house prices bubbles and their determinants in the czech republic and its regions luboš komárek...

TRANSCRIPT

House Prices Bubbles and their Determinants in the Czech Republic and its Regions

Luboš Komárek and Michal HlaváčekCzech National Bank

Prague

Based on CNB WP 12/2009The views expressed in this presentation are not

necessarily those of the Czech National Bank.

How we see our house….

... as seen by those interested in buying it, ...

... as seen by your bank, ...

... as seen by an appraiser ...

... and how the tax office sees it

7

O U T L I N E

• 1. Why to study house prices?• 2. Factors influencing house prices• 3. Sources of house price data in the Czech Republic• 4. Empirical analysis

4.1 Simple indicators

4.2 Time series analysis (the CR and Prague)

4.3 Panel Analysis (by districts)

• 5. Conclusion

8

1. Why study house prices? International comparision

• Until 2006- low price growth similar to GER or AT, 2007 renewed growth• In 2008- growth of prices in the CR despite price drops in the USA, Ireland, UK,

Spain, 2009 further price drops• House prices of our neighbors/ trade partners/ similar countries

Property prices - international comparisondeveloped countries (absolute index; 2006 Q1 = 100)

Source: BIS, CZSO, Case-Shiller (US), Nationwide (UK)

50

100

150

200

I/03 III I/04 III I/05 III I/06 III I/07 III I/08 III I/09 III I/10

CZ UK FR IE USAES AT GER

Property prices - international comparisonCEECs (absolute index; 2006Q1 = 100)

Source: BIS, CZSO, national central banks and statistical offices

50

100

150

200

I/03 III I/04 III I/05 III I/06 III I/07 III I/08 III I/09 III I/10

CZ HU SK PL LT LV BG

9

Why to study house prices? (II)

• Role of house price bubbles and mortgage loans in recent financial crisis- Could this happen in the CR?

• Macroeconomic impacts of bursting of such bubbles are higher than for bubbles for other asset classes (e.g. stocks) because these effects:

(i) last longer (4 Y compared 1.5 Y for stock market), (ii) present larger threat for the FS of giver country/region because

house pricesa) form the biggest part of HH wealthb) influence HH consumption via wealth effectb) function as collateral in balances of banking sector

10

1. Why study house prices? Impact to the Czech Republic

• High growth of house prices in 2H2006-2008• Growth of household loans for house purchases• Long horizon of those loans- increased probability of mis-pricing,

change of conditions of HH, …• House prices might influence PD and LGD• Record housing construction• Dynamics of loans to developers- again risk to banks• Potential mutual relationship between housing prices and housing

loans

11

1. Why study house prices? Complications for the analysis

• Complications for house price analysis • Standard problems: market heterogeneity (size, location,

depreciation…), lower quality of data• Transitive problems: converge character of the Czech

Economy (catching-up effect), development of the mortgage market, increases im housing quality, distortion effects arising from rent deregulation

12

2. Factors Determining Housing Prices

• Supply factors (conditional on profitability of construction industry; Supply inelastic in the short term):

• Saturation of housing needs and its dynamics (number of existing and newly finished apartments; (-)

• Cost factors (building plots prices; building construction costs); (+)

• Demand factors: • Disposable income of households (wage); (+)• Unemployment rate (-)• Ratio of economic activity, number of vacancies (+)• Demographic factors: Divorces (+), marriages (+), natural population

growth and migration (+)• Financial market development (+)• Interest rate (-)• Rents (+)

13

3. Sources of Housing Price Data in the CR

• Two basic types of data:• Transfer prices: CZSO- from 1998, but time lag• Supply prices: CZSO, IRI, Dolanský (Realit), King Sturge

• Tax evasion vs. Unrealistic advertisements, Completeness, Averages vs. Selected prices vs. Hedonic indexes

Apartment prices in Prague (2007 Q1=100)

Source: CZSO, IRI, Realit

70

80

90

100

110

120

130

140

150

I/04 III I/05 III I/06 III I/07 III I/08 III I/09 III I/10 III

CZSO transfer CZSO supply

IRI supply Dolanský supply

Apartment prices in the rest of the CR (2007 Q1=100)

Source: CZSO, IRI, Realit

70

80

90

100

110

120

130

140

150

I/04 III I/05 III I/06 III I/07 III I/08 III I/09 III I/10 IIICZSO transfer CZSO supply

IRI supply Dolanský supply

14

House Price variability and the variability of its possible determinants is often higher across regions than across time.

Descriptive statistics (figures for average region; annual data for 1998-2008)

Variable Unit Mean Median

Variability over time

(%) b)

Variability across regions

(%) b)

Apartment prices a) Kč/m213 000 12 128 27.4 37.6

Building plots prices a) Kč/m2 1 338 1 090 15.5 66.5

Apartment construction prices a) Kč/m2 23 369 22 756 4.5 10.3Completed apartments (without family houses)% of hous. stock 0.32 0.31 27.5 59.2No. of apartments per 1,000 inhabitants number 428.7 429.6 2.0 5.9

Marriages % of MYP 0.52 0.51 5.0 6.2Divorces % of MYP 0.30 0.30 9.3 14.3Natural population growth % of MYP -0.05 -0.08 238.0 166.9Net migration % of MYP 0.14 0.07 194.3 607.0Unemployment rate % 7.30 6.59 19.7 38.5Economic activity rate of population % 59.7 59.5 1.7 2.4Vacancies/labour force % 0.35 0.29 48.9 37.3

Average monthly wage a) CZK 13 458 13 385 13.0 11.0

Rent per month a) CZK/m2 75.0 72.6 14.2 27.5Loans a)

CZK millions 15 235 8 354 82.9 112.1

Source: CZSO, CNB, IRI

Notes: a) In 1998 pricesb) Variability computed as standard deviation in % of mean

MYP denotes mid-year population

Supp

ly

fact

ors

Dem

and

fact

ors

3. Sources of Housing Price Data in the CR

15

4.1 Empirical analysisSimple indicators of house price sustainability: Rental Return

• Rental return is inverse value to price-to-rent ratio

• 2007/08- Due to increase of prices decrease of the rent returns

• …despite increase of yields by alternative assets and interest of house purchase loans

• 2009/10- situation better

Rental returns (averages for period in %; comparison with yields on

10Y government bond and house purchase loan rates)

Source: IRI, CNB

3

5

7

9

11

2004 2006 II/07 IV II/08 IV II/09 IV II/10

Praha BrnoOstrava Liberec10Y yield Interest housing loansÚstí nad Labem

16

• Decrease of ratio in 2003-2006- due to wage growth

• 2007/8- Price growth higher than growth of wages

• Regions with lower wages have lower price-to-income ratio

• Prague as the most risky region.

4.1 Empirical analysisSimple indicators of house price sustainability: Price-to-Income

Price-to-income ratios

(ratio of price of 68 m2 apartment to wage for last 4 quarters)

Source: CZSO, CNB calculationNote: 2009 and 2010 data preliminary or calculated from supply prices

1

3

5

7

9

11

I/00 IV III II I/03 IV III II I/06 IV III II I/09 IV III

Czech Republic Prague Brno

Ústí n.L. Hradec Králové Ostrava

17

4. Empirical Analysis 4.2 Time series analysis:

overall regression statistics for the CR and for Prague

• Period of: 1998 Q1 – 2009 Q2, 46 Q observations, differences, real variablesVariable

Apartment prices a Coefficient Std. dev. b Coefficient Std. dev. b Coefficient Std. dev. b

Building plots prices a 0.481* 0.240 - - - -

Construction output price index a -0.576 0.504 0.764 0.492 0.263 0.685

Completed apartments a,c 0.000 0.000 0.000 0.000 0.000 0.000No. of apartments per 1,000 inhabitants 0.000 0.001 0.001 0.001 0.001 0.001

Marriages c 0.963 0.968 0.650 1.228 1.249 0.886Divorces 0.120 0.496 0.107 0.575 0.147 0.661Natural population growth c 0.665 0.528 0.703** 0.335 0.599* 0.320

Net migration 0.100* 0.057 0.068 0.095 0.011 0.019

Unemployment rate 0.004 0.006 0.001 0.006 -0.0385* 0.021

Economic activity -0.0055 0.006 -0.007 0.005 -0.0087* 0.005Vacancies/labour force 0.101** 0.049 0.132** 0.050 -0.016 0.042

Average monthly wage a,c 1.215*** 0.424 1.239* 0.641 0.398 1.393

Rent per month a 0.459** 0.195 - - - -

Loans a 0.048 0.061 0.006 0.080 0.099 0.2091Y Pribor 0.003 0.003 0.003 0.005 0.000 0.006Ratio of FDI to GDP 0.000 0.001 0.001 0.0010 0.001 0.0009

Adjusted R2 0.54 0.19 0.07Durbin-Watson statistic 1.78 1.22 1.23

CZ - Estimate A Prague - Estimate BCZ - Estimate B

18

4. Empirical Analysis 4.2 Time series analysis:

overall regression statistics for the CR and for Prague

• Period of: 1998 Q1 – 2009 Q2, 46 Q observations, differences, real variables

Apartment prices in the Czech Republic (CZK thousands per m2)

Source: CZSO, CNB calculation

5

10

15

20

1998 2000 2002 2004 2006 2008

Actual prices Regression estimate HP estimate

Gap in prices in the Czech Republic - deviation of actual prices from estimate in CZK thousands per m2(dashed lines indicate 10% confidence interval)

-2.5

-1.5

-0.5

0.5

1.5

2.5

1998 2000 2002 2004 2006 2008Regression gap HP filter gap

19

4. Empirical Analysis 4.3 Panel data analysis:

compared to OLS on differences (whole CR)

Variable

Apartment prices OLS PR OLS PR OLS PR

Apartment prices a x 0.938*** x 0.776*** x 0.859***Building plot prices b 0,633 1.223* x x x xApartment construction prices b 0,016 0,007 0,012 0,001 0,014 0,019Completed apartments -1,158 0,402 -16,161 -0,598 -11,456 5,813No. of apartments per 1,000 inhabitants -0.148*** -0,031 -0.297*** -0,155 -0.295*** -0,411Marriages -0,504 3,006 1,178 -66,890 -3,932 -49,907Divorces 50.739** 82.321** 76.245*** 75,974 68.843** 71,099

Natural population growth 38.941*** 70.323*** 16,269 56.733** 34.292** 78.167***Net migration 3,902 6,983 9.540* 15.395** 9,479 9,995

Unemployment rate -1.407*** -2.155*** -2.675*** -4.406*** -2.487*** -4.106***

Economic activity rate of population -1,005 0,880 -0,512 1,220 -0,636 1,342

Vacancies/labour force 11.958** 3,985 13.444* 7,303 8,127 2,086

Average monthly wage b 1.807*** 2.001*** 2.756*** 3.017*** 2.499*** 3.179***Rent per month b 102.285*** 95.205*** x x x xLoans b 0.048* -0,011 0.071** 0,013 0,095 0,0441Y Pribor 1,515 1,958 2,066 1,311 2,693 1,899

CZ - Estimate A CZ - Estimate B CZ excl. Prague - Estimate B

20

4. Empirical Analysis 4.3 Panel data analysis:

overall regression statistics for the CR and for Prague

• Panel regression across regions

-1500

-1000

-500

0

500

1000

1500

5 000 15 000 25 000 35 000 45 000

2007 apartment price (in CZK per m2)

Ave

rag

e r

esi

du

al (

in C

ZK

pe

r m

2)

U

A

Source: CZSO, IRI, CNB, CNB calculationNote: Region abbreviations given in abbreviations list.

T

C

J

L

E

P

K

O

Z

H

B

Apartment price overvaluation relative to apartment price(average residual for 1998-2008)

Apartment price gaps in the CR – devations of actual prices from estimates(CZK th. per m2; positive values overvaluation, negative undervaluation)

Source: CZSO, CNB calculation (WP 12/2009)

-2,5

-1,5

-0,5

0,5

1,5

2,5

I/98 IV III II I/01 IV III II I/04 IV III II I/07 IV III II/09

Gap time series HP filter gap Gap panel regression

21

5. Conclusion

• House Price determinants• Demographic factors: confirmation of positive influence of net

population growth and partly also migration and divorces. • Supply Factors: mixed evidence- significant building plots prices. • Demand Factors: significant influence of wage growth and rents,

partly unemployment.• Our estimate identified (in line with expectations) a bubble in house

prices for 2002/03 and for 2007/08. • However, in the second period the level of overvaluation much

lower despite similar house price dynamics in both periods. • Panel regression has shown that regions with higher prices are

more likely to be over-valued.• … with the exception of Prague. .

Thank you for your attention!

www.cnb.cz

Luboš KomárekCzech National Bank

Michal HlaváčekCzech National Bank

23

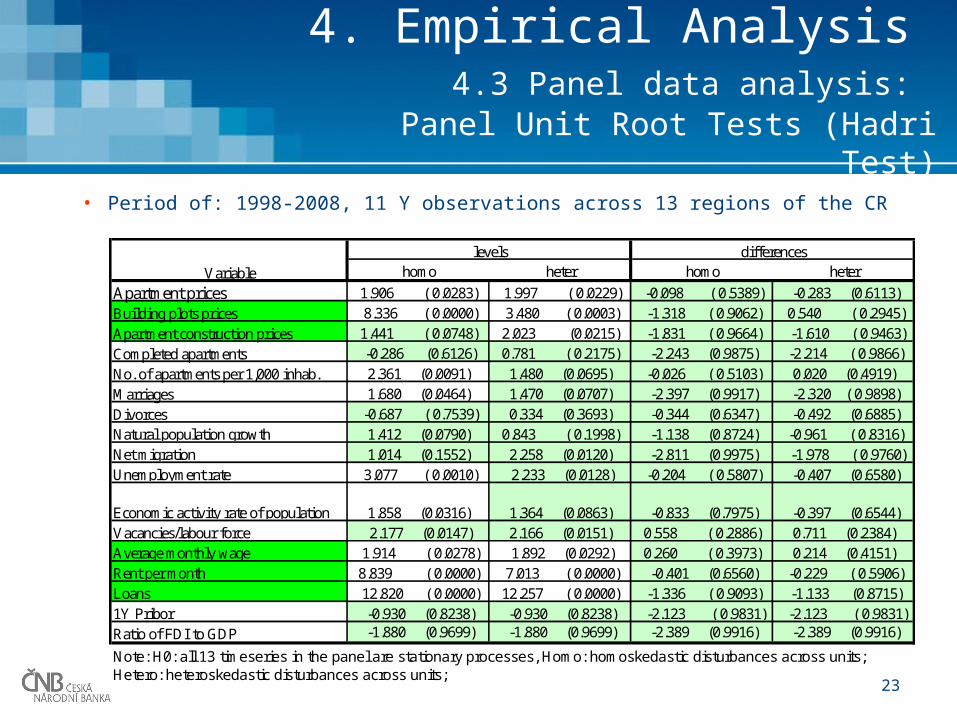

4. Empirical Analysis 4.3 Panel data analysis:

Panel Unit Root Tests (Hadri Test)

• Period of: 1998-2008, 11 Y observations across 13 regions of the CR

homo heter homo heter

Apartment prices 1.906 ( 0.0283) 1.997 ( 0.0229) -0.098 ( 0.5389) -0.283 (0.6113)

Building plots prices 8.336 ( 0.0000) 3.480 ( 0.0003) -1.318 ( 0.9062) 0.540 ( 0.2945)

Apartment construction prices 1.441 ( 0.0748) 2.023 (0.0215) -1.831 ( 0.9664) -1.610 ( 0.9463)

Completed apartments -0.286 (0.6126) 0.781 ( 0.2175) -2.243 (0.9875) -2.214 ( 0.9866)

No. of apartments per 1,000 inhab. 2.361 (0.0091) 1.480 (0.0695) -0.026 ( 0.5103) 0.020 (0.4919)

Marriages 1.680 (0.0464) 1.470 (0.0707) -2.397 (0.9917) -2.320 ( 0.9898)

Divorces -0.687 ( 0.7539) 0.334 (0.3693) -0.344 (0.6347) -0.492 (0.6885)Natural population growth 1.412 (0.0790) 0.843 ( 0.1998) -1.138 (0.8724) -0.961 ( 0.8316)Net migration 1.014 (0.1552) 2.258 (0.0120) -2.811 (0.9975) -1.978 ( 0.9760)Unemployment rate 3.077 ( 0.0010) 2.233 (0.0128) -0.204 ( 0.5807) -0.407 (0.6580)

Economic activity rate of population 1.858 (0.0316) 1.364 (0.0863) -0.833 (0.7975) -0.397 (0.6544)Vacancies/labour force 2.177 (0.0147) 2.166 (0.0151) 0.558 ( 0.2886) 0.711 (0.2384)Average monthly wage 1.914 ( 0.0278) 1.892 (0.0292) 0.260 ( 0.3973) 0.214 (0.4151)Rent per month 8.839 ( 0.0000) 7.013 ( 0.0000) -0.401 (0.6560) -0.229 ( 0.5906)Loans 12.820 ( 0.0000) 12.257 ( 0.0000) -1.336 ( 0.9093) -1.133 (0.8715)1Y Pribor -0.930 (0.8238) -0.930 (0.8238) -2.123 ( 0.9831) -2.123 ( 0.9831) Ratio of FDI to GDP -1.880 (0.9699) -1.880 (0.9699) -2.389 (0.9916) -2.389 (0.9916)

Note: H0: all 13 timeseries in the panel are stationary processes, Homo: homoskedastic disturbances across units; Hetero: heteroskedastic disturbances across units;

levels differences

Variable

Determining the equilibrium prices is tough task