hra self-financing update what it means & what we’ve done housing briefing 19 january 2012

TRANSCRIPT

HRA Self-Financing UpdateWhat it means & what we’ve done

Housing Briefing 19 January 2012

Content• What is HRA Self-Financing?• Benefits of HRA Self-Financing (CLG)• What the council has done about it• Asset Management Planning• HRA Business Planning• Treasury Management• Tenant Engagement• Future governance arrangements• Timetable for transition to Self-Financing• Any questions?

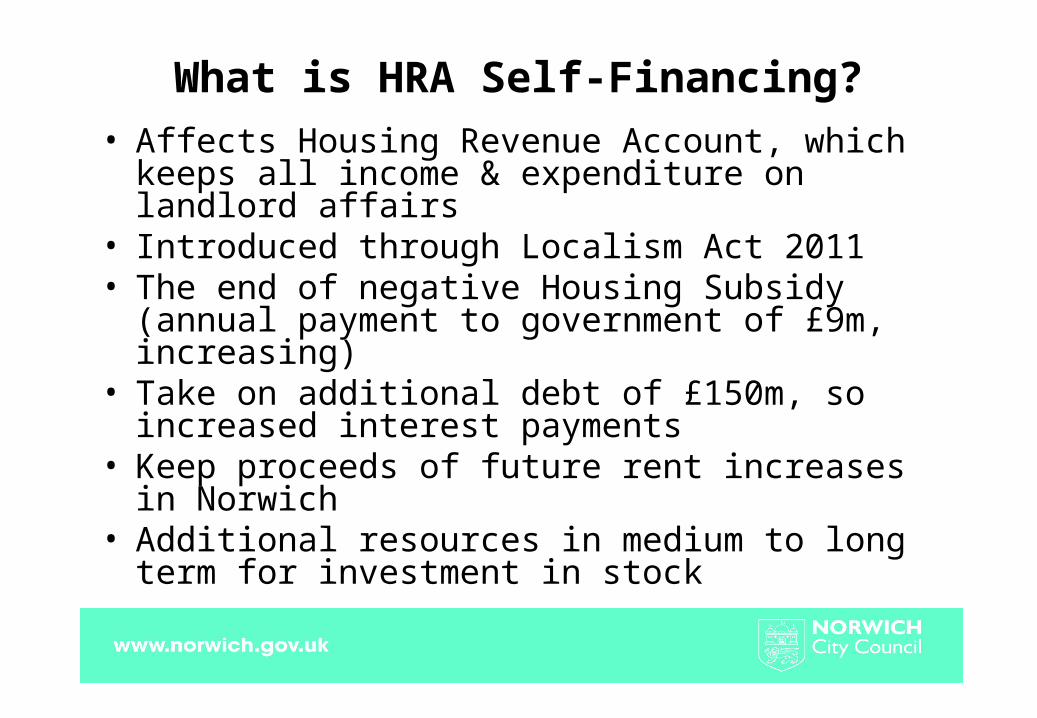

What is HRA Self-Financing?

• Affects Housing Revenue Account, which keeps all income & expenditure on landlord affairs

• Introduced through Localism Act 2011• The end of negative Housing Subsidy (annual

payment to government of £9m, increasing)• Take on additional debt of £150m, so increased

interest payments• Keep proceeds of future rent increases in

Norwich• Additional resources in medium to long term for

investment in stock

Benefits of HRA Self-Financing (CLG)• Tenants will benefit because self-financing provides the opportunity

for business planning to be guided by local priorities, rather than central government rules.

• Tenants will benefit because councils will have more money to spend on council houses.

• Tenants will also be able to trace a clear connection between the rents charged locally and the service provided.

• Councils will publish annual, transparent information on charges and costs.

• Tenants’ rights – such as right to repair, and right to buy - will not change

• Tenants’ landlord will not change – self-financing does not change the council’s position as a housing provider in any way

• Tenants’ rents – the level of rent tenants pay will continue to be a decision for the council, though could be covered by standards set by the regulator as directed by the government

What the council has done• Responded to CLG consultation welcoming the

principle of HRA Self-Financing• Formed a project team to work on planning &

implementation• Coordinated 5 workstreams:

– Asset Management Planning– HRA Business Planning– Treasury Management– Tenant Engagement– Future governance arrangements

• Submitted data to CLG for calculation of new debt

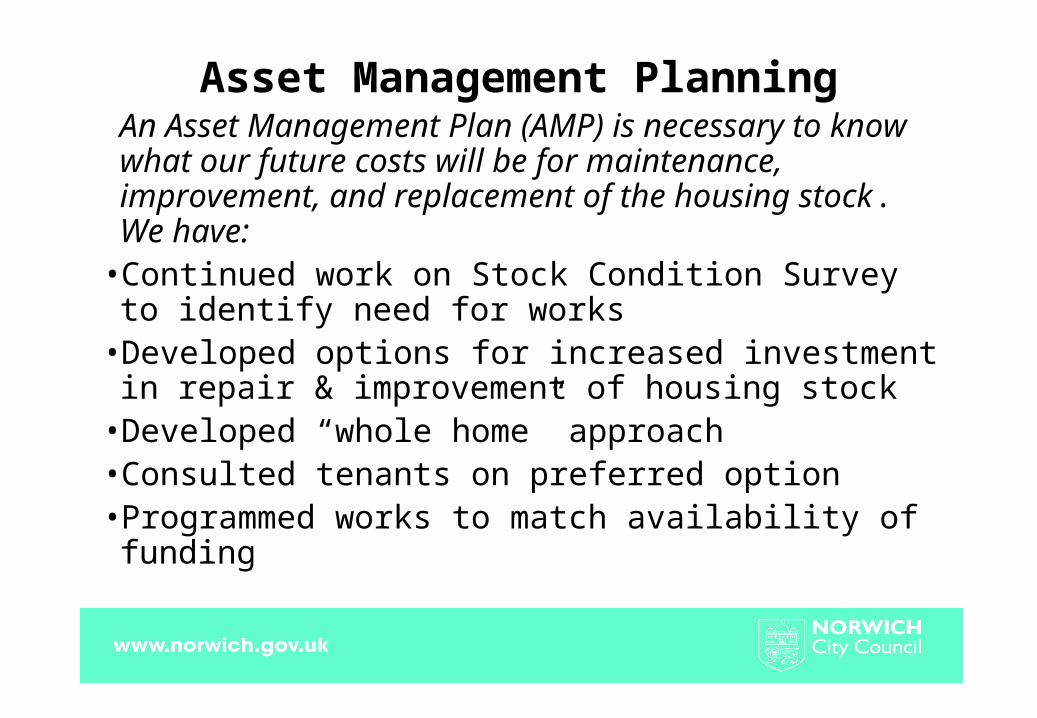

Asset Management Planning An Asset Management Plan (AMP) is necessary to know what our future costs will be for maintenance, improvement, and replacement of the housing stock. We have:

• Continued work on Stock Condition Survey to identify need for works

• Developed options for increased investment in repair & improvement of housing stock

• Developed “whole home” approach• Consulted tenants on preferred option• Programmed works to match availability of funding

HRA Business Planning A Business Plan looks at all costs (including debt

repayment, negative subsidy, investment needs, services and management) and income (rent and service charges) over a 30 year period.

• Identified current & future expenditure and income, and impact of internal & external factors which affect them

• Identified impact of ending Subsidy payments and increased interest payments on new debt

• Calculated affordability of investment and availability of funding

• Identified sensitivities in plan (contract costs, rent income, RTB sales, inflation & interest rates)

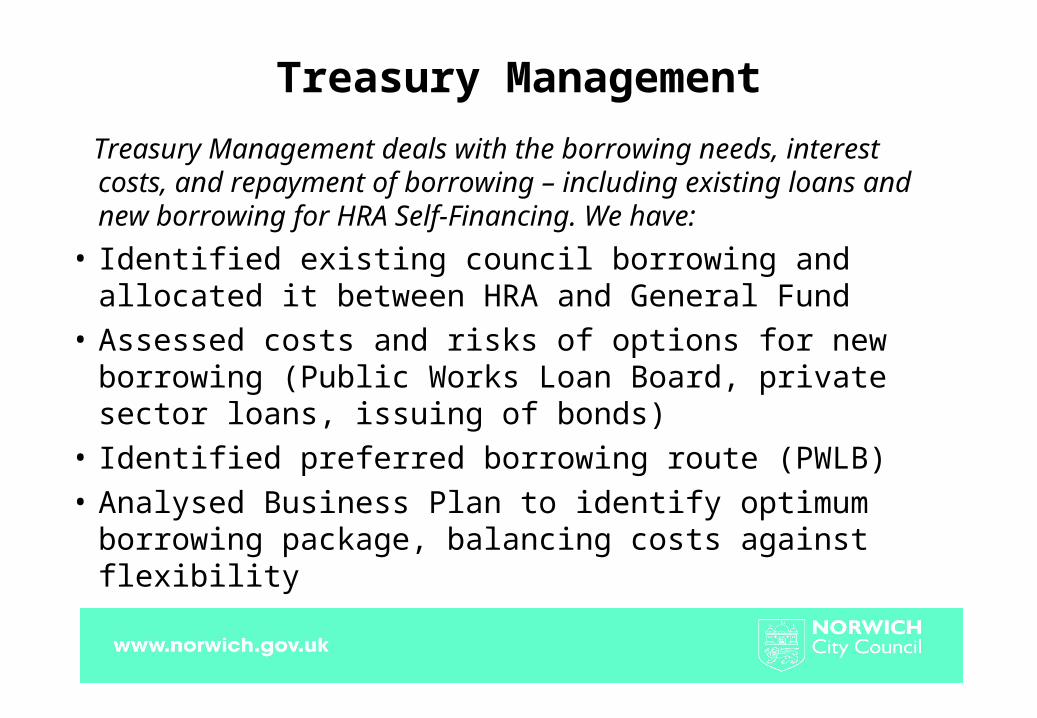

Treasury Management

Treasury Management deals with the borrowing needs, interest costs, and repayment of borrowing – including existing loans and new borrowing for HRA Self-Financing. We have:

• Identified existing council borrowing and allocated it between HRA and General Fund

• Assessed costs and risks of options for new borrowing (Public Works Loan Board, private sector loans, issuing of bonds)

• Identified preferred borrowing route (PWLB)• Analysed Business Plan to identify optimum borrowing

package, balancing costs against flexibility

Tenant Engagement We have consulted tenants (focus group and Finance &

Repairs Sub-Groups of CWB) since the last government’s proposals were “opt in” and required the council’s consent. We have:

• Explained the relationship between rents, subsidy, and investment capacity, and demonstrated the impact of Self-Financing through the Business Plan.

• Consulted tenants on options for investment in housing stock to identify their preferences

• Kept tenants informed on the council’s work on planning and implementing HRA Self-Financing

• Consulted (today) on the key issues – investment in stock & rent increase,

Future governance arrangements The government (through the Tenant Standards

Authority/Homes & Communities Agency) will issue directions requiring increased transparency and tenant involvement in monitoring and making decisions. We have:

• Reviewed our involvement structure to take account of government directions

• Looked to build on existing involvement and increase stakeholder input and scrutiny

• Involved tenants and leaseholders in the review through focus groups and a constitution group

• Developed final proposals to go to cabinet in March 2012

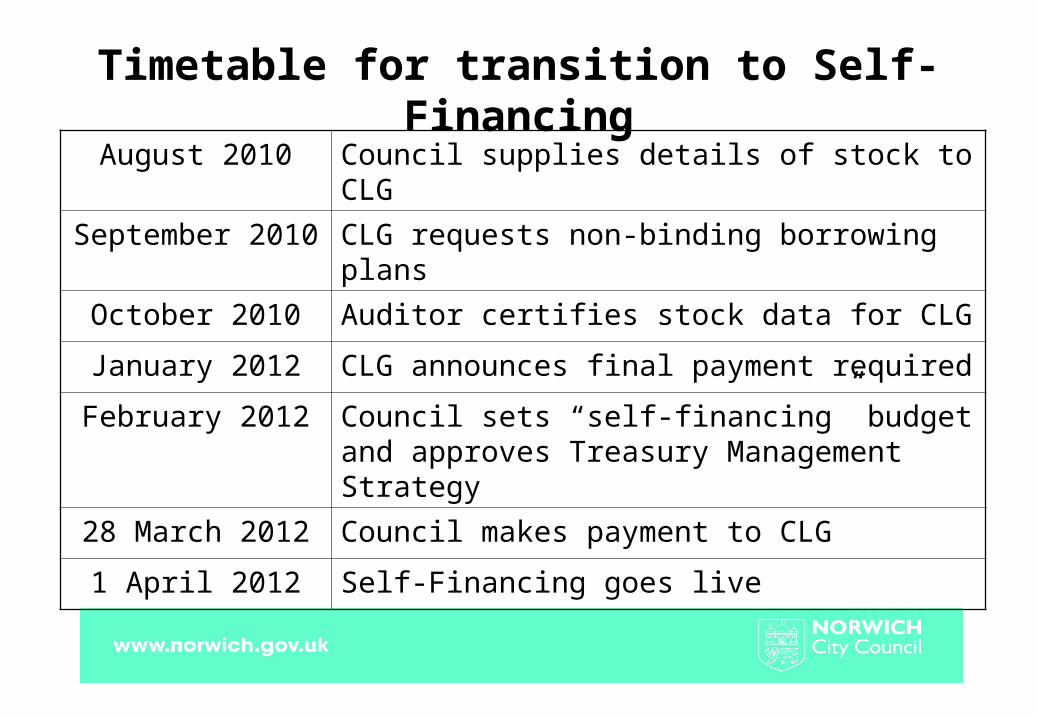

Timetable for transition to Self-Financing

August 2010 Council supplies details of stock to CLG

September 2010 CLG requests non-binding borrowing plans

October 2010 Auditor certifies stock data for CLG

January 2012 CLG announces final payment required

February 2012 Council sets “self-financing” budget and approves Treasury Management Strategy

28 March 2012 Council makes payment to CLG

1 April 2012 Self-Financing goes live

Any Questions?

Responses to any questions regarding HRA

Self-Financing and the process of transition