home buyer’s uide - title advantage buyers guide cfpb 2018.pdf · life of an escrow 15 title ......

TRANSCRIPT

Home Buyer’s Guide A Complete Guide To Help You Navigate The Home Buying Process

Including Consumer Financial Protection Bureau Information

Provided by Your Partners In Title & Escrow Protecting Your Property Rights

www.FirstCentennial.com

2018

Table of Contents

THE BUYING PROCESS

Important Contacts For Your Transaction 2

Buyer’s Needs Evaluation 3

Property Critique 4

The Buying Process 5-6

Homebuyer’s Glossary 7

The Inspection Process 8

THE LOAN PROCESS

THE ESCROW PROCESS

THE TITLE PROCESS

USEFUL INFORMATION & TIPS

Types of Loans 9

Outline of a Loan 10

The Loan Process 11

Information Needed at Loan Application 12

Mortgage Loan Points Explained 13

What is a Settlement Agent 14

Life of an Escrow 15

Title Insurance 16

What to Check on Every Preliminary Title Report 17

How You Take Title 18

Common Ways To Hold Title in Nevada 19

Important Terms to Know 20-21

Checklist for Moving 22

Moving Expenses and Taxes 23

First Centennial Title Consumer Discounts 24

Who Pays For What? 25

CFPB Website and Information 26

State of Nevada Title Guide

Dear Home Buyer, Thank you for giving me the opportunity to help guide you through your home buying process. It can be very confusing, sometimes complicated, and is always important to you, your family, your future and me. Please be assured you will receive my very best service incorporating all my experience and training to make a committed effort to have this process be understandable, hassle free and hopefully, a pleasure for all involved. So let’s get started! The information in the handbook will educate and assist you with the following:

Help determine your wants and needs Steps of the buying process Loan information Explaining the escrow and title process Physical inspections process Helpful Moving Tips

I look forward to working with you during the entire home buying process. I welcome any questions you may have after reading this information. Please feel free to contact me at anytime.

Home Buyer’s Guide

1

The Buying

Process

Real Estate Professional Title/Escrow

Contact:

Important Contacts for your Transaction

Name:

Company:

Address:

City/State/Zip:

Office:

Cell:

E-mail:

Fax:

Notes:

Name:

Company:

Address:

City/State/Zip:

Office:

Cell:

E-mail:

Fax:

Notes:

Name:

Company:

Address:

City/State/Zip:

Office:

Cell:

E-mail:

Fax:

Notes:

Name:

Company:

Address:

City/State/Zip:

Office:

Cell:

E-mail:

Fax:

Notes:

Contact:

2

Buyer’s Needs Evaluation Name (s): Address: Phone: (Home): (Work): Buyer 1: Buyer II: OWN RENT Children? YES NO If Yes, Ages: Why have you decided to move? When would you like to move? How long have you been looking? Describe your present home: What do you like most about your present home? What do you like least about your present home? Hobbies & special interests: Are there any particular areas, neighborhoods or homes you like? Is your home currently on the market? YES NO Needs & Wants: Bedrooms: Baths: Stories: Separate Dining Room Eat-in kitchen Family room Fireplace Acreage Transportation needs School district

3

Property Critique Below is a chart to help you compare and remember each property you preview.

Address:

Beds: Baths:

Sq. Ft.: F/P:

Living: Dining:

Address:

Beds: Baths:

Sq. Ft.: F/P:

Living: Dining:

Address:

Beds: Baths:

Sq. Ft.: F/P:

Living: Dining:

Address:

Beds: Baths:

Sq. Ft.: F/P:

Living: Dining:

PROS CONS

PROS CONS

PROS CONS

PROS CONS

4

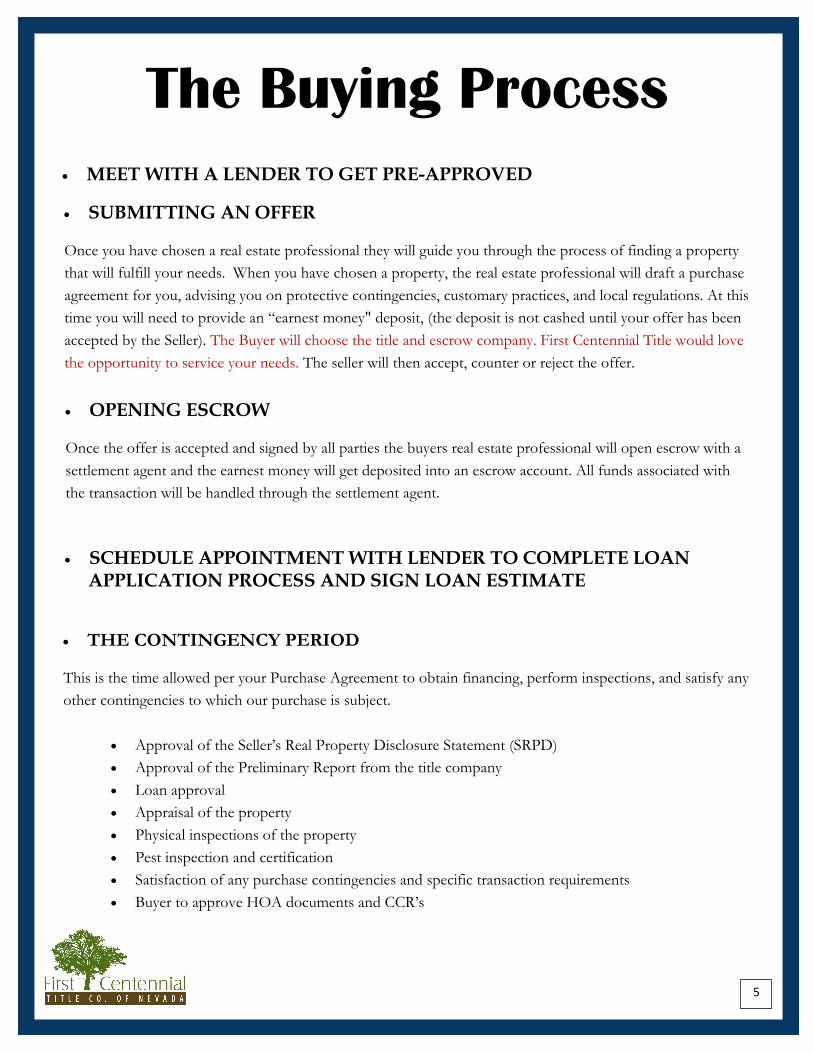

The Buying Process

SUBMITTING AN OFFER

Once you have chosen a real estate professional they will guide you through the process of finding a property

that will fulfill your needs. When you have chosen a property, the real estate professional will draft a purchase

agreement for you, advising you on protective contingencies, customary practices, and local regulations. At this

time you will need to provide an “earnest money" deposit, (the deposit is not cashed until your offer has been

accepted by the Seller). The Buyer will choose the title and escrow company. First Centennial Title would love

the opportunity to service your needs. The seller will then accept, counter or reject the offer.

OPENING ESCROW

Once the offer is accepted and signed by all parties the buyers real estate professional will open escrow with a

settlement agent and the earnest money will get deposited into an escrow account. All funds associated with

the transaction will be handled through the settlement agent.

THE CONTINGENCY PERIOD

This is the time allowed per your Purchase Agreement to obtain financing, perform inspections, and satisfy any

other contingencies to which our purchase is subject.

Approval of the Seller’s Real Property Disclosure Statement (SRPD)

Approval of the Preliminary Report from the title company

Loan approval

Appraisal of the property

Physical inspections of the property

Pest inspection and certification

Satisfaction of any purchase contingencies and specific transaction requirements

Buyer to approve HOA documents and CCR’s

MEET WITH A LENDER TO GET PRE-APPROVED

SCHEDULE APPOINTMENT WITH LENDER TO COMPLETE LOANAPPLICATION PROCESS AND SIGN LOAN ESTIMATE

5

The Buying Process (cont.) HOMEOWNERS INSURANCE Before the close of escrow the buyer must obtain homeowners insurance that is acceptable by the lender. The

real estate professional will coordinate between your insurance agent and the Escrow Officer to make sure

your policy is in effect at the close of escrow.

DOWN PAYMENT FUNDS You will need a cashier’s check or wire transfer several days prior to the closing date of escrow. Escrow will

provide a settlement statement with the required amount of funds needed to close including down payment

and closings costs.

SIGNING CLOSING DISCLOSURE/LOAN DOCUMENTS When all of the conditions of the Purchase Agreement have been met, you will either and/or receive your CD-

Closing Disclosure with a mandatory 3-day “review period” per the CFPB (Consumer Financial Protection

Bureau). Escrow usually sets up the appointment for your final signing.

CLOSING ESCROW After loan documents are signed, the buyer has deposited the remaining balance of funds needed to close and

all of the purchase agreement requirements have been met the lender will review the loan documents. If every-

thing is satisfactory, the lender will fund the loan. The Deed will then be recorded at the County Recorder’s

office and the buyer will take ownership of the home.

6

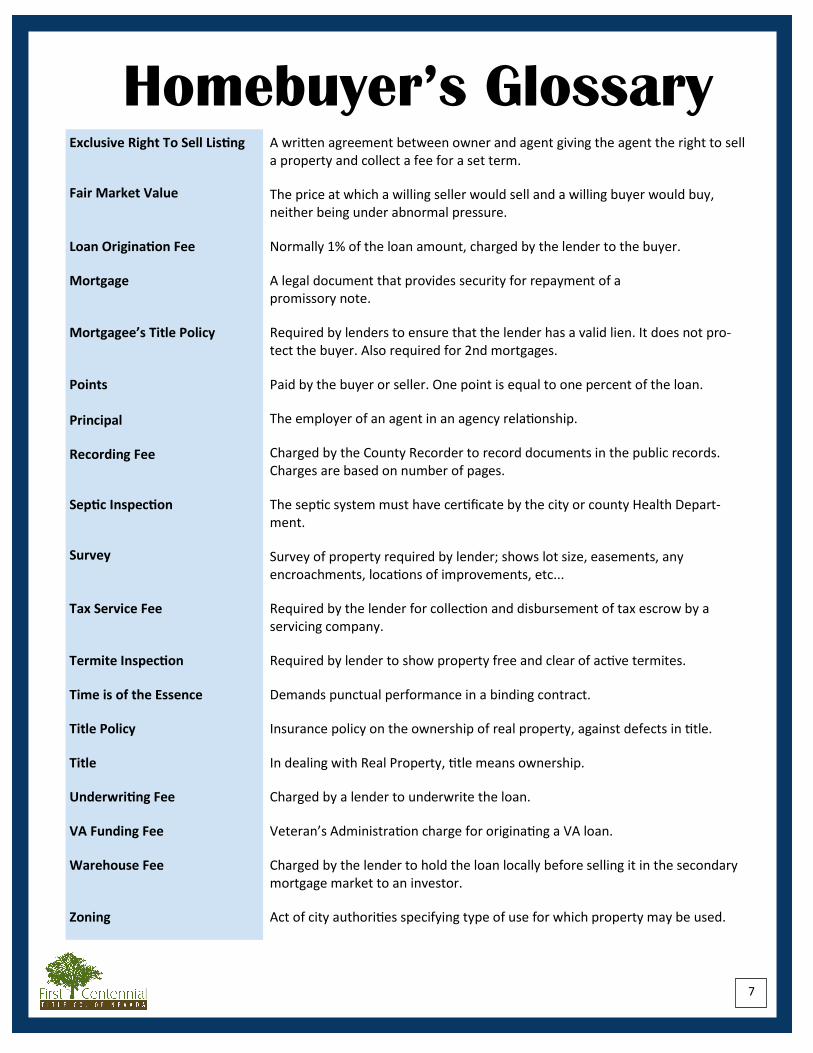

Exclusive Right To Sell Listing

Fair Market Value

Loan Origination Fee

Mortgage

Mortgagee’s Title Policy

Points

Principal

Recording Fee

Septic Inspection

Survey

Tax Service Fee

Termite Inspection

Time is of the Essence

Title Policy

Title

Underwriting Fee

VA Funding Fee

Warehouse Fee

Zoning

Homebuyer’s Glossary A written agreement between owner and agent giving the agent the right to sell a property and collect a fee for a set term.

The price at which a willing seller would sell and a willing buyer would buy, neither being under abnormal pressure.

Normally 1% of the loan amount, charged by the lender to the buyer.

A legal document that provides security for repayment of a promissory note.

Required by lenders to ensure that the lender has a valid lien. It does not pro-tect the buyer. Also required for 2nd mortgages.

Paid by the buyer or seller. One point is equal to one percent of the loan.

The employer of an agent in an agency relationship.

Charged by the County Recorder to record documents in the public records. Charges are based on number of pages.

The septic system must have certificate by the city or county Health Depart-ment.

Survey of property required by lender; shows lot size, easements, any encroachments, locations of improvements, etc...

Required by the lender for collection and disbursement of tax escrow by a servicing company.

Required by lender to show property free and clear of active termites.

Demands punctual performance in a binding contract.

Insurance policy on the ownership of real property, against defects in title.

In dealing with Real Property, title means ownership.

Charged by a lender to underwrite the loan.

Veteran’s Administration charge for originating a VA loan.

Charged by the lender to hold the loan locally before selling it in the secondary mortgage market to an investor.

Act of city authorities specifying type of use for which property may be used.

7

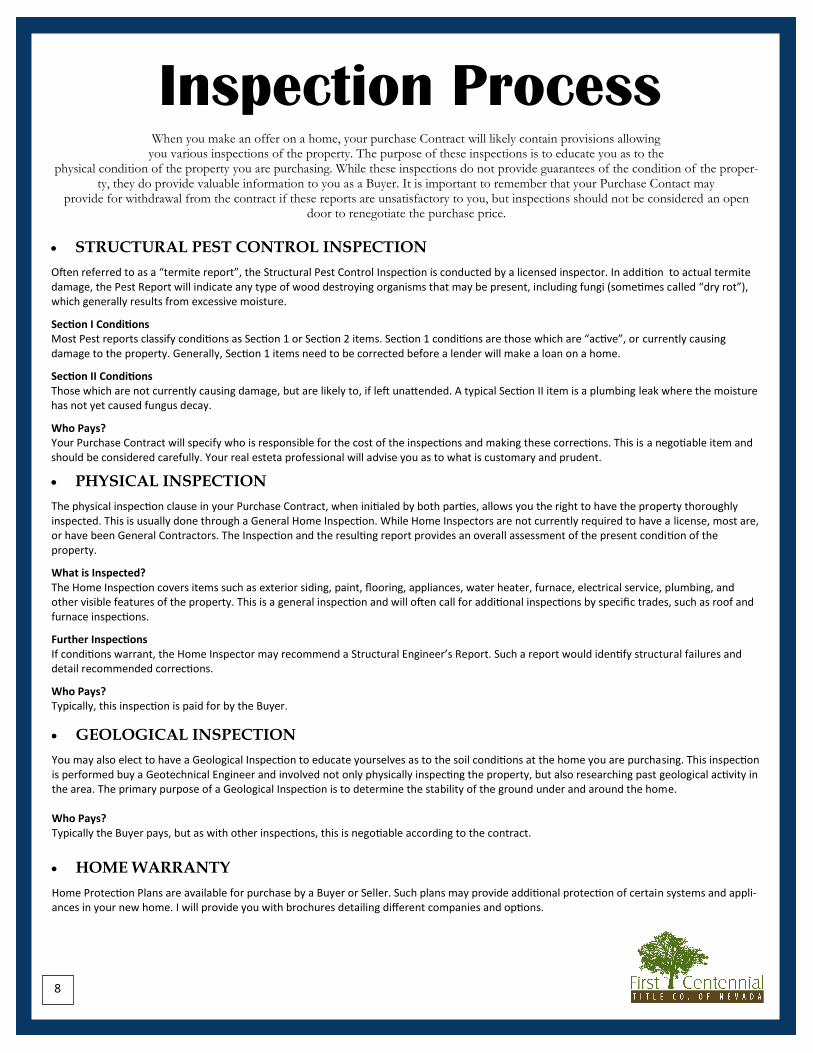

Inspection Process When you make an offer on a home, your purchase Contract will likely contain provisions allowing

you various inspections of the property. The purpose of these inspections is to educate you as to the physical condition of the property you are purchasing. While these inspections do not provide guarantees of the condition of the proper-

ty, they do provide valuable information to you as a Buyer. It is important to remember that your Purchase Contact may provide for withdrawal from the contract if these reports are unsatisfactory to you, but inspections should not be considered an open

door to renegotiate the purchase price.

STRUCTURAL PEST CONTROL INSPECTION

Often referred to as a “termite report”, the Structural Pest Control Inspection is conducted by a licensed inspector. In addition to actual termite damage, the Pest Report will indicate any type of wood destroying organisms that may be present, including fungi (sometimes called “dry rot”), which generally results from excessive moisture.

Section I Conditions Most Pest reports classify conditions as Section 1 or Section 2 items. Section 1 conditions are those which are “active”, or currently causing damage to the property. Generally, Section 1 items need to be corrected before a lender will make a loan on a home.

Section II Conditions Those which are not currently causing damage, but are likely to, if left unattended. A typical Section II item is a plumbing leak where the moisture has not yet caused fungus decay.

Who Pays? Your Purchase Contract will specify who is responsible for the cost of the inspections and making these corrections. This is a negotiable item and should be considered carefully. Your real esteta professional will advise you as to what is customary and prudent.

PHYSICAL INSPECTION

The physical inspection clause in your Purchase Contract, when initialed by both parties, allows you the right to have the property thoroughly inspected. This is usually done through a General Home Inspection. While Home Inspectors are not currently required to have a license, most are, or have been General Contractors. The Inspection and the resulting report provides an overall assessment of the present condition of the property.

What is Inspected? The Home Inspection covers items such as exterior siding, paint, flooring, appliances, water heater, furnace, electrical service, plumbing, and other visible features of the property. This is a general inspection and will often call for additional inspections by specific trades, such as roof and furnace inspections.

Further Inspections If conditions warrant, the Home Inspector may recommend a Structural Engineer’s Report. Such a report would identify structural failures and detail recommended corrections.

Who Pays? Typically, this inspection is paid for by the Buyer.

GEOLOGICAL INSPECTION

You may also elect to have a Geological Inspection to educate yourselves as to the soil conditions at the home you are purchasing. This inspection is performed buy a Geotechnical Engineer and involved not only physically inspecting the property, but also researching past geological activity in the area. The primary purpose of a Geological Inspection is to determine the stability of the ground under and around the home. Who Pays? Typically the Buyer pays, but as with other inspections, this is negotiable according to the contract.

HOME WARRANTY

Home Protection Plans are available for purchase by a Buyer or Seller. Such plans may provide additional protection of certain systems and appli-ances in your new home. I will provide you with brochures detailing different companies and options.

8

The Loan

Process

Adjustable Rate Mortgage

Balloon Payment Loan

Buy-Down Loan

Community Homebuyer’s Program

Conventional Loan

FHA Loan

Fixed Rate Loan

Graduated Payment Mortgage

Non-Qualifying Loan (Assumable)

VA Loan

Types of Loans Adjustable rate mortgages have an interest rate that is adjusted at certain intervals based on a specific index during the life of the loan.

A fixed rate loan that is amortized over 30 years but becomes due and payable at the end of a certain time. May be extendible or may roll-over into another type of loan.

Buy-Down loans are fixed rate loans where the interest rate and the payment are reduced for a specific period of time by paying the interest up front to subsidize the lower payment.

A fixed rate loan for first time buyers with a low down payment, usually 3-5%, no cash reserve requirement and easier qualifying ratios. Subject to borrower meeting income limits and attendance of a four hour training course on home ownership.

Conventional loans are sometimes more lenient with the appraisal and condition of the property. When you are buying a “fixer upper” you may need to use a conventional loan. Homes purchased above the FHA loan limit are usually financed with conventional loans.

FHA loans are insured by the Federal Housing Administration under H.U.D. They offer a low down payment and are easier to qualify for than conventional loans.

A fixed rate loan has one interest rate that remains constant through-out the life of the loan.

A fixed rate loan that has payments starting lower than a standard fixed rate loan, which then increases by a predetermined amount each year for a set number of years.

Non-Qualifying loans are pre-existing loans which can be assumed by a buyer from the seller of a property without going through the qualifying process. The buyer pays the seller for their equity and then starts making payments.

VA loans are guaranteed by the Veterans Administration. A veteran must have served 180 days active service.

9

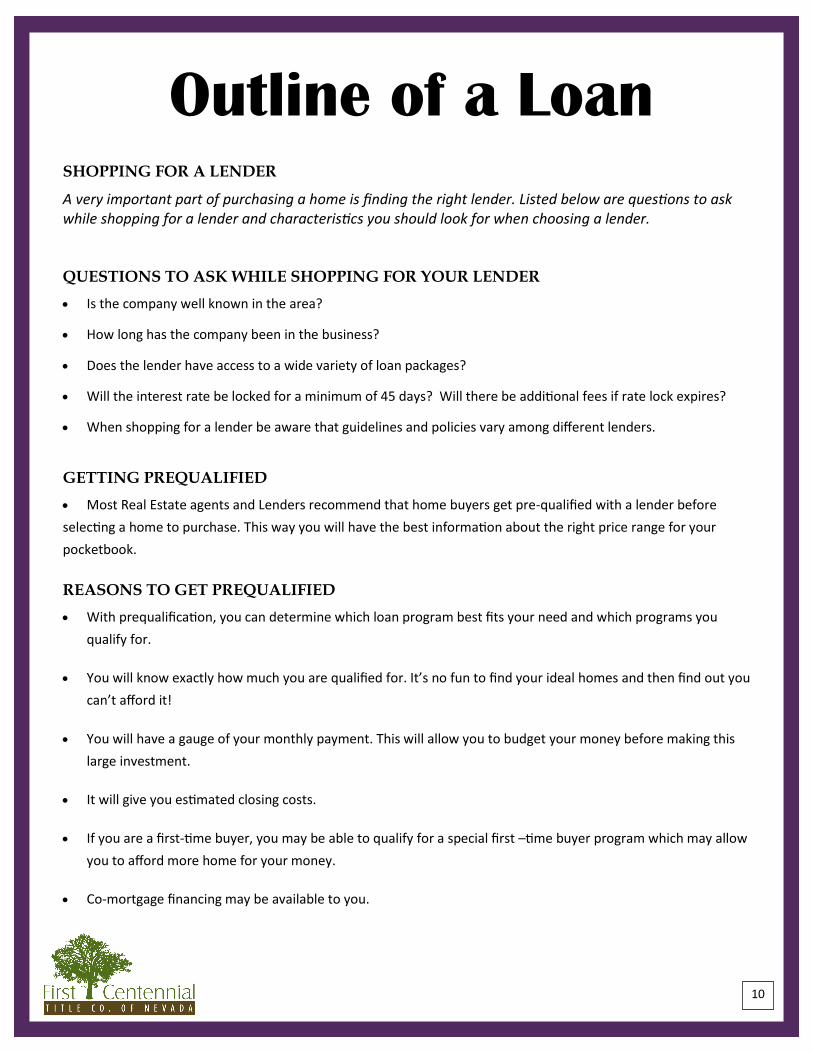

SHOPPING FOR A LENDER

A very important part of purchasing a home is finding the right lender. Listed below are questions to ask while shopping for a lender and characteristics you should look for when choosing a lender. QUESTIONS TO ASK WHILE SHOPPING FOR YOUR LENDER

Is the company well known in the area?

How long has the company been in the business?

Does the lender have access to a wide variety of loan packages?

Will the interest rate be locked for a minimum of 45 days? Will there be additional fees if rate lock expires?

When shopping for a lender be aware that guidelines and policies vary among different lenders.

GETTING PREQUALIFIED

Most Real Estate agents and Lenders recommend that home buyers get pre-qualified with a lender before

selecting a home to purchase. This way you will have the best information about the right price range for your

pocketbook.

REASONS TO GET PREQUALIFIED

With prequalification, you can determine which loan program best fits your need and which programs you

qualify for.

You will know exactly how much you are qualified for. It’s no fun to find your ideal homes and then find out you

can’t afford it!

You will have a gauge of your monthly payment. This will allow you to budget your money before making this

large investment.

It will give you estimated closing costs.

If you are a first-time buyer, you may be able to qualify for a special first –time buyer program which may allow

you to afford more home for your money.

Co-mortgage financing may be available to you.

Outline of a Loan

10

PRE-APPROVAL/INTERVIEW

Buyer to schedule appointment with their lender to completeloan application upon offer and acceptance.

Sign loan estimate

SIGNED LOAN SUBMISSION SIGNED LOAN ESTIMATE (Letter of Intent) We recommend this be signed upon delivery or as soon as possible. This intent to proceed document is not binding. This document was added in 2010 when the GFE was revamped (there is no signature line on the GFE). Typically the only fees you would be “on the hook” for would be the appraisal if one was done and possibly a credit report fee. Also some banks charge a non-refundable application fee. If you do withdraw, be sure to inform your Broker so that work can cease on your file. Loan Estimate (LE): Form designed to provide disclosure that will be helpful to consumers in understanding the key features, costs and risks of the mortgage loan for which they are applying. Initial disclosure to be given to the consumer three (3) business days after applications and replaces the GFE and early TIL. In addition DON’T FORGET: These are requested items upfront for the most accurate Closing Disclosure: SRPD, Inspections, Repairs, Withholds, HOA info, Home Warranty

DOCUMENTATION Supporting documents come in Lender checks on any problems Requests for any additional items are made

LOAN APPROVAL Parties are notified of approval

DOCUMENTS ARE DRAWN Loan documents are completed and sent to escrow Borrowers come in for final signatures

FUNDING Lender reviews the loan package Funds are transferred by wire

RECORDING OF DOCUMENTS First Centennial Title records the Deed of trust at the County Recorder’s office. Escrow is now officially closed.

The Loan Process

CLOSING DISCLOSURE (CD) Will be Issued by the Lender to the Borrower The Closing Disclosure form is designed to provide disclosures that will be helpful to

consumers in understanding all of the costs of the transaction. This form will be given to the consumer three (3) business days before closing and replaces the HUD-1 and final Truth

in Lending (TIL) disclosure on impacted transactions.

CONGRATULATIONS! YOU ARE A PROUD HOMEOWNER! 11

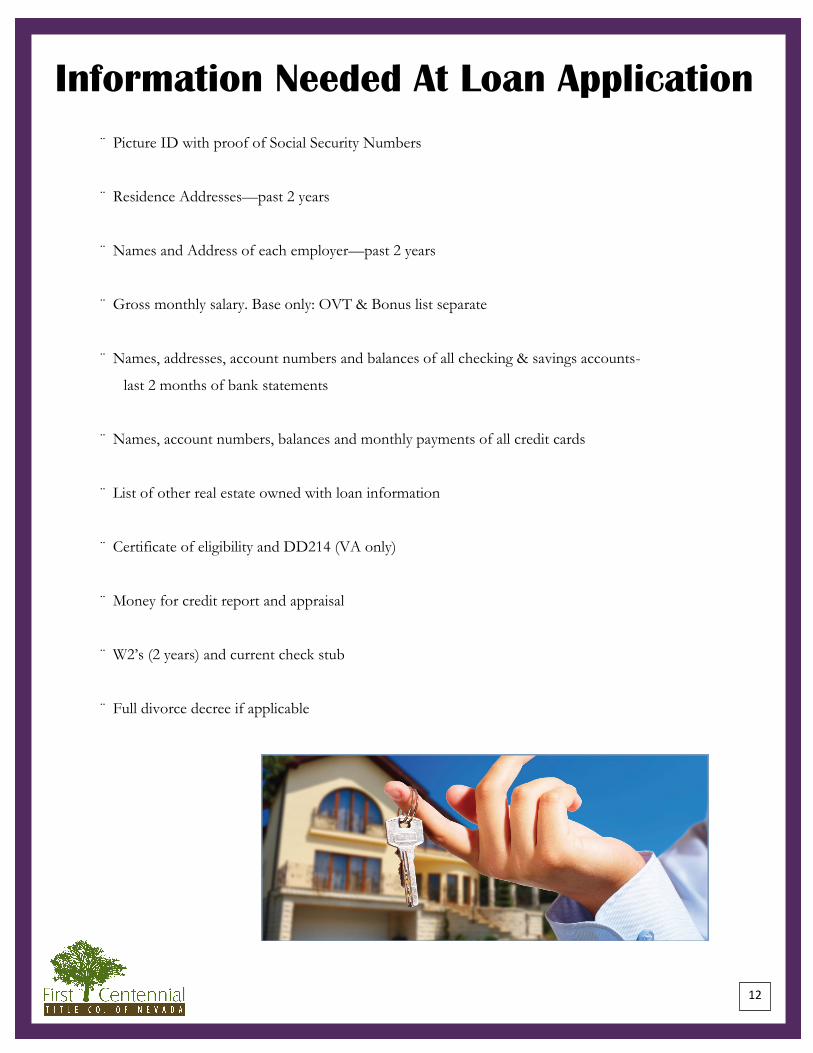

¨ Picture ID with proof of Social Security Numbers

¨ Residence Addresses—past 2 years

¨ Names and Address of each employer—past 2 years

¨ Gross monthly salary. Base only: OVT & Bonus list separate

¨ Names, addresses, account numbers and balances of all checking & savings accounts-

last 2 months of bank statements

¨ Names, account numbers, balances and monthly payments of all credit cards

¨ List of other real estate owned with loan information

¨ Certificate of eligibility and DD214 (VA only)

¨ Money for credit report and appraisal

¨ W2’s (2 years) and current check stub

¨ Full divorce decree if applicable

Information Needed At Loan Application

12

What is a Point? One point is equal to 1% of the NEW Loan Amount.

Why do Lenders charge Points? Whenever governmental regulation, state usury law and/or competitive practices prohibit the lender from charging a rate of interest which would make the real estate loan competitive with other fields of investments, the lender must seek some method of increasing the yield for the investors. By charging “points”, the lender can bring the real estate loan up to those other investments.

Are points called by different names? Yes. Loan Origination Fee, Commitment Fee, Discount Fee, Warehousing Fee, Funding Fee, etc.

Who must pay the points? FHA: the buyer is usually charged with the Loan Origination Fee; the Discount Fee can be paid by the Buyer or Seller. VA: the Buyer is usually charged with the Loan Origination Fee and the Funding Fee. Conventional: points can be paid by the Buyer, the Seller, or split between the two. State on Contract of Sale! City/County/State government sponsored loans: as published by them.

Do the number of points charged fluctuate? Yes. If the rates on mortgage loans are lower that other investments (such as stocks, bonds, etc.) then funds will be drawn away from the mortgage market. Also, when there is a heavy demand upon the money market because of business needs, role requirements or other government borrowing, the result is that money for home mortgages become scarce and more expensive. When this occurs, more points can be charged. Points balance the market. Points are not set by government regulation but by each lender individually.

On VA loans, is there any way to lock in the number of points? Not without jeopardizing the sale. Even when a lender stipulates in writing the number of points to be charged, that guarantee states “if the interest rate is not changed by the government”. Points charged on an FHA or conventional loan are usually not changed from commitment time to settlement.

Is FHA or VA financing unfair to sellers? No. Homes can sell faster because more buyers can qualify with the lower down payment requirement, lower interest rate, long term loans with lower monthly payments. Sellers receive all cash for their equity to reinvest in a new home or other investment. The purpose of these loans is to provide purchasers the opportunity to buy homes with minimal cash investment this providing a bigger market for sellers.

Are points deductible for income tax purposes? Points on a home mortgage (for the purchase or improvement of, and secured by, the taxpayer’s principal residence) are deductible currently if points are generally charged in the geographical area where the loan is made and to the extent of the number of points generally charged in that area for a home loan. If you are in doubt about points being deductible you should contact your tax return preparer.

Mortgage Loan Points Explained

13

The Escrow

Process

An Escrow/Settlement Agent is an independent, impartial “stakeholder” account and is the vehicle by which the interests of all parties to the transaction are protected.

The Escrow is created after you execute the contract of sale of your home and becomes the depository for all

monies, instructions and documents pertaining to the sale of said property. Some aspects of the sale are not

part of the escrow. For example, the buyer and seller must decide which fixtures or personal property are

included in the sale agreement. Similarly, loan negotiations occur between the buyer and the lender. Your

real estate agent can guide you in these non-escrow matters.

How does the escrow process work?The Escrow Officer/Settlement Agent takes instructions based on the terms of your Purchase Agreement and

the lenders' requirements. The escrow officer can hold inspection reports and bills for work performed as

required by the Purchase Agreement. Other elements of the escrow include hazard and title insurance, and the

grant deed from seller to you. Escrow cannot be completed until these items have been satisfied and all parties

have signed escrow documents.

How do I open escrow?Either real estate agent may open escrow. As soon as you execute the Purchase agreement, your agent will

place your initial deposit into an escrow account at the escrow/settlement company.

How do I know where my money goes?Written evidence of the deposit is generally included in your copy of the sales contact. The funds will then be

deposited in a separate escrow or trust account. You will receive a receipt for the funds from the escrow

company.

What information do I need to provide?You will be asked to complete a statement of identity as part of the paperwork. Because many people have the

same name, the Statement of Identity is used to identify the specific person in the transactions through such

information as date of birth, social security number etc. This information is considered confidential.

Homeowner’s documents and CCR’s must be ordered and reviewed

How long is the escrow?The amount of time necessary to complete an escrow is determined by the terms of the Purchase Agreement.

It is normally 45 to 60 days, but can range from a few days to a few months.

What Is a Settlement agent?

14

Life of an Escrow Prepare Escrow Instructions

& pertinent documents

Obtain signatures

Order Title Search

Request demands (if any) Request clarification of other

Liens (if any) & review Taxes on report

Obtain funds and signatures from Buyer

Review to determine that all conditions have been met & that all documents are correct and available for signature. (Termite inspection, contingencies

released, fire insurance ordered, additional documents second deed of trust, bill of sale, etc. have been prepared.)

Process financing

Request or prepare new loan application

Closing Disclosure Delivered CFPB mandatory three(3)

day review

Forward documents to Title Company

Timeline may vary w/Lender

Fund & order recording

Return loan documents and CD Timeline may vary w/Lender

Close file, prepare statements and disburse funds

Obtain loan approval & determine that terms

are correct

Request loan funds

Receive & review Preliminary Report

Receive demands and enter into file Request loan documents

Request Beneficiary Statement

Receive Beneficiary Statement & enter into file. Review terms of transfer & current payment

status. (if prior approval necessary to record)

Complete closing. Forward final documents to all interested parties (Buyer-Seller-Lender)

15

The Title

Process

Many home buyers just assume that when they purchase a piece of property, possession of the deed to the property is all they need to prove ownership. This is not true. Hidden hazards may attach to real estate. A property owner’s greatest protection is a policy of title insurance.

What Is Title Insurance?

It is a contract of indemnity which guarantees that the title is as reported and, if not reported and the owner is damaged, the title policy covers the insured for their loss up to the amount of the policy.

Title insurance assures owners that they are acquiring marketable title. Title insurance is designed to eliminate risk or loss caused by defects in title from the past. Title insurance provides coverage only for title problems which were already in existence at the time the policy was issued.

The Title Search

Title companies work to eliminate risks by performing a search of the public records or through the title company’s own plant. The search consists of public records, laws and court decisions pertaining to the property to determine the current recorded ownership, any recorded liens or encumbrances or any other matters of record which could affect the title to the property. When a title search is complete, the title company issues a preliminary report detailing the current sta-tus of title.

The Preliminary Report

A preliminary report contains vital information which can affect the close of escrow: Ownership of the subject property; where the current owners hold title; matters of record that specifically affect the subject property or the owners of the property; a legal description of the property and an informational plat map.

Title Insurance

16

The preliminary report indicated the type of title insurance offered by the title company. It also

indicates the exclusions and exceptions from coverage under which the policy will be issued.

VESTING - Make sure the names on the preliminary Report are the correct names and that the property is

the same as the property on the purchase contract.

TAXES AND ASSESSMENTS - Look for an exemption or classification designation that would change the

tax amount as a result of the sale.

DEED OF TRUST - Make sure all paid off Deeds of Trust are reconveyed. Upon proof of payment and/or an

indemnity, the title company may insure around the encumbrance.

IDENTITY MATTERS - A “Statement of Information” can clear up identity issues that may arise. If there

are judgments and liens that belong to the party in question and have been paid then a release or satisfaction

must be obtained and recorded or files to eliminate the matter.

PENDING ACTIONS - A civil action affecting real property generally will have to be dismissed before title

can insure. A divorce or probate doesn’t have to be finalized but special requirements may exist. Check with

your Title Rep or Title Officer for more information.

JOINT USE MATTERS - Driveways, party walls and easements may prompt Lenders to require a joint

maintenance agreement. The preliminary report will show such agreements if one is of record.

EXTENDED COVERAGE MATTERS - If a physical inspection of the subject property discloses encroach-

ments, lien rights, or other matters, these must be addressed before the lender will close. An extended cover-

age owners policy may be requested and a survey of the property will be required.

LEGAL DESCRIPTION - The legal description should be always be compared to the legal description in the

purchase and sale agreement to be sure that all the property being conveyed had been included in the

preliminary report.

What to Check on Every

Preliminary Report

17

1

HOW YOU TAKE TITLEHOW YOU TAKE TITLEHOW YOU TAKE TITLE

Advantages and Limitations

Title to real property in Nevada may be held by

individuals, either in Sole Ownership or in Co-Ownership.

Co-Ownership of real property occurs when title is held by

two or more persons. There are several variations as to

how title may be held in each type of ownership. The

following brief summaries reference eight of the more

common examples of Sole Ownership and Co-Ownership.

2

4

3

SOLE OWNERSHIP

A Single Man/Woman

A man or woman who is not legally married.

Example: John Doe, a single man.

An Unmarried Man/Woman

A man or woman, who having been married is legally

divorced. Example: Joe Doe, an unmarried man.

A Married Man/Woman, As His/Her Sole And

Separate Property

When a married man or woman wishes to acquire title in

his or her name alone, the spouse must consent, by

quitclaim deed or otherwise, to transfer thereby

relinquishing all right, title and interest in the property.

Example: John Doe, a married man, as his sole and sep-

arate property.

CO-OWNERSHIP

Community Property

Nevada defines community property acquired by husband

and wife, or by either. Real property conveyed to a married

man or woman is presumed to be community property,

unless otherwise stated. Under community property, both

spouses have the right to dispose of one half of the

community property. If a spouse does not exercise his/her

right to dispose of one-half to someone other than his/her

spouse, then the one-half will go to the surviving spouse

without administration. If a spouse exercises his/her right

to dispose of one-half, that half is subject to administration

in the estate. Example: John Doe & Mary Doe, husband and

wife. Example: John Doe, a married man.

5

6

7

8

Joint Tenancy

A joint tenancy estate is defined as follows: “ A joint interest

is one owned by two or more persons in equal shares, by a

title created by a single will or transfer, when expressly

declared in the will or transfer to be a joint tenancy.” A chief

characteristic of joint tenancy property is the right of

survivorship. When a joint tenant dies, title to the property

immediately vests in the surviving joint tenants (s). As a

consequence, joint tenancy property is not subject to

disposition by will. Example: John Doe and Mary Doe,

husband and wife, as joint tenants.

Tenancy In Common

Under tenancy in common, the co-owners own undivided

interests; but unlike joint tenancy, these interests need not

be equal in quantity or duration, and may arise at different

times. There is no right or survivorship; each tenant owns an

interest which, on his or her death, vests in his or her heirs

or devisees. Example: John Doe, a single man, as to an

undivided 3/4ths interest, and George Smith, a single man,

as to an undivided 1/4th interest, as tenants in common.

Trust

Title to real property may be held in a title holding trust. The

trust holds legal and equitable title to the real estate. The

trustee holds title for the trust/beneficiary who retains all of

the management rights and responsibilities.

Community Property With Right of Survivorship

Community Property of a husband and wife, when expressly

declared in the transfer document to be community property

with the right of survivorship, and which may be accepted in

writing on the face of the document by a statement signed

or initialed by the grantees, shall, upon the death of one of

the spouses, pass to the survivor, without administration,

subject to the same procedures as property held in joint

tenancy.

The preceding summaries are a few of the more common

ways to take title to real property in Nevada and are

provided for informational purposes only. For a more

comprehensive understanding of the legal and tax

consequences, appropriate consultation is recommended.

There are significant tax and legal consequences on how

you hold title. We strongly suggest contacting an attorney

and/or CPA for specific advise on how you should actually

vest your title.

This chart is made available for information purposes only. FCT deems its contents to be true and correct, however, certain personal circumstances may effect the above information. We encourage you to seek advise from your Attorney or Certified Public Accountant to assist you in determining the best way for you to hold title.

19

Useful Info

And Tips

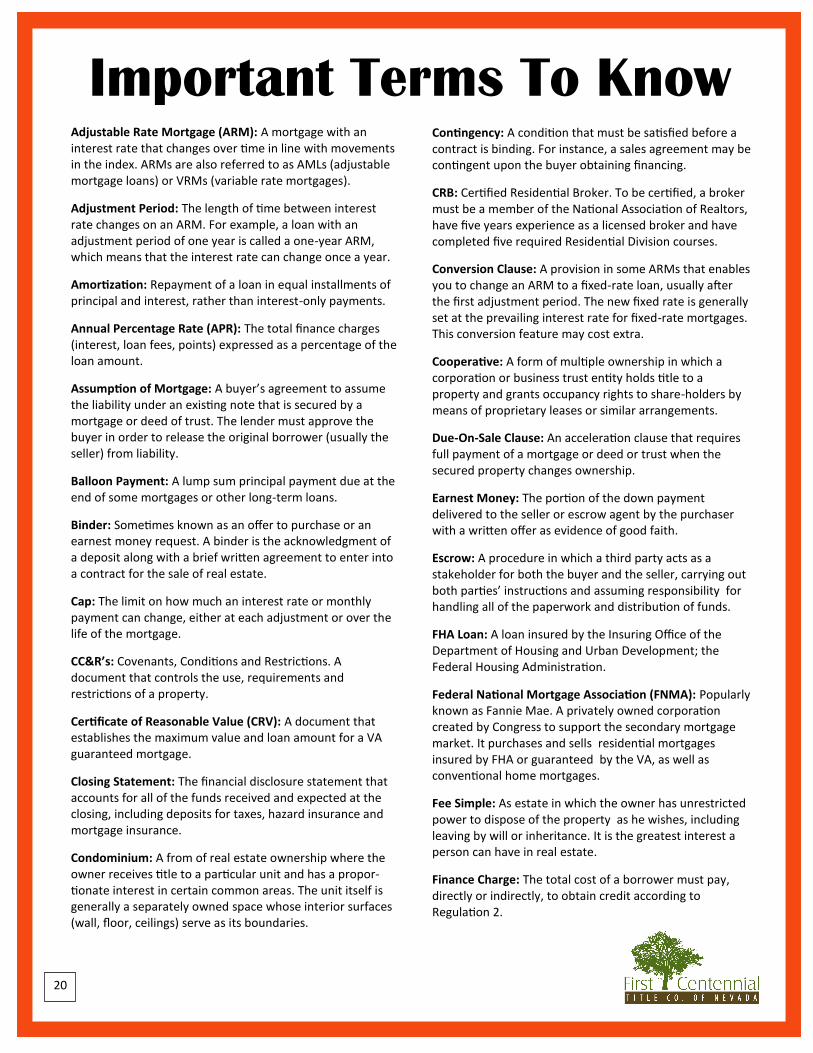

Important Terms To Know Contingency: A condition that must be satisfied before a contract is binding. For instance, a sales agreement may be contingent upon the buyer obtaining financing.

CRB: Certified Residential Broker. To be certified, a broker must be a member of the National Association of Realtors, have five years experience as a licensed broker and have completed five required Residential Division courses.

Conversion Clause: A provision in some ARMs that enables you to change an ARM to a fixed-rate loan, usually after the first adjustment period. The new fixed rate is generally set at the prevailing interest rate for fixed-rate mortgages. This conversion feature may cost extra.

Cooperative: A form of multiple ownership in which a corporation or business trust entity holds title to a property and grants occupancy rights to share-holders by means of proprietary leases or similar arrangements.

Due-On-Sale Clause: An acceleration clause that requires full payment of a mortgage or deed or trust when the secured property changes ownership.

Earnest Money: The portion of the down payment delivered to the seller or escrow agent by the purchaser with a written offer as evidence of good faith.

Escrow: A procedure in which a third party acts as a stakeholder for both the buyer and the seller, carrying out both parties’ instructions and assuming responsibility for handling all of the paperwork and distribution of funds.

FHA Loan: A loan insured by the Insuring Office of the Department of Housing and Urban Development; the Federal Housing Administration.

Federal National Mortgage Association (FNMA): Popularly known as Fannie Mae. A privately owned corporation created by Congress to support the secondary mortgage market. It purchases and sells residential mortgages insured by FHA or guaranteed by the VA, as well as conventional home mortgages.

Fee Simple: As estate in which the owner has unrestricted power to dispose of the property as he wishes, including leaving by will or inheritance. It is the greatest interest a person can have in real estate.

Finance Charge: The total cost of a borrower must pay, directly or indirectly, to obtain credit according to Regulation 2.

Adjustable Rate Mortgage (ARM): A mortgage with an interest rate that changes over time in line with movements in the index. ARMs are also referred to as AMLs (adjustable mortgage loans) or VRMs (variable rate mortgages).

Adjustment Period: The length of time between interest rate changes on an ARM. For example, a loan with an adjustment period of one year is called a one-year ARM, which means that the interest rate can change once a year.

Amortization: Repayment of a loan in equal installments of principal and interest, rather than interest-only payments.

Annual Percentage Rate (APR): The total finance charges (interest, loan fees, points) expressed as a percentage of the loan amount.

Assumption of Mortgage: A buyer’s agreement to assume the liability under an existing note that is secured by a mortgage or deed of trust. The lender must approve the buyer in order to release the original borrower (usually the seller) from liability.

Balloon Payment: A lump sum principal payment due at the end of some mortgages or other long-term loans.

Binder: Sometimes known as an offer to purchase or an earnest money request. A binder is the acknowledgment of a deposit along with a brief written agreement to enter into a contract for the sale of real estate.

Cap: The limit on how much an interest rate or monthly payment can change, either at each adjustment or over the life of the mortgage.

CC&R’s: Covenants, Conditions and Restrictions. A document that controls the use, requirements and restrictions of a property.

Certificate of Reasonable Value (CRV): A document that establishes the maximum value and loan amount for a VA guaranteed mortgage.

Closing Statement: The financial disclosure statement that accounts for all of the funds received and expected at the closing, including deposits for taxes, hazard insurance and mortgage insurance.

Condominium: A from of real estate ownership where the owner receives title to a particular unit and has a propor-tionate interest in certain common areas. The unit itself is generally a separately owned space whose interior surfaces (wall, floor, ceilings) serve as its boundaries.

20

Important Terms To Know (cont.)

Origination Fee: A fee or charge for work involved in evalu-ating, preparing, and submitting a purposed mortgage loan. The fee is limited to 1 percent for FHA and VA loans.

PITI: Principal, interest, taxes and insurance.

Planned Unity Development (PUD): A zoning designation for property developed at the same or slightly greater overall density that conventional development, sometimes with improvements clustered between open and common areas. Uses may be residential, commercial or industrial.

Point: An amount equal to 1 percent of the principal amount of the investment or note. The lender assesses loan discount points at closing to increase the yield on the mortgage to a position competitive with other types of investments.

Prepayment Penalty: A fee charged to a mortgager who pays a loan before its due. Not allowed for FHA or VA loans.

Private Mortgage Insurance (PMI): Insurance written by a private company protecting the lender against loss if the borrower defaults on the mortgage.

Purchase Agreement: A written document in which the purchaser agrees to buy certain real estate and the seller agrees to sell under stated terms and conditions. Also called a sales contract, earnest money contract, or agree-ment for sale.

Realtor: A real estate broker or associate active in the local real estate board affiliated with the National Association of Realtors.

Regulation Z: The set of rules governing consumer lending issued by the Federal Reserve Board of Governors in ac-cordance with the Consumer Protection Act.

Tenancy in Common: A type of joint ownership of property by two or more persons with no right of survivorship.

Title Insurance Policy: A policy that protects the purchaser, mortgagee or other party against losses.

VA Loan: A loan that is partially guaranteed my the Veter-ans Administration and made by a private lender.

Graduated Payment Mortgage: A residential mortgage with monthly payments that start at a low level and increase at a predetermined rate.

GRI: Graduate, Realtors Institute: A professional designa-tions granted to a member of the National Association of Realtors who has successfully completed twelve courses covering Law, Finance and Principles of Real Estate.

Home Inspection Report: A qualified inspector’s report on a property’s overall condition. The report usually includes as evaluation of both the structure and mechanical systems.

Home Warranty Plan: Protection against failure of mechani-cal systems within the property. Usually includes plumbing, electrical, heating systems and installed appliances.

Index: A measure of interest rate changes used to deter-mine changes in an ARM’s interest rate over the term of the loan.

Joint Tenancy: An equal undivided ownership of property by two or more persons. Upon the death of any owner, the survivors take the decedent’s interest in the property.

Lien: A legal hold or claim on property as security for a debt or charge.

Loan Commitment: A written promise to make a loan for a specified amount on specified terms.

Loan-To-Value Ratio: The relationship between the amount of the mortgage and the appraised value of the property, expressed as a percentage of the appraised value.

Margin: The number of percentage points the lender adds to the index rate to calculate the ARM interest rate at each adjustment.

Mortgage Life Insurance: A type of term life insurance often bought by mortgagers. The coverage decreases as the mort-gage balance declines. If the borrower dies while the policy is in force, the debt is automatically covered by insurance proceeds.

Negative Amortization: Negative amortization occurs when monthly payments fail to cover the interest cost. The inter-est that isn’t covered is added to the unpaid balance, which means that even after several payments you could owe more than you did at the beginning of the loan. Negative amortization can occur than an ARM has a payment cap that results in monthly payments that aren’t high enough to cov-er the interest.

21

Checklist for Moving On Moving Day: Carry enough cash or travelers checks to cover cost of

moving services and expenses until you make banking

connections in your new city.

Carry jewelry and documents yourself; or use

registered mail

Plan for transporting pets

Let a close friend or relative know route and schedule

you will travel including overnight stops; use him or

her as message headquarters

Double check closets, drawers, shelves to be sure they

are empty

Leave all old keys needed by new tenant or owner

with Realtor or neighbor

At your New Address: Obtain certified check or cashiers check necessary for

closing real estate transaction

Check on service of telephone, gas, electricity, water

and garbage

Have appliances checked

Check pilot on stove, hot water heater and furnace

Ask mail carrier for mail he or she may be holding for

your arrival

Have new address recorded on drivers license

Visit city offices and register for voting

Register car within five days after arrival in state or a

penalty may have to be paid when getting new license

plates

Obtain inspection sticker and transfer motor club

membership

Register family in your new place of worship

Register children in school

Arrange for medical services; doctor, dentist,

veterinarian, etc.

Before You Leave: Address Change: Post office: give forwarding address Charge accounts, credit cards Subscriptions Friends and Relatives Bank: Transfer funds, arrange check cashing in new city Arrange credit references Insurance: Notify company of new location for coverage Life, Health, Fire and Auto Utility Companies: Gas, light, water, telephone, fuel, garbage Get refunds on any deposits made Delivery service: Laundry, newspaper, changeover of services Medical, Dental, Prescription Histories: Ask Doctor and Dentist for referrals; transfer needed pre-

scriptions, eyeglasses, X-rays Obtain birth records, medical Pets: Ask about regulations for licenses, vaccinations, tags, etc. Don’t forget to: Empty freezer; plan use of food

Defrost freezer and clean refrigerator. Place charcoal

inside to dispel odors

Have appliances serviced for moving

Remember arrangements for TV and antenna

Clean rugs or clothing before moving

Check with your moving counselor; insurance coverage,

packing and unpacking labor, arrival days, various

shipping papers, method and time of expected payment

Plan for special care needs of infants or pets

22

Moving Expenses When you meet the IRS’s definition of a qualifying move, the following items are tax

deductible:

The cost of trips to the area of a new job to look for a home. Your home shopping

expedition does not have to be successful for the cost to be deducted.

The cost of having your furniture and other household items shipped, including the cost

of packing, insurance and storage for up to 30 days.

The cost of getting your family to the new home town, including food, lodging and

expenses on the trip.

The cost of lodging and 80% of food expenses for up to 30 days in the new home town, if

these temporary living expenses are necessary because you have not found your ideal

home or it is not ready when you arrive.

Certain costs associated with the sale of your old home and purchase of the new one.

These expenses, including real estate commission, legal fees, state transfer taxes and

appraisal and title fees, could be used to either reduce the gain on the sale of the

previous home or to boost the basis of a new one. But it’s usually beneficial to count

them as moving expenses up to the allowable dollar limits, because that gives you an

immediate tax benefit.

*Provided for informational purposes only. Consult your tax or legal advisor for advise on your particular situation.

23

FCT now offers an amazing discount rate for consumers:

RESIDENTIAL REFINANCE/REVAMP DISCOUNT RATE

50% off Title Fee (min $350.00) & a BUNDLED ESCROW FEE $295.00

ALTA Residential Policies issued unless otherwise requested (single family, one to four units) ALTA Homeowner’s Extended Policy available for a minimal fee (single family, one to four units)

* Only one discount rate per sales transaction

First Centennial Title Reduced Rate Certifi-

cate

This certificate entitles you

to reduced rates for an Own-

er’s Policy should you sell

your property within three (3)

years.

FCT Consumer Discounts

Owner

Escrow Number

Real Estate Agent

Recorded Sale Date

This offer is applicable only if the policy is issued by First Centennial Title or its agents. To ensure your discount, present this certificate to

your real estate agent when you list your home for sale.

FIRST TIME HOMEBUYER 50% off Escrow Fee

ACTIVE MILITARY 25% off Escrow Fee

ACTIVE TEACHERS 25% off Escrow Fee

SENIOR CITIZEN (Sellers 55+) 25% off Escrow Fee (Resale Only)

NON-PROFIT ORGANIZATION 50% off Title Fee

SHORT TERM OWNERS

TITLE POLICY 20% off Title Fee up to 3 years

RESIDENTIAL REFINANCE/REVAMP

BUNDLED ESCROW FEE

50% off Title Fee (min of $350.00)

$295.00 Escrow Fee (excluding any additional doc prep fees, signing service fees, legal

fees, or recording fees)

CONCURRENT ESCROW 20% off Escrow Fee for FCT customer buying or

selling at FCT within six month period

Additional Information

SELLER:

Real Estate Commission

Document preparation fee for Deed

Documentary transfer tax (negotiable)

Any loan fees required by Buyer’s lender (VA, FHA)

Payoff all loans in seller’s name

Interest accrued to lender being paid off, Statement fees,

reconveyance fees and any prepayment penalties

Termite inspection (VA Loan) (negotiable)

Termite work/repairs (negotiable)

Home warranty (negotiable)

Any judgments, tax liens, etc., against the seller

Tax proration (for any taxes unpaid at time of transfer of

title)

HOA sellers package

Any unpaid Homeowner’s dues and transfer fees

Owners Title Insurance premium

Recording charges to clear all documents of record

against seller

Any bonds or assessments (negotiable)

Any and all delinquent taxes

Mobile notary (if applicable)

Escrow Fee (split)

Wood stove exemption and/or certificate

*FHA/VA have upfront fees/premiums due at closing

Who Pays For What?

One very common question of real estate transactions is. “Who pays for what on a real

estate transaction”. Below is a list to give you an idea of some of the common expectations, but this list will vary

from region to region. Also, if it’s a buyer’s or a seller’s market could possibly change the common fee responsibil-

ity. This is a breakdown of what the SELLER and BUYER would each

generally be expected to pay for.

BUYER:

Lenders Title Insurance Premium

Escrow Fee

Mobile notary (if applicable)

Document preparation fee (if applicable)

Recording charges for all documents in buyer’s name

Termite inspection (according to contract)

Tax proration (from date of acquisition)

Set up/Capital contribution fees

All new loan charges (except those required by the

lender for seller to pay

Interest on new loan from date of funding to 30 days

prior to the first payment date

Inspection fees (roofing, property inspection, etc.)

Home warranty (according to contract)

Homeowners insurance premium for first year

Transfer Tax

Wood stove exemption and/or certificate

25

Additional Information Consumer Finance Protection Bureau

www.consumerfinance.gov

26

4 BR 2 BA 1 THING to know before you sign.

CONSUMER’S GUIDE TO TITLE INSURANCE

When it comes to title insurance, the choice is yours.

What is title insurance?

Are you aware that you have a choice when selecting a title agency?

Did you know there could be a difference in price for the same title insurance policy?

CONSUMER’S GUIDE TO TITLE INSURANCE 1

Introduction

For many people the purchase of a home is the American Dream. The purchase of their

home (or other real property) will be the largest purchase they will make. The excited

buyers purchase homeowners or other property insurance to protect their investment.

Some of these new owners shop before purchasing that insurance to ensure they

receive the best deal or best service. However, there is another insurance purchase

made at the same time that is just as crucial — the purchase of title insurance. Yet,

many people do not compare rates and are not even aware that they have a choice in

the selection of title insurers.

The Nevada Division of Insurance has designed this consumer brochure as a tool for

consumers to protect the purchase of their real estate. This brochure is presented in

two parts: 1) Answers to Questions About Title Insurance; and 2) Tips When Buying

Title Insurance.

Dream

2

Answers to Questions About Title Insurance

Here, we explain the basics of title insurance including its nature and purpose, the types of policies

available and how to purchase it.

“Title” means the collective ownership records for a piece of property. This includes all previous

transfers of ownership and liens on the property. The title to your property outlines your legal rights to

own, use, possess, control or dispose of the property.

Transferring title to real property, meaning land and any buildings or other improvements built on

the land, is more complex than transferring title to a car or other kinds of property. While land is

permanent, land usage may change over time. For example, you may retain ownership of a piece of real

property while transferring certain rights to the property, such as mineral rights, to someone else.

CONSUMER’S GUIDE TO TITLE INSURANCE 3

What Is a Title Defect or Encumbrance? A title defect or encumbrance is a problem or

omission in the ownership records of a property

that may impair your legal rights to that property.

Defects in a title may include errors and omissions

in recorded deeds, missing or undisclosed heirs,

conflicting wills, fraud or forgery, mistakes in

examining records, liens for unpaid taxes and

contractor liens.

What Is Title Insurance? Title insurance is a contract in which the title

insurance company, in exchange for a one-time

premium at close of escrow, protects against

future losses resulting from defects in the title to

real property that exist at the time of purchase

but are unknown or undisclosed.

Title insurance is significantly different from

homeowners insurance and other casualty

insurance. Casualty insurance provides

protection from losses due to unknown future

events such as fire or theft for a specified period

of time (e.g. a yearly premium for a year of

coverage). Title insurance provides protection

for a one-time premium for an indefinite period

of time from future losses because of events that

have already occurred (e.g. claims of ownership).

Because of this, title insurers eliminate risks and

prevent losses in advance through extensive

searches of public records and thorough

examination of the title.

For example, in the event that there is a claim

against the title to your property by the ex-wife

of the seller that was unknown or undisclosed

at the time the title policy was issued, the title

insurer would be obligated to defend that claim

against your property. If it was proven in a court

of law that the ex-wife did have a right to the

property, the title insurer would be obligated to

compensate you for your losses.

4

What are the Different Types of Title Insurance? There are two types of title insurance policies—the owner’s policy and the lender’s policy. The owner’s

policy will typically be issued in the form of the Standard Coverage Form in the amount of the purchase

price of the property. It does not cover increases in value unless you purchase an endorsement. It

covers the buyer’s interest in the property for as long as the buyer or his or her heirs have an interest in

the property subject to certain limitations.

The lender’s policy will typically be issued in the form of the Extended Coverage Form in an amount

equal to the mortgage loan. It covers the lender’s interest in the property for the life of the loan. It

provides additional coverage not found in a typical owner’s policy such as unrecorded easements and

boundary discrepancies.

Owners may also elect to purchase a Homeowner’s Policy of Title Insurance instead of the Standard

Coverage Form. Introduced in the 1990s, this policy includes the standard coverages of a typical

owner’s policy and additional coverages, such as forgery occurring after the policy effective date and

increases in the value of the property. The premium for the Homeowner’s Policy is typically 10 percent

higher than the Standard Policy premium.

LenderOwner

CONSUMER’S GUIDE TO TITLE INSURANCE 5

Do I Need Title Insurance? If you are borrowing money for a piece of

property, most lenders will require a lender’s

policy to protect their interest in the property.

You are not required to purchase an owner’s

policy, but you should weigh the potential

impact of a loss against the cost of the title

insurance. Neither the lender’s policy nor the

policy of the previous owner will protect you

if there is a claim. Also, there is generally a

substantial discount when a lender’s policy

and owner’s policy are purchased together.

I Am Purchasing a Newly-Built Home. Do I Really Need Title Insurance? Even though you are the first owner of the

home, there have likely been many previous

owners of the unimproved land. There may be

mechanics’ liens on the property placed by

unpaid contractors and subcontractors. A title

search will uncover any existing liens, and a

survey will determine the boundaries of the

property being purchased.

I Am Refinancing My Home. Why Does the Lender Require a New Title Policy? It is not necessary to purchase a new owner’s

policy when you refinance a home. Your original

policy purchased when you bought your home

is effective as long as you and your heirs have

an interest in the property. However, most

lenders require a new policy based on the new

transaction amount to protect their investment

in the property because defects in title might

have arisen between the original purchase and

the refinance. For example, a building contractor

may have put a mechanic’s lien on the property,

or you may have incurred a judgment for unpaid

taxes, child support or homeowners association

fees. The new policy would also cover defects not

detected when the previous policy was issued.

Many title insurers have a discounted rate for

lender’s policies on a refinance. Be sure to ask

your lender or title agent about these discounts.

6

What Does My Title Insurance Policy Cover? A title insurance policy protects you from financial loss due to covered claims against your title, pays

your legal costs if the title insurance company is required to defend your title against covered claims

and pays successful claims against your title.

Claims typically covered under an owner’s title insurance policy include:

• Someone other than the insured who owns an interest in the property.

• Forgery, fraud, undue influence, duress, incompetency, incapacity, or impersonation.

• Defective recording of a document.

• Restrictive covenants.

• Undisclosed liens due to a deed of trust, unpaid taxes, special assessments or homeowners association charges.

• Unmarketability of title.

• Lack of access to and from the land.

Ask your title insurance agent to explain what is and is not covered under your title insurance policy.

CONSUMER’S GUIDE TO TITLE INSURANCE 7

What Is a Title Search and Examination? Because title insurance covers losses due to defects that already exist, a major part of the title insurance transaction is the title search and examination. Before issuing a policy, the insurer will conduct a detailed examination of the historical public records concerning the property. These records include, but are not limited to, deeds, mortgages, wills, tax records and maps.

The title search should show all defects and encumbrances including judgments, liens and other restrictions. According to the American Land Title Association, 26 percent of title searches find a problem which the title insurer cures before issuing the policy. After the title search and examination, the insurer will issue a Preliminary Report of Title or Commitment for Title Insurance listing the existing encumbrances. If these encumbrances cannot be cured, they are excluded from coverage. Title insurance provides protection against undisclosed defects. It is generally not intended to protect against defects that are uncovered by the title search but cannot be cured.

How Are Title Insurance Premiums Paid? Title insurance premium is paid one time at the time of closing usually through the title agency. It is based on the amount of insurance you purchase. Insurers are required to file their schedule of rates including any discounts or other modifications. Modifications include discounts for short-term policies or refinances, special rates for large commercial projects and charges for optional endorsements.

Title Insurance Rates are available to view and compare online at titlerates.doi.nv.gov.

Local custom determines who pays the premium for title insurance. In Nevada, the seller usually pays the premium for the owner’s policy and the buyer usually pays the premium for the lender’s policy. This may, however, be negotiated between the buyer and seller. There is a substantial discount for the lender’s policy when purchased simultaneously with the owner’s policy.

8

Where Can I Purchase Title Insurance? Although your real estate or mortgage broker may recommend a particular title agency, Nevada law prohibits them from requiring that consumers use a particular agent or insurer. You may purchase title insurance from any title insurer authorized to do business in Nevada. You should verify that an insurer is authorized in Nevada at DOI.NV.GOV or by calling toll-free anywhere in Nevada (888) 872-3234.

In order to help you make the best purchasing decision, the Division now has an online Title Insurance Rate Comparison Tool, which allows you to put in the purchase price, down payment, county and other details to then view and compare the title insurance and escrow rates available in your area. This comparison tool can be found at TITLERATES.DOI.NV.GOV.

Title insurers may offer their policies directly to consumers through affiliated or independent agents. Different title agents – also known as title companies – may offer different services, and title insurance rates and escrow fees may vary between companies. Again, you may purchase title insurance through any Nevada licensed title company. Verify a title agent’s license with the Division of Insurance online at DOI.NV.GOV/LICENSING-SEARCH or by phone at (888) 872-3234.

There are many reasons a real estate or mortgage broker may recommend a title agency. The title agency may be conveniently located or may provide efficient and accurate service. However, the broker may have a financial interest in the title agency or other business incentives to refer customers to the agency. For this reason, it is important to shop around and make the selection that makes the most sense for your situation.

Some factors to consider when choosing a title agent or title insurer are the cost of the title insurance and escrow fees, speed and accuracy of closing services, quality and timeliness of claims resolution and frequency and resolution of consumer complaints filed with the Division of Insurance. Ask friends, relatives or business associates regarding their experience and satisfaction with a title agency. Or, you can contact the Division of Insurance and inquire about the number of complaints received and the nature of those complaints.

VerifyResearch Select

CONSUMER’S GUIDE TO TITLE INSURANCE 9

What Should I Do if I Have a Claim? Be sure to keep a copy of your title insurance policy. As soon as you discover a title-related problem, contact the insurer listed on your policy. Make your claim in writing and include copies of all relevant documents including any correspondence related to the claim. Keep copies of all documents for your own records. Nevada law requires insurers to acknowledge receipt of a claim within 20 working days after receipt of the claim notice and to accept or deny a claim within 30 working days after receiving properly executed proofs of loss.

What Other Costs May Be Involved?

Escrow Fee – Besides title insurance premiums, you must pay the title company a fee for escrow and closing services. This is called the escrow fee. Escrow and closing services generally include holding the purchase funds in an escrow account and distributing them to the proper parties at the close of sale, gathering all required documents and presiding over their signing, and recording the deed. Nevada law requires each title insurer and title agent to make available to the public its schedule of fees and charges, including escrow fees. Some title companies have the schedules available on their website.

Short Sale and Foreclosure – Today’s real estate market includes more and more short sales and real-state owned (REO) properties. A short sale is one in which the sale price of the property is less than the amount owned on the mortgage. Because of this, the lender must approve any short sale before it occurs. An REO property is one owned by the lender as a result of an unsuccessful sale at a foreclosure auction. Short sales and REO closings involve more time and expense for the title company than a regular closing. Because of this, many title companies impose a short-sale fee or REO fee on top of the basic escrow fee. Different title companies have different fees. Be sure to shop and compare prices before selecting a title company.

Private Transfer Fee – Some developers include a Private Transfer Fee (PTF) covenant in their sales contracts. A PTF covenant requires that each time the home is resold, a percentage of the sale price is paid to the original developer. A typical PTF covenant requires that for the next 99 years, when the buyer and any subsequent buyer resell the home, they must each pay a 1% fee to the developer. These covenants became common in the mid 2000s but may be less common in the future as some states are banning the use of PTF covenants, and the Federal Housing Finance Agency is restricting Fannie Mae, Freddie Mac and Federal Home Loan Banks from dealing in mortgages that include PTF covenants.

10

Where Can I Find More Information? For questions or problems with title insurers or title agents, contact the Nevada Division of

Insurance toll free in Nevada at (888) 872-3234, the Carson City Office at (775) 687-0700, or the

Las Vegas Office at (702) 486-4009. Visit our website at DOI.NV.GOV for other consumer guides.

For questions or problems with mortgage lenders and escrow companies licensed in this

state, contact the Nevada Division of Mortgage Lending at (702) 486-0780, or visit its website

at MLD.NV.GOV.

For questions or problems with real estate agents and brokers licensed in this state, contact

the Nevada Real Estate Division at (702) 486-4033, or visit its website at RED.STATE.NV.US.

For information on title insurance and title agents, contact the American Land Title Association

toll free at (800) 787-ALTA, or visit its website at ALTA.ORG.

For information on buying or selling a home, contact the U.S. Department of Housing and

Urban Development at (202) 708-1112, or visit its website at HUD.GOV for information

regarding the federal Real Estate Settlement Procedures Act (RESPA).

12

Tips When Buying Title Insurance

Here are some things to keep in mind when buying title insurance.

• Verify that the title insurer and title agent are licensed to conduct business in Nevada.

You can verify the status of a license by visiting the Division’s website at DOI.NV.GOV.

• Compare title insurance and escrow rates at TITLERATES.DOI.NV.GOV.

• Check that the policy amount is correct. The owner’s policy should insure the full purchase

price of the property. The lender’s policy should provide coverage equal to the amount of

the mortgage loan.

• Determine who is going to pay for each policy. In Nevada, the seller usually pays for the

owner’s policy and the buyer pays for the lender’s policy. However, this may be negotiated

between the buyer and seller.

CONSUMER’S GUIDE TO TITLE INSURANCE 13

• Verify the effective date of the policy. It should be the same date as the close of escrow.

• Check to make sure that the policy describes all of the property being purchased and

all the interests being acquired by you.

• Read and understand the terms of the insurance contract, including any limitations and

exclusions in the policy. Ask your agent if you do not understand something.

• Make sure the name of the insurance company and the title agency appear on any legal

documents in case you need to file a claim or file a complaint in the future. Keep these

documents in a safe place.

• Check with your title agent to see if your purchase may qualify for any discounts on title

premium or escrow fees. Some title insurers and agents offer discounts for short-term

financing or refinancing.

• Title insurers may offer concurrent or reduced rates if they are providing both the owner’s

policy and lender’s policy in the same transaction.

• Compare rates, services and policies offered. Talk to your title insurance agent about

which policy (standard, extended or homeowners) is right for you.

• Your real estate or mortgage broker might have an ownership interest in the title agency

selected to close the loan. Ask about any and all relationships with the title agency.

• Report any suspicious activity to the Division of Insurance. Rebates are illegal in Nevada.

• Remember: you are able to choose any title insurer/agent you desire. You are not

required to use any title insurer or title agent suggested or recommended by a

lender or real estate agent.

CONSUMER’S GUIDE TO TITLE INSURANCE 15

Search and Compare Title Insurance and Escrow Rates Online

Before choosing a title insurance company, use the Division’s Title Insurance Rate Comparison Tool to view and compare custom title insurance and escrow rates at TITLERATES.DOI.NV.GOV. The title and escrow rates listed are based on rates approved by the Division of Insurance for basic title

and escrow services in conjunction with a real estate and mortgage transaction in order to provide a

fair basis of comparison among companies.

Compare Rates Online

This Consumer’s Guide to Title Insurance is intended to assist consumers in understanding title insurance. It is not intended as an “all inclusive” informational source. Please refer to your title insurance policy for coverage details.

Services provided in these basic rates include: • Review, compliance with, and

downloading of instructions and documents • Preparation of commission instructions

and escrow instructions • Procurement of demand statements • Ordering of preliminary reports/

commitments • Figuring files • Complying with lender requirements • Procuring proper signatures, including

loan documents, as necessary • Preparing closing statements • Receiving and disbursing funds

• Communication • Local delivery • Ordinary mailing and postage • Ordinary emails, faxes and phone calls

There may be additional charges or discounts applicable to your particular transaction. Some examples of discounts and additional fees include: • First-time homebuyer discount • Senior citizen discount • Document preparation fee • Overnight delivery fee • Real estate owned transaction fee • Wire fees

16

State of Nevada Department of Business and Industry

Brian Sandoval, Governor

C.J. Manthe, Director

Division of Insurance

Barbara D. Richardson, Commissioner

If you have a question about this guide or about a title insurer or agency, please contact:

Carson City Office Las Vegas Office

1818 College Pkwy., Suite 103 3300 W. Sahara Ave, Suite 275

Carson City, NV 89706-7986 Las Vegas, NV 89102

Phone: (775) 687-0700 Phone: (702) 486-4009

Fax: (775) 687-0787 Fax: (702) 486-4007

Website Address: DOI.NV.GOV

E-mail Address: [email protected]

Consumer Services Section

For consumer complaints, contact one of our Consumer Services Sections:

Carson City: (775) 687-0700

Las Vegas: (702) 486-4009

Toll-Free anywhere in Nevada (888) 872-3234

A pool. A spa.An important

decision before you sign.