how to fill in your tax return 2021

TRANSCRIPT

SA150 Notes 2020-21 Page TRG 1 HMRC 12/20

These notes will help you to fill in your paper tax return. Alternatively, why not complete it online? Because:•it’squick,easyandsecure•you’llhaveanextra3monthstosendittous•youdonothavetocompleteitallatonce–youcansaveyourdetailsandfinishitlaterifyouwant

A For more information about Self Assessment Online, go to www.gov.uk/self-assessment-tax-returns

Ifyouhavenotcompletedataxreturnonlinebefore, go to www.gov.uk/log-in-file-self-assessment-tax-returnWhenyou’vesignedup,we’llpostyouanActivationCode.Thiscan take10workingdaystoarrive(orupto21daysifyou’resettingupyouraccountfromabroad)soplease register in plenty of time.

A If you do not think you need to complete a tax return for this year, go to www.gov.uk/check-if-you-need-a-tax-return

A If you do not need to fill in a return, you must contact us by 31 January 2022 to avoid paying penalties.

ContentsWhatmakesupyourtaxreturn TRG2

Startingyourtaxreturn TRG4

Income TRG5

Taxreliefs TRG9

StudentLoanandPostgraduateLoan repayments TRG11

HighIncomeChildBenefitCharge TRG12

Incorrectlyclaimedcoronavirussupport schemepayments TRG12

MarriageAllowance TRG13

Finishingyourtaxreturn TRG13

Signingyourformandsendingitback TRG15

Aroughguidetoyourtaxbill TRG16

Tax return deadlines and penaltiesIf you:•wanttofillinapapertaxreturn,youmustsend

it to us by 31October2021 (or3monthsafterthedateonyournoticetocompleteataxreturnifthat’slater)•decidetofillinyourtaxreturnonlineoryoumissthepaperdeadline,youmustsenditonlineby 31January2022(or3monthsafterthedateonyournoticetocompleteataxreturnifthat’slater)–ifyouwantustouseyourtaxcodeto collect any tax you owe through your wages or pension, you must file online by 30December2021

Thedeadlineforpayingyourtaxbill,orany Class2NationalInsurance,is31January2022.

Ifwedonotreceiveyourtaxreturnbythedeadlines,you’llhavetopaya£100penalty–evenifyoudonotoweanytax.We’llchargeyoufurther penalties if your return is more than 3,6and12monthslate.

A For more information about penalties, go to www.gov.uk/self-assessment-tax-returns/penalties

Before you startYoumayneedthefollowingdocumentstohelpyou fill in the tax return:•yourformsP60,‘EndofYearCertificate’, P11D,‘Expensesorbenefits’orP45,‘Detailsofemployeeleavingwork’,payslipsoryourP2,‘PAYE CodingNotice’•ifyouworkforyourself,yourprofitorlossaccountoryourbusinessrecords•yourbankstatements,buildingsocietypassbooks,dividendcounterfoilsor investmentbrokers’schedules•personalpensioncontributionscertificates

Donotsendanyreceipts,accountsorotherpaperworkorcorrespondencewithyourtaxreturn,unlessweaskforthem.Ifyoudo,itwilltakelongertodealwithyourtaxreturnandwilldelayanyrepayment.

Use these notes to help you fill in your tax return

Tax Return notesTax year 6 April 2020 to 5 April 2021 (2020–21)

Page TRG 2

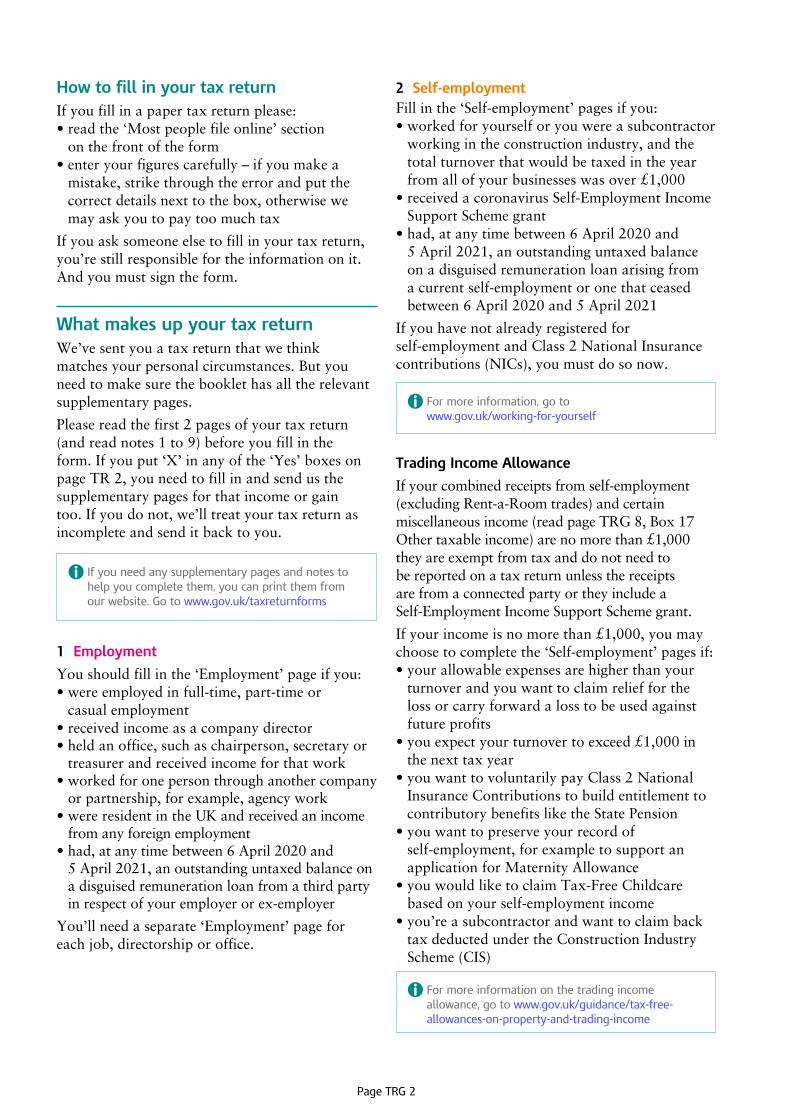

How to fill in your tax returnIf you fill in a paper tax return please: •readthe‘Mostpeoplefileonline’section

on the front of the form•enteryourfigurescarefully–ifyoumakeamistake,strikethroughtheerrorandputthecorrectdetailsnexttothebox,otherwisewemayaskyoutopaytoomuchtax

Ifyouasksomeoneelsetofillinyourtaxreturn,you’restillresponsiblefortheinformationonit.Andyou must sign the form.

What makes up your tax returnWe’vesentyouataxreturnthatwethinkmatches your personal circumstances. But you needtomakesurethebooklethasalltherelevantsupplementary pages.

Pleasereadthefirst2pagesofyourtaxreturn(andreadnotes1to9) before you fill in the form.Ifyouput‘X’inanyofthe‘Yes’boxesonpageTR2,youneedtofillinandsendusthesupplementary pages for that income or gain too.Ifyoudonot,we’lltreatyourtaxreturnasincompleteandsenditbacktoyou.

A If you need any supplementary pages and notes to help you complete them, you can print them from our website. Go to www.gov.uk/taxreturnforms

1 Employment

Youshouldfillinthe‘Employment’ page if you:•wereemployedinfull-time,part-timeor

casual employment•receivedincomeasacompanydirector•heldanoffice,suchaschairperson,secretaryortreasurerandreceivedincomeforthatwork•workedforonepersonthroughanothercompanyorpartnership,forexample,agencywork•wereresidentintheUKandreceivedanincome

from any foreign employment•had,atanytimebetween6April2020and 5April2021,anoutstandinguntaxedbalanceonadisguisedremunerationloanfromathirdpartyinrespectofyouremployerorex-employer

You’llneedaseparate‘Employment’ page for eachjob,directorshiporoffice.

2 Self-employmentFillinthe‘Self-employment’pagesifyou:•workedforyourselforyouwereasubcontractorworkingintheconstructionindustry,andthetotalturnoverthatwouldbetaxedintheyearfromallofyourbusinesseswasover£1,000•receivedacoronavirusSelf-EmploymentIncome Support Scheme grant•had,atanytimebetween6April2020and 5April2021,anoutstandinguntaxedbalanceonadisguisedremunerationloanarisingfromacurrentself-employmentoronethatceasedbetween6April2020and5April2021

Ifyouhavenotalreadyregisteredforself-employmentandClass2NationalInsurancecontributions(NICs),youmustdosonow.

A For more information, go to www.gov.uk/working-for-yourself

Trading Income Allowance

Ifyourcombinedreceiptsfromself-employment(excludingRent-a-Roomtrades)andcertainmiscellaneousincome(readpageTRG8,Box17Othertaxableincome)arenomorethan£1,000theyareexemptfromtaxanddonotneedtobereportedonataxreturnunlessthereceiptsarefromaconnectedpartyortheyincludeaSelf-EmploymentIncomeSupportSchemegrant.

Ifyourincomeisnomorethan£1,000,youmaychoosetocompletethe‘Self-employment’pagesif:• your allowable expenses are higher than your turnoverandyouwanttoclaimreliefforthelossorcarryforwardalosstobeusedagainstfuture profits•youexpectyourturnovertoexceed£1,000in

the next tax year •youwanttovoluntarilypayClass2NationalInsuranceContributionstobuildentitlementtocontributorybenefitsliketheStatePension•youwanttopreserveyourrecordofself-employment,forexampletosupportanapplication for Maternity Allowance•youwouldliketoclaimTax-FreeChildcarebasedonyourself-employmentincome•you’reasubcontractorandwanttoclaimbacktaxdeductedundertheConstructionIndustryScheme(CIS)

A For more information on the trading income allowance, go to www.gov.uk/guidance/tax-free-allowances-on-property-and-trading-income

Page TRG 3

Thereare2typesof‘Self-employment’ pages. If your business is:•straightforwardandyourannualturnoverwaslessthan£85,000,andyoudonothaveanoutstandinguntaxedbalanceonadisguisedremunerationloan,usethe‘Self-employment’ short pages•morecomplex,oryourannualturnoverwas£85,000ormore,oryouneedtoadjustyourprofits,oryouhaveanoutstandinguntaxedbalanceonadisguisedremunerationloan,usethe‘Self-employment’fullpages

You’llneedseparate‘Self-employment’ pages for each business.

Ifyouworkedwithsomeoneelseinpartnership,usethe‘Partnership’pages.

3 PartnershipThereare2typesof‘Partnership’pages–shortonesandfullones.Eachpartnermustfillintheirown‘Partnership’pages,andonepartnerwillhavetocompletetheSA800,‘PartnershipTaxReturn’.

4 UK propertyFillinthe‘UKproperty’pagesifyoureceivedincome from:•anyUKpropertyrentalincludingrentsfromlandyouownorleaseout•furnishedholidaylettingfrompropertiesin theUKorEuropeanEconomicArea(EEA)•lettingfurnishedroomsinyourownhome(butifyouprovidedmealsandotherservices,you’llneedtofillinthe‘Self-employment’pages)ofover£1,000(includinganyincomefromaforeignpropertybusinessreportedinthe‘Foreign’pages).

Property Income Allowance

Ifyourtotalpropertyincome(excludingincomeeligibleforRent-a-Roomrelief)isnotmorethan£1,000itisexemptfromtaxanddoesnotneedtobereportedonataxreturnunlesstheincomeisfromaconnectedparty.

Ifyourincomeisnomorethan£1,000,youmaychoosetocompletethe‘UKproperty’pagesif:•yourallowableexpensesarehigherthanyourpropertyincomeandyouwanttoclaimreliefforthelossorcarryforwardalosstobeusedagainst future profits•you’reanon-residentlandlordandyouwanttoclaimbacktaxpaid(inbox21),underthenon-residentlandlordscheme

IfyouclaimtheRent-a-Roomrelief,youcannotalso claim the property income allowance on Rent-a-Roomincome.

A For more information on the property income allowance, go to www.gov.uk/guidance/tax-free-allowances-on-property-and-trading-income

5 ForeignUsethe‘Foreign’pagesifyoureceived:•interest(over£2,000)andincomefrom overseassavings–ifyouronlyforeignincomewasuntaxedforeigninterestupto£2,000, youcanputthisamountinbox3onpage TR3ofyourtaxreturninsteadofcompletingthe‘Foreignpage’(seepageTRG5)•dividends(over£2,000)fromforeigncompanies•distributionsandexcess‘reportedincome’fromreportingoffshorefunds–thisistaxableincomeaccumulatinginanoffshorefundthatyou havenotyetreceived•overseaspensions(includingtaxablelumpsumsfromoverseasschemestreatedaspensionincome),socialsecuritybenefitsandroyalties•incomefromlandandpropertyabroad (notfurnishedholidaylettingsintheEuropeanEconomicArea,thesegointhe‘UKproperty’pages)over£1,000–ifyourtotalincomefromUKandforeignpropertywas£1,000orless,thismaybeexemptedbythePropertyIncomeAllowance,see‘4UKproperty’orgoto www.gov.uk/guidance/tax-free-allowances-on-property-and-trading-income for more information•discretionaryincomefromnon-residenttrusts•incomeorbenefitsfromapersonabroador anon-residentcompanyortrust(including aUKtrustthathaseitherbeen,orhasreceived,incomefrom,anon-residenttrust)•gainsonforeignlifeinsurancepoliciesorondisposalsinoffshorefunds

Youshouldalsofillinthe‘Foreign’ pages if you wanttoclaimForeignTaxCreditReliefor SpecialWithholdingTaxonincomeyoureport on other pages.

6 Trusts etcFillinthe‘Trusts etc’ pages if you were:•abeneficiaryofatrust(nota‘bare’trust)or

settlement •thesettlorofatrustorsettlementwhoseincomeisdeemedtobeyours

Ifyoureceivedincomefromtheestateofapersonwhohasdied,donotfillinthe‘Trusts etc’ pages if:•youwereentitledtoafixedsumofmoneyor

a specific asset•yourlegacywaspaidwithinterest(puttheinterestinbox1orbox2onpageTR3ofyour taxreturn)

Page TRG 4

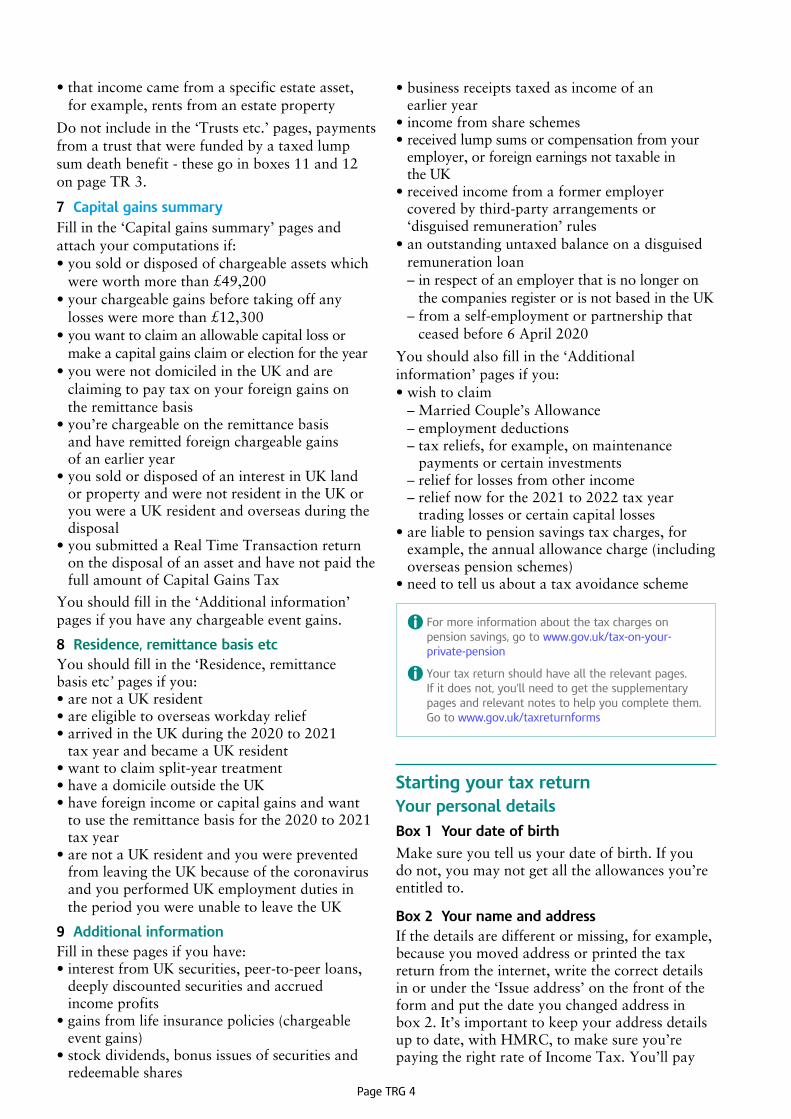

•businessreceiptstaxedasincomeofan earlier year•incomefromshareschemes•receivedlumpsumsorcompensationfromyour

employer, or foreign earnings not taxable in theUK•receivedincomefromaformeremployer coveredbythird-partyarrangementsor‘disguisedremuneration’rules•anoutstandinguntaxedbalanceonadisguised

remuneration loan –inrespectofanemployerthatisnolongeronthecompaniesregisterorisnotbasedintheUK

–fromaself-employmentorpartnershipthatceasedbefore6April2020

Youshouldalsofillinthe‘Additionalinformation’ pages if you: •wishtoclaim –MarriedCouple’sAllowance –employmentdeductions –taxreliefs,forexample,onmaintenance

payments or certain investments –reliefforlossesfromotherincome –reliefnowforthe2021to2022taxyeartradinglossesorcertaincapitallosses

•areliabletopensionsavingstaxcharges,forexample,theannualallowancecharge(includingoverseaspensionschemes)•needtotellusaboutataxavoidancescheme

A For more information about the tax charges on pension savings, go to www.gov.uk/tax-on-your-private-pension

A Your tax return should have all the relevant pages. If it does not, you’ll need to get the supplementary pages and relevant notes to help you complete them. Go to www.gov.uk/taxreturnforms

Starting your tax returnYour personal detailsBox 1 Your date of birth

Makesureyoutellusyourdateofbirth.Ifyoudonot,youmaynotgetalltheallowancesyou’reentitledto.

Box 2 Your name and addressIfthedetailsaredifferentormissing,forexample,becauseyoumovedaddressorprintedthetaxreturnfromtheinternet,writethecorrectdetailsinorunderthe‘Issueaddress’onthefrontoftheformandputthedateyouchangedaddressin box2.It’simportanttokeepyouraddressdetailsuptodate,withHMRC,tomakesureyou’repayingtherightrateofIncomeTax.You’llpay

•thatincomecamefromaspecificestateasset, for example, rents from an estate property

Donotincludeinthe‘Trustsetc.’pages,paymentsfromatrustthatwerefundedbyataxedlumpsumdeathbenefit-thesegoinboxes11and12onpageTR3.

7 Capital gains summaryFillinthe‘Capitalgainssummary’pagesandattach your computations if:•yousoldordisposedofchargeableassetswhichwereworthmorethan£49,200•yourchargeablegainsbeforetakingoffanylossesweremorethan£12,300•youwanttoclaimanallowablecapitallossormakeacapitalgainsclaimorelectionfortheyear•youwerenotdomiciledintheUKandare

claiming to pay tax on your foreign gains on the remittance basis•you’rechargeableontheremittancebasis andhaveremittedforeignchargeablegains of an earlier year•yousoldordisposedofaninterestinUKlandorpropertyandwerenotresidentintheUKoryouwereaUKresidentandoverseasduringthedisposal•yousubmittedaRealTimeTransactionreturnonthedisposalofanassetandhavenotpaidthefullamountofCapitalGainsTax

Youshouldfillinthe‘Additionalinformation’ pages if you have any chargeable event gains.

8 Residence, remittance basis etcYoushouldfillinthe‘Residence,remittancebasis etc’ pages if you:•arenotaUKresident•areeligibletooverseasworkdayrelief•arrivedintheUKduringthe2020to2021 taxyearandbecameaUKresident•wanttoclaimsplit-yeartreatment•haveadomicileoutsidetheUK•haveforeignincomeorcapitalgainsandwant

to use the remittance basis for the 2020 to 2021 tax year•arenotaUKresidentandyouwereprevented fromleavingtheUKbecauseofthecoronavirus andyouperformedUKemploymentdutiesin theperiodyouwereunabletoleavetheUK

9 Additional informationFill in these pages if you have:•interestfromUKsecurities,peer-to-peerloans,deeplydiscountedsecuritiesandaccrued income profits•gainsfromlifeinsurancepolicies(chargeableeventgains)•stockdividends,bonusissuesofsecuritiesandredeemableshares

Page TRG 5

Ifyourbankorbuildingsocietypaysyouanalternative finance return or profit share return insteadofinterest,puttheamountinbox1ifit istaxed,orbox2ifitisnot.

UK interestIncludeinbox1or2anyinterestfrom:•bankandbuildingsocietysavings,including

internet accounts •UKauthorisedunittrusts,open-endedinvestmentcompaniesandinvestmenttrusts–thesearepaidwithouttaxdeducted–includethefullamountofthesedistributionsinbox2•NationalSavingsandInvestmentsaccountsandsavingsbonds•taxableinterestreceivedoncompensation

payments, for example, payment protection insurance(PPI)•certificatesoftaxdeposit•creditunionsandfriendlysocieties

DonotincludeinterestfromUKgovernmentsecurities(gilts),orinterestfrombonds,loannotesorsecuritiesissuedbyUKcompanies.Thesego inthe‘Additionalinformation’ pages.

Box 1 Taxed UK interest – the net amount after tax has been taken off

Copythenetinterestdetailsfromyourstatementsor electronic vouchers. If you have more than one account,addupallyournetinterestandputthetotal in box 1.

Includeanynetincome(aftertaxhasbeen takenoff)fromapurchasedlifeannuity. Usethedetailsonyourpaymentcertificateandonly put the income part of the payment in box 1. Donotinclude the rest of the payment.

Ifyoureceivedcashorsharesfollowingthetakeoverormergerofbuildingsocieties,youmayhavetopaytaxontheincome.Ifyoudo,includeitinbox1.Ifyou’renotsure,puttheamountinbox17andgiveusdetailsin‘Anyotherinformation’onpageTR7.

Box 2 Untaxed UK interest – amounts which have not had tax taken off

If you have an account that pays you gross interest (for example, abankorbuildingsocietyaccount),put the gross amount in box 2.

Box 3 Untaxed foreign interest (up to £2,000)Ifyouronlyforeignincomewasuntaxedforeigninterest(ofupto£2,000),puttheamount(inUKpounds)inbox3insteadoffillinginthe ‘Foreign’pages.

the appropriate rate of income tax for the year dependingonwhetheryoulivedinScotland,WalesortherestoftheUKforthemajorityofthetax year.

A For information about income tax rates in Scotland and the rest of the UK, go to www.gov.uk/income-tax-rates

A For information about income tax rates in Wales, go to www.gov.uk/welsh-income-tax

Box 4 Your National Insurance numberIfyourNationalInsurancenumberisnotatthetop of your tax return, it will be on:•apayslip,P45oryourP60fortheyear•aP2,‘PAYECodingNotice’•anyletterfromusortheDepartmentforWorkandPensions

Example of a National Insurance number

IncomeInterest and dividends from UK banks and building societiesThisincludes:•anyinterestyoureceiveonbank,buildingsocietyandothersavingsaccounts•dividendsandotherqualifyingdistributionsfromUKcompaniesandUKauthorisedunittrustsoropen-endedinvestmentcompanies•incomefrompurchasedlifeannuities•interestyoureceiveinnon-cashform

DonotincludeanyinterestfromIndividualSavingsAccount(ISAs),UlsterSavingsCertificates,SaveAsYouEarnschemesoraspartofanawardbyaUKcourtfordamages.

Weusuallytreatincomefrominvestmentsheldinjointnamesasallreceivinganequalshare.However,ifyouholdunequalshares,youcanelecttoreceivetheincomeandpaytaxonthoseproportions. Onlyputyourshareofanyjointincome on the tax return.

If a nominee receives investment income on your behalf,orifyou’reabeneficiaryofabaretrust,fillinboxes1to5onpageTR3(notthe‘Trusts etc’pages).

Ifyoumakegiftstoanyofyourchildrenwhoareunder18thatproducesmorethan£100income(beforetax),youneedtoincludethewholeamountof the income in your tax return.

Page TRG 6

Ifyourtotaldividendincome(includingUKandforeigndividends)isover£2,000andyouwanttoclaimForeignTaxCreditRelief,donotincludetheforeigndividendinthisbox.Completethe‘Foreign’pagesinstead.

UK pensions, annuities and other state benefits receivedNotallbenefitsaretaxable.Donotincludethefollowinginboxes8to13:•AttendanceAllowance,lumpsumBereavementSupportPaymentorPersonalIndependencePayments•StatePensionCredit,WorkingTaxCredit, ChildTaxCreditorUniversalCredit•additionstoStatePensionsorbenefitsfordependentchildren•income-relatedEmploymentandSupportAllowance,Jobfinder’sGrantorEmploymentZone payments•MaternityAllowance•WarWidow’sPensionandsomepensionspaid tootherforcesdependantsifthedeathinservicewasbefore6April2005•pensionsandotherpaymentsfordisability,injuryorillnessduetomilitaryservice•somebeneficiaries’pensionswherethememberdiedbeforeage75•overseaspensions–thesegoonthe‘Foreign’ pages

A For more about what is and what is not taxable income, go to www.gov.uk/income-tax

A For more about tax on beneficiaries’ pensions, go to www.gov.uk/tax-on-pension-death-benefits and for war widow(er) pensions, go to www.gov.uk/war-widow-pension

Box 8 State PensionUsetheletter‘Aboutthegeneralincreaseinbenefits’thatthePensionServicesentyoutofindyourweeklyStatePensionamount.

Adduptheamountyouwereentitledtoreceivefrom6April2020to5April2021andputthetotalinbox8.DonotincludeanyamountyoureceivedforAttendanceAllowance.

IfyourStatePensionchangedduringtheyearoryouonlyreceiveditforpartoftheyear,multiplyeachamountbythenumberofweeksthatyouwereentitledtoreceiveit.Addupyour amounts carefully.

IfyoudonothavetheletterfromthePensionService,phonethemon08007310469 (textphone08007310464)andaskthemfor the information.

You must put the name of the country where the interestarosein‘Anyotherinformation’on pageTR7.

Ifitwasmorethan£2,000,you’llneedtofillinthe‘Foreign’pages.

UK dividendsYoudonotpaytaxonthefirst£2,000ofdividendincomeyoureceive(thedividendallowance).Youpaytaxondividendsabovethedividendallowanceatthefollowingrates: •7.5%ondividendincomewithinthebasic rateband•32.5%ondividendincomewithinthehigher rateband•38.1%ondividendincomewithintheadditionalratebandIncludeallofyourdividendincome,evenifit’slessthan£2,000,asitwillcounttowardsyourbasicorhigherratebandsandmayaffecttherateoftaxthatyoupayondividendsreceivedinexcessofthe£2,000allowance.

A For more information, go to www.gov.uk/tax-on-dividends

Box 4 Dividends from UK companies – the amount receivedYourdividendvoucherwillshowyourshares inthecompany,thedividendrateanddividendpayable.Putthetotaldividendpaymentsinbox4.

Includeanydividendsfromemployeeshareschemes. Donotinclude:•PropertyIncomeDistributionsfromRealEstateInvestmentTrusts(REITs)orPropertyAuthorisedInvestmentFunds(PAIFs)–thesegoinbox17,andthetaxtakenoffinbox19•stockdividendsornon-qualifyingdividends–thesegointhe‘Additionalinformation’ pages

Box 5 Other dividends – the amounts receivedThisincludesdividenddistributionsfromauthorisedunittrusts,open-endedinvestmentcompanies,andinvestmenttrusts.Puttheamountonyourdividendvoucherinbox5.

Includeinbox5anydividendfromaccumulationunitsorsharesthatareautomaticallyreinvested.Donotincludeany‘equalisation’amounts.

Box 6 Foreign dividends (up to £2,000)Ifyouronlyforeignincomewasdividendsupto£2,000,putthenetamount(inUKpounds)in box6.Puttheforeigntaxtakenoffinbox7.

Page TRG 7

dateofdeathofthememberwhohasdied,fromyourR185(PensionLSDB)certificate–putthegrossamountandtaxpaidfiguresfromyourcertificateinboxes11and12

10% deductionIfyoureceiveaUKpensionforformerservicetoanoverseasgovernment,only90%ofthebasicpensionistaxableintheUK.Take10%offthevalue of the pension before you put the amount in box 10.

The territories are:•anycountryformingpartofHerMajesty’sdominions•anyCommonwealthcountry(excludingtheUK)•anyterritoryunderHerMajesty’sprotection

A For more about tax on pensions, go to www.gov.uk/tax-on-pension

For help about payments from the Financial Assistance Scheme covering several years, look under ‘key information’ at www.pensionprotectionfund.org.uk/FAS

Box 12 Tax taken off box 11UsetheP60orcertificateyourpensionpayer gaveyou,andputthetotalamountoftaxtakenoff all your pensions in box 12.

SA100 2016 Page TR 1

Income

Interest and dividends from UK banks, building societies etc

1 Taxed UK interest etc – the net amount after tax has been taken off - read the notes

£ 0 0•

2 Untaxed UK interest etc – amounts which have not had tax taken off - read the notes

£ 0 0•

3 Untaxed foreign interest (up to £2,000) – amounts which have not had tax taken off - read the notes

£ 0 0•

4 Dividends from UK companies – the net amount, do not include the tax credit - read the notes

£ 0 0•

5 Other dividends – the net amount, do not include the tax credit - read the notes

£ 0 0•

6 Foreign dividends (up to £300) – the amount in sterling after foreign tax was taken off. Do not include this amount in the ‘Foreign’ pages

£ 0 0•

7 Tax taken off foreign dividends – the sterling equivalent

£ 0 0•

UK pensions, annuities and other state benefits received

8 State Pension – amount you were entitled to receive in the year, not the weekly or 4-weekly amount - read the notes

£ 0 0•

9 State Pension lump sum – the gross amount of any lump sum - read the notes

£ 0 0•

10 Tax taken off box 9

£ 0 0•

11 Pensions (other than State Pension), retirement annuities and taxable triviality payments – the gross amount. Tax taken off goes in box 12

£ 0 0•

12 Tax taken off box 11

£ 6 4 0 0 0•

13 Taxable Incapacity Benefit and contribution-based Employment and Support Allowance - read the notes

£ 0 0•

14 Tax taken off Incapacity Benefit in box 13

£ 0 0•

15 Jobseeker’s Allowance

£ 0 0•

16 Total of any other taxable State Pensions and benefits

£ 0 0•

Other UK income not included on supplementary pagesDo not use this section for income that should be returned on supplementary pages. Share schemes, gilts, stock dividends, life insurance gains and certain other kinds of income go on the ‘Additional information’ pages.

17 Other taxable income – before expenses and tax taken off

£ 0 0•

18 Total amount of allowable expenses – read the notes

£ 0 0•

19 Any tax taken off box 17

£ 0 0•

20 Benefit from pre-owned assets - read the notes

£ 0 0•

21 Description of income in boxes 17 and 20 – if there is not enough space here please give details in the‘Any other information’ box, box 19, on page TR 7

Example of tax return, box 12

IfyourP60showsthatyoureceivedarefund, itwillhavean‘R’nexttoit.Putaminussign intheshadedboxinfrontofthefigure.

Box 13 Taxable Incapacity Benefit and contribution-based Employment and Support Allowance (ESA)NotallIncapacityBenefitistaxable.Itisnottaxableinthefirst28weeksofincapacityorifyourincapacitybeganbefore13April1995andyou have been getting it for the same illness ever since.

Allcontribution-basedEmploymentandSupportAllowanceandESATimeLimitedSupplementaryPayment(paidNorthernIrelandonly)istaxable.

UsetheP60(IB),P45(IB),P60(U)orP45(U)thattheDepartmentforWorkandPensions(DWP)gaveyou.Putthetotaltaxableamountofyourbenefitorallowanceinbox13andanytaxtakenoffyourpaymentsinbox14.

IfyoureceivedalumpsumbecauseyoudeferredyourStatePensionfromanearlieryear,puttheamountinbox9,notinbox8.

DonotincludeStatePensionCredit,theChristmasbonus,WinterFuelPaymentoranyadditionfor adependentchild.

Boxes 9 and 10 State Pension lump sumOnlyfillinbox9ifyoudeferredyour StatePensionforatleast12monthsandchose toreceiveitasaone-offlumpsuminthe 2020to2021taxyear.Putthegrossamount(beforetaxtakenoff)inbox9andthetaxtakenoff in box 10. Donotinclude any lump sum amountinbox8.

Box 11 Pensions (other than State Pension), retirement annuities and taxable lump sums treated as pensionsYourpensionpayerwillgiveyouaP60,‘EndofYearCertificate’orsimilarstatement.AddupyourtotalUKretirementannuitiesandpensions (nottheStatePension),andputthetotalgrossamount(beforetaxtakenoff)inbox11.

Thisincludestaxablepensions:•fromyour,oryourdeceasedfamilymember’s

employer•frompersonalpensionplansandstakeholder

pension plans•paidasdrawdownpensionsfromaregistered

pension scheme•fromAdditionalVoluntaryContributionsschemes•forinjuriesatworkorforwork-relatedillnesses•fromserviceintheArmedForces•fromretirementannuitycontractsortrustschemes•fromtheFinancialAssistanceScheme•paidafterage75asaseriousill-healthlumpsumorlumpsumdeathbenefit

Italsoincludesthetaxablepartofany:•lumpsumsyoureceivedinsteadofasmallpension (‘trivialcommutationlumpsum’)•‘uncrystallisedfundspensionlumpsum’youwithdrewunderpensionflexibility

Donotincludenon-taxablepensiondeathbenefitsyou’refirstentitledtofrom6April2015.

Pleasegiveusthefollowingdetailsin‘Anyotherinformation’onpageTR7:•detailsofyourpensionorannuitypayerand

your reference number •yourPAYEreference•thepaymentbeforetaxandtheamountoftaxtakenoff•ifyoureceivedataxablelumpsumdeathbenefitthroughatrust,thename,dateofbirthand

Page TRG 8

–paymentsafterage75asaseriousill-healthlumpsumorauthorisedlumpsumdeathbenefit

Ifyou’reunsureifanyincomeistaxable,pleasecontact the payer of the income to confirm how it shouldbetreatedbeforecompletingthisbox.

Receiptsfromself-employment(readpageTRG2ofthesenotes)andcertainmiscellaneousincomeof£1,000orlessareexemptfromtaxanddonotneedtobereportedonataxreturn.Ifthetotalreceiptsfrombotharemorethan£1,000,the‘Self-employment’pagesmustbecompletedtoreporttheself-employmentincomeandthemiscellaneousincomemustbereportedinbox17.

Donotincludeanyincomefromyouremployment,self-employmentorcapitalgains,oranymiscellaneousincomeexemptedbythetradingincomeallowance.Ifyou’vealreadyclaimedpartorallofyour£1,000tradingincomeallowanceagainstself-employmentincome,thenit’stheunusedamount,ifany,thatisexempthereandyoushouldstillshowanymiscellaneousincomeexceedingthatamountinBox17.

ExampleTony has self-employed income of £500 and miscellaneous income of £800.

As this income is over £1,000 it has to be reported in his tax return.

Tony puts £500 in box 9 (Turnover) and £500 in box 10.1 (Trading income allowance) of his Self-employment (short) pages.

Amount of allowance remaining = £500

Tony puts £300 in box 17 (£800 minus £500 (remaining amount of trading income allowance)).

Makesureyoutelluswhatthisincomeisinbox21.

A For more information on the trading income allowance and miscellaneous income that attracts the allowance, go to www.gov.uk/guidance/tax-free-allowances-on-property-and-trading-income

For more information on other income, go to www.gov.uk and search for ‘HS325’.

Box 18 Total amount of allowable expensesThisincludesanyexpensesthat:•youhadtospendsolelytoearntheincome•werenotforprivateorpersonaluse•werenotcapitalitems,suchasacomputer

Ifyouuseyour£1,000tradingincomeallowance against your miscellaneous income orself-employmentincomedonotincludeanyamountsyouhadtospendtoearnthismiscellaneousincomeinbox18.

Box 15 Jobseeker’s AllowanceUsetheP60(IB),P45(IB),P60(U)orP45(U)thatDWPgaveyouandputthetotalamountofJobseeker’sAllowanceinbox15.

Ifyoustoppedclaimingbefore5April2021, you’llfindthetotalamountonyourP45(U).

Box 16 Total of any other taxable State Pensions and benefitsIfyouhadanyofthefollowing,addupyourpaymentsandputthetotalinbox16.•BereavementAllowanceorWidow’sPension•WidowedParent’sAllowanceorWidowedMother’sAllowance•IndustrialDeathBenefit•Carer’sAllowanceorCarer’sAllowanceSupplementaryPayment(wherereceivedtoreplaceCarer’sAllowance-paidNorthernIrelandonly)•Carer’sAllowanceSupplement(wherereceivedasanextrapaymentforpeopleinScotlandwhogetCarer’sAllowance)•StatutorySickPayorStatutoryMaternity,PaternityorAdoptionPayandSharedParentalPaybutonlyifpaidbyHMRevenueandCustoms(notyouremployer)

DonotincludetheChristmasBonusandWinterFuelPayment,oranyColdWeatherPayments.

Other UK income not included on supplementary pages

Box 17 Other taxable incomeThisincludes:•miscellaneousincome–forexample,fromcasual earnings, commission or freelance income (not exemptedbythetradingincomeallowance)•taxablecoronavirussupportpayments(ifnot reportedelsewhereinthistaxreturn)•businessreceiptswhereyourbusinesshasceased•PropertyIncomeDistributions(PIDs)from RealEstateInvestmentTrusts(REITs)andPropertyAuthorisedInvestmentFunds(PAIFs)•paymentsfromapersonalinsurancepolicy forsicknessordisabilitybenefits•incomefromunauthorisedunittrusts•taxableannualpayments•profitsfromcertificatesofdeposit•non-cashbenefitsyoureceivedforbeing a former employee•thefollowingauthorisedpaymentsfrom an overseas pension scheme: –thetaxablepartofan‘uncrystallisedfundspensionlumpsum’,awinding-uplumpsumora trivial commutation lump sum

Page TRG 9

YourPAYEtaxcodemaybeaffectedbyinformation you supply in your tax return if we receiveitbefore31December2021.

If you expect any of the amounts or claims in boxes1,2,5,6or13tochangeduringthe2021to2022taxyear,youmustinformHMRCtoensureweupdateyourcurrentPAYEtaxcode.

A For more information, go towww.gov.uk/tax-codes/updating-tax-code

Paying into registered pension schemes and overseas pension schemesFillinboxes1to3forpaymentstoregisteredpensionschemesandbox4forpaymentstooverseas pension schemes.

You can claim tax relief on your personal contributionstoaregisteredpensionschemeifyoupaidthembeforeyoureachedage75andhave:•beenaUKresidentinthetaxyear•hadtaxableUKearnings,suchasemployment incomeorprofitsfromself-employment•hadUKtaxableearningsfromoverseasCrown employment(oryourspouseorcivilpartnerdid)•beenaUKresidentwhenyoujoinedthepension scheme,andatanytimeinthe5taxyearsbefore 2020 to 2021 tax year

Donotincludeanyamountsfor:•personaltermassurancecontributions•youremployer’sowncontributions•contributionstakenfromyourpaybeforeit wastaxed

A For more information, go to www.gov.uk/pension-types

Limits to reliefThe maximum personal contributions you can claim tax relief on is either: •uptotheamountofyourtaxableUKearningsin the tax year•upto£3,600gross(thatis,£2,880youpaidplus£720taxreliefclaimedbyyourpensionprovider)toa‘reliefatsource’schemeonly

The limits also apply to overseas pension schemes.

If your pension savings are more than theAnnualAllowance,andataxchargeisdue,youmustusethe‘Additionalinformation’pagesandpayataxcharge.

A For more information on the Annual Allowance, go to www.gov.uk and search for ‘HS345’, or go to www.gov.uk/tax-on-your-private-pension

Makeanoteinbox21oftheamountoftradingincomeallowanceclaimedagainstyourmiscellaneous income.

Box 20 Benefit from pre-owned assets

Pre-ownedassets(property)includeslandandbuildingsorchattels,forexample,worksofart,furniture,antiques,carsoryachts,oranyassetsheldinasettlement.

You may have to pay a tax charge on benefits receivedifyoupreviouslyownedorhelpedtobuyassets(pre-ownedassets(POA)).

You may have to pay tax if:•during2020to2021taxyearyou –occupiedlandwithoutpayingafullmarket

rent for it –usedorenjoyedgoodswithoutpayingfullyfor

the benefit –couldbenefitfrompropertyyou’vesettledifincomefromthepropertyistreatedasyours

•andatsometimesince17March1986you –ownedthepropertyyou’renow

benefiting from –ownedandsoldpropertyandusedtheproceedstobuythepropertyyou’renowbenefiting from

–gavesomeoneelseproperty,includingcash, andtheyusedittobuythepropertyyou’renow benefiting from

–settledassetsintothetrustthatyoucan benefit on

Pleasetellusinbox21howyouworkedoutthebenefit or charge that you put in box 20.

Donotincludethebenefitif:•thepropertycouldbeliabletoInheritanceTaxwhenyoudie•thetotalbenefitfortheyearis£5,000orless•youmadethecashgiftbefore6April2013

A For more information about pre-owned assets and help working out your benefit either:• gotowww.gov.uk/government/collections/

hmrc-manuals and read page IHTM44000 in the Inheritance Tax Manual

• phonetheProbateandInheritanceTaxHelpline on 0300 123 1072

Tax reliefsThis section covers tax relief for payments to pensionschemes,charitiesandforBlindPerson’sAllowance. If you wish to claim other reliefs, for example,MarriedCouple’sAllowancewhereoneofthecouplewasbornbefore6April1935,pleaseusethe‘Additionalinformation’ pages.

Page TRG 10

Personal contributions that had tax relief in the scheme

Box 1 Payments to registered pension schemes operating ‘relief at source’Underthe‘reliefatsource’system,yourpensionproviderclaimsbasicratetaxrelief(of20%)onyourpersonalcontributionsandaddsthattoyourpension pot.

Putthetotalamountinbox1–thatis,yourpersonalcontributionspaidtothescheme,plusthebasicratetaxrelief.Includeanyone-offcontributionsyoumadeintheyearandprovidethedetailsofanyone-offcontributionsin‘Anyotherinformation’onpageTR7.

Usethepensioncertificateorreceiptyougetfromtheadministratortofillinbox1orworkoutthefigurebydividingtheamountyouactuallypaid by80andmultiplyingtheresultby100.

ExampleEmma paid £700 into her pension scheme. She puts £875 in box 1 (£700 divided by 80 and multiplied by 100), which is her net payment plus the tax relief of £175 (£875 at 20%).

Ifyoupaytaxatarateabove20%youshouldstillfillinbox1withtheamountyoupaidinplusthebasicrate(20%)taxrelief.We’llworkouttheextrataxreliefduetoyouoverthebasicrateclaimedbyyourpensionprovider.

Personal contributions with full relief still to claim Box 2 Payments to a retirement annuity contractIfyourretirementannuitycontract(RAC)providerdoesnotusethe‘reliefatsource’schemetheydonotclaimthebasicrate(20%)taxreliefonyourbehalf.PutyourtotalpersonalcontributionstotheRACinthe2020to2021taxyearinbox2.

Box 3 Payments to your employer’s scheme which were not deducted from your pay before taxInsomeschemes,anemployertakesyourpersonalcontributions from your pay before they tax what’sleft.Ifyou(orsomeoneelsewhoisnotyouremployer)paidintosuchaschemeandnotax relief was given, you can claim that tax relief now.Putthetotalunrelievedamountyoupaidinthe2020to2021taxyearinbox3.

This may happen if: •youpaidmorecontributionsthanyouearnedin

that job

•youremployercouldnottakeanycontributionsfrom your pay before taxing it, for example if youwerepaidcloseto5April•you’renotanemployeebutareamemberof

a public services pension scheme or a marine pilots’fund

Donotincludeanypersonalcontributionsthathadreliefatsource,suchasagrouppersonalpension scheme.

Box 4 Payments to an overseas pension schemeYoumaygettaxreliefifyou’reeligibleformigrantmemberrelief,transitionalcorrespondingrelieforreliefunderadoubletaxationagreement.Puttheamountthatqualifiesfortaxreliefin box4.

Charitable givingTellusaboutthegiftstocharitiesandCommunityAmateurSportsClubs(CASCs)thatyou’reclaiming relief for.

A For more information about giving to charity, go to www.gov.uk/donating-to-charity

For an A to Z of registered CASCs, go to www.gov.uk/government/publications/community-amateur-sports-clubs-casc-registered-with-hmrc--2

Gift AidGiftAidisataxreliefforgiftsofmoneytocharitiesandCASCs.

If you pay tax at a rate above the basic rate, you’reentitledtoadditionaltaxrelief–thecalculationworksitoutforyou.

Box 5 Gift Aid payments made in the year to 5 April 2021PutthetotalGiftAidpaymentsyoumadefrom6April2020to5April2021inthisbox.DonotincludeanypaymentsunderPayrollGiving.

Box 6 Total of any ‘one-off’ payments in box 5TohelpusgetyourPAYEtaxcoderight,ifyouhaveone,putanyone-offpaymentsyouincludedinbox5inbox6.ThesewillbeGiftAidpaymentsmadefrom6April2020to 5April2021thatyoudonotintendtorepeatintheyearto5April2022.

Box 7 Gift Aid payments made in the year to 5 April 2021 but treated as if made in the year to 5 April 2020Putinbox7anyGiftAidpaymentsthatyoumadebetween6April2020and5April2021,which

Page TRG 11

youwantustotreatasifyoumadetheminthetaxyear6April2019to5April2020.

Box 8 Gift Aid payments made after 5 April 2021 but to be treated as if made in the year to 5 April 2021IfyouwantustotreatGiftAidpaymentsyoumadebetween6April2021andthedateyousendusyourtaxreturn,asifyoumadethemintheyearto5April2021,puttheamountinbox8.Forexample,ifyouknowyou’llnotbepayinghigherratetaxthisyearbutyoudidintheyear to5April2021.

Box 9 Value of qualifying shares or securities gifted to charityYoucanclaimtaxreliefforanyqualifyingsharesandsecuritiesgifted,orsoldatlessthantheirmarketvalue,tocharities.Qualifyingshares andsecuritiesare:•thoselistedonarecognisedstockexchangeordealtinonadesignatedmarketintheUK•unitsinanauthorisedunittrust•sharesinanopen-endedinvestmentcompany•aninterestinanoffshorefund

Putinbox9thenetbenefitofthesharesorsecurities,minusanyamountsorbenefitsreceivedfromthecharity.Addanyincidentalcostsforthetransfer,suchasbrokers’feesorlegalfees.

A For more information about charitable giving, go to www.gov.uk and search for ‘HS342’.

Box 10 Value of qualifying land and buildings gifted to charityYou can claim tax relief for any gift or sale at lessthanmarketvalue,ofa‘qualifyinginterestinland’–thatis,thewholeofyourbeneficialinterestinthatfreeholdorleaseholdlandin theUK.

Putinbox10thenetbenefitoftheland,minusanyamountsorbenefitsreceivedfromthecharity.Addanycostsofthegiftorsale,suchaslegalorvaluer’sfees.

Box 11 Value of qualifying investments gifted to non-UK charities in boxes 9 and 10Youcanclaimreliefforgiftsofqualifyingshares,securities,landorbuildingstocertainnon-UKcharities.Ifanyamountsincludedinbox9or box10aretocharitiesoutsidetheUK,puttheamountinbox11andgiveusdetailsin ‘Anyotherinformation’onpageTR7.

Box 12 Gift Aid payments to non-UK charities in box 5YoucanclaimreliefforGiftAiddonations tocertainnon-UKcharities.Ifanyamountsincludedinbox5aretocharitiesoutsidetheUK,puttheamountinbox12andgiveusdetails in‘Anyotherinformation’onpageTR7.

Blind Person’s Allowance

Box 14 Enter the name of the local authority or other registerIfyouliveinEnglandorWales,thelocalauthoritywill put your name on their register of sight impaired(blind)peoplewhenyoushowthemaneyespecialist’scertificatestatingyou’reblindorseverelysightimpaired.

IfyouliveinScotlandorNorthernIrelandand are not on a register, you can claim the allowance ifyoureyesightissobadyoucannotdoanyworkforwhicheyesightisessential.Write‘Scotland’ or‘NorthernIreland’inbox14.

Ifyouaskedyoureyespecialisttotell HMRCthatyou’resightimpairedwrite‘specialist’inbox14.

Box 15 If you want your spouse’s, or civil partner’s, surplus allowanceOnlyput‘X’inthisbox,ifyourspouseorcivilpartnerhasclaimedBlindPerson’sAllowancebutdoesnothaveenoughtaxableincometouseitall,andyouwanttoclaimthesurplus.

Box 16 If you want your spouse, or civil partner, to have your surplus allowanceOnlyput‘X’intheboxifyouclaimtheallowancebutcannotuseitall,andyouwanttogivethebalance to your spouse or civil partner.

Ifyouput‘X’inbox15orbox16,pleasetellusyourspouse’sorcivilpartner’snameandNationalInsurancenumberin‘Anyotherinformation’onpageTR7.

Student Loan and Postgraduate Loan repaymentsTheStudentLoansCompany(SLC)willwrite totellyouthedatethatyoushouldstartrepayingyourIncomeContingentRepaymentLoan.YoumustfillintheStudentLoanandorPostgraduateLoanboxesfromthisdate.We’llusetheloanandorplantypeheldbySLCtoworkoutanyStudentLoanandorPostgraduateLoanrepayment.

Page TRG 12

A For more detailed information about repaying your Student Loan, go to www.gov.uk/guidance/tell-hmrc-about-a-student-loan-in-your-tax-return and www.gov.uk/repaying-your-student-loan

Boxes 1 to 3Put‘X’inbox1ifyou’vereceivedaletterfromtheSLCnotifyingyouthatrepaymentofanIncomeContingentLoanbeganbefore 6April2021.

Inbox2,putthetotalamountofallStudentLoandeductionstakenfromallPAYEemployments. You’llfindthisinformationonyourP60andpayslips.

Inbox3,putthetotalamountofallPostgraduateLoandeductionstakenfromallPAYEemployments.YouwillfindthisinformationonyourP60andpayslips.

High Income Child Benefit ChargeFillinthissectionifduringthe2020to2021 tax year:•yourindividualincomewasover£50,000•yourincomewashigherthanyourpartner’sincome,andeither –youoryourpartnergotChildBenefit,or –someoneelseclaimedChildBenefitfor achildwholivedwithyou

Box 1PutthetotalamountofChildBenefityouor your partner got for the 2020 to 2021 tax year. Donotincludeanyarrearspaymentsreceivedthatrelate to previous tax years. This is the amount ofChildBenefitforafullweek,whereaMondayfalls within the tax year. For the 2020 to 2021 taxyear,thefirstweekstartsonMonday6April2020andthelastweekstartsonMonday5April2021.Thereare53Mondaysinthe2020to2021tax year. If you got payments for the full year, put thetotalfor53weeksinbox1.

Alsoputinbox1,theamountofChildBenefityou got if you or your partner: •startedtogetChildBenefitonorafter 6April2020–puttheamountfromthedateitstartedto5April2021•stoppedgettingChildBenefitbefore 6April2021–puttheamountreceiveduptothatdate

Box 2PutthetotalnumberofchildrenyouoryourpartnergotChildBenefitforon5April2021.

Box 3IfyouoryourpartnerstoppedgettingallChildBenefitpaymentsbefore6April2021(butafter 5April2020),putthedatethepaymentsstoppedinbox3.IfyouhavetopaytheHighIncomeChildBenefitChargeforthe2021–22taxyearandyoudonotwant us to collect it through your pension or wagesbyadjustingyour2021–22taxcodeduringtheyear,put‘X’inbox3onpageTR6.

A For help working out your Child Benefit payments received, go to www.gov.uk/child-benefit-tax-calculator

For more about the High Income Child Benefit Charge, go to www.gov.uk/child-benefit-tax-charge

Incorrectly claimed coronavirus support scheme paymentsOnlyfillinthissectionifyouincorrectlyclaimedanypaymentsfromtheCoronavirusJobRetentionScheme(CJRS),EatOuttoHelpOutScheme,Self-EmploymentIncomeSupportScheme(SEISS)orfromanyotherapplicableHMRCcoronavirussupportschemeandyouhavenot:•alreadytoldHMRCabouttheseamounts•receivedanassessmentissuedbyanofficerof HMRCfortheseamounts

lfyoureceivedaCJRS,EatOuttoHelpOut,SEISSoranyotherapplicableHMRCcoronavirussupportschemepaymentthatyouwereentitledto,donotincludethemhere.Instead,includetheminthe relevant boxes of the supplementary pages for your business.

IfyouwerenotentitledtosomeorallofthepaymentsreceivedandyouhavenottoldHMRC,wehavetherighttoassessandrecoverthefullamountofanyincorrectlyclaimedpaymentbymakingan‘officer’sassessment’fortheamountthatyouwerenotentitledtoandhavenotrepaid.

Ifwehavealreadycontactedyoutoraiseanassessment,youdonotneedtodeclaretheoverpaidamountsinthissection.

For more information on receiving payments you werenotentitledtoandpenalties,seefactsheetsCC/FS48andCC/FS11.Gotowww.gov.ukandsearchfor‘CC/FS48’and‘CC/FS11’.

Amountsenteredinbox1andbox2willbeaddedtoyourincometaxliability.Thismayaffectwhetherornotyou’rerequiredtomakepaymentsonaccountfor2021–22,ormayincreasetheamount of payment on account you have to pay.

Page TRG 13

Youmaywanttoconsiderclaimingtoreduceyourpaymentsonaccountfor2021–22.

Readthenotesinsection12ofthe‘Taxcalculationsummarynotes’formoredetails.

Box 1 Amount of HMRC coronavirus support scheme payments (other than SEISS) incorrectly claimed

IfanerrorhasbeenmadeinaclaimthathasresultedinyoureceivingtoomuchofanHMRCcoronavirus support scheme payment (other than SEISS),youmustpaythisbacktoHMRC. IfyouhavenotputthatrightalreadybymakingavoluntaryadjustmentorrepaymentthatwasagreedbyHMRC,puttheincorrectlyclaimedamountinbox1.Donotincludeanypaymentsthatyouwereentitledtoorhavealreadyrepaidorbeenassessedonasthiswillleadtoyoupayingtoomuchtax.

Box 2 Amount of SEISS payments incorrectly claimed

IfyouwerenotentitledtooneormoreSEISSpayments,youmustpaythisbacktoHMRC.Ifyouhavenotpaiditbackorhavenotbeenassessedontheamount,puttheamountyouwerenotentitledtoinbox2.Donotincludeanypaymentsthatyouwereentitledtoorhavealreadyrepaidorbeenassessedonasthiswillleadto you paying too much tax.

Marriage AllowanceIfyourearningsfrom6April2020to 5April2021werelessthan£12,500(plusupto£6,000insavingsinterest),youcouldbenefitasacoupleifyoutransfer£1,250ofyourpersonalallowance.Youmustfillinboxes1to5andputyourdateofbirthinbox1onpageTR1.

Bytransferring£1,250ofyourpersonalallowancetoyourspouseorcivilpartnertoreducetheamountoftaxtheypaybyupto£250,youmayhave to pay some tax yourself. To be able to benefit, all of the following must apply:•youweremarriedto,orinacivilpartnership

with, the same person for all or part of the tax year•youdonotclaimMarriedCouple’sAllowance•yourpartner’sincomewasnottaxedatarateotherthanthebasicrate,thedividendordinaryrate or the starting rate for savings

A Use the Marriage Allowance calculator to see if you can benefit, go to www.gov.uk/marriage-allowance

For more about personal allowances and tax rates, go to www.gov.uk/income-tax-rates

IfyoudonotliveintheUKbutareacitizenofaEuropeanEconomicArea(EEA)country,youcanstillmakeatransferbutyourworldwideincome(inUKpounds)mustbelessthanyourpersonalallowance for you to be eligible.

If you or your partner were born before 6April1935,youmaybenefitmoreasacouplebyclaimingMarriedCouple’sAllowanceinsteadof Marriage Allowance. You cannot have both.

A For more information about Married Couple’s Allowance, go to www.gov.uk/married-couples-allowance

Finishing your tax returnCalculating your taxIfwereceiveyourpapertaxreturnbythedeadline,we’llworkoutifyouhaveanytaxtopayandtellyou before 31January2022.We’llsendyouatax calculation that also tells you if you have to makepaymentsonaccountforthe2021to2022 tax year.

A For more information about payments on account,go to www.gov.uk/understand-self-assessment-bill/payments-on-account

Ifyouwanttoworkouttheamountoftaxthatyouoweormayberepaid,use‘Aroughguide toyourtaxbill’onpageTRG16ofthesenotes.

Theguidedoesnottakeintoaccountanypaymentsonaccountthatyou’vealreadymadetowardsyour2020-21SelfAssessmenttaxbill.

Tax refunded or set off

Box 1Ifyou’vereceivedataxrefund(rebate)becauseyou:•stoppedworkingandmadeanin-yearrepaymentclaimfromtaxpaidonyour –employment –self-employmentintheconstruction industryscheme(CIS)

•claimedthetaxyoupaidontrivial pension income•sentanin-yeartaxreturntoclaimarefund ontaxpaid•receivedarepaymentfromthejobcentreafter 6April

puttheamountrefundedinthebox.

Ifyou’reamendingyourtaxreturn,donotincludeanyrepaymentyoureceivedfromusafteryoufiledyouroriginalreturn.

Page TRG 14

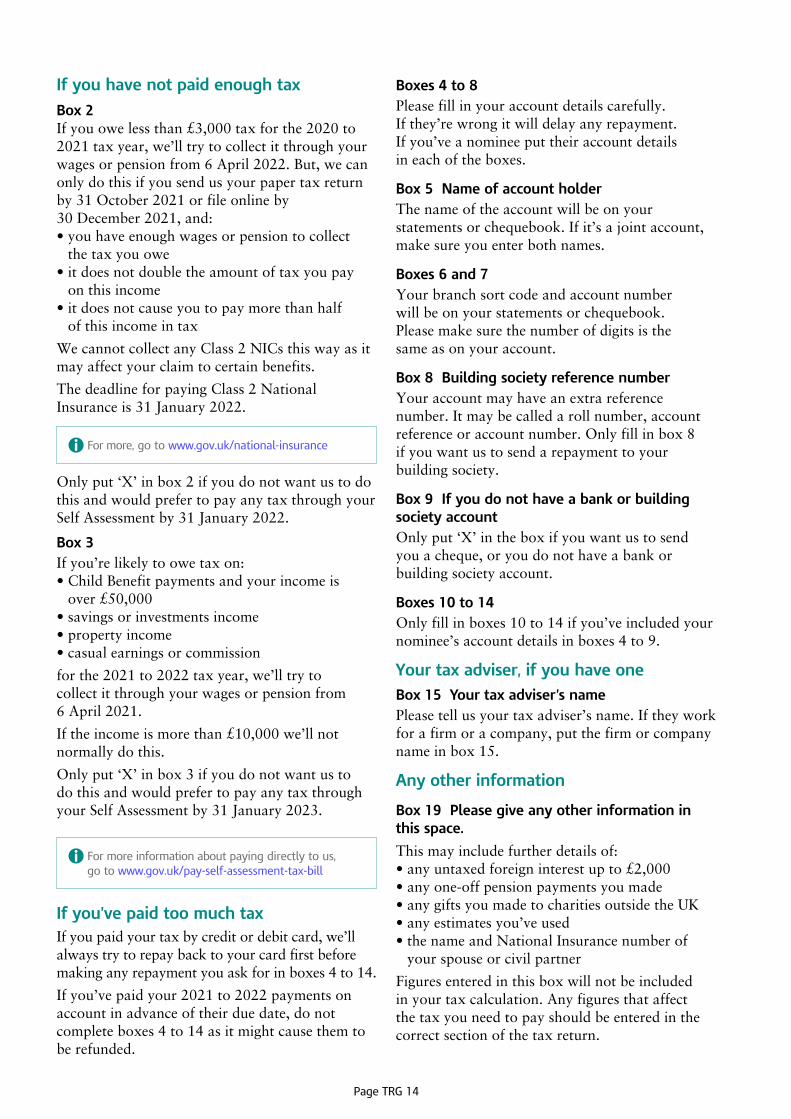

If you have not paid enough tax

Box 2Ifyouowelessthan£3,000taxforthe2020to2021taxyear,we’lltrytocollectitthroughyourwagesorpensionfrom6April2022.But,wecanonlydothisifyousendusyourpapertaxreturnby31October2021orfileonlineby 30December2021,and:•youhaveenoughwagesorpensiontocollect

the tax you owe•itdoesnotdoubletheamountoftaxyoupay

on this income•itdoesnotcauseyoutopaymorethanhalf

of this income in tax

WecannotcollectanyClass2NICsthiswayasitmay affect your claim to certain benefits.

ThedeadlineforpayingClass2NationalInsuranceis31January2022.

A For more, go to www.gov.uk/national-insurance

Onlyput‘X’inbox2ifyoudonotwantustodothisandwouldprefertopayanytaxthroughyourSelfAssessmentby31January2022.

Box 3Ifyou’relikelytoowetaxon:•ChildBenefitpaymentsandyourincomeis over£50,000•savingsorinvestmentsincome•propertyincome•casualearningsorcommission

forthe2021to2022taxyear,we’lltryto collect it through your wages or pension from 6April2021.

Iftheincomeismorethan£10,000we’llnotnormallydothis.

Onlyput‘X’inbox3ifyoudonot want us to dothisandwouldprefertopayanytaxthroughyourSelfAssessmentby31January2023.

A For more information about paying directly to us, go to www.gov.uk/pay-self-assessment-tax-bill

If you’ve paid too much taxIfyoupaidyourtaxbycreditordebitcard,we’llalwaystrytorepaybacktoyourcardfirstbeforemakinganyrepaymentyouaskforinboxes4to14.

Ifyou’vepaidyour2021to2022paymentsonaccountinadvanceoftheirduedate,donotcompleteboxes4to14asitmightcausethemtoberefunded.

Boxes 4 to 8Pleasefillinyouraccountdetailscarefully. Ifthey’rewrongitwilldelayanyrepayment. Ifyou’veanomineeputtheiraccountdetails in each of the boxes.

Box 5 Name of account holderThe name of the account will be on your statementsorchequebook.Ifit’sajointaccount,makesureyouenterbothnames.

Boxes 6 and 7Yourbranchsortcodeandaccountnumber willbeonyourstatementsorchequebook. Pleasemakesurethenumberofdigitsisthe same as on your account.

Box 8 Building society reference numberYour account may have an extra reference number.Itmaybecalledarollnumber,accountreferenceoraccountnumber.Onlyfillinbox8 ifyouwantustosendarepaymenttoyourbuildingsociety.

Box 9 If you do not have a bank or building society accountOnlyput‘X’intheboxifyouwantustosend youacheque,oryoudonothaveabankorbuildingsocietyaccount.

Boxes 10 to 14Onlyfillinboxes10to14ifyou’veincludedyournominee’saccountdetailsinboxes4to9.

Your tax adviser, if you have oneBox 15 Your tax adviser’s namePleasetellusyourtaxadviser’sname.Iftheyworkfor a firm or a company, put the firm or company nameinbox15.

Any other information

Box 19 Please give any other information in this space.

Thismayincludefurtherdetailsof:•anyuntaxedforeigninterestupto£2,000•anyone-offpensionpaymentsyoumade•anygiftsyoumadetocharitiesoutsidetheUK•anyestimatesyou’veused•thenameandNationalInsurancenumberof

your spouse or civil partner

Figuresenteredinthisboxwillnotbeincludedin your tax calculation. Any figures that affect thetaxyouneedtopayshouldbeenteredinthecorrect section of the tax return.

Page TRG 15

These notes are for guidance only and reflect the position at the time of writing. They do not affect the right of appeal.

Signing your form and sending it backPleasemakesureyousignanddatetheformyourself.Ifyouforget,wecannotacceptitandwillhavetosenditbacktoyou.

Box 20 If this tax return contains provisional figures

Onlyput‘X’inthisboxifyouhaveusedprovisionalfiguresandyouintendtosendfinalfigures as soon as you can. You must tell us in ‘Anyotherinformation’onpageTR7whyyouhaveusedprovisionalamountsandwhenyouexpect to give us your final figures.

Donotput‘X’inbox20ifyou’veusedestimatedfigures,buttellusinthe‘Anyotherinformation’box why you have.

Box 20.1 Coronavirus support payments declaration

Ifyourbusinessreceivedandretainedanycoronavirussupportschemepaymentsput‘X’in box 20.1 to confirm that these payments have beenincludedastaxableincomeintherelevantboxes of this tax return for the purposes of calculating your profits.

Readtheguidancefortherelevantsupplementarypagesforyourbusiness(es)forfurtherdetailsonwheretoincludethesepayments.

Youdonotneedtocompletethisboxifyouronlysupportpaymentsreceivedwereasaresultofbeingfurloughedasanemployee.

Boxes 23 to 26 Youonlyneedtofillintheseboxesifyou:•areanexecutordealingwithadeceased’sestatefrom6April2020tothedatethepersondied•areappointedbyaUKcourttocomplete

a tax return on behalf of someone who is not mentallycapableofunderstandingit•haveanenduringorlastingpowerofattorney

to act on behalf of someone who is not physically or mentally capable of filling in a tax return

Ifyouhavenotpreviouslysentevidenceofyourappointment,pleasesendtheoriginaldocument,orcertifiedcopy,withthistaxreturn.

Acertifiedcopyshouldbesignedandcertified asatrueandcompletecopy,oneverypage,byeitherthedonorofthepower,asolicitoror astockbroker.We’llsenditbacktoyouwithin 15workingdays.

More help if you need itTo get copies of any tax return forms or helpsheets go to www.gov.uk/taxreturnforms

You can phone the Self Assessment Helpline on 03002003310forhelpwithyourtaxreturn.

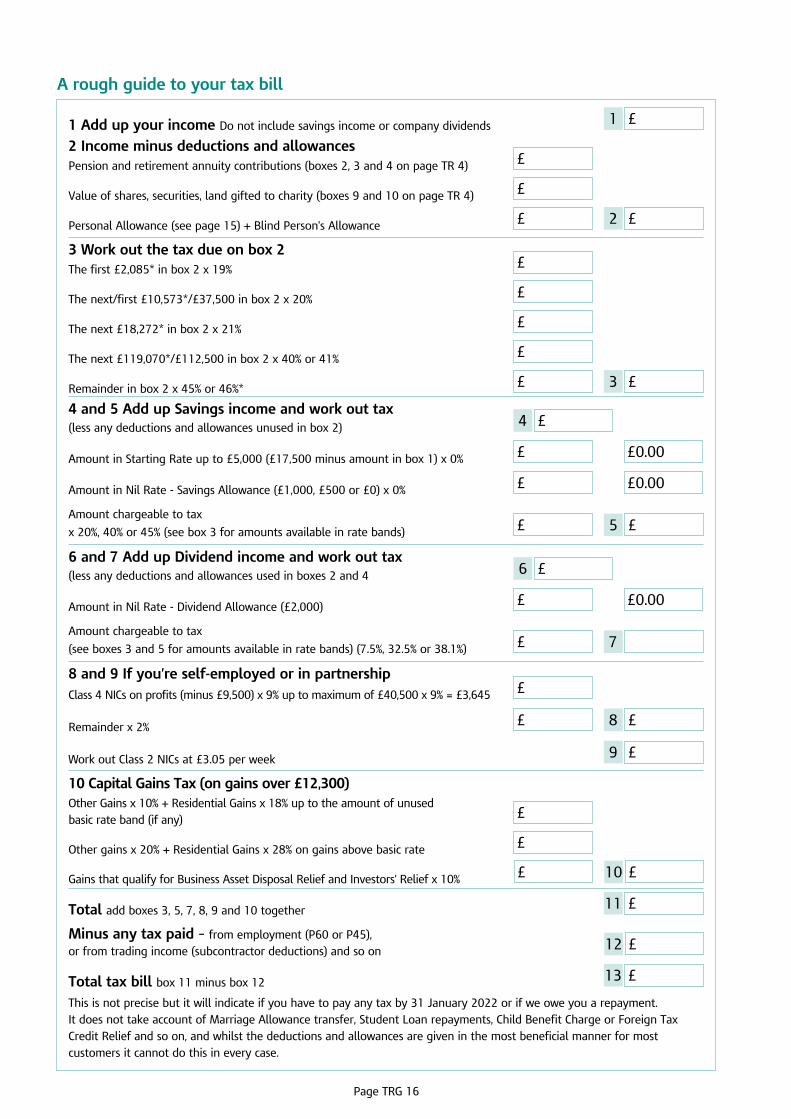

A Personal Allowance£12,500 – if your total income is between £100,000 and £125,000 reduce £12,500 by £1 for every £2 your income exceeds £100,000. If your total income is £125,000 or more Personal Allowance is zero. Blind Person’s Allowance, if claimed, is £2,450.

A Tax rate bands *£10,573 and £37,500 can be increased by any personal pension payments (box 1 on page TR 4) and grossed up Gift Aid (box 5 minus box 7 + box 8 on page TR 4 x 100/80). Income Tax in box 1 uses the £0 to £37,500* and next £112,500* tax bands first, then savings, dividends and Capital Gains.

*If you’re a Scottish taxpayer, the Scottish Income Tax rates and bands may be different from the rest of the UK.

For Scottish taxpayers the tax bands for income in boxes 1 to 3 only are *£2,085, *£10,573, *£18,272 and *£119,070.

A Savings Allowance - you are eligible for £1,000. But if you’re taxable at 40%/41% (box 5) or 32.5% (box 7) it’s £500 or, if taxable at 45%/46%/38.1%, it’s 0.

Page TRG 16

1 Add up your income Do not include savings income or company dividends £1

2 Income minus deductions and allowancesPension and retirement annuity contributions (boxes 2, 3 and 4 on page TR 4) £

Value of shares, securities, land gifted to charity (boxes 9 and 10 on page TR 4) £

Personal Allowance (see page 15) + Blind Person’s Allowance £ £2

3 Work out the tax due on box 2The first £2,085* in box 2 x 19% £

The next/first £10,573*/£37,500 in box 2 x 20% £

The next £18,272* in box 2 x 21% £

The next £119,070*/£112,500 in box 2 x 40% or 41% £

Remainder in box 2 x 45% or 46%* £ £3

4 and 5 Add up Savings income and work out tax (less any deductions and allowances unused in box 2) £4

Amount in Starting Rate up to £5,000 (£17,500 minus amount in box 1) x 0% £ £0.00

Amount in Nil Rate - Savings Allowance (£1,000, £500 or £0) x 0% £ £0.00

Amount chargeable to tax

x 20%, 40% or 45% (see box 3 for amounts available in rate bands) £ £5

6 and 7 Add up Dividend income and work out tax (less any deductions and allowances used in boxes 2 and 4 £6

Amount in Nil Rate - Dividend Allowance (£2,000) £ £0.00

Amount chargeable to tax

(see boxes 3 and 5 for amounts available in rate bands) (7.5%, 32.5% or 38.1%) £ 7

8 and 9 If you’re self-employed or in partnershipClass 4 NICs on profits (minus £9,500) x 9% up to maximum of £40,500 x 9% = £3,645 £

Remainder x 2% £ £8

Work out Class 2 NICs at £3.05 per week £9

10 Capital Gains Tax (on gains over £12,300)Other Gains x 10% + Residential Gains x 18% up to the amount of unused basic rate band (if any) £

Other gains x 20% + Residential Gains x 28% on gains above basic rate £

Gains that qualify for Business Asset Disposal Relief and Investors’ Relief x 10% £ £10

Total add boxes 3, 5, 7, 8, 9 and 10 together £11

Minus any tax paid – from employment (P60 or P45), or from trading income (subcontractor deductions) and so on £12

Total tax bill box 11 minus box 12 £13

This is not precise but it will indicate if you have to pay any tax by 31 January 2022 or if we owe you a repayment.It does not take account of Marriage Allowance transfer, Student Loan repayments, Child Benefit Charge or Foreign Tax Credit Relief and so on, and whilst the deductions and allowances are given in the most beneficial manner for most customers it cannot do this in every case.

A rough guide to your tax bill