hospitality financial management by robert e. chatfield and michael c. dalbor ©2005 pearson...

TRANSCRIPT

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-1

Chapter 10 Introduction

Capital budgeting was introduced in Chapter 9. The estimation of a project’s cash flows was covered, including both the net investment and net cash flows.

The focus of this chapter is the analysis of a project’s cash flows in order to make a project acceptance or rejection decision.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-2

Organization of Chapter 10

Capital budgeting decision methods:

Payback period Discounted payback period Net present value Profitability index Internal rate of return Modified internal rate of return

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-3

Organization of Chapter 10

Capital budgeting decisions with:

Independent projects Mutually exclusive projects Projects with cash flows that are not normal

The advantages and disadvantages of each of the capital budgeting decision methods

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-4

Project Cash Flows

The capital budgeting decision is essentially based upon a cost/benefit analysis.

We call the cost of a project the net investment.

The benefits from a project are the future cash flows generated. We call these the net cash flows.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-5

Capital Budgeting Decision Methods

Capital budgeting decision methods essentially compare a project’s net investment with its net cash flows. Project acceptance or rejection is based upon this comparison.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-6

Payback Period

A project’s payback period is the number of years its takes for a project’s net cash flows to pay back the net investment. Shorter paybacks are better than longer paybacks.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-7

Payback Period

Suppose a project has a $200,000 net investment and net cash flows (NCFs) of $70,000 annually for 7 years. What is the payback?

In 3 years, the project will generate a total of $210,000 from net cash flows. Therefore, the payback must be a little less than 3 years. It is more precisely:

Years 2.86

$70,000

$200,000 PeriodPayback ==

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-8

Payback Period

The payback period is useful as a measure of a project’s liquidity risk, but it has several weaknesses:

Does not account for the time value of money

No objective criterion for what is an acceptable payback period

Cash flows occurring after the payback period have no impact upon the payback computation.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-9

Discounted Payback Period

This improves upon the payback period by taking into account the time value of money.

A project’s discounted payback period is the number of years it takes for the net cash flows’ present values to pay back the net investment. Again, shorter paybacks are better than longer paybacks.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-10

Discounted Payback Period

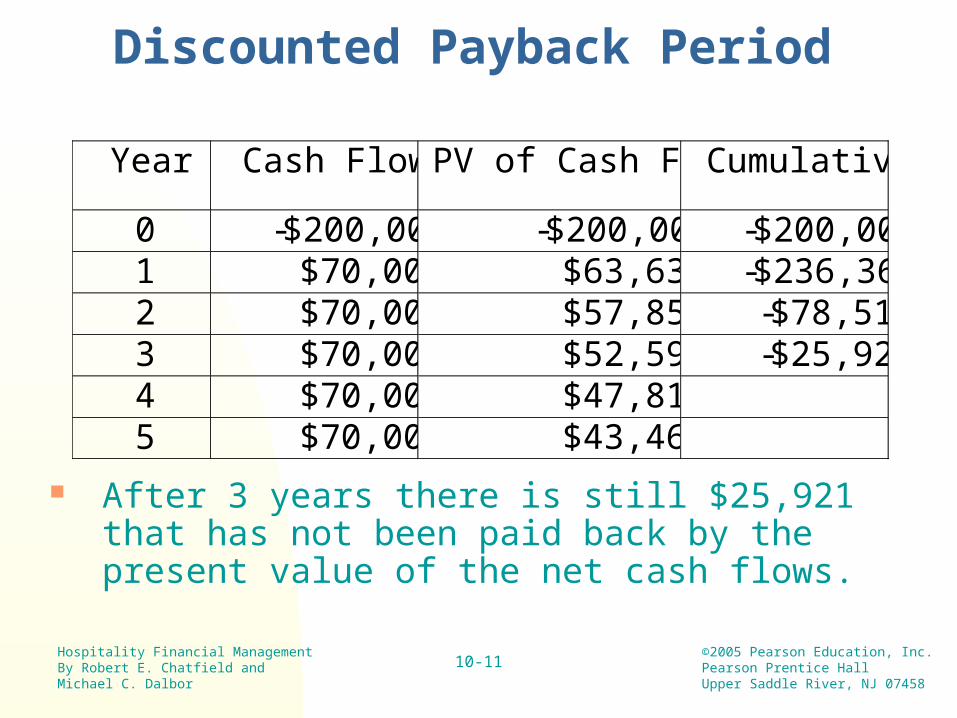

We will compute the discounted payback period (DPP) using the same example. We will need a required rate of return for the computation. Let’s use 10%.

The following table is used to compute the project’s DPP.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-11

Discounted Payback Period

After 3 years there is still $25,921 that has not been paid back by the present value of the net cash flows.

Year Cash Flow PV of Cash Flow Cumulative

0 -$200,000 -$200,000 -$200,000 1 $70,000 $63,636 -$236,364 2 $70,000 $57,851 -$78,513 3 $70,000 $52,592 -$25,921 4 $70,000 $47,811 5 $70,000 $43,464

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-12

Discounted Payback Period

The DPP will be 3 years plus whatever proportion of year 4 is needed to pay back the final $25,921.

The discounted payback is 3.54 years. This project recovers its net investment in 3.54 years when considering the time value of money.

54.3$47,811

$25,921 3 DPP =+=

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-13

Discounted Payback Period

The DPP is an improvement upon the payback period in 2 ways:

The DPP takes into account the time value of money.

There is an objective criterion for an acceptable DPP if a project has normal cash flows. Under these circumstances a project is acceptable if the DPP is less than the economic life of the project.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-14

Net Present Value

A project’s net present value (NPV) is the most straightforward application of cost-benefit analysis.

The cost is the net investment.

The benefit is the sum of the present values.

NPV is the sum of the present values of the net cash flows minus the net investment. The cash flows are discounted at a project’s required rate of return.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-15

Net Present Value

Using the same example, the NPV with a 10% required rate of return is:

A positive NPV indicates a project is acceptable.

A negative NPV indicates a project is not acceptable.

( )355,65$000,200$

10%10%1

1-1

x $70,000 NPV5

=−

⎥⎥⎥⎥

⎦

⎤

⎢⎢⎢⎢

⎣

⎡+

=

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-16

Net Present Value

A project’s NPV is also an estimate of the change in a firm’s value caused by investment in a project.

In the example, the firm’s value is expected to increase by $65,355 if the project is accepted.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-17

Profitability Index

A project’s profitability index (PI) also compares a project’s costs to its benefits.

Cost and benefits for the PI are measured the same as for the NPV.

The comparison of costs and benefits is different for the PI than for the NPV. It is the ratio of a project’s benefit to its cost.

A project’s PI is the sum of the present values of the net cash flows divided by the net investment.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-18

Profitability Index

Using the same example and a 10% required rate of return, the project’s PI is

( )

33.1$200,000

$265,355

$200,000

10%10%1

1-1

x $70,000

PI

5

==⎥⎥⎥⎥

⎦

⎤

⎢⎢⎢⎢

⎣

⎡+

=

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-19

Profitability Index

The PI can also be computed as follows:

A PI of 1.33 indicates a project is expected to generate $0.33 of NPV for every $1.00 invested in the project. Keep in mind, NPV is a measure of value over and above the project’s net investment.

33.1$200,000

$65,3551

InvestmentNet

NPV 1 PI =+=+=

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-20

Profitability Index

A PI greater than 1.0 indicates a project is acceptable.

A PI less than 1.0 indicates a project is not acceptable.

The PI is most useful when a firm is facing capital rationing. The PI indicates which projects generate the greatest NPV per dollar invested.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-21

Internal Rate of Return

An internal rate of return (IRR) is a project’s true annual percentage rate of return based upon the estimated cash flows.

IRR can also be defined as the interest rate causing a project’s NPV to be equal to zero. Therefore, the IRR equation is adapted from the NPV equation.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-22

Internal Rate of Return

Using the same example, the IRR equation is:

IRR equals 22.11%.

( )0000,200$

IRRIRR1

1-1

x $70,0005

=−

⎥⎥⎥⎥

⎦

⎤

⎢⎢⎢⎢

⎣

⎡+

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-23

Internal Rate of Return

The IRR equation can also be expressed as:

And of course the IRR still equals 22.11%.

( )000,200$

IRRIRR1

1-1

x $70,0005

=

⎥⎥⎥⎥

⎦

⎤

⎢⎢⎢⎢

⎣

⎡+

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-24

Internal Rate of Return

A project is:

Acceptable if the IRR > required rate of return.

Unacceptable if the IRR < required rate of return.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-25

Internal Rate of Return

Notice we did not use the 10% required rate of return to compute the IRR in our example. But we do determine project acceptability by comparing the IRR to the required rate of return.

In our example, the project is acceptable since the 22.11% IRR is greater than the 10% required rate of return.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-26

Modified Internal Rate of Return

A project’s modified internal rate of return (MIRR) is the interest rate equating a project’s investment costs with the terminal value of the project’s net cash flows.

The present value of a project’s investment costs is called the beginning value.

The future value of a project’s net cash flows is called the terminal value.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-27

Modified Internal Rate of Return

A project’s beginning value is the sum of the present values of all investment cash outflows for a project.

If all investment cash outflows occur at the very beginning (time = 0), then the beginning value equals the net investment.

If investment outlays occur over several years, the discount rate used to compute present values is usually the required rate of return.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-28

Modified Internal Rate of Return

A project’s terminal value is the sum of the future values of the net cash flows at the end of the project’s economic life.

The interest rate used to compute the future values is usually the required rate of return.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-29

Modified Internal Rate of Return

Using the same example, the project’s beginning value is just the net investment of $200,000. The project’s terminal value (TV) is:

( )357,427$

10%

110%1 x $70,000 TV

5

=⎥⎦

⎤⎢⎣

⎡ −+=

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-30

Modified Internal Rate of Return

The project’s MIRR equates the PV of the beginning value with the FV of the terminal value:

The MIRR equals 16.40%.

( )5MIRR1

$427,357 $200,000

+=

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-31

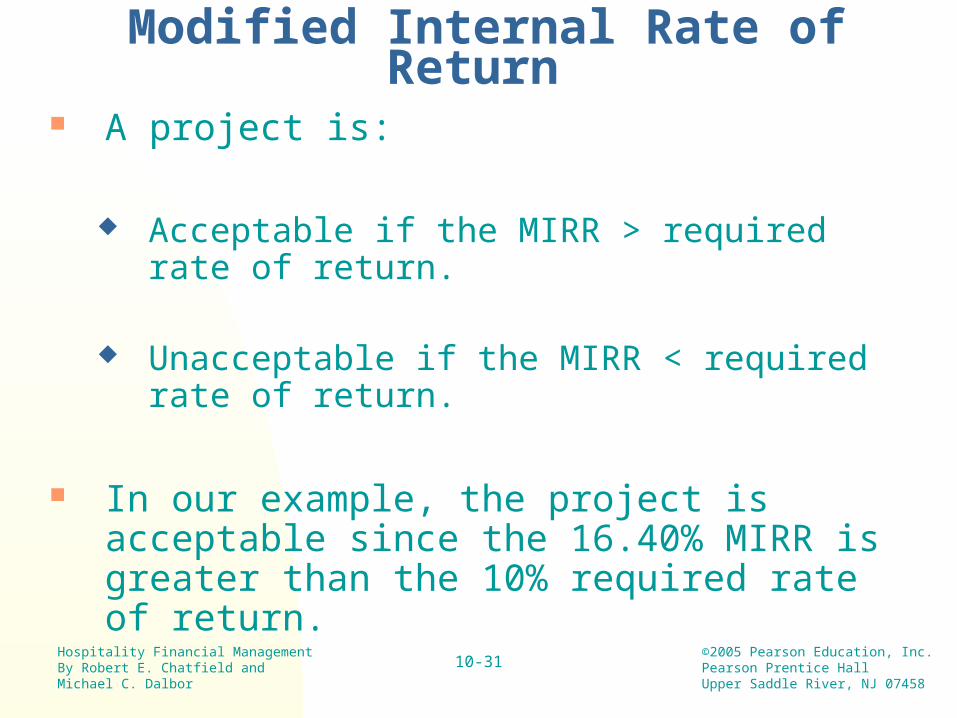

Modified Internal Rate of Return

A project is:

Acceptable if the MIRR > required rate of return.

Unacceptable if the MIRR < required rate of return.

In our example, the project is acceptable since the 16.40% MIRR is greater than the 10% required rate of return.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-32

Independent Projects and Decision Making

An independent capital budget project presents a standalone decision. A single project is simply evaluated to determine if it is expected to increase firm value or decrease firm value.

If a project has normal cash flows and is independent, then any of the methods besides payback period can be used to determine acceptability.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-33

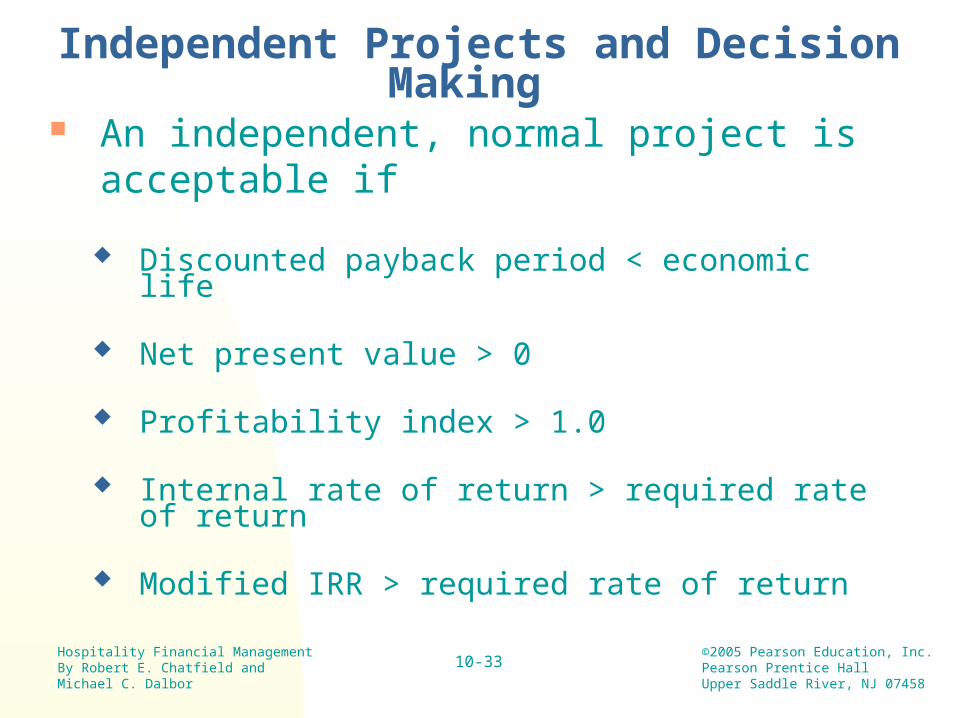

Independent Projects and Decision Making An independent, normal project is

acceptable if

Discounted payback period < economic life

Net present value > 0

Profitability index > 1.0

Internal rate of return > required rate of return

Modified IRR > required rate of return

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-34

Mutually Exclusive Projects and Decision Making Mutually exclusive capital budgeting decisions

require the evaluation of several projects to determine the one project that maximizes firm value.

All the mutually exclusive projects need to be ranked with only the best project accepted.

The project with the highest NPV is by definition the project expected to maximize firm value.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-35

Mutually Exclusive Projects and Decision Making Other methods besides NPV may not rank

projects correctly if:

Projects have scale differences—net investments are different sizes.

Projects have cash flow timing differences.

Cash flows are not normal—one or more future net cash flows are negative.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-36

Mutually Exclusive Projects and Decision Making When projects have scale differences:

Only the NPV will definitely rank projects correctly.

The payback period, DPP, PI, IRR, and MIRR may not rank projects correctly.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-37

Mutually Exclusive Projects and Decision Making

When projects have cash flow timing differences:

The NPV, PI, and MIRR will rank projects correctly.

The payback period, DPP, and IRR may not rank projects correctly.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-38

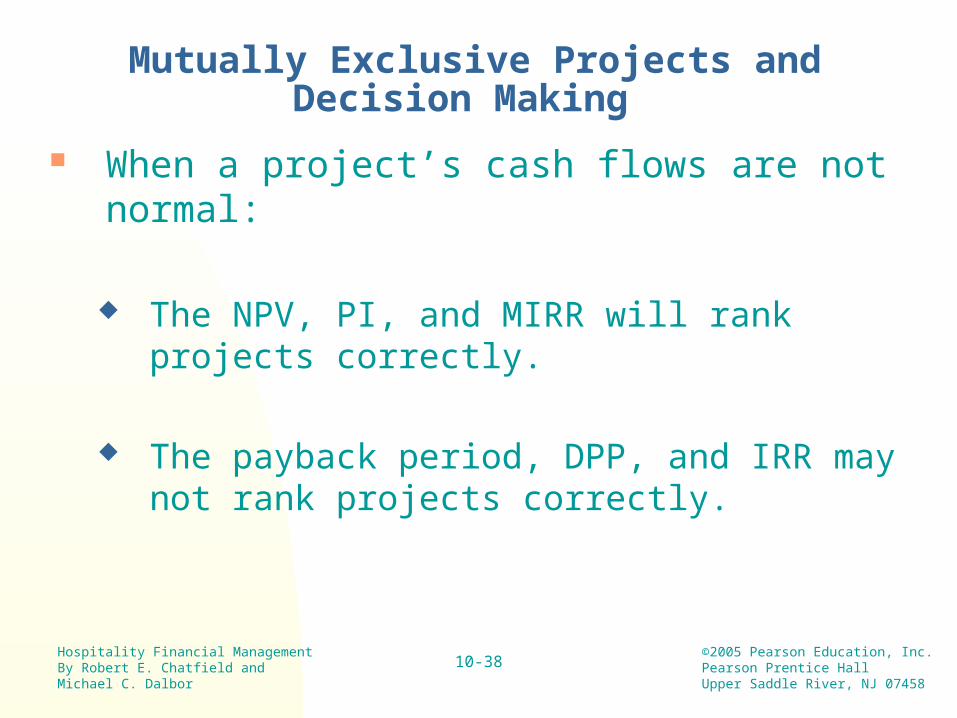

Mutually Exclusive Projects and Decision Making

When a project’s cash flows are not normal:

The NPV, PI, and MIRR will rank projects correctly.

The payback period, DPP, and IRR may not rank projects correctly.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-39

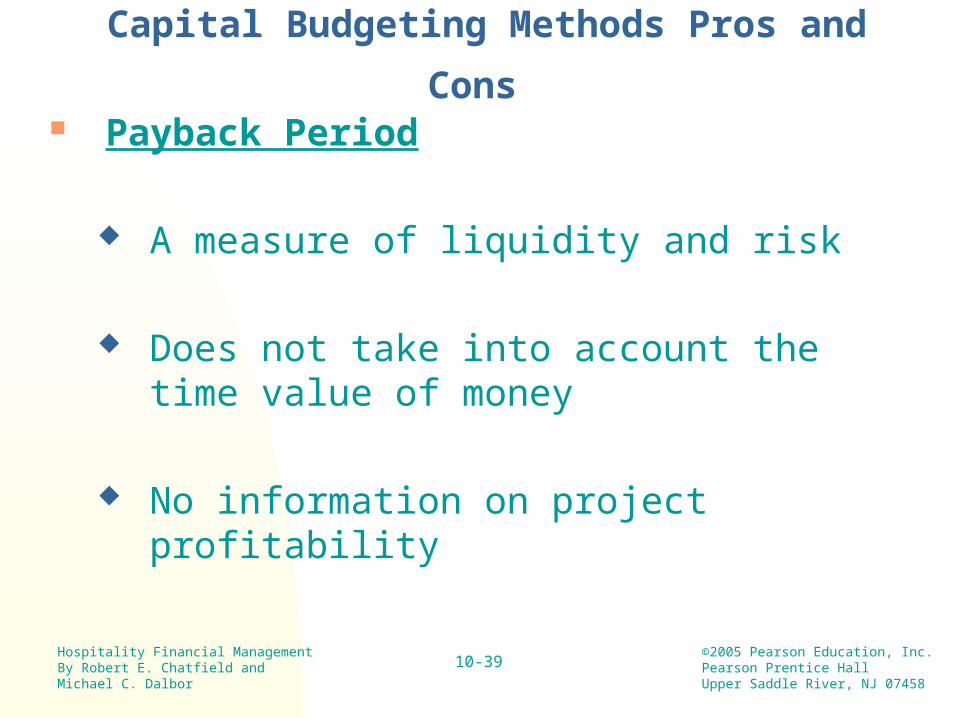

Capital Budgeting Methods Pros and Cons Payback Period

A measure of liquidity and risk

Does not take into account the time value of money

No information on project profitability

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-40

Capital Budgeting Methods Pros and Cons

Discounted Payback

A better measure of liquidity and risk than the ordinary payback period

Does take into account the time value of money

Provides an objective criterion for normal projects: DPP < economic life

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-41

Capital Budgeting Methods Pros and Cons

Net Present Value

Best measure of project profitability.

Does not provide much information about project risk.

Is consistent with maximizing firm value.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-42

Capital Budgeting Methods Pros and Cons

Profitability Index

A relative measure of profitability

Provides some information about project risk

May not rank mutually exclusive projects correctly

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-43

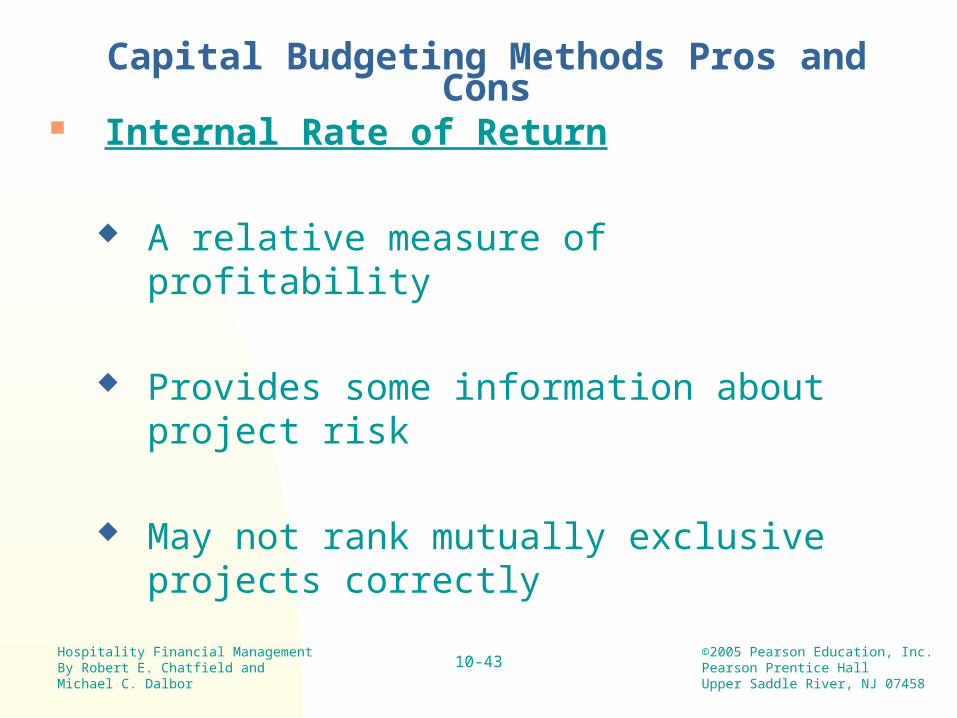

Capital Budgeting Methods Pros and Cons Internal Rate of Return

A relative measure of profitability

Provides some information about project risk

May not rank mutually exclusive projects correctly

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-44

Capital Budgeting Methods Pros and Cons

Modified Internal Rate of Return

A relative measure of profitability

Provides some information about project risk

May not rank mutually exclusive projects correctly if scale differences exist between projects

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-45

Summary of Chapter 10 Topics

The NPV is the single best measure of a project’s profitability.

The PI, IRR, and MIRR provide a measure of a project’s margin of safety.

The payback period and DPP provide a measure of liquidity risk.

Hospitality Financial ManagementBy Robert E. Chatfield and Michael C. Dalbor

©2005 Pearson Education, Inc.Pearson Prentice HallUpper Saddle River, NJ 07458

10-46

Summary of Chapter 10 Topics

We have covered the following in this chapter:

Computation of 6 capital budgeting decision methods and their pros and cons

Making decisions with independent projects

Making decisions with mutually exclusive projects