately, as the State Department of Revenue only reports sales tax as a

gross amount collected from each County and major city, and the County

•does not track sales tax paid by the City of Laramie or by individual

businesses. However, an approximate retail sales tax estimate can be

calculated from the estimated sales that have been rep0l1ed by individual••••�businesses. The tax calculation is then based on the statutory 4% collected by

the State of Wyoming, and the additional 2% optional tax levied by Albany

County.

A further refinement must be made to separate those sales that are "exempt"

••• from sales tax, such as the City of Laramie, Albany County, religious

organizations, schools, nonprofit organizations, retail sales of prescription

drugs, newspapers, most professional services, etc., as defined by the•••Wyoming DepaJ1ment of Revenue. Of the 295 businesses in the Study Area,

49% are subject to retail sales tax collection. Their reported estimated 2006

sales of $54,280,863 represent $3,256,852 sales tax collected (at 6%).

•• The following table is a comparison of the Study Area to Albany County and

the City of Laramie. The Sales and Sales Tax calculations are based on:

• Study Area Retail Sales Tax Reported Estimated Taxable Retail Sales=

multiplied by 6%.

• Analysis # 1: Albany County Total Retail Sales State Reported Albany=

County Total Sales Tax Collected divided by 6%.

• Analysis #2: Albany County Retail Trade + Leisure and Hospitality Sales

State Reported Retail Trade + Leisure &� Hospitality Sales Tax=

Collected divided by 6%.

• Analysis #3: Albany County Retail Trade, Accommodation &� Food

Services Sales State Reported Retail Trade, Accommodation & Food=•• Laramie Sales Tax Gross Revenue divided by 6%.••••

26•

Services Sales Tax Collected divided by 6%.

• Analysis #4: City of Laramie Retail Sales = State Reported City of

•••

•�•••••�•�•�•�•�•�••�••�•�•••�•�••�•••�••� •••••�••�••�•••�••�

MAIN STREET� LARAMlt WYOMING

SALES TAX CALCULATION

Study Area 1 - Taxable Retail Sales (Reported)�

Sales Tax based on Taxable Retail Sales (Calculated from Reported Taxable Retail Sales)�

Analysis #1 Albany County' - Total Retail Sales FY 2006 (Calculated from Reported Tax Coffected)

f-~ Percent of Study Area's Taxable Retail Sales to Total Albany County Retail Sales Total Sales Tax Collection - Albany County FY 2006 (Reported)

Percent 01 Study Area's Retail Sales Tax to Total Albany County's Retail Sales Tax

Analysis #2 Albany Countv' - Retail Trade. Leisure & Hospitalily Sales (Calculaled lrom Reported Tax Coffecled)

Percent 01 Study Area's Taxable Relail Sales 10 Albany County Retail Sales Sales Tax Collection - Albany County FY 2006 (Reported)

Percent 01 Study Area's Retail Sales Tax to Tolal Albany County's Retail Sales Tax

Analysis #3 Albany County" - Retail Trade, Accommodation, Food Services Sales (Calculated lrom Reported Tax Coffected)

Percent 01 Study Area's Taxable Relail Sales 10 Atbany Counly Retail Sales Sales Tax CollecUon - Albany County FY 2006 (Reported)

Percenl 01 Siudy Anaa's Retail Sales Tax to Total Albany County's Retail Sales Tax

Analvsis #4 City of Laramie' - Sales (Calculated lrom Reported Sales Tax Gross Revenue)

Percent of Siudy Area's Taxabfe Relail Sales /0 Tolal Cily of Laramie City of Laramie - Seles Tax Gross Revenue (Reported)

Percenl of Siudy Anaa's Relail Safes Tax 10 Total City of Laramie

S<XXoos.;

,. WMRC & ESRJ

~f1!6nl of AdminlsHslion end Infotm8llon, Economic AnalySIS DrVlsion & Wyom:1'!9 Deperlmenf of Revo()()lj,

Wyoming Safes, Use, end Lodging Tex R6Vfmue Report- 1(}11f2006, Tol8/ Sales Tax Co!foclions by Courly

J. Oeparlmen/ o{ Admm/slre/ion and fnfrxmw.ion, Economic AnB/ysls f:)visioo &. WYomIng D8parlmenl of Revenue.

iNYomlng Seles, Use, and Lcx1glflfj Tax Revenue Report - 1011f2006. Albany County Retsil Trade & Leisure &: Hosp:te/i/ Solos Tex CoHeet/on

4. Dep8f1ment of Admnlstr81lon 8nd fnformetlon. EconomIC AnalySis DrviSJOn & 1-\Ycmmg Dep8ltJnenl of Rsv9fJIJ9,

2006 Sales 4% Tax 6% Tax

$ 54,280,863 S 2,171,235 $ 3,256,852

-

$ 459,218,317 11.8%

$ 18,368,851 S 27,553,099 11.8% 11.8%

S 293,257,417 18.5%

$ 11,730,269 $ 17,595,445 18.5% 18.5%

S 292,367,950 18.6%

S 11,694,691 S 17,542,077 18.6% 18.6%

S 362,868,117 15.0%

S 14,514,725 S 21,772,087 15.0% 15.0%

~omlflg S8fas. Usa, 8I'1d Lodging Tax Rf1V9flW RepM- UY112OO6. AJb8t'IY County Ratall. ACXXJmmooaUon &. Food SeMceS 58/as Tax Col1ectlon

5. Wyomtng Dep8ftJnfKll of R9V9flUe, AdminiSlrslio(J - Annual Raport 2006, AW9981& 581&$ and USB Tax - DisJriblAlOfl RapOO JOf Fiscal Y(Jar '2006

The chart above illustrates that the businesses in the Study Area contribute,

from taxable retail sales, an estimated 15% of the total City of Laramie sales

tax collected, and an estimated 18,5% of

the Albany County retail sales tax

collected.

While the 15% contribution of retail sales

tax by the Study Area appears to be

substantial, it is important to understand

that when the sales tax collections are

distributed back to the City's general fund

from the State Depaltment of Revenue,

those dollars benefit the entire Laramie community in terms of critical revenue to

pay for essentials including, Municipal

--- r-

• .16011,;;"4W

1', '.

..."r. r->t>,.. '7'F.,E I~) a~ - j- 4,

-

.

1-

ji -t '\~.~ //-

/ r \

fr {III\!/ I 1'''\ ]

1~~ f- J, ". ""-r--- (111' I l"""" -:tl"~ ,/' , ~~ I -[,/ I i

:t'i'7 ·\lh,lT1~· i"'.l..~ I1J'.1n~(~

(.'u.rdl...IH.J.IU'"� -..,. .... .t-_._~.

operating costs, infrastructure

, "

2007 Albany County Tax Districts I City of Laramie

rIUlJJlri,.- - "- " f--- ~ l-Ll,; J,v..

I 1-1

improvements, public facilities & parks maintenance, fire & police

protection, streets & roads maintenance, uti1ities/waterlsewer/trash, special

community events, and other special projects desired by the community.

27

•••••

••�••••�• • •••

Distribution of the sales tax collected by the State is based on a formula,

which basically results in 69% of the total collected sales tax is distributed to

the State General Fund, and after deducting an administrative fee, the balance

is distributed to the Counties, Cities and Towns based upon population

(population as determined by the last federal census). The optional sales tax

revenue, less State administrative fees, is returned to the County of origin.

Because the collection of sales tax and its subsequent distribution are based

on entirely different methodologies, comparisons of sales tax collections to

sales tax distribution (if it could be calculated) to a specific area within a

County or City, would be irrelevant.

The State Department of Revenue Statutes read:

State Rate Tax - 4%

•

••••••••••w.s. 39-15-111 and 39-16-111 govern the distribution processes for sales and use state rate tax, respectively. State rate tax is distributed to the general fund as directed in Ws. 39-15-111 (b)(i): " ... credit sixty-nine percent (69%) to the state general fund ... " The remaining 31 % is distributed according to•••• Ws. 39-15-111(b)(ii): "Deduct one percent (1%) from the remaining share to cover all administrative expenses and costs attributable to the remaining share and credit the general fund for that amount. " Ws. 39-15-111 (b)(iii) further states that: "From the remaining share, ... deduct an amount equivalent to one percent (1%) of the tax collected under Ws. 39-15-104. From this amount, the state treasurer shall distribute ... forty thousand dollars ($40,000) annually to each county in equal monthly installments and then distribute the remainder to each county in the proportion that the total population of the county bears to the total population of the state. The balance shall then be paid monthly to the treasurers of the counties, cities and towns for payment into their respective general funds.

••• • The percentage of the balance that will be distributed to each county and its

cities and towns will be determined by computing the percentage that net sales taxes collected attributable to vendors in each county including its cities and towns bear to total net sales taxes collected of vendors in all counties including their cities and towns ... , this percentage of the balance shall be distributed within each county as follows: (A) To each county in the proportion that the population of the county situated outside the corporate•••• limits of its cities and towns bears to the total population of the county including cities and towns, and (B) To each city and town within the county in the proportion the population ofthe city or town bears to the population of the county." Population as defined in Ws. 39-15-101(a)(iii) "means the population as determined by the last federal census (Census 2000) ... "

•••••� 28�

•••• •••••••••

••••• ••••• ••• •••

•�•� MAIN STREET

LARAMIE WYOMING

••••�

General Purpose Option Tax Ws. 39-15-2JJ governs the distribution of the local option sales taxes. Ws. 39-15-211(a)(i) directs the general purpose option tax distribution in that a 1% administrative fee is deducted and sent to the state general fund, and the remainder is distributed to the county imposing the tax and its cities and towns. The county amount is distributed by population in the proportion of the county outside corporate limits to the total county population. Ws. 3915-211 (a)(i)(II) directs the distribution to cities and towns: "To the incorporated cities and towns within the county ... in the proportion the population ofeach city or town bears to the total population ofthe county. "

Specific Purpose Option Tax Ws. 39-15-2JJ(a)(iii) governs the distribution ofthe specific purpose option tax. After a one percent (1%) deduction for administrative expenses, the remainder is to be distributed monthly to the county treasurer of the county imposing the tax. The county treasurer is responsible for distributing that tax to the sponsoring entity.

Albany County Sales Tax Collections

Eating and Drinking Plaeos�

Lodging Sorvleos�

Mlseolla noous Reta II�

General Merohandlse Stores�

Department Stores�

Clothing and Shoe Storos

Liquor Stores�

Grooery and Food Stores�

Building Matorlal and Garden Suppllos

Eleotronlc and Appllanoe Stores�

Home Furniture and Furnishings�

GasolIne Stations�

Auto Dealers and Parts�

•••• 29

•••••�

o oo

ooo

ooo

oo o. g~ ~- ~

N ..; ..0,

• FY 2004 4% Taxes • FY 20064% Taxes

Source: Slate of Wyoming, DepMmenl of Revenue

•••••••• Building Chaloactel"istics• The responses to Building and Business Survey illustrated the scope of age,

features, and multiple use of the building in the Laramie Downtown Study•Area. The responses to the questions specific to building conditions and•utilization for upper floors is limited based on the understanding that in some• cases tenants were unwilling to respond to questions not directly related to• their lease space, and not all building owners responded to the survey.

Survey question: What year was your building built? ••

Number ofresponses to this question: 66•• NUMBER OF RESPONSES BY CATEGORY

•Late

•• 1900's Late

4 Mid 1900's 1800's•

24 17

••••• Early 1900's•••

21

••• Buildings in the Study Area vary in size from small one-story building to

larger structures with multiple floors. Many of the buildings represented in

the survey have basements. Survey responses indicate that nearly all•••basements are used for storage, rather than for commercial, retail, or residential use.

• Survey question: Does your building have upperfloors?�

Number ofresponses to this question: 101� Yes: 62%�

•�•• No: 38%�

••30•••

•• ••• •••• •• •• ••••• • • • •• • • • •• •• •

•�

••••• ~

••••�

••�

Survey question: What is the approximate square feet of the entire building?

Number ofresponses to this question: 66 Responses ranged from a building size of 800 sq. ft. to 32,000 sq. ft.

The responses to the questions specific to building conditions and utilization

of upper floors is limited based on the understanding that in some cases

tenants were unwilling to respond to questions not directly related to their

lease space, and not all building owners responded to the survey. Therefore,

the category of use, specifically residential use, is thought to be slightly

understated among the business/building owner survey responses.

Survey question: Indicate the category of use for each floor of your building.

Number ofresponses to this question: Varies, see categories below

Residential Use: Street Level

Second Floor

Third Floor

Fourth Floor

Fifth Floor

Office: Street Level

Second Floor

Third Floor

Foulih Floor

Commercial: Street Level

Second Floor

Third Floor

No responses

25 positive responses

4 positive responses

2 positive responses

2 positive responses

16 positive responses�

20 positive responses�

3 positive responses�

I positive response�

54 positive responses

10 positive responses

No responses

The building condition section of the survey included questions about the

type and condition of all building components: roof, exterior walls, interior

walls, number of restrooms, etc. In addition, respondents were asked to rank

the condition of each building component: excellent, good, fair, poor.

31�

•�•••••� The number of respondents to the building condition section of the survey

varies; however, it is important to state that the building components

reflected in the survey responses are indicated as being in fair, good, or

excellent condition. Building owners and/or their tenants should be

complimented on their obvious commitment to repairs and maintenance, and

to renovation, restoration, and creative reuse of older or historic buildings.

A blank copy of the Building and Business Survey questionnaire is included in the Appendix.

•••••••••••••••••••••�•••••�

•• 32

••••••••••

MAIN STREET LARAMIE WYOMING

CHAPTER III BUSINESS ENVIRONMENT

Business Clusters Business in the Downtown Laramie area can be grouped according to types

of businesses that share a similar customer base, or provide similar goods and

services. These groupings are called "clusters" and can reveal important

information about the patterns of retail Downtown for current business

owners, business development and new business recruitment opportunities.

As illustrated on the following map (not all businesses are shown on the

map), there are clear business clusters identifiable in the Downtown area.

The primary cluster with the highest concentration of similar or

complimentary businesses is labeled #1. This area also appears to be the

"retail shopping center" of Downtown Laramie. This cluster for example, in

approximately a one-square block area includes 40-retail businesses:

• 6-restaurants, • I-coffey shop • 4-variety retail stores, • 3-antique stores, • 4-sporting goods stores, • I-drinking place, • 2-beauty salons, • 4-bakery, specialty food stores, • 4-clothing/jewelry stores, • 2-book stores, • I-doctor, • 4-Lawyers, legal services,

• I-CPA, • I-furniture, home furnishing store, and • 3-art galleries.

Other smaller identified clusters, #2 to #9, have the same characteristics of

similar or complementary businesses, or that serve similar customers, and/or

are in close proximity to each other.

It seems that the Office Supply store is a "loner" and might benefit by being

closer to the municipal offices, county offices, or the Downtown businesses.

Since it is the only office supply store, location may not be a factor.

••••••••••••••••••••••••••••••••••••••••••••� 33�

MAIN STREET LARAMIE WYOMIN\;

However, it does present a possible opportunity for a second "office supply"

business in another Downtown location.

As displayed on the map, the "Opportunity Area" presents opportunities for

business development which might capitalize on specific high volume

customer bases, such as the municipal offices and county offices. Businesses

that might benefit include restaurants, drinking places, office supply stores,

legal services, printing/copying services, courier services, civil/social/family

services, and accounting/financial services.

••••••••••••••••••• The results of the Retail Sales Potential (Chapter IV) identify Retail Gaps, or

"Leakage", in the categories of Apparel, Food & Beverage, and Sports &

Hobby, and define potential for new business development or recruitment.

Based on the Cluster Theory and analysis below, new business development

opportunities in these categories would have a higher probability of success

in Clusters #1, #4, #5, and #8.•••••••••••••••••••••••••� 34�

•••••••••••••••••••••••••••• •••••• •••••••••

MAIN STREET LARAMIE WYOMINc;

•�

Laramie Main Street,(.~ t:I Book Stores, News Dealers - Misc. Varlely Relall m Clinic, Doclors, DenllstWCF,lEDC

* Clothing, Jewelry, Shoe Stores Office Supplies*<> Art Galleries Accounllng, CPA's

<> Sporllng Goods Printing Services a� Bakeries, Specialty Foods I-±J� lawyers

• Banks0 Restaurants Appliance, Radio, TV, Electronics \QI Antiques, Used Merchandise

• Drinking Places Furniture. Home Furnishings @ laundry, Dry Cleaners'i~ Beauty Salons, Barber

City of laramie Municipal

* Florists Tobacco Slores W Hotels, Molels 0�Movie Theater Albany Counly OfficesShops, Personal Care

35�

••� MAIN STREET�

LARAMIE WYOMINl;

#1

Alexander's Fine Jewelry Inc

Antique Fever

Artisans Gallery

Atmosphere Mountainworks

Augusta Mzzlwtts Back of Wagon

Bead Shop

Big Hoss Mountain Sports

Buckhorn Bar

Chickering Bookstore Inc

Chocolate Cellar Cid Walck CPA LLC Coal Creek Coffee Co

Copper Kettle LLC

Corthell & King PC

Cross Country Connection

•••••••••••••••••••••••••

Curiosity Shoppe

Earth, Wind & Fire Galleries

Elmer Lovejoy's Bar & Grill

Frausto Enterprises Inc

Gallery West & Frame Plant

Grand Bazaar

Green Gold

1st Story Cafe

Jeffrey's Bistro

John A Holtz

Judy Coburn

Law Offices of Janel L Tyler

Medicine Bow Natural Foods

Melissa Sweet••• Overland Restaurant

Palladium Hair Studio

Pedal House

Prairie Sage Pottery

Ronald D Copenhaver

Saras Bakery

Second Story Bookstore

Sensuous She

Stickley & Stickley Entrprs

Sweet Pickles

Visions Hair Salon

Whole Earth Grainery

Opportunity Area

City of Laramie

County of Albany

••••••••••••••�

Business Clusters - Business Lists

#2

Atmosphere Mountainworks

Coal Creek Coffee Co

Elmer Lovejoy's Bar & Grill

Frausto Enterprises Inc

Green Gold

1st Story Cafe

Melissa Sweet

Overland Restaurant

Palladium Hair Studio

Pedal House Seccnd Story Bookstore

#3

Bead Shop

Buckhorn Bar

Chocolate Cellar

Frausto Enterprises Inc

Gallery West & Frame Plant

1st Story Cafe

Jeffrey's Bistro

Overland Restaurant

Seccnd Story Bookstore

Sensuous She

Sweet Pickles

Whole Earth Grainery

#4

Alexander'S Fine Jewelry Inc

Augusta Mzzlwtts Back of Wagon

Big Hoss Mountain Sports

Chickering Bookstore Inc

Spm Inc

Stickley & Stickley Entrprs

#5

A Touch of Country

Altitude Chophouse & Brewery

Bridgetech Inc

Buck & Doe

Citrus Salon

Heron Night Books

Home Bakery

Ken's Music Box Inc

Maurices Inc

Quiltessentials

Terrapin Inc

Three Peaks Pottery

36

#6

Aspen Appliance Inc

Direct Maytag

Doddscc Inc

Dollar Partners Inc

Dove Lonesome

Lopez, Tony S Attorney At Law

Undercover Waterbed & Spa

#7 Aphrodites Antiques Community First National Bank Junction Tobaccc Shop

Killian's Florist

Kn Energy Appliance Store

Mister Pawn Shop

Radioshack Corp

#8

Connor Flower Shop

Dave Perry

First Interstate Bank

Grand Ave Pizza

Grand Newsstand

Mark Cupps Dr

Martindale's Western Store LLC

Mountain Woods Furniture Inc

Naural Balance

New Hair ERA

Old Town Bagel & Ice Cream

Pro Dish

Room To Grow

Tommy Jacks

Tumblin Dice Inc

Wyo Barber Shop

#9

Bagelmakers

Corral West Ranchwear Inc

Daylight Donuts

Dini Chiropractic Center

Grounds Internet & Coffee

Habanero Mexican Grill

Laramie Travel Inn

Subway

Travelodge Downtown Motel

••••••••••••••••••••• •••• ••••••• ••• •••••• •••

MAIN STREET lARAMI~ WYOMING

CIIAPTERIV� TRADE AREA ANALYSIS�

The demographic information contained In this Study is included here to

define those characteristics of the City of Laramie and the surrounding

community that are indicators of its ability to support the development of

expanded retail and commercial services in Downtown Laramie. The

economy of Laramie and Albany County is stable and consistent. While

much of the state is experiencing the chal1enges of rapid growth due to

increased extraction activity, Albany County is relatively unaffected.

To provide a perspective on the City of Laramie demographic groupings,

which defines the primary trade area for businesses in the Study Area, the

data is presented relative to Wyoming communities that are (like Laramie)

border communities, not dramatically impacted by the activity in the

extraction industries: Sheridan and Cody. Cheyenne has also been included

for comparison as it represents a competitive trade area and its influences,

like the City of Laramie, are primarily internal rather than external

It is important when reviewing community demographics that City of

Laramie is unique among Wyoming cities, whether through demographic

comparisons or in stand-alone data. The University of Wyoming and

Wyoming Technological Institute and their associated student populations,

approximately 10,000 students and 2,000 students per year respectively, tend

to influence age, income, and other community profile factors particularly

when presented as percentages of the whole. It is therefore recommended

when reviewing the following data, to look at the past and future trends,

rather than percentages, in order to use the information effectively.

COimnlulity Profile As the City of Laramie's community profile is developed, the first element is

the population size of the City and surrounding area. For purposes of this

study, for the City of Laramie and the comparative communities, the market

area is considered to be within a 3-mile radius of the City. Population growth

over any given period is an indicator of a community's ability to support

existing, expanding, or new expanding commercial and retail services.

37

••••••••••••••

The population growth trend forecasted for Laramie appears to match that of

the comparison communities. The student population of the University of

Wyoming and Wyoming Technological Institute are included in the

following total population numbers. While the students represent a consumer

block, or target market, their income is generally relatively low and therefore

their purchasing ability is generally limited. However, the student consumer

block should not be ignored when assessing the retail sales potential within

the City of Laramie trade area.

PROJECTED POPULATION GROWH COMPARATIVE COMMUNITIES

•••••••• 2011 ~••~:::..l..__L_..L_~ Ul c: o

••;;

QlCJ

'£ 2006 .....~~;:.J..__.J. ~_..

••011 II! III

~ 2000 •••~~~::"J..__.J. ~...

•• ::J Ul c: Ql

U 1990 ••IIJ;;;;;:::......l..._...J.__L ..

o 10,000 20,000 30,000 40,000 50,000 60,000

o Cheyenne • Cody 0 Sheridan Laramie

Source: AnySile Online

••••••• The projected population growth of all of the comparative communities for

the period 2006 through 20 II, is similar with Cody projected as the fastest

growing of the four communities. Cheyenne and Laramie are both projected

to grow at nearly the same rate over this period.•••••••••� 38�

-- - -- --

•••••• MAIN STREET

LARAMIE WYOMING

PROJECTED PERCENTAGE OF POPULATION GROWTH •••• OVER PERIOD: 2006 - 2011

•3.50% /

;:;iiiiiiiIj. 3.00%

•• QI 01 2.50%c l.ev .t: 0 /

2.00% -0 1- -- 1-- -~ 0

'0 1.50%g u .QI

/'e- 1.00% a.. , - I- -- ,-

0.50%

,-I- ~~

~

••••••• 0.00% L ,. ~

Cheyenne Cody Sheridan Laramie

Source: AnySitc Online

••••••••Income of the residents within the primary trade area is an important

indicator of the community's ability to support retail and commercial

development. The comparative communities have been included in this

•• analysis as a reference point from which to consider the level of commercial

and retail development communities can support. Again, it is important to

consider that Laramie's large student population, not yet into their full

earning capacity, are included in all of the data relative to income presented

• ••••

here:

Per Capita Income: the income of an entire study area divided by

the entire population (regard less of age) in the same study area.

A verage Household Income: the total income within a study area

divided by the number of households in the same study area.

Median Household Income: a mid-point between the income of the

household(s) with the lowest income range and the household(s) at

the highest income range within the same study area.

•••••39••••

•••• MAIN STREET•• L'\RAMIE WYO.\IING

•• COMPARATIVE PER CAPITA INCOME•.. I I I I II

••Cheyenne

~ I•• I I I I I I 1 u U

Cody N I ,] I I I I I

••••••

U U Sheridan

II II - 1 I I I I I I D U

Laramie II I I••

"I 1�

/ /�

$10,000 $12,000 $14,000 $16,000 $18,000 $20,000 $22,000 $24,000 $26,000 $28,000

• 02000 .2006 02011

• Source: AnySite Online•• COMPARATIVE AVERAGE HOUSEHOLD INCOME•••

( ....I

1u U

ICheyenne A••I

.II I I I I

• n U Cody

•II

I I I II U

Sheridan•••

H •

•~ I I I n tJ

Laramie II • I I•• r'

$10,000 $20,000 $30,000 $40,000 $50,000 $60,000 $70,000

02000 _2006 02011

••• Source: AnySite Online

•• 40••

•••••• COMPARATIVE MEDIAN HOUSEHOLD INCOME

•••••�••••••�•�•�••�•�•�•�•�•�•�•�••�••••�•�•�•�•�•�••�•�••�

., ..--------------------~ I I I I I I ,

1 I II L

II

1'1

Cheyenne

I I I • I II

IICody

I II 1 I I II U

II n

Sheridan

I I I I • I II 0

~ ... Laramie • I

, J I I

/ ,

$10,000 $15,000 $20,000 $25,000 $30,000 $35,000 $40,000 $45,000

02000 .2006 02011

Source: AnySite Online

COMPARATIVE MEDIAN HOUSEHOLD INCOME� PROJECTED GROWTH 2000-2011�

Cheyenne

Cody

Sheridan

Laramie

0% 10% 20% 30% 40%

Projected Growth Over Period 2000 - 2011

Source: AnySite Online

41�

•••• MAIN STREET LAUAMIE WYOMING•�

•••

••• The income trends in the graph above indicate that the City of Laramie and

the surrounding area are projected to experience a greater increase in median

household income than that projected for the comparative communities, over

the 2006 through 2011 period.•• At a micro level, the household income for Laramie households presents an

interesting trend relative to supporting and sustaining commercial and retail•••••

growth. The projections below indicate that the number of households at the

lower income levels will decrease over the period, as individuals experience

a slightly higher income over the five year period. The number of households

in the highest income range is also projected to increase significantly.

• LARAMIE HOUSEHOLD INCOME

YEAR 2000 2006 2011 Change•• Total Number Of Households: 11,336 12,155 12,726 2000-2011'-------1

•�Number Of Households By Income:�

<$15,000 3,366 2,861 2,486 (880)� $15,000-$24,999 1,970 1,980 1,763 (177)

•• $25,000-34,999 1,487 1,437 1,611 (124) $35,000-$49,000 1,570 1,653 1,693 123 $50,000-$74,999 1,725 1,964 1,974 249

••••$75,000-$99,999 708 1,058 1,293 585 $100,000-$149,000 383 950 1,373 990 $150,000-$199,000 74 96 312 238 >$200,000 81 155 221 140

Chart Illformation SOl/ree: ESRI

••• Median household income and per capita income are both factors which can

indicate a solid consumer base. Even more important however is disposable income, sometimes referred to as discretionary income, the money used for

•••discretionary purchases: clothing, entertainment, toys (child & adult),

vehicles, etc. Individuals in Wyoming enjoy a relatively high disposable

income, primarily due to:

• Low cost of housing, both rental units and homeownership•• • Low State Sales Tax

• • No State Income Tax

The State of Wyoming Economic Analysis Division calculates disposable

income as 87% of med ian household income.••••• 42

••

••••••

••••••••• COMPARATIVE PROJECTED DISPOSABLE INCOME

•• ......... I

••!

I

U Cheyenne

II"I I I IJ

••n

•Cody

•.1 I I I I

u Sheridan••

II

J I I •

•y II

Laramie I I I•

$10,000 $15,000 $20,000 $25,000 $30,000 $35,000 $40,000

02000 .2006 02011

Source: AnySite Online

••• Another component of the Community Profile relative to the potential to

support and sustain current and future retail and commercial expansion and

development is the population by age group. Age groupings within the

overall population can be defined as target markets - the products purchased

by a 15 year old, for example, may be very different that the products

••purchased by a 65 year old - given the same disposable income.

The following graph depicts the City of Laramie and surrounding area's•• population by age groupings. For this depiction, the 2000 U.S. Census

numbers are most hel pfu I, as projections for 2006 and 2011 are based on the

•••most recent census data and projected into the future using certain

assumptions. One such assumption is that the population identified in the

census is a fixed component of the overall population and therefore will

continue to age with the overall population over time. In Laramie however,•• this trend does not apply, and is influenced by the relatively fixed the age

group of the student population. As long as the University of Wyoming and

•• the Wyoming Technical Institute continue to attract a relatively large student

population, every ten-year census will indicate a large portion of the City of

Laramie population between 18 and 24 years of age.

•• 43

•••

•• •

•••

••• • • •• •••• •

-------

•�••• MAIN STREET LARAMIE WYOMING••••�

•••••�••�•�••�••�••�••�

••�

While this student population does represent a target market, it is impol1ant

to also see the percent of the population by all other age groups, which

represent the non-student population of the Study Area. The age distribution

of the Study Area, coupled with its disposable income, and the projections

for future growth are all very encouraging indicators for the future of

Downtown Laramie's commercial and retail businesses.

PERCENT OF THE POPULATION BY AGE GROUP

18.00'.· .. 16.00%·

14.00'.·· .

-�12.00'.

-�10.00%'"�

8.00'. .. - -~

-.. - - ,.6.00%- . .. - _. ...- '-i"'~ - - - -

4.00'.I" ..- - -- - - I- - - --

2.00%

I- ..... ..... .... ;....,j JlJ1Jl.ILrL.... .... h- .... 0.00% ~ -

0-5 6·13 14-17 18-20 21·24 25-29 30-34 36-39 40-44 45-49 60-64 65-59 60-64 66-69 70·74 75-79 8O-&l 86+

Ago Groups

Source: AnySite Online

44�

•••• MAIN STREET LARAMIE WYOMING••••• Retail Sales Potential As it is true for many cities in the US, retail sales in the City of Laramie area will benefit from the influences of several positive factors, such as projected•increased growth in the Wyoming and US economies, exceptionally low• unemployment (3-3.5%), Laramie's population growth, increase in wages, increasing disposable income, all resulting in increased consumer demand for goods and services.

••• As displayed in the charts below, retail sales in the City of Laramie area are •• projected to grow at a positive cumulative rate of 18.6% from 2006 to 20 II

•••

(shown in "today's" dollars). Although each general category of retail sales is projected to grow at relatively the same rate, those showing the highest

potential growth in dollar sales are General Merchandise, Furniture/Home

Furnishings/Appliances, Food and Beverage, and Automotive. (See Category••Definitions at end ofChapter IV)

• Laramie Retail Sales Potential 2006 2011 % Increase

• Apparel $24,623,308 $29,191,215 18.6%

•Automotive $63,608,599 $75,483,134 18.7%

• Building Material $23,046,748 $27,429,562 19.0%

Electronics $11,901,222 $14,124,484 18.7%

Food & Beverage $80,761,890 $95,762,186 18.6%

• Furniture Stores, Home Furnishings, Appliances & Furniture $97,751,903 $115,991,229 18.7%

Gasoline $41,135,036 $48,791,408 18.6%

•General Merchandise $148,095,600 $175,691,352 18.6%•• Health & Personal Care $27,525,853 $32,662,863 18.7%

Miscellaneous $4,502,700 $5,350,706 18.8%

Sports & Hobby $11,495,759 $13,622,878 18.5%

• Total Retail $634,448,618 $634,101,017 18.6%