how do strategic repositioning moves impact the ... · how do strategic repositioning moves impact...

TRANSCRIPT

1

HOW DO STRATEGIC REPOSITIONING MOVES IMPACT THE EFFECTIVENESS

OF FIRM’S IT GOVERNANCE, RISK, AND CONTROL MECHANISMS?

By

Hüseyin Tanriverdi

The University of Texas at Austin

Red McCombs School of Business

Information, Risk and Operations Management (IROM) Department

1 University Station, B6500, CBA 5.208

Austin, Texas 78712-0212

+1 (512) 232-9164

&

Kui (Andy) Du

College of Management

University of Massachusetts Boston

100 Morrissey Blvd

Boston, MA 02125

October 19, 2016

Under Revision

Limited circulation for feedback

Please do not cite or circulate without the permission of authors

2

HOW DO STRATEGIC REPOSITIONING MOVES IMPACT THE EFFECTIVENESS

OF FIRM’S IT GOVERNANCE, RISK, AND CONTROL MECHANISMS?

ABSTRACT

In an increasingly digitized economy, undesired IT events such as data security and privacy

breaches, digital fraud, and operational IT glitches have emerged as wicked IT-related risks. Firms

institute IT governance, risk, and control (IT-GRC) mechanisms to defend against such IT-related

risks. However, the pervasiveness of the undesired IT events indicates that firms struggle to

maintain effective IT-GRC mechanisms. This study explains how and why a firm’s own strategic

repositioning moves could reduce the effectiveness of the firm’s IT-GRC mechanisms. A firm is

a complex adaptive system operating in a complex, and dynamically changing environment. To

seize emerging opportunities or cope with unexpected threats in the environment, a firm makes

adjustments to the strategic positions of its business portfolio. For example, it diversifies into new

product market positions in domestic and foreign markets; it engages in mergers and acquisitions;

it divests some of its existing businesses; and it internally restructures its business portfolio. We

hypothesize that such strategic repositioning moves could disrupt and reduce the effectiveness of

the firm’s current IT-GRC mechanisms and make it challenging to design and operate new IT-

GRC mechanisms effectively. We find empirical support for these ideas in a longitudinal study of

2,248 publicly traded U.S. firms. We discuss the implications of these findings for IS research and

practice.

Keywords: IT risks, IT Governance, Risk and Control, Diversification, Acquisition, Divestiture,

Restructuring, Complexity

3

HOW DO STRATEGIC REPOSITIONING MOVES IMPACT THE EFFECTIVENESS

OF FIRM’S IT GOVERNANCE, RISK, AND CONTROL MECHANISMS?

The very digital technologies that open up productivity, profitability, and growth opportunities

for firms also expose firms to major IT-related risks such as data security and privacy breaches,

digital fraud, deception, theft, and disruptions through operational IT glitches (IIA 2012). The year

2014 was dubbed as “the year of the data breach.” Cyberattacks compromised the security and

privacy of over a billion personal data records in publicly traded firms such as Target, Home Depot,

JPMorgan and eBay.1 As digital spend has increased, so has the digital fraud. For example, $1 out

of every $3 spent on digital ads is lost to ad fraud.2 Glitches in IT operations have also risen. In

2015, computer glitches forced the United, Southwest, and American Airlines to ground or delay

large percentages of their flights.3 Such IT-related risks also expose firms to strategic, financial,

operational, and regulatory compliance risks.

To defend against the IT-related risks, firms institute IT governance, risk, and control (IT-GRC)

mechanisms4 . IS practice classifies IT-GRC into: (i) IT general controls (ITGC) and (ii) IT

application controls, also known as automated process controls (APC). ITGC aims to mitigate risks

in the firm’s general computing environment. It includes the firm’s strategic IT plans, IT policies,

procedures, standards, and processes. ITGC governs and controls the firm’s IT infrastructures,

applications, computer operations, IT human resources, IT program development, IT change

management, and the segregation of IT duties. APC aims to mitigate risks in the IT applications

that automate business processes of the firm. It includes input controls, processing controls, output

controls, and segregation of duty controls embedded in the applications that support business

1 http://www.cnbc.com/2015/02/12/year-of-the-hack-a-billion-records-compromised-in-2014.html 2 http://adage.com/article/digital/ad-fraud-eating-digital-advertising-revenue/301017/ 3 http://money.cnn.com/2015/10/11/news/companies/southwest-technical-issues-flight-delay/ 4 Appendix A provides a list of common IT-GRC mechanisms used by firms and external audit firms.

4

processes. These IT-GRC mechanisms seek to ensure the confidentiality, integrity, accessibility,

and privacy of the firm’s data. They also seek to ensure the continuity of the firm’s business.

Ultimately, the IT-GRC mechanisms seek to minimize the probability of loss and the magnitude

of loss associated with IT-related risks of the firm.

However, firms struggle to maintain effective IT-GRC mechanisms. The proliferation and

increasing frequency of data security and privacy breaches, digital fraud, digital deception, digital

theft, and operational IT glitches all point to weaknesses in IT-GRC mechanisms of firms. This

paper seeks to explain why firms struggle to maintain effective IT-GRC mechanisms.

An obvious explanation could be that firms may not be instituting IT-GRC mechanisms. While

this explanation was partially valid until early 2000s, it is no longer valid. Due to increasing IT-

related risks in the environment, a multitude of laws, regulations, and industry standards have been

instituted to require firms in general, and publicly traded firms in particular, to institute IT-GRC

mechanisms. For example, the Sarbanes-Oxley (SOX) Act of 2002 mandates that the CEO and

CFO of public firms be held personally accountable for instituting and effectively operating

internal controls over financial reporting including IT-GRC (Li et al. 2012; Li et al. 2010; Masli

et al. 2016). Periodically, executives as well as the independent external auditors of the firms assess

the design and operating effectiveness of the firms’ IT-GRC mechanisms for compliance with a

multitude of relevant laws, regulations, and industry standards (e.g., SOX, HIPAA, GLB,

PCI/DSS, etc.).5

In SOX audits, the finding of a material weakness, the most severe type of control deficiency,

in internal controls of a firm, including the IT-GRC, could have serious consequences for the firm,

its investors, and it top executives. After the enactment of SOX, the quality of Internal Controls

5 SOX: The Sarbanes–Oxley Act; HIPAA: The Health Insurance Portability and Accountability Act; GLB: The Gramm-Leach-

Bliley Act; PCI/DSS: The Payment Card Industry Data Security Standard.

5

over Financial Reporting (ICFR) became highly visible to capital markets. Failing to maintain an

effective ICFR, including an effective IT-GRC, elicits negative reactions from the capital markets

(Beneish et al. 2008; Hammersley et al. 2008); increases noise in accounting information of the

firm and causes unintentional accounting and forecasting errors (Ashbaugh-Skaife et al. 2008;

Feng et al. 2009); increase firm’s compliance costs (Hogan and Wilkins 2008; Krishnan et al. 2008;

Raghunandan and Rama 2006); increase firm’s cost of capital (Ashbaugh-Skaife et al. 2009); and

leads to more frequent executive turnover (Johnstone et al. 2011; Li et al. 2010; Masli et al. 2016).

Under certain circumstances, it can also lead to the de-listing of the firm from the stock exchange.

The CEO and CFO of the firm could be fined up to $5 Million and sent to jail for up to 20 years.

IS researchers who focus on consequences of ineffective IT-GRC mechanisms find that firms

that have material weaknesses in their IT-GRC mechanisms: (1) are not able to make accurate

management forecasts (Li et al. 2012); (2) are more likely to terminate the employments of their

CEOs and CFOs (Masli et al. 2016) who in turn have a hard time in finding comparable jobs

(Haislip et al. 2015); (3) report lower accounting earnings and lower market valuations (Stoel and

Muhanna 2011); (4) have less ability to pay their debts (Kuhn et al. 2013); and (5) and end up

reporting more material weaknesses and misstatements than firms which do not have material

weaknesses in their IT controls (Klamm and Watson 2009).

Given what is at stake for the firm and the executives, a more plausible explanation could be

that firm institutes the IT-GRC mechanisms required by the relevant laws, regulations, and

industry standards, but that the mechanisms become ineffective over time. If the firm’s business

is changing dynamically to adapt to the changes in the environment, the IT-GRC mechanisms can

fail to catch up with the changing business objectives, risk profile, and the new IT-GRC needs of

the firm. In this study, we focus on this explanation. We seek to identify strategic repositioning

6

moves of the firm that have unintended negative impacts on the effectiveness of the firm’s IT-

GRC mechanisms.

We ground our theoretical development in complexity science. We view both firms and their

competitive environments as complex adaptive systems (CAS). As the complexity level in the

external CAS increases, firms face adaptive tension (Boisot and McKelvey 2011). They address

the adaptive tension by adjusting the variety and complexity levels within their internal CAS

(Ashby 1956). They make strategic repositioning moves that add new businesses to their business

portfolio or delete some of the existing ones. An unintended consequence of such strategic

repositioning moves is that they change the business objectives and the risk profile of the firm.

Accordingly, they also change the IT-GRC requirements of the firm. Thus, we expect strategic

repositioning moves to significantly disrupt and reduce the effectiveness of the firm’s IT-GRC

mechanisms.

In complex dynamically changing environments, firms make diversification and merger and

acquisition (M&A) moves to add new businesses to adjust the internal variety and complexity of

their business their portfolios. Such moves have significant implications for IT integrations across

the old and the newly added businesses, which could disrupt the existing IT-GRC mechanisms of

the firm (Tanriverdi 2005; Tanriverdi and Uysal 2011; Tanriverdi and Uysal 2015). Firms also

make divestiture moves to sell off some of their businesses and focus their business portfolios.

However, carving out and separating previously integrated IT systems of the divested unit often

proves problematic to the remaining businesses, and hence, it could disrupt the effectiveness of

IT-GRC mechanisms (Tanriverdi and Du 2009). Firms also make internal restructuring moves to

redefine the relationships among their businesses in ways to match the changing complexity level

in the environment (Eisenhardt and Brown 1999). Such restructuring initiatives could also disrupt

7

and reduce the effectiveness of IT-GRC mechanisms.

In section II, we review the theoretical foundations in which the proposed theory will be

grounded. In section III, we develop hypotheses to explain how and why strategic repositioning

moves impact the effectiveness of the IT-GRC mechanisms. In section IV, we present the sample,

data, and procedures used for testing the hypotheses, and present the results. In section V, we

discusses the contributions and implications of the proposed theory for IS research and practice.

THEORETICAL FOUNDATIONS

Management control theory provides the theoretical underpinnings of our dependent construct,

IT-GRC mechanisms. IS literatures on governance, control and risks provide the foundations for

different types of IT-GRC mechanisms. Complexity science provides the theoretical foundations

for developing the nomological links between our independent constructs, strategic repositioning

moves of firms, and our dependent construct, the effectiveness of IT-GRC mechanisms.

Management Control Theory

Firms have business objectives such as profitability, growth, and shareholder wealth creation.

However, there is a multitude of hurdles that could inhibit the achievement of those business

objectives: e.g., technical risk, financial risk, operational risk, regulatory compliance risk, etc. Risk

is defined as the probability of loss and the magnitude of loss (Tanriverdi and Ruefli 2004).

Management control systems aim to avoid or minimize such hurdles, and enable the firm to achieve

its business objectives.

Management control systems refer to a wide range of formal and informal governance and

control mechanisms (Simons 1991). Informal mechanisms include leadership, culture, values, and

norms (Macintosh 1994). Formal mechanisms include agreements and assumptions about firm’s

business objectives and the risks that could potentially inhibit their achievement (Goold and Quinn

8

1990). Then, managers institute formal GRC or internal control mechanisms to provide reasonable

assurance (not absolute assurance) for the achievement of the business objectives and the

minimization of the risks. The scope of the GRC mechanisms usually covers: (i) effectiveness and

efficiency of operations, (ii) reliability of financial reporting, and (iii) compliance with applicable

laws and regulations (COSO 1992). After designing and implementing the GRC mechanisms,

managers also continuously monitor their operating effectiveness (Eisenhardt 1985; Ouchi and

Maguire 1975). If there are deviations from the desired business objectives, managers intervene

by imposing sanctions, redesigning the GRC mechanisms, changing the objectives, etc. (Goold

and Quinn 1990).

Information Systems Literature on IT-GRC Mechanisms

In an increasingly digital world, firms digitize their products, services, business processes, and

relationships with their customers and business partners. While digitization offers many business

benefits and opportunities, it also increases IT-related risks such as data security and privacy

breaches, digital fraud, and operational IT glitches (IIA 2012). Hence, IT becomes an increasingly

critical component of a firm’s management control systems (Weidenmier and Ramamoorti 2006).

Consistent with the management control theory, IS research and practice recommend IT-GRC

mechanisms for mitigating IT-related risks of firms in: (i) the general computing infrastructure of

the firm, and (ii) the IT applications that automate and support the firm’s business processes (IIA

2008; IIA 2009; IIA 2012).

IT general controls (ITGC). In the general computing infrastructure of the firm, the firm

faces many risks in: (i) planning and organizing its IT assets, (ii) acquiring and implementing the

IT assets, (iii) delivering and servicing the IT solutions, and (iv) monitoring if the general

computing infrastructure of the firm operate as intended on an ongoing bases (ITGI 2007).

9

The IS literature on IT governance, control, and security focus on such ITGC risks: e.g., IT

investment risks, IT application development risks, IT implementation risks, IT operational failure

risks, IT security risks, IT outsourcing risks, etc. (e.g., Barki et al. 2001; Keil et al. 1998; Lyytinen

et al. 1998; Weill and Broadbent 1998). To mitigate the ITGC risks, IS researchers suggest various

IT-GRC mechanisms such as aligning business and IT strategies and investment objectives

(Henderson and Venkatraman 1993); setting up IT governance structures (Sambamurthy and

Zmud 1999; Weill and Ross 2005); choosing proper control modes to regulate individual behaviors

and obtain desired behaviors in software development projects and IT implementation projects

(e.g., Kirsch 1996; Kirsch 1997); establishing IT security policies, training users for IT security

awareness, and establishing security countermeasures (e.g., D'Arcy et al. 2009; Ransbotham and

Mitra 2009; Straub 1990). IS practice also suggests IT-GRC mechanisms for IT human resource

management, IT documentation, IT program change management, segregation of IT duties, backup

and recovery, and business continuity (ITGI 2007).

Automated process controls (APC). Firms also face IT-related risks in IT applications that

automate their business processes. For example, input data going into an IT application might be

at risk of being invalid, incorrect, incomplete or unauthorized. The processing logic embedded in

the IT application might be at risk of not following the most up-to-date business rules and look-up

tables, not handling the exceptions, and hence, not being valid. The outputs coming out of the IT

application might be at risk of not being valid, not displaying the relevant outputs, or not being

accurate (IIA 2009). In addition, if the duties of users who have access rights to the IT applications

are not segregated properly, opportunities for fraud could be created. For example, if a user, who

has access rights to create vendors in the system, is also mistakenly given access rights to pay

vendors, opportunity is created for fraud. The user can create fake vendors and pay himself. To

10

mitigate such risks, firms embed automated process controls (APC) into the IT applications. APC

cover input controls, processing controls, outcome controls, and segregation of duty controls (IIA,

2009).

Managers inject explicit business rules, norms, roles, process prescriptions, and APCs into IT

applications (Gosain 2004). Then, the IT applications monitor and regulate the inputs, outputs, and

processing integrity of the business processes in real time. Automating the process controls offer

many benefits such as continuous auditing, remote monitoring, real-time alerts on errors and

glitches, and automatic match, validation, and reconciliation of different data sources (Hansen and

Hill 1989). For example, one IT application can automatically validate a payment transaction prior

to the actual payment by matching the purchase order, the receiving report, and the invoice from

vendors, raise a flag and alert management if exceptions are identified. In addition to automating

preventive controls, APC also increases the effectiveness of detective and corrective controls by

increasing the traceability of business transactions through recording of audit trails or logs along

with the execution of each business transaction (Weber 1982). To automate business processes,

managers standardize and document the inner workings of, and the interfaces among, processes,

which further increase the transparency and thus the auditability of business processes (Chapman

and Kihn 2009).

Complexity Science

Complexity is a property of a system that is made up of a large number of parts that interact

with each other in non-linear ways (Maguire 2011). The focal complex system of interest in this

study is a firm, which is made up of businesses. The parts of this complex system are the business

units. Relationships among the business units (e.g., resource sharing) are the interactions among

the parts (Eisenhardt and Piezunka 2011). Business units are heterogeneous, intelligent, and

11

adaptive parts. They can observe and interpret stimuli from each other and from the environment.

They can learn, change their behaviors, and adapt to the changes in the environment intelligently

(Casti 1997; Holland 1995). Business units can also have agency. They can pursue their own self-

interests rather than the strategies, objectives, and prescribed behaviors of the corporate center of

the firm. While the corporate center emphasizes cross-business synergies to maximize the overall

performance of the corporation (Tanriverdi 2005), individual business units can forego the

synergies and seek to maximize their own performance, which is suboptimal for the performance

of the corporation (Campbell et al. 2014). Thus, there is constant tension between the business

units and the corporate center as to which objectives the business units ought to pursue. This is

important for our theory because the changing business objectives change the risk profile of the

firm, which in turn changes the IT-GRC needs of the firm.

The competitive environment in which the firm operates is also a complex adaptive system

(CAS). The parts of the external CAS are customers, markets, rival firms, regulators, etc.

Competitive actions and reactions of rival firms, changing customer needs, market conditions, and

regulations are the interactions among the parts of the external CAS. As the complexity in the

external CAS changes, firms face adaptive tension (Boisot and McKelvey 2011). Ashby (1956)

law of requisite variety suggests that firms can address the adaptive tension by adjusting their

internal complexity. Indeed, managers adjust internal structures of their firms based on the

complexity and uncertainty levels in the external environment (Davis et al. 2009). Managers

strategically reposition their business portfolios. They reconfigure the composition of the

businesses in the portfolio (parts) and the nature of the relationships (interactions) among them in

order to adjust the variety and complexity levels of their internal CAS in ways to match the external

CAS. Such strategic repositioning moves are likely to change the business objectives, risk profiles,

12

and hence, IT-GRC needs of the firm.

In this study, we build on the corporate strategy literature to identify the strategic repositioning

moves that enable managers to adjust the complexity level of their internal CAS (Campbell et al.

2014; Eisenhardt and Brown 1999; Ramanujam and Varadarajan 1989). First, firms increase their

internal variety and complexity by adding new businesses (new parts) to their business portfolios.

They do so through organic diversification moves or mergers and acquisitions. Further, firms can

diversify within domestic markets or foreign (international) markets. Second, firms strategically

decide on the nature of the relationships (interactions) among the businesses in their portfolio.

They either create related, synergistic business portfolios (tight interactions) or diverse, unrelated

business portfolios (loose interactions). Third, firms decrease their internal variety and complexity

by exiting some of their businesses (parts) through divestiture moves. They cut the relationships

(interactions) between the divested business and the rest of the business portfolio. Fourth, firms

make internal restructuring moves to patch and restitch a continually shifting mix of businesses in

their portfolios to match the changing complexity in the external environment (Eisenhardt and

Brown 1999). In the next section, we explain how and why these strategic repositioning moves are

likely to impact the effectiveness of IT-GRC mechanisms.

HYPOTHESES DEVELOPMENT

Corporate Diversification and the Effectiveness of IT-GRC Mechanisms

A key element of a firm’s corporate strategy choices is where to position and play. Some

firms choose to focus on one industry position or a limited number of industry positions while

others diversify across multiple industry positions (Campbell et al. 2014). Diversification is

defined as the entry of a firm into new lines of businesses that entail changes in the firm’s

administrative structures, systems, and other management processes (Ramanujam and Varadarajan

13

1989). Firms diversify for both proactive and defensive reasons. Diversification can enable a firm

to seize emerging new opportunities in a dynamically changing environment. Diversification can

also enable the firm to diversify its cash flow risks. While cash flows from some businesses can

decline, cash flows from other businesses can increase and smooth out the overall cash flows of a

diversified firm. The firm can strategically adjust its diversification level up or down over time to

adapt to the changing variety and complexity levels in the external CAS.

Increasing diversification level increases the variety and complexity of a firm’s internal CAS

by adding more parts (businesses) to it. While it helps to match the variety and complexity of the

external CAS, increasing diversification level also increases the scope and diversity of the

businesses in the firm’s business portfolio and puts strains on the firm’s administrative structures,

managerial systems, processes, and controls (Chandler 1962). In response, the firm seeks to expand

the scope of its IT environment to accommodate the increased communication, coordination, and

knowledge management needs of its business portfolio (Tanriverdi 2005; Tanriverdi 2006).

Accordingly, the IT-GRC mechanisms need to be revised or redesigned to accommodate the new

business objectives, the new risk profile, and the new IT-GRC needs of an expanded portfolio of

businesses. Such changes are likely to disrupt the firm’s IT-GRC mechanisms.

H1: Firms that have higher diversification levels are more likely to reduce the effectiveness of

their IT-GRC mechanisms.

Foreign (international) Operations and the Effectiveness of IT-GRC Mechanisms

The “direction of diversification” is another key element of a firm’s corporate strategy choices:

e.g., which customers and geographic markets to enter (Ramanujam and Varadarajan 1989). In an

increasingly global economy, boundaries of the firm’s external environment are no longer confined

to the domestic economy. Firms make strategic moves to take advantage of opportunities emerging

in foreign (international) economies as well. According to Goldman Sachs, S&P 500 firms

14

generated 33% of their aggregate revenues from foreign operations in 2014.6 Such statistics attest

to the pervasiveness and the importance of firms’ strategic repositioning moves to foreign markets.

Entry into foreign operations not only adds more parts (businesses and markets) to the internal

CAS of the firm, but it also increases the diversity of the parts and the interactions among the parts.

Diversity of the parts increases due to the differences in the institutional environments (e.g., laws,

regulations, intellectual property regimes, currencies), cultural environments (e.g., norms, beliefs,

language), and geographies (e.g., time zones) of the firm’s businesses and markets across the globe.

Diversity of the interactions among the parts also increases due to increasing resource flows and

arbitrage opportunities. For example, recent policy debates stemming from currency fluctuations

and tax differentials across world economies affect the strategic decisions and performance of not

only the foreign subsidiaries of a firm but also the entire firm. The increasing diversity of the parts

and the interactions within the firm’s CAS has significant implications for the IT environment and

IT-GRC mechanisms of the firm. IS researchers coined the term, “digitally-enabled, globally

extended enterprise” to emphasize the central role that IT plays in enabling foreign operations

(Krishnan et al. 2007). IT-GRC mechanisms which used to be optimized for the domestic

operations of the firm will need to take into account the new business objectives, new risk profiles,

and new IT-GRC needs of the newly added foreign operations. Such changes are likely to disrupt

the firm’s IT-GRC mechanisms.

H2: Firms that operate in foreign markets are more likely to reduce the effectiveness of their

IT-GRC mechanisms.

Corporate Acquisitions and the Effectiveness of IT-GRC Mechanisms

The “mode of diversification” is also a key element of the firm’s corporate strategy choices

(Ramanujam and Varadarajan 1989). In diversifying into a new market, the firm can either use the

6 http://www.businessinsider.com/foreign-revenues-by-region-2015-7

15

processes of internal business development or acquire an existing firm in that market. Increasing

costs of internal business development coupled with rapidly changing market conditions motivate

firms to rely more on corporate acquisitions as the mode of diversification (Ramanujam and

Varadarajan 1989). In acquisition transactions, acquirers often aim to integrate targets to achieve

synergy benefits. Most of the synergies are IT-dependent because administrative structures,

managerial systems, processes, and controls of modern firms are implemented in IT (e.g., Mehta

and Hirschheim 2007; Tanriverdi and Uysal 2011).

From a complexity perspective, the post-acquisition IT integrations are very challenging and

disruptive to both acquirers and targets (Tanriverdi and Uysal 2015). To start with, each firm is a

CAS. Bringing the two CAS together means that there will be disruptions to both (Allen et al.

2002). Even if the strategies, structures, processes, control systems, cultures, human resources, and

information systems of the two CAS were very similar, during the integration process there are

two competing parts for each new part of the integrated CAS. For example, there are two CIOs,

two sets of IT infrastructures, two sets of IT applications, etc. One of them will survive, the other

one will have to go; or both will have to go; or both will survive but will assume new roles and

functions. This is a highly political and emotional change management process in which both CAS

experience disruptions in creating the new CAS (Allen et al. 2002). The implication for IT-GRC

mechanisms is that the IT-GRC mechanisms of the acquirer and the target will also be disrupted,

but that the requirements of the new IT-GRC mechanisms of the merged CAS will not be clear

until after the rational, political, and emotional dynamics of the integration unfold and stabilize.

Thus:

H3: Firms that have higher M&A intensity levels are more likely to reduce the effectiveness of

their IT-GRC mechanisms.

Corporate Divestitures and the Effectiveness of IT-GRC Mechanisms

16

Corporate divestiture is the opposite “mode of diversification” in which a firm reduces the

scope and the diversification level of its business portfolio by selling some of its business positions

or assets to another firm (Brauer 2006). Firms often use divestitures to exit positions whose

profitability levels decline over time due to changes in the environment. By reducing the number

of parts in the firm’s internal CAS, divestiture can reduce the internal variety of the firm. However,

divestiture does not necessarily reduce the complexity level of the firm’s internal CAS.

Prior to the divestiture, the seller and the to-be-divested unit were in a parent-subsidiary

relationship. To be able to comply with the relevant laws and regulations, parent firms integrate

mundane support functions such as accounting, finance, HR, payroll, treasury, tax, etc., even

though the businesses in their portfolios are unrelated in terms of customers and products

(Tanriverdi 2005). Since the mundane support functions are implemented in IT systems and

applications, there is also IT integration between parents and business units. After the divestiture

transaction, the divested unit needs to be legally separated from the parent. Thus, the parent needs

to carve out and separate it from the shared support and IT services environment of the corporation.

Carving out and separating one of the parts of the firm’s internal CAS means that some of the

connections and interactions of the remaining parts need to be terminated, or rewired and redefined.

As the IT carve-out and separation process severs the previous connections and interactions, it

causes disruptions to both the parent and the divested unit (Tanriverdi and Du 2009). The previous

IT-GRC mechanisms, which were designed for a larger scope and diversity of businesses, also

need to be redesigned. The changing business objectives, risk profiles, and the IT-GRC needs of

the smaller, more focused portfolio of businesses is likely to disrupt the IT-GRC mechanisms.

H4: Firms that have higher divestiture intensity levels are more likely to reduce the

effectiveness of their IT-GRC mechanisms.

Corporate Restructuring and the Effectiveness of IT-GRC Mechanisms

17

Corporate restructuring refers to changes in administrative structures, management

systems, processes, and workforce reconfiguration moves of corporations (Brauer 2006; McKinley

and Scherer 2000). After a period of strategic repositioning moves such as the diversification,

foreign entry, M&A, and divestiture moves discussed above, the firm’s internal administrative

structures, systems, processes, and workforce skills are likely to lose coherence. Firm makes

corporate restructuring moves to patch and restitch the continually shifting mix of businesses to

better match its internal CAS better with the external CAS (Eisenhardt and Brown 1999). The

scope of changes in structuring is very large since the administrative structures, management

systems, processes, and workforce skills of the corporation are affected. Those changes also imply

major changes in the IT-GRC mechanisms. Thus, the risk of disruption to the IT-GRC mechanisms

is high.

H5: Firms that engage in corporate restructuring are more likely to reduce the effectiveness

of their IT-GRC mechanisms.

METHODS

Data and Research Context

The test of the proposed theory requires a longitudinal data set in which strategic repositioning

moves and IT-GRC effectiveness of firms could be measured. Data for measuring strategic

repositioning moves are available from Compustat, SDC platinum, and SEC’s EDGAR databases.

Longitudinal data on the effectiveness of IT-GRC mechanisms is available for publicly traded

firms in the US that are subject to the Sarbanes–Oxley (SOX) Act. Section 404 of SOX requires

publicly traded firms to design and effectively operate IT-GRC mechanisms, as part of their

internal controls, to ensure the accuracy and reliability of financial information generated through

the IT systems of the firm.

In SOX 404 compliance audits, external auditors evaluate hundreds of IT controls that

18

constitute a firm’s IT-GRC mechanisms, and issue an opinion about their overall effectiveness (Li

et al. 2012; Masli et al. 2016). They classify the severity of any IT control deficiencies into: (i)

lowest severity: ordinary deficiency (D); (ii) moderate severity: significant deficiency (SD); or (iii)

highest severity: material weakness (MW). If the IT control deficiencies remain at low (D) or

moderate (SD) severity levels, auditors conclude that the IT-GRC mechanism of the firm is

effective. They report the D and SD types of IT control deficiencies only to the management of

the firm. Thus, our dataset indicates that the firm’s IT-GRC mechanism is effective even when the

firm may have D and SD types of IT control deficiencies. If the auditors elevate the severity level

of IT control deficiencies to MW, they conclude that the IT-GRC mechanism of the firm is

ineffective. This means that the financial information that goes into the financial statements of the

firm is not reliable. This conclusion as well as the detail of the IT control deficiencies are reported

to the SEC and the investing public. Our dataset captures the MW type of IT control deficiencies.

Strategic repositioning moves of firm could potentially create D (low), SD (moderate), or MW

(high) types of deficiencies in the firm’s IT-GRC mechanisms. By capturing whether or not there

is any MW type of IT control deficiency in firms, our data allows the strongest possible test of the

proposed theory. If this dataset shows that the hypothesized strategic repositioning moves create

MW in IT-GRC mechanisms, it would imply that the hypothesized relationships are so strong that

they are detected with even the most severe type of IT control deficiencies.

Sample

Our sampling frame is the list of publicly traded firms in the U.S. stock markets. SOX 404

audit results of these firms are available in Audit Analytics, a premium public company

intelligence database. Our study timeframe ranges from firms’ fiscal year 2004, the first SOX

compliance year, to their fiscal year 2009. We use the “SOX 404 Internal Controls” section of the

19

database and rely on the independent auditor’s opinion rather than the management’s own opinion.

If a firm restates its SOX auditing reports several times for a particular year, we use the latest

available restatement.

We selected our sample based on three criteria. First, following previous studies in the SOX

context (e.g., Feng et al. 2015), we selected only those firms known as “accelerated filers,” which

are defined by the SEC based on the size of firms’ public shares.7 Second, we excluded foreign

firms that were listed in the U.S. stock markets. This criterion ensures that all firms in our sample

are U.S firms and that they are subject to the same regulatory environment.8 Third, following

previous studies (e.g., Iliev 2010), we exclude firms from the financial industry because they had

long been under other regulations similar to SOX.

We then collected further data from a variety of data sources for the computation of

independent and control variables, including Compustat, SDC platinum, SEC’s EDGAR, Bureau

of Economic Analysis’s industrial IT investment database, and the Information Week 500 annual

rankings. The final estimation sample consists of 2,475 firms with 10,938 observations across six

years (2004-2009).

Dependent Variables

Internal Control MW, Non-IT Control MW, and IT-GRC MW. While our primary

research interest is to develop and test the relationships between strategic moves and the

effectiveness of IT GRC mechanisms, our empirical investigation started by analyzing the

7 After the SOX Act was enacted in 2002, the regulator required publicly-traded firms with a public float of at least $75 million,

known as accelerated filers, to comply with the regulation in 2004, while non-accelerated filers did not have to comply before

2007. In addition, accelerated filers need to comply with both Section 404(a) and 404(b) of the SOX Act, while non-accelerated

filers only need to comply with 404(a). Thus, excluding non-accelerated filers can ensure the comparability of firms in our

sample. In addition, because we are theoretically interested in complexity, accelerated filers, which by definition are larger in size

than non-accelerated filers, provide a better empirical context for our hypothesis testing. 8 Foreign firms listed in the U.S. stock markets are also subject to the SOX rules but with a different deadline. While U.S.

accelerated filers need to comply with the regulation in 2004, foreign firms only need to submit their SOX 404 audit reports for

the fiscal year ending on or after 15 July 2006 (Piotroski and Srinivasan 2008).

20

influence of these moves on the overall internal control effectiveness. The relationships between

some of the strategic moves (diversification, foreign operation, acquisitions, and restructuring) and

the overall internal control systems have been empirically investigated in the accounting literature

(e.g., Ashbaugh-Skaife et al. 2007; Doyle et al. 2007; Ge and McVay 2005). We started by trying

to replicate the previous findings by using new datasets and new estimation techniques. In addition,

because divestiture has not been emphasized in the literature, we also aim to add to the general

accounting literature by testing the influence of divestiture on the overall internal control systems.

Thus, our first dependent variable is the presence [1] or absence [0] of material weaknesses (MWs)

in a firm’s overall internal control systems in a given year.

A firm reporting MWs in its internal control systems could have both IT-related and non-IT-

related MWs. To better understand the specific control mechanisms that could be disrupted by

various strategic moves, we use the presence [1] or absence [0] of only non-IT control MWs and

IT GRC MWs in a firm in a given year as our second and third dependent variables respectively.

For a firm with MWs identified, the Audit Analytics database will also record the nature of the

MWs by coding them into a list of predefined categories. IT-related MWs are coded as #22, and

we treat all the other types of MWs as non-IT MWs. However, prior studies report that Audit

Analytics make occasional classification mistakes by labeling some non-IT weaknesses as IT

weaknesses (Canada et al. 2009). Thus, following prior studies (Canada et al. 2009; Masli et al.

2016), we read the original SEC annual filings (usually forms 10-K or 10-KSB) of firms that

reportedly had MW in their IT-GRC. We identified that in 14 cases Audit Analytics misclassified

non-IT MW as IT MWs. We corrected them accordingly. After this correction, 163 unique firms

in our sample had reported IT GRC MW in our study timeframe.

Categorizing IT-GRC Mechanism MWs. While our primary dependent variable (IT GRC

21

MW) appears to be a binary variable capturing whether the external auditor found material

weaknesses in the IT GRC mechanisms of the firm or not, this opinion is the result of an extensive

review and evaluation of the design and the operating effectiveness of hundreds of IT general

controls (ITGC) and IT application controls, or automated process controls (APC) as we label

them in this study. The auditors’ evaluation also covers both the design and the operation

effectiveness of IT GRC mechanisms. If a firm’s external auditors conclude that its IT GRC is free

of MWs, the firm does not need to disclose any further detailed information. However, if MWs in

IT-GRC exist in either its design or its operation, the firm will disclose the specific IT controls and

the nature of their MWs in its regulatory filings. This allows us to conduct additional analyses as

to whether the hypothesized strategic repositioning moves affect (1) the ITGC and APC, and (2)

IT GRC design and operation in similar or different ways. To be able to conduct such analyses,

we manually coded the IT-GRC MW disclosures along two dimensions: ITGC MW versus APC

MW; and design MWs versus operation MWs.

To code IT GRC MWs, we followed the similar procedures used in previous studies from the

same research context (e.g., Li et al. 2012; Masli et al. 2016). We started with developing a coding

scheme that classifies IT controls into ITGC/APC and design/operation by synthesizing the

academic and practitioner literatures on ITGC audits and IT application audits (AICPA 2004; IIA

2009; IIA 2012; ITGI 2006; ITGI 2007). The coding scheme was then refined based on our

intensive discussion with partners and senior managers from big public accounting firms. The final

coding scheme used is presented in Appendix A. As shown in the coding scheme, ITGC controls

include IT governance controls, IT human resource controls, IT documentation controls, IT access

controls, IT computer operations controls, IT program development controls, IT change

management controls, and IT segregation of duty controls. Automated process controls (APC)

22

include controls embedded in IT applications such as input controls, processing controls, output

controls, and segregation of duty controls in business roles. The design of IT GRC mechanisms is

concerned with whether necessary mechanisms are present, adequate, and effective to mitigate

various IT-related risks at least on paper, and the operation of IT GRC mechanism is concerned

with whether the mechanisms are actually carried out consistently and effectively as designed.

From the SEC’s EDGAR database, we collected the annual filings of the firms that experienced

material weaknesses in their IT-GRC and excerpted the contents disclosing the nature of these

weaknesses. We then had two independent coders follow the coding scheme to classify whether

the IT material weaknesses were in ITGC/APC and design/operation categories. The concordance

rates between the classifications of the two coders, measured as Cohen’s Kappa (Cohen 1960),

were well over 90%. Remaining discrepancies, mostly caused by the ambiguity of the original

disclosure wording, were discussed by the authors to make final coding decisions.

Independent Variables

Diversification Level. As in prior studies, we use Palepu’s (1985) entropy measure of total

diversification to compute the total diversification level of a firm’s business portfolio across

different business segments in a given year. Specifically, Palepu computes the total diversification

with: ∑ 𝑃𝑖ln(1

𝑃𝑖)𝑁

𝑖=1 , where Pi is the share of the sales in segment i to the total sales of the firm; N

is the number of business segments the firm operates in. The data is obtained from Compustat

segment database.

Foreign Operations. As in prior SOX studies (e.g., Ashbaugh-Skaife et al. 2007; Doyle et al.

2007), we measure if a firm has foreign operations or not by examining if the firm reported [1]

foreign currency translation gain/loss [Compustat item FCA] in its firm’s financial statements or

not [0]. Because financially immaterial items are not reported separately, the presence of foreign

23

currency transaction gain/loss in a financial statement is a reliable indicator of the firm’s foreign

operations (Doyle et al. 2007; Masli et al. 2010).

Acquisition Intensity. We build on Moeller et al. (2004) in computing the acquisition intensity

of a firm in a given year. We compute the ratio of the total value of the firm’s acquisition

transactions completed during that year to the market value of the firm’s invested capital at the

end of that year. This measure captures what percentage of the firm’s year-end market value came

through the acquisitions during the year. We first select all acquisition transactions of the firm in

a given year from the SDC Platinum database and sum their transaction values. Then, we follow

previous finance studies (e.g., Hitchner 2006; Moeller et al. 2004) to compute the market value of

the firm’s invested capital as the sum of the market value of the firm's outstanding shares

[Compustat item CSHO multiplied by item PRCC_F], the liquidating value of preferred stock

[Compustat item PSTKL], the book value of long-term debt [Compustat item DLTT], and the book

value of debt in current liabilities [Compustat item DLC]. The specific fiscal year ending date of

each firm had been taken into account to formulate the correct one-year time window to select

acquisition transactions. There were five observations in which the total transaction value of the

firms’ acquisitions in a particular year exceeded the firms’ year-end market value. We excluded

those observations to avoid extreme acquisition cases.

Divestiture Intensity. We build on Klein (1986) in computing the divestiture intensity of the

firm as the total value of a firm’s divestiture transactions completed during a year divided by the

firm’s market value of invested capital at the beginning of that year. This measure captures what

percentage of the firm’s market value at the beginning of the year was divested during the

divestiture transactions that year. The value of divestiture transactions was obtained from the SDC

database. The market value of the firm’s invested capital was calculated with the same formula as

24

in the acquisition intensity. We dropped one observation where the firm’s divestiture intensity in

a particular year exceeded 100% of the firm’s market value of invested capital.

Corporate Restructuring. As in prior studies, we examine the presence [1] or absence [0] of

restructuring costs [CompuStat item RCP] in the firm’s financial statement to measure if the firm

engaged in significant corporate restructuring in that year (Masli et al. 2010). The generally

accepted accounting principles mandate that, to be reported as a separate item in financial

statements, a restructuring cost needs to be significant enough.

Control Variables

There are potential alternative explanations at the industry and firm levels as to why a firm’s

IT-GRC mechanism could become ineffective. At the industry level, industries that change

dynamically and digitize more intensively could increase disruptions to IT-GRC mechanisms. At

the firm level, if the overall governance and internal control environment of the firm is weak, if

the firm is financially distressed, or if the firm has poor IT capabilities, IT-GRC mechanisms could

also be weak. We control for these factors to be able to rule out the alternative explanations and

minimize endogeneity concerns. We also control for year effects.

Environmental Turbulence and Munificence levels of the firm’s businesses. Environmental

turbulence refers to the extent which the environment changes frequently and unpredictably, and

environmental munificence refers to the extent to which the environment can provide abundant

resources and opportunities to support a firm’s sustained growth (Dess and Beard 1984). As our

theory implies, firms operating in more turbulent environments face more adaptive tension, and

hence they may make more strategic repositioning moves and increase the likelihood of disruption

to their IT-GRC mechanisms. In contrast, firms operating in munificent environments often

accumulate more slack resources internally, and thus, they may be buffered from immediate

25

environmental disruptions.

We follow Dess and Beard (1984) to compute environmental turbulence and munificence. First,

we measure the two constructs at the level of an industry sector, defined based on NAICS (North

American Industry Classification System). Then, we compute the measures at the firm level by

taking a revenue-weighted average of the industry level measures based on the industry sectors

from which the firm generates revenues. In specific, for an industry sector i at year t, we calculate

the average revenue of all the firms in that sector, denoted as yit. Then, for each industry sector i

and year t, we regress the sector-average revenue on time in a five-year time window by estimating

equations yit = βit+ βitT+εit, where T takes values of t, t-1, t-2, t-3, t-4, and t-5 and εit is the residual.

Then, the environmental turbulence of the industry segment i at year t is computed as the standard

error of estimated βit divided by the average of yit in the past five years; while the environmental

munificence is computed as the estimated value of βit divided by the average of yit in the past five

years (Dess and Beard 1984). Second, we calculate turbulence and munificence for a given firm

by analyzing the industry sector(s) in which the firm operates. For a firm operating in only one

industry sector, we apply the turbulence and munificence measures of the same industry sector to

the firm. For a firm operating in multiple industry sectors, we measure environmental turbulence

and munificence as the revenue weighted average of all industry-level turbulence and munificence

scores of the industry sectors in which the firm operates. The weight of a sector is the percentage

of revenue the firm generates from that sector (Carpenter and Fredrickson 2001).

Environmental IT intensity of the firm’s businesses. We also argued that industries in which

digitization levels are higher could be subject to more disruptions in IT GRC. Thus, we need to

control for the environmental IT intensity of a firm’s businesses. We first computed the IT intensity

of every industry sector as the ratio of the software and hardware stock value to the total equipment

26

stock value in that segment (McAfee and Brynjolfsson 2008). Bureau of Economic Analysis (BEA)

provided these industry-level IT data needed for this calculation. Then, we computed firm-level

IT intensity as the revenue-weighted average of the IT intensity levels of all industry sectors in

which the firm operates in a particular year.

Following previous studies (e.g., Ashbaugh-Skaife et al. 2007; Doyle et al. 2007; Masli et al.

2010), we also control for firms’ size, profitability, and financial leverage ratios.

Firm size. We measure firm size as the book value of the firm's total assets [CompuStat item

AT]. We log-transform this measure to reduce its skewness.

Firm profitability. We measure a firm’s profitability with the firm’s return on equity (ROE),

calculated as Earnings Before Interest and Taxes / (Total Assets – Total Liabilities) [CompuStat

items EBIT / (AT - LT)]. Following previous studies (e.g., Doyle et al. 2007), we winsorized the

ROE variable at the 1th and 99th percentiles to limit extreme values.

Firm’s financial leverage. We measure a firm’s financial leverage as the ratio of the firm’s

total liability [CompuStat item LT] to total assets [CompuStat item AT].

Corporate Governance Weaknesses. If the overall corporate governance environment of the

firm is weak, IT-GRC mechanisms could by negatively influenced by the “tone at the top” and

also become weak. Thus, we control for weaknesses in the firm’s overall corporate governance.

As part of the SOX audit, independent external auditors assess a variety of corporate governance

mechanisms. We use three of them to measure this control. First, auditors assess whether the Board

of Directors (BoD) has an effective, adequately staffed Audit Committee. An Audit Committee

that has adequate experience and expertise can constantly engage in overseeing internal controls

and communicating with auditors about potential control deficiencies and remediation (Hoitash et

al. 2009; Krishnan 2005; Zhang et al. 2007). Second, auditors assess whether the Top Management

27

Team (TMT) is competent, whether the TMT sets an appropriate, ethical tone at the top for the

organization, and whether the TMT is reliable. TMT and CFOs in particular are immediately

responsible for the effectiveness of internal control systems. Their qualification and experiences

will influence the quality of internal control systems. Similarly, CIO experience and IT experiences

of other senior executives will influence the IT aspect of SOX compliance (Li et al. 2007; Li et al.

2010). Finally, auditors assess whether the firm has a sufficient internal audit function.9 If there is

an MW in any of these governance mechanisms, it would indicate that the firm has weak

governance structures. We count the MWs in these three categories to measure the weakness of

the firm’s overall corporate governance.

Auditor Status. The quality of a public firm’s external auditors could signal the firm’s

confidence on its financial reporting and internal control effectiveness. Thus, following previous

studies (e.g., Masli et al. 2010), we control for a firm's auditor status by including a binary variable

indicating whether [1] or not [0] the firm was audited by one of the prestigious “Big Four”

accounting firms (i.e., KMPG, PricewaterhouseCoopers, Ernst & Young, and Deloitte).

IT Capability of firm. There are differences in firms’ IT capabilities, i.e., how they use IT

resources to develop technological, procedural, and organizational innovations. The differences in

IT capabilities could affect IT-GRC mechanisms as well. Thus, we control for firms’ IT

capabilities. Every year, Information Week (IW) magazine invites firms to submit application

packages for listing consideration in the annual IW500 list. IW asks a panel of IW experts and

industry peers of the applicants to assess whether IT capabilities of the applicant firms are above

average in their respective industries. This assessment is not simply about IT investments of firms

9 In the Audit Analytics database, material weaknesses in corporate governance are reported as categories #11

(“Ineffective, non-existent, or understaffed audit committee”), #13 (“Senior management competency, tone, reliability

issues”), and #18 (“Insufficient or non-existent internal audit function”).

28

into generic IT applications and services provided by IT vendors. It is about how the firm

configures and customizes those generic IT resources to its specific business, and how the firm

achieves technological, procedural, and organizational innovations with those IT resources. If a

firm is selected into the IW500 list, it is considered to have strong IT capabilities. Thus, following

previous studies (e.g., Bharadwaj 2000), we measure IT capability of a firm by assessing whether

or not the firm was listed [1=strong IT capability] in the IW500 list [0=weak IT capability] in a

year.

Year Effects. We include dummy variables to control for unobserved year fixed effects.

To mitigate the risk of reverse causality, we lagged all our explanatory covariates, except for

environmental variables and auditor status, for one year. Table 1 presents descriptive statistics and

correlations among the study variables.

---Insert Table 1 about Here---

Model Specification

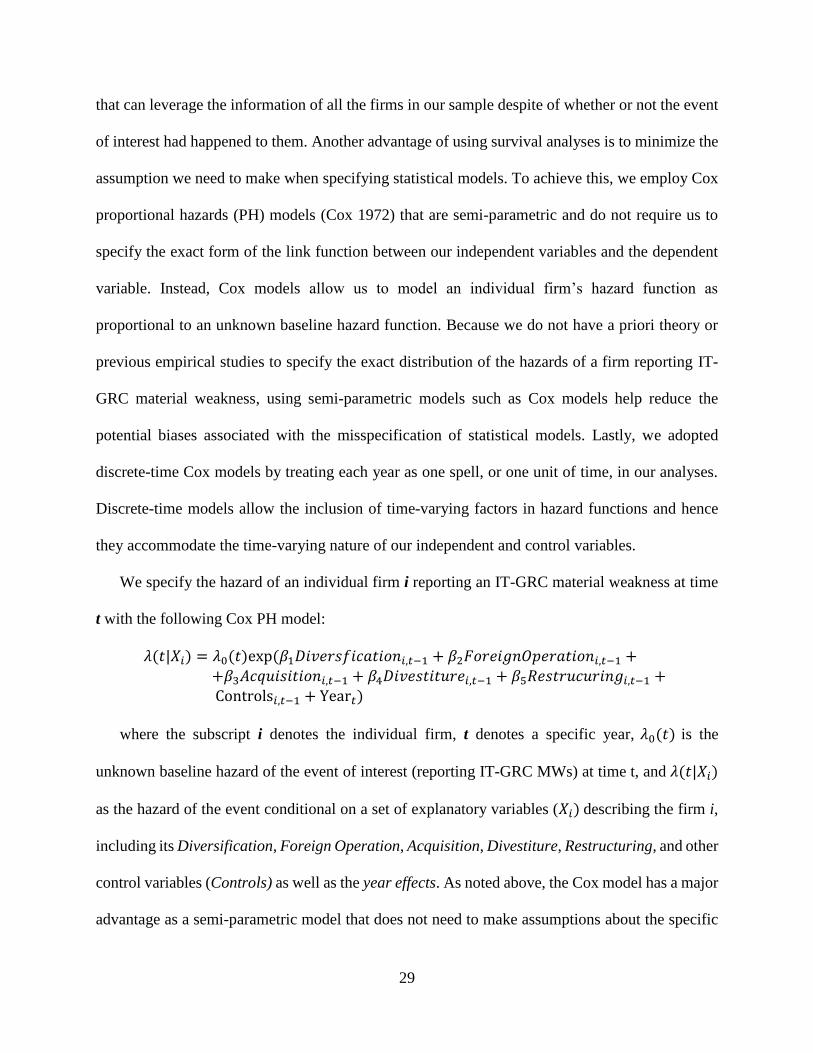

We adopt survival analysis (Allison 2010) as our primary estimation method. In our research

context, when the SOX Act turned effective in 2004, big public firms in the U.S. entered a “risk

set” such that they started to face the hazard of having their IT-GRC MWs, if exist, disclosed to

the public. Survival analysis techniques allow us to directly estimate the influence of various

factors on the hazards of a firm reporting MWs in its internal control systems in general or in its

IT or non-IT controls in specific.

One of the major advantages of using survival analysis in this research context is to account

for the issue of right censoring in our observations. Right censoring happens when the event of

interest (i.e., reporting IT GRC MWs) had not occurred for some firms in our sample at the end of

our study time window. Instead of disregarding these observations, we adopted survival analyses

29

that can leverage the information of all the firms in our sample despite of whether or not the event

of interest had happened to them. Another advantage of using survival analyses is to minimize the

assumption we need to make when specifying statistical models. To achieve this, we employ Cox

proportional hazards (PH) models (Cox 1972) that are semi-parametric and do not require us to

specify the exact form of the link function between our independent variables and the dependent

variable. Instead, Cox models allow us to model an individual firm’s hazard function as

proportional to an unknown baseline hazard function. Because we do not have a priori theory or

previous empirical studies to specify the exact distribution of the hazards of a firm reporting IT-

GRC material weakness, using semi-parametric models such as Cox models help reduce the

potential biases associated with the misspecification of statistical models. Lastly, we adopted

discrete-time Cox models by treating each year as one spell, or one unit of time, in our analyses.

Discrete-time models allow the inclusion of time-varying factors in hazard functions and hence

they accommodate the time-varying nature of our independent and control variables.

We specify the hazard of an individual firm i reporting an IT-GRC material weakness at time

t with the following Cox PH model:

𝜆(𝑡|𝑋𝑖) = 𝜆0(𝑡)exp(𝛽1𝐷𝑖𝑣𝑒𝑟𝑠𝑓𝑖𝑐𝑎𝑡𝑖𝑜𝑛𝑖,𝑡−1 + 𝛽2𝐹𝑜𝑟𝑒𝑖𝑔𝑛𝑂𝑝𝑒𝑟𝑎𝑡𝑖𝑜𝑛𝑖,𝑡−1 ++𝛽3𝐴𝑐𝑞𝑢𝑖𝑠𝑖𝑡𝑖𝑜𝑛𝑖,𝑡−1 + 𝛽4𝐷𝑖𝑣𝑒𝑠𝑡𝑖𝑡𝑢𝑟𝑒𝑖,𝑡−1 + 𝛽5𝑅𝑒𝑠𝑡𝑟𝑢𝑐𝑢𝑟𝑖𝑛𝑔𝑖,𝑡−1 +Controls𝑖,𝑡−1 + Year𝑡)

where the subscript i denotes the individual firm, t denotes a specific year, 𝜆0(𝑡) is the

unknown baseline hazard of the event of interest (reporting IT-GRC MWs) at time t, and 𝜆(𝑡|𝑋𝑖)

as the hazard of the event conditional on a set of explanatory variables (𝑋𝑖)describing the firm i,

including its Diversification, Foreign Operation, Acquisition, Divestiture, Restructuring, and other

control variables (Controls) as well as the year effects. As noted above, the Cox model has a major

advantage as a semi-parametric model that does not need to make assumptions about the specific

30

form of the baseline hazard function 𝜆0(𝑡). Instead, it assumes only that the hazard of an event for

firm i at time t is proportional to the baseline hazard, and then it directly models how the hazard

of the event per time unit varies in response to a set of time varying explanatory covariates (Cox

1972; Hosmer et al. 2008).

About 26% of the firms in our sample repeatedly reports IT GRC MWs in multiple years.

However, MWs in a firm sometimes persist for a couple of years, or one MW in a previous year

may morph into or trigger a different one in the consequent year (Klamm et al. 2012). Thus, a firm

that repeatedly reports MWs in multiple years does not necessarily have new MWs in each of those

years. By checking the original disclosure documents, we concluded that the majority of the firms

with multiple-year IT-GRC MW disclosures in our sample actually experienced the same MWs

that persisted for multiple years.10 Thus, we removed a firm from the risk set after it reports an IT-

GRC material weakness for the first time to avoid modeling multiple MW disclosures as new

events.

Diagnostic Analyses

The proportionality of hazards is the key assumption underlying Cox models. We followed

the recommendations of Cleves et al. (2010, ch.11) and conducted three diagnostic tests on this

proportionality assumption. First, we conducted the link test as a general specification test. After

estimating our primary Cox model and obtaining the estimated vector of coefficients �̂�, the link

test re-estimates the hazard model by using the linear predictor 𝑋�̂� and its squared term (𝑋�̂�)2 as

independent variables. Under the assumption that 𝑋𝛽 is the correct specification, the estimated

10 We manually checked all the IT GRC MW disclosure documents of the firms with multiple-year disclosures. In our

study time window (2004 – 2009), out of the 317 pubic firms that had ever reported IT GRC weaknesses in at least

one year, 83 (26%) reported IT GRC weaknesses in multiple years. Among them, in only 13 firms, IT GRC MWs

originally reported in an earlier year were fully remedied but new IT GRC weaknesses were found in subsequent

years. Dropping these 13 firms with multiple IT GRC MW occurrences, or dropping all the 83 firms with IT GRC

MW disclosures, will not qualitatively change our conclusions.

31

coefficient of 𝑋�̂� should be significant while the estimated coefficient of (𝑋�̂�)2 should be

insignificant, which we confirmed in our diagnostic test.

The second test is to directly check the proportional-hazard assumption of Cox models by

including interactions between all the time-varying independent variables and the logarithm of

survival time (Hosmer et al. 2008). Under the proportional-hazard assumption, the estimated

coefficient of these interaction items should not be significant. Following the recommendations of

Cleves et al. (2010) and Hosmer et al. (2008), we interact our five primary independent variables

with ln(t) and re-estimate the Cox models after including the interaction items. None of the

estimated coefficients of the interaction items are significant, thus supporting the use of Cox Model.

The third test is to check proportional-hazard assumption based on the analyses of residuals,

as discussed by Therneau and Grambsch (2000) and Cleves et al. (2010). We conducted the

proportionality test, and the results again failed to reject the proportionality assumption, and

provided support for the use of Cox model.

Alternative Statistical Methods

We also considered panel data models as alternative statistical methods to check the

robustness of our results. In selecting the most appropriate panel data model, we need to address

the same issue as discussed above that IT GRC weaknesses reported in different years are most

likely the same, persisting weaknesses instead of new ones. Thus, when organizing our data as a

cross-sectional, time-series data set, there would be high serial correlations among observations

from the same subject across years. We ran the serial correlation test, as discussed by Wooldridge

(2010) and implemented by Drukker (2003). The test result confirmed the existence of significant

serial correlation (F-value = 39.727, p-value < .001).

We then chose to use Generalized Estimating Equation (GEE) models, which allow us to

32

directly model the possible serial correlation among the outcomes from the same subject in

multiple years. GEE is a specific type of generalized linear models that apply to longitudinal data

analyses (Hardin and Hilbe 2003). It utilizes both cross-sectional and time-series information of a

panel data and directly accounts for the correlation structure of observations from the same subject

by estimating a parameterized correlation matrix (Zeger and Liang 1986). Our primary conclusions

are qualitatively unchanged based on GEE models.

RESULTS

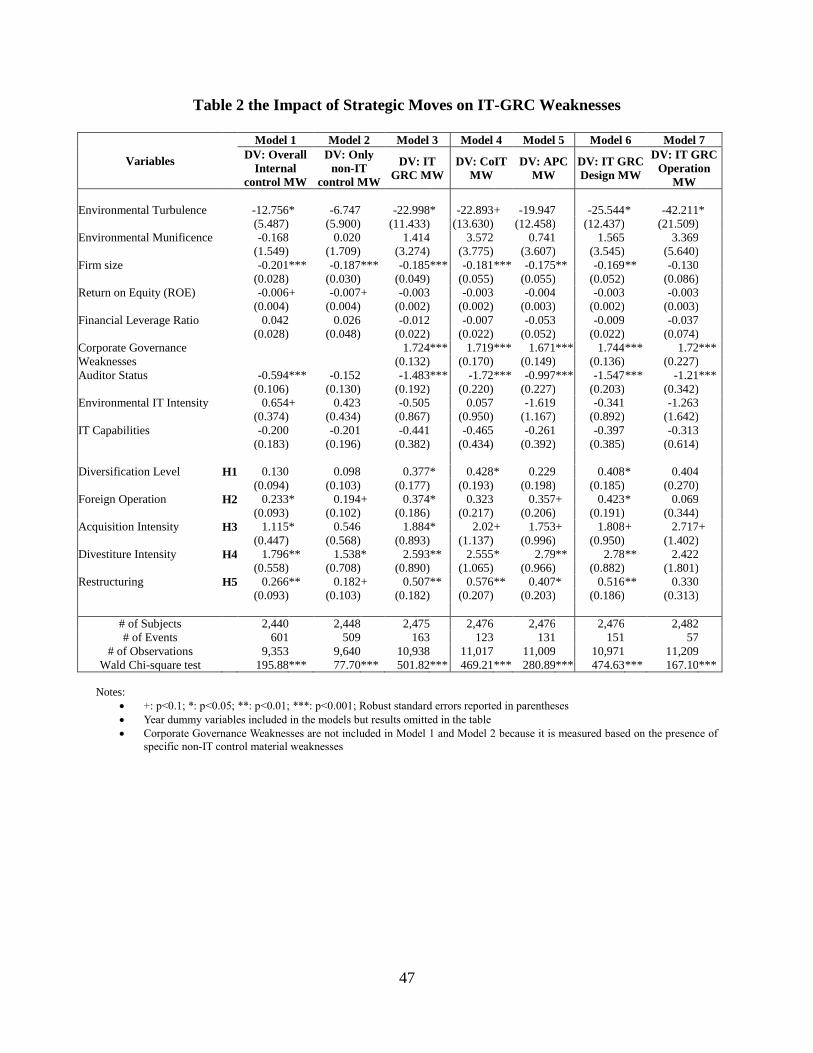

We report our primary results in Table 2 below. In Model 1 of Table 2, we used the presence

[1] or absence [0] of overall internal control MWs as the dependent variable and estimated the

hazard of its presence based on a firm’s audit report. In Model 2, we used the presence [1] or

absence [0] of only non-IT control MWs as the dependent variable. In Model 3, we used the

presence [1] or absence [0] of IT-GRC MWs as the dependent variable. Then, we moved further

to investigate the different types of IT-GRC MWs. In Model 4 and Model 5, we estimated the

hazards of reporting CoIT MWs and APC MWs respectively. In Model 6 and Model 7, we

estimated the hazards of reporting IT-GRC design MWs and IT-GRC operation MWs. All the

models were estimated based on Cox models as specified above.

--Insert Table 2 about Here--

The Impact of Strategic Repositioning Moves on Overall and Non-IT Controls

The results of Model 1 in Table 2 show that foreign operation, intensive acquisition and

divestiture, and restructuring all increase the hazard that a firm experiences MWs in its overall

internal control system. For the roles of foreign operation, acquisition, and restructuring, previous

studies in the accounting literature have reported largely similar results (e.g., Ashbaugh-Skaife et

al. 2007; Doyle et al. 2007; Ge and McVay 2005; Krishnan and Visvanathan 2007; Zhang et al.

33

2007). They have reported mixed results in the role of diversification, while in our analyses,

diversification has no significant impact. Most of these previous studies used cross-sectional data,

relatively simplified measures, and logistic regression techniques. Thus, first, our study provided

further confirmation to the previous findings in the accounting literature by using different dataset,

measurements, and statistical methods. We also added to the literature by introducing the

disruptive role of divestiture to overall internal controls.

When we separated the disruption to an internal control system into non-IT and IT-related

areas, as in Model 2 and Model 3, it becomes evident that IT-GRC mechanisms are more prone to

be disrupted during strategic repositioning moves. According to the results of Model 2, non-IT

control mechanisms are significantly disrupted by divestiture and marginally so by foreign

operation and restructuring, but IT-GRC mechanisms are disrupted by all the five types of moves.

The Impact of Strategic Repositioning Moves on IT-GRC

Our hypotheses were validated based primarily on the results of Model 3. According to them,

the hazard of experiencing a material weakness in IT-GRC mechanisms increases significantly

with: (H1): diversification level (β = .377, p-value <.05); (H2): presence in foreign operations (β

= .374, p-value < .05); (H3): acquisition intensity (β = 1.884, p-value <.05); (H4): divestiture

intensity (β = 2.593, p-value < .01; and (H5): engagement in corporate restructuring (β = .507, p-

value < .01). These results provide empirical support for our theory that corporate strategy

repositioning moves of firms significantly disrupt and reduce the effectiveness of the IT-GRC

mechanisms, over and beyond the effects of alternative explanations discussed in the prior

literature and in practice.

The Impact of Strategic Repositioning Moves on ITGC and APC

As discussed earlier, we categorized whether the IT-GRC MWs were in the IT general controls

34

(ITGC) and or in the automated process controls (APC). Models 4 and 5 of Table 2 respectively

report how the hypothesized strategic repositioning moves affect the ITGC and APC.

The results indicate that the diversification level significantly increases the hazard of MW in

ITGC, but not in APC. Foreign operation increases the hazard of MW in APC marginally, but not

in ITGC. Corporate restructuring, acquisition, and divestiture all increase the hazard of MW in

both ITGC and APC in similar ways. Overall, we noticed some but not dramatic differences in the

disruptive effects of strategic moves on ITGC and APC.

The Impact of Strategic Repositioning Moves on IT-GRC Design and Operation

As discussed earlier, we also categorized whether the IT-GRC MWs were related to the design

or the operation of IT-GRC mechanisms. Models 6 and 7 of Table 2 respectively report how the

hypothesized strategic repositioning moves affect the design and operation of IT-GRC

mechanisms.

The results indicate that all the five types of strategic repositioning moves increases the hazard

of MW in the design of IT-GRC mechanisms, but only acquisition marginally increases the hazard

of MW in their operation. The contrast suggests show evidence that IT-GRC mechanisms appear

disrupted during strategic repositioning moves mostly because they become at least temporarily

obsolete. The design of IT-GRC mechanism, which were likely optimized based on the old

business environments, cannot be updated timely during the turmoil periods of strategic

repositioning moves.

The Impact of Strategic Repositioning Moves on Detailed Categories of IT-GRC

When categorizing IT-GRC mechanisms into ITGC and APC, we used a finer-grained coding

scheme that includes eight subcategories of ITGC and four subcategories of APC. We further

explored how the hypothesized strategic repositioning moves affect these twelve subcategories of

35

IT-GRC mechanisms. The results are reported in Table 3 below.

--Insert Table 3 about Here--

The results indicate that access controls, or the controls that ensure authorized access to

various IT resources such as hardware, network, databases and applications, are most prone to be

disrupted during all types of strategic repositioning moves. One commonality among the five

hypothesized strategic moves in our study is the implication on personnel turnover and

organizational redesign. Layoffs and reorganization are common during these strategic moves, but

updating user profiles and access privileges in a complex IT environment is often a daunting task

and may not be done timely or completely.

Probably due to the same effects of personnel turnover and organizational redesign, MWs

associated with IT human resources and the input controls to various IT applications also appear

to be associated with more types of strategic moves according to Table 3. After a major strategic

move, the IT department of the firm often also experiences major changes, including personnel

turnover. Even The retained IT employees are also likely to experience the “survivor’s syndrome”

(Cascio 1993) under which employees exhibit low morale, resist change, withdraw, and become

paralyzed after their peers are eliminated and their workloads increase (Ranganathan and Outlay

2009). Similarly, because of the organizational redesign, many previously integrated IT systems

need to be rewired, and the interfaces among them need to be updated or replaced. The input

controls embedded in these systems need to reflect the new business rules, processing logic, and

the roles of end users, which themselves are often in flux during a strategic move (Du and

Tanriverdi 2014).

DISCUSSION AND CONCLUSION

In an increasingly digital world, IT-related risks of firms are on the rise. The main defense

36

mechanism against the IT-related risks has been IT governance, risk, and control (IT-GRC)

mechanisms. IT-related risks impact not only firms but also investors and customers. Thus, a

multitude of laws, regulations, and industry standards are instituted to require firms to design and

effectively operate IT-GRC mechanisms to minimize the probability of loss and magnitude of loss

associated with the IT-related risks. Despite these efforts, the frequency and pervasiveness of data

privacy and security breaches, operational IT glitches, and digital fraud and theft incidents indicate

that even well governed firms that institute state-of-the-art IT-GRC mechanisms struggle to main

the effectiveness of their IT-GRC mechanisms over time and become vulnerable to IT-related risks.

This study contributes to IS research and practice by explaining how and why a firm’s own

strategic repositioning moves play a significant role in this problem.

Contributions to IS research

One potential contribution of this research is to the IS research stream on IT risks and the

management control theory. The findings indicate that the current theory is too static to address

the dynamically changing IT risks and IT-GRC needs of firms in an increasingly complex digital

world.

The predominant theory that informs the design of IT-GRC mechanisms for mitigating IT-

related risks of the firm is the management control theory. This theory assumes that business

objectives and risks of firms are understood well and that they remain relatively stable during the

planning cycle of firms, typically an annual cycle. Accordingly, the theory also assumes that the

IT-GRC mechanisms that are designed based on the business objectives and risk profiles of firms

can also remain effective during the planning cycle. This research challenges these assumptions

on the grounds that the business objectives, risk profiles, and hence, IT-GRC needs of firms change

dynamically. The external environment is a complex adaptive system (CAS) that continuously

37

produces new opportunities and threats. In response, firms adjust their internal CAS, through

strategic repositioning moves, to match the external CAS in ways to seize the emerging

opportunities and cope with the emerging threats. The repositioning moves change the business

objectives of firms, which in turn change the risk profiles of firms, which in turn render the existing

IT-GRC mechanisms of firms less relevant. Accordingly, IT-GRC mechanisms become less

effective or ineffective. The findings imply the need for a more dynamic management control

theory that can enable firms to realign their IT-GRC mechanisms dynamically with changing IT-

related risks of their businesses.

Complexity science provides some guidance for the development of more dynamic IT-GRC

mechanisms in the firm. First, complexity science cautions that the wicked problems produced by

complex adaptive systems such as the dynamically changing IT risks of firms cannot be “solved”

fully, but that they can be “tamed.” Second, complexity science recommends four interrelated

capabilities for “taming” the wicked problems (McDaniel 2007): (a) sensing, (b) sense making, (c)

improvising, and (d) learning on the fly. Sensing capability can spot the changes in business