how to use social q&a! - vermont captive … 2017/autonomous vehicles and...promote a...

TRANSCRIPT

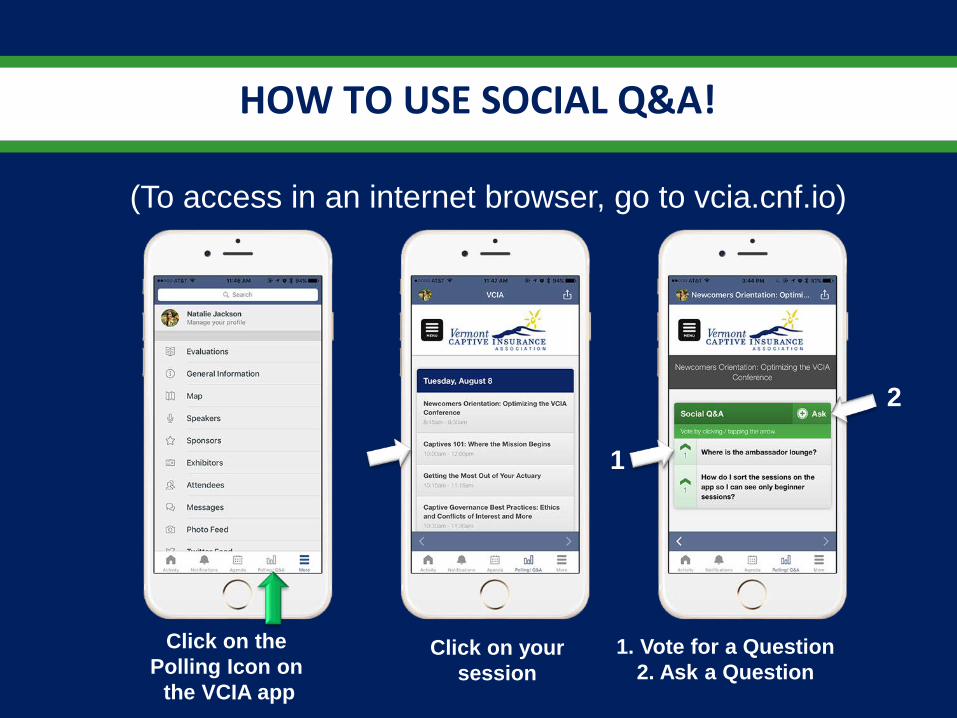

HOW TO USE SOCIAL Q&A!

(To access in an internet browser, go to vcia.cnf.io)

1. Vote for a Question 2. Ask a Question

Click on the Polling Icon on

the VCIA app

Click on your session

1

2

© 2017 VCIA; Speaker materials used by VCIA under license.

Autonomous Vehicles and Their Impact – Ready or Not, Here They Come

Chris Kogut, FCAS, MAAAPrincipal – Milliman, Inc.

August 9, 2017

Christina KindstedtSr. VP – Advantage Insurance

3

Catalyst for Change

Elements for Transformation

Insurance Implications

Recent and Upcoming Developments

Opportunities

Insurance Revisited

Agenda

4

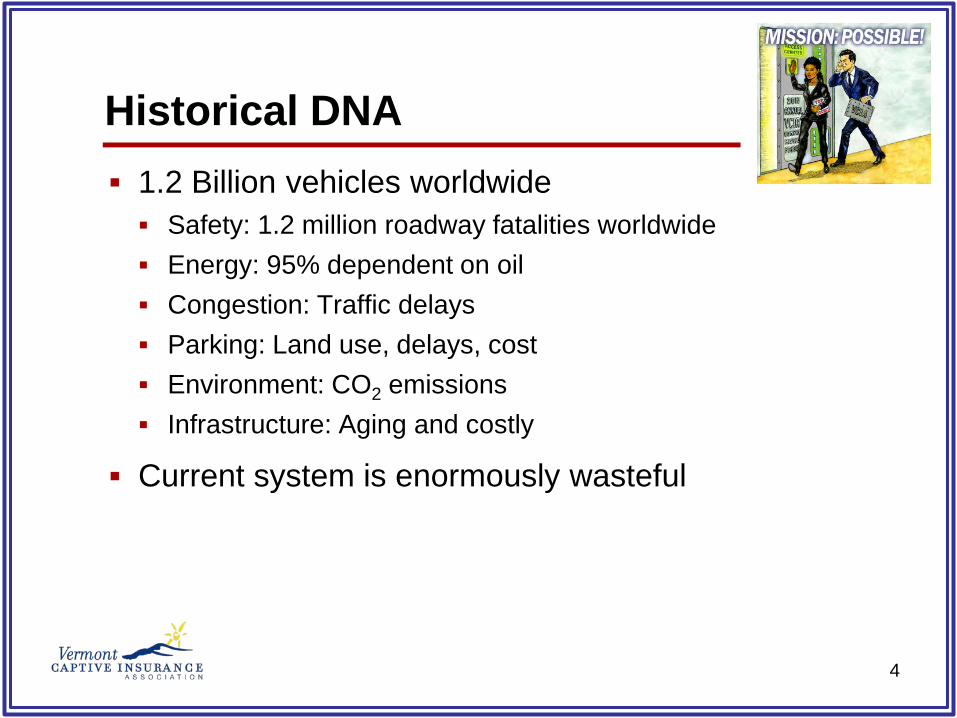

1.2 Billion vehicles worldwide Safety: 1.2 million roadway fatalities worldwide Energy: 95% dependent on oil Congestion: Traffic delays Parking: Land use, delays, cost Environment: CO2 emissions Infrastructure: Aging and costly

Current system is enormously wasteful

Historical DNA

5

Electrical drive Electric motors Diverse energy sources Connected and coordinated Shared Driverless Tailored

Evolution or Transformation

2017 2025

6

Eliminate “negatives” of automobile transportation Enable compelling mobility experiences Reduction in costs Promote a sustainable future

Driverless & ConnectedVehicles

7

Safer More productive More personalized More affordable More convenient

“We are on the cusp of a new era in automotive technology with enormous potential to save lives, reduce greenhouse gas emissions, and transform mobility for the American people.”

Transformation

8

Technology Infrastructure Regulatory Legal Consumer Data

Elements for Transformation

9

The whales (Google, Uber, Ford’s Argo…) have their own captives and can spend up to $1 billion on R&D

Middle market companies have raised $20MM -$100MM each for R&D

The minnows have raised <$20 million each for R&D “We have to carry insurance for R&D but we may not

be around next week after we’ve burned through $20MM. Find me an insurance solution now.”

The Transformers

10

Insured risks: Full blown AVs Kits/modifiers Fleet size

Premiums aren’t commensurate with accident rates in testing

Middle market developers and minnows are paying exorbitant premiums in testing stage

What will their premiums be when they commercialize their AVs or kits?

Risk Profile vs. Premium Rating

11

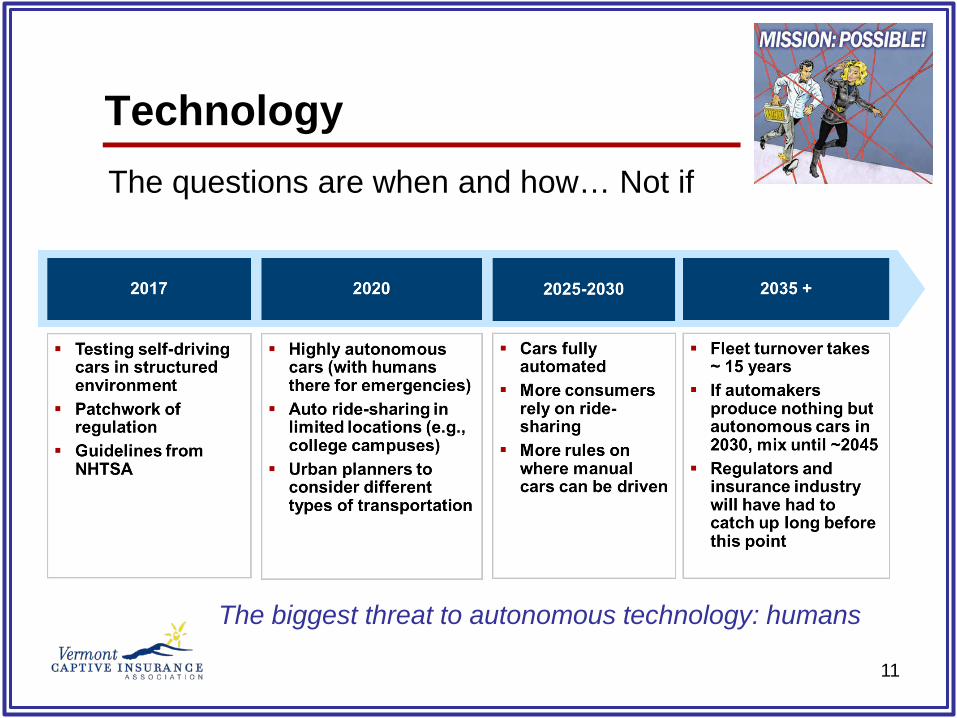

The questions are when and how… Not if

Technology

The biggest threat to autonomous technology: humans

12

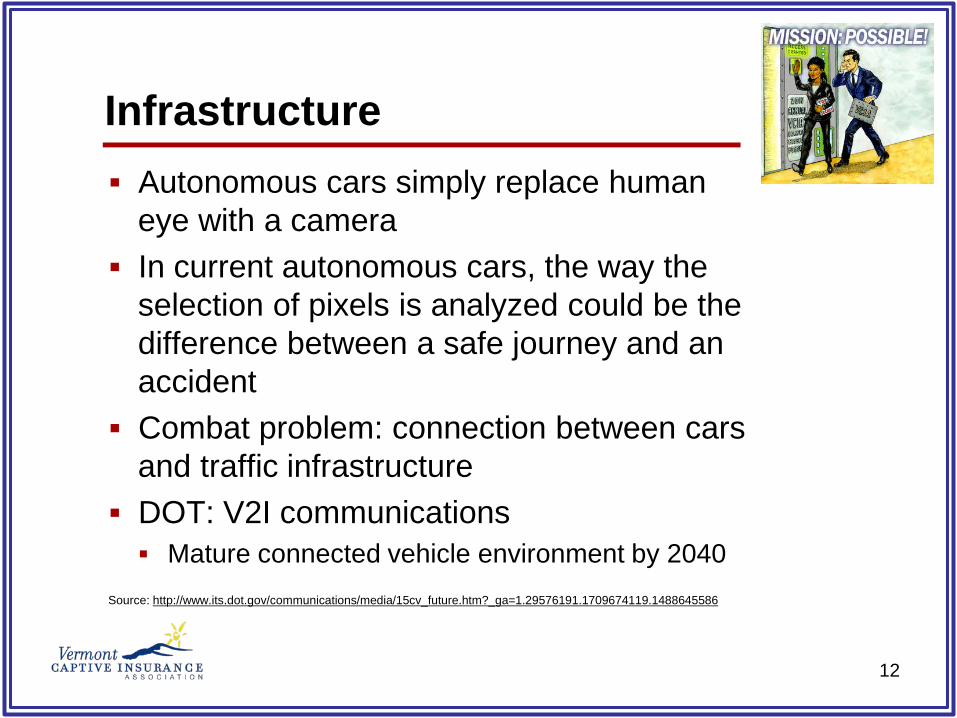

Autonomous cars simply replace human eye with a camera

In current autonomous cars, the way the selection of pixels is analyzed could be the difference between a safe journey and an accident

Combat problem: connection between cars and traffic infrastructure

DOT: V2I communications Mature connected vehicle environment by 2040

Source: http://www.its.dot.gov/communications/media/15cv_future.htm?_ga=1.29576191.1709674119.1488645586

Infrastructure

13

Auto insurance is highly regulated, but which laws apply as AVs change the traditional operator / passenger roles?

Confusion over limits and coverage and policy forms Testing versus commercialization and their impact

on insurance needs Because AVs will be expensive to own initially,

possible new ownership models will complicate the traditional way of assigning financial responsibility

Legal & Regulatory Environment

14

NHTSA – Federal Automated Vehicles Policy, September 2016

Liability and insurance States responsible for determining liability rules for HAVs Rules and laws allocating liability could have significant

effect on both consumer acceptance and rate of deployment

DOT – National Connected Vehicle Field Infrastructure Analysis Press release 12/13/16: DOT advances deployment of

connected vehicle technology

Regulatory

15

DOT – NHTSA – Federal Automated Vehicles Policy

16

State Position

17

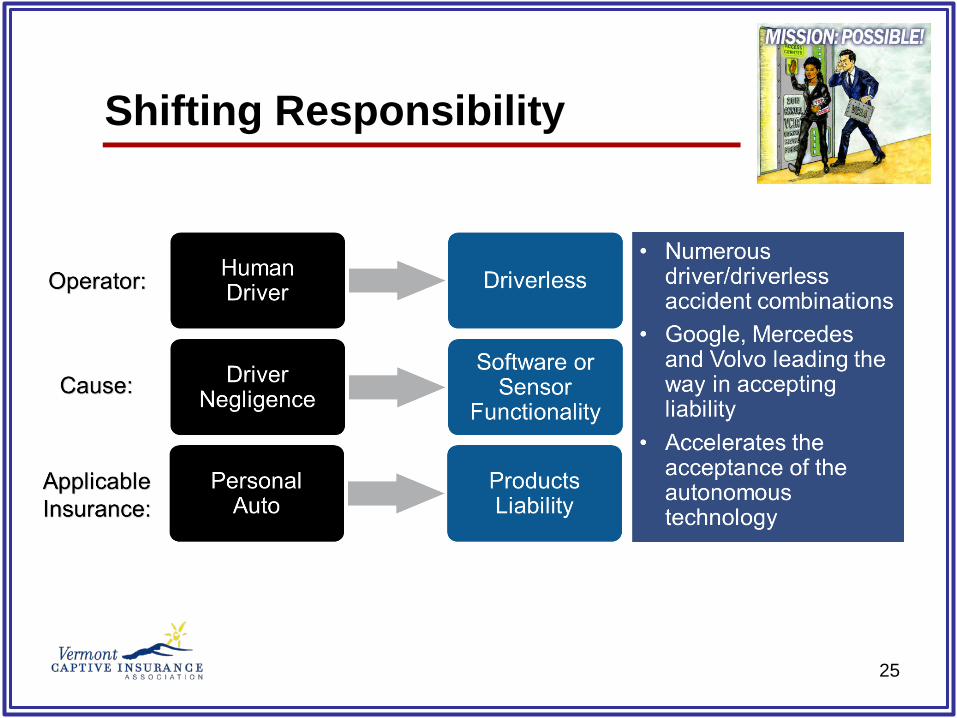

Who will be held responsible in the case of an accident?

Assignment will be determined over time Will start on a case-by-case basis

Could shape opportunities for insurers

Key players are starting to develop legal strategies

Legal

18

Supply side is ready, but what about demand?

Each driver has a unique value proposition

Studies showed mixed interest But there is only a vague understanding of the technology

Suppliers will spend lots of money to make the public more aware of the capabilities

Consumer

19

A “tsunami of data will roll” Between vehicles, infrastructure, and other sources

The dashboard will connect the driver to email, internet, TV, phone

Data management: integrity, ownership, privacy, and analytics

Data

20

Insurance industry Product development Underwriting Ratings Claims

Insurance Implications

21

Autonomous vehicles dramatically affect all aspects of the insurance company’s entire business, from functional operations to market strategy

Yet 32% of insurance executives believe it will have no impact on the industry in the next 10 years

Insurance Market

22

Traditional carriers, given their nature, are slow to respond to AVs’ insurance needs.

Whales have their own captives which are expected to continue AV coverage after commercialization

RRGs can only write third party liability Group captives could provide a one-stop shop for medium and

small AV developers’ insurance needs but they need fronting carriers from limited pool of insurers who currently write AV coverage

None of medium or small developers are interested in a single parent captive as they see insurance as a product they have to buy in the current stage; when they become the next Google, they’ll develop their own single parent captive

Captive Insurance for AVs

23

Motivations for captive In a few cases, the premium is higher than the AV’s

construction cost, and that’s even before commercialization There’s no rationale in the premiums they’re paying to

traditional carriers right now Commercialization will take the premiums to a new high

Obstacles to captive Developers don’t want to share data, not unlike the ship

owners from the early 1700s until the ship owners realized they had to work together to spread their risks

A high ratio of AV developers go out of business very quickly

Reasons for/against Captives

24

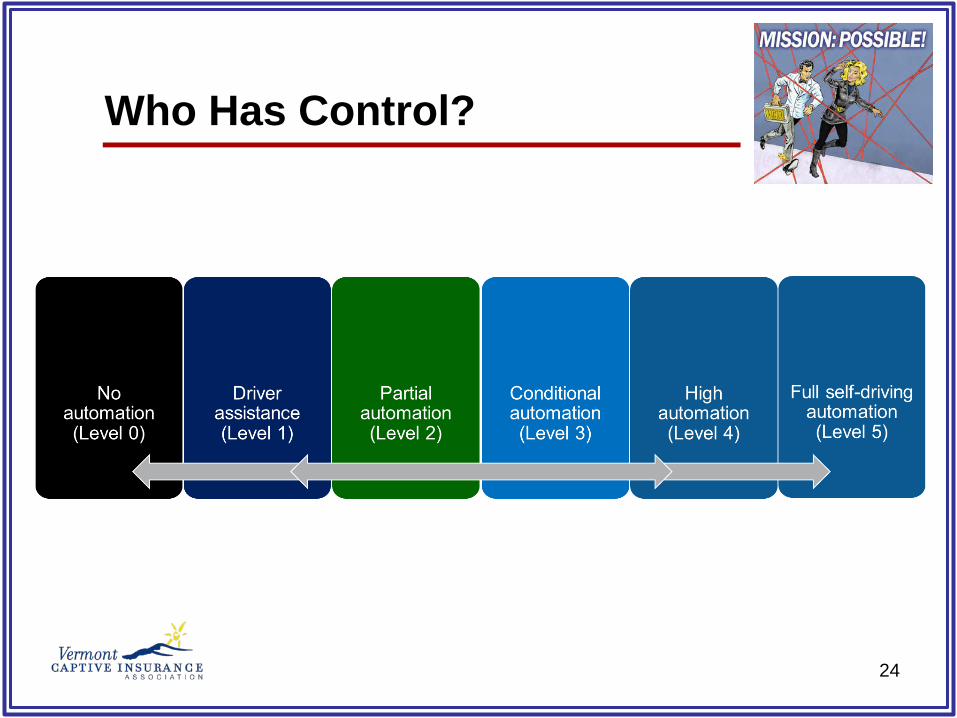

Who Has Control?

25

Shifting Responsibility

26

Product Liability Sub-line of General Liability insurance

Manufacturer responsible for compensating an injured party for injury caused by defective product Product liability insurance provides protection against

financial loss stemming from the legal liability incurred because of injury or damage resulting from the use of covered merchandise

Historical Shift of “buyer beware” to strict liability for manufacturing

defects

27

Risk profile of vehicles on road will substantially decrease, leading to lower total losses for insurers

More than 90% of accidents each year caused by driver error

Potential 80% reduction in accident frequency by 2040 Results in ~2 accidents per 10,000 vehicles

HHS: Automating some parts of driving task is leading to reduction in claim frequency

More expensive components could increase severity Maybe Industry loss costs could drop by 40%

Loss Experience

28

New areas of risk in an autonomous world

Handle products liability

New products and/or risk management services

Product Development

29

Appropriate risk factors

Absorb real time data on vehicle and driver

Manufacturer control of information

Data privacy and security

Underwriting

30

Effects of new capabilities on loss frequency

Effects of next generation products (e.g., V2V communication)

Consumers start to demand discount?

Severity change

A new rate plan?

Rating

31

Expertise in product liability

Changes in coverage

New areas of risk

Systems to collect “accident” data

Expertise to understand data

Can you shape tort law and shape precedence in your state?

Claims

32

First known fatality in Tesla’s autopilot mode

Uber self-driving fleet in Pittsburgh

GM buys Cruise

Mobileye and Delphi team up

Volvo and Uber team up

Uber buys Otto

Fully autonomous hardware on all new Teslas

In the News…

33

Strategy

Change management

Opportunities

34

One size does not fit all Depends on business plan

Know what to look for and be open to new considerations Diversity Innovation Partner

Opportunities

35

What is the right level of investment, now and over time Environment influx

Future IT plans contemplate massive amount of data

Competitive advantage

Right mix of business

Alliances and partnerships to consider

If premium volume falls, how will costs be reduced

Strategic Change

36

Change Management How much does your organization –

executives, board, stakeholders – know (or need to know) about autonomous vehicles?

How will you educate?

Quantify potential effects

Managing/mitigating the risk

37

Autonomous Vehicles:Are We Ready?

38

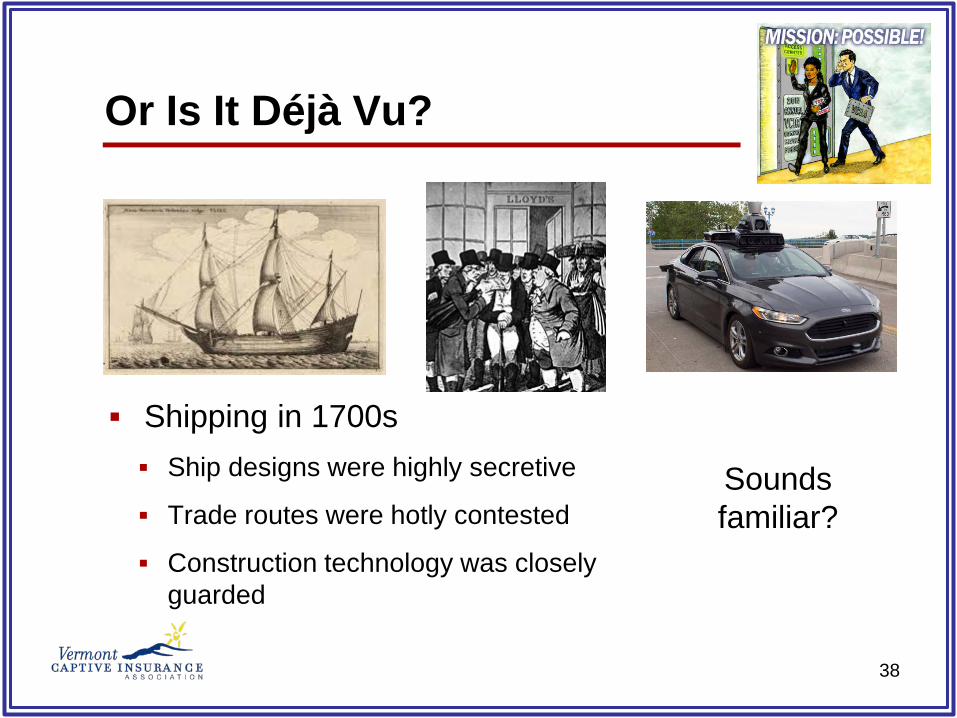

Or Is It Déjà Vu?

Sounds familiar?

Shipping in 1700s Ship designs were highly secretive

Trade routes were hotly contested

Construction technology was closely guarded

39

QUESTIONS

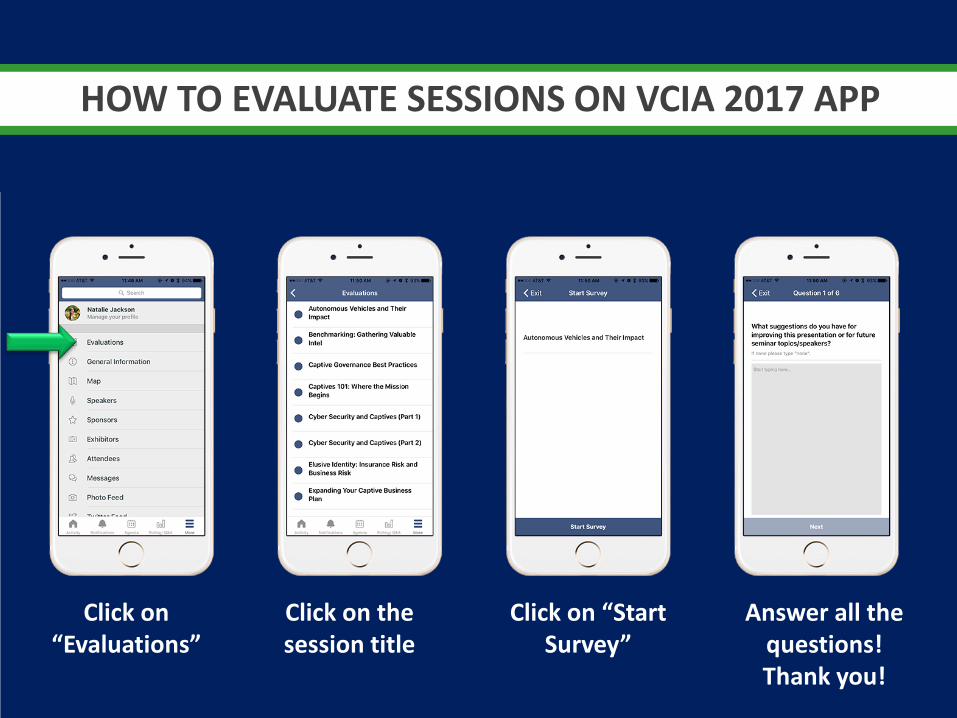

Click on “Evaluations”

Click on the session title

Answer all the questions! Thank you!

HOW TO EVALUATE SESSIONS ON VCIA 2017 APP

Click on “Start Survey”

41

This presentation contains general information only. VCIA and its guest speakers are not, by means of this presentation, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This presentation is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Neither VCIA nor its guest speakers shall be responsible for any loss sustained by any person who relies on this presentation.

Disclaimer