hotel intelligence mexico market insight - · pdf filehotel intelligence mexico february 2014...

TRANSCRIPT

Hotel Intelligence MexicoFebruary 2014

Market Insight • The budding economic and political climate in Mexico is

leading to a positive outlook for the Mexican lodging sector.

• Newly emerging domestic investment vehicles are targetingthe hotel sector; this increased liquidity, coupled with growinginterest from foreign investors, is expected to result in hotelacquisition volumes exceeding US $700 million in 2014.

“ Improved hotel performance metrics coupled

with rising hotel demand underpin a robust

environment for continued global investment

in Mexico’s lodging sector.”

Jones Lang LaSalle’s Hotels & Hospitality Group serves as the hospitality industry’s global leader in real estate services for luxury, upscale, select service and budget hotels; timeshare and fractional ownership properties; convention centers; mixed-use developments and other hospitality properties. The firm’s 300 dedicated hotel and hospitality experts partner with investors and owner/operators around the globe to support and shape investment strategies that deliver maximum value throughout the entire lifecycle of an asset. In the last five years, the team completed more transactions than any other hotels and hospitality real estate advisor in the world totaling nearly US $36 billion, while also completing approximately 4,000 advisory, valuation and asset management assignments. The group’s hotels and hospitality specialists provide independent and expert advice to clients, backed by industry-leading research.

For more news, videos and research from Jones Lang LaSalle’s Hotels & Hospitality Group, please visit: www.jll.com/hospitality or download the Hotels & Hospitality Group’s iPhone app or iPad app from the App Store.

Clay Dickinson Executive Vice President [email protected]

Fernando Garcia-Chacon Executive Vice President [email protected]

Alfonso de Gortari Senior Vice President [email protected]

Stewart Brown Senior Vice President [email protected]

Wendy Chan Associate [email protected]

Eric Gorenstein Analyst [email protected]

Contributors

February 2014 | Hotel Intelligence Mexico 3

Table of contentsHotel Intelligence Mexico .....................................................................4

Macroeconomic perspective ................................................................5

Travel and tourism trends .....................................................................5

Investment activity ................................................................................6

Trends shaping Mexico’s hotel market .................................................7

Market spotlight: Mexico City ...............................................................8

Market spotlight: Cancun ......................................................................9

Market spotlight: Los Cabos ...............................................................10

4 Hotel Intelligence Mexico | February 2014

Despite the turmoil affecting some emerging markets today, Mexico continues to offer a robust outlook for investors. Most of this bullishness can be tied to the country’s improving political environment. During most of the 20th century, the country was ruled by the Institutional Revolutionary Party (or PRI, its Spanish acronym), which had been known for election fraud and corruption. However, after losing its first election in 2000, the PRI returned to power in 2012 under a reform platform that has surprised many.

After gaining consensus with the opposition, President Enrique Peña Nieto, who leads Mexico’s current administration, embarked on a series of developments that have shaken many of the country’s historic norms. In early 2013, the government arrested the head of the powerful teacher’s union, thus paving the way for an education reform that was approved last September.

Other improvements include the PRI’s passing of a telecommunication legislation designed to bring more competition to the sector. Likewise, the government has implemented various fiscal adjustments.

But perhaps the most surprising development was the government’s energy reform package, which was approved last year, to allow foreign investment in this sector. The PRI recognized it will need assistance in exploring its vast reserves, and such a move could translate into US $20 billion in annual investment.

The aforementioned developments bode well for the lodging and tourism sector. From a leisure travel standpoint, Mexico offers unparalleled riches, from Caribbean-like beaches to desert vistas and mountain ranges. According to the UNWTO, with over 23.4 million visitors, Mexico already ranks as the most visited country in Latin America, earning its spot among the top 15 most visited destinations worldwide.

Although drug-related violence has undoubtedly impacted visitation volume, a growing number of tourists are beginning to understand that most of this violence is specific to certain geographic areas such as Ciudad Juarez, Sinaloa and Acapulco. On the other hand, Cancun and Mexico City are enjoying record visitation and, likewise, Los Cabos is recovering strongly.

From a capital markets perspective, and focusing on the tourism sector, the biggest development has been the introduction of REIT-like structures (known as FIBRAs1) and related entities, such as CKDs2. These investment vehicles have introduced liquidity to a market that traditionally witnessed very limited transaction activity. Namely, domestic institutional funds, which were long prevented from acquiring real estate, now have the ability to participate in the domestic real estate market. FIBRAs have formed partnerships with global hotel companies, such as Marriott International, and developers to expand their hotel portfolio across key primary and secondary markets in Mexico.

Hotel Intelligence Mexico

1Fideicomiso de Inversión en Bienes Raíces de Mexico, or FIBRA, are similar to the real estate investment trust (REIT) structure in the U.S., and allow for a more favorable tax structure.2Certificados de Capital de Desarrollo (CKD) structure is comprised of securities that allow investors to participate in private equity projects through long-term public fund structures. This structure will become prevalent both for acquisition of existing hotels and/or development of new hotels. CKDs mark a vehicle whereby domestic institutional capital is able to invest in hotels and other real estate.

February 2014 | Hotel Intelligence Mexico 5

Macroeconomic perspective

Mexico’s real GDP is set to average 4% annual growth over the next several years, an increase that is more than one percentage point above that of the United States. Mexico’s economy is considered by many to be in its incipient stages of dramatic growth.

Mexico’s manufacturing industry is blossoming once again, particularly in light of the re-shoring of some manufacturing activity that had been outsourced to China. Also, Mexico’s automobile industry, driven by low labor costs, continues to achieve record-setting production and export levels as existing and new global auto companies continue investing in manufacturing plants across secondary markets. This, coupled with the nation’s oil extraction capabilities following the recent energy reform, is anticipated to boost Mexico’s export levels in the near-term—particularly to the U.S. given the proximity of the countries.

Moreover, Mexico’s emerging middle class has stimulated growth in the services industry, which now comprises over 60% of the nation’s GDP, a benchmark that generally corresponds to substantial growth in lodging demand as has been observed in the U.S. and the U.K. The aforementioned industrial and manufacturing activity is bolstering the economic performance of many primary and secondary markets, which are showing signs of a growing services economy with the entry of several branded select-service hotels.

Mexico’s economic outlook is promising, and investors, both foreign and domestic, are eager to partake in the investment potential across various industries, including tourism and lodging.

Travel and tourism trends

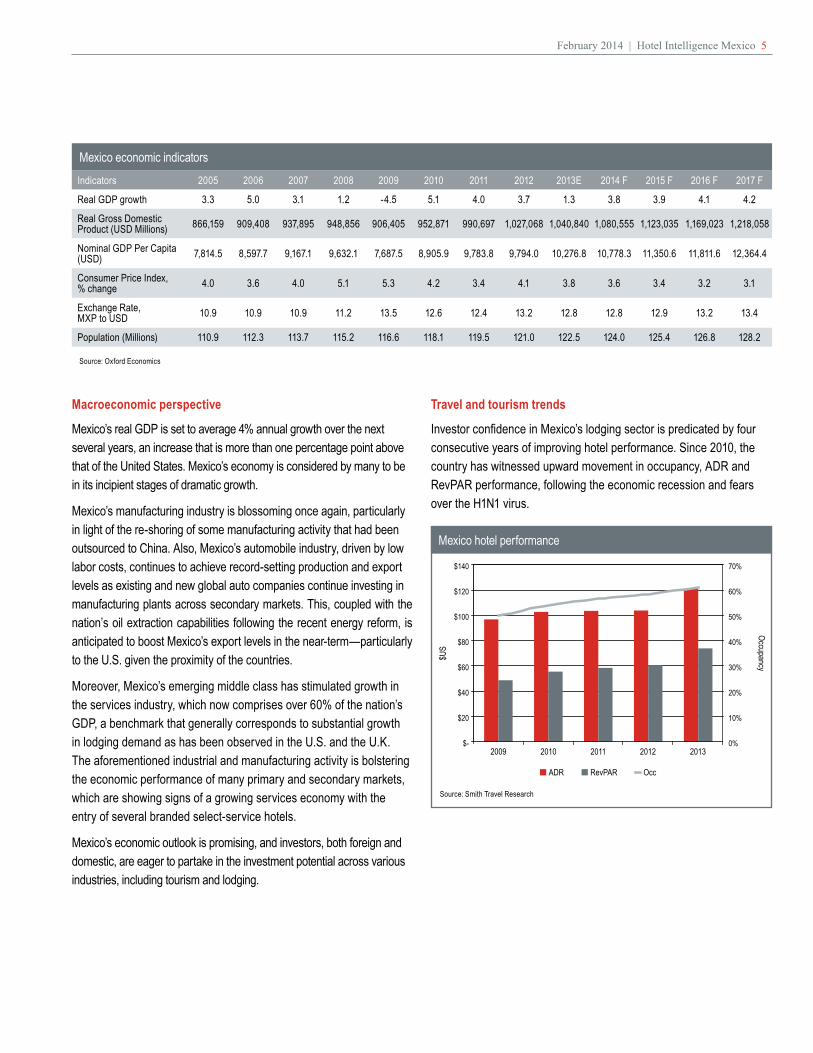

Investor confidence in Mexico’s lodging sector is predicated by four consecutive years of improving hotel performance. Since 2010, the country has witnessed upward movement in occupancy, ADR and RevPAR performance, following the economic recession and fears over the H1N1 virus.

Mexico economic indicators

Source: Oxford Economics

Indicators 2005 2006 2007 2008 2009 2010 2011 2012 2013E 2014 F 2015 F 2016 F 2017 F

Real GDP growth 3.3 5.0 3.1 1.2 -4.5 5.1 4.0 3.7 1.3 3.8 3.9 4.1 4.2

Real Gross Domestic Product (USD Millions) 866,159 909,408 937,895 948,856 906,405 952,871 990,697 1,027,068 1,040,840 1,080,555 1,123,035 1,169,023 1,218,058

Nominal GDP Per Capita (USD) 7,814.5 8,597.7 9,167.1 9,632.1 7,687.5 8,905.9 9,783.8 9,794.0 10,276.8 10,778.3 11,350.6 11,811.6 12,364.4

Consumer Price Index, % change 4.0 3.6 4.0 5.1 5.3 4.2 3.4 4.1 3.8 3.6 3.4 3.2 3.1

Exchange Rate, MXP to USD 10.9 10.9 10.9 11.2 13.5 12.6 12.4 13.2 12.8 12.8 12.9 13.2 13.4

Population (Millions) 110.9 112.3 113.7 115.2 116.6 118.1 119.5 121.0 122.5 124.0 125.4 126.8 128.2

Mexico hotel performance

Source: Smith Travel Research

$US

Occupancy

RevPARADR Occ

0%

10%

20%

30%

40%

50%

60%

70%

$-

$20

$40

$60

$80

$100

$120

$140

2009 2010 2011 2012 2013

6 Hotel Intelligence Mexico | February 2014

In terms of total consumer spending in Mexico’s hotel sector, following the low point in 2009, the country has experienced steady growth with spending on accommodation services rising by 6% annually from 2010 to 2013. Over the next three years consumer spending at hotels in Mexico is expected to see 8% annual growth, according to Oxford Economics. These growth rates are well above those in most mature economies.

Investment activity

Against the backdrop of steady top-line growth, the hotel investment climate has resurged. From a low of under $100 million in hotel transactions in 2009, capital has increasingly flowed into the sector, and hotel transaction volumes topped $600 million in 2013.

Driving the country’s record-level transaction volume are newly formed investment vehicles such as FIBRAs and CKDs, which accounted for 25% and 50% of hotel acquisition volume in 2012 and 2013, respectively. As such, these newcomers to the market have quickly ratcheted up to half of hotel transaction volumes in the country.

Recent news reports announced the partnership between FibraHotel and Marriott International, which affirms both the investment capacity of FIBRAs and the desirability of secondary markets. FibraHotel plans to develop 20 Marriott branded hotels in secondary markets by 2016. This highlights growth prospects for institutional quality branded hotel rooms.

Based on our review of drivers impacting the hotel investment landscape, we expect deal flow to rise by another 15% in 2014, which would equate to over US $700 million in hotel transactions. This would make 2014 the highest annual level of transaction volume on record, which further exemplifies the stronghold that the newly formed investment vehicles have on the market.

Mexico hotel transaction volume

Source: Jones Lang LaSalle

0

1,000

2,000

3,000

4,000

5,000

6,000

$-

$100

$200

$300

$400

$500

$600

$700

$800

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014F

Rooms sold

Millio

ns ($

US)

Consumer spending on lodging in Mexico

Source: Oxford Economics

Consumer spending on accommodation services Annual % change

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

$-

$5,000

$10,000

$15,000

$20,000

$25,000

2007 2008 2009 2010 2011 2012E 2013E 2014F 2015F 2016F

Annual % changeMi

llions

($US

)

February 2014 | Hotel Intelligence Mexico 7

Consumers increasingly seeking branded hotels

While Mexico’s hotel stock is the most sophisticated in all of Latin America in terms of the proportion of branded hotels, it still lags the United States where nearly three quarters of hotel rooms are affiliated with a hotel brand. In Mexico, 70% of hotel rooms are unbranded. Business travelers and tourists are increasingly seeking standards and consistency while owners want access to larger reservation systems to boost occupancy. Expect to see hotels raise flags by partnering with U.S. management companies or local groups, like City Express, to increase the low proportion of branded hotel stock in Mexico over the next three to five years.

Developers in historically illiquid market see more favorable exit strategies

The presence of FIBRAs and CKDs is boosting market liquidity. Hold periods are compressing, giving developers more certainty regarding an eventual exit. Having favorable exit strategies in sight will lead to more new development projects. In addition, as FIBRAs and CKDs acquire a number of the value-add purchase opportunities on the market, they will look to new development as a means to achieve yield. These groups are expected to also build new stand-alone hotels as well as mixed-use developments with hotel components in areas where land is available.

Increase in foreign investment

As yields tighten in the U.S., some investors are turning to emerging markets like Mexico for higher rates of return. Over the past three years, investors from the U.S. accounted for a relatively minimal 15% of hotel acquisitions in Mexico given the high amount of product on the market in the U.S. as well as opportunistic plays available domestically. In 2014 and 2015, we expect U.S. buyers seeking exposure outside of their home country to review investment opportunities among Mexico’s branded full-service hotels in both primary and secondary markets.

Safety of tourist areas improves

Mexico’s drug violence has generally been restricted to specific areas of the country, including Ciudad Juarez, the state of Sinaloa and the Acapulco area. The country’s top leisure destinations like Cancun/Riviera Maya, Los Cabos and Puerto Vallarta are largely perceived as safe. Likewise, the nation’s capital has successfully mitigated the negative perception of violence that once tainted the city’s reputation, evidenced by increasing domestic and international visitation, which increased in 2013 by 6% and 8%, respectively, over the prior year’s figures. Although violence will not disappear in the short-term, Mexican authorities have put in place a longer-term strategy to reduce these threats.

Mexico’s “white space” for future hotel development is vast

Jones Lang LaSalle studied economic indicators and demand drivers in Mexico and estimates that approximately 191,600 new hotel rooms will be warranted through 2022, which represents a compound annual growth rate in room supply of 4.9%. This would be more than three times the growth rate expected for the U.S. Jones Lang LaSalle’s analysis is based on an industry-sponsored white paper which looked at ± 200 infrastructure projects across 13 economic sectors to assess Mexico’s transformation from an industrial to a services-oriented economy. The full paper can be accessed online at: http://www.jll.com/hospitality-latam.

Trends shaping Mexico’s hotel market

8 Hotel Intelligence Mexico | February 2014

Market spotlight: Mexico City

Mexico City is among the largest five cities in the world, with a population of over 20 million people in the greater metropolitan area, making it the most populous metropolitan area in Latin America. However, the city’s room supply is relatively small—the market’s stock of 28,000 quality hotel rooms is comparable in size to that of secondary markets in the U.S., underscoring the opportunity for growth.

Nevertheless, the supply pipeline is constrained due to the high barriers to entry including both the increasing cost and lack of available land in prominent submarkets within Mexico City such as Polanco and Reforma. The improving market fundamentals are thus driving values of existing properties. Following are three factors impacting the investment market:

1. RevPAR has exceeded the previous peakRevPAR in Mexico City has exceeded prior peak levels, following compound annual average growth of 11.5% since 2009. The market has now recovered from the combined impact of the H1N1 virus and the financial downturn. Given renovations in the market and the limited outlook for new supply, hotel performance is expected to see steady growth over the next several years.

2. Hotel owners driving capital investment cycleHotel owners perceive considerable runway for growth and are increasing capital expenditure as a means to drive room rates. Following a number of years of lower capital expenditure, Mexico City hotels are witnessing both large and small-scale renovations. The JW Marriott recently completed a major US $30 million renovation, while the adjacent InterContinental Presidente is undergoing a property-wide renovation. The former Hotel Nikko also underwent a renovation for its rebranding as the Hyatt Regency.

3. Mexico City earns gateway city statusIn 2013, Mexico City witnessed hotel transaction volume totaling US $270 million, earning the title as Latin America’s most liquid hotel transaction market. Given the aforementioned trends, Jones Lang LaSalle anticipates growing transaction volume in Mexico City and increases in real estate values with cap rates for prime assets as low as 6.5% to 7%.

Mexico City lodging performance, selected upper-tier hotels

Source: Smith Travel Research

RevPARADR Occ

0%

20%

40%

60%

80%

100%

$-

$20

$40

$60

$80

$100

$120

$140

$160

$180

$200

2007 2008 2009 2010 2011 2012 2013

$US

Occupancy

February 2014 | Hotel Intelligence Mexico 9

Market spotlight: Cancun

Cancun/Riviera Maya, located in the state of Quintana Roo, is among Mexico’s largest and most international resort markets, generating almost half of the country’s spillover from foreign exchange induced by the tourism industry, according to a report from Banxico. Moreover, the Cancun/Riviera Maya corridor contains among the highest number of hotel rooms among resort markets globally.

Relative to the rest of Mexico, Cancun has a greater share of branded rooms—approximately 60% of rooms are affiliated with either U.S. or European brands. Such hotels remain on investors’ radar given the more robust reservation systems and loyalty programs associated with larger brands. Here are four factors impacting the Cancun/Riviera Maya investment market:

1. Institutional investors enter the all-inclusive segmentCancun already stands out as the Mexican resort market where the all-inclusive structure is most common, and the prevalence of the all-inclusive operating model is on the rise. While all-inclusive operations require a different distribution model of American and European plan hotels, institutional investors are making strategic investments into all-inclusive hotel companies’ operating platforms as a means to acquire their expertise and couple it with their strong brand platforms.

The all-inclusive sector is becoming increasingly attractive to institutional investors. Notably, Hyatt Hotels Corporation purchased a stake in Playa Hotels & Resorts and is debuting new brands in Cancun, and Bain Capital invested in Apple Leisure Group, parent of AMResorts. The continued foray by institutional-grade investors into this sector is expected in 2014 and beyond, which will elevate the quality of sector as a whole.

2. Five years of RevPAR growthCancun has seen compound annual RevPAR growth of 8.9% since 2009. In 2013, the market’s 10.5% RevPAR growth was driven by a 6.6 percentage point increase in occupancy, resulting in record occupancy levels. Nonetheless, there is still upside potential for ADR as it remains 21% below the previous peak of 2008. Riviera Maya is expected to see disproportionately higher ADR growth due to the addition of upper-tier and luxury American and European plan hotels.

3. Target for investment capitalSince 2010, Cancun has notched US $250 million in hotel transaction volume, making this Mexico’s second most liquid hotel market. Opportunistic investors from the U.S. such as private equity groups are looking to markets such as Cancun as hold periods in Mexico shorten and yields in the U.S. tighten. We expect investors to capitalize on branding opportunities as well as make capital infusions to drive rate.

4. Supply pipeline is tepid and comprised of smaller hotelsNew supply remains in check as a number of projects originally conceived before the downturn struggle to obtain funding. Likewise, new construction has been stalled by zoning and environmental regulations impacting wetlands. Nevertheless, we expect that a number of these stalled projects will be recapitalized over the next 18-24 months, at which time the market could see an uptick in supply.

The market’s recent hotel openings include AMResorts’ 495-room Secrets the Vine, the 274-room NIZUC Hotel & Spa as well as the 180-room aloft Cancun. Incoming supply includes 950 rooms that are anticipated to enter the market by 2015.

Cancun lodging performance, selected upper-tier hotels

Source: Smith Travel Research

0%

20%

40%

60%

80%

100%

$-

$20

$40

$60

$80

$100

$120

$140

$160

$180

$200

2007 2008 2009 2010 2011 2012 2013

RevPARADR Occ

$US

Occupancy

Select hotels under development in Cancun

Source: Jones Lang LaSalle Note: Based on publicly available information; dates and projects are subject to change

Property Proposed opening date

Rooms Status

Four Points Cancun Centro 2014 112 In Construction

Holiday Inn Express 2014 160 In Planning

Andaz Mayakoba 2015 213 In Planning

Hyatt Playa del Carmen 2015 332 In Planning

Thompson Playa del Carmen 2015 125 In Planning

10 Hotel Intelligence Mexico | February 2014

Market spotlight: Los Cabos

Los Cabos garners the highest average room rates in Mexico due to the high quality of rooms. Los Cabos is a popular destination for U.S. travelers, especially from the West Coast. In addition to the high-quality hotel product, the favorable exchange rate for U.S. travelers is also a draw given the dollar’s strong buying power—and exchange rates are expected to continue to favor the U.S. dollar. Following are key trends in the market:

1. Operating fundamentals have not reached previous peakLos Cabos witnessed compound annual RevPAR growth of 12% since 2009, driven in large part by rising occupancy. As of year-end 2013, ADR, occupancy and RevPAR were still below peak levels last seen in 2007, affirming continued upside potential. The outlook for Los Cabos is strong given the strengthening economic environment in California, Los Cabos’ largest source market, and the U.S. as a whole.

2. New development cycle slowly emergingThe healthy recovery of the Los Cabos lodging market following the economic downturn and negative impact stemming from fears over the H1N1 virus in 2009 and 2010 has increased developer interest as of late. While the proposed new hotel stock is well below the level of increases seen in the early 2000s, additions to the market include the recent opening of the 157-room Hyatt Place San Jose del Cabo. The following pipeline is comprised both of luxury boutique hotels and branded select service hotels.

Los Cabos lodging performance, selected upper-tier hotels

Source: Smith Travel Research

RevPARADR Occ

0%

20%

40%

60%

80%

100%

$-

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

2007 2008 2009 2010 2011 2012 2013

$US

Occupancy

Select hotels under construction in Los Cabos

Source: Jones Lang LaSalle Note: Based on publicly available information; dates and projects are subject to change

Property Proposed opening year

Rooms

2014 90

2014 114

2014 130

2014 150

2015 124

Holiday Inn Express Los Cabos

Thompson Cabo San Lucas

Courtyard by Marriott Los Cabos

Hampton Inn & Suites Los Cabos

Ritz-Carlton Researve Puerto Los Cabos

JW Marriott Puerto Los Cabos 2015 300

February 2014 | Hotel Intelligence Mexico 11

COPYRIGHT © JONES LANG LASALLE 2014All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means without prior written consent of Jones Lang LaSalle. It is based on material that we believe to be reliable. While every effort has been made to ensure its accuracy, we cannot offer any warranty that it contains no factual errors. We would like to be told of any such errors in order to correct them.

Jones Lang LaSalle Hotels & Hospitality Group Dedicated OfficesAtlanta tel: +1 404 995 2100 fax: +1 404 995 2109

Auckland tel: +64 9 366 1666 fax: +64 9 309 7628

Bangkok tel: +66 2624 6400 fax: +66 2679 6519

Barcelona tel: +34 93 318 5353 fax: +34 93 301 2999

Beijing tel: +86 10 5922 1300 fax: +86 10 5922 1346

Brisbane tel: +61 7 3231 1400 fax: +61 7 3231 1411

Buenos Aires tel: +54 11 4893 2600 fax: +54 11 4893 2080

Chengdu tel: +86 28 6680 5000 fax: +86 28 6680 5096

Chicago tel: +1 312 782 5800 fax: +1 312 782 4339

Dallas tel: +1 214 438 6100 fax: +1 214 438 6101

Denver tel: +1 303 260 6500 fax: +1 303 260 6501

Dubai tel: +971 4 426 6999 fax: +971 4 365 3260

Düsseldorf tel: +49 211 13006 0 fax: +49 211 13399 0

Exeter tel: +44 1392 423696 fax: +44 1392 423698

Frankfurt tel: +49 69 2003 0 fax: +49 69 2003 1040

Glasgow tel: +44 141 248 6040 fax: +44 141 221 9032

Istanbul tel: +90 212 350 0800 fax: +90 212 350 0806

Jakarta tel: +62 21 2922 3888 fax: +62 21 515 3232

Leeds tel: +44 113 244 6440 fax: +44 113 245 4664

London tel: +44 20 7493 6040 fax: +44 20 7399 5694

Los Angeles tel: +1 213 239 6000 fax: +1 213 239 6100

Lyon tel: +33 4 7889 2626 fax: +33 4 7889 0476

Madrid tel: +34 91 789 1100 fax: +34 91 789 1200

Manchester tel: +44 161 828 6440 fax: +44 161 828 6490

Marseille tel: +33 495 091313 fax: +33 495 091300

Melbourne tel: +61 3 9672 6666 fax: +61 3 9600 1715

Mexico City tel: +52 55 5980 8054 fax: +52 55 5202 4377

Miami tel: +1 305 529 6345 fax: +1 305 529 6398

Milan tel: +39 2 8586 8672 fax +39 2 8586 8670

Moscow tel: +7 495 737 8000 fax: +7 495 737 8011

Munich tel: +49 89 2900 8882 fax: +49 89 2900 8888

New Delhi tel: +91 124 331 9600 fax: +91 124 460 5001

New York tel: +1 212 812 5700 fax: +1 212 421 5640

Paris tel: +33 1 4055 1718 fax: +33 1 4055 1868

Perth tel: +61 8 9322 5111 fax: +61 8 9481 0107

Rome tel: +39 6 4200 6771 fax: +39 6 4200 6720

San Francisco tel: +1 415 395 4900 fax: +1 415 955 1150

São Paulo tel: +55 11 3071 0747 fax: +55 11 3071 4766

Shanghai tel: +86 21 6393 3333 fax: +86 21 6393 7890

Singapore tel: +65 6536 0606 fax: +65 6533 2107

Sydney tel: +61 2 9220 8777 fax: +61 2 9220 8765

Tokyo tel: +81 3 5501 9240 fax: +81 3 5501 9211

Washington, D.C. tel: +1 202 719 5000 fax: +1 202 719 5001