how robots conquer industry worldwide · pdf filehow robots conquer industry worldwide. ifr...

TRANSCRIPT

How robots conquer industry worldwide

IFR Press Conference, 27 September 2017Frankfurt

Schedule

• Welcome and introduction of the panelists• Global robot market up to 2020

by Joe Gemma• Today‘s trends – tommorow‘s robots

by Steven Wyatt• Questions

International Federation of RoboticsRepresenting the global robotics industry

• Robotics turnover 2016: $40 billion• More than 50 members:

• National robot associations• R&D institutes• Robot suppliers• Integrators

• Sponsor of the International Symposium on Robotics (ISR)

• Co-sponsor of the IERA Award

• Primary resource for worldwide data on use of robotics – IFR Statistical Department

Speakers on the Panel

Joe GemmaIFR President

President and CEO,KUKA Robotics Corp., USA

Gudrun LitzenbergerIFR General SecretaryFrankfurt

Steven WyattIFR Executive Board Member

Group Vice President,and Head of Marketing & Sales Robotics, ABB, CH

Joe Gemma, IFR President

Global Robot Market up to 2020

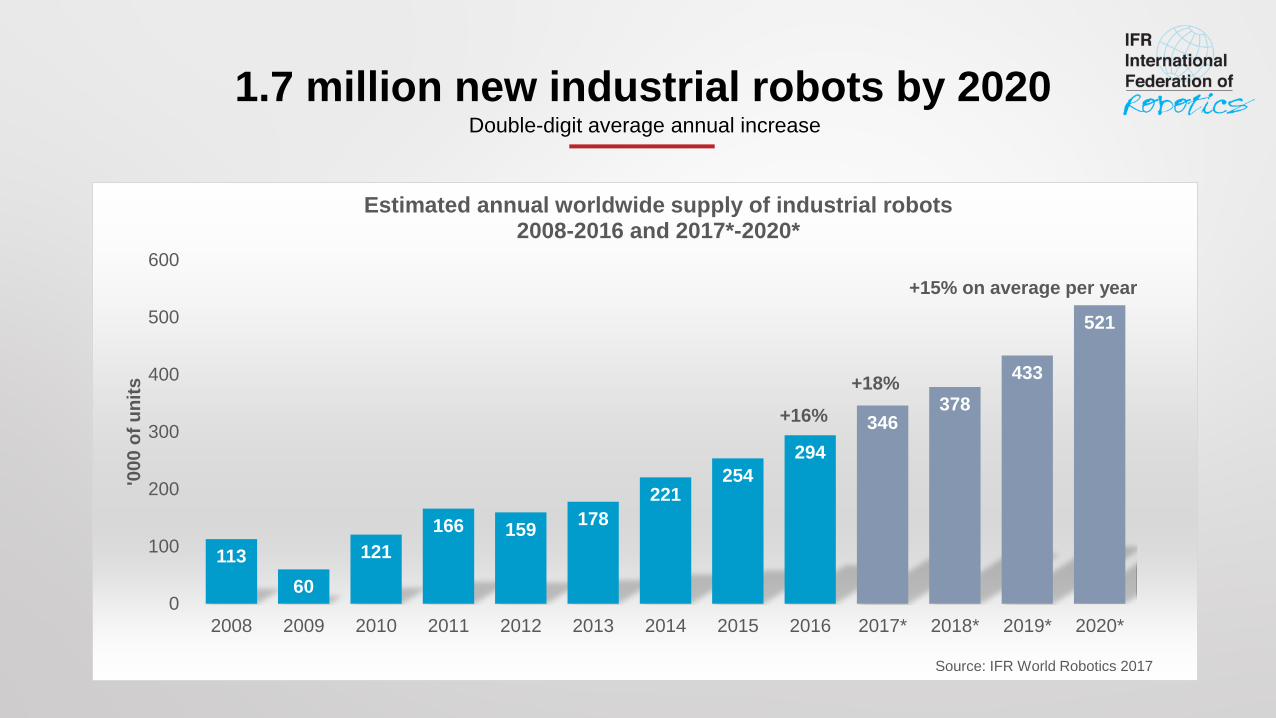

1.7 million new industrial robots by 2020Double-digit average annual increase

11360

121166 159 178

221254

294346

378433

521

0

100

200

300

400

500

600

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017* 2018* 2019* 2020*

'000

of u

nits

Estimated annual worldwide supply of industrial robots2008-2016 and 2017*-2020*

Source: IFR World Robotics 2017

+16%

+15% on average per year

+18%

Continued increase in major industries

24

11

7

17

21

46

94

20

15

7

20

29

65

98

24

19

8

20

29

91

103

0 20 40 60 80 100 120

Unspecified

Others

Food

Chemical, rubber and plastics

Metal

Electrical/electronics

Automotive industry

'000 of units

Estimated annual supply of industrial robots at year-endby industries worldwide 2014-2016

2016 2015 2014

Source: IFR World Robotics 2017

+6%

+41%

-3%

-4%

+20%

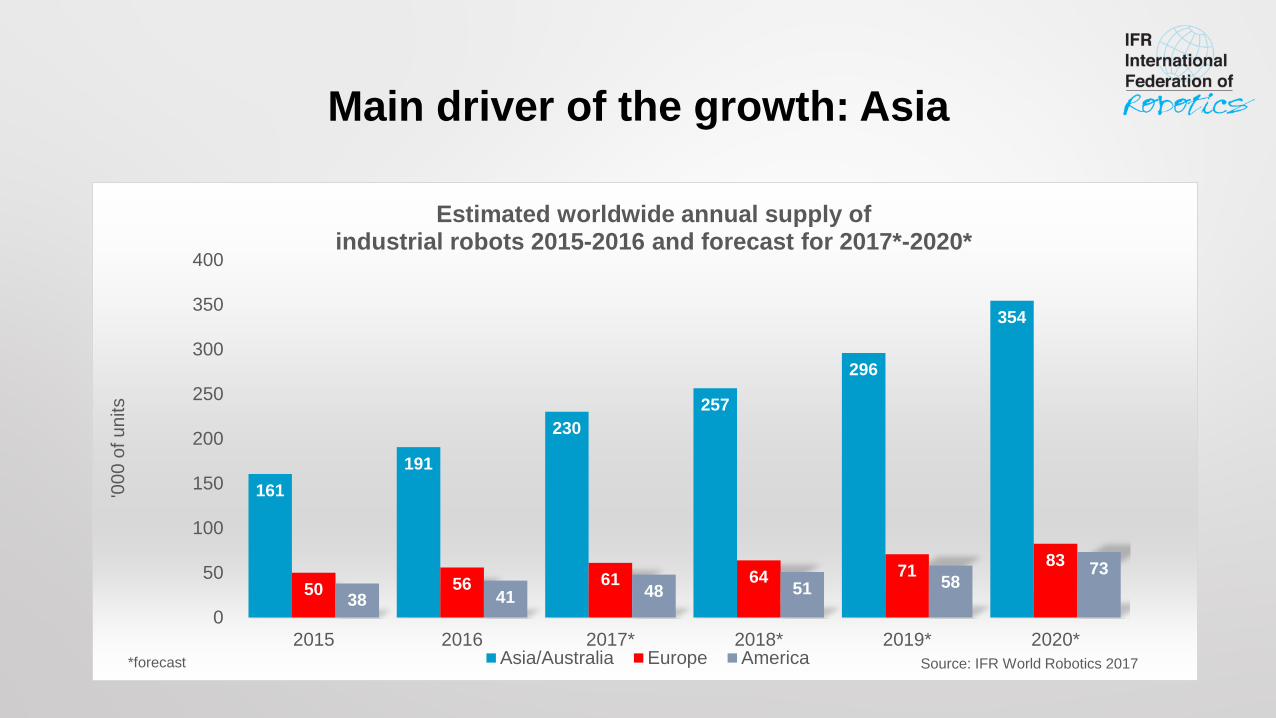

Main driver of the growth: Asia

161191

230257

296

354

50 56 61 64 71 83

38 41 48 51 5873

0

50

100

150

200

250

300

350

400

2015 2016 2017* 2018* 2019* 2020*

'000

of u

nits

Estimated worldwide annual supply ofindustrial robots 2015-2016 and forecast for 2017*-2020*

Asia/Australia Europe America Source: IFR World Robotics 2017*forecast

2016: 5 markets account for 74% of total supply

2,02,32,62,62,6

3,94,2

5,96,57,6

20,031,4

38,641,4

87,0

0 10 20 30 40 50 60 70 80 90 100

Czech RepublicCanada

SingaporeIndia

ThailandSpain

FranceMexico

ItalyTaiwan

GermanyUnited States

JapanRepublic of Korea

China

'000 of units

Estimated worldwide annual supply of industrial robots15 largest markets 2016

Source: IFR World Robotics 2017

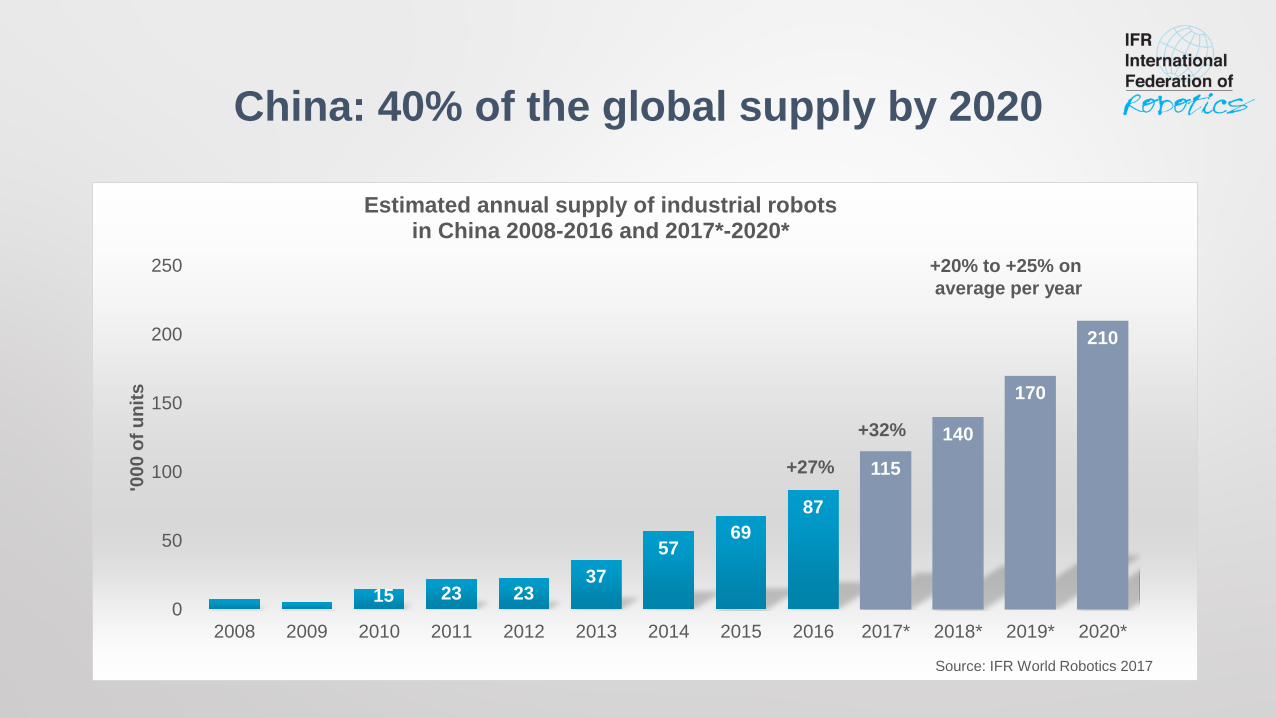

China: 40% of the global supply by 2020

15 23 2337

5769

87

115

140

170

210

0

50

100

150

200

250

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017* 2018* 2019* 2020*

'000

of u

nits

Estimated annual supply of industrial robotsin China 2008-2016 and 2017*-2020*

Source: IFR World Robotics 2017

+27%

+20% to +25% onaverage per year

+32%

Rep. of Korea: considerable increase since 2010

128

24 26

19 2125

3841 44 42 44

50

0

10

20

30

40

50

60

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017* 2018* 2019* 2020*

'000

of u

nits

Estimated annual supply of industrial robotsin the Rep. of Korea 2008-2016 and 2017*-2020*

Source: IFR World Robotics 2017

+8%

+5% to +10% onaverage per year

+5%

Japan: significant recovery and continued growth

33

13

22

28 2925

29

3539

42 44 4548

0

10

20

30

40

50

60

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017* 2018* 2019* 2020*

'000

of u

nits

Estimated annual supply of industrial robotsin Japan 2008-2016 and 2017*-2020*

Source: IFR World Robotics 2017

+10%

+5% onaverage per year

9%

USA: considerable increase since 2010

13

7

14

21 22 2426 28

3136 38

45

55

0

10

20

30

40

50

60

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017* 2018* 2019* 2020*

'000

of u

nits

Estimated annual supply of industrial robotsin the USA 2008-2016 and 2017*-2020*

Source: IFR World Robotics 2017

+14%

+15% onaverage per year

15%

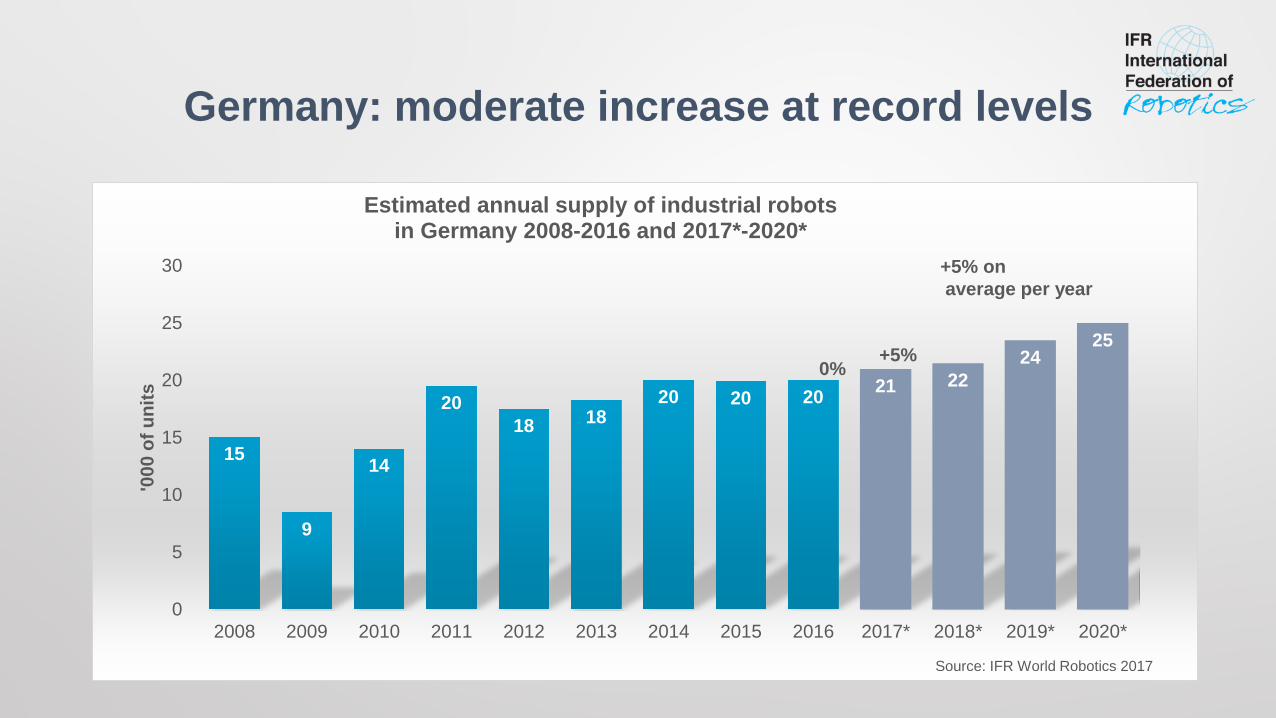

Germany: moderate increase at record levels

15

9

14

2018 18

20 20 20 21 2224

25

0

5

10

15

20

25

30

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017* 2018* 2019* 2020*

'000

of u

nits

Estimated annual supply of industrial robotsin Germany 2008-2016 and 2017*-2020*

Source: IFR World Robotics 2017

0%

+5% onaverage per year

+5%

2020: 3 million industrial robots in operation

1.035 1.021 1.059 1.153 1.235 1.3321.472

1.6321.828

2.0552.323

2.644

3.053

0

500

1.000

1.500

2.000

2.500

3.000

3.500

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017* 2018* 2019* 2020*

'000

of u

nits

Estimated worldwide operational stock ofindustrial robots 2015-2016 and forecast for 2017*-2020*

Source:IFR World Robotics 2017

+12%+12%

+14% on averageper year

*forecast

2020: 1.9 million operating in Asian factories

8871.025

1.1861.380

1.618

1.912

433 460 493 527 563 612

274 300 326 359 397 453

0

500

1.000

1.500

2.000

2.500

2015 2016 2017* 2018* 2019* 2020*

'000

of u

nits

Estimated worldwide operational stock ofindustrial robots 2015-2016 and forecast for 2017*- 2020*

Asia/Australia Europe America Source: IFR World Robotics 2017*forecast

2020: 950,000 robots operating in China

256340

451

585

748

950

287 287 285 292 301 316

0

100

200

300

400

500

600

700

800

900

1.000

2015 2016 2017* 2018* 2019* 2020*

'000

of u

nits

Estimated operational stock of industrial robotsin China and in Japan 2015-2016 and forecast for 2017*-2020*

China Japan Source: IFR World Robotics 2017*forecast

Steven Wyatt, IFR Executive Board

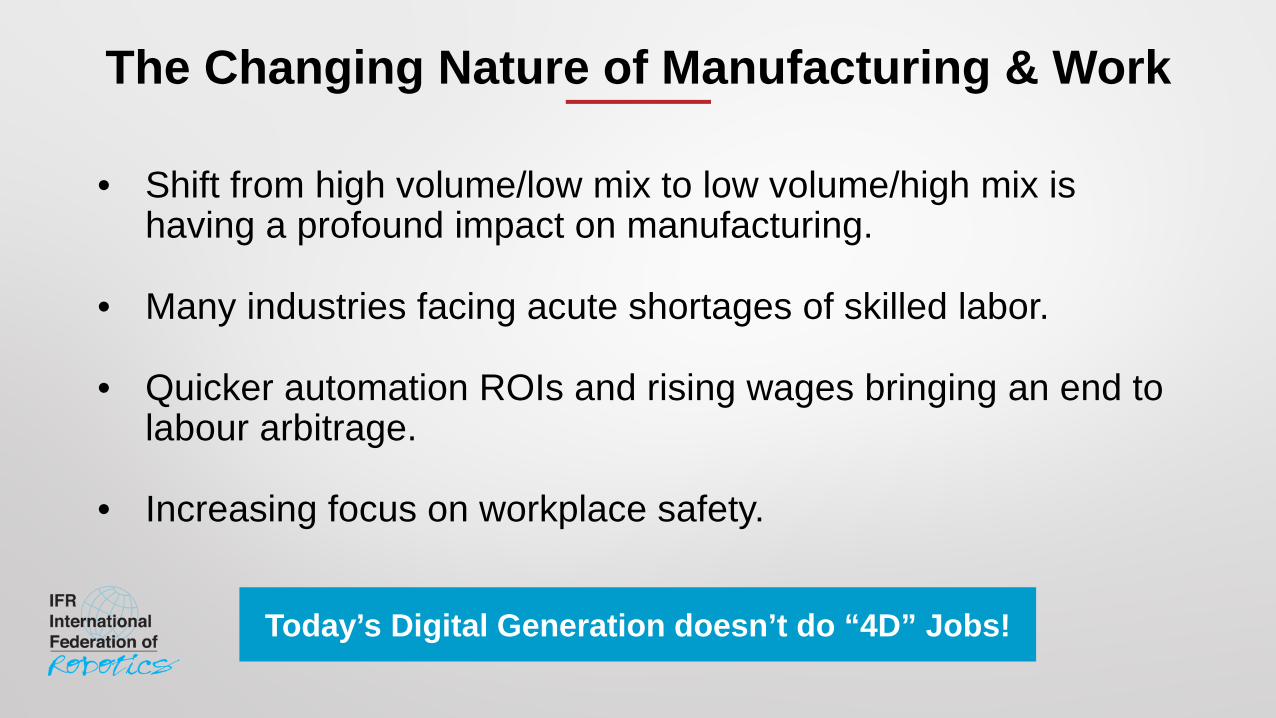

Today’s trends, tomorrow’s robots!

• Shift from high volume/low mix to low volume/high mix is having a profound impact on manufacturing.

• Many industries facing acute shortages of skilled labor.

• Quicker automation ROIs and rising wages bringing an end to labour arbitrage.

• Increasing focus on workplace safety.

The Changing Nature of Manufacturing & Work

Today’s Digital Generation doesn’t do “4D” Jobs!

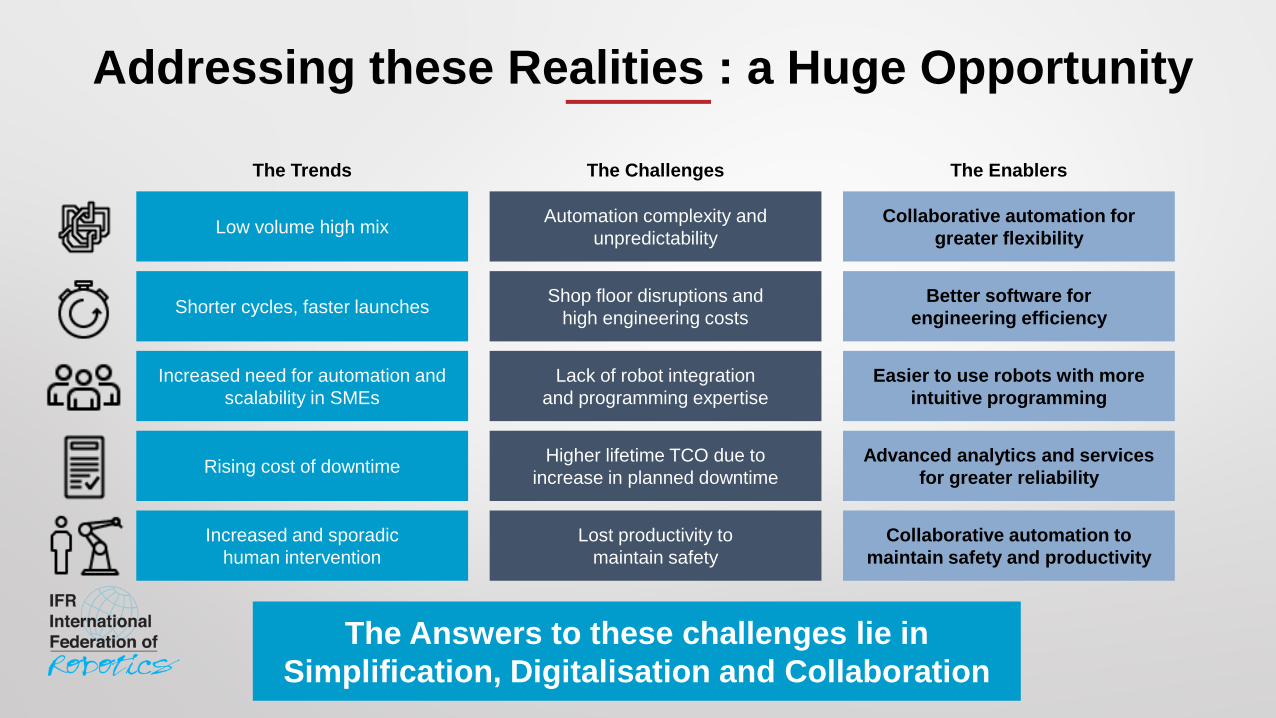

Addressing these Realities : a Huge Opportunity

Low volume high mix

Shorter cycles, faster launches

Increased need for automation and scalability in SMEs

Rising cost of downtime

Automation complexity and unpredictability

Shop floor disruptions and high engineering costs

Lack of robot integration and programming expertise

Higher lifetime TCO due to increase in planned downtime

The Trends The Challenges

Increased and sporadichuman intervention

Lost productivity to maintain safety

Collaborative automation for greater flexibility

Better software for engineering efficiency

Easier to use robots with more intuitive programming

Advanced analytics and services for greater reliability

The Enablers

Collaborative automation to maintain safety and productivity

The Answers to these challenges lie in Simplification, Digitalisation and Collaboration

• Robots which are easier to install, program and operate will unlock entry barriers to the large, untapped market of small and medium enterprises (SMEs).

• Trend towards having production closer to the end consumer driving the importance of standardisation & consistency across global brands.

Simplification

Simplification critical to SMEs, but also important for large Global Manufacturers

• Industry 4.0, linking the real-life factory with a virtual one, will play an increasingly important role in global manufacturing.

• Vision and sensing devices, coupled with analytics platforms, will pave the way for new industry business models.

• Machine Learning will drive many robotics developments over the coming years.

Digitalisation

Big Data allowing People to make better Decisions about Factory Operations

• Collaborative robots are shifting the traditional limits of “what can be automated?”

• Collaborative robots increase manufacturing flexibility as ‘low volume high mix’ becomes the new normal

• Collaboration is also about productivity with increased human/robot interaction

Collaboration

Collaboration means different Things to Different People, but is changing the Face of Manufacturing

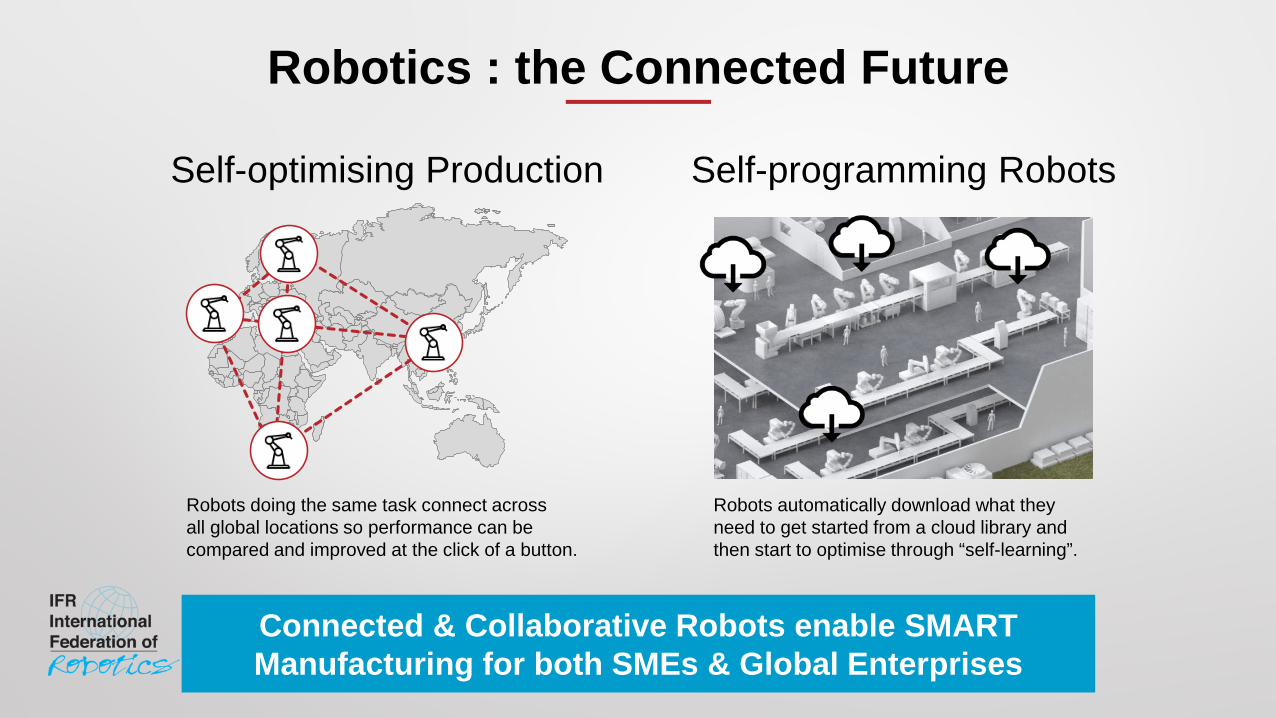

Self-programming Robots

Robotics : the Connected Future

Self-optimising Production

Robots doing the same task connect across all global locations so performance can be compared and improved at the click of a button.

Robots automatically download what they need to get started from a cloud library and then start to optimise through “self-learning”.

Connected & Collaborative Robots enable SMART Manufacturing for both SMEs & Global Enterprises

Thank you!

Contact:Gudrun LitzenbergerInternational Federation of Robotics IFRc/o VDMA Robotics+Automation60528 Frankfurt Main, GermanyEmail: [email protected]: +49 69 6603 1502Internet: https://ifr.org/