hmv strategy analysis

DESCRIPTION

HMV Strategy AnalysisTRANSCRIPT

strategy analysis

FORMERLY THE LOBLAW GROUP

1. KIRAN CHADARAM 2. NIANJIU LI

3. VI NGO 4. SEBASTIEN ROSNER

5. VARUN SHARMA 6. JEREMY WONG

1 1 © 2012 SGMT 6000

HMV GROUP SUBJECT TO CLASS PEER EVALUATION, SEE PROFESSOR TAN’S INSTRUCTIONS

33⅓ R.P.M.

company background

• First store opened in 1921 (London, England) • Public company; headquartered in England

• 252 stores (UK, Ireland, Singapore, and Hong Kong)

• Entertainment retail: music, film, games, and music accessories/technologies

• HMV Live: owns venues, organizes concerts and festivals

• HMV Digital: online music sale

strategic issue

• Industry structural changes: online delivery (Apple iTunes) • Price competition against supermarkets (Tesco) and online

retailers (Amazon)

• Seasonal; 1/3 of sales in December

• Declining sales, negative net income, financial distress

• Divesting Live business; sold HMV Canada and Waterstone (book retail chain)

Re-focus on in-store experience and bank on technology sales OR change strategic direction?

external environment

• Consumers shunning high street retail

• Online piracy + streaming vs. owning

• Online downloads and streaming (e.g. Spotify, Songza, Pandora) increasingly popular

• Proliferation of mobile and social media

• Poor economy and tight access to cash

• iDevices + accessories, headphones, etc. growth market

industry analysis

• Industry: Entertainment retail

• Last 5 years: revenue fell at 6.0% per year

• Next 5 years: market will shrink by 1.7% per year

• Key success factors: adoption of technology, online presence, relationship with suppliers, copyright protection

• Life cycle: CD/DVD à decline, video games à maturity

• Highly-concentrated: Tesco, Amazon, Apple, HMV

• Products are “made for the internet”

main competitors

• Tesco:

• Supermarket • Sells CDs and DVDs as loss leaders • Price competition

• Amazon:

• Online retail • Sells physical and digital, at lower prices, with reviews and

recommendations • Price competition & differentiated services

• Apple:

• Online and store retail • Biggest seller of music player and mp3s (iPod and iTunes) • Differentiated products

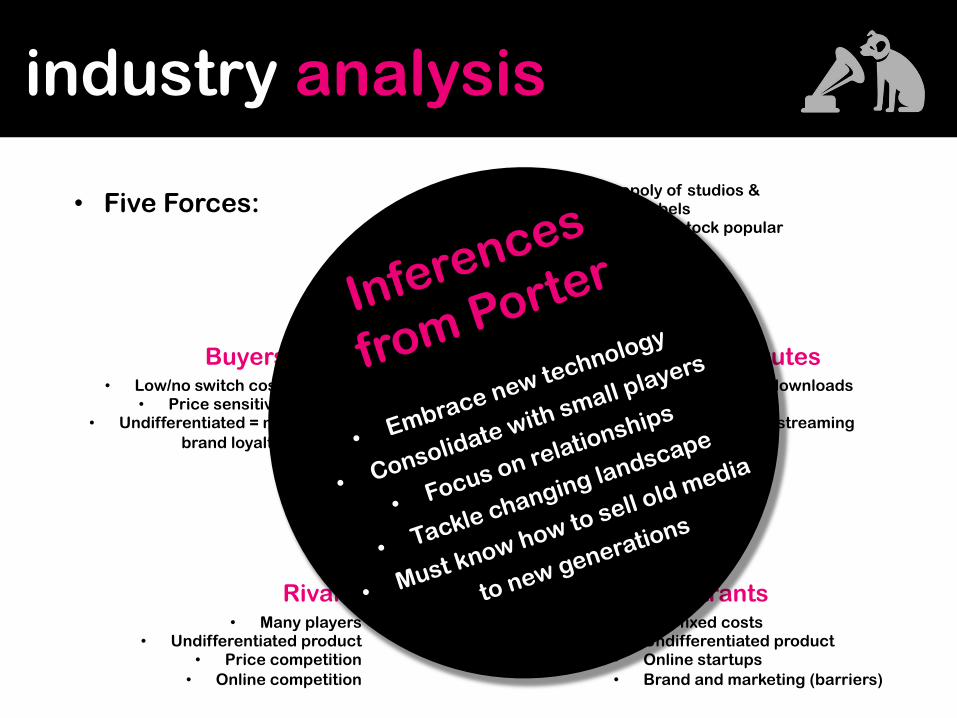

industry analysis

• Five Forces:

1

2

3

4

5 Suppliers

Substitutes

New Entrants Rivalry

Buyers

• Oligopoly of studios & record labels

• Store must stock popular items

• Legal downloads • Piracy • Online streaming

• Low fixed costs • Undifferentiated product • Online startups • Brand and marketing (barriers)

• Many players • Undifferentiated product

• Price competition • Online competition

• Low/no switch cost • Price sensitive

• Undifferentiated = no brand loyalty

industry analysis

• Five Forces:

1

2

3

4

5 Suppliers

Substitutes

New Entrants Rivalry

Buyers

• Oligopoly of studios & record labels

• Store must stock popular items

• Legal downloads • Piracy • Online streaming

• Low fixed costs • Undifferentiated product • Online startups • Brand and marketing (barriers)

• Many players • Undifferentiated product

• Price competition • Online competition

• Low/no switch cost • Price sensitive

• Undifferentiated = no brand loyalty

Inferences

from Porter

• Embrace new technology

• Consolidate with small players

• Focus on relationships

• Tackle changing landscape

• Must know how to sell old media

to new generations

internal environment

• Century-old brand, specialist reputation

• Industry experience (retail & live music)

• Solid relationship with artists, record labels, and studios

• Campaign and promotion experience

• Formerly owned by EMI; music in its DNA

• Laggard in the mp3 segment; not much success

value chain

Strong

• Marketing: brand • Procurement: artist and studio relations

• Sales: knowledgeable employees

• Operations: brick and mortar stores, locations Weak

• Technological Development: online presence

swot analysis

Strengths

• Established Brand • Great relationship with

artists, labels, and studios

• Industry expertise • Retail experience • Live events experience

Weaknesses

• Inadequate technological capability

• Inexperienced in online retail

• Seasonal business • Lack of cash

Opportunites

• Live concert streaming (untapped market)

• Niche markets (classical, jazz, audiophiles)

Threats

• Fierce competition • Changing consumer

preferences

alternative evaluation 1. Status Quo:

• Re-focus on core retail business and ride on growing technology sales; divest HMV Live

• Technology undifferentiated; future uncertain

2. Attack the Niche:

• Digital delivery of classical and jazz • Growing market of young listeners • Existing player: X5 Musical Group

3. Live Concert Streaming:

• Adapt to consumer preference for streaming • Uncontested market à first mover advantage • Leverage all strengths • No geographic barriers, revenue all year round • Will not cannibalize existing retail (studio-recorded)

recommendation 1. Status Quo:

• Re-focus on core retail business and ride on growing technology sales; divest HMV Live

• Technology undifferentiated; future uncertain

2. Attack the Niche:

• Digital delivery of classical and jazz • Growing market of young listeners • Existing player: X5 Musical Group

3. Live Concert Streaming:

• Adapt to consumer preference for streaming • Uncontested market à first mover advantage • Leverage all strengths • No geographic barriers, revenue all year round • Will not cannibalize existing retail (studio-recorded)

Unique

Position.

Awesome

Fit.

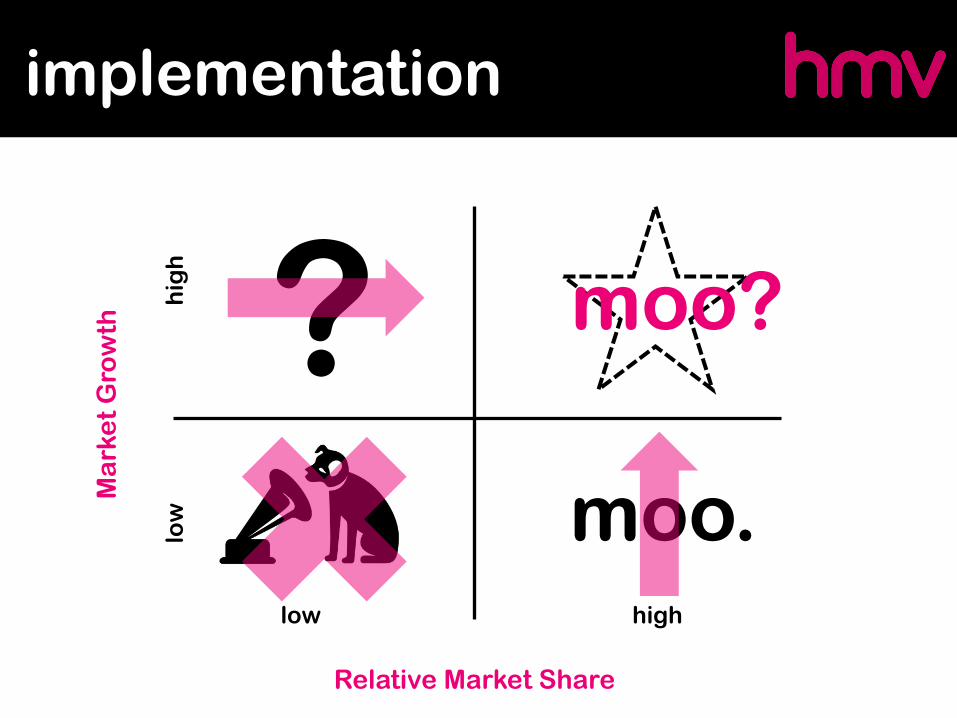

implementation

low high

low

h

igh

Relative Market Share

Ma

rke

t G

row

th ?

moo.

implementation

low high

low

h

igh

Relative Market Share

Ma

rke

t G

row

th ?

moo.

moo?

implementation

• Sell remaining venues to improve cash flow • Retain and revive HMV Live: keep talents who know the in’s

and out’s of running live concerts; maintain industry relations (artists and record labels)

• Negotiate and gain buy-in from artists and record labels

• Strategic alliances & joint ventures with small live streaming firms, e.g. Livestream.com, for missing technological capabilities (they need access to the labels)

• Synergy between retail and live business: share resources and capabilities (e.g. marketing, industry connections); develop cross-divisional teams

evaluation & control

• Cost may > revenue in the beginning; think long-term

• Monitor geographic and demographics trends

• Collect and analyze demand data; provide it to suppliers

• Make sure it does not hurt ticket sales, as implicitly promised

• Exit strategy: sell rights to or partner with Microsoft for its war against Apple? (Remember the Zune?)

thank you.

(sorry, no encores)