historical perspective of alternative acquisition

TRANSCRIPT

Historical Perspective of Alternative Acquisition Approaches for Launch

Systems

2021 NASA Cost & Schedule SymposiumApril 7, 2021

Presented By:

Richard WebbKAR Enterprises

Outline

• Alternative Acquisition Approaches– Overview– Definitions

• Contract Consolidation– Shuttle– Evolved Expendable Launch Vehicle (EELV)– International Space Station (ISS)

• Commercialization– Commercial Atlas Program– Commercial NASA Programs– Commercial DOD Program

• Other Approaches – Insight/Oversight• Government-Owned Corporations (“G-Corps”)• Summary

2

Overview of Alternative Acquisition Approaches

• “Glidepath” from Development to Production and Operations (P&O) is a continuum that has many potential paths/options

• Choices of appropriate paths very dependent upon overall program goals and characteristics– Not all paths are mutually exclusive

• Set of common requirements regardless of paths chosen• Lots of previous experience, potential analogs, lessons to learn

– “Commercial-like Operations”• NASA – Commercial Cargo & Crew; LSP• DOD/General Dynamics: Commercial Atlas – 1st U.S. “commercial launch

service”; National Security Space Launch (NSSL – EELV follow-on)– “Consolidated Contractor”

• Shuttle - United Space Alliance• EELV - United Launch Alliance (pre 2012)• International Space Station

– Other Approaches• Government-Owned Corporations 3

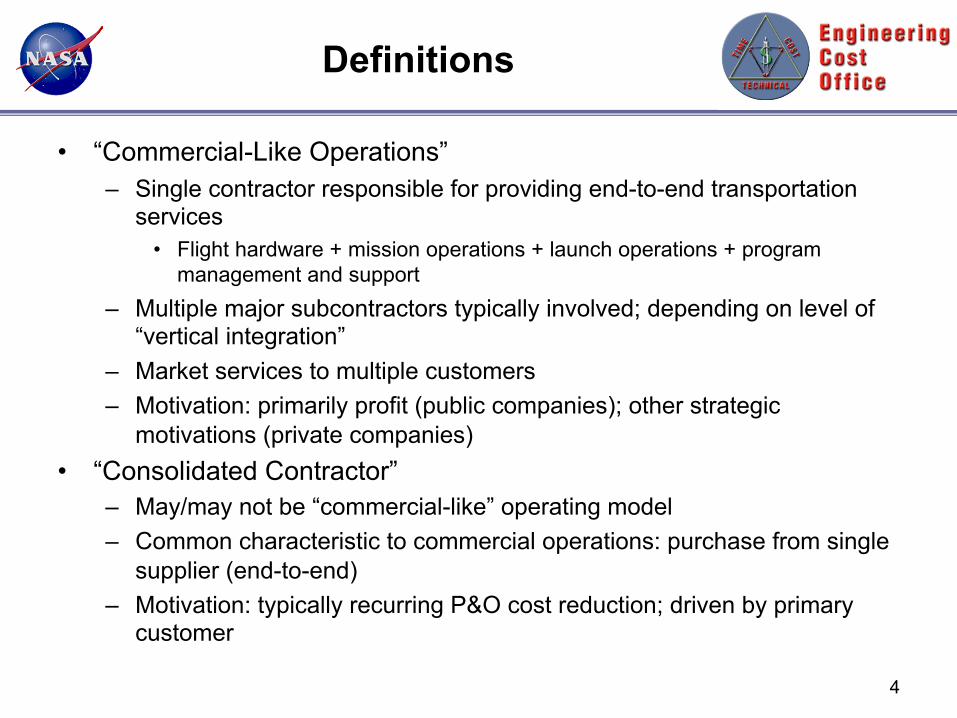

Definitions

• “Commercial-Like Operations”– Single contractor responsible for providing end-to-end transportation

services• Flight hardware + mission operations + launch operations + program

management and support– Multiple major subcontractors typically involved; depending on level of

“vertical integration”– Market services to multiple customers– Motivation: primarily profit (public companies); other strategic

motivations (private companies)• “Consolidated Contractor”

– May/may not be “commercial-like” operating model– Common characteristic to commercial operations: purchase from single

supplier (end-to-end)– Motivation: typically recurring P&O cost reduction; driven by primary

customer

4

Contract Consolidation –Shuttle (USA)

• Consolidated multiple Shuttle prime contracts to single prime run by 50/50 Boeing/Lockheed LLC United Space Alliance in late 1995– Cost plus award/incentive contract structure– Consolidation was never completed (ET, SSME, RSRM not included)

• Total Shuttle program cost reductions between 1993 and 1998 approx. 30%

5

• GAO, NASA IG, and other reports noted that reduction in Shuttle workforce/cost was result of several ongoing initiatives, not just USA contract consolidation

• Difficult to differentiate savings related to each initiative

• Columbia Accident Investigation Board (CAIB) and other studies noted that by early 2000’s downsizing had “gone to far” at which point NASA “reversed the trend”

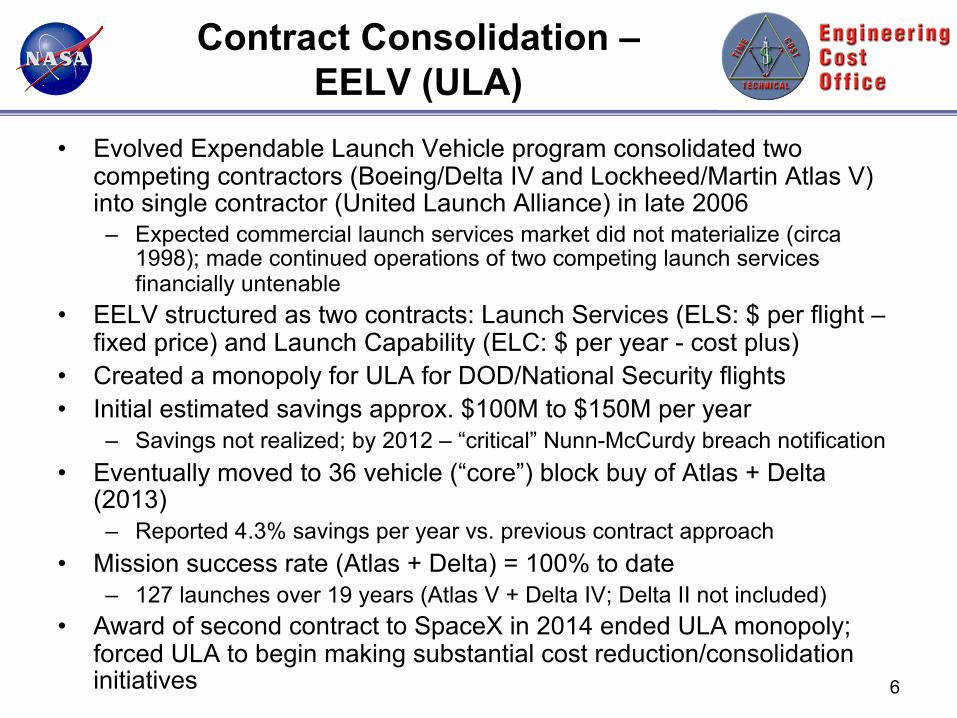

Contract Consolidation –EELV (ULA)

• Evolved Expendable Launch Vehicle program consolidated two competing contractors (Boeing/Delta IV and Lockheed/Martin Atlas V) into single contractor (United Launch Alliance) in late 2006– Expected commercial launch services market did not materialize (circa

1998); made continued operations of two competing launch services financially untenable

• EELV structured as two contracts: Launch Services (ELS: $ per flight –fixed price) and Launch Capability (ELC: $ per year - cost plus)

• Created a monopoly for ULA for DOD/National Security flights• Initial estimated savings approx. $100M to $150M per year

– Savings not realized; by 2012 – “critical” Nunn-McCurdy breach notification• Eventually moved to 36 vehicle (“core”) block buy of Atlas + Delta

(2013)– Reported 4.3% savings per year vs. previous contract approach

• Mission success rate (Atlas + Delta) = 100% to date– 127 launches over 19 years (Atlas V + Delta IV; Delta II not included)

• Award of second contract to SpaceX in 2014 ended ULA monopoly; forced ULA to begin making substantial cost reduction/consolidation initiatives 6

Contract Consolidation –International Space Station

• Consolidation of 4 Work Package contracts initially awarded for Space Station Freedom consolidated to single Prime (Boeing) 1993– McDonnell Douglas and Rocketdyne relegated to subcontractors;

cancellation of 4th Work Package– Boeing subsequently acquired both McDonnell Douglas and

Rocketdyne• Significant amount of change surrounding transition from Space

Station Freedom to ISS makes it difficult to extract useful data or draw useful general quantifiable conclusions

7

Image taken from 2006 presentation of Space

Station Cost History Team

• Multiple schedule slips• Requirements changes and several design iterations• Flat funding profile beginning in 1990 not well suited for development program• Bringing International Partners on board• Cost-cutting measures and RIF undertaken at the same time - loss of key staff

Commercialization –Commercial Atlas

8

• First (known to us) U.S. Government purchase of commercial launch services -General Dynamics Space Systems (GDSS) Atlas II “Commercial Atlas” program

– GD Board authorized non-recurring investment and purchase of 62 unsold Atlas II shipsets begin ca. 1985

– First commercial Atlas launch: NASA CRES 7/25/1990

• Commercial Atlas provides insights into implementation of commercial approach– Asset ownership transfer – Use of Barter– Block buys – purchase of 62 shipsets - GD issued Firm Fixed Price subcontracts for primary

system elements• MA-5 (Rocketdyne), RL-10 (Pratt Whitney), INU (Honeywell), Data Acquisition System (Gulton), Solid

Motors (Thiokol); Savings approx. 30%+– Subcontract termination liability “saved” program from early cancellation by GD due to early

launch failures; sold GDSS to Martin Marietta (1993)– Anchor tenants – USG acted as “anchor tenants” for initial 62 vehicles

• After GD commitment, DOD purchased blocks of 9 DSCS (USAF) and 11 UHF (Navy) satellite launches; USG ultimately accounted for 47% of 80 flights of commercial Atlas program

– Investment Incentives – Future investments in follow-on systems made possible• Eventual success of commercial Atlas II program enabled Lockheed Martin investment in Atlas V

EELV program, which enabled ULA, which enabled investment in Vulcan

“General Dynamics acquired the remaining Atlas/Centaur Program assets from NASA in exchange for performing one launch service (AC-69 CRRES). These assets included the Intellectual Property; one mostly completed vehicle, lots of parts, and the Launch Complex 36 ground support equipment at Cape Canaveral.”

E. Bock, former GDSS Atlas Program Manager, www.marsretirees.org/Moments/hist2012Q2.pdf

Commercialization - NASA

9

• Commercial Cargo, Commercial Crew, Launch Services– NASA procures end-to-end launch service from multiple providers

• Competition• Each provider has access to multiple other transportation markets

– Levels of NASA insight/oversight vary depending on specific mission• Crew: substantial insight into contractors’ crew capsule and launch vehicle designs• Cargo: substantial initial insight/integration with ISS in particular; reduced as systems

certified/flown• LSP: varies depending on NASA’s classification/certification of launch system risk (Risk

Category 1 through 3) and payload Mission Class (A through D)• All contracts are OTA/SAA’s for development; IDIQ Fixed Price per launch for

launch services– No cost-plus contracts: no DCAA-approved cost accounting systems; limited cost

insight– Contractor investment required– Each suppliers’ systems based on incremental modifications to systems already

flying/flown; have application or potential application to other markets– Enables SpaceX and Blue Origin participation (no DCAA approved cost accounting

system)• NASA estimates commercial approach has reduced cost for NASA and other

customers (NASA IG-18-016)– Introduction of competition– Increases flight rate/amortization of fixed costs over greater number of flights for each

supplier

Commercialization - DOD

10

• Addition of SpaceX to EELV program (2012) forced ULA to make significant cost reductions to compete

• Cost reduction initiatives reduced ULA prices by 50% between 2012 and present– Halving of ULA workforce (approx. 3,700 EP to 1,800 EP)– Consolidation/evolution of Atlas and Delta vehicles to Vulcan– Booster engine cost reduction/RD-180 replacement (BE-4 vs. AR-1)– Eliminate facilities (LC-37, SLC-6, Harlingen)

• Long term supplier partnerships (Blue Origin (BE4), AR (RL10), Ruag (Fairings/Composites), L3 (Avionics (INCA))

• EELV program transitioned to National Security Space Launch program (2019)– NSSL Phase 2: IDIQ Fixed-Price Contracts – fixed price per launch– ULA awarded 60% of future launches (8/7/2020) = ~20 launches

through 2027 (SpaceX awarded 40%)“Maintaining a competitive launch market, servicing both government and commercial customers, is how we encourage continued innovation on assured access to space.”• Dr. William Roper, Assistant Secretary of the Air Force for Acquisition, Technology and Logistics

Other Approaches –Insight/Oversight

11

• Most insight/oversight-type studies limited to impacts of Earned Value Management requirements– The "definitive" Coopers & Lybrand study in 1994 found a cost impact of up

to +18% of "value added" cost– Subsequent studies (circa 2017) say that the additional/incremental impact

has shrunk to very minimal since 1994- most contractors use EVM on all projects

– EXCEPT when the government “mis-applies” the requirements• Other Insight/Oversight aspects: Government Property, Customer

Interactions, Data Requirements– EXAMPLE: ATK -provided historical data “benchmarks” relative to contract

differences between Titan IV Solid Rocket Motor Upgrade (SRMU) and Shuttle RSRM and Constellation 1st Stage Booster

Total estimated labor headcount (cost) savings ~ 67% of selected departments

• Contract Type (RSRM = CPAF-prime with NASA, SRMU = FPI/CPFF-subcontract with Lockheed Martin)

• Customer Interactions/Expectations (“ATK interacts with ~200 NASA and DCMA customers . . . ATK interacted ~20 LM and DCMA customers”)

• Data Requirements (DRDs, CDRLs; 213 vs. 44)• Inspection Points/Gov’t Mandated Inspection Points (1,300 vs. 115)

Government-Owned (“G”) Corporations - Overview

• Top-level literature search of alternative potential contract structures revealed several options

• One possibly promising option: a Government corporation = “G-Corp” = “Corporations chartered by U.S. Congress”– Multiple organizational options; Lack of consistent G-Corp definition

• “An agency of Government established by Congress to perform a public purpose which provides a market-oriented service and produces revenue that meets or approximates its expenditures”

• “Separate legal entities that are created by Congress, generally with the intent of conducting revenue-producing commercial-type activities and are generally free from certain government restrictions related to personnel and procurement.”

– Examples: Tennessee Valley Authority, AMTRAK, Corporation for Public Broadcasting, Conrail, U.S. Enrichment Corp., In-Q-Tel (CIA)

• NOT same as a Government Sponsored Entity (GSE): Fannie Mae

12

Government-Owned (“G”) Corporations - Application

• Objective of forming a launch system G-Corp would presumably be to serve as transition path to eventual privatization– As opposed to a perpetuity G-Corp (e.g. TVA) or non-profit (e.g. In-Q-Tel,

Corporation for Public Broadcasting)• Examples of public to private transitional G-Corps

– Conrail: Formed in 1976 to “save” northeast U.S. freight rail system• Sold to Norfolk Southern and CSX in 1993, both companies are profitable

– U.S. Enrichment Corp: Privatize uranium enrichment operations to provide materials to meet DOD and commercial nuclear fuel needs

• Started 1993; bankruptcy reorganization 2013; now Centrus Energy, recently became profitable

• Attributes likely needed for use of a G-Corp as transition to privatization– Ability to offer end-to-end launch services– Financially competitive and/or offer unique service to space transportation

market– Longer term high probability profit-making market opportunities

• Presumably including, but not limited to NASA– Motivation for capital investment– Title transfer of assets: property, plant, equipment, Intellectual Property

13

Summary –Common Requirements

14

• Key requirements regardless of acquisition approach– Maintain safety

• Incentives and accountability• Maintain critical checks and balances

– Effective workforce transition• Minimize workforce disruption• Maintain critical skills at acceptable levels• Incentivize skill retention; attract new workers• Maximize knowledge transfer

– Incentivize Long-term commitment vs. Short-term profit• Incentive structures, asset transfer

• All while reducing recurring cost

Summary –Common Characteristics

15

• Program characteristics shared by essentially all alternative acquisition approaches

– System Optimized for Cost and Reliability• Not performance

– Evolution, not Revolution• Incremental Development Approach

– Commonality & Heritage - Components and Systems• Change one thing at a time

– No new technologies required - at least on critical path– Unity of Command

• One governing organization - the prime contractor– Accountability and Transparency– Limited External Dependencies– Insight/Oversight - Less is More

• Approach to oversight vs. number of overseers• Embedded oversight - attend all internal meetings/reviews (limited heads)• Minimal reporting requirements (e.g. Gov’t approved CDRL’s)

– Stable Funding– Fixed price with milestones/payment schedule

Summary –Observations

16

• Commercialization - Appears to offer best opportunity for significant reductions– Commercial approach has (reportedly) reduced cost for NASA and other customers– Introduction of competition increases flight rate/amortization of fixed costs over greater

number of flights for each supplier• NASA LSP: reduced Atlas V price $20M per launch• EELV/NSSL: reduced Atlas V price 50% per launch

– Important to not conflate cost and price – particularly in commercial market

• Contract Consolidation - Difficult to differentiate savings attributable to previous consolidation initiatives

– NASA-Shuttle: Columbia Accident Investigation Board (CAIB) and other studies noted that by early 2000’s downsizing had “gone to far” at which point NASA “reversed the trend”

– DOD-EELV: Contract consolidation did not reduce cost. Introduction of competition did.

• Insight/Oversight - Other programmatic and technical approaches appear to offer lesser opportunities for significant savings

– Depending on definition of “insight/oversight”, potential recurring cost reductions range from moderate to low relative to other alternatives

– Achievement of significant savings using these approaches will most likely depend on implementation of multiple integrated initiatives

• G-Corps – May offer “out-of-the-box” alternative acquisition approach to achieving lower cost launch services