how does imf lending operate? a two-level …paperroom.ipsa.org/papers/paper_31888.pdfa two-level...

TRANSCRIPT

1

How Does IMF Lending Operate? A Two-Level Principal-Agent Model

Merih Angin, PhD Candidate, Department of International Relations/Political Science

The Graduate Institute of International and Development Studies Geneva, Switzerland

ABSTRACT: The literature examining the institutional aspects of the IMF can be grouped under two categories: state-centric and public choice approaches. The state-centric approach focuses on the influence of the powerful states in explaining the variation in the conditionalities of IMF loans, whereas public choice approaches put a greater emphasis on the intellectual dominance of the IMF staff. However, neither of these approaches fully explains the variation as they neglect the impact of the relation between the Executive Board, the IMF staff and the recipient country, on the decision-making of the institution. This paper presents a research project attempting to analyze the variations in IMF conditionalities through building a new conceptual framework. By focusing on the case study and theory dimensions that elucidate the puzzle of the research, the paper introduces a “Two-Level P-A Model” of IMF lending with hypotheses that will be tested using a single country study, namely the Turkish case.1

*1The author wishes to express her deepest gratitude to Cédric Dupont for his detailed comments on successive drafts and supervision throughout the research. Helpful comments and criticisms of Liliana Andonova and Thomas Biersteker, as well as the guidance of Charles Wyplosz and James Vreeland are also gratefully acknowledged.

2

How Does IMF Lending Operate? A Two-Level Principal-Agent Model

Introduction

Questioning the legitimacy of the International Monetary Fund (IMF) has been fairly

popular since the collapse of the Bretton Woods System and especially after the Asian Financial Crisis of 1997, regularly by those who believe that the IMF has failed in fulfilling its mission.2 Indeed, based on their empirical research, Przeworski and Vreeland found a negative correlation between participation in IMF programs and economic growth.3 Consequently, the emerging markets had decided to increase the accumulation of international reserves to avoid an IMF loan4 with many strings attached, which could ultimately worsen their situation. For that reason, the Fund was transformed into an international financial institution whose mandate was mainly providing technical assistance, rather than an international lender of last resort. However, things are changing today; the deus ex machina is back. The current global economic crisis that is the worst one ever experienced after the Great Depression of the 1930s, which has impaired Europe more than predicted, has given the IMF a strong role to play. “Whither the IMF?” has become a popular question both in the academia and among policymakers. In the year 2008, the Fund was born out of its ashes. After the London Summit, Dominique Strauss-Kahn, who was then the Managing Director of the Fund, stated explicitly that “the IMF is back.”5 Many of the members of the European Union (EU), particularly those who have become members with the Eastern Enlargement, faced recession with growing budget deficits. Consequently, Romania has received a Stand-By Arrangement (SBA), while Greece, Portugal and Ireland- the biggest borrowers of the Fund- have received Extended Arrangements, and Poland is one of the countries receiving the biggest precautionary loan.6 Without doubt, these lending processes provide academics with new research questions and case studies. The difference between the way the Fund treats Europeans and its treatment of developing countries in the late 1990s and early 2000s will definitely make the question of “who runs the organization” stand out more in the literature.

Understandably, putting together an Extended Credit Facility (ECF) for a low income country follows fairly different dynamics from a big SBA for a medium-income emerging market country or a distressed euro-zone member. It has been a common claim in the academia that countries that are strategically important for G7 or the United States in particular, are always favored by the Fund.7 In this context, several “high-profile” IMF lending cases, including Russia, Ukraine, Argentina and Turkey, are often mentioned as instances where the US pressure caused laxity in “enforcing conditionalities.”8 Undeniably, the US pressure was particularly visible in the case of Russia, where the IMF was harshly

2 See Gerald K. Helleiner, “Stabilization, Adjustment and the Poor,” World Development 15, no. 12 (1987); Lance Taylor, Varieties of Stabilization Experience: Toward Sensible Macroeconomics in

the Third World (New York: Oxford University Press, 1987); Tony Killick, IMF Programmes in Developing

Countries: Design and Impact (London: Routledge, 1995); Matthew Martin, The Crumbling Facade of African

Debt Negotiations: No Winners (London:Macmillan, 1991); Ngaire Woods and Domenico Lombardi, “Uneven Patterns of Governance: How Developing Countries Are Represented in the IMF,” Review of International

Political Economy 13 (2006). 3 Adam Przeworski and James Raymond Vreeland, “The Effect of IMF Programs on Economic Growth,” Journal of Development Economics 62 (2000): 403. 4 Barry Eichengreen, “A Blueprint for IMF Reform: More than just a Lender,” International Finance 10, no.2 (2007): 153. 5 Allan Meltzer, “The IMF returns,” The Review of International Organizations 6, no. 3 (2011): 445. 6 International Monetary Fund, “The IMF at a Glance,” http://www.imf.org/external/np/exr/facts/glance.htm. 7 See Randall W. Stone, Lending Credibility: The International Monetary Fund and the Post-Communist

Transition (Princeton: Princeton University Press, 2002). 8 Randall W. Stone, “The Scope of IMF Conditionality,” International Organization 62, no. 4 (2008): 617.

3

criticized for the stringency of the conditionality it imposed. The Unites States “called for” a softening in lending to Russia,9 which was followed by the approval of a SDR (Special Drawing Rights) 6.9 billion Extended Fund Facility (EFF) for Russia on March 26, 1996 by the Executive Board (EB), which was then the largest EFF in IMF history.10 According to Stiglitz, “many of the staff at the IMF… did not think that the 1998 loan to Russia made any sense… [y]et the IMF is a hierarchical organization, and the people at the top actually believed that the program would work.”11 On the other hand, there exist cases where technocratic decision-making is believed to be at work, such as the case of Africa, which results in tougher conditionalities being imposed. Based on the interview she conducted, Best states that “a former member of the Executive Board suggested that it was during Köhler's Africa tour that his concern with the scope of IMF conditionality came visibly to the surface after witnessing the level of Fund conditions on the Mozambique cashew industry.”12 However, according to Stone, “the enforcement of IMF conditionality is indeed politicized, even in Africa.”13 Opposing the aforementioned common belief that the strategic allies of the US are always favored by the Fund, whereas it is the IMF staff who has the main leverage over the design of conditionalities when low-income countries are borrowing from the Fund, I claim that what we observe in reality is that the difference between those two cases is more subtle than expected. This paper outlines my research that offers a conceptual framework for studying the variation in loan features of the IMF, and it focuses on the case study and theory dimensions that elucidate the puzzle of the research.

The rest of the paper is organized as follows: The next section outlines the IMF decision- making flow, followed by a brief literature review on the IMF lending behavior in order to introduce the puzzle of this research. It then outlines the Principal-Agency (P-A) Theory that this research is taking on board to build a new conceptual framework, followed by the description of the Two-Level P-A Model and the working hypotheses. The last sections explain the case study and methods with a short conclusion summarizing some preliminary findings of the research. Decision-Making at the IMF

The variation in loan features of the IMF, particularly its conditionalities leads us to question the decision-making processes of the Fund. The “evolution” of the Fund as discussed previously, with its changing role makes the study of the lending behavior of the IMF highly important for the study of International Organizations (IOs). Despite numerous empirical studies, the root of the problems with Structural Adjustment Programs (SAPs) of the Fund is still a debated issue, as it lies on the question of who runs the organization: the powerful states via the EB or the IMF staff? There is a growing literature on the “political aspects” of the institution, which is the main focus of this research, contrary to the previous studies assuming that the decisions of the Fund are purely based on macroeconomic criteria.14 In order to

9 Nigel Gould-Davies and Ngaire Woods, “Russia and the IMF,” International Affairs 75, no. 1 (1999): 10. 10 International Monetary Fund, “IMF Chronology,” http://www.imf.org/external/np/exr/chron/chron.asp. 11 Joseph E. Stiglitz, “Democratizing the International Monetary Fund and the World Bank: Governance and Accountability,” Governance: An International Journal of Policy, Administration, and Institutions 16, no. 1 (2003): 130. 12 Jacqueline Best, “Legitimacy Dilemmas: The IMF's Pursuit of Country Ownership,” Third World Quarterly 28, no. 3 (2007): 477. 13 Randall W. Stone, “The Political Economy of IMF Lending in Africa,” American Political Science Review 98, no. 4 (2004): 578. 14 Graham Bird and Dane Rowlands, “Political Economy Influences Within the Life-Cycle of IMF Programmes,” The World Economy 26, no. 9 (2003): 1256.

4

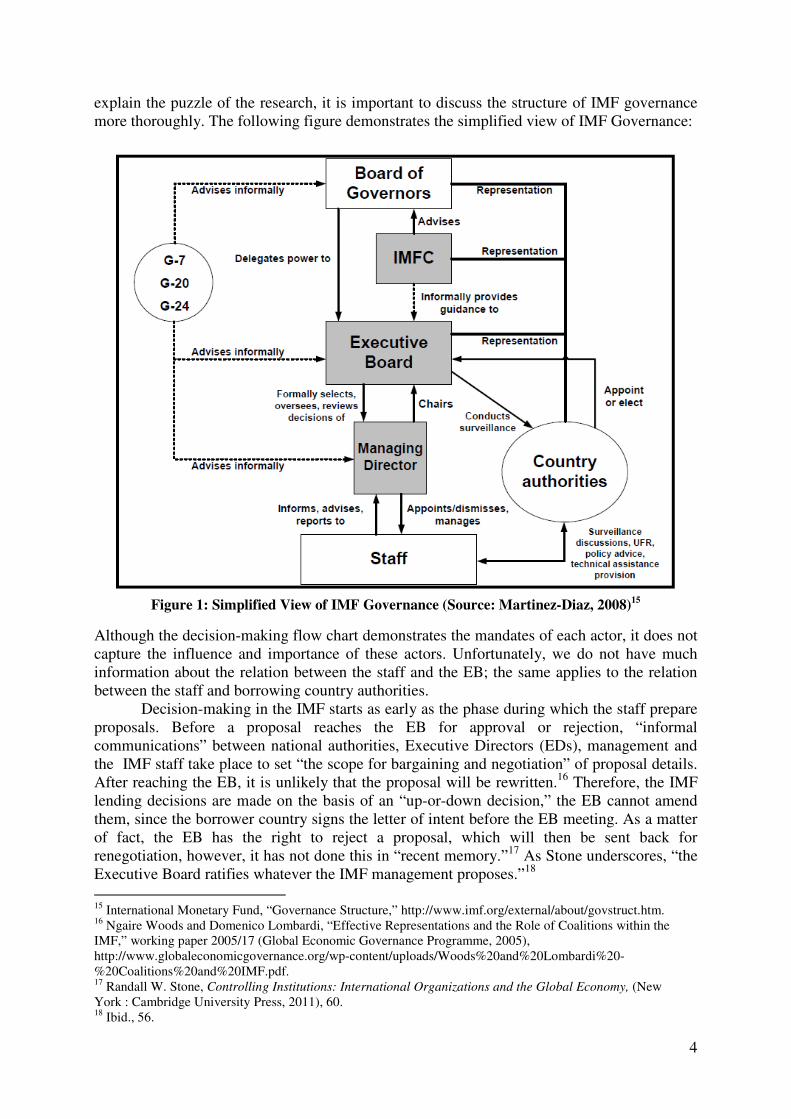

explain the puzzle of the research, it is important to discuss the structure of IMF governance more thoroughly. The following figure demonstrates the simplified view of IMF Governance:

Figure 1: Simplified View of IMF Governance (Source: Martinez-Diaz, 2008)

15

Although the decision-making flow chart demonstrates the mandates of each actor, it does not capture the influence and importance of these actors. Unfortunately, we do not have much information about the relation between the staff and the EB; the same applies to the relation between the staff and borrowing country authorities.

Decision-making in the IMF starts as early as the phase during which the staff prepare proposals. Before a proposal reaches the EB for approval or rejection, “informal communications” between national authorities, Executive Directors (EDs), management and the IMF staff take place to set “the scope for bargaining and negotiation” of proposal details. After reaching the EB, it is unlikely that the proposal will be rewritten.16 Therefore, the IMF lending decisions are made on the basis of an “up-or-down decision,” the EB cannot amend them, since the borrower country signs the letter of intent before the EB meeting. As a matter of fact, the EB has the right to reject a proposal, which will then be sent back for renegotiation, however, it has not done this in “recent memory.”17 As Stone underscores, “the Executive Board ratifies whatever the IMF management proposes.”18

15 International Monetary Fund, “Governance Structure,” http://www.imf.org/external/about/govstruct.htm. 16 Ngaire Woods and Domenico Lombardi, “Effective Representations and the Role of Coalitions within the IMF,” working paper 2005/17 (Global Economic Governance Programme, 2005), http://www.globaleconomicgovernance.org/wp-content/uploads/Woods%20and%20Lombardi%20-%20Coalitions%20and%20IMF.pdf. 17 Randall W. Stone, Controlling Institutions: International Organizations and the Global Economy, (New York : Cambridge University Press, 2011), 60. 18 Ibid., 56.

5

According to Stone, extensive “authority” delegated to management “weakens the Executive Board” and causes a great deal of “information asymmetries.” Lending decisions of the Fund are of primary importance to the recipient country. They involve considerable “information asymmetries” among the other member states and “substantial delegation” to the IMF management and staff.19 EDs do not take part in the “mission to countries” or the negotiation process for the programs, with the exception of the recipient country’s representative. Moreover, they do not have access to “confidential documents” that are crucial for the negotiation process, including the “mission briefs” and “back-to-office reports.” The EDs’ influence on conditionality is thwarted by the aforesaid “information asymmetry.”20

The following section briefly mentions the literature review on the IMF lending behavior, which will be useful in understanding the puzzle of this research.

A Brief Literature Review on the Institutional Aspects of the IMF

The literature examining the institutional aspects of the IMF can be grouped under two main categories: state-centric and public choice approaches. The scholars with the state-centric approach put emphasis on the influence of the powerful states, namely G7 or the US in particular, in explaining the variation in the conditionalities of IMF loans. The IMF is often criticized for its “one size fits all approach,”21 as its SAPs to a large extent consist of the list of the conditions set, labeled as the “Washington Consensus.”22 Nevertheless, it is usually acknowledged that the Fund’s lending policies vary across time and space.23 As Biersteker underscores “within the general guidelines of orthodox stabilization and adjustment, there is room for considerable variation in the specific terms of agreements.”24 While Broome considers the variation in the conditionalities attached to the current loans granted to Iceland, Belarus and Mexico as “flexibility in the use of loan conditionality,” which illustrates that the Fund is learning from its previous mistakes,25 other scholars perceive them as reflections of powerful states’ interests. Based on a data set drawn from the IMF’s record of conditionality, Randall Stone has found evidence of US influence in cases where the Fund lends to politically important countries.26 He calls this view “informal governance,” signifying the US intervention in contradiction with the formal rules.27 By the same token, Copelovitch suggests a “common agency” framework in explaining the variation in the IMF loan size and conditionality, where the G5 countries exercising a “de facto control over the Executive Board,” act as the “political principal” of the institution. He argues that “preference heterogeneity” among the G5 determines the said variation. Based on his empirical research, he claims that when G5 countries’ “interests” are not “intense”, the “agent,” namely the IMF staff, enjoys greater “autonomy”; consequently, the lending policies reflect “technocratic

19 Ibid., 52. 20 Ibid., 57. 21 See Joseph E. Stiglitz, Globalization and Its Discontents (New York: W.W. Norton & Company, 2003). 22 “Washington Consensus” is a term first coined by John Williamson. For the details see John Williamson, “The Washington Consensus as Policy Prescription for Development” (speech to the Practitioners of Development Seminar Series delivered at the World Bank, January 13, 2004). 23 Seonjou Kang, “Agree to Reform? The Political Economy of Conditionality Variation in International Monetary Fund Lending, 1983–1997,” European Journal of Political Research 46 (2007): 685. 24 Thomas J. Biersteker, “International Financial Negotiations and Adjustment Bargaining: An Overview,” in Dealing with Debt: International Financial Negotiations and Adjustment Bargaining, ed. Thomas J. Biersteker (Boulder, CO: Westview Press, 1993), 4. 25 Andre Broome, “The International Monetary Fund, Crisis Management and the Credit Crunch,” Australian

Journal of International Affairs 64, no. 1 (2010): 37. 26 Randall W. Stone, “The Scope of IMF Conditionality,” International Organization 62, no. 4 (2008): 590. 27 Ibid., 617.

6

and/or bureaucratic interests.”28 On the other hand, “public choice” approaches assume that the IMF staff is a “highly independent actor,” therefore “bureaucratic politics” rather than the interests of the major shareholders, are the main “political factor” in the Fund lending policies.29 In this context, Chwieroth argues that “the Fund staff by and large adopted, interpreted, and applied the norm on their own.”30 Similarly, Momani argues that the Fund staff has “intellectual dominance and discretion in the design of loan conditionality, writing of surveillance reports, and provision of technical and policy advice.”31

To sum up, despite a substantial empirical literature, there is an ongoing debate about the main factors explaining the variation in the IMF loan sizes and conditionalities shaping SAPs.32 The majority of the scholarly work done so far is based on quantitative analysis, since it is a highly challenging task to collect and operationalize qualitative data. Admittedly, at first glance a rough econometric model seems to be a promising option, since there are many actors involved in decisions about conditionality. However, such methodologies fail in examining the relationship between the actors who have the main impact on the formation of SAPs. As I try to explain meticulously throughout the paper, this research attempts to take on board mixed methods to examine the variation in the loan features of SAPs. In this context, the Principal-Agency (P-A) theory will be used to analyze the impact of the relationship between the EB, IMF staff and the recipient country. My main aim is to disentangle the puzzle of how the IMF lending policies with different conditionalities are formed. As Gutner stresses, the flexibility of P-A theory makes it a useful tool for understanding IOs and modeling their performance through examination of the “interactions among the politics and preferences of member states,” “internal incentives” for IO staff and borrowing country actors. The “success” of IOs is very “dependent” on the way “complex P-A relationships are created and managed.”33 The following section discusses some of the key concepts and assumptions of the P-A theory that will be used in the formulation of the hypotheses of my P-A model.

Principal-Agency Theory in Application to IOs

P-A Theory argues that “incomplete” and “asymmetric information” leads to the

principal-agent problem, which refers to the situation that the “principal” faces difficulties in deeming the agent responsible for seeking the interests of the principal.34 Due to the different interests of the principal and agent, the principal faces “Madison’s dilemma,” in which the agent can use the powers obtained through the principal’s “delegated authority” against the principal.35

As described by Andonova, P-A models in application to IOs are based on the assumption that IOs “use their autonomy” in pursuit of “organizational interests,” which include “survival” as well as preserving their “budget, competences, legitimacy, and

28 Mark S. Copelovitch, “Master or Servant? Common Agency and the Political Economy of IMF Lending,” International Studies Quarterly 54 (2010): 50-1. 29 Ibid., 54. 30 Jeffrey M. Chwieroth, “Normative Change from Within: The International Monetary Fund’s Approach to Capital Account Liberalization,” International Studies Quarterly 52 (2008): 155. 31 Bessma Momani, “IMF Staff: Missing Link in Fund Reform Proposals,” Review of International

Organizations 2, no. 1 (2007): 39. 32 Copelovitch, “Political Economy of IMF Lending,” 50. 33 Tamar Gutner, “World Bank Environmental Reform: Revisiting Lessons from Agency Theory,” International

Organization 59, no. 3 (2005): 782. 34Mary M. Shirley, “Bureaucrats in Business: The Roles of Privatization versus Corporatization in State-Owned Enterprise Reform,” World Development 27, no. 1 (1999): 116. 35 Daniel L Nielson and Michael J Tierney, “Delegation to International Organizations: Agency Theory and World Bank Environmental Reform,” International Organization 57, no. 2 (2003): 246.

7

authority.” IOs could “reinterpret institutional contracts,” “set policy agendas” and promote particular policy instruments to the benefit of having increased authority, which may not always be in correspondence with the preferences of principals.36 What matters to the “international agents” is the “survival and growth of their organization.”37

Any “control” on IOs comes from governments of member states and their representatives, which is hindered by “legal restrictions, high information cost and incentive problems.”38 If not filtered through authoritative institutional channels, pressure on IO agents is unlikely to be successful. The absence of “rewards” to staff members at IOs causes them to “ignore” the demands of “interest groups in given member countries.”39

According to P-A theory, “institutional behavior” and change can be predicted based on the “contractual relationship.” While the main concern of the principal is to “delegate authority” without “losing control,” agents engage in behaviors that target increasing “slack” and “autonomy,” such as “hiding information” or taking action without the principal’s consent.40 “Agency slack” is defined as “independent action by an agent that is undesired by the principal” by Hawkins et al. They classify agency slack into two forms: “shirking, when an agent minimizes the effort it exerts on its principal's behalf, and slippage, when an agent shifts policy away from its principal's preferred outcome and toward its own preferences.”41

To predict change in IOs, P-A models focus on “proximate principals,” which are entities with “the closest formal authority to an agent.” Despite pressure from several entities such as voters, non-governmental organizations (NGOs), and “distal principals,” Fund management and staff will most likely focus on demands of their proximate principal, “ignoring” the demands of those other entities.42

As briefly mentioned earlier, the EB’s influence on conditionalities is prevented by the “information asymmetry” in the Fund. After the Asian financial crisis of 1997, the IMF has made the letters of intent accessible online. Nonetheless, according to Stone, the staff kept on “filtering” the information it provided to the EB.43 Willett asserts that the IMF staff ‘‘seek to do good, but are not immune to bureaucratic incentives and external pressures.’’44 Public choice theorists emphasize that the reasons of staff’s “proposing larger loans” with more strings attached lie in interests including maximization of its “budget, autonomy, and influence.”45

P-A theory, which has been highly influential in studying IOs, is the backbone of this research. The following section defines the main features of my P-A model.

36 Liliana Andonova, “Why Do International Organizations Innovate? A Principal-Agent Perspective on Partnership for Sustainable Development,” paper prepared for the Annual Congress of the Swiss Political Science Association, 2010, http://www.sagw.ch/svpw/taetigkeiten/Kongress/Kongress-2010/Papiers_2010.html. 37 Roland Vaubel, “Principal-agent problems in international organizations,” The Review of International

Organizations 1, no. 2 (2006): 126-127. 38 Ibid., 131. 39 Nielson and Tierney, “Delegation to International Organizations,” 250. 40 Mark R. Hibben, “What Explains IMF Policy Shifts In Regards to Low Income Countries?” SSRN eLibrary (2011), http://papers.ssrn.com/sol3/papers.cfm?abstract_id=1900215. 41 Darren G. Hawkins, David A. Lake, Daniel L. Nielson, and Michael J. Tierney, “Delegation Under Anarchy: States, International Organizations, and Principal-Agent Theory,” in Delegation and Agency in International

Organizations, ed. Darren G. Hawkins, David A. Lake, Daniel L. Nielson, and Michael J. Tierney (New York: Cambridge University Press, 2006): 8. 42 Hibben, “What Explains IMF Policy Shifts.” 43 Stone, Controlling Institutions, 61. 44 Thomas Willett, “A Soft-Core Public Choice Analysis of the International Monetary Fund,” working paper 2000/56 (Claremont Colleges, 2000), http://www.claremontmckenna.edu/rdschool/papers/ 2000-56.pdf. 45 Copelovitch, “Political Economy of IMF Lending,” 57.

8

A Two-Level P-A Model

According to Nielson and Tierney, agency problems in the case of IOs are complicated by “three understudied factors,” one of which is that “the transmission of demands from ultimate principals to IOs” is complex due to IOs’ long “chain of delegation.”46 As indicated in the following series of P-A relationships that exists while implementing IMF SAPs, there is more than one principal and one agent:47

i. 185 member constituencies � their governments ii. these governments � the Board of Governors iii. the Board of Governors � the EB iv. the EB � the IMF Managing Director v. the IMF Managing Director � the IMF staff vi. the IMF staff � a borrower country vii. this government � domestic policy makers.48

As Gutner points out, the application of the P-A theory to IOs customarily focuses on the relationship between the member states and the IOs, which is certainly useful in questioning why state principals “delegate” authority to IO agents.49 However, when we stop the “chain of delegation” with the IO, we neglect a potential exogenous variable, namely the relation between the IMF staff and borrowing country authorities, which might be significant in explaining the variation in the number and scope of IMF conditionalities. Conditionality is a P-A issue, as all it involves is borrower countries (agent) being asked to change certain policies by donors (principals) “in return for aid.” This fact draws similarity between the “traditional P-A relationship” of private lenders-borrowers and the International Financial Institution (IFI) principals lending to borrower country agents, and the P-A problems arising from “asymmetric information” is common to both.50 Therefore, both sets of relationships matter in explaining the dependent variable (DV) of this research, i.e. the number and scope of conditionalities, which will be explained more thoroughly in the following sections. However, it is important to note that the P-A problem in the relationship between the IMF and the borrowing governments is highly “complex” due to “the nature of the task and the underlying contract, the mandate and structure of the principal, and the characteristics of the agents.”51 For that reason, a simple P-A model that takes the IMF as a unitary actor and examines its relations with the borrowing country (the agent) fails in capturing all the dynamics involved in designing conditionality. In this context, Putnam’s famous two-level game theory, which asserts that “we need to move beyond the mere observation that domestic factors influence international affairs and vice versa, and beyond simple catalogs of instances of such influence, to seek theories that integrate both spheres, accounting for the areas of entanglement between them,”52 has been a great inspiration for building a two-level P-A

46 Nielson and Tierney, “Delegation to International Organizations,” 242. 47 Raymond Vreeland, The IMF and Economic Development, (New York: Cambridge University Press, 2003), quoted in Sawa Omori, “Assessing the IMF Conditionality Programs: Implications for Governance of International Finance,” Interdisciplinary Information Sciences 15, no. 2 (2009): 192. 48 Ibid. 49 Gutner, “World Bank Environmental Reform,” 780. 50 Tamar Gutner, “Explaining the Gaps between Mandate and Performance: Agency Theory and World Bank Environmental Reform,” Global Environmental Politics 5, no. 2 (2005): 14. 51 Mohsin S. Khan and Sunil Sharma, “IMF Conditionality and Country Ownership of Programs,” working paper 01/142 (IMF Institute, 2001), http://www.imf.org/external/pubs/ft/wp/2001/wp01142.pdf. 52 Robert D. Putnam, “Diplomacy and Domestic Politics: The Logic of Two-Level Games,” International

Organization 42, no. 3 (1988): 433.

9

model. Purely focusing on the P-A problem between neither the EB and the IMF staff nor the IMF staff and the borrowing countries can account for the variation in the number and scope of IMF conditionalities. Instead, we need theories that “account simultaneously for the interaction of domestic and international factors,” as suggested by Putnam.53 In our case, this requires a two-level analysis of IMF lending.

As mentioned, the aforesaid shortcoming in the literature inspired me to form a two-

level P-A model for this research: at Level 1, the IMF staff is the agent and the EB is the principal, whereas at Level 2, the staff is the principal and the borrower country is the agent. I claim that in order to have a full picture of the P-A problem in the formation of SAPs, we need to take into account both sets of relationships. One can easily draw an analogy between the "two-table" metaphor Putnam uses to “capture the dynamics” of the negotiations at the Bonn summit conference of 197854 and the two-level P-A model this research builds to analyze variation in IMF lending behavior.

I do not observe the relation between the EB and the recipient country, since the staff acts as a mediator between the two and I observe the IMF management and the staff as a unitary actor. Therefore, I limit my discussion to the basic delegation from states to an IO, but I acknowledge that each step in the chains of delegation may lead to increases in “agency slack.”55

Level I: Principal Level II: Agent

Level I: Agent Level II: Principal

Figure 2: The Two-Level P-A Model

P-A models stress on incentives for the IMF staff to exploit “agency slack” in an effort to maximize the “likelihood of program success” and their “autonomy or budget.”56 However, as Gould points out, it has been commonly acknowledged that measuring the degree of

53 Ibid., 430. 54 Ibid., 434. 55 Erica R. Gould, “Delegating IMF Conditionality: Understanding Variations in Control and Conformity,” in Delegation and Agency in International Organizations, ed. Darren G. Hawkins, David A. Lake, Daniel L. Nielson, and Michael J. Tierney (New York: Cambridge University Press, 2006), 288. 56 Copelovitch, “Political Economy of IMF Lending,” 54.

Executive

Board

(member

states)

Borrower

country

IMF

management

and staff

10

agency slack is arduous.57 The design of the conditionality agreement is very uncertain in many aspects.58 Yet, it is a common belief that there are various aspects where Fund conditionality deviates from principal instructions, among which the number and “types of conditions” tend to have the most agency slack, while the “length” of Fund conditionality programs conform pretty closely to the instructions and the "conformance of the phasing of Fund conditionality programs is somewhere in between the two.59 Accordingly, this P-A model uses the number and scope of conditionalities instead of the length of the conditionality programs as its DV.

The two-level P-A model tries to examine not only agency slippage, but also what Gutner terms as antinomic delegation as a possible cause of the P-A problems in IMF lending, particularly at Level I, i.e. the EB-IMF staff relation. P-A theory recognizes the presence of “multiple or collective principals” in bureaucracies, who try to achieve goals that might sometimes be in “conflict.”60 “Antinomic delegation” is defined as “delegation consisting of conflicting or complex tasks that are difficult to institutionalize and implement.” In the presence of antinomic delegation, it is not possible to blame “performance problems” only on “agency shirking,” as they might as well be caused by the difficulty agents have in implementing goals that are challenging to specify and balance.61

The following section briefly explains the working hypotheses formulated so far, which will be tested with this P-A model. Obviously, as our theory and data interact and the theory evolves in the course of data collection, we do not need to have “a complete theory” in advance. As Keohane, King and Verba (KKV) argue, “some theory is always necessary before data collection and some data are required before any theorizing… learning from the data may be as important a goal as evaluating prior theories and hypotheses.”62 In this regard, further hypotheses can be formulated throughout data collection.

Working Hypotheses

As explained previously, the DV of this model is the number and scope of conditionalities. As a matter of fact, loan size could have been selected as another DV to measure, however, as Copelovitch’s quantitative model demonstrates, “in general, the staff enjoys greater autonomy and influence over the Fund’s use of conditionality, while G5 governments exert greater control over decisions about loan size.”63 Since this research examines the P-A problem in IMF lending, I use only the number and scope of conditionalities because we need to observe delegation of authority in order to examine agency slack.

As underlined by Denzin, the general approach in any study is to use a small set of hypotheses and gather data specifically along the dimensions considered, although approaching data with “multiple perspectives” and hypotheses would have value. Data that would prove “central hypotheses” false could be gathered and different theoretical points of view could be compared in terms of their “power” and “utility.”64 This strategy is called

57 Gould, “Delegating IMF Conditionality,” 286. 58 Ibid., 305. 59 Ibid., 303. 60 Gutner, “Mandate and Performance,” 21. 61 Ibid., 11. 62 Gary King, Robert O. Keohane, and Sidney Verba, Designing Social Inquiry: Scientific Inference in

Qualitative Research, (Princeton: Princeton University Press, 1994), 46. 63 Copelovitch, “Political Economy of IMF Lending,” 73. 64 Norman K. Denzin, The Research Act: A Theoretical Introduction to Sociological Methods, (Chicago: Aldine Publishing, 1970), 303.

11

“theoretical triangulation” in qualitative methods and there are many advantages it brings. Westie notes that it “minimizes the likelihood” of presenting a seemingly “coherent set of propositions,” where possibly “contradictory propositions” are neglected.65 The procedure requires consideration of “all relevant propositions” before starting the investigation, which should prevent a “particularistic explanation” of data by researchers.66 It could be the case that each of the propositions has a “kernel of truth.”67 Then a “final propositional network” can bring together features from initially contradictory hypotheses.68 The following working hypotheses were formulated based on the aforementioned strategy:

Level I:

H1: The number and scope of conditionality is proportionate to the agency slippage. The logic behind H1 was explained in detail in the previous section. Although the conventional wisdom expects the Fund to ease conditionality when a strategic ally of the G7 countries is borrowing, what we observe in some cases is many strings attached to the loans, which is contradictory with the principal’s preferences. Based on the discussion of the agency slippage of the IMF staff, we can surmise that in some cases, the staff had the leverage to push for more strings attached to the loans, owing to the information asymmetry. Clearly, the formulation of H1 is based on the well-known argument of Vaubel, which assumes that “international bureaucrats have the same utility function as national bureaucrats and that the economic theory of bureaucracy applies to both of them. Both try to maximize their power in terms of budget size, staff and freedom of discretion... Both enjoy some freedom to pursue these objectives because, in many respects, they have acquired an information monopoly and because the politicians need their cooperation.”69

Undoubtedly, we need variation in agency slippage over time to operationalize an independent variable (IV) that can account for the variation in the DV, which requires different cases to study. However, it is impracticable to observe the degree of slippage in different country cases, since in different political contexts slippage might have different denotations. In this regard, it makes more sense to test this hypothesis with a single country study, as concentrating on the temporal variations within multiple cases in a single country provides precision in the measurement of the said IV.

H2: The number and scope of conditionality is proportionate to the antinomic delegation.

The first hypothesis assumes a P-A problem. However, as discussed earlier, the problem might also come from the delegation side, as the principals could be delegating very “complex tasks” or tasks that are difficult to conform to the “mission of the institution” and “internal incentive systems.”70 In this regard, under the presence of antinomic delegation, we infer H2.

It is a challenging task to tailor a program that is supposed to save a country facing a deep economic crisis. However, if that country is strategically important to the principal, the EB tells the IMF staff to sign an agreement nonetheless. This is risky for the institution

65 Frank K. Westie, “Toward Closer Relations Between Theory and Research: A Procedure and an Example,” American Sociological Review 22 (1957): 154. 66 Denzin, The Research Act, 306. 67 Ibid., 307. 68 Ibid. 69 Roland Vaubel, “A Public Choice Approach to International Organization.” Public Choice 51, no. 1 (1986): 52. 70 Gutner, “Mandate and Performance,” 21.

12

because if the program fails, the legitimacy of the Fund, which has been periodically questioned since the collapse of the Bretton Woods System, will be damaged. Therefore, the IMF staff may design tough programs with many strings attached in order to ensure that even if the program fails, the IMF will not be declared as the scapegoat.

Level II:

As explained earlier, we observe P-A problems at Level II as well. As Drazen underscores, “the IMF (the principal) establishes a mechanism intended to ensure that reforms will be undertaken by the country authorities (the agent), in a setting in which the objectives of the Fund and the authorities do not fully coincide and there are informational asymmetries associated with the fact that the Fund cannot directly observe some aspects of the authorities’ actions objectives and/or circumstances.”71 H3: The number and scope of conditionality is proportionate to the past experience of agency slack as perceived by the IMF staff (who is the principal at this level). Observably, there is “path dependence”72 at this level. If the IMF staff is convinced that the country authorities shirked and resisted the reforms that they were supposed to implement as part of the agreement they signed with the Fund, the same country will face an increase in the number and scope of conditionality the next time it intends to borrow from the Fund. This working hypothesis is formulated partially based on the “Staff Statement on Principles Underlying the Guidelines on Conditionality” itself, which explicitly states that “[t]he member’s past performance in implementing economic and financial policies will be taken into account as one factor affecting conditionality, with due consideration to changes in circumstances that would indicate a break with past performance.”73 As emphasized by Khan and Sharma, since only countries facing macroeconomic or structural imbalances ask for loan from the Fund, the IMF conditionality has some “bite” to avoid the “moral hazard problem.”74 However, that “bite” precludes “full ownership” of the program by the borrowing country,75 and it might be part of the reason for agency slack at Level II. It goes without saying that testing this hypothesis requires a single country study in order to observe path dependence. H4: The number and scope of conditionality is proportionate to the degree of domestic opposition the borrowing government faces while carrying out the reforms. Agency slack and antinomic delegation are not the only sources of P-A problems. Drazen argues that “when a government faces domestic opposition to reform, conditionality can play a role even when the IMF and the government agree on the objectives of an assistance program.”76 The IMF defines national ownership as “a willing assumption of responsibility

71 Allan Drazen, “Conditionality and Ownership in IMF Lending: A Political Economy Approach,” IMF Staff

Papers 49, special issue (2002): 39. 72 I take on board the “narrower definition” of path dependence that is employed by Margaret Levi and Paul Pierson, which states that steps taken previously in a particular direction lead to movement in that same direction. For details see Margaret Levi, "A Model, a Method, and a Map: Rational Choice in Comparative and Historical Analysis," in Comparative Politics: Rationality, Culture, and Structure, ed. Mark I. Lichbach and Alan S. Zuckerman (Cambridge: Cambridge University Press, 1997), 28; Paul Pierson, “Increasing Returns, Path Dependence, and the Study of Politics,” The American Political Science Review 94, no. 2 (2000): 252. 73 International Monetary Fund, “Guidelines on Conditionality,” IMF, September 25, 2002, http://www.imf.org/external/np/pdr/cond/2002/eng/guid/092302.htm 74 Khan and Sharma, “Country Ownership of Programs.” 75 Ibid. 76 Drazen, “Conditionality and Ownership in IMF Lending,” 65.

13

for an agreed program of policies, by officials in a borrowing country who have the responsibility to formulate and carry out those policies, based on an understanding that the program is achievable and is in the country’s best interest.”77 However, in practice, country ownership is much more intricate than the way the IMF defines the concept. In this context, Drazen underlines that “though the authorities may “own” the program, this is not identical with ownership by the country as a whole. More formally put, since policymaking is the process of collective choice in the face of conflicting interests, ownership by some important policymakers is not ownership by the “policymaking apparatus.” Conditionality may then “strengthen the hands” of the reformers who are committed to carrying out reform but face domestic opposition.”78 Building on this argument, we can surmise that the IMF staff will set tougher conditionalities if the recipient country government is facing opposition domestically.

The Turkish Case

KKV underscores that “case studies are essential for description, and are, therefore, fundamental to social science. It is pointless to seek to explain what we have not described with a reasonable degree of precision.”79 Evidently, a single country study exploring the ways in which SAPs of the Fund are formed will be fundamental for this research and the motives are partially explained in the previous section. The country case that will be studied to solve the puzzle of this research is the Turkish case and the selection criteria are explained in detail in this section.

Turkey, who is a “key strategic ally” of the United States,”80 can be an interesting case to study, not only because of its importance for the G5 countries, but also because it has been one of what Bird, Hussain and Joyce might term as the “recidivist” borrowers81 of the Fund despite the consecutive crises it faced following the implementation of an IMF-led disinflation program that was launched in December 1999. Among the ten largest loans since 1983, Turkey has received three, holding the 18th largest quota.82

Turkey has been a member of the IMF since 1947 and received its first financial support from the Fund the following year. It requested assistance in the form of SBAs for the first time in 1961 and it became one of the most ardent borrowers of the Fund. As stated by the IMF in 2002, it borrowed resources over 15 times its quota,83 which leads us to think that the quota system is not strict as long as the borrower is strategically important for the G7 countries. It is especially the approval of lending approximately SDR 13 billion with the SBA signed in February 2002 that was then the largest one the IMF extended,84 which makes one think it was the United States pushing the Fund for providing big loans to Turkey. In this context, Stone claims that “Turkey’s access to IMF loans appeared to be assured throughout the 1990s in return for its cooperation with the United States–led operation to contain Iraq.”85

On the other hand, it was partly the implementation of the conditionalities urged by the Fund that led to undesirable consequences for the economy and the society as a whole,

77 International Monetary Fund, “Strengthening Country Ownership of Fund-Supported Programs,” IMF, December 5, 2001, http://www.imf.org/external/np/pdr/cond/2001/eng/strength/120501.pdf. 78 Drazen, “Conditionality and Ownership in IMF Lending,” 43. 79 King, Keohane, and Verba, Designing Social Inquiry, 44. 80 Ngaire Woods, “Understanding Pathways Through Financial Crises and the Impact of the IMF: An Introduction,” Global Governance 12 (2006): 384. 81 Graham Bird, Mumtaz Hussain and Joseph P. Joyce, “Many Happy Returns? Recidivism and the IMF,” Journal of International Money and Finance 23 (2004): 231. 82 Copelovitch, “Political Economy of IMF Lending,” 51. 83 IMF, IMF Annual Report, (Washington, District of Columbia: IMF, 2000), 166-169. 84 International Monetary Fund, “IMF Chronology.” 85 Stone, “IMF Lending in Africa,” 578.

14

which makes us go beyond the state-centric approach in making sense of the formation of SAPs. The instability and continuing high inflation rates during 1999 led the 57th coalition government to launch a disinflation program following the signing of an SBA with the IMF, starting from December 1999.86 The program was novel in the sense that it was a reflection of the “Post-Washington Consensus” that puts great emphasis on institutional reforms.87 The implementation of the “IMF-engineered” disinflation program however did not prevent the country from facing severe economic crises in November 2000 and February 2001 consecutively. The 2000 program was based on a “nominally pegged (anchored) exchange rate system for disinflation and on fiscal prudence.”88 Yeldan summarizes the impact of the Fund program as follows:

Over 2001 the GDP contracted by 7.4% in real terms, whole sale price inflation soared to 61.6%, and the currency lost 51% of its value against the major foreign monies. Real wages fall abruptly by 20% upon impact in 2001… The IMF has been involved with the macro management of the Turkish economy both prior and after the crisis, and provided financial assistance of $20.4 billion, net, between 1999 and 2003. Following the crisis, Turkey has implemented an orthodox strategy of raising interest rates and maintaining an overvalued exchange rate. The government was forced to follow a contractionary fiscal policy, and promised to satisfy the customary IMF demands: reduce subsidies to agriculture, privatize, and reduce public sector in economic activity.89

Therefore, on the one hand, one may assume that Turkey should be getting favorable conditions with fewer strings attached to the loans because of its strategic proximity as well as its economic relations with the G7 countries. Based on their “panel data analysis of 206 letters of intent from 38 countries submitted during the period April 1997 through February 2003,” Dreher and Jensen found evidence that “closer allies of all G7 countries were given significantly fewer conditions.”90 Likewise, Copelovitch claims that the IMF staff has greater “autonomy” only in the case of “non-intense” G5 country interests, leading to lending policies reflecting “bureaucratic interests,” again based on empirical research.91 On the other hand, we observe many strings attached to the loans that Turkey received, especially during the implementation the IMF-led disinflation program launched in 1999. This leads us to cast doubt on the state-centric approach claiming that the strategic allies of the United States are always favored by the IMF. In this regard, studying the Turkish case is crucial for this research. Although in 2009 Turkey declared that it preferred to “manage without IMF support and interference,”92 its long experience with the Fund will be illuminating. The numerous SBAs signed with the Fund provide us with variation in conditionalities over time, which extends the scope of this research beyond a single case study. Testing particularly H4 with

86 Erinc Yeldan, “Assessing the Privatization Experience in Turkey: Implementation, Politics and Performance Results,” (report submitted to the Economic Policy Institute, Washington, DC, 2005), http://www.bilkent.edu.tr/ ~yeldane/EPI_Report2005_Yeldan.pdf. 87 Ziya Onis, “Beyond the 2001 Financial Crisis: The Political Economy of the New Phase of Neo-Liberal Restructuring in Turkey,” paper no. 924623 (Social Science Research Network, 2006), http://papers.ssrn.com/ sol3/ papers.cfm?abstract_id=924623. 88 Umit Cizre and Erinc Yeldan, “The Turkish Encounter with Neo-liberalism: Economics and Politics in the 2000/2001 Crises,” Review of International Political Economy 12, no. 3 (2005): 387. 89 Erinc Yeldan, “Patterns of Adjustment Under the Age of Finance: The Case of Turkey as a Peripheral Agent of Neoliberal Globalization,” working paper no. 126 (Political Economy Research Institute, 2007), http://scholarworks.umass.edu/cgi/viewcontent.cgi?article=1100&context=peri_workingpapers. 90 Axel Dreher and Nathan M. Jensen, “Independent Actor or Agent? An Empirical Analysis of the Impact of U.S. Interests on International Monetary Fund Conditions,” Journal of Law and Economics 50, no. 1 (2007): 119. 91 Copelovitch, “Political Economy of IMF Lending,” 50. 92 Meltzer, “The IMF returns,” 445.

15

this critical case study will be helpful in disentangling the puzzle of this research, which is elucidated by the following instance.

The IMF program launched in 2005 relied on three pillars: “(1) fiscal austerity that targets achieving a 6.5 percent surplus for the public sector as a ratio to GDP, (2) contractionary monetary policy (through an independent central bank) that exclusively aims at price stability (via eventual inflation targeting), and (3) structural reforms consisting of many of the traditional IMF demands (privatization, large-scale layoffs in public enterprises, and removal of any form of subsidies).”93 The IMF staff seemed to be content with the performance of Turkey in implementing the Fund program. In evaluating the performance of the 2005 program, the IMF Staff Mission to Turkey stated that “[t]he outlook for the Turkish economy remains positive overall.”94 They added that “[t]he mission welcomed the authorities' intentions to implement important structural measures, in particular overhauling the social security system by early next year, tackling rising tax evasion by enhancing auditing capacity under the Revenue Administration, privatizing Halkbank, and adopting measures to restore financial soundness to energy companies (including by allowing full cost-recovery pricing).”95 The Turkish experience in privatization in the 2000s is an illuminating instance in this context. Privatization of large-scale state economic enterprises (SEEs) was one of the main pillars of the 2005 program.96 The SBA signed with the IMF for the May 2005-May 2008 period set strict targets for the privatization of the most profitable SEEs of Turkey. The Article 33 of the Letter of Intent submitted to the IMF envisaged the sale of the shares of PETKİM (Petrochemical Conglomerate), TÜPRAŞ (Turkish Petroleum Refineries Corporation), ERDEMİR (iron and flat steel producer) and Türk Telekom (the incumbent operator in the Turkish fixed line telecommunications) by the end of 2005.97 The privatizations of these large-scale SEEs, all of which were highly profitable, via block sales led to huge controversies domestically, particularly concerning the legality of the tender processes. However, the Justice and Development Party (AKP) government has been exceptionally “successful” in suppressing the opposition against the block sales, despite various accusations of corruption claims against the AKP and its bureaucrats. As a result, the AKP sold nearly all of the targeted SEEs that had been on the privatization agenda since the 1980s in return for amounts that were equal to a couple of year profits of these enterprises. Despite the neo-liberal claim of market efficiency on the basis of competition, the block sales of these SEEs, most of which used to be state monopolies, have transformed them into private monopolies. The Fund neglected the fact that privatizing SEEs without building necessary institutional infrastructures that would develop competition in the market would lead to the formation of private monopolies, operating against consumers.98 The staff set strict targets for the privatization of the aforementioned SEEs and put a great emphasis on the importance of privatization per se for the success of the IMF-led program, which supports H4 in the Turkish case. As supported by this instance among many others, the Turkish case is a critical case to study, which will provide insight into the answer to our puzzle. A country that has signed 19 SBAs with the Fund in 47 years certainly offers variation in a single country study. The time frame and details of data collection are explained in the following sections.

93 Erinc Yeldan, “Neoliberal Global Remedies: From Speculative-Led Growth to IMF-Led Crisis in Turkey,” Review of Radical Political Economics 38 (2006): 209. 94 International Monetary Fund, “Statement by the IMF Staff Mission to Turkey Press Release No. 07/239,” http://www.imf.org/external/np/sec/pr/2007/pr07239.htm. 95 Ibid. 96 For a detailed analysis of the aforementioned program and the privatizations, see Merih Angin, “Turkish Experience in Privatization: The Privatizations of Large-Scale State-Economic Enterprises in the 2000s” (master’s thesis, Middle East Technical University, 2010). 97 Yeldan, “Assessing the Privatization Experience." 98 Stiglitz, Globalization and Its Discontents, 220.

16

Operationalization of the Dependent Variable

As explained earlier, my P-A model uses the number and scope of conditionalities

instead of the length of the conditionality programs as the dependent variable. However, there are certain clarifications that need to be made regarding the operationalization of my DV, since measuring the stringency of conditionality is not as straightforward as it might seem.

The number of conditionalities has led to numerous controversies hitherto. As Dreher and Jensen recall, “in 1999 the U.S. Congress threatened to refuse ratification of a quota increase if the IMF did not reduce the stringency and number of its policy conditions,”99 and debates of that nature have rendered the analysis of the number of conditions intriguing for scholars. As “objectively” measuring and comparing the “intrusiveness and stringency” of certain conditions is a challenging task,100 various scholars such as Kang, Copelovitch, Dreher and Jensen101 set the DV for their empirical analyses as the number of IMF conditions.102 Due to the lack of a “comprehensive index” of Fund structural conditionality covering a long period of time, scholars used to rely on a set of statistics to measure conditionality.103 However, in January 2009 a previously internal IMF database, MONA (the Monitoring of Fund Arrangements), was released on the website of the Fund upon recommendation by the Independent Evaluation Office of the IMF, approved by the Board. MONA is a collection of comparable data on the economic objectives and results of arrangements supported by the IMF.104 As this is the only dataset providing a comprehensive view of all types of structural conditions (SCs) by including prior actions (PAs), performance criteria (PCs), conditions for completion of program reviews and structural benchmarks (SBMs),105 it is increasingly used by scholars to analyze IMF conditionality quantitatively. Conditionality of an IMF-led program changes shape over time based on the policies of the country as well as unexpected events.106 Therefore, as underlined by Stone, analyzing letters of intent to observe the scope of a program may give a “misleading” view of a still evolving program.107 Most arrangements approved since 2002 are included in the MONA database. Unfortunately, the SBA Turkey signed in 2002, which was approved on April 2, 2002, is one of the six arrangements that are not included.108 This leaves us with only one option, which is merging the data available in MONA database with the MONA archive that provides data for the period 1993-2003. Accordingly, we set the time frame of the research from 1994 to 2008, as the first SBA covered by the archived MONA data was approved by the Fund on July 8, 1994.109 Even if

99 Dreher and Jensen, “Independent Actor or Agent,” 110. 100 Ibid. 101 See Copelovitch 2010; Dreher and Jensen 2007; Kang 2007. 102 As a matter of fact, measuring the average tightness of a program via counting the number of conditions imposed as the dependent variable is a method developed by Mosley, Harrigan and Toye. Nonetheless, they did not explicitly state the way they counted conditions. For details, see Paul Mosley, Jane Harrington and John Toye, Aid and Power: The World Bank and Policy-based Lending, Volume I: Analysis and Policy Proposals London: Routledge, 1995). 103 Morris Goldstein, “IMF Structural Conditionality: How Much Is Too Much,” working paper 01-04 (Institute for International Economics, 2000), http://ww.petersoninstitute.org/publications/wp/01-4.pdf. 104 International Monetary Fund, “Frequently Asked Questions: MONA,” http://www.imf.org/external/np/pdr/ mona/monafaq.aspx. 105 Goldstein, “IMF Structural Conditionality.” 106 Stone, “Scope of IMF Conditionality,” 599. 107 Stone, Controlling Institutions, 157. 108 International Monetary Fund, “Frequently Asked Questions: MONA.” 109 International Monetary Fund, “Turkey: History of Lending Arrangements from May 01, 1984 to May 31, 2012,” http://www.imf.org/external/np/fin/tad/extarr2.aspx?memberKey1=980&date1key=2012-05-31.

17

the archived MONA database covered the SBA approved on April 04, 1984, it would be highly difficult to collect data for the right hand side of the model in order to explain the variation, if there was any, since some of the IVs of the model are purely based on the interviews with the IMF staff and Turkish technocrats.

The several types of conditionality included in the Fund programs differ in how specific they are, what they include and their monitoring requirement, which results in a difference in how “binding” they are on the recipient country.110 The IMF lists the different forms of conditions as follows:

Prior actions are measures that a country agrees to take before the IMF’s Executive Board approves financing or completes a review... Quantitative performance criteria (QPCs) are specific and measurable conditions that have to be met to complete a review. Indicative

targets are used to supplement QPCs for assessing progress. Sometimes they are also set when QPCs cannot because of data uncertainty about economic trends... Structural

benchmarks are (often non-quantifiable) reform measures that are critical to achieve program goals and are intended as markers to assess program implementation during a review. They vary across programs: examples are measures to improve financial sector operations, build up social safety nets, or strengthen public financial management.111

Policy conditions have always been an essential part of IMF lending. While IMF conditionality was mainly based on “macroeconomic policies” until the early 1980s, in later years “structural conditions” faced an increase in complexity and scope.112 There are several studies reporting the trend increase in the number of conditions per program. Copelovitch’s analysis reports a roughly constant mean at 6.5 for the number of PCs contained in “nonconcessional IMF loans” over time. However, this comes with non-negligible cross sectional variation for the period 1984-2003, where the number of PCs ranges from “0 to 16.” Based on the analysis, IMF has significantly increased its use of targets, PAs and benchmarks in recent years, with “the average number of non-PC conditions” going from the 1984 number of 0.3 to 11 in 2003. A significant variation was also observed in the use of “non-PC (softer) conditionality” in different cases, where “the number of benchmarks/targets” varies between 0-27 with a mean of 4.1, and “the number of PAs” is in the range 0-37 with a mean of 2.7.113 Alternatively, Goldstein reports that “the number of structural policy conditions” in the case of “a typical one-year SBA” would be in the range 9-15.114 He further claims that the Fund SBAs aimed to keep the number of “structural policy performance criteria” at a minimum while avoiding “micro” conditionality.115 Nevertheless, the observed number of structural conditions greatly exceeds what would be expected if the “only in exceptional cases” guideline in the conditionality guidelines for SBAs composed in 1979 was adhered to.116 This reinforces the hypothesis (H1) that the number and scope of conditionality is proportionate to the IMF staff’s engagement in agency slippage.

In a nutshell, the aforementioned results essentially indicate that solely counting the number of PCs cannot reflect the changing nature of conditionalities. Taking into consideration Goldstein’s analysis reporting that “a typical one-year SBA” has about “a dozen structural conditions” when performance criteria, conditions for program reviews, structural

110 Copelovitch, “Political Economy of IMF Lending,” 52. 111 International Monetary Fund, “Factsheet: IMF Conditionality,” http://www.imf.org/external/np/exr/facts/ conditio.htm. 112 Ibid 113 Copelovitch, “Political Economy of IMF Lending,” 53. 114 Goldstein, “IMF Structural Conditionality.” 115 Ibid. 116 Ibid.

18

benchmarks and prior actions are combined, we cannot exclude the structural conditions from our analysis.117 What is more, in time, the Fund has changed the instruments for “monitoring structural conditionality,” with its focus shifting more towards the use of conditions for program reviews, structural benchmarks and prior actions rather than “formal performance criteria.” Before 1980s, performance reviews concerning structural policies were very rare for SBAs and the IMF would hesitate about asking for prior actions,118 which was no longer the case when Turkey was heavily borrowing during the 1990s and early 2000s. Goldstein’s analysis states that the combined number of structural benchmarks, prior conditions and program reviews was about “five times” as many as structural performance criteria, when the average number of structural conditions for SBAs in the period 1996-99 is considered,119 which was more or less the case in Turkey too. Some basic performance criteria are included in almost all programs so that without the inclusion of structural benchmarks variation is small.

After a comprehensive review, the IMF revised the guidelines on conditionality in 2002. In an effort to bolster its capacity for “prevention and resolution of crises,” the IMF made changes in its conditionality framework in March 2009, which included abolishing structural performance criteria “requiring formal waivers,” and having structural reforms “covered by overall program performance reviews.”120 However, since Turkey has not borrowed from the Fund after 2008, the 2009 reform has no effect on this analysis. All things considered, solely taking into account the number of PCs, which is a method used by some scholars such as Kang,121 we may not have enough variation over time in a single country study. Below I explain the operationalization of the DV more thoroughly.

Stone introduced a new method in 2008, which measures the substantive scope of conditionality as a DV instead of a simple count of the number of conditions.122 As a result, he showed that there is great variation in the “substantive focus” of IMF programs, and the “breadth of the programs” is partly shaped by the domestic political constraints of the borrower countries.123 His foremost dependent variable was set as “the number of categories of conditions” that would be tested in a “particular review.” He claims that this is a good measure for capturing the “scope of conditionality.”124 Stone’s method has been an inspiration for the operationalization of the DV of this research and in a similar fashion; my plan is to use the following economic sector categories commonly used in the classification of quantitative conditions: Total domestic credit, Credit to Government/Public Sector, BOP/Reserve Test, Medium/Long-Term External Debt, Subceiling on Medium/Long-Term External Debt, Short-Term Debt, No new arrears/default, Ceilings on external arrears, Fiscal Deficit, Domestic Arrears and Exchange rates.125 However, the picture is more blurred while coding structural conditionality.

Due to the “heterogeneity” of structural conditions, a within-program or cross-program unit of account allowing for the aggregation and comparison of structural conditionality measures fails to exist. While a single policy action can be subject to a “single condition” in some cases, it can be separated into steps in another case, with a separate

117 Ibid. 118 Ibid. 119 Ibid. 120 International Monetary Fund, “Factsheet: IMF Conditionality.” 121 See Kang 2007. 122 Stone, “Scope of IMF Conditionality,” 591. 123 Ibid. 124 Ibid., 599. 125 International Monetary Fund, “MONA Glossary,” http://www.imf.org/external/np/pdr/mona/glossary.aspx.

19

condition for each step.126 This is the main shortcoming of Stone’s method and Stone himself acknowledges that “a six-fold categorization of structural reforms exaggerates the similarity of conditions across countries.”127 The same applies to our single country study, where we get the variation in the various SAPs implemented in Turkey. The solution to this limitation can be derived from the method suggested in the IEO’s evaluation report on “Structural Conditionality in IMF-Supported Programs” (2007), which refers to the degree of structural change that SCs would bring about if implemented as the “structural content” or “structural depth (SD)” of conditions.128 The analysis uses three categories to distinguish the SD of SBMs, PCs and PAs: i) “Little or No (0):” The conditions in this category can be “stepping stones” on the way to major reforms, although they are not capable of causing “meaningful economic changes” on their own. ii) “Little SD (1):” The conditions in this category can have an “immediate and possibly significant effect,” but for the effect to last, they need to be succeeded by other measures. iii) “High SD (2):” The conditions in this category are self-sufficient to lead to “changes in the institutional environment” that are “long lasting.”129

The aforementioned categorization is the other inspiration for the operationalization of the DV of my P-A model. Different methodologies are needed to address the questions on IMF lending behavior due to the variance in the “nature of the questions.”130 As underscored in an evaluation by the IEO, some questions require an analysis of “patterns across” many programs and use of “quantitative indicators,” whereas “qualitative judgments” is best for answering others. The best way to address the questions requiring qualitative judgments is using “case studies,” which is the method that this research takes on board.131 The interviews with Turkish technocrats will help me categorize the SCs according to their structural depth. For instance, privatizations of large-scale SEEs in Turkey in the 2000s, as well as the major consolidation that the Turkish banking sector went through during between 1999 and 2003 in the aftermath of a failed IMF-led disinflation program can be categorized as High SD and interviews with the technocrats will certainly provide insight into the categorizations of this sort. Obviously, categorizations are never perfectly objective. Nevertheless, I believe that relying on the Turkish technocrats’ as well as the IMF staff’s view on the SD of the SCs will be instrumental in classifying them. The Fund has identified ten policy areas as categories for measure of structural policy conditions, namely exchange system, tax & expenditure reform, financial sector, trade system, pricing & marketing policies, public enterprises and privatization, systemic and ownership reform, social safety net, labor market, agricultural sector.132 It remains to be seen how many of these policy areas will be utilized to examine the variation in the structural conditionalities attached to the SAPs implemented in Turkey. To sum up, all types of SCs, i.e. SBMs, PAs and PCs will first be coded in categories according to their policy areas, which will be followed by the categorization based on SD.

Taking everything into account, the DV of my P-A model will measure the scope of conditionality via coding the IMF conditionality in twenty-one categories, ten of of which are quantitative conditions, while the rest are structural conditions. More than likely, the number of categories will be reduced once the merged dataset is clean. As I tried to explain

126 International Monetary Fund, “Evaluation of Structural Conditionality in IMF-Supported Programs,” Issues

Paper for an Evaluation by the Independent Evaluation Office (IEO), May 17, 2005, http://www.ieo-imf.org/ ieo/files/issuespapers/051805.pdf. 127 Stone, Controlling Institutions, 159. 128 Independent Evaluation Office of the International Monetary Fund, “Structural Conditionality in IMF-Supported Programs,” Evaluation Report (IEO, 2007), http://www.ieo-imf.org/ieo/files/completedevaluations/ 01032008SC_main_report.pdf. 129 Ibid. 130 International Monetary Fund, “Evaluation of Structural Conditionality.” 131 Ibid. 132 Goldstein, “IMF Structural Conditionality.”

20

thoroughly, although categorization is less objective than counting the raw number of conditions, the usefulness of that method is not well-supported, as it cannot capture the stringency of conditionality.

Independent Variables

As mentioned previously, P-A theory is fairly powerful in explaining “opportunities

for agency losses.”133 However, as Gould points out, most of the work in the P-A tradition is based on quite thin assumptions regarding agent interests, which are mainly maximization of budget and “slack” as well as task expansion.134 As it will be explained more thoroughly in the following sections, the interviews with both the IMF and Turkish technocrats will be analyzed to develop more scrupulous assumptions about agent preferences over their activity in the context of IMF lending. This research is not based on the “thin assumptions” of the standard P-A models regarding bureaucratic interests, as explained previously. Through conducting interviews, I am expecting to derive more specific preferences over agent activity instead of accepting the standard P-A theory assumption of self-interested, self-maximizing bureaucrats pursuing their own preferences owing to information asymmetries and the IVs of the model will be operationalized accordingly. As mentioned earlier, the research will use mixed methods to solve its puzzle. Interviews with the IMF staff and Turkish technocrats will be crucial to get further insights. I am conducting interviews in Turkey to derive conclusions about the P-A issues both at Level I and Level II. As Denzin underscores, “triangulating data sources” would allow us to use the same methods to achieve “maximum theoretical advantage.” 135 In this context, data triangulation will be taken on board to analyze the EB-IMF staff and IMF staff-Turkish technocrat relations.

Qualitative Analysis

In order to measure the degree of agency slack, I rely on a comparison between the EB

preferences extracted from the EB meeting minutes and the interviews with Turkish technocrats that might give hints about the extent of IMF staff’s engagement in agency slippage. To measure antinomic delegation, I mainly rely on the interviews with the IMF staff and EDs, and compare them with the EB meeting minutes. I am essentially looking at the divergence of views between the EB and the staff. As for Level II, the interviews with the IMF staff and Turkish technocrats will be used to test H3 and H4.

Clegg points out that the minutes of EB meetings, which provide a “verbatim record of Board discussions including prepared statements as well as spontaneous comments,” are a great resource for “observing the shifting balance of ideas” of IMF’s “top table”.136 There is a growing literature on the IMF lending behavior, drawing on minutes of EB meetings, one of which is Clegg’s research analyzing the “internal dynamics” of the Fund, focusing on how “the power of money was mediated through the power of words in IMF Board room discussions of the Enhanced Structural Adjustment Facility”137 between 1987 and 1998. His application of quantitative coding techniques to the analysis of EB meetings is an inspirational

133 Gutner, “World Bank Environmental Reform,” 780. 134 Gould, “Delegating IMF Conditionality,” 308. 135 Denzin, The Research Act, 301. 136 Liam Clegg, “Global Governance Behind Closed Doors: The IMF Boardroom, the Enhanced Structural Adjustment Facility, and the Intersection of Material Power and Norm Stabilisation in Global Politics,” The

Review of International Organizations 7, no. 3 (2012): 297. 137 Ibid., 2.

21

“methodological innovation” in this literature.138 This technique could be promising for my research as well, since recently the embargo on minutes of EB meetings was reduced from ten to five years,139 which will be sufficient for this research’s time frame as Turkey signed its last SBA with the Fund in 2005, which ended in 2008. The recorded minutes of the EB may provide significant insights about the preferences of the EB regarding the SAPs designed for Turkey.

Gould’s research, which provides an assessment of variations in the IMF’s agency slack with respect to the design of Fund conditionality agreements, uses new measures of IMF conditionality and principal references.140 In the 16 interviews the author did between September 1999 and May 2002 in Washington DC, San Francisco and New York, she asked open-ended questions about constructing, influencing and revising Fund conditionality programs as well as the roles of an ED/staff member and the role of the Fund in the international system.141 For measuring “principal preferences” over Fund conditionality design, Gould mainly relies on Conditionality Guidelines, which are debated and passed by the EB according to the decision rule used to approve conditionality agreements.142 My research is designed in a similar fashion; however, I use EB meeting minutes instead of Conditionality Guidelines to derive information about principal preferences.

To sum up, the research will be conducted with quantitative and qualitative methods, which is well-suited for the eclectic approach that is used to solve the puzzle of this research. The quantitative analysis of the research, which is currently being tested, is beyond the scope of this paper, therefore, without going into details, I briefly explain the use of a quantitative model for this research in the following section.

A Tentative Quantitative Model

As explained previously, this research is taking on board data and theoretical triangulation and it will use mixed methods to solve its puzzle, which can be analogous to what is termed as “methodological triangulation” in sociological research,143 assuming that if a hypothesis can “survive the confrontation of a series of complementary methods of testing, it contains a degree of validity unattainable by one tested within the more constricted framework of a single method.”144 As Denzin emphasizes, “the rationale for this strategy is that the flaws of one method are often the strengths of another, and by combining methods, observers can achieve the best of each, while overcoming their unique deficiencies.”145 In this regard, I am considering an analysis of the variation in conditionalities using quantitative methods, which will be utilized as a stepping stone for the qualitative analysis for the following reasons.

As discussed earlier, there is a growing number of quantitative studies of conditionality in the literature with different conclusions. Some of “the empirical tests support the theory that political economic factors influence IMF conditionality, superseding an explanation based solely on economic criteria,”146 whereas according to some others, “there is

138 Ibid., 3. 139 Ibid., 21. 140 Gould, “Delegating IMF Conditionality,” 283. 141 Ibid., 285. 142 Ibid., 287-8. 143 Denzin, The Research Act, 308. 144 Eugene J. Webb, Donald T. Campbell, Richard D. Schwartz, and Lee Sechrest. Unobtrusive Measures:

Nonreactive Research in the Social Sciences (Chicago: Rand McNally, 1966), 174. 145 Denzin, The Research Act, 308 146 Kang, “Agree to Reform,” 708.

22

substantial evidence across the models that technocratic economic factors are key determinants of IMF conditionality.”147 However, this research tests its hypotheses with a single country study, therefore in contrast to previous studies that used a pooled sample of countries, this is the only, to the best of my knowledge, single country investigation attempting to analyze variation in IMF conditionality. I believe that the quantitative analysis part of this study is important due to its methodology and the estimations, which can easily be applied to other country cases.